1 polish bank association boleslaw meluch expert real estate finance committee vice president,...

TRANSCRIPT

1

Polish Bank Association

Boleslaw MeluchExpert

Real Estate Finance Committee

Vice President, European Property Vice President, European Property InstituteInstitute

„The Role of Data Base in Mortgage Market Development,

Polish Experiences”

2nd Hypothecary ForumMarch 1-2, 2007Sankt Petersburg

2

Agenda

1. Why data bases are to be built ?

2. Standardization in Risk Management Process

3. Mortgage Loans Processes Standardization

4. Mortgage Loans Portfolio Risk Management

5. Regulatory Requirements in Mortgage Portfolio Management in Poland

6. Our achievements

7. Future (development plans)

Polish Bank Association

3

Polish Bank Association

1. Product standardization

2. Documentation standardization

3. Business practices

standardization

4. Data and information access

standardization

5. Property Appraisal

Standardization

Standardization in Risk Management Process

4

Polish Bank Association

1. Origination

2. Underwriting

3. Servicing

4. Funding

Mortgage Loans Processes Standardization

5

Polish Bank Association

1. Origination• Pricing• Advertising and Marketing• Consumer Education• Closing of the mortgage

• Consumer credit reporting• Settlement cost

o title insurance,o survey, o appraisals, o credit checks, o loan origination and

documentationo fees, o commitment and

processing fees, o hazard and mortgage

insuranceo interest prepayments.

