1 revenue recognition instructor adnan shoaib part ii: corporate accounting concepts and issues...

TRANSCRIPT

1

Revenue Recognition

InstructorInstructorAdnan ShoaibAdnan Shoaib

PART II: Corporate Accounting Concepts and PART II: Corporate Accounting Concepts and IssuesIssues

Lecture 20Lecture 20

2

1. Apply the revenue recognition principle.

2. Describe accounting issues for revenue recognition at point of

sale.

3. Apply the percentage-of-completion method for long-term

contracts.

4. Apply the completed-contract method for long-term contracts.

5. Identify the proper accounting for losses on long-term contracts.

6. Describe the installment-sales method of accounting.

7. Explain the cost-recovery method of accounting.

Learning ObjectivesLearning ObjectivesLearning ObjectivesLearning Objectives

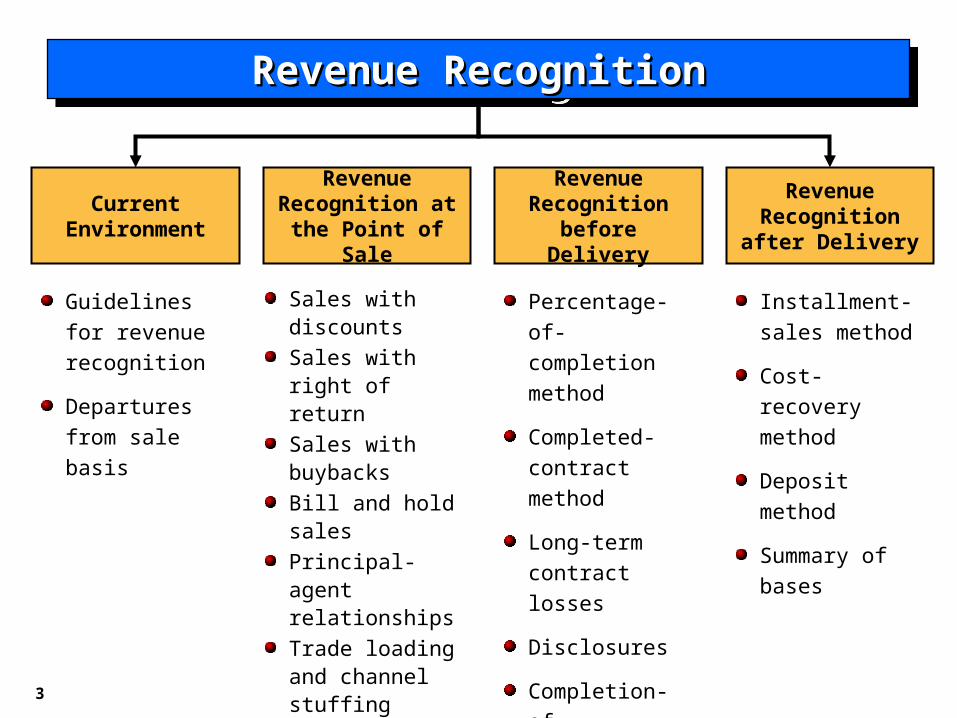

3

Current Environment

Guidelines for

revenue

recognition

Departures from

sale basis

Revenue Recognition at the

Point of Sale

Revenue Recognition

before Delivery

Revenue Recognition after

Delivery

Sales with discounts

Sales with right of return

Sales with buybacks

Bill and hold sales

Principal-agent relationships

Trade loading and channel stuffing

Multiple-deliverable arrangements

Installment-sales

method

Cost-recovery

method

Deposit method

Summary of

bases

Percentage-of-

completion

method

Completed-

contract method

Long-term

contract losses

Disclosures

Completion-of-

production basis

Revenue RecognitionRevenue RecognitionRevenue RecognitionRevenue Recognition

4

Realization PrincipleRealization PrincipleRealization PrincipleRealization Principle

Record revenue when:

Revenues are inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both)

from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central

operations.

