1 iso confidential material1 predictive modeling & marketing

TRANSCRIPT

1

ISO Confidential Material 1

Predictive Modeling & Marketing

2

– A quick peek at what Marketing says it does– “wallet share”– Risk scoring– Aligning marketing and UW

– A quick peek at what Marketing says it does– “wallet share”– Risk scoring– Aligning marketing and UW

OverviewOverview

3

Sales and Distribution

Producer SegmentationMarket PlanningRevenue ForecastingCross sell and Up sellRetention and Profitability

Underwriting

Risk Selection and PricingPortfolio ManagementPremium AdequacyBilling and Collections Management

Claims

Payment AccuracyClaim Collaboration > Fraud Detection > Subrogation > Risk Transfer > 3rd Party Deductible > Reinsurance Recoverable

General Organizational OverviewAn information business focused on risk taking.Make. Sell. Serve.

4

Student

Travel

Car insurance Family needs Mortgage

Expenditure

Income

$ over time

CoverageAt School

Coverage Out of country

AutoInsurance

Life Home SVP Umbrella

Customer Focus: Products across life stages

As income increases, the needs for insurance grow

5

Personal Auto Policy Homeowners

$250 $250 $250

Personal Umbrella

$100K

$300K

$50K

$300K

$1.3 million

$1 million

Stackable Coverage can show ‘wallet share’ of customers and point out opportunities for cross-sell and up-sell

6

Most Profitable

Responder New Customer

NOT Profitable

Forced Churn

VoluntarilyLeft YouNext Most

ProfitableTargetMarket

Prospect Responder Current Customers Former

•Acquisition Campaigns

•Cross-sell Campaigns •Upsell Campaigns

•Attrition Prediction•Forced Cancellation•Winback Campaigns

•Segmentation•Risk Selection•Pricing•Yield Management

Customer Life Cycle ManagementBest Practice use of CLTV is to incorporate it into all stages during a customer’s lifecycle

7

Case Study: Database MarketingImplementation ApproachCase Study: Database MarketingImplementation Approach

SERVICE DIFFERENTIATION BASED ON “PORTFOLIO POSITION”SERVICE DIFFERENTIATION BASED ON “PORTFOLIO POSITION”

Most Profitable

NOT Profitable

Next Most Profitable

Retention Programs

Cross-sell / Up-sell

Loss Control Services

Agency Contact

Re-underwriting

Cross-sell / Up-sellForced Churn (where legally appropriate)

Price to Risk

8

Portfolio View for Underwriting AnalysisPortfolio View for Underwriting Analysis

9

Grow Your Book in the Right Direction

10

A vast array of CRM applications demand a common glue -- Analytics

11

Universe of all Prospects

Sales Pipeline

Lead Qualification

Lead Gathering and Targeting

Selling, Contracting

Hot

Cold

Customer

Process

Lead

Opportunity

Warm

Sales FunnelSales Funnel

Analyze, learn, grow customer

Your Selected Prospects

12

Mass Targeted

Competitive Attention Selective Attention

Breadth Depth

Remember Respond

Impression Decision

Pay for Everyone Pay for Targets

General Advertising and Direct Mail – A Simple ComparisonGeneral Advertising and Direct Mail – A Simple Comparison

Advertising Direct Marketing

13

Selection FactorsSelection Factors

• Consumer Lists– Age– Income– Gender– Marital Status– Homeowner– Dwelling Type (home

or apartment)– Mail order buying (by

product type)– Interests– Presence of children– Geographical (zip,

SCF, county, state, carrier route)

• Consumer Lists– Age– Income– Gender– Marital Status– Homeowner– Dwelling Type (home

or apartment)– Mail order buying (by

product type)– Interests– Presence of children– Geographical (zip,

SCF, county, state, carrier route)

• Business Lists– SIC (Standard

Industrial Classification)

– Employee Size– Annual Sales/Revenue– Title– Any other information

captured on subscription form (publications)

– Corporate linkage information

– # of years in business– Geographical (zip,

SCF, county, state)– Credit information

14

B2B Marketing Profile – Banking, Finance & InsuranceB2B Marketing Profile – Banking, Finance & Insurance

Base: N= 47 Source: Forrester Consulting Survey for ABM

2005 Budget Allocation

General business magazines 6.2%

Custom publications10.7%

Industry-specific/trade magazines 6.2%

Direct mail10.5%

Online marketing 7.3%

In-person events5.4%

Other10.4%

Radio3.8%

Printed newsletters6.9%

Public relations3.0%

TV11.1%

Printed directories1.8%

Newspapers16.7%

15

Data Driven Campaign ManagementData Driven Campaign Management

Targeted Marketing

Crosssell

Retention&

Loyality

Credit Risk

NewProduct

NewChannels

NewServices

Data Analysis

ReportingOLAP Data Market

Research

Analysis Mining

Data Warehouse

Data Driven Campaign

management

Segmentation & Scoring

16

Personal Auto Risk FrameworkPersonal Auto Risk Framework

State

Territory

Vehicle Age& Symbol

Limits &Deductibles

SpecialAdjustments

Environmental Risk Module:

Weather, Street, Businesses, Traffic Density, Driving Patterns

etc

Vehicle Risk Module:Weight, Engine Size, etc.