Mortgage Loans Processes Standardization

6

Polish Bank Association

2. Underwriting• Collateral

o Appraised value of the homeo Down payment

• Credit reputationo Credit history

• Capacityo Income Verificationo Debt ratioo Cash reserves (Verification of

assets)o Taxes

• Standard scoring methods across lenders

Mortgage Loans Processes Standardization

7

Polish Bank Association

3. Servicing

• Payment Processing

• Collections

• Customer Service

• Loss Mitigation

• Reporting to Credit Bureau

Mortgage Loans Processes Standardization

8

Polish Bank Association

4. Funding

• Source of funding

• Cost of funding

• Margin Determination

• Secondary Mortgage Market Conduit

Requirements

Mortgage Loans Processes Standardization

9

Polish Bank Association

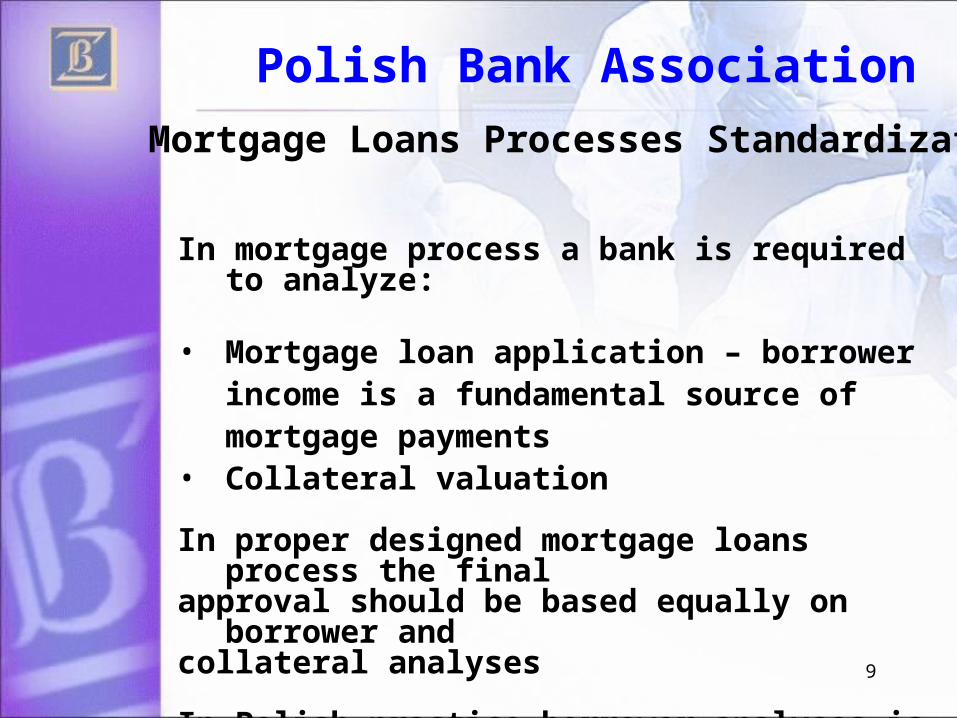

In mortgage process a bank is required to analyze:

• Mortgage loan application – borrower income is a fundamental source of mortgage payments

• Collateral valuation

In proper designed mortgage loans process the final

approval should be based equally on borrower and

collateral analyses

In Polish practice borrower analyses is more important

Mortgage Loans Processes Standardization

10

Polish Bank Association

Mortgage Loans Portfolio Risk ManagementCredit Risk of

MortgagePortfolio

Identification

Measurement

Modeling Instruments

Borrower Income • Credit history

• Client’s ability to repay

• Client’s credibility

• Probability of Default

• Prepayment Models

• Debt Service Ratio

• Net Disposable Income

• Payment to Income Ratio

Internal data

base:• Scoring

cards Application score

• Automated underwriting

• Automated credibility assessment

External data

base: • Credit

Information Bureau

• Tax office

11

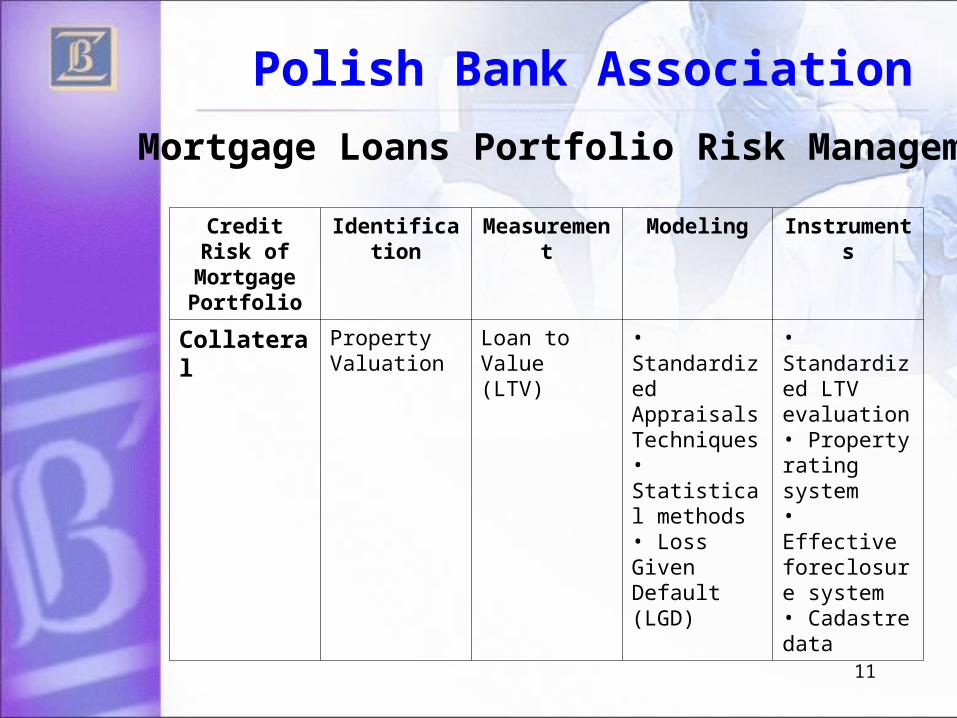

Polish Bank Association

Mortgage Loans Portfolio Risk Management

Credit Risk of

MortgagePortfolio

Identification

Measurement

Modeling Instruments

Collateral

Property Valuation

Loan to Value (LTV)

