1 legislative session february 17, 2006. 2 proposed legislative changes increase wpa bonding...

TRANSCRIPT

1

Legislative SessionFebruary 17, 2006

2

Proposed Legislative Changes

• Increase WPA bonding capacity from $1 billion to $3 billion

• Expand State Treasurer’s investment authority to invest in WPA bonds from funds other than just the Permanent Wyoming Mineral Trust Fund.

• Change name from “Wyoming Natural Gas Pipeline Authority” to the “Wyoming Pipeline Authority”.

• Constitutional amendment allowing Wyoming to invest in works of internal improvement associated with pipeline projects.

3

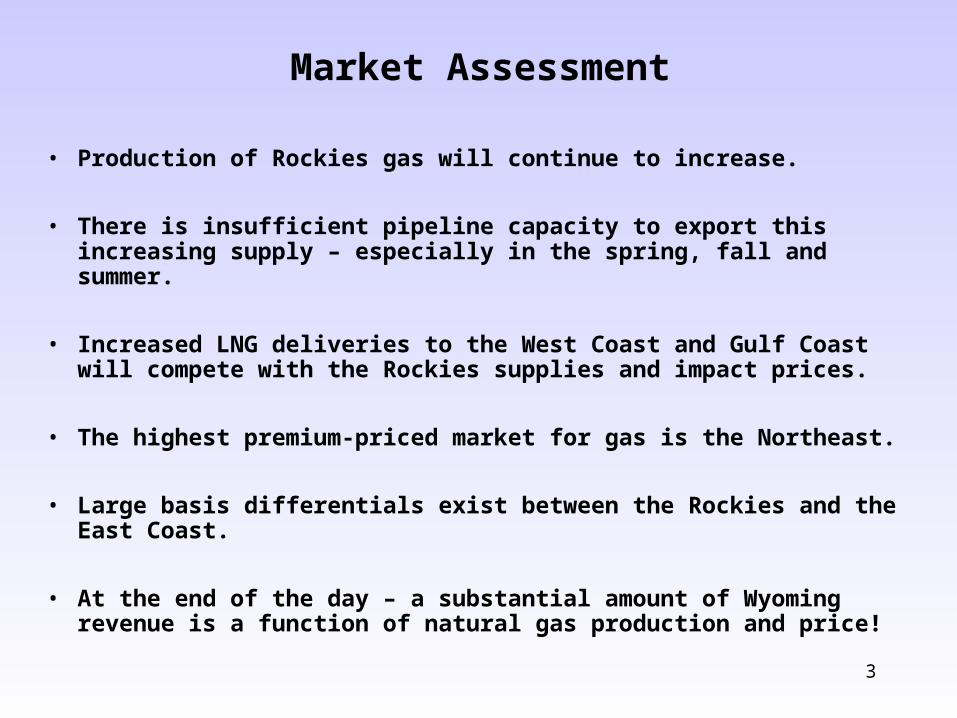

Market Assessment

• Production of Rockies gas will continue to increase.

• There is insufficient pipeline capacity to export this increasing supply – especially in the spring, fall and summer.

• Increased LNG deliveries to the West Coast and Gulf Coast will compete with the Rockies supplies and impact prices.

• The highest premium-priced market for gas is the Northeast.

• Large basis differentials exist between the Rockies and the East Coast.

• At the end of the day – a substantial amount of Wyoming revenue is a function of natural gas production and price!

4

Production

5

Production Will Increase From These Wyoming Areas

• Jonah/Pinedale Anticline – Record of Decision due on Jonah EIS Q1-06 which will allow for more than 3,000 additional wells.

• BP has proposed spending $2 billion in the Wamsutter/Echo Springs area to double capacity.

• 10’s of thousands of wells remain to be drilled in the Powder River Basin where production is once again increasing.

• Devon has proposed drilling over 1250 new wells in their Creston/Blue Gap Project area.

• Anadarko and Double Eagle awaiting Record of Decision on coal bed methane development in their Atlantic Rim project area.

• Anticipate renewed interest in developing or accelerating production from deep sour productive intervals knows to exist in SW Wyoming and the Madden area.

