1 lovely professional university lecture 2. global business – global finance and tax planning...

TRANSCRIPT

1

Lovely Professional UniversityLecture 2.

Global Business – Global Finance

and Tax PlanningHoward Godfrey, Ph.D., CPA

Professor of AccountingCopyright © 2010

Profile of Multinational Businesses

Subject to U.S. Tax Law – Part I. Inbound InvestmentsBy Howard Godfrey and Casper Wiggins

Investing in CharlotteNote: some foreign investors simply buy stock in U.S. corporations or invest in mutual funds. We are not considering those types of investments in this presentation. We focus on a more direct ownership of business operations.

3

Investing in CharlotteA corporation or an individual investor in India wants to invest in the United States and take advantage of the expected recovery from the recession.

What are some alternative ways to invest?

Which these would be appropriate for the new business mentioned in the first presentation: India-in-Charlotte?

4

Foreign investors expand into the U.S. with inbound investments. Inbound investments include:1. buying or organizing U.S. subsidiary corporations, 2. operating U.S. branches, 3. investing in partnerships that have U.S. business operations, 4. investing in U.S. real estate.

Investing in Charlotte

Each of the four types of investments on the preceding slide has its own set of tax issues.

6

U.S. investors may also choose to expand business operations in foreign countries with outbound investments that follow the same patterns.

This paper (Part I) focuses on multinational businesses with inbound investments, i.e., foreign investors with business operations in the U.S.

Over 60,000 U.S. corporations are foreign controlled.

Foreign investors also have about 15,000 U.S. branches in the United States, and

about 7,000 foreign partnerships report U.S. source income on annual U.S. partnership tax returns.

Foreign investors' equity interest in (and loans to) U.S. affiliates grew at the rate of 14% to $2 trillion in 2007.

On the outbound side, about 11,000 U.S. corporations have over 75,000 foreign subsidiaries with assets of about $10 trillion and net income of about $400 billion. Individuals reported foreign income on 7.6 million individual tax returns for 2006

and claimed foreign tax credits of $11 billion for foreign income taxes paid on foreign source income.

U.S. owned equity in (and loans to) foreign affiliates reached $2.8 trillion at the end of 2007, an increase of 14% over 2006.

Note for the next slide A U.S. Corporation opens a branch in India.

The Corporation has net income in India of $100,000.

Assume India has a 30% income tax rate and the company pays Indian income tax of $30,000.

Assume the U.S. has a 40% income tax rate and the company pays U.S. income tax of $40,000.

Is the global tax burden equal to $70,000?

Incomein India U.S. India Total Taxby U.S. business $100,000 $100,000Tax Rates 40% 30%Gross US. Tax $40,000 $40,000Gross India Tax $30,000 $30,000Gross Tax $70,000

U.S. Gross TaxCredit for India TaxNet U.S. Tax

How Tax Credits Work

Incomein India U.S. India Total Taxby U.S. business $100,000 $100,000Tax Rates 40% 30%Gross US. Tax $40,000 $40,000Gross India Tax $30,000 $30,000Gross Tax $70,000

U.S. Gross Tax $40,000Credit for India Tax ($30,000)Net U.S. Tax $10,000

How Tax Credits Work

In 2007, foreign persons invested $277 billion to acquire interests in U.S. businesses or to start new businesses here.

Most of this investment (92%) was for the acquisition of existing U.S. firms.

U.S. corporations that have foreign owners are termed foreign-controlled domestic corporations (FCDC’s).

They (FCDCs) have essentially the same requirements for filing corporate income tax returns and paying taxes as other domestic corporations.

Investing in CharlotteWhat is the income tax filing and payment procedure for India-in-Charlotte, Inc.?(covered in preceding lecture)

14

Number and Importance of FCDCs

For tax years ending between July, 2005 and June 2006, 61,820 corporate income tax returns were filed by U.S. corporations that were foreign controlled. These FCDCs had total receipts of $3.5 trillion and assets of $9.2 trillion.

They paid U.S. income tax of $42.4 billion. Almost 10% (5,736) were consolidated returns. This indicates that the number of U.S. corps under control of foreign persons is substantially larger than 61,820.

