1 progressive states network: aca 101 sara rosenbaum, j.d. harold and jane hirsh professor, health...

TRANSCRIPT

1

Progressive States Network:ACA 101

Sara Rosenbaum, J.D.

Harold and Jane Hirsh Professor, Health Law and Policy

June 10, 2013

What Key Problems Was the ACA Designed to Address?

1. The lack of an accessible pathway to affordable insurance coverage for millions who– lack employer coverage– do not qualify for Medicaid because they don’t fit

the traditional coverage pathways and have incomes that are too “high”

– face a broken individual insurance market that barred people on the basis of health, cost, or both

2

What Key Problems Was the ACA Designed to Address?

2. Coverage that lacked value, leaving people without protection against both preventive benefits and catastrophic costs

– At one end, failure to cover high-value preventive benefits such as immunizations and screening for cancer, high blood pressure and other conditions

– At the other end, annual and lifetime limits on coverage that left persons with uncovered catastrophic costs

– Commonwealth Fund: 125 million Americans uninsured or underinsured

3

What Key Problems Was the ACA Designed to Address?

3. Poor access to health care services, especially urban and rural medically underserved communities lacking primary care

4. A health care system characterized by high costs and poor quality

– The highest per capita health spending in the world

– Failure to deliver services of known value in appropriate settings

– Failure to connect patients with medical and health homes

– Insufficient attention to prevention

– Payment systems that incentivize volume over value

– Excessive readmissions and preventable hospital-acquired conditions

4

Affordable Care Act Provisions Focus and Opportunities

Cathy Schoen, Senior Vice PresidentThe Commonwealth Fund

Progressive States Network ACA 101 WebinarJune 10, 2013

6

National Legislation – State/Local Reforms: Resources and Opportunities to Improve

• Insurance reforms: expand and improve coverage

– Enhance affordability and new market rules

• Payment reforms to support and stimulate innovation

– Primary care and Patient-Centered Care Teams

– Accountable Care Organizations

– Medicare, Medicaid and Private Initiatives

• Innovation Center: flexibility to partner/try new ideas

• Information systems and transparency

• New resources and tools to improve

– Access, quality/outcomes, and lower costs

7

Source: Modification of S. Guterman, et al. “Innovation in Medicare And Medicaid Will Be Central To Health Reform’s Success,” Health Affairs 29, no. 6 (June 2010).

ACA Timeline: Insurance, Payment and System Innovation Reforms

2010 2011 2012 2013 2014 2015

Initial insurance reforms

10% Medicare Primary Care

Increase

Innovation Center (CMMI)

Value-based Purchasing for

Hospitals

Primary Care and Health Homes

Reduce Payment for Preventable

Readmissions

Medicare Shared Savings (ACOs)

National Medicare Payment Bundling

Pilot

Major Insurance Expansions

Insurance Exchanges +

Credits

Medicaid

Insurance Market reforms

Value-based Purchasing for

Physicians

Medicaid Primary Care Payment up

to Medicare Levels

Reduce Payment for Hospital

Acquired Infections

Patient Centered Outcomes Research

Pioneer ACOs

Bundled Payment Improvement

Initiative

State InnovationGrants

October EnrollmentStarts for InsuranceExchanges for Jan 1, 2014

8

Insurance Expansion and Market Reforms

• New insurance marketplaces in all states for individuals and small business– Choice of qualified plans – web-based enrollment– Federal credits to lower premiums and cost sharing– State-based: federally run, partner, or state-run– Enrollment starts Oct 2013 for coverage in 2014

• Medicaid expansion to 138% of poverty ($ ) at state option– First 3 years 100 percent federal financed– Phase to 90 percent federal

• Insurance market reforms for all states– Premium oversight and benefit standards– Prohibition on higher premiums based on sex or health– Requirement to have insurance (low penalty starts 2014)

3% - 7%8% - 12% 13% - 18%19% - 24%25% - 31%

Adults Children

50 Million Uninsured 2010/11Percent of Adults (19-64) and Children (0-18) Uninsured

Data Source: Commonwealth Fund analysis U.S. Census Bureau, March 2011-12 Current Population Survey

9

9

Four levels of cost-sharing: 1st tier (Bronze) actuarial value: 60% 2nd tier (Silver) actuarial value: 70% 3rd tier (Gold) actuarial value: 80% 4th tier (Platinum) actuarial value: 90%

