1 safta india-pakistan-afghanistan trade harsh vivek february 1, 2006 – taj mahal palace and...

TRANSCRIPT

1

SAFTAIndia-Pakistan-Afghanistan

Trade

Harsh Vivek

February 1, 2006 – Taj Mahal Palace and Towers, Mumbai

India Development Foundation

2

The Presentation Agenda

SAFTA

Trade: India-Pak-Afghan

Customs duties

The way forward

3

Why regional trade?

• More integrated markets• Benefits of trade multipliers in the region• Intra-bloc trade – ‘cluster approach to development’

– Exploit trade complementarities of neighbouring countries

• Cooperate to compete (India-China energy example)• Price competitiveness of intra-bloc trade• More benefits (relatively) to small countries in intra-

bloc trade– E.g. Sri Lanka gaining relatively more from India-Sri Lanka

trade

4

SAFTA

• SAFTA Agreement – “Strengthen intra-SAARC economic cooperation to maximize the realization of the region’s potential for trade.”

• Governed by WTO principles– Reciprocity, special and differential treatment– Awareness of the needs of least developed members

(Revenue Compensation Mechanism)

• Focus on elimination of tariff and non-tariff barriers• Two institutions to oversee implementation

– SAFTA Ministerial Council (highest decision-making body)– Committee of Experts (senior economic official from each

member-state)– Role of the SAARC Secretariat (?)

5

Tariffs and Non-tariff barriers

• Tariffs (10 year phase-out of tariffs)– Least developed members reduce tariffs to a maximum of 30

per cent (in first 2 years).

– Tariffs already below 30 per cent will be reduced by 5 per cent annually for least developed members

– Non-least developed members reduce tariffs to a maximum of 20 per cent (first 2 years)

– Tariffs already below 20 per cent will be reduced by 10 per cent annually for non-least developed members

• Non-tariff barriers – QRs eliminated for products not on sensitive-list

6

The Presentation Agenda

SAFTA

Trade: India-Pak-Afghan

Customs duties

The way forward

7

Contribution to SAARC trade (2001)