6

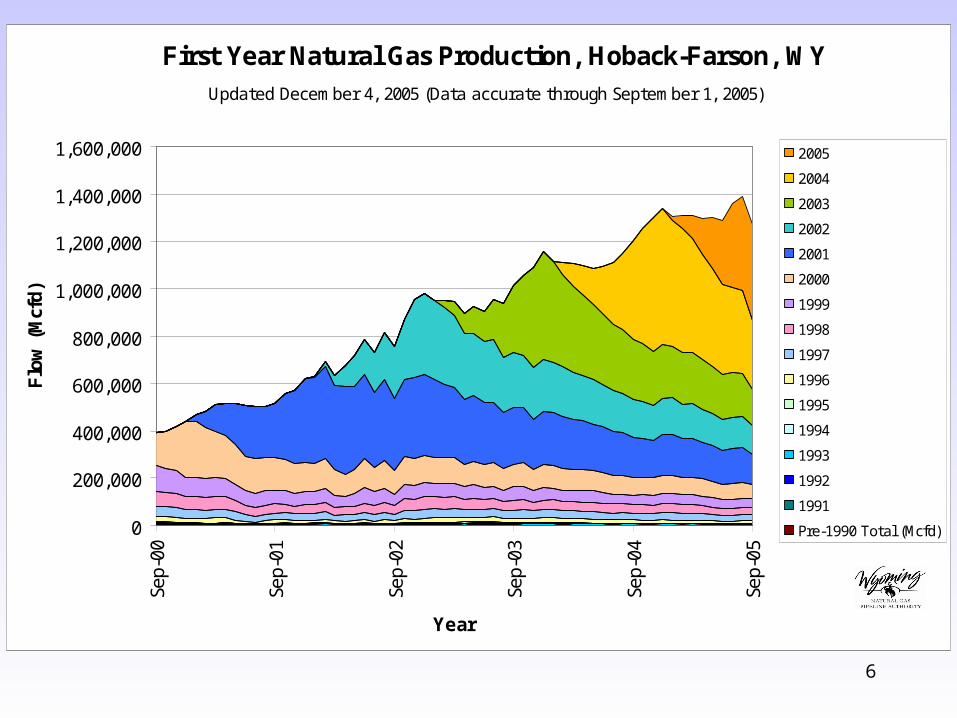

First Year Natural Gas Production, Hoback-Farson, WY

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000Se

p-00

Sep-

01

Sep-

02

Sep-

03

Sep-

04

Sep-

05

Year

Flo

w (M

cfd)

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

Pre-1990 Total (Mcfd)

Updated December 4, 2005 (Data accurate through September 1, 2005)

7

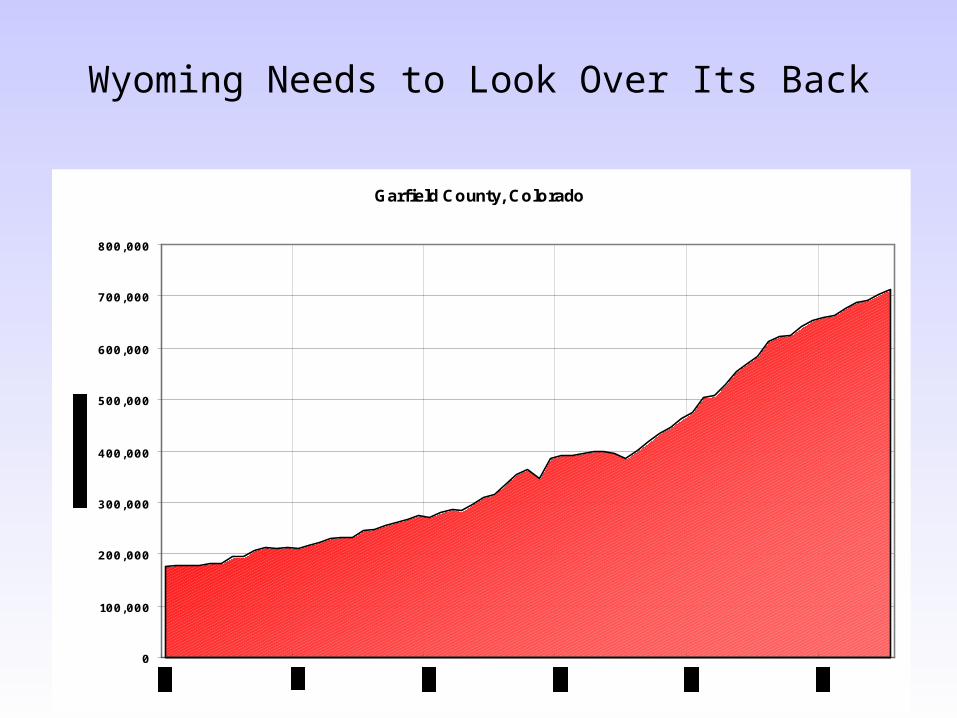

Garfield County, Colorado

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Wyoming Needs to Look Over Its Back