• Standardized Appraisals Techniques• Statistical methods• Loss Given Default (LGD)

• Standardized LTV evaluation• Property rating system• Effective foreclosure system• Cadastre data

12

Polish Bank Association

Mortgage Loans Portfolio Risk ManagementCredit Risk of

MortgagePortfolio

Identification

Measurement

Modeling Instruments

Enhancement

Elementary risk table:Credit Application BorrowerCredit targetCredit collateral

Borrower’s credibilityCurrent and future creditworthinessCredit purposePossibility of recovering the invested capital in the event of foreclosureFormal and legal conditions of the transaction and framework.

Scoring bank’s proceduresScoring bank’s monitoring system

Mortgage gap insuranceUnemployment insuranceMortgage guarantee insuranceLife insurance

13

Polish Bank Association

Mortgage Loans Portfolio Risk Management

Credit Risk of

MortgagePortfolio

Identification

Measurement

Modeling Instruments

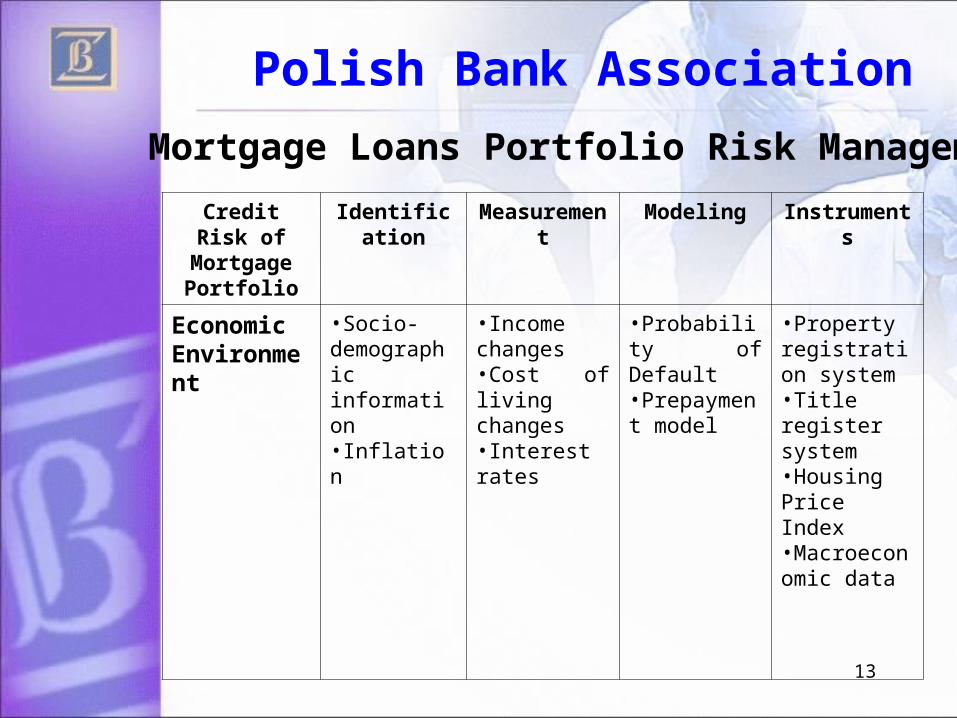

Economic Environment

•Socio-demographic information•Inflation

•Income changes •Cost of living changes•Interest rates

•Probability of Default•Prepayment model

•Property registration system•Title register system•Housing Price Index•Macroeconomic data