Export To/From Bangladesh Bhutan India Maldives Nepal Pakistan Sri Lanka

Bangladesh 1.58 23.42 75.00

India 37.53 5.38 1.41 22.75 7.24 25.69

Maldives 1.45 98.55

Nepal 0.56 0.19 99.22 0.03

Pakistan 46.72 21.45 0.43 4.35 27.05

Sri Lanka 32.47 50.90 16.63

8

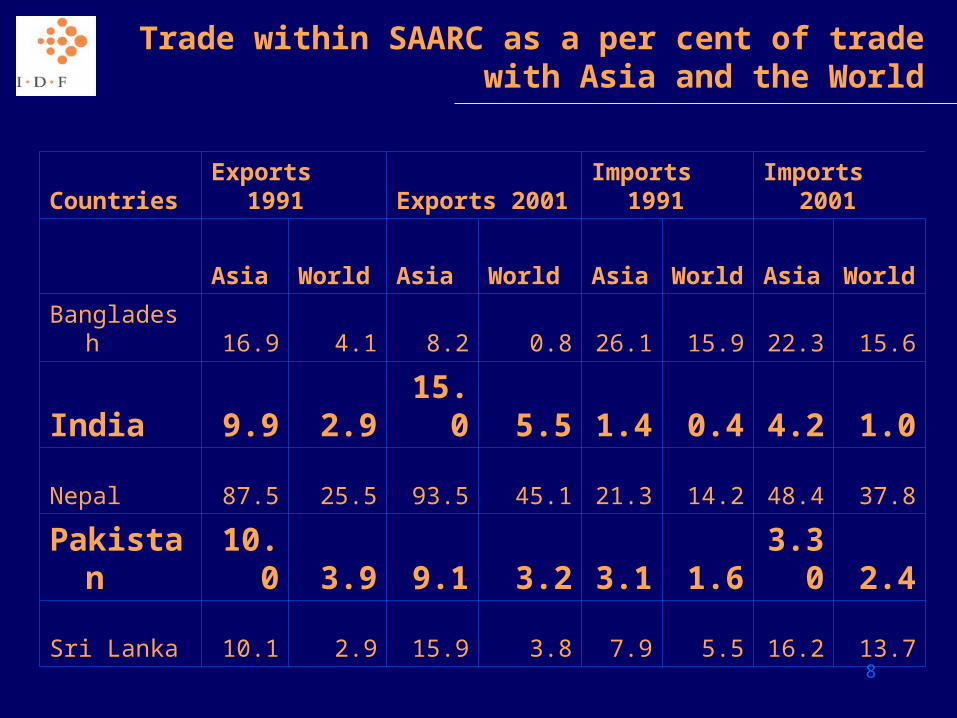

Trade within SAARC as a per cent of trade with Asia and the World

Countries Exports 1991 Exports 2001 Imports 1991 Imports 2001

Asia World Asia World Asia World Asia World

Bangladesh 16.9 4.1 8.2 0.8 26.1 15.9 22.3 15.6

India 9.9 2.9 15.0 5.5 1.4 0.4 4.2 1.0

Nepal 87.5 25.5 93.5 45.1 21.3 14.2 48.4 37.8

Pakistan 10.0 3.9 9.1 3.2 3.1 1.6 3.30 2.4

Sri Lanka 10.1 2.9 15.9 3.8 7.9 5.5 16.2 13.7

9

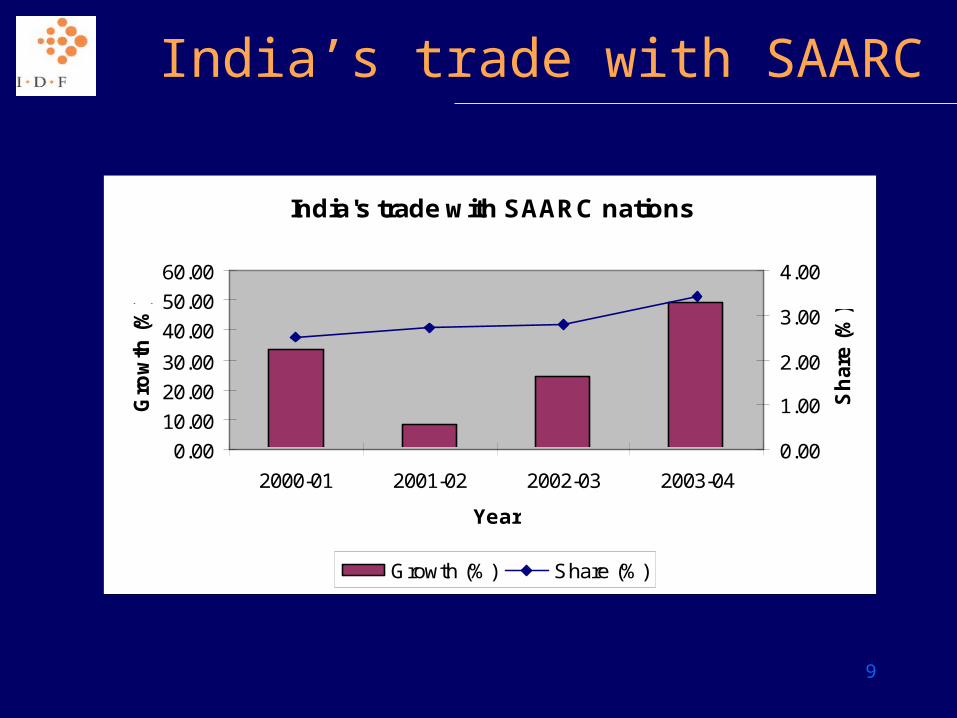

India’s trade with SAARC

India's trade with SAARC nations

0.00

10.00

20.00

30.00

40.00

50.00

60.00

2000-01 2001-02 2002-03 2003-04

Year

Gro

wth

(%

)

0.00

1.00

2.00

3.00

4.00

Sh

are

(%

)

Growth (%) Share (%)