8

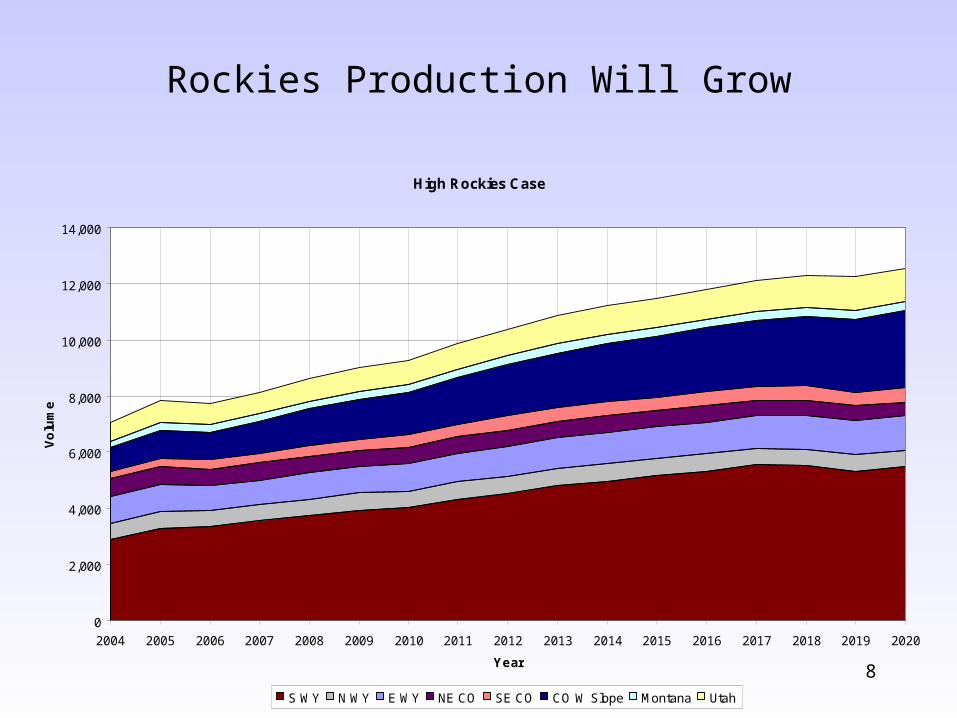

Rockies Production Will Grow

High Rockies Case

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Year

Vo

lum

e

S WY N WY E WY NE CO SE CO CO W Slope Montana Utah

9

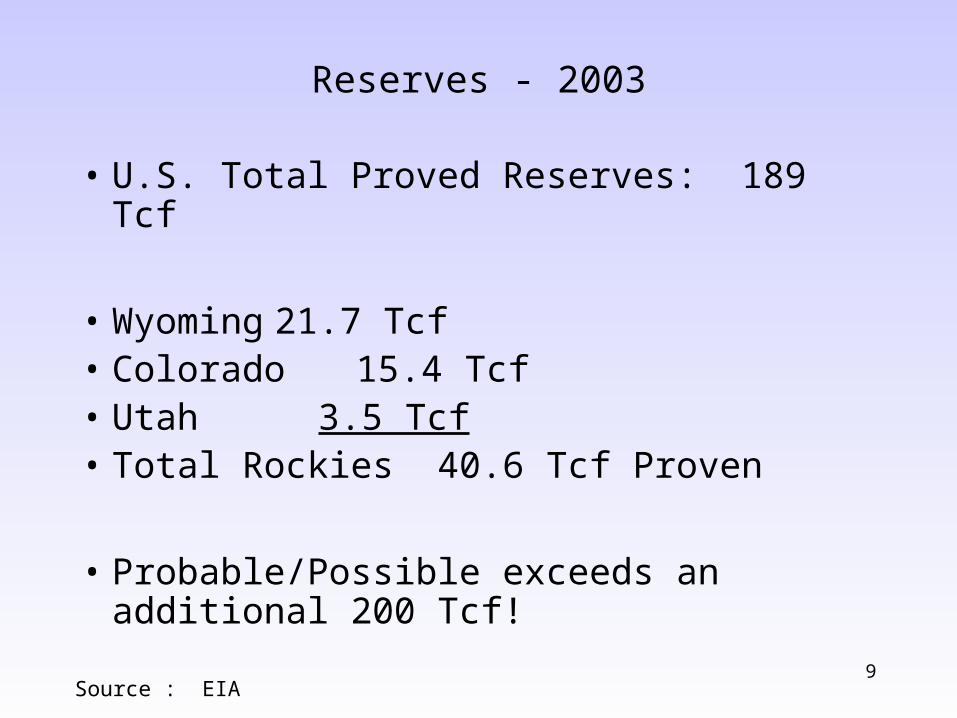

Reserves - 2003

• U.S. Total Proved Reserves: 189 Tcf

• Wyoming 21.7 Tcf• Colorado 15.4 Tcf• Utah 3.5 Tcf• Total Rockies 40.6 Tcf Proven

• Probable/Possible exceeds an additional 200 Tcf!