Premium Tax Credits and Cost-Sharing ProtectionsUnder the Affordable Care Act

Federal Poverty Level

IncomePremium

contribution as a share of income

Out of Pocket limits

Actuarial value: Silver plan

< 100%S: $11,490F: $23,550

MedicaidNo credits available Medicaid Medicaid

100 to 133% S: <$15,282F: <$31,322

2% if credit (or Medicaid)

S: $1,983F: $3,967

94%

133%- 149%S: $15,282 - <17,235F: $31,322 - <35,325

3.0%–4.0% 94%

150%–199%S: $17,235 - <22,980F: $35,325 - <47,100

4.0%–6.3% 87%

200%–249%S: $22,980 - <28,725F: $47,100 - <58,875

6.3%–8.05%S: $2,975F: $5,950

73%

250%–299%S: $28,725 - <34,470F: $58,875 - <70,650

8.05%–9.5% 70%

300%–399%S: $34,470 - <45,960F: $70,650 - <94,200

9.5%S: $3,967F: $7,933

70%

400%+S: $45,960+F: $94,200+

—S: $5,950F: $11,900

—

Note: Actuarial values: average percent of medical costs covered by plan. Premium and cost-sharing credits are for silver plan.Source: Federal poverty levels are for 2013; Commonwealth Fund Health Reform Resource Center: What’s in the Affordable Care Act? (PL 111-148 and 111-152), http://www.commonwealthfund.org/Health-Reform/Health-Reform-Resource.aspx.

10

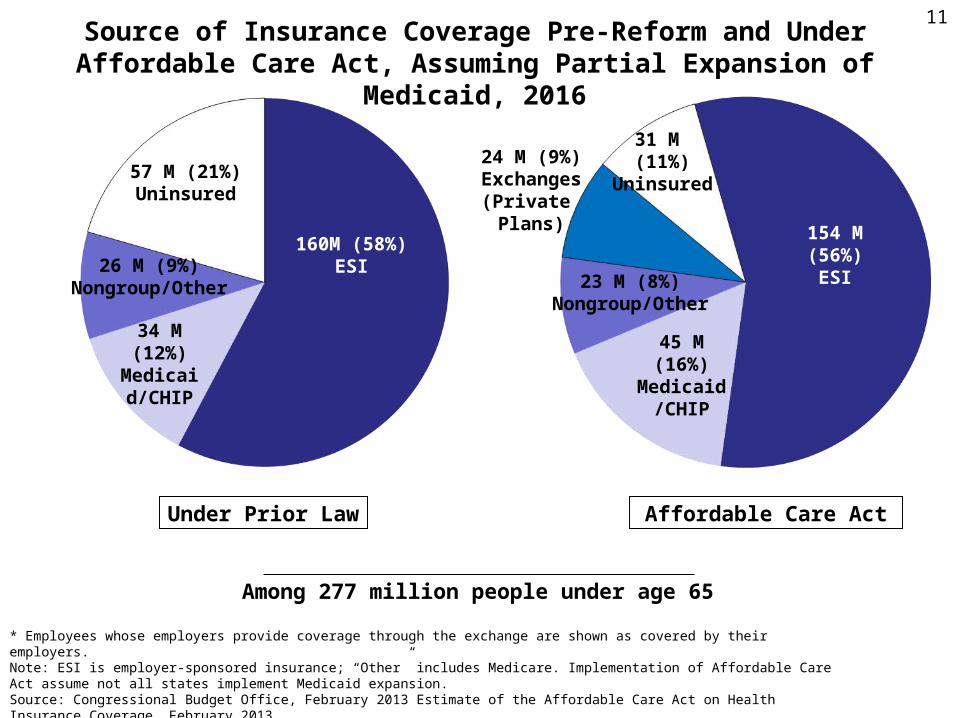

Source of Insurance Coverage Pre-Reform and Under Affordable Care Act, Assuming Partial Expansion of Medicaid, 2016

* Employees whose employers provide coverage through the exchange are shown as covered by their employers. Note: ESI is employer-sponsored insurance; “Other” includes Medicare. Implementation of Affordable Care Act assume not all states implement Medicaid expansion.Source: Congressional Budget Office, February 2013 Estimate of the Affordable Care Act on Health Insurance Coverage, February 2013. http://www.cbo.gov/sites/default/files/cbofiles/attachments/43900_ACAInsuranceCoverageEffects.pdf

Among 277 million people under age 65

Under Prior Law Affordable Care Act

45 M (16%)Medicaid/

CHIP

24 M (9%)Exchanges

(Private Plans)

23 M (8%)Nongroup/Other

31 M (11%)

Uninsured

154 M (56%)ESI

160M (58%)ESI

34 M (12%)

Medicaid/CHIP

57 M (21%)Uninsured

26 M (9%)Nongroup/Other

11

Source: National Conference of State Legislatures, Federal Health Reform: State Legislative Tracking Database. http://www.ncsl.org/default.aspx?TabId=22122; Avalere State Reform Insights; Center of Budget and Policy PrioritiesPolitico.com; Commonwealth Fund Analysis.