14

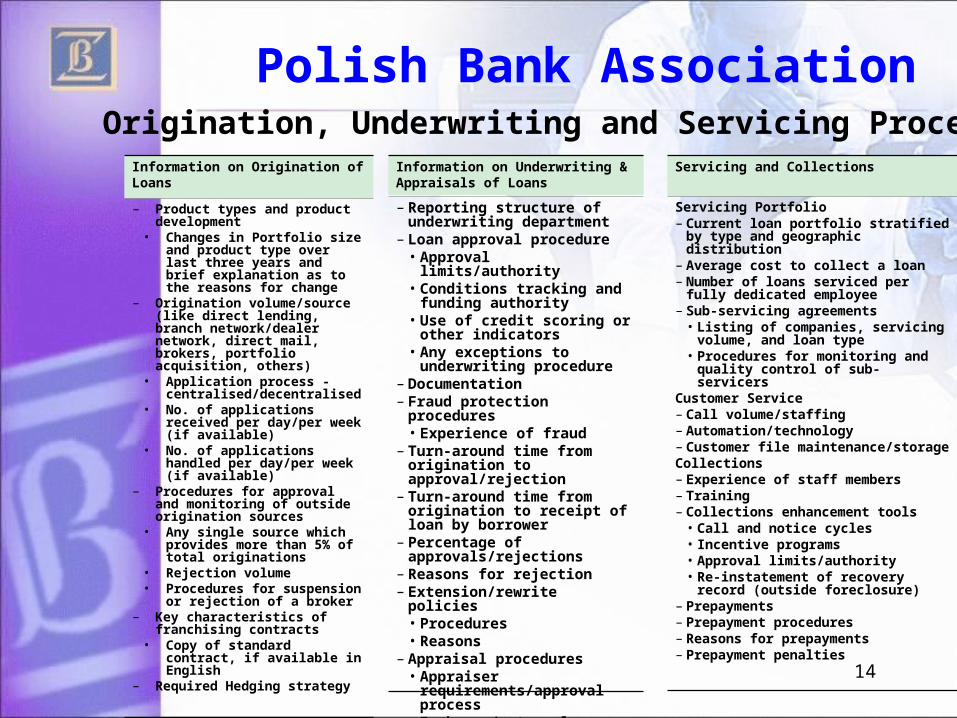

Polish Bank Association

Information on Origination of Loans

– Product types and product development

• Changes in Portfolio size and product type over last three years and brief explanation as to the reasons for change

– Origination volume/source (like direct lending, branch network/dealer network, direct mail, brokers, portfolio acquisition, others)

• Application process - centralised/decentralised

• No. of applications received per day/per week (if available)

• No. of applications handled per day/per week (if available)

– Procedures for approval and monitoring of outside origination sources

• Any single source which provides more than 5% of total originations

• Rejection volume• Procedures for

suspension or rejection of a broker

– Key characteristics of franchising contracts

• Copy of standard contract, if available in English

– Required Hedging strategy

Information on Underwriting & Appraisals of Loans

– Reporting structure of underwriting department

– Loan approval procedure • Approval limits/authority• Conditions tracking and

funding authority• Use of credit scoring or

other indicators • Any exceptions to

underwriting procedure– Documentation– Fraud protection

procedures• Experience of fraud

– Turn-around time from origination to approval/rejection

– Turn-around time from origination to receipt of loan by borrower

– Percentage of approvals/rejections

– Reasons for rejection– Extension/rewrite policies

• Procedures• Reasons

– Appraisal procedures• Appraiser

requirements/approval process

• In-house/external• Training/qualifications• Monitoring and quality

control

Servicing and Collections

Servicing Portfolio– Current loan portfolio stratified

by type and geographic distribution

– Average cost to collect a loan– Number of loans serviced per

fully dedicated employee– Sub-servicing agreements

• Listing of companies, servicing volume, and loan type

• Procedures for monitoring and quality control of sub-servicers

Customer Service– Call volume/staffing– Automation/technology– Customer file

maintenance/storageCollections– Experience of staff members– Training– Collections enhancement tools

