1. property value, tax levy, and taxpayers – the confusing questions equalization aid summer...

TRANSCRIPT

1

SCHOOL FINANCE ESSENTIALS

WASDA NEW ADMINISTRATORS WORKSHOP

* Bruce Anderson

School Finance ConsultantKaren Kucharz Robbe

School Finance Consultant

Department of Public Instruction

November 4, 2014

Property Value, Tax Levy, and Taxpayers – The Confusing Questions

Equalization Aid Summer School Fees

Agenda

Sample District Simplified Percentage Method (#1) District-Specific Simplified Percentage Method

District-Specific Formula Positioning (color grid) District-Specific Analysis of Equalization Aid

Formula Components

2 Focus Articles (used with permission from the Wisconsin Taxpayer’s Alliance)

School Property Tax Overview

Extra Resource Referenced: DOR 2014 Guide for Property Owners

Handouts

Property Value, Tax Levy, and

Taxpayers

Explaining the Tax LevyQuestions You’ll Likely Be Getting Soon

1. How can the school levy on one residential taxpayer’s bill go up by 15%, and the guy’s across the road from him go up by 25%?

2. How can a residential tax bill show an increase in the school district tax levy of 5.8% when the % year over year increase on the PI-401 was only 2.98%?

1. How can the school levy on one taxpayer’s bill go up by 15%, and the guy’s across the road from him go up by 25%?A. They live in different municipalities in

the school district. (the obvious answer, but may not be the only thing going on……)

Reasons (so far) That Answer Question #1

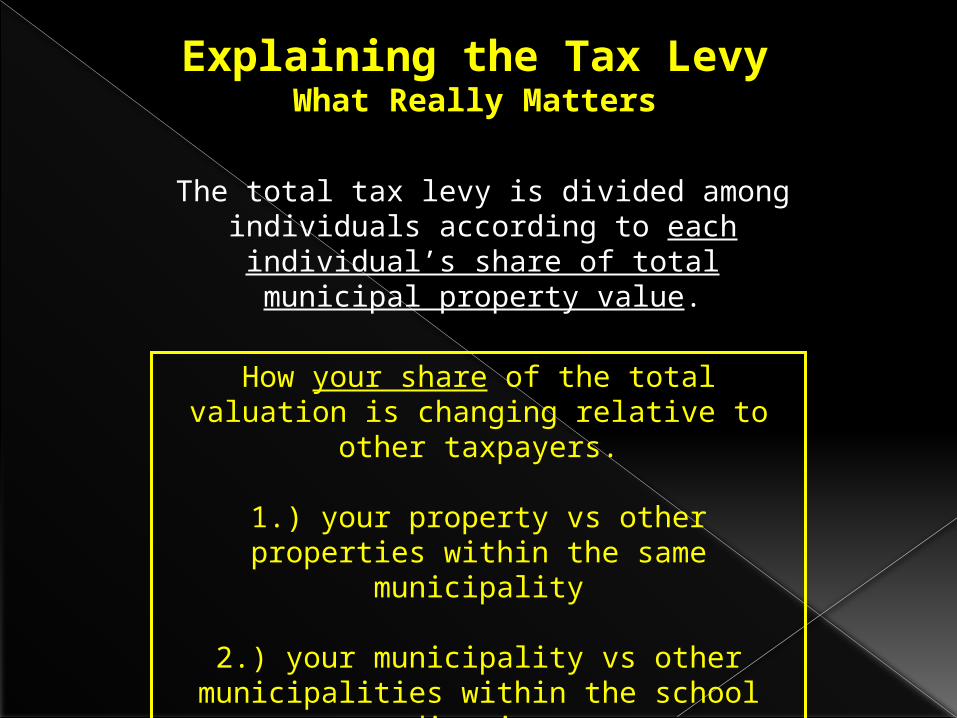

Explaining the Tax LevyWhat Really Matters

How your share of the total valuation is changing relative to other taxpayers.

1.) your property vs other properties within the same municipality

2.) your municipality vs other municipalities within the school district

The total tax levy is divided among individuals according to each individual’s share of total municipal property value.

Equalized & Assessed ValuationWhy Both?

1.) Assessment practices differ across the state. Property can be assessed at different percentages of market (equalized) value.

2.) Not all property is re-assessed every year.

Only requirements are: 1.) the assessment is within 10% of market

value; and 2.) there is equity between taxpayers within the

municipality.Each year, the Department of Revenue turns local

assessed valuations into equalized valuations. All school finance computations use equalized valuations.