Source : EIA

10

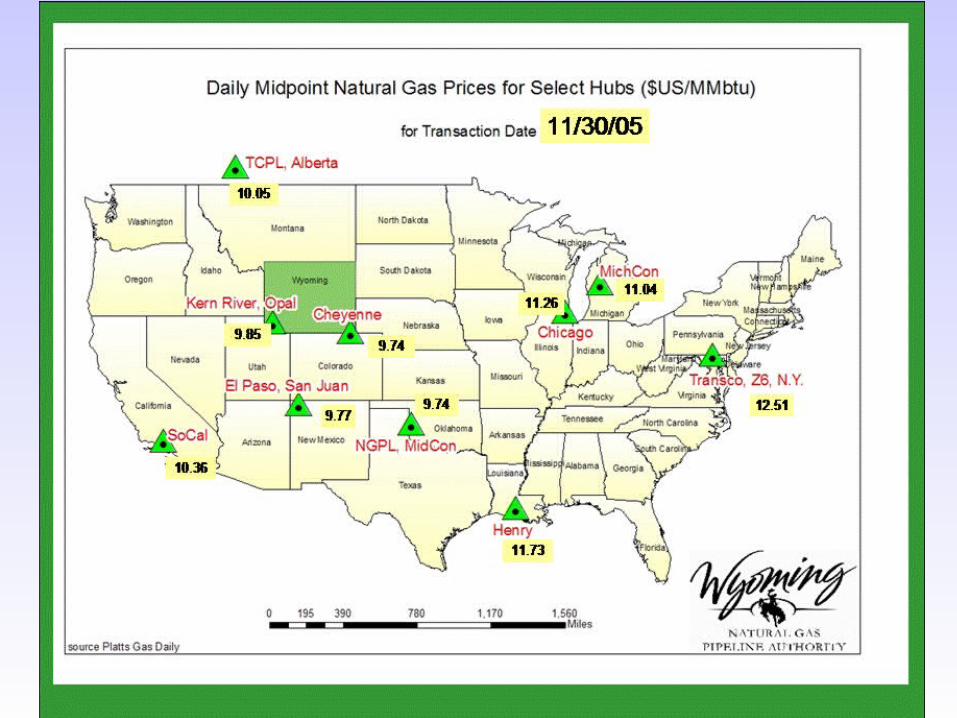

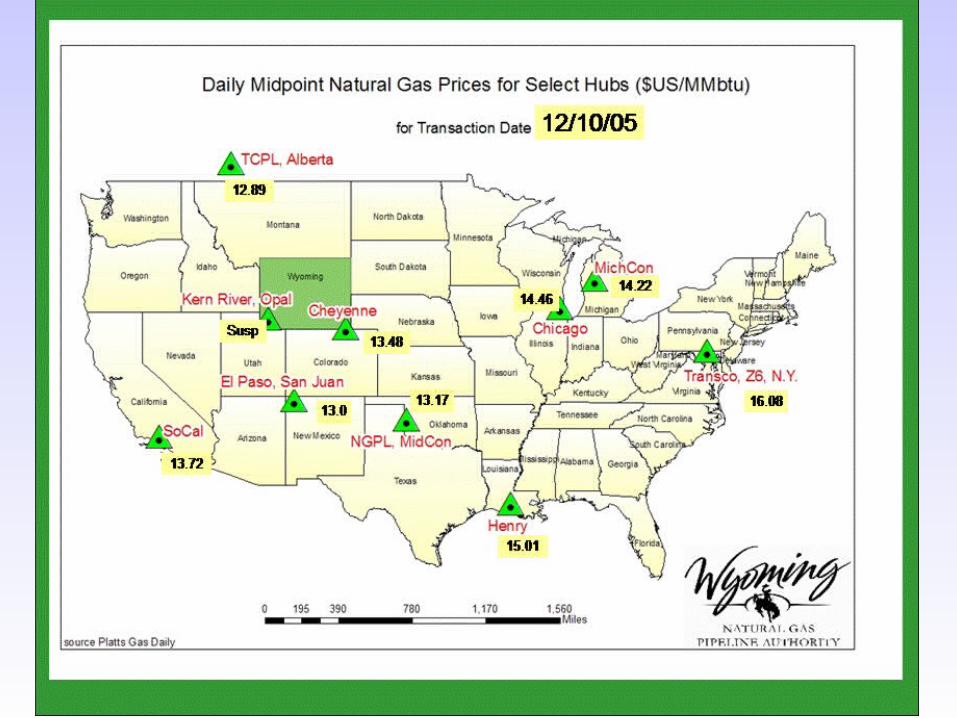

Pricing

11

12

13

14

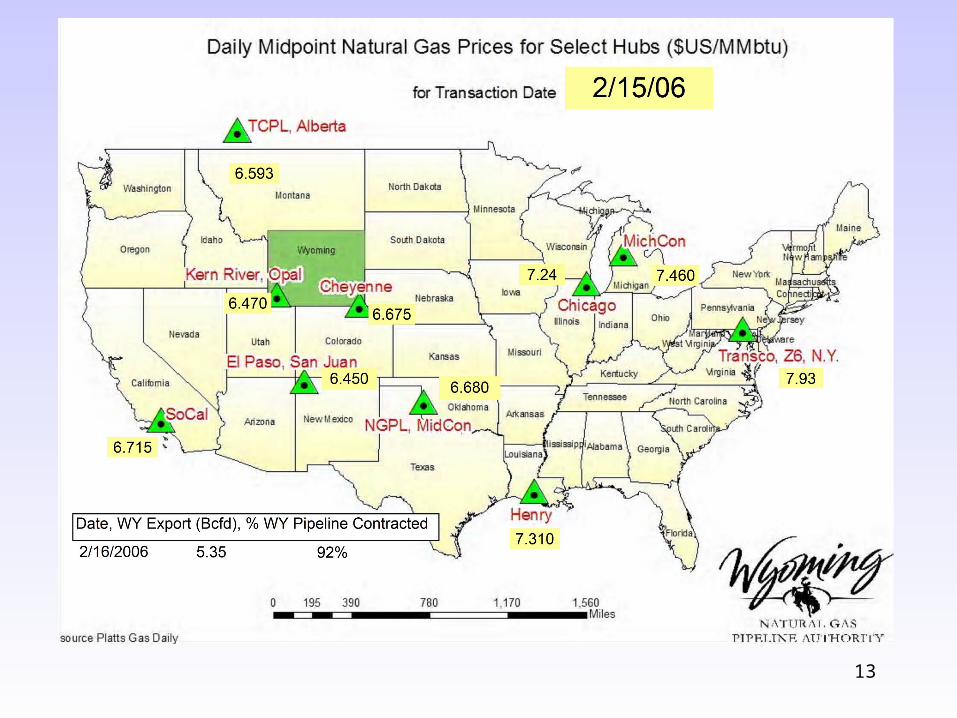

Basis Spreads Support New Pipeline

•Basis differential versus Henry Hub

•Source: Historical Prices – GasDat, Forward Prices – Sempra Commodities Oct 05 Curve