• Call and notice cycles• Incentive programs• Approval limits/authority• Re-instatement of recovery

record (outside foreclosure)– Prepayments– Prepayment procedures– Reasons for prepayments– Prepayment penalties

Origination, Underwriting and Servicing Procedures

15

Polish Bank Association

Data Fields Requested by Rating AgenciesPortfolio Data

– Portfolio Cut Off Date•Information on the Borrower and Property– Borrower Name– Borrower Identification Number– Borrower Legal Form and Employment

Type– Property Region and Address– Property Type/Description– Owner Occupancy– Net Rental and Total Income of Borrower– Rating (internal and external) of Debtor– Details of Court Judgments•Information on the Loan– Origination and Drawing Date– Loan Purpose – Currency – Loan Amount Requested– Original Loan Size– Current Loan Balance– Existing Charge Balance– Limit loan amount (for undrawn amounts) – Subsidised flag (yes/no, if yes subsidised

amount and entity) – Legal Final Maturity– Weighted Average Life– Original Terms (months)– Remaining terms (months)– Payment Date, First Amortisation Date – Amortization Profile (bullet; amortisation

rate)

• Interest – Interest Rate Type (fixed/ floating /

mixed)– Current Interest Rate– Conversion Option (if any Conversion

Date and post Conversion interest rate)– Index Name/ Value– Marchgin– Interest Rate Cap/ Floor (if any)– Payment Date– Payment Frequency (Monthly/

Quarterly/ Semi-Annual / Other) – Interest Day Count– Interest Rate Reset Frequency • Security – Type of Security– Valuation of Security Amount – Valuation of Security Date– Lien Position/ Lien Value (for Mortgage

Loan)– Other Guarantees on Loans/ Insurance• Performance Status– Arrears Balance, Total Arrears– Bankruptcy– Current Principal Due, Current Interest

Due– Number of days/periods the loan is in

arrears– Arrears Multiple– Amount of arrears repaid without

losses– Arrears gone into possession

Rating Agency Portfolio Data Requirements

16

Legal framework requirements • 20 July 2000, General Inspectorate of

Banking Supervision - Recommendation J - creation by banks database about real estate market

• 10 December 2001 (amended on 10 of December 2003) Minister of Finance Ordinance about principles of creating reserves on risk with activity of bank

• New Capital Accord – Basel II• March 2006 - Recommendation S • 2006 - Banking Supervision Committee’s

Resolution on loans currency exposure - draft

Polish Bank Association

17

Realities in banking sector

• Fragmentary databases

• Differentiated range of information

• Traditional form

Polish Bank Association

18

Purposes of System AMRON• Implementation by banks of

supervisory regulations’ requirements ,

• Effective management risk,

• Depending on current market rate value estate prediction

• Rationalization of bank activity cost,

• Cutting costs incurred by clients.