Apportioning Taxes

Assessed Value

% of Total

$40,000

Levy

Tax Using

Assessed Value

Muni #1 $2,100,000

29.6% $40,000

$11,831

Muni #2 $4,500,000

63.4% $40,000

$25,352

Muni #3 $500,000 7.0% $40,000

$ 2,817

School District

$7,100,000

100.0%

$40,000

Assessment Ratio

(assessed ÷ equalized)

105%

90%

91%

EqualizedValue

% of Total

$40,000

Levy

Tax Using

Equalized Value

Equalized MillRate

Muni #1 $2,000,000

26.5% $40,000 $10,596 5.298

Muni #2 $5,000,000

66.2% $40,000 $26,490 5.298

Muni #3 $550,000 7.3% $40,000 $2,914 5.298

School District

$7,550,000

100.0%

$40,000

Muni AMuni B

Muni C

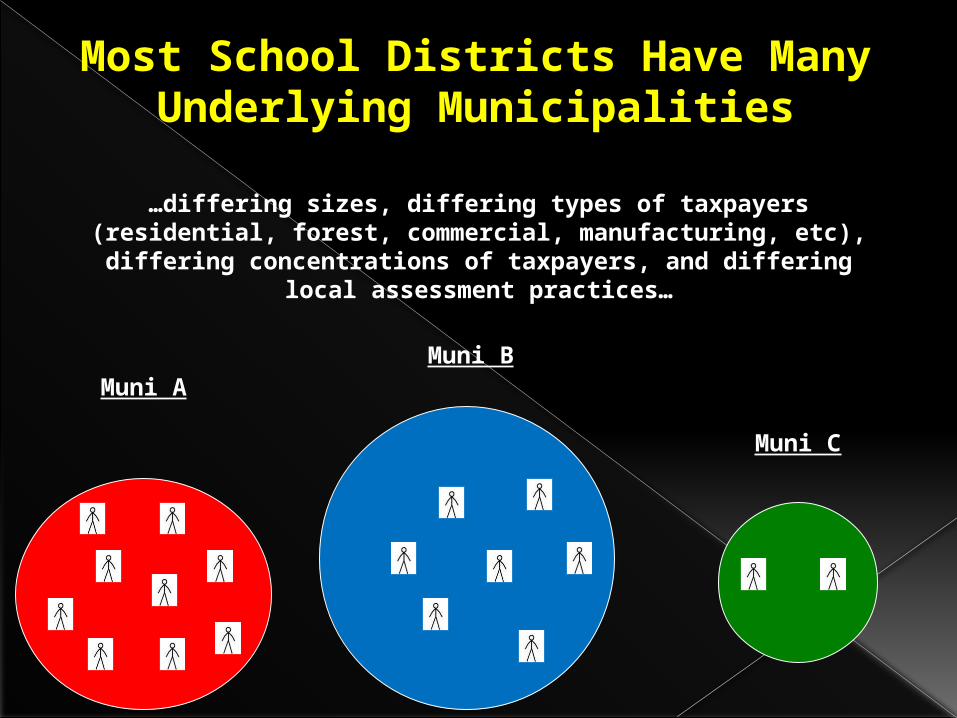

Most School Districts Have Many Underlying Municipalities

…differing sizes, differing types of taxpayers (residential, forest, commercial, manufacturing, etc),

differing concentrations of taxpayers, and differing local assessment practices…

Change in Assessed Valuation2 Residential Taxpayers

Total Municipal Assessed Property Value = $200,000

$100,00050%

$2,000 $2,000

$100,00050%

Each shares in the total property value at 50%, so each pays 50% of the total

levy.

Total Municipal Levy = $4,000

Change In Assessed Valuation2 Residential Taxpayers

Total Municipal Assessed Property Value = $300,000

Total Municipal Levy = $4,000

$2,320 $1,680

$174,00058%

$126,00042%

Assessed rate = $4,000/$300,000 = 13.34 mils ($13.34 per $1,000 of assessed

property value).

$126,000 x .01334

$174,000 x .01334

Explaining the Tax LevyMisconceptions

1. Higher assessments don’t necessarily mean higher taxes. Depends on how your assessment is changing in relation to the rest of the municipality.

How Assessed Valuation Works2 Residential Taxpayers

Total Municipal Assessed Property Value = $300,000

Total Municipal Levy = $4,000

$2,900 $1,680

$174,00058%

$126,00042%

$126,000 x .01334

$174,000 x .01334

Assessed rate = $4,000/$300,000 = 13.34 mils ($13.34 per $1,000 of assessed

property value).