15

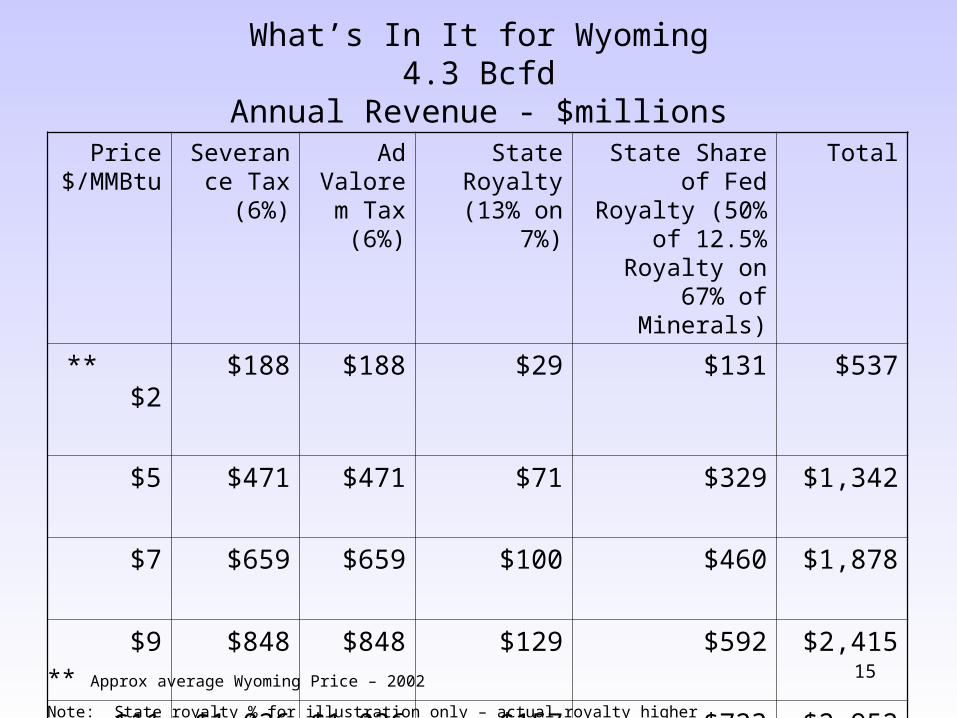

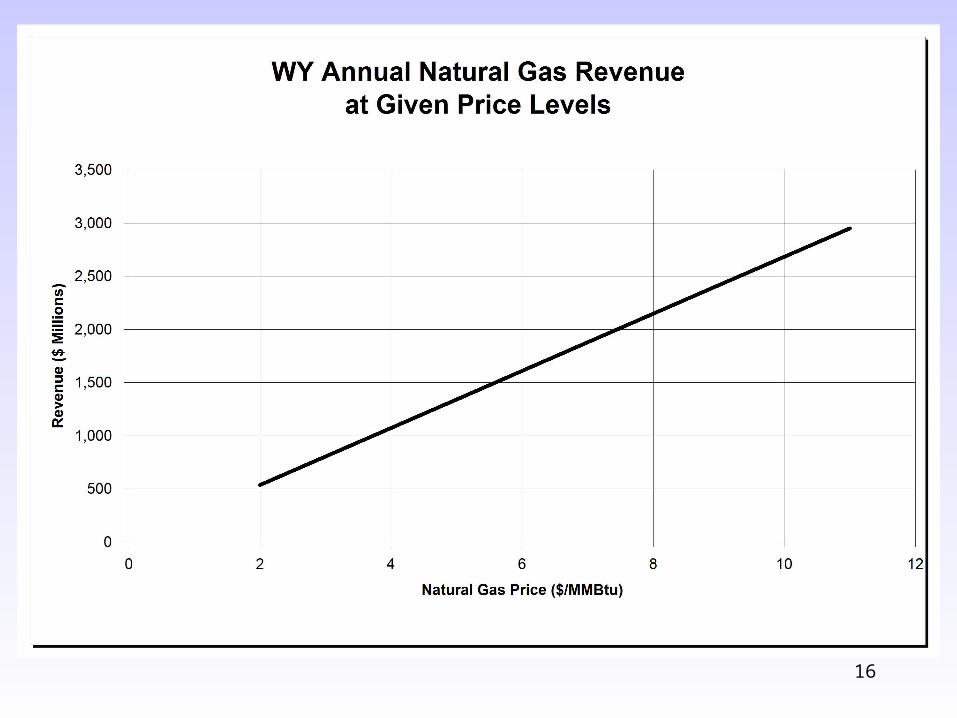

What’s In It for Wyoming4.3 Bcfd

Annual Revenue - $millionsPrice

$/MMBtuSeverance Tax (6%)

Ad Valorem

Tax (6%)

State Royalty (13% on 7%)

State Share of Fed Royalty (50% of

12.5% Royalty on 67% of Minerals)