10

Share of developing and Asian countries in India’s trade

Share of developing and Asian countries in India's trade

0.0010.0020.0030.0040.0050.0060.00

2000 2001 2002 2003 2004

Year

Per

cen

tag

e

Developing Countries Asia

11

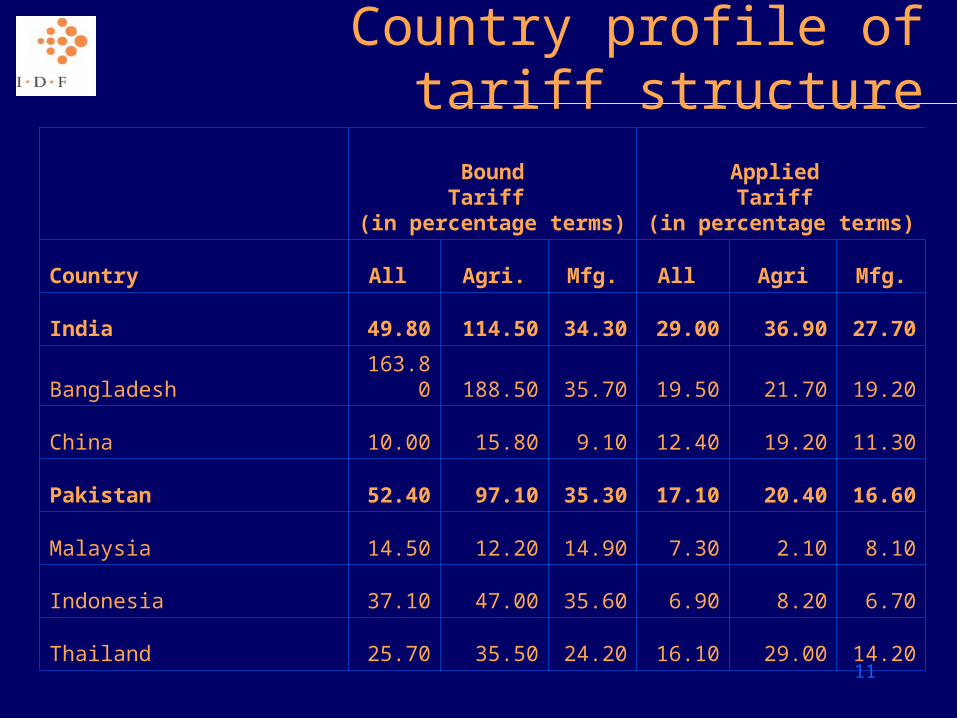

Country profile of tariff structure

BoundTariff

(in percentage terms)

Applied Tariff

(in percentage terms)

Country All Agri. Mfg. All Agri Mfg.