Medicaid Expansion

State Action on Establishing Health Insurance Marketplaces and Participation in Medicaid Expansion, As of May 2013

Health Insurance Marketplaces

Expanding (22 + DC)

Not expanding (16)

Unclear/undecided (9)

Expanding with variation (3)

Pursuing state-run exchange (17 + DC)

Pursuing state-federal partnership exchange (7)

Pursuing federally facilitated exchange (26)

12

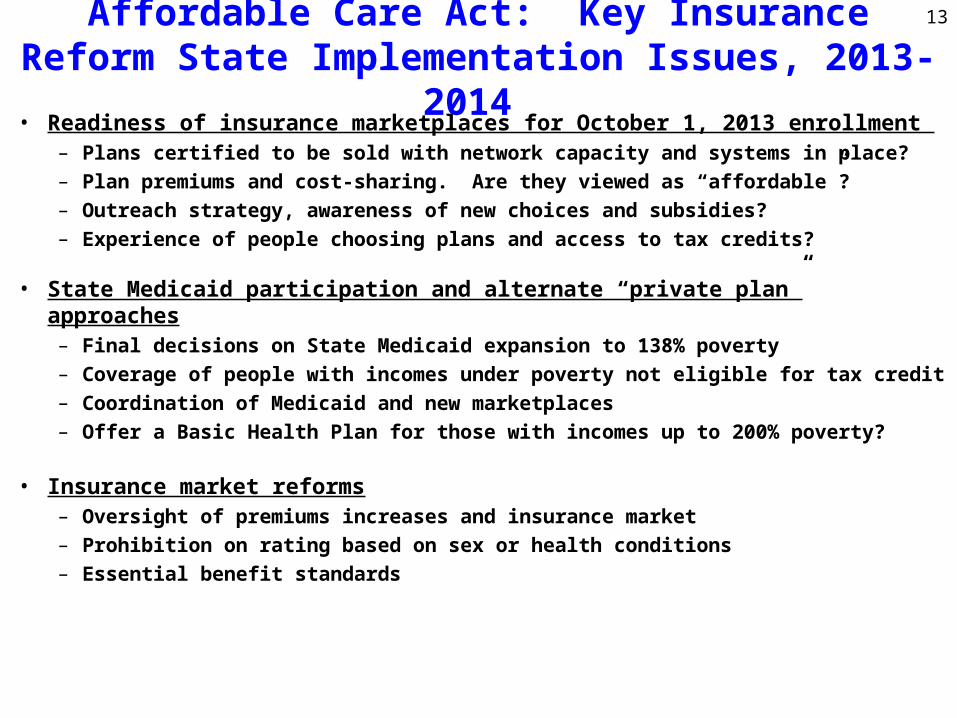

Affordable Care Act: Key Insurance Reform State Implementation Issues, 2013-2014

• Readiness of insurance marketplaces for October 1, 2013 enrollment – Plans certified to be sold with network capacity and systems in place?– Plan premiums and cost-sharing. Are they viewed as “affordable”? – Outreach strategy, awareness of new choices and subsidies? – Experience of people choosing plans and access to tax credits?

• State Medicaid participation and alternate “private plan” approaches– Final decisions on State Medicaid expansion to 138% poverty– Coverage of people with incomes under poverty not eligible for tax credit – Coordination of Medicaid and new marketplaces – Offer a Basic Health Plan for those with incomes up to 200% poverty?

• Insurance market reforms– Oversight of premiums increases and insurance market– Prohibition on rating based on sex or health conditions– Essential benefit standards

13

Common ACA Myths1. The federal government will control the health care system

– A fundamentally state-based approach to system reform, within very broad federal parameters

2. Medicaid is costly and broken and needs an entire makeover – Medicaid is effective in improving health care access and

population health– Per capita Medicaid costs well below private insurance– States get $9.00 for every $1.00 invested. The 2014 adult

expansion = virtually no new net costs to states compared to current spending levels

3. Health Insurance Marketplaces are too complicated to work– Similar to any online shopping experience – Prior experience in Massachusetts and Utah– Outreach and assistance through Navigators & enrollment

assisters

14

Common ACA Myths

4. Reform will harm small employers– Smaller low-wage employers without health plans

are the biggest beneficiaries of the new Marketplaces and Medicaid expansions

5. Health insurance costs will skyrocket

Early reports: premium costs below projections without taking premium subsidies and cost-sharing assistance into account.