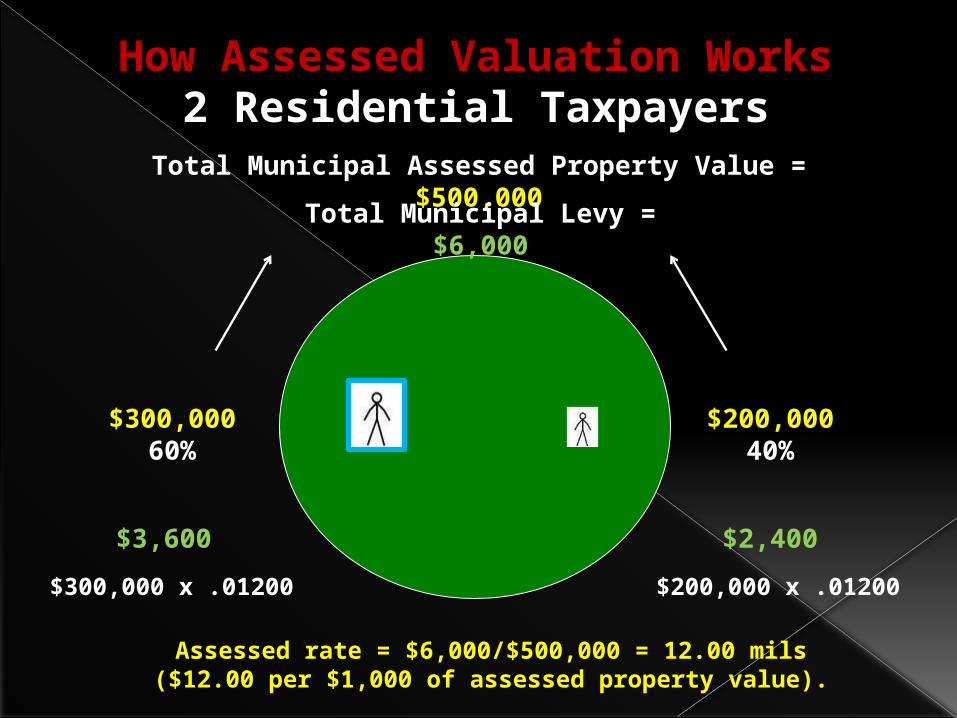

How Assessed Valuation Works2 Residential Taxpayers

Total Municipal Assessed Property Value = $500,000

Total Municipal Levy = $6,000

$3,600 $2,400

$300,00060%

$200,00040%

$200,000 x .01200

$300,000 x .01200

Assessed rate = $6,000/$500,000 = 12.00 mils($12.00 per $1,000 of assessed property value).

Explaining the Tax LevyMisconceptions

1. Higher assessments don’t necessarily mean high taxes. Depends on how your assessment is changing in relation to the rest if the municipality.

2. Lower tax rates don’t necessarily mean lower taxes. Depends on how the total levy and your assessment is changing.

1. How can the school levy on one taxpayer’s bill go up by 15%, and the guy’s across the road from him go up by 25%?A. They live in different municipalities in

the school district.

B. Individual property owner’s value increases as a percent of the municipality.

C. Municipal levy increases and/or individual property owner’s value increases as a percent of the municipality.

Reasons (so far) That Answer Question #1

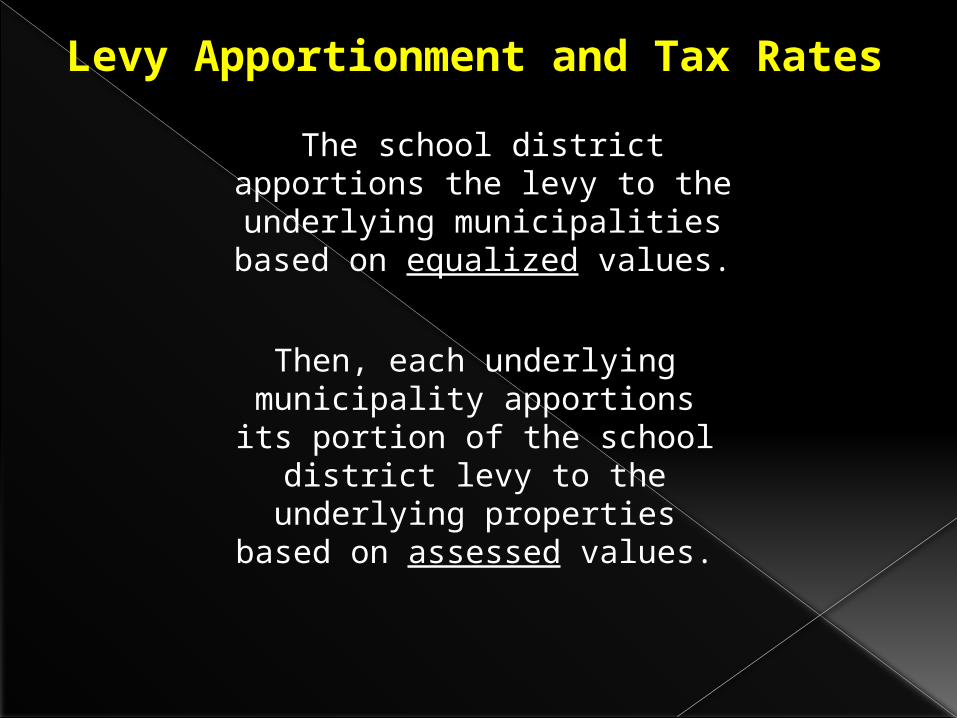

Levy Apportionment and Tax Rates

The school district apportions the levy to the underlying municipalities based on

equalized values.

Then, each underlying municipality apportions its

portion of the school district levy to the underlying

properties based on assessed values.