Polish Bank Association

19

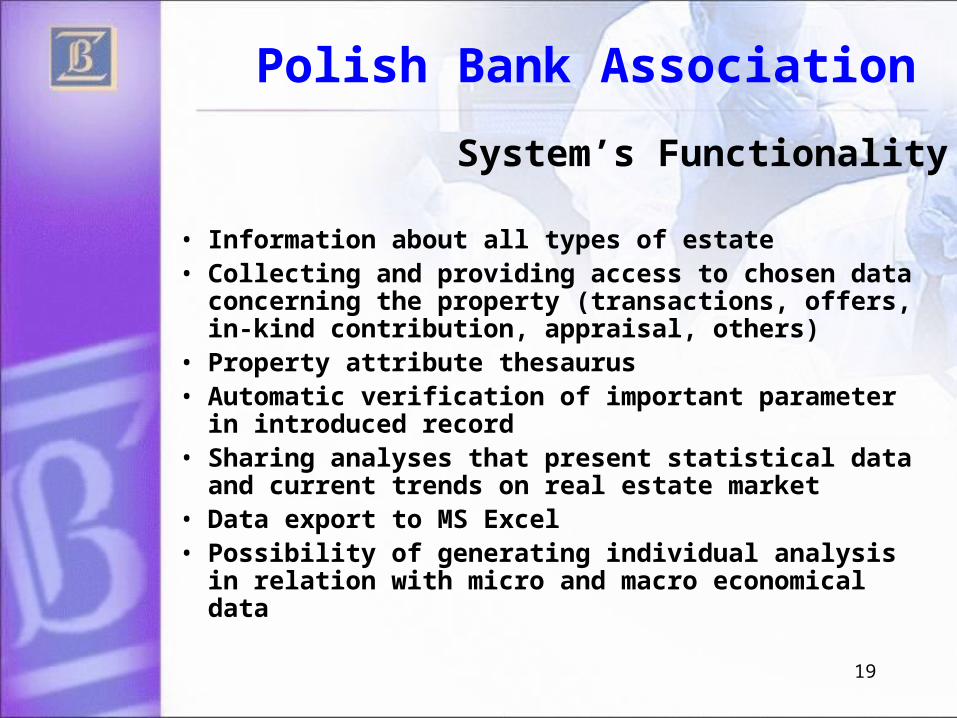

System’s Functionality

• Information about all types of estate• Collecting and providing access to chosen data

concerning the property (transactions, offers, in-kind contribution, appraisal, others)

• Property attribute thesaurus• Automatic verification of important parameter

in introduced record • Sharing analyses that present statistical data

and current trends on real estate market• Data export to MS Excel• Possibility of generating individual analysis in

relation with micro and macro economical data

Polish Bank Association

20

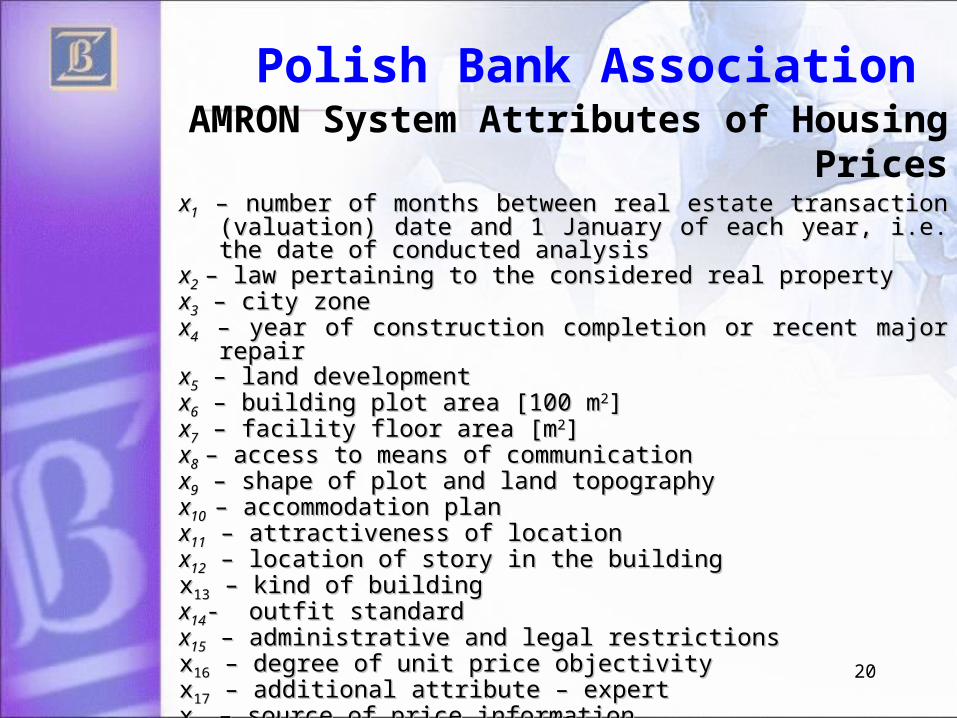

AMRON System Attributes of Housing Prices

xx11 – number of months between real estate transaction – number of months between real estate transaction (valuation) date and 1 January of each year, i.e. the date of (valuation) date and 1 January of each year, i.e. the date of conducted analysisconducted analysis