India 49.80 114.50 34.30 29.00 36.90 27.70

Bangladesh 163.80 188.50 35.70 19.50 21.70 19.20

China 10.00 15.80 9.10 12.40 19.20 11.30

Pakistan 52.40 97.10 35.30 17.10 20.40 16.60

Malaysia 14.50 12.20 14.90 7.30 2.10 8.10

Indonesia 37.10 47.00 35.60 6.90 8.20 6.70

Thailand 25.70 35.50 24.20 16.10 29.00 14.20

12

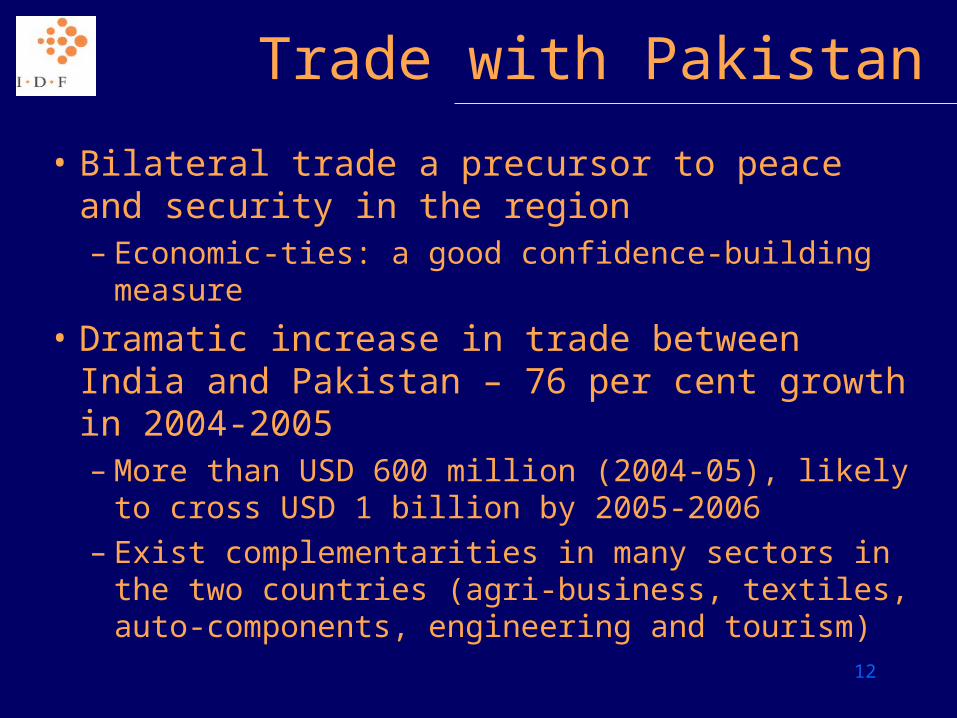

Trade with Pakistan

• Bilateral trade a precursor to peace and security in the region– Economic-ties: a good confidence-building measure

• Dramatic increase in trade between India and Pakistan – 76 per cent growth in 2004-2005– More than USD 600 million (2004-05), likely to

cross USD 1 billion by 2005-2006– Exist complementarities in many sectors in the two

countries (agri-business, textiles, auto-components, engineering and tourism)

13

List of export-import commodities

Pakistan import list / India export list

• Electric and power machinery

• Iron-ore, pig iron

• Medicine and pharma products

• Organic chemicals, pesticides and insecticides

• Rubber tyres

• Pulp and paper

Pakistan export list/ India import list

• Animal hides and skins

• Raw cotton

• Edible nuts

• Metal scrap

• Precious and semi-precious stones

• Jewelry

Source: International Trade Statistics Yearbook (2001), United Nations

14

Composition of India-Pak trade

• Major trade in mfg. goods (60 per cent)

• Bulk trade in agriculture and allied products– Sugar and onions (recent

examples)

• Good potential for increase in trade– Textiles

– Petroleum

Exports from India to Pakistan (2004-05)

20%

4%

60%

6%

1%

2%

7%

Agri. and allied Ores and minerals Mfg goods

Engg goods Machinery Textiles

Petroleum

15

Trade in agriculture commodities

Commodity Name

Pakistan Exports (USD Million)

India Imports (USD Million)

a) Tobacco 1.95 3.63

b) Fish 2.02 5.36

c) Natural honey 2.33 1.18

d) Nuts 12.44 19.04

Commodity Name

India Exports (USD Million)

Pakistan Imports (USD Million)