Total

** $2 $188 $188 $29 $131 $537

$5 $471 $471 $71 $329 $1,342

$7 $659 $659 $100 $460 $1,878

$9 $848 $848 $129 $592 $2,415

$11 $1,036 $1,036 $157 $723 $2,952

** Approx average Wyoming Price – 2002

Note: State royalty % for illustration only – actual royalty higher

16

17

Making Sure Prices and Production Stay in Sync

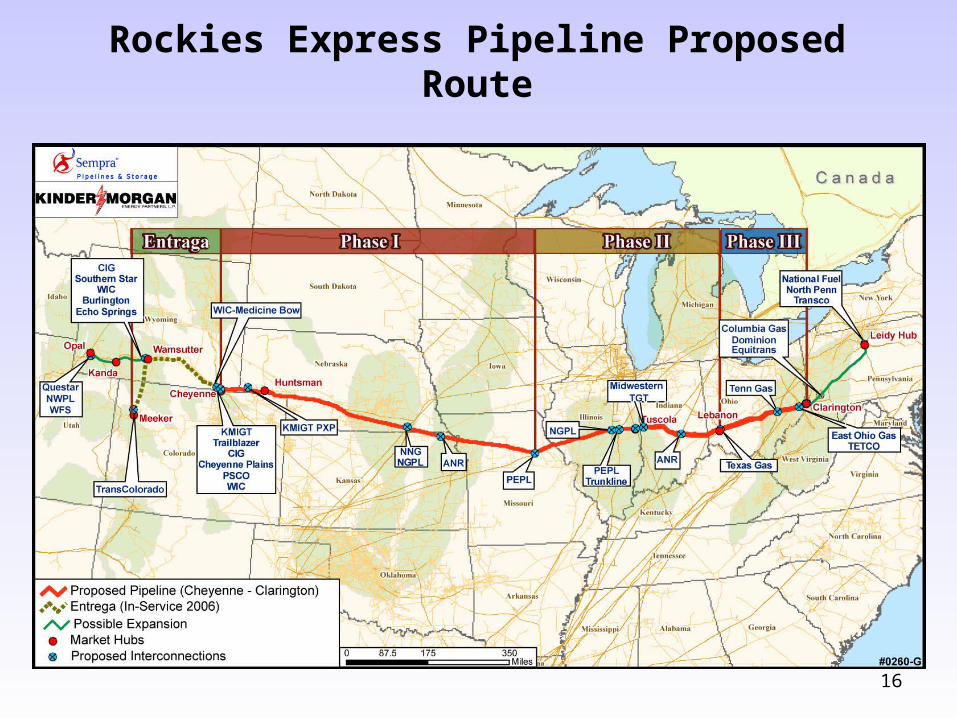

Rockies Express Pipeline Proposed Route

16

19

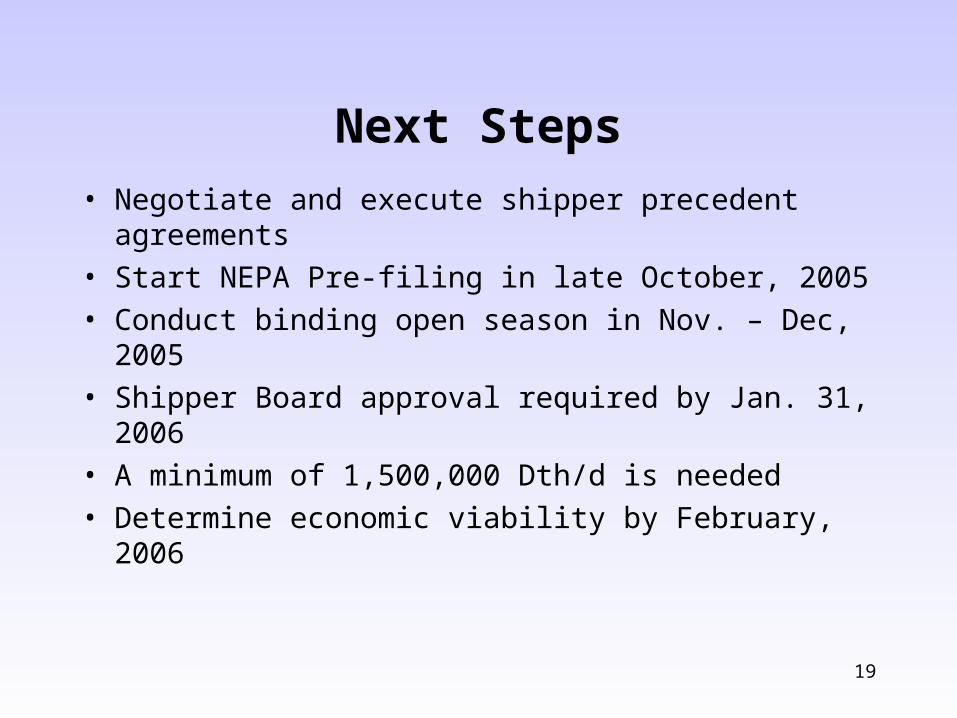

Next Steps

• Negotiate and execute shipper precedent agreements

• Start NEPA Pre-filing in late October, 2005• Conduct binding open season in Nov. – Dec, 2005• Shipper Board approval required by Jan. 31, 2006• A minimum of 1,500,000 Dth/d is needed• Determine economic viability by February, 2006

Which Brings Us Full Circle to……….