5

Realization PrincipleRealization PrincipleRealization PrincipleRealization Principle

Revenue recognition is often tied to delivery of the product from the seller to the buyer.

6

The Current EnvironmentThe Current EnvironmentThe Current EnvironmentThe Current Environment

Restatements for improper revenue recognition are

relatively common and can lead to significant share price

adjustments.

Revenue recognition is a top fraud risk and regardless

of the accounting rules followed (IFRS or U.S. GAAP),

the risk or errors and inaccuracies in revenue reporting is

significant.

7

The revenue recognition principle provides that

companies should recognize revenue

Guidelines for Revenue Recognition

The Current EnvironmentThe Current EnvironmentThe Current EnvironmentThe Current Environment

LO 1 Apply the revenue recognition principle.

(1) when it is realized or realizable and

(2) when it is earned.

8

Sale of product from inventory

Type of Transaction

Rendering a service

Permitting use of an asset

Sale of asset other than inventory

Date of sale (date of delivery)

Services performed and

billable

As time passes or assets are

used

Date of sale or trade-in

Gain or loss on disposition

Revenue from interest, rents, and royalties

Revenue from fees or

services

Revenue from sales

Description of Revenue

Timing of Revenue

Recognition

The Current EnvironmentThe Current EnvironmentThe Current EnvironmentThe Current Environment

LO 1 Apply the revenue recognition principle.

Revenue Recognition Classified by Type of Transaction

9

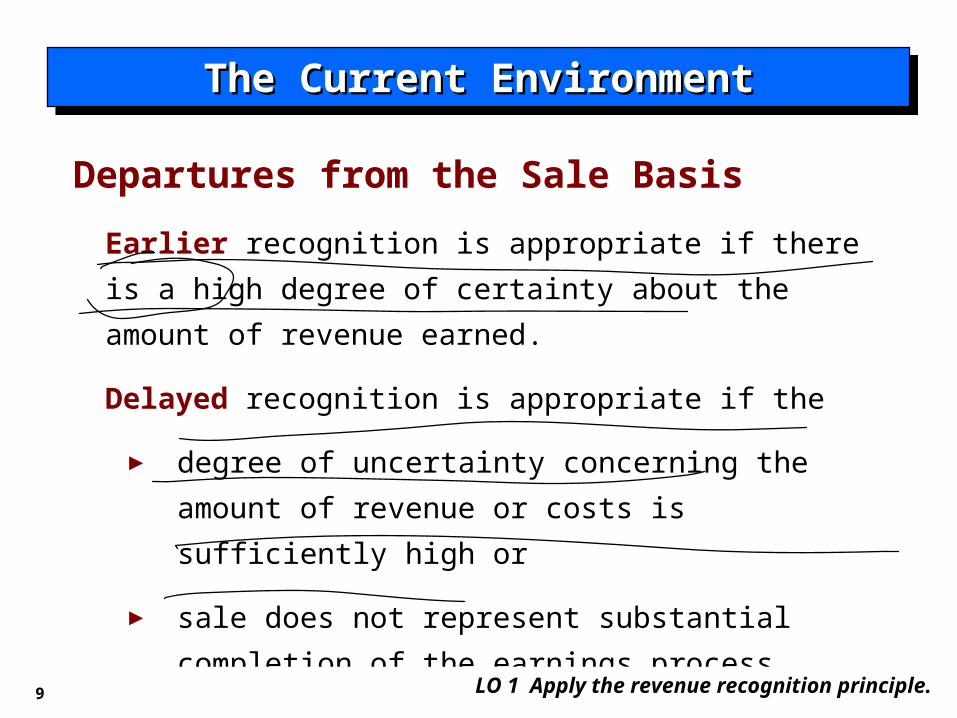

Earlier recognition is appropriate if there is a high degree of

certainty about the amount of revenue earned.