a) Wheat 1.42 3.92

b) Sunflower oil 1.55 5.79

c) Coconut oil 4.63 1.83

d) Tea 3.18 6.11

e) Pepper 124.47 5.22

f) Processed cereals 1.27 9.39

16

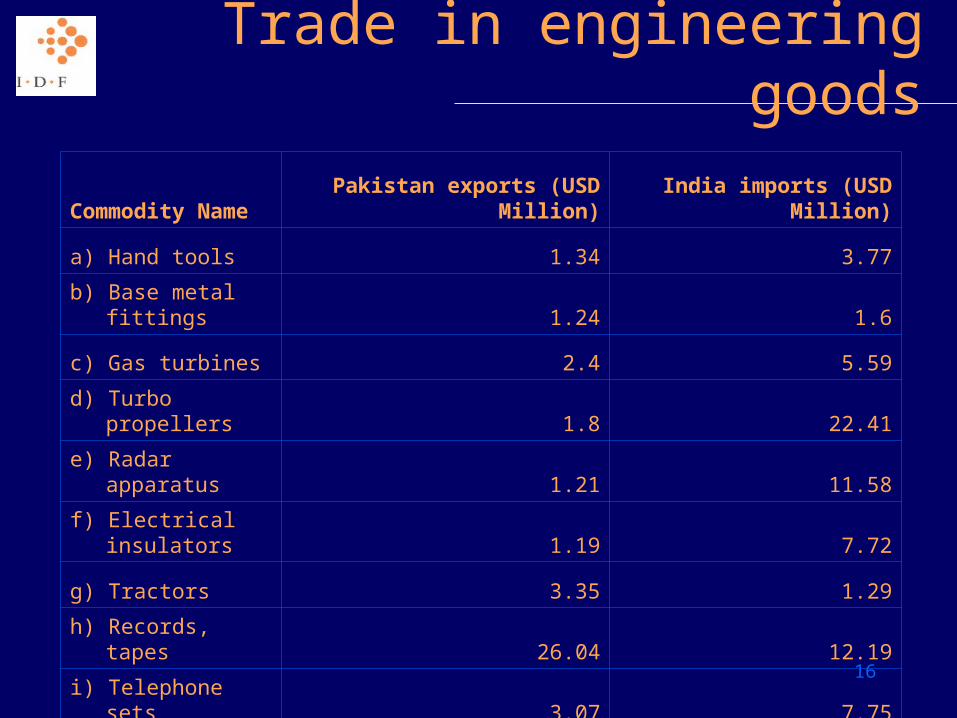

Trade in engineering goods

Commodity Name Pakistan exports (USD Million) India imports (USD Million)

a) Hand tools 1.34 3.77

b) Base metal fittings 1.24 1.6

c) Gas turbines 2.4 5.59

d) Turbo propellers 1.8 22.41

e) Radar apparatus 1.21 11.58

f) Electrical insulators 1.19 7.72

g) Tractors 3.35 1.29

h) Records, tapes 26.04 12.19

i) Telephone sets 3.07 7.75

17

Afghanistan’s trade

• Trade suffered a setback due to prolonged strife, civil wars and political turmoil

• Total exports to India and Pakistan (2004) – USD 150 million (approx)

• Bulk of Afghanistan’s exports go to Pakistan (69 per cent in 2004)

• India (8%) and Russia (6%) other major trading partners

• Imports from a larger number of countries

18

Afghanistan trade destinationsExports by destination (2004)

69%

8%

6%

4%

13%

Pakistan India Russia Europe Others

Imports by destination (2004)

18%

14%

9%

6%

4%

3%

46%

China Japan Pakistan India Germany Kenya Unspecified

19

Composition of Afghan. trade (2004)

Commodity (Exports)

Pakistan (%)

India (%)

Dry fruits 69.40 7.10

Animal skins and fur 89.40 0.00

Carpets 81.80 0.90

Medicinal seeds 33.40 45.20

Fresh fruits 82.70 2.80

Wool 45.30 0.00

Cotton 99.40 0.00

Others 31.10 7.20

Total trade(exports) 69.00 8.00

Commodity (Imports)

Pakistan (%)

India (%)

Fabrics 0.40 3.20

Tyres and tubes 0.00 23.20

Metals 16.60 0.80

Wheat and flour 88.80 0.00

Tea 0.00 3.40

Vegetable oil 22.90 0.00

Cement 10.60 0.00

Medicines 1.70 22.60

Sugar 37.80 14.90

Bicycles 1.60 6.30

Stationery 4.00 8.00

Total trade (imports) 9.00 6.00

20

The Presentation Agenda

SAFTA

Trade: India-Pak-Afghan

Customs duties

The way forward

21

Customs Valuation

• Indian Customs requires extensive documentation.

• Processing delays often due to complex tariff structure and multiple exemptions, which may vary according to product or user.

22

Customs Valuation• On an average, documents required for importing or

exporting one consignment in/out of India includes:

Type of documents 29

No. of copies 118

No. of Signatures 256

Manpower Required 7

Cost of procedures 10 % of consignment value

Source: An UN ESCAP estimate.