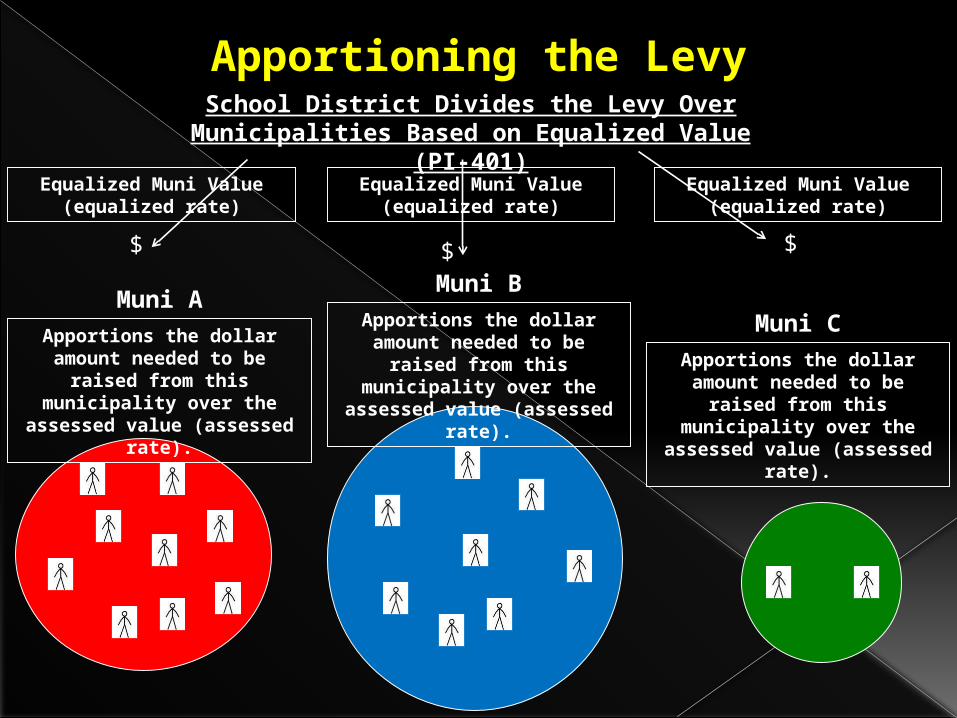

Apportioning the Levy

Muni AMuni B

Muni C

School District Divides the Levy Over Municipalities Based on Equalized Value

(PI-401)Equalized Muni Value

(equalized rate)Equalized Muni Value

(equalized rate)Equalized Muni Value

(equalized rate)

Apportions the dollar amount needed to be

raised from this municipality over the

assessed value (assessed rate).

Apportions the dollar amount needed to be

raised from this municipality over the

assessed value (assessed rate).

Apportions the dollar amount needed to be

raised from this municipality over the

assessed value (assessed rate).

$ $ $

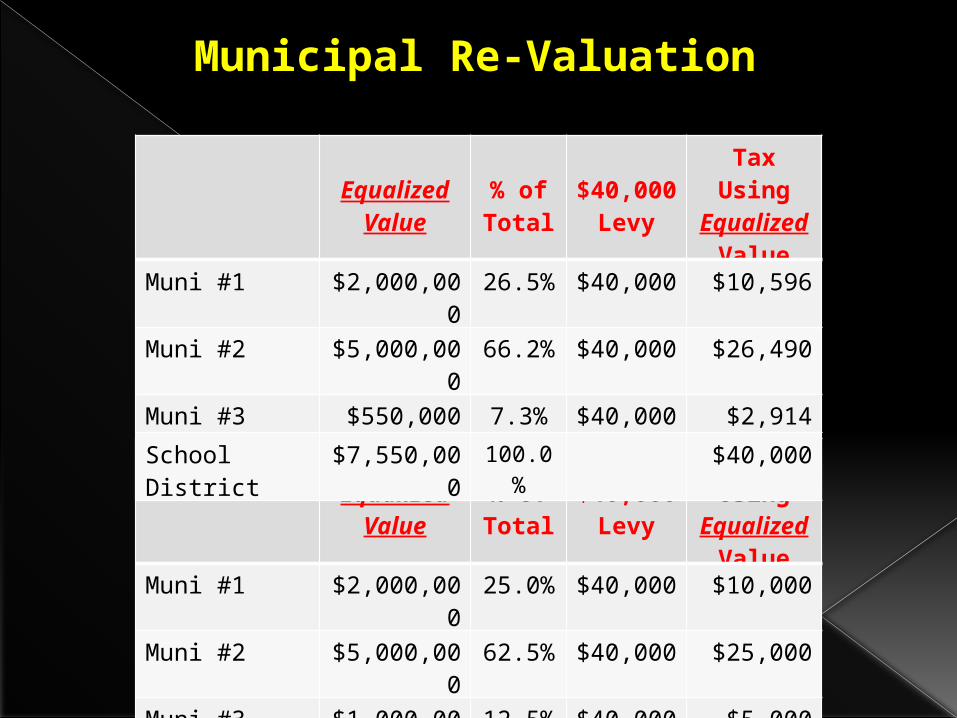

Municipal Re-Valuation

EqualizedValue

% of Total

$40,000

Levy

Tax Using

Equalized Value

Muni #1 $2,000,000

25.0% $40,000 $10,000

Muni #2 $5,000,000

62.5% $40,000 $25,000

Muni #3 $1,000,000

12.5% $40,000 $5,000

School District

$8,000,000

100.0%

$40,000

EqualizedValue

% of Total

$40,000

Levy

Tax Using

Equalized Value

Muni #1 $2,000,000

26.5% $40,000 $10,596

Muni #2 $5,000,000

66.2% $40,000 $26,490

Muni #3 $550,000 7.3% $40,000 $2,914

School District

$7,550,000

100.0%

$40,000

1. How can the school levy on one taxpayer’s bill go up by 15%, and the guy’s across the road from him go up by 25%?A. They live in different municipalities in

the school district.