Delayed recognition is appropriate if the

► degree of uncertainty concerning the amount of

revenue or costs is sufficiently high or

► sale does not represent substantial completion of the

earnings process.

Departures from the Sale Basis

The Current EnvironmentThe Current EnvironmentThe Current EnvironmentThe Current Environment

LO 1 Apply the revenue recognition principle.

10

The Current EnvironmentThe Current EnvironmentThe Current EnvironmentThe Current Environment

LO 1 Apply the revenue recognition principle.

Illustration 18-2

Revenue Recognition Alternatives

11

Revenue Recognition at DeliveryRevenue Recognition at DeliveryRevenue Recognition at DeliveryRevenue Recognition at Delivery

When the product or service has been delivered to the

customer and cash has been received or a receivable has

been generated that has reasonable assurance of

collectibility.

When the product or service has been delivered to the

customer and cash has been received or a receivable has

been generated that has reasonable assurance of

collectibility.

Recognize Revenue

12

FASB’s Concepts Statement No. 5, companies usually

meet the two conditions for recognizing revenue by the time

they deliver products or render services to customers.

LO 2 Describe accounting issues for revenue recognition at point of sale.

Implementation problems,

Sales with Discounts

Sales When Right of

Return

Sales with Buybacks

Bill and Hold Sales

Principal-Agent Relationships

Trade Loading and Channel

Stuffing

Multiple-Deliverable

Arrangements

Revenue Recognition at Point of Sale (Delivery)Revenue Recognition at Point of Sale (Delivery)Revenue Recognition at Point of Sale (Delivery)Revenue Recognition at Point of Sale (Delivery)

13 LO 2 Describe accounting issues for revenue recognition at point of sale.

Trade discounts or volume rebates should reduce

consideration received or receivable and the related

revenue.

If payment is delayed, seller should impute an interest

rate for the difference between the cash or cash

equivalent price and the deferred amount.

Sales with Discounts

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

14

Facts: Sansung Company has an arrangement with its customers that

it will provide a 3% volume discount to its customers if they purchase

at least $2 million of its product during the calendar year. On March

31, 2012, Sansung has made sales of $700,000 to Artic Co. In the

previous two years, Sansung sold over $3,000,000 to Artic in the

period April 1 to December 31. Sansung makes the following entry on

March 31, 2012.

LO 2 Describe accounting issues for revenue recognition at point of sale.

Accounts receivable 679,000

Sales revenue 679,000

Illustration 18-3

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

VOLUME DISCOUNTVOLUME DISCOUNT Illustration 18-3

15 LO 2 Describe accounting issues for revenue recognition at point of sale.

Cash 679,000

Accounts receivable 679,000

Illustration 18-3

Facts: Sansung Company has an arrangement with its customers that

it will provide a 3% volume discount to its customers if they purchase

at least $2 million of its product during the calendar year. On March

31, 2012, Sansung has made sales of $700,000 to Artic Co. In the

previous two years, Sansung sold over $3,000,000 to Artic in the

period April 1 to December 31. Assuming Sansung’s customers meet

the discount threshold, Sansung makes the following entry.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

VOLUME DISCOUNTVOLUME DISCOUNT Illustration 18-3

16

VOLUME DISCOUNTVOLUME DISCOUNT

LO 2

Cash 700,000

Accounts receivable 679,000

Sales discounts forfeited 21,000

Illustration 18-3

Facts: Sansung Company has an arrangement with its customers that

it will provide a 3% volume discount to its customers if they purchase

at least $2 million of its product during the calendar year. On March

31, 2012, Sansung has made sales of $700,000 to Artic Co. In the

previous two years, Sansung sold over $3,000,000 to Artic in the

period April 1 to December 31. Sansung makes the following entry on

March 31, 2012. If Sansung’s customers fail to meet the discount

threshold, Sansung makes the following entry upon payment.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

17

Sales with Right of Return

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

LO 2 Describe accounting issues for revenue recognition at point of sale.