23

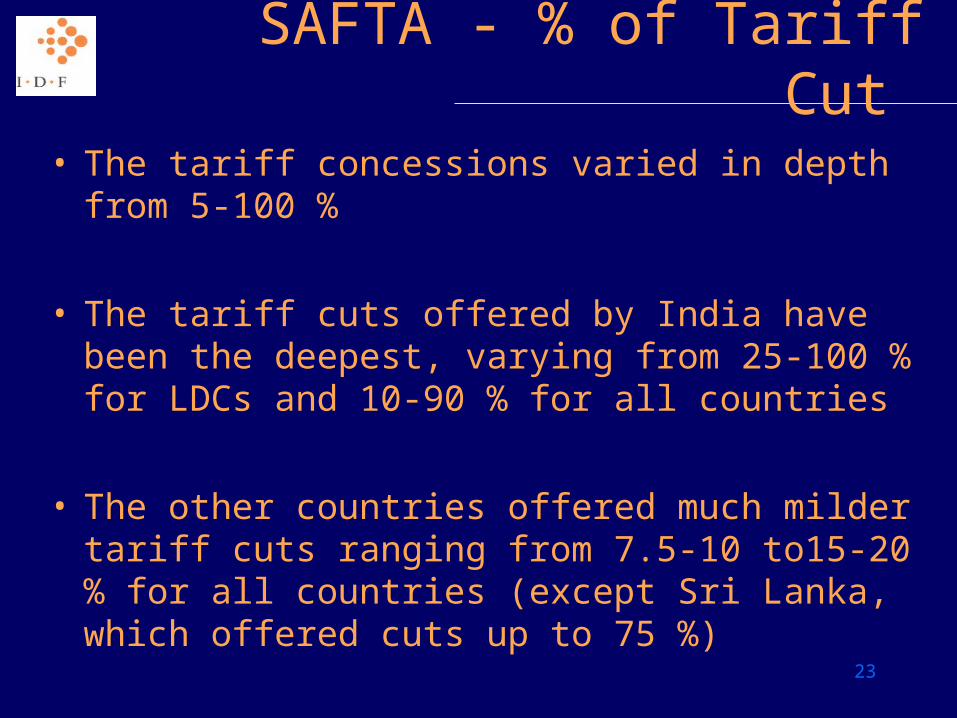

SAFTA - % of Tariff Cut

• The tariff concessions varied in depth from 5-100 %

• The tariff cuts offered by India have been the deepest, varying from 25-100 % for LDCs and 10-90 % for all countries

• The other countries offered much milder tariff cuts ranging from 7.5-10 to15-20 % for all countries (except Sri Lanka, which offered cuts up to 75 %)

24

SAFTA - Tariff Structure

• Provides free trade in goods

– The Agreement does not look at trade in services

– The issue of cross-border investments is also not dealt with strongly in

the Agreement

• Each SAFTA nation will maintain a Sensitive List to protect the

interests of the domestic stakeholders

• The Agreement also provides for an institutional mechanism of

the SAFTA Ministerial Council (SMC)

• Detailed Dispute Settlement Mechanism (on the lines of the

WTO)

– Proper documentation, case based on scientific, verifiable evidences

25

India’s Trade with SAFTA Nations

India's Export to SAARC Nations

INR In billion

SAARC Nations

2002-03

2003-04

2003-04 Apr-Oct

Afghanistan 762.82 936.81 467.55

Bangladesh 56.91 7.99 41.83

Nepal 16.96 30.76 15.77

Pakistan 9.98 13.19 4.03

Sri Lanka 44.57 60.62 32.31

Source: DGCI&S

India's Import from SAARC Nations

INR In billion

SAARC Nations

2002-03

2003-04

2003-04 April-Oct

Afghanistan .89 1.86 .77

Bangladesh 3.00 3.56 2.00

Nepal 13.64 13.14 6.31

Pakistan 2.17 2.64 1.87

Sri Lanka 4.40 8.94 3.51

Source: DGCI&S

26

India's Market among SAFTA Nations

• India’s Market in SAARC for it’s Major Export Commodities

Bangladesh Organic chemical, jewelry, articles of iron & steel, pharmaceutical products, computers

Nepal Medicines and drugs, oil, ores, organic chemical, articles of iron & steel, electrical machinery, processed foods, textiles

Pakistan Ores, slag & ash, chemicals, iron & steel (articles), mfg. products, tea, sugar, processed foods, spices, computers, auto-components (e.g. Tyres)

Sri Lanka Ores, slag & ash, organic chemicals, cotton, iron & steel (articles), electrical machinery, auto-components and parts, pharmaceutical products

27

The Presentation Agenda

SAFTA

Trade: India-Pak-Afghan

Customs and transit rights

The way forward

28

The Way Forward

• Need to strengthen the Agreement– Expanding the scope to include trade in services

• Focus on cross-border investments• Simplification of trade procedures and documentation• Strengthening the implementation of the Agreement –

focus on trade reforms in SAARC• Involvement of international organisations

– Harmonizing tariffs and standards between nations

– Working-out a compensation mechanism for the revenue loss by the least developed countries in the region

29

In conclusion…

“The success of SAFTA greatly depends on the political commitment and harmony among all the signatory members, and on the vigour and vision with which India and Pakistan – the two largest economies in the region – lead meaningful trade reforms.”

30

Thank you.www.idfresearch.org