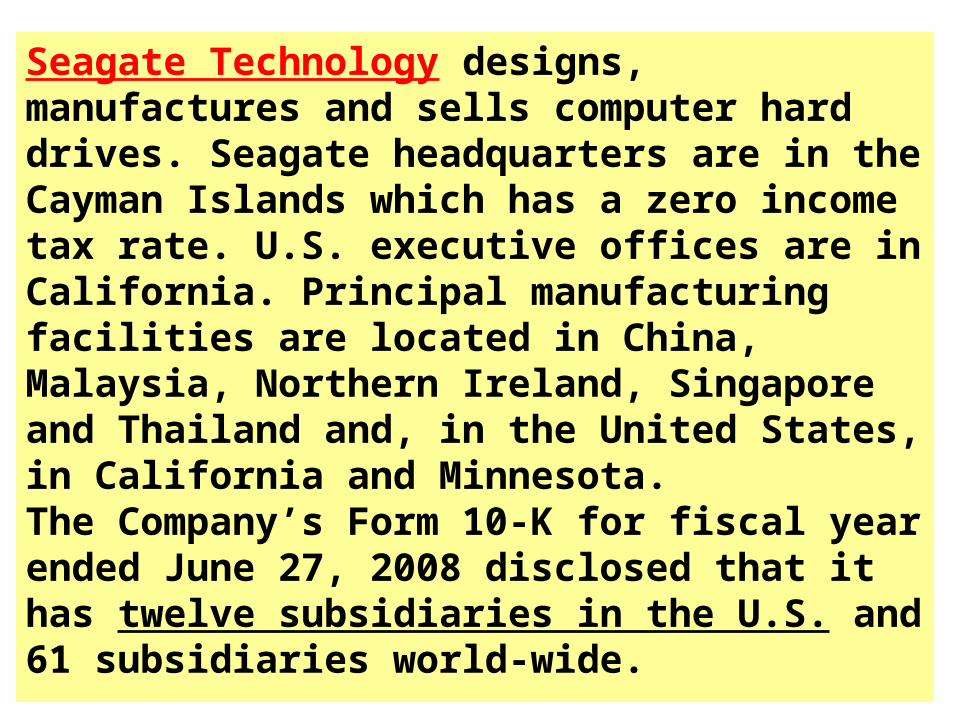

Seagate Technology designs, manufactures and sells computer hard drives. Seagate headquarters are in the Cayman Islands which has a zero income tax rate. U.S. executive offices are in California. Principal manufacturing facilities are located in China, Malaysia, Northern Ireland, Singapore and Thailand and, in the United States, in California and Minnesota. The Company’s Form 10-K for fiscal year ended June 27, 2008 disclosed that it has twelve subsidiaries in the U.S. and 61 subsidiaries world-wide.

Seagate Technology

How is Seagate

Saving Income Tax

by not being a

U.S. Corporation?

Seventy percent of FCDC receipts were reported by FCDCs with parents in five countries. Twenty percent of all receipts of FCDCs were reported by UK owned subs in the U.S., followed by Japan (16%), Germany (12%), Netherlands (12%), and Canada (8.7%).

Although Canada and Mexico are major trading partners with the U.S., there are fewer U.S. subsidiaries with parents in those countries.

Profitability of FCDCs FCDCs are less profitable than their non-foreign controlled competitors in the U.S. Manufacturing FCDCs reported gross profit of 21.5% of gross receipts, while large non-foreign controlled manufacturers reported average gross profit rates of 27.5%, a 6% difference. FCDCs in wholesale and retail sales had gross profit rates of 19.3% (23% for their non-foreign controlled counterparts). Gross profit is business receipts less cost of sales.

Role of Intercompany Transactions-1

The global income tax burden of a parent and subsidiary corporation can be managed when one entity is in a high tax (i.e. income tax) country and the other entity is in a low tax country.

Role of Intercompany Transactions-2

A parent corp. (in a low tax country) may increase the price it charges the subsidiary (in a high tax country) for inventory. This decreases the amount of income reported in the high tax country such as the U.S., and increases the amount of income reported in the low tax country. Global tax liability is reduced by a change in the intercompany pricing policy.

India-in-CharlottePlease take a look at the financial information handed out for India-in-Charlotte.

What transfer pricing issues may be present for this company?