B. Individual property owner’s value increases as a percent of the municipality.

C. Municipal levy increases and/or individual property owner’s value increases as a percent of the municipality.

D. Municipality goes through a re-valuation.

Reasons That Answer Question #1

Muni AMuni B

Muni C

Most School Districts Have Many Underlying Municipalities

…differing sizes, differing types of taxpayers (residential, forest, commercial, manufacturing, etc),

differing concentrations of taxpayers, and differing local assessment practices…

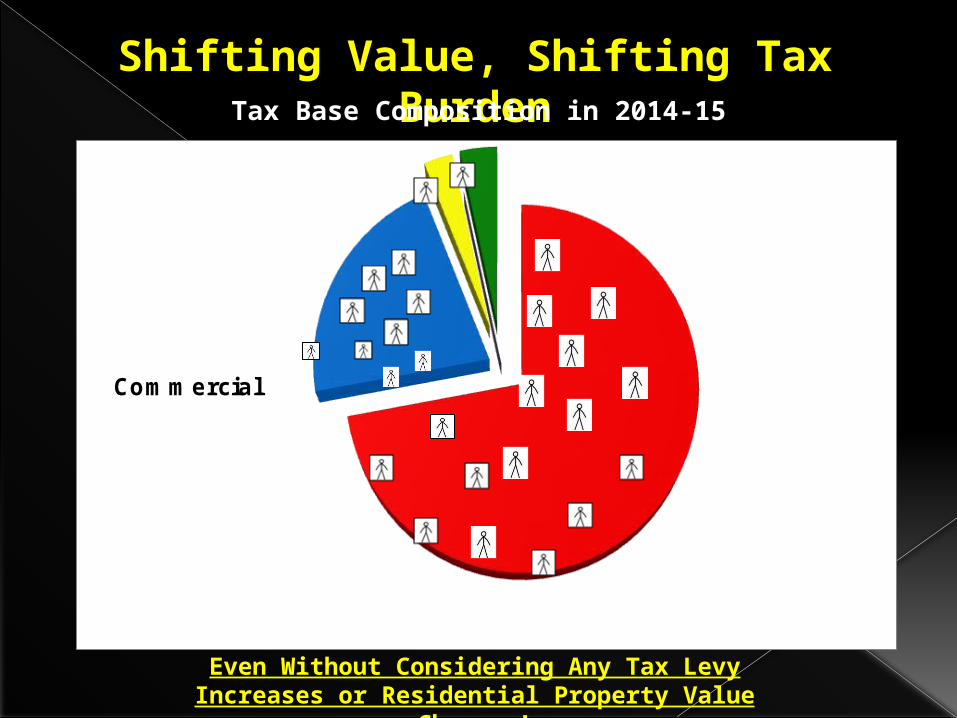

Tax Base Composition Shifting(what happens within just 1 municipality)