15

16Moving Forward: Improving Care System Performance and Confronting Cost

Uninsured Rates

Quality of Care Chasm

Costs of Care

Fragmentation &

Complexity

2003 2011

Affordability a Shared Concern: Premiums Rising Faster than Incomes Across the Country: 2003 and 2011

Sources: 2003 and 2011 Medical Expenditure Panel Survey–Insurance Component (for total average premiums for employer-based health insurance plans); 2003–04 and 2010–11 Current Population Surveys (for median household incomes for under-65 population).

Less than 14% 14%–16.9% 17%–19.9% 20% or more

ND

SD

DC

ID

DE

IA

IN

WI

CA

HI

KS

UT

AZ NM AR

LA

KYVA

VT NH

MA

CTRI

NJ

AK

ALMS

MI

ME

WV MDCO

NE

WY

OR

IL

TN NC

SCGA

FL

PA

NY

OH

MO

MN

OK

TX

MT

NV

WA

ND

SD

DC

ID

DE

IA

IN

WI

CA

HI

KS

UT

AZ NM AR

LA

KYVA

VT NH

MA

CTRI

NJ

AK

ALMS

MI

ME

WV MDCO

NE

WY

OR

IL

TN NC

SCGA

FL

PA

NY

OH

MO

MN

OK

TX

MT

NV

WA

80 percent of under-65 population live where premiums amount to 20 percent or more of median (middle) income

SOURCE: Schoen et al., State Trends in Premiums and Deductibles, 2003–2011: Eroding Protection and Rising Costs Underscore Need for Action, The Commonwealth Fund, December 2012.

17

ACA: Payment and Health System Reforms: Improving Outcomes and Lowering Cost

• Payment reforms to support and stimulate system innovation

– Primary care: enhance payment and “medical homes”

– Accountable care organizations: provider networks accountable for outcomes and total costs

– More “bundled” payments: total costs of care episode

– Pay for value: reduced payment for infections, readmissions

• Partnership with State Medicaid and Private Payers

• Federal Innovation Center: support private and state initiatives

• Investment in Information Systems & Data: guide and inform

18

19

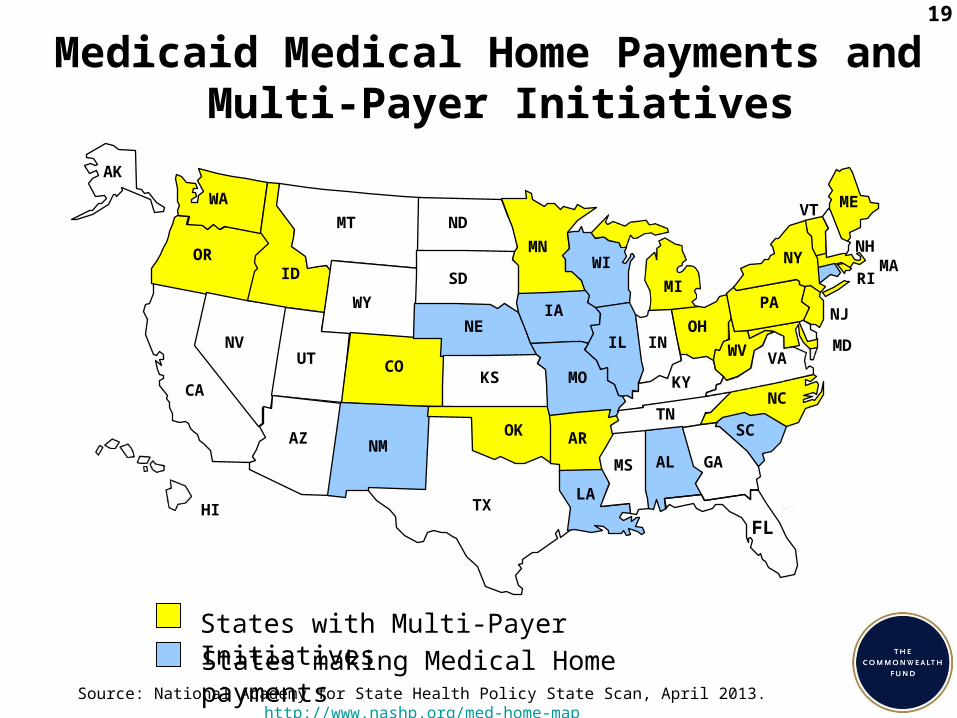

Medicaid Medical Home Payments and Multi-Payer Initiatives

Source: National Academy for State Health Policy State Scan, April 2013. http://www.nashp.org/med-home-map