22

Case-2006-IRS settlement with GSK over transfer pricing issues for tax years 1989-2005. GSK agreed to pay a record amount of $3.4 billion to the IRS. The IRS position was that GSK understated its U.S. profits. Transfer pricing issues related to trademarks & other intangibles developed by company’s U.K. parent, and the value of GSK’s marketing and other contributions in the U.S. IRS stated, “Transfer pricing that allocates an appropriate return to the U.S. affiliates of multinational groups is a key focus for the IRS.”

Purpose of Form 5472.

Congress was concerned about the potential for using intercompany transactions to shift taxable income to other countries.

For this reason, Section 6038A was added to the Code, which requires extensive record keeping and reporting of information about inter company transactions with foreign related parties.

Form 5472 is used for reporting of intercompany sales & purchases of inventory and other assets, intercompany rent payments, insurance premiums, commissions, loans, interest payments, etc.

Form 5472 must be filed by a “reporting corporation” which is a domestic corporation and is at any time during the year a 25-percent foreign-owned entity. The reporting corporation provides information about inter company transactions with a 25-percent foreign owner and other parties that are related.

Case. Foreign Partnership (FP) owns 100 percent of U.S. Corp (USC), and 25 percent of Foreign Corp (FC). The remaining 75 percent of FC is publicly owned by many small shareholders. Sales transactions occur between USC and FC. USC is a reporting corporation. USC and FC are each controlled by FP under section 482 and the related regulations.

Therefore, FC is related to USC within the meaning of section 482 and is a related party to USC. Sales transactions between USC and FC are subject to section 6038A.

Importance of Form 5472. A reporting corp. is required to file Form 5472 with its income tax return for the taxable year by the due date (including extensions) of that return.

If a reporting corp fails to file the Form 5472 within the prescribed deadline, the reporting corp may be assessed a monetary penalty of $10,000 for each taxable year for which such failure occurs.

29

Transactions of Large FCDCs with Related Foreign Persons. In 2004, transactions (other than loans) between large foreign owned domestic corps and related foreign parties reached $1 trillion. Large FCDCs filed 774 corp income tax returns, with large corp being defined as those with total receipts of $500 million or more. These large corps account for about 75% of all assets and all receipts of the entire population of FCDCs. FCDCs file about 16,600 forms (Form 5472) with their income tax returns.

30

Sales and purchases of inventory accounted for 86% of the non-loan intercompany transactions. Large FCDCs paid $608 billion to foreign related parties for inventory and received $371 billion for sales of inventory to those parties. Large corps owed foreign related parties a total of $307 billion at the end of 2004, and paid interest of $26 billion to foreign related parties.

31

Information on Form 5472 provides the IRS with a basis for challenging intercompany pricing for sales of inventory, interest rates charged, fees paid for managerial services, royalties for use of intellectual property, etc.

32

Withholding on Dividends & InterestU.S. individuals or businesses making payments of U.S.-source income to foreign persons withhold taxes on this income (except where there is an exemption created by statute or treaty), or to appoint a withholding agent to manage the process. Financial institutions often serve as withholding agents. Interest and dividends are two important types of such payments. Foreign corporations receive most of the payments of U.S source income.

33

Withholding on Dividends & Interest

Amount of income paid to each recipient is reported on Form 1042S. A payer is liable for all withholding taxes owed on such payments. The standard income tax withholding rate is 30%, but the withholding rate on certain types of income may be reduced (possibly to a rate of zero) because of a treaty with the country of residence of the recipient.

34

Withholding on Dividends & Interest

Amount of Withholding on U.S. Source Income Paid to Foreigners. In 2006, 3.7 million withholding Forms 1042S were filed, reporting a total of $545 billion in payment of U.S. source income to foreign recipients. Taxes of $8.4 billion were withheld on payments of $69 billion which were subject to withholding. The balance of the $476 billion was not subject to withholding, typically because of provisions of tax treaties with applicable countries.

India-in-CharlottePlease take a look at the financial information handed out for India-in-Charlotte.

What withholding issues may be present for this company related to dividends paid to owner in India?

35

India-in-Charlotte-Continued

What is the impact of a treaty with India (on tax withholding)?