xx22 – law pertaining to the considered real property– law pertaining to the considered real propertyxx33 – city zone – city zonexx44 – year of construction completion or recent major repair – year of construction completion or recent major repairxx55 – land development – land developmentxx66 – building plot area [100 m – building plot area [100 m22]]xx77 – facility floor area [m – facility floor area [m22]]xx88 – access to means of communication– access to means of communicationxx99 – shape of plot and land topography – shape of plot and land topographyxx1010 – accommodation plan– accommodation planxx1111 – attractiveness of location – attractiveness of location xx1212 – location of story in the building – location of story in the buildingxx1313 – kind of building – kind of buildingxx1414- outfit standard- outfit standardxx1515 – administrative and legal restrictions – administrative and legal restrictionsxx1616 – degree of unit price objectivity – degree of unit price objectivityxx1717 – additional attribute – expert – additional attribute – expertxx18 18 – source of price information– source of price informationc c – real estate unit price [zł/m– real estate unit price [zł/m22]]d d – rent for accommodation area unit [zł/m– rent for accommodation area unit [zł/m22 x year] x year]

Polish Bank Association

21

Analyses and monitoring• Models of scaling of ratios of risks,

– In free transactions of sales – In free transactions of sales in

different intervals of times – In foreclosure procedures – In future transactions of sales – On base of offered property prices

• Property value prediction models,• Discount rate calculation models

Polish Bank Association

22

Examples of types of reports

• Report A - general, descriptive (property type, area, transaction price etc., presented in the territorial aspect)

• Report B - detailed, describing a particular property (full data on property gathered in the database)

• Report C - summary – cross-section of the given real estate market (region, type).

• Report D – presenting trends on the real estate market (generated periodically).

Polish Bank Association

23

How system is taken advantage?

250 000 PLN

How much this property is worth ?

200 000 PLN

Lack of

payments Risk management

Value of estate in foreclosure procedures

Monitoring the collateral’s (property)

value during the crediting term.

Polish Bank Association

24

Benefits of AMRON• Access to all data on estate market• Increasing risk management in real estate

financing market including limiting risk associated with undervalued collateral.

• Possibility for a trustworthy verification of property appraisals through comparison of external appraisals with data from system.

• Shortening the time of credit decision – fast verification of property value will decrease the time the client waits for the banks decision.

• Limiting the possibility of a unfair and negligent valuation of property that might cause an undercolleralization of the loan value.

• Possibility of monitoring the collateral’s (property) value during the whole crediting period.

Polish Bank Association

25

Benefits of AMRON• Wider access to data gathered by particular

participants of the system, giving a better picture of the real estate market.

• Possibility of predicting demand for mortgage loans from the territorial perspective.

• Creating analyses with statistics and current trends on the real estate market.

• Facilitating and developing the mortgage baked liabilities transfer.

• Granting loans with high LTV values.• Improving data concerning the propertied

legal status.• Decreasing costs resulting from the creation

of a private database.• Decreasing costs of credit (Valuator 100$ /

statistical methods – 20$)

Polish Bank Association

26

AMRON System Development Plans

• Invitation for cooperation to insurance companies

• Creation interface between credit information, and information about client

• Monitoring of estate market and observation of business cycle.

• Cooperation with National Bank of Poland on market analysis creation

• House Pricing Index

Polish Bank Association

27

Boleslaw Meluch

Expert

Real Estate Finance Committee

8 Kruczkowskiego Str., 00-380

Warszawa

+48-22-48-68-137

European Property InstituteEuropean Property Institute

Vice PresidentVice President

mobile 506-108-364mobile 506-108-364

Polish Bank Association