Proposed Legislative Changes

21

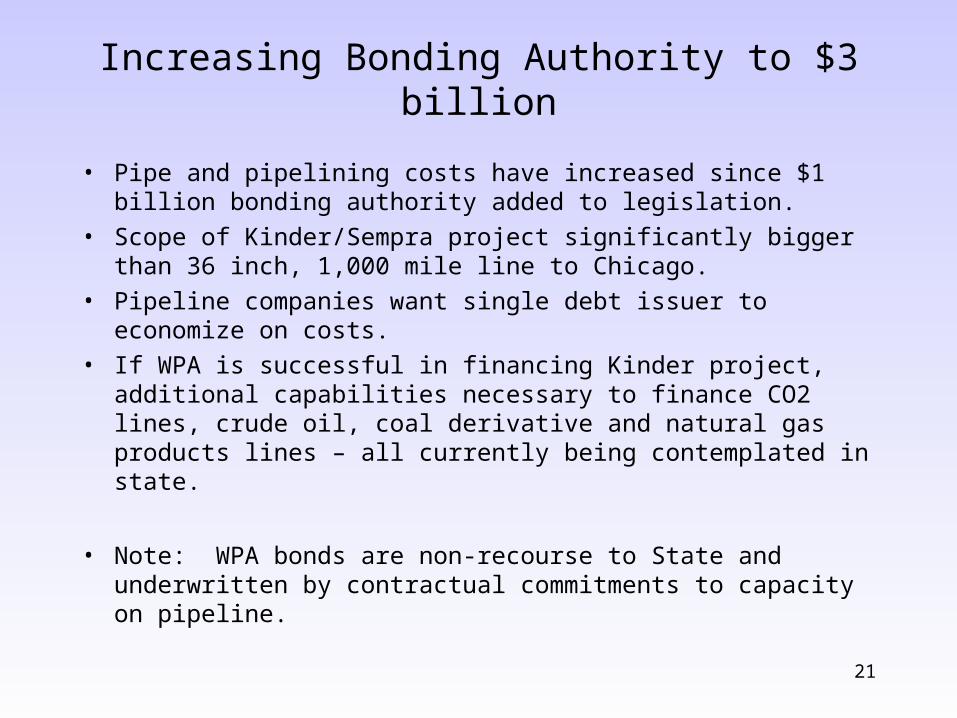

Increasing Bonding Authority to $3 billion

• Pipe and pipelining costs have increased since $1 billion bonding authority added to legislation.

• Scope of Kinder/Sempra project significantly bigger than 36 inch, 1,000 mile line to Chicago.

• Pipeline companies want single debt issuer to economize on costs.

• If WPA is successful in financing Kinder project, additional capabilities necessary to finance CO2 lines, crude oil, coal derivative and natural gas products lines – all currently being contemplated in state.

• Note: WPA bonds are non-recourse to State and underwritten by contractual commitments to capacity on pipeline.

22

Expand Treasurers Investment Authority

• Treasurer has requested.

• Allows for diversity across portfolio of funds managed.

• Increases ability to invest in greater amount of WPA bonds.

• Decreases bond concentration in any one particular portfolio of managed funds.

• Note: This should also be considered for Wyoming Infrastructure Authority.

23

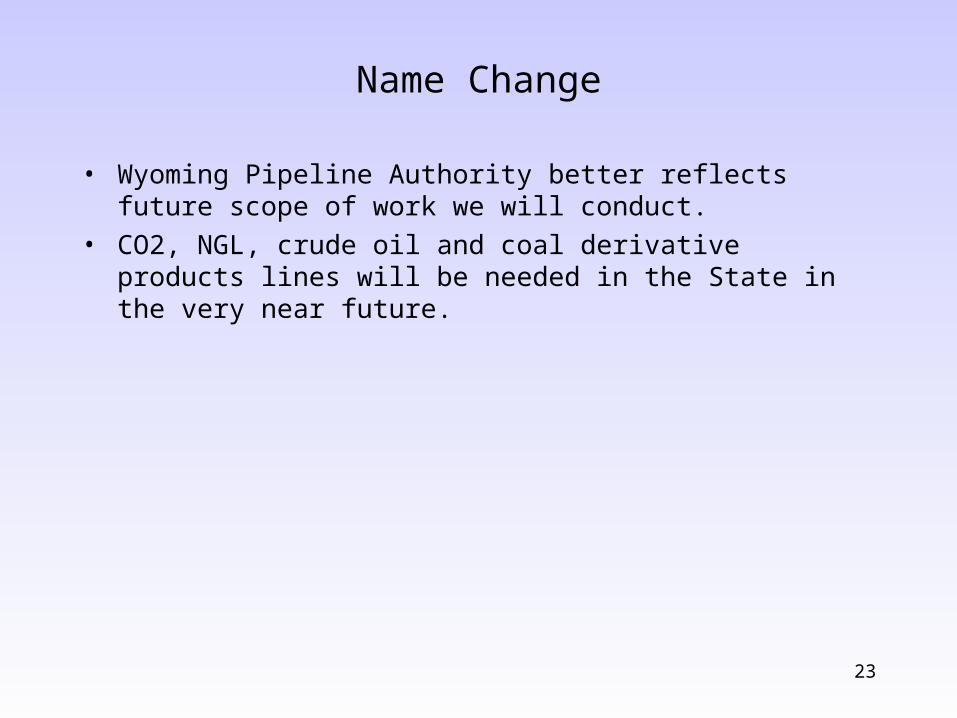

Name Change

• Wyoming Pipeline Authority better reflects future scope of work we will conduct.

• CO2, NGL, crude oil and coal derivative products lines will be needed in the State in the very near future.

24

Constitutional Amendment

• If industry doesn’t step to the plate………Wyoming needs to have the ability to defend its revenue stream.

25

Contact Information

Bryan Hassler - Executive DirectorE-mail – [email protected]

Carla Hubbard – AdministratorE-mail – [email protected] Colby Drechsel - Associate Director

E-mail – [email protected]

152 N. Durbin Street – Suite 230Casper, Wyoming 82601

Office (307) 237-5009

www.wyopipeline.com