Three possible revenue recognition methods are available when

the right of return exposes the seller to continued risks of

ownership:

1. not recording a sale until all return privileges have expired

or

2. recording the sale, but reducing sales by an estimate of

future returns.

3. Recording the sale and accounting for the returns as they

occur.

18

Recognize revenue only if six conditions have been met.

LO 2 Describe accounting issues for revenue recognition at point of sale.

1. The seller’s price to the buyer is substantially fixed or

determinable at the date of sale.

2. The buyer has paid the seller, or the buyer is obligated to pay

the seller, and the obligation is not contingent on resale of the

product.

3. The buyer’s obligation to the seller would not be changed in the

event of theft or physical destruction or damage of the product.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

Sales with Right of Return

19 LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

Sales with Right of Return

Recognize revenue only if six conditions have been met.

4. The buyer acquiring the product for resale has economic

substance apart from that provided by the seller.

5. The seller does not have significant obligations for future

performance to directly bring about resale of the product by the

buyer.

6. The seller can reasonably estimate the amount of future

returns.

20

Question: When should Pesido recognize the revenue for the sale of the Question: When should Pesido recognize the revenue for the sale of the new laser equipment?new laser equipment?

Facts: Pesido Company is in the beta-testing stage for new laser

equipment that will help patients who have acid reflux problems. The

product that Pesido is selling has been very successful in trials to date. As

a result, Pesido has received regulatory authority to sell this equipment to

various hospitals. Because of the uncertainty surrounding this product,

Pesido has granted to the participating hospitals the right to return the

device and receive full reimbursement for a period of 9 months.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

LO 2

Illustration 18-5SALES WITH RETURNSSALES WITH RETURNS Illustration 18-5

Solution: Given that the hospital has the right to rescind the purchase for

a reason specified in the sales contract and Pesido is uncertain about the

probability of return, Pesido should not record revenue at time of delivery.

21

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

LO 2

Pesido sold $300,000 of laser equipment on August 1, 2012, and

retains only an insignificant risk of ownership. On October 15,

2012, $10,000 in equipment was returned.

August 1, 2012

Accounts receivable 300,000

Sales 300,000

October 15, 20121

Sales returns and allowances 10,000

Accounts receivable

10,000

SALES WITH RETURNSSALES WITH RETURNS

22

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

At December 31, 2012, based on prior experience, Pesido

estimates that returns on the remaining balance will be 4 percent.

Pesido makes the following entry to record the expected returns.

December 31, 2012

Sales returns and allowances 11,600

Allowance for sales returns and allowances

11,600

[($300,000 - $10,000) x 4% = 11,600]

LO 2 Describe accounting issues for revenue recognition at point of sale.

SALES WITH RETURNSSALES WITH RETURNS

23

If a company sells a product in one period and agrees to

buy it back in the next period, has the company sold the

product?

The economic substance of this transaction is that the

seller retains the risks of ownership.

Sales with Buybacks

LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

24

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

Facts: Morgan Inc., an equipment dealer, sells equipment to Lane

Company for $135,000. The equipment has a cost of $115,000.

Morgan agrees to repurchase the equipment at the end of 2 years

at its fair value. Lane Company pays full price at the sales date,

and there are no restrictions on the use of the equipment over the

2 years. Morgan records the sale as follows:

Cash 135,000

Sales Revenue

135,000

Cost of Goods Sold 115,000

Inventory

115,000LO 2

SALES WITH BUYBACKSALES WITH BUYBACK

25

Bill and Hold Sales

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

Buyer is not yet ready to take delivery but does take title.

Illustration 18-4

BILL AND HOLDBILL AND HOLD Illustration 18-7

Facts: Butler Company sells $450,000 of fireplaces to a local coffee

shop, Baristo, which is planning to expand its locations around the

city. Under the agreement, Baristo asks Butler to retain these

fireplaces in its warehouses until the new coffee shops that will

house the fireplaces are ready. Title passes to Baristo at the time the

agreement is signed.