One Final Thing to Consider

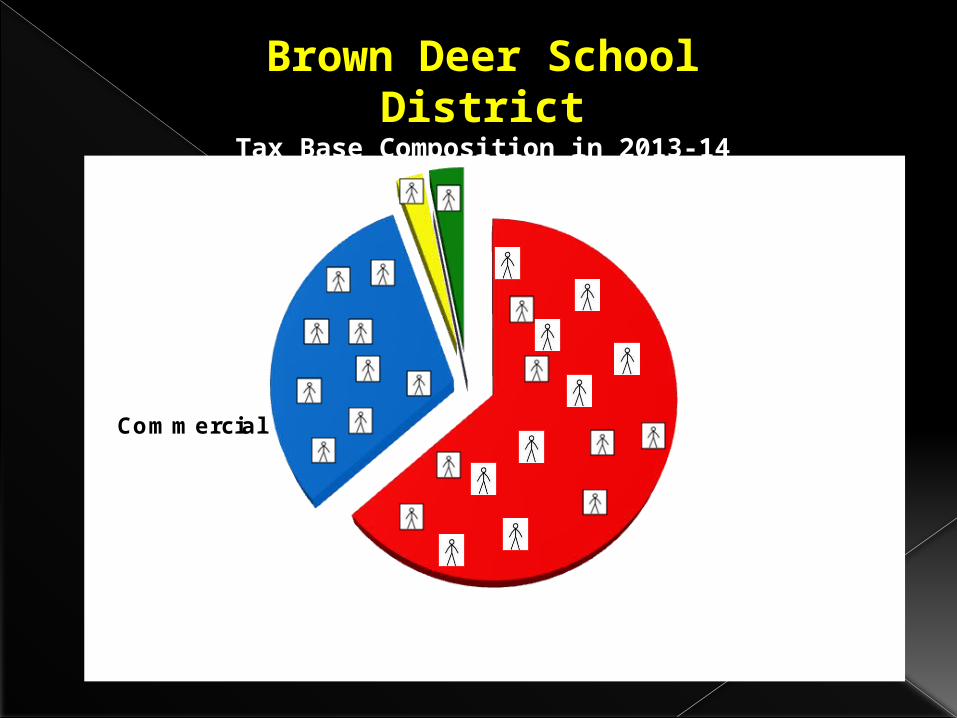

Brown Deer School District

Item 2013-14 2014-15 % Change

Residential 63.66324% 64.55778% 1.41%

Commercial 30.79951% 29.52597% -4.13%

Manufacturing 2.41129% 2.65067% 9.93%

Agricultural .00019% .00019% 1.17%

Personal 3.12577% 3.26538% 4.47%

100.000% 100.000% 0.00%

Brown Deer School DistrictTax Base Composition

Commercial

Residential

Brown Deer School District

Tax Base Composition in 2013-14

Commercial

Residential

Shifting Value, Shifting Tax Burden

Even Without Considering Any Tax Levy Increases or Residential Property Value

Changes!

Tax Base Composition in 2014-15

Reasons That Answer Question #2

1. Tax base composition shifting.

2. The percentage the credits (School Levy, Lottery and Gaming, First Dollar) were of the total changed from 2013-14 to 2014-15.

Tracking the details that cause property tax changes, given the many underlying municipalities in a school

district, is virtually impossible.

But, now you have a list of items that could be the cause.

Conclusion

Equalization Aid

Under Article 10 of WI State Constitution, the State Legislature is responsible for establishing school

districts which are to be:

“as uniform as practicable … ”

“free and without charge for tuition to all children”

“each town and city shall be required to raise by tax, annually, for the support of common schools therein……”

How does the Legislature achieve this?