36

37

Case. Seagate Technology designs, manufactures, markets and sells computer hard drives. Seagate is a holding company in the Cayman Islands which has a zero income tax rate.

38

Case. Seagate Technology.

Form 10-K for the fiscal year ended June 27, 2008 disclosed that dividend distributions received from the Company’s U.S. subsidiaries may be subject to U.S. withholding taxes when, and if, distributed to the Cayman parent.

39

Case. Seagate Technology.

The Cayman Islands holding company would not incur U.S. federal income tax if it receives dividends from U.S. subsidiaries, and would incur no Cayman Islands income tax on such dividends.

40

Case. Morgan Pacific Corp. was formed as an Oregon (U.S.) corp. Both Morgan Pacific Corp. and Mid-Coast Finance (a Netherland Antilles corp.) were controlled by Jay Holdings, a Jersey, Channel Islands corporation. Morgan Pacific made an interest payment of $455,000 on its debt of $4,550,000 to Mid-Coast.

41

Case. Morgan Pacific Corp.

Morgan Pacific did not withhold income tax on the interest payment because a U.S. treaty with Netherlands Antilles provided that no U.S. income tax would be withheld on payments of interest to residents of that country.

42

Branch Return on Form 1120-FA foreign corporation may choose operate as a U.S. branch rather than to buy or organize a domestic corporation when expanding into the United States. If a foreign corporation operates a business through a branch in the U.S., the foreign corporation is subject to U.S. tax on income “effectively connected” with the conduct of a U.S. trade or business in a manner similar to that used to tax domestic corporations.

43

Branch Return on Form 1120-FForm 1120-F is a U.S. income tax return filed by foreign corporations that: (1) engage in a trade or business in the U.S., (2) have income, gains or losses that are treated as being effectively connected with a U.S. business, or (3) have U.S. source income and the liability for U.S. tax on that income has not been satisfied through a withholding tax.

44

Branch Return on Form 1120-F.

A domestic corporation is organized in the United States.

A branch is not incorporated in the United States, although the company may be incorporated in a foreign country.

ReviewWhich of the charlotte area businesses (with ownership in India) is a branch?

45

46

Number and Importance of Branch Returns

In 2006, 14,897 foreign corps filed Forms 1120-F. They paid U.S. income tax of $3.2 billion on income effectively connected with the U.S., and about $141 million on other income such as interest income received from the U.S.

47

Number and Importance of Branch Returns

They paid branch profits tax of about $83 million. This is the counterpart of the withholding tax on dividends paid by U.S. subsidiaries to their foreign parent corps or other foreign persons. Branch profits tax rate is 30%, but may be reduced by treaty, possibly to zero.

48

File Form 1120-F on Time

A foreign corporation that fails to file Form 1120-F on a timely basis loses the right to claim most deductions on the return. Reg. Sec. 1.882-4(a)(3)(ii)

49

Partnership Withholding Requirements

A domestic or foreign partnership is subject to withholding tax requirements when it:

(1) has taxable income from a U.S. business operation (called effectively connected taxable income or ECTI) and

(2) some of that income is allocated to a foreign partner.

50

Partnership Withholding Requirements

If the foreign partner is an individual, the withholding rate is the highest individual income rate. The highest corporate income tax rate applies to other types of partners. These withholding requirements do not apply to amounts allocated or paid to U.S. partners.

51

When foreign partner files a U.S. income tax return for the year and reports U.S income, a credit is allowed for the withholding tax. A foreign partner may file Form 8804-C to reduce the amount of required withholding (or possibly eliminate the withholding requirement), when the foreign partner's U.S. income tax liability will be less than the standard withholding amount.

52

Importance of Partnership Returns

A partnership return must be filed by a domestic partnerships and a foreign partnership that engages in a business in the U.S. or has income from sources in the U.S. The IRS receives about 3 million partnership returns each year covering about 16.7 million partners.

53

Importance of Partnership Returns

About 7,000 of those are foreign partnership returns covering 181,000 foreign partners. Corp. partners receive the largest amount of income allocations from partnerships, followed by individual partners, partners that are partnerships, etc.

ReviewWould the partnership form be applicable for India-in-Charlotte?Please Explain.