Question: Should Butler report the revenue from this bill and hold Question: Should Butler report the revenue from this bill and hold arrangement when the agreement is signed, or should revenue be arrangement when the agreement is signed, or should revenue be deferred and reported when the fireplaces are delivered?deferred and reported when the fireplaces are delivered?

LO 2

26

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

Solution: Butler should record the revenue at the time title

passes, provided

1. the risks of ownership have passed to Baristo, that is,

Butler does not have specific performance obligations

other than storage;

2. Baristo makes a fixed commitment to purchase the goods,

requests that the transaction be on a bill and hold basis,

and sets a fixed delivery date; and

3. goods must be segregated, complete, and ready for

shipment.

LO 2 Describe accounting issues for revenue recognition at point of sale.

27

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

LO 2 Describe accounting issues for revenue recognition at point of sale.

Accounts receivable 450,000

Sales 450,000

Illustration 18-4BILL AND HOLDBILL AND HOLD Illustration 18-7

Facts: Butler Company sells $450,000 of fireplaces to a local coffee

shop, Baristo, which is planning to expand its locations around the

city. Under the agreement, Baristo asks Butler to retain these

fireplaces in its warehouses until the new coffee shops that will

house the fireplaces are ready. Title passes to Baristo at the time the

agreement is signed. Butler makes the following entry.

28

Principal-Agent Relationships

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

LO 2 Describe accounting issues for revenue recognition at point of sale.

Amounts collected on behalf of the principal are not

revenue of the agent.

Revenue for the agent is the amount of the commission

it receives.

29

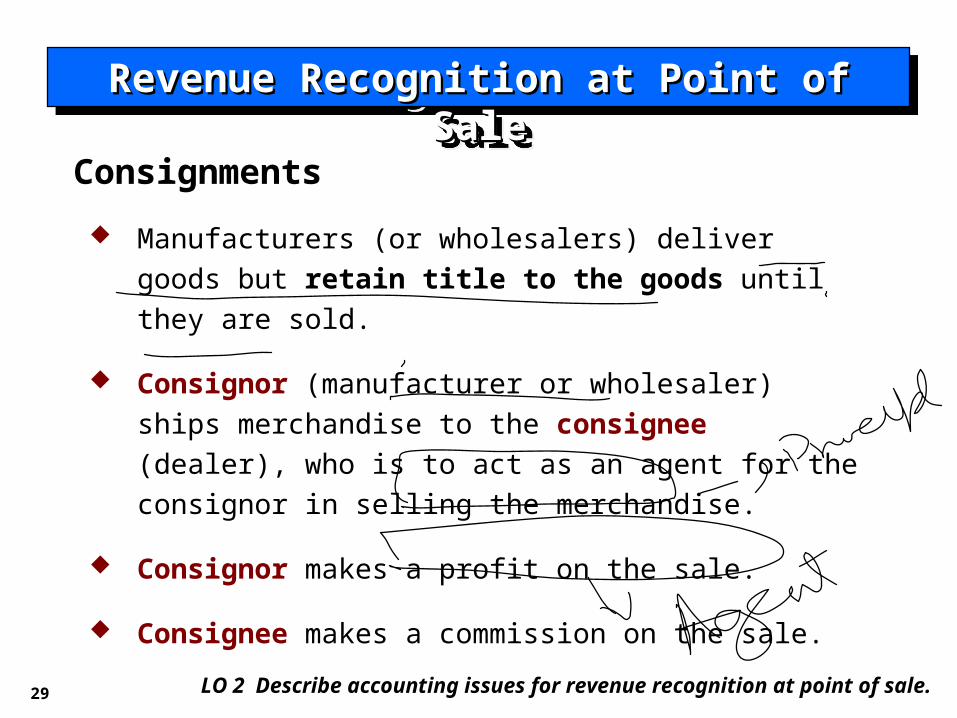

Consignments

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

LO 2 Describe accounting issues for revenue recognition at point of sale.