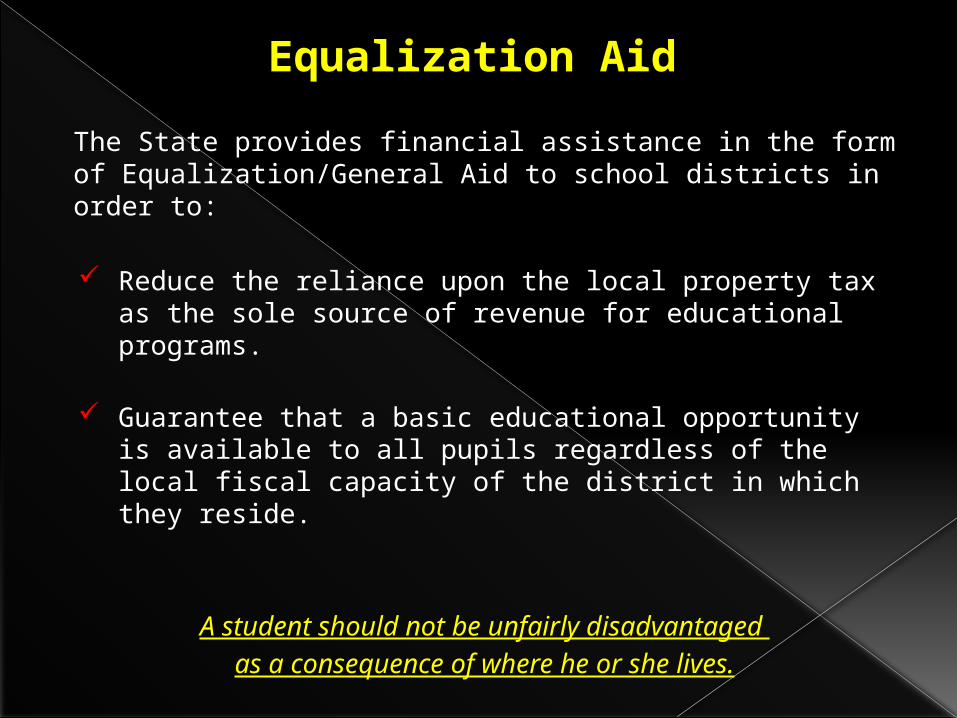

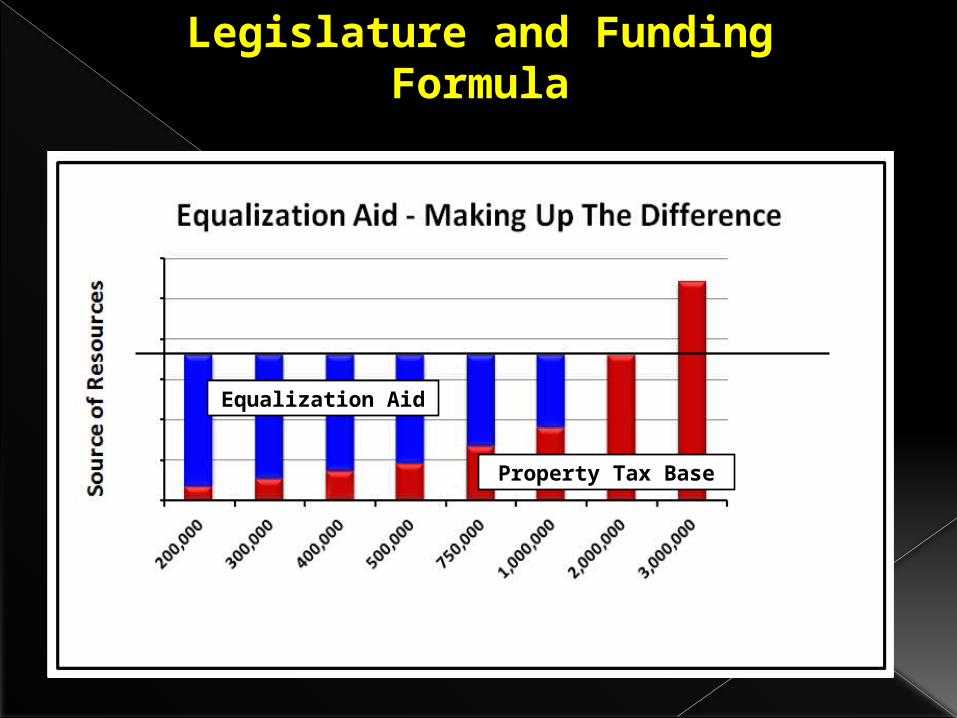

Why Equalization Aid?

Equalization Aid

The State provides financial assistance in the form of Equalization/General Aid to school districts in order to:

Reduce the reliance upon the local property tax as the sole source of revenue for educational programs.

Guarantee that a basic educational opportunity is available to all pupils regardless of the local fiscal capacity of the district in which they reside.

A student should not be unfairly disadvantaged as a consequence of where he or she lives.

Legislature and Funding Formula

Equalization Aid

Property Tax Base

Why do you need to know how to calculate aid when DPI calculates it for you?

Because you will be asked by your board members, constituents, and the media.

So you can figure out why your aid has changed AND explain why.

Because you may want to do estimates and run “what if” scenarios …

Equalization Aid

State “shares” in district cost.

Aid is based on a district’s ability to pay, as measured by its property wealth per member.

Basic premise: The more property wealth per member a district has, the lower the percent (proportion) of shared costs that will be aided by the state through the

equalization aid formula.

Equalization Aid

District Factors

- shared cost

- equalized property value

- membership

State Factors

- cost ceilings

- guaranteed valuations per member

- total amount of funding available for distribution

What determines where a district is in the formula?

Equalization Aid

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary Aid

Positive Tertiary

Aid

District Value per Member

10% 90%

75%25%

50%50%

Equalization Aid Formula

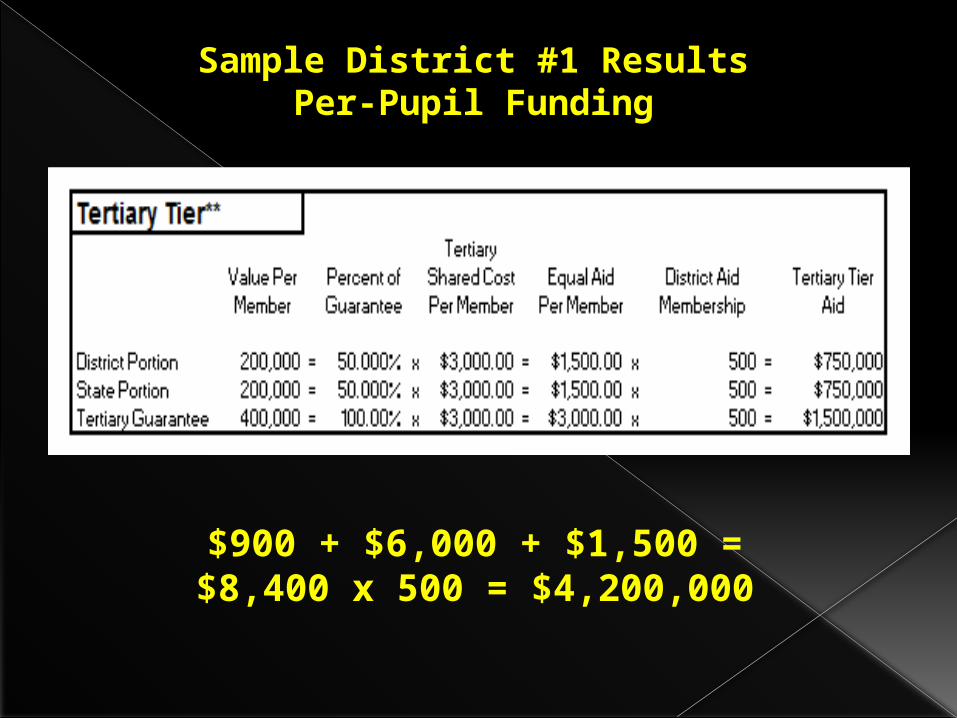

Sample District #1 ResultsPer-Pupil Funding

Sample District #1 ResultsPer-Pupil Funding

$900 + $6,000 + $1,500 = $8,400 x 500 = $4,200,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