WA

OR

TX

CO

NC

LA

PA

NY

IA

VA

NE

OK

RI

AL

MD

MT

ID

KS

MN NHMA

ME

AZ

VT

MOCA

WY

NM

IL

WI

MI

WV

SC

GA

FLHI

UTNV

ND

SD

AR

INOH

KY

TN

MS

AK

States with Multi-Payer InitiativesStates making Medical Home payments

NJ

Hawaii Puerto Rico

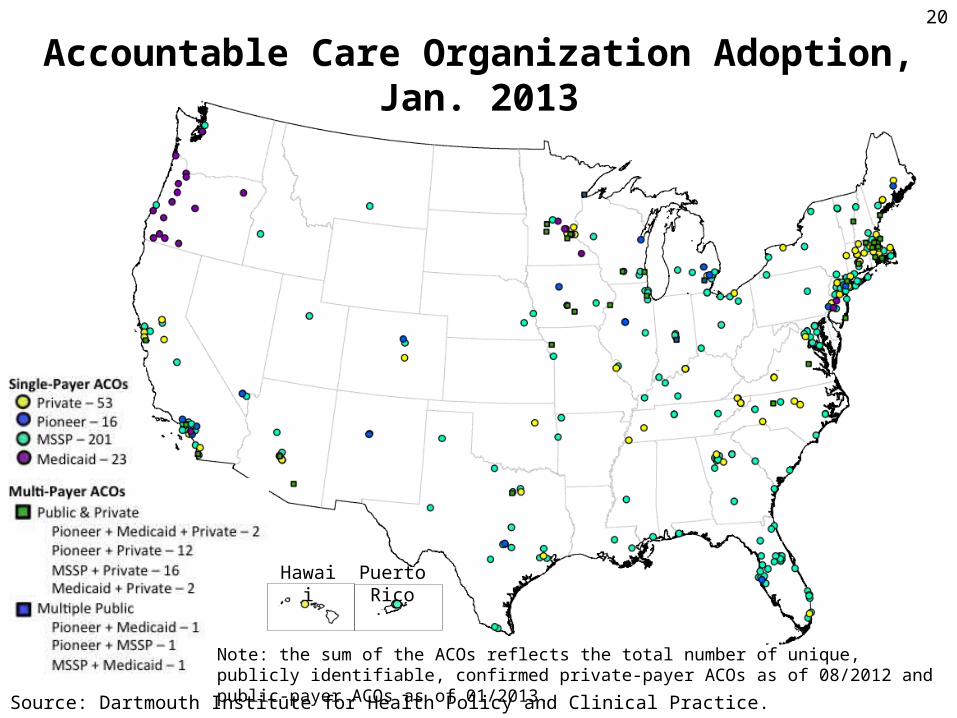

Accountable Care Organization Adoption, Jan. 2013

Note: the sum of the ACOs reflects the total number of unique, publicly identifiable, confirmed private-payer ACOs as of 08/2012 and public-payer ACOs as of 01/2013.

Source: Dartmouth Institute for Health Policy and Clinical Practice.

20

Reduced Payments for Avoidable Complications

Medicare Advantage Plan Bonuses

Bundled Payments

Physician Quality Reporting System

Meaningful Use

Value Based Purchasing

AccountableCare Organizations

Hospital Inpatient Quality Reporting

Medical Homes

The Affordable Care Act21

Prevention and PopulationHealth

ACA and Beyond: State Actions

• ACA reforms provide a foundation + new resources, tools– State policy and care system leaders’ action to move forward

• Key opportunities to build on momentum– Payer partnership with Medicare, Medicaid, private– Build innovation into state supported programs– Transparent all-payer data on quality and costs– Targets and benchmarks: populations and geographic areas

• Strategic action for public health as well as delivery systems

• Oversight to hold care systems and insurers accountable

– Licensure and regulatory authority

– Malpractice and other market reforms

• Future webinar: Delivery system and payment reforms

22