Manufacturers (or wholesalers) deliver goods but retain

title to the goods until they are sold.

Consignor (manufacturer or wholesaler) ships

merchandise to the consignee (dealer), who is to act as

an agent for the consignor in selling the merchandise.

Consignor makes a profit on the sale.

Consignee makes a commission on the sale.

30

“Trade loading is a crazy, uneconomic, insidious practice

through which manufacturers—trying to show sales, profits,

and market share they don’t actually have—induce their

wholesale customers, known as the trade, to buy more

product than they can promptly resell.”

Trade Loading and Channel Stuffing

LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

31

A similar practice is referred to as channel stuffing. When

a software maker needed to make its financial results look

good, it offered deep discounts to its distributors to overbuy,

and then recorded revenue when the software left the

loading.

Trade Loading and Channel Stuffing

LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

32

MDAs provide multiple products or services to customers as

part of a single arrangement.

The major accounting issues related to this type of

arrangement are how to allocate the revenue to the various

products and services and how to allocate the revenue to

the proper period.

Multiple-Deliverable Arrangements

LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

33

All units in a multiple-deliverable arrangement are

considered separate units of accounting, provided that:

1. A delivered item has value to the customer on a

standalone basis; and

2. The arrangement includes a general right of return

relative to the delivered item; and

3. Delivery or performance of the undelivered item is

considered probable and substantially in the control of the

seller.

Multiple-Deliverable Arrangements

LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

34

Multiple-Deliverable Evaluation Process

Multiple-Deliverable Arrangements

LO 2 Describe accounting issues for revenue recognition at point of sale.

Revenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of SaleRevenue Recognition at Point of Sale

Illustration 18-9

35

Two Methods:

Percentage-of-Completion Method.

► Rationale is that the buyer and seller have

enforceable rights.

Completed-Contract Method.

Most notable example is long-term construction contract

accounting.

Revenue Recognition Before DeliveryRevenue Recognition Before DeliveryRevenue Recognition Before DeliveryRevenue Recognition Before Delivery

LO 2 Describe accounting issues for revenue recognition at point of sale.

36

Must use Percentage-of-Completion method when estimates

of progress toward completion, revenues, and costs are

reasonably dependable and all of the following conditions

exist:

Revenue Recognition Before DeliveryRevenue Recognition Before DeliveryRevenue Recognition Before DeliveryRevenue Recognition Before Delivery

1. Contract clearly specifies the enforceable rights regarding

goods or services by the parties, the consideration to be

exchanged, and the manner and terms of settlement.

2. Buyer can be expected to satisfy all obligations.

3. Contractor can be expected to perform under the contract.

LO 2 Describe accounting issues for revenue recognition at point of sale.

37

Companies should use the Completed-Contract method when

one of the following conditions applies when:

Revenue Recognition Before DeliveryRevenue Recognition Before DeliveryRevenue Recognition Before DeliveryRevenue Recognition Before Delivery

1. Company has primarily short-term contracts, or

2. Company cannot meet the conditions for using the percentage-of-completion method, or

3. There are inherent hazards in the contract beyond the normal, recurring business risks.

LO 2 Describe accounting issues for revenue recognition at point of sale.

38

Formula for Total Revenue to Be Recognized to Date

LO 3 Apply the percentage-of-completion method for long-term contracts.

Illustration 18-13

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration 18-14

Illustration 18-15

Percentage-of-Completion Method

39 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration: Blue Diamond Construction Company has a

contract to construct a $4,500,000 bridge at an estimated cost

of $4,000,000. The contract is to start in July 2012, and the

bridge is to be completed in October 2014. The following data

pertain to the construction period.

40 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration: Compute percentage complete.Illustration 18-16

41 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration: Blue Diamond would make the following entries

to record (1) the costs of construction, (2) progress billings,

and (3) collections.Illustration 18-17

42

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration: Percentage-of-Completion Revenue, Costs, and

Gross Profit by YearIllustration 18-18

LO 3 Apply the percentage-of-completion method for long-term contracts.