0 200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary

Aid

Positive

Tertiary

Aid

Negative Tertiary Aid

Equalization Aid Formula

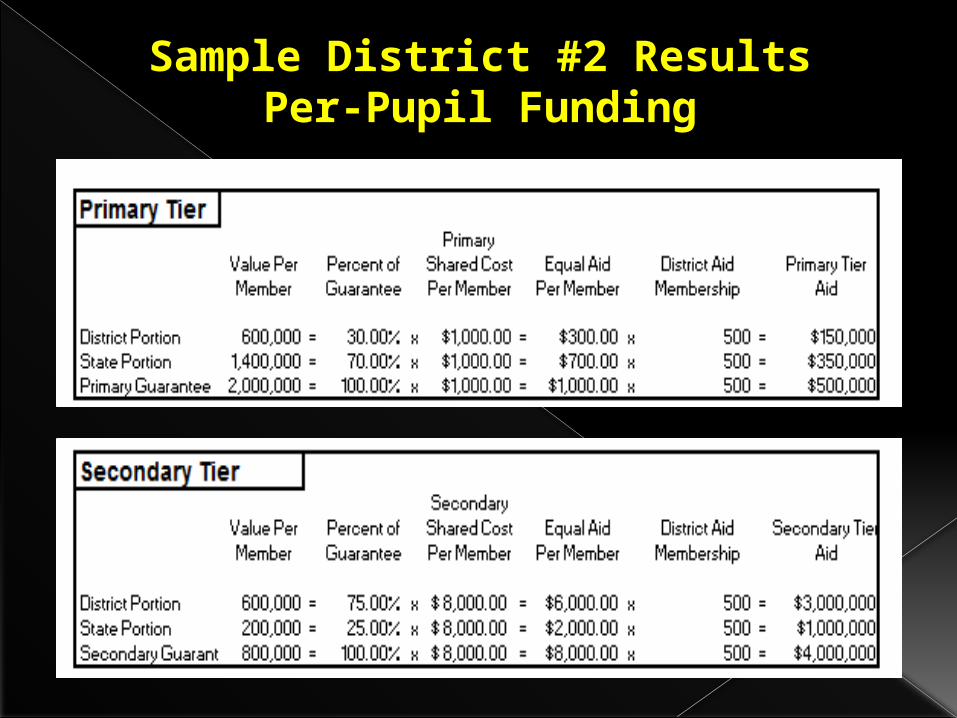

Sample District #2 ResultsPer-Pupil Funding

Sample District #2 ResultsPer-Pupil Funding

$700 + $2,000 - $1,500 = $1,200 X 500 = $600,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

DISTRICT VALUE PER MEMBER

DIS

TR

ICT

SH

AR

ED

CO

ST

PE

R M

EM

BE

R

Positive Primary Aid

Positive Secondary Aid

Positive Tertiary

Aid

District Value per Member

Equalization Aid Formula

Bonduel’s property value is fairly consistent, but their membership is really dropping, causing their value per member to increase over time. As value per member increases, the formula gives less aid.

Equalization Aid Resources on the School Financial Services Website

“October 15, 2014 Equalization Aid Computation – Percentage Method – Algebraic

Format”

Location: SFS Homepage > Longitudinal Data > Equalization Aid

http://sfs.dpi.wi.gov/sfs_buddev_eq

“2014-15 Equalization Aid Formula Position”“Multi-Year Longitudinal Analysis of General and Equalization Aid Formula Components”

Suggested Monitoring Activities

(after the summer program) Confirm fees collected

Confirm expenditures for eligible supplies

Compare fees collected with actual costs

If you have an excess of revenues over expenditures then refund the under spent portion of the fee

This is done on a course by course basis

Summer School Fees

What will auditors ask for? PI-1804W-2 (Worksheet)

Summer school list of classes and fees

Should not be a flat fee (difficult to link a flat fee to actual expenditures)

Expenditures (by course) for the classes that charge fees

Run a detailed report of the appropriate function and object and identify for auditor those used for summer school

May be asked to pull some invoices

Summer School Fees

What will auditors test for? Fees are not charged as a flat fee across

all courses Costs identified by course are eligible costs Costs that are eligible do not exceed fees

charged (by course)

For full presentation from WASBO Accounting Conference - March 18-20, 2014 go to:

http://sfs.dpi.wi.gov/sites/default/files/imce/sfs/ppt/Summer%20School_March%202014.pptx

Summer School Fees

VISIT OUR WEBSITE: http://sfs.dpi.wi.gov… or CALL US (all 608 Area Code):

• Robert Soldner, Director 266-6968 • Bruce Anderson, Consultant 267-9707• Carey Bradley, Consultant 267-3752 • Dan Bush, Consultant 267-9212• Karen Kucharz Robbe, Consultant 266-3464• Gene Fornecker, Auditor 267-7882• Brian Kahl, Auditor 266-3862• Michele Gundrum, Auditor 267-9218• Victoria Chung, Accountant 266-9205

Thanks to WASDA for the opportunity to speak to you

today!