54

55

U.S. Partners of Foreign Partnerships

A U.S. person files Form 8865 with respect to foreign partnerships (when the U.S. person owns a controlling interest in the foreign partnership, contributes assets to the partnership, etc.) The form has various schedules, including a schedule K-1 which is used to report the U.S. person’s share of foreign partnership items of income, expense, etc.

56

Taxation of Income from Real EstateA nonresident alien or foreign corporation with rental income from property in the U.S. is subject to the flat 30-percent (or lower treaty) withholding tax rate if the rental activity is not effectively connected with the conduct of a trade or business within the United States. A foreign owner of rental real estate located in the U.S. is generally not considered to be in a U.S. trade or business. Taxing real estate rental income at a flat 30-percent rate without the allowance of allocable deductions can result in heavy tax burdens on this type of income.

57

Taxation of Income from Real Estate

Foreign owner with real estate income files Form 1040NR (for an individual) or 1120-F for a foreign corp, for income that is connected with the conduct of a trade or business. U.S. income tax on effectively connected income of a foreign corp. is computed using regular corporate income tax rates applied to net income, after deductions for expenses.

58

Taxation of Income from Real EstateA foreign owner of U.S. real estate may elect to treat real property income as if it were income effectively connected with a U.S. business. With this election, withholding is not required, but the owner is required to file a U.S. income tax return and report the rental income on the return. This enables the owner to claim deductions related to the real property income. However no deduction is available on a Form 1120-F, unless it is timely filed, which can be a trap for the unwary when an owner delays filing an election and a Form 1120-F in the belief that no tax is due because losses are realized.

59

Taxation of Income from Real Estate

Case. Rosas, a citizen and resident of Mexico, organized Swallows Holding, Ltd, in Barbados. Swallows owned 160 acres of unimproved real estate in California (U.S.). Swallows had a separate business activity in Barbados, but never engaged in a trade or business in the U.S. In a three-year period, Swallows reported gross income of $99,000 from rental and options, and expenses of $179,519, resulting in total losses of $80,518.

60

Taxation of Income from Real EstateCase. without an election to treat income from the real property as being effectively connected with the conduct of a U.S. business, gross rental revenue would have been subject to a withholding rate of 30%. The company did not make such election, but on its non-timely filed Forms 1120-F had information that the IRS accepted as the equivalent of an election. However, the IRS denied all deductions because the corporate returns were filed late, and assessed taxes of $14,850. After losing the case in Tax Court, the IRS prevailed at the appellate level.

Review

Suppose the owner of India-in-Charlotte buys a building in Charlotte to rent to businesses?Tax Factors?

61

62

Gains & Losses from Sale of Real Property

Gain or loss from a sale or other disposition of a U.S. real property interest is taken into account as if the seller (nonresident alien individual or foreign corporation) were engaged in a trade or business in the U.S. and as if the gain or loss were effectively connected with such trade or business.

The foreign owner must file a U.S. income tax return, reporting the gain on the sale.

A credit is allowed for the tax that was withheld on the disposal.

63

Gains & Losses from Sale of Real Property

A buyer (or other transferee) of a "U.S. real property interest" from a foreign person must withhold a tax equal to 10 percent of the amount paid to the foreign person. U.S. real property interest includes direct ownership of property, and may include an interest in a corporation that owns real estate. Assets held by partnerships, estates and trusts are treated as being held proportionately by partners or beneficiaries.

64

Gains & Losses from Sale of Real Property

There are several exceptions to this requirement, including an exemption for persons who purchase property for use as a residence for $300,000 or less. The transferor can apply for and receive a certificate from the IRS authorizing a reduced amount of withholding. This is appropriate where the income tax on the gain will be less than 10% of the selling price.

65

Income Paid to Foreign Owners

For 2005, rents and royalties were $21.5 billion, or 5.7 percent of total U.S. income paid to foreign recipients and reported on Form 1042S. Corp. recipients earned 92.8 percent of rents and royalties income paid to foreign recipients. About 75% went to residents of UK and Japan. This IRS report does not provide separate amounts for rental income and royalty income, but presumably the bulk of this amount is rental income.

Summary and Review

What are your thoughts about the impact of global taxes on global business?

66

Thanks for letting me meet with you.

Good Luck!67

68

The

End