43 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration: Blue Diamond’s entries to recognize revenue

and gross profit each year and to record completion and final

approval of the contract.Illustration 18-19

44 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration: Content of Construction in Process Account—

Percentage-of-Completion MethodIllustration 18-20

45 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Financial Statement Presentation—Percentage-of-

Completion

Illustration 18-21

Computation of Unbilled Contract Price at 12/31/12

46 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

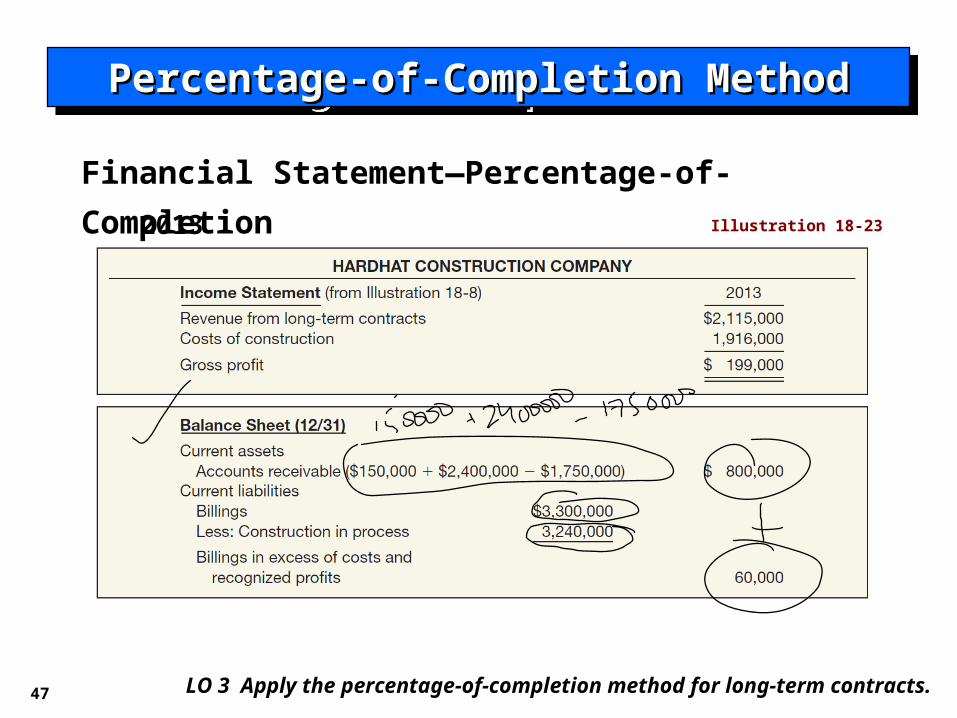

Financial Statement—Percentage-of-Completion

Illustration 18-22

Blue Diamond Construction Company

2012

47 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Financial Statement—Percentage-of-Completion

Illustration 18-23

Blue Diamond Construction Company

2013

48

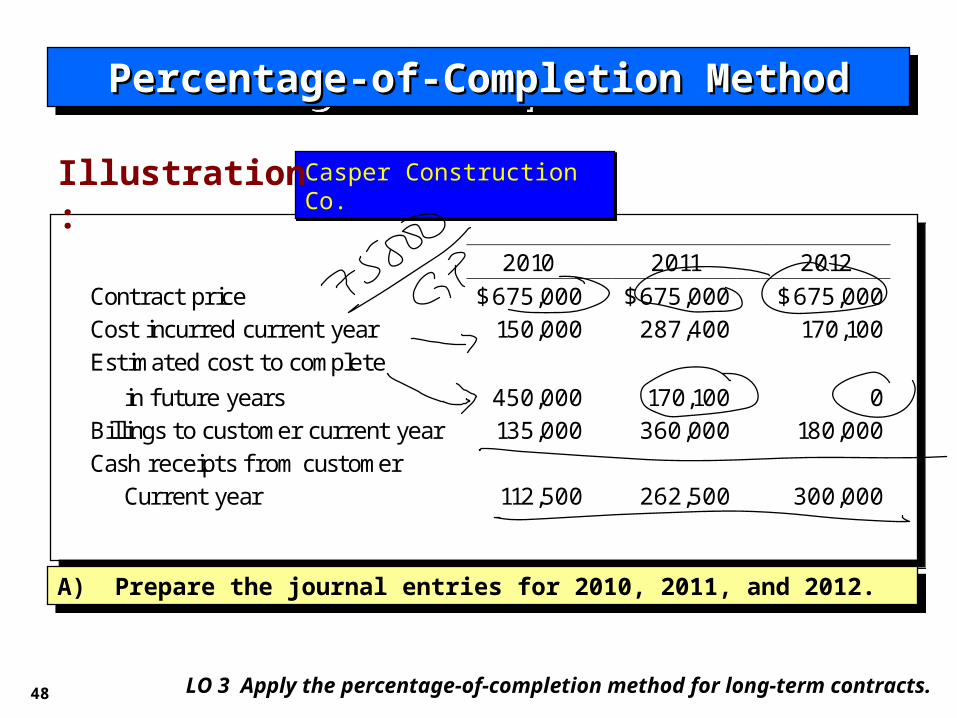

2010 2011 2012 Contract price $675,000 $675,000 $675,000 Cost incurred current year 150,000 287,400 170,100 Estimated cost to complete in future years 450,000 170,100 0 Billings to customer current year 135,000 360,000 180,000 Cash receipts f rom customer Current year 112,500 262,500 300,000

2010 2011 2012 Contract price $675,000 $675,000 $675,000 Cost incurred current year 150,000 287,400 170,100 Estimated cost to complete in future years 450,000 170,100 0 Billings to customer current year 135,000 360,000 180,000 Cash receipts f rom customer Current year 112,500 262,500 300,000

A) Prepare the journal entries for 2010, 2011, and 2012. A) Prepare the journal entries for 2010, 2011, and 2012.

Casper Construction Co. Casper Construction Co.

LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration:

49 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

2010 2011 2012

Costs incurred to date 150,000$ 437,400$ 607,500$

Estimated cost to complete 450,000 170,100

Est. total contract costs 600,000 607,500 607,500

Est. percentage complete 25.0% 72.0% 100.0%

Contract price 675,000 675,000 675,000

Revenue recognizable 168,750 486,000 675,000

Rev. recognized prior year (168,750) (486,000)

Rev. recognized currently 168,750 317,250 189,000

Costs incurred currently (150,000) (287,400) (170,100)

Gross profi t recognized 18,750$ 29,850$ 18,900$

Illustration:

50 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration:Construction in progress 150,000 287,400 170,100

Cash 150,000 287,400 170,100

Accounts receivable 135,000 360,000 180,000 Billings on contract 135,000 360,000 180,000

Cash 112,500 262,500 300,000 Accounts receivable 112,500 262,500 300,000

Construction in progress 18,750 29,850 18,900 Construction expense 150,000 287,400 170,100

Construction revenue 168,750 317,250 189,000

Billings on contract 675,000 Construction in progress 675,000

20122010 2011

51 LO 3 Apply the percentage-of-completion method for long-term contracts.

Percentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion MethodPercentage-of-Completion Method

Illustration:

Income Statement 2010 2011 2012

Revenue on contracts 168,750$ 317,250$ 189,000$

Cost of construction 150,000 287,400 170,100 Gross profit 18,750 29,850 18,900

Balance Sheet (12/31)Current assets:

Accounts receivable 22,500 120,000 - Cost & profits > billings 33,750

Current liabilities:Billings > cost & profits 9,000

52

End of Lecture 20End of Lecture 20End of Lecture 20End of Lecture 20