Class Driver History Module

No Change

No Change

Policy Risk ModuleInteractions of all Variables

State

VIN

Address

Personal Identifiers

Address, Drivers,Vehicles

Rating Plan Input

17

ZIP Code 94109: A TourZIP Code 94109: A Tour

The Tenderloin: "...the haunt of the low and vile of every kind. ….Licentiousness, debauchery, pollution, loathsome disease, insanity from dissipation, misery, poverty, blasphemy and death are there. And Hell, yawning to receive the putrid mass, is there also. “

Robert Louis Stevenson declared "Nob Hill, the Hill of Palaces, must certainly be counted the best part of San Francisco."

Japantown

Fishermen’s Wharf

18

Small-Area Geography OverviewSmall-Area Geography Overview

19

Newark NJ AreaCombined RelativityNewark NJ AreaCombined Relativity

"8

"8

"8

"8

"8

"8

"8

"8

"8

"8

"8

"8"8

"8

"8

"8

"8

"8

"8"8

"8

"8

"8

"8

"8

"8 "8

"8

"8

"8

"8

"8

"8

"8

"8

"8

"8

"8"8

"8

"8"8

Clark

Union

Kearny

Linden

Newark

Nutley

Orange

Summit

Verona

Bayonne

Hoboken

Passaic

RoselleCranford

Fairview

Harrison

Hillside

Millburn

Secaucus

Elizabeth

Irvington

Lyndhurst

Maplewood

Montclair

Westfield

Belleville

Bloomfield

GuttenbergLivingston

RidgefieldRutherford

Union City

WallingtonCedar Grove

East Orange

Jersey City

Springfield

West Orange

Little Ferry

Roselle Park

South Orange

Scotch Plains

West Caldwell

West New York

Palisades Park

North Arlington

Ridgefield Park

20

Combining Risk Scores for MarketingCombining Risk Scores for Marketing

21

Competitive AdvantageCompetitive Advantage L

oss

$

Risk

• Carriers establish a base rate for each rating territory that represents the average expected loss cost.

Base Rate

22

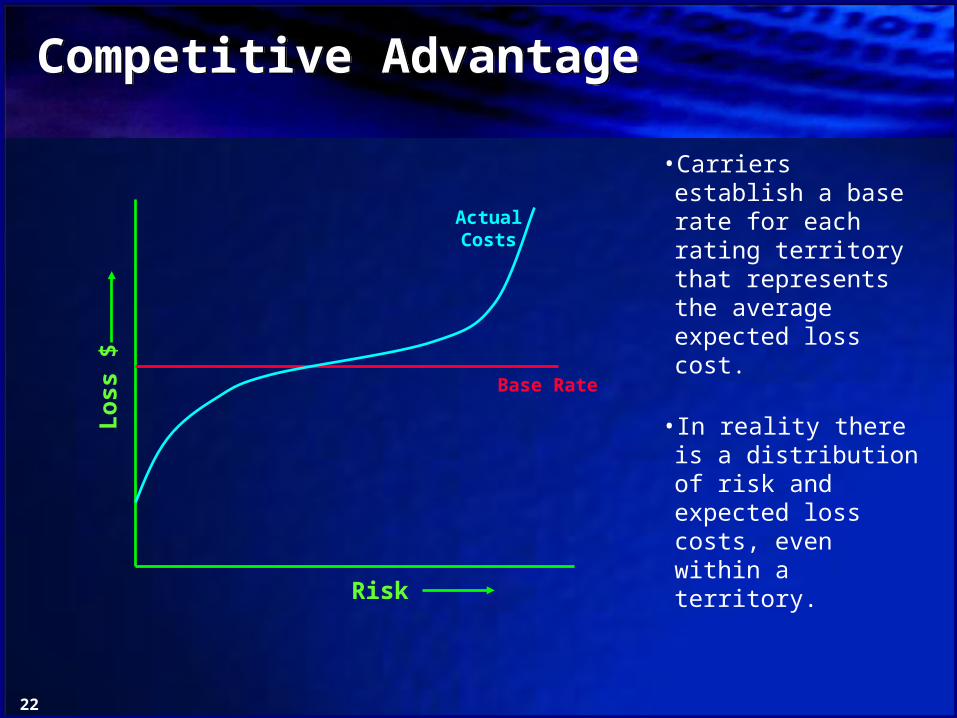

Competitive AdvantageCompetitive Advantage

Risk

• Carriers establish a base rate for each rating territory that represents the average expected loss cost.

• In reality there is a distribution of risk and expected loss costs, even within a territory.

Base Rate

ActualCosts

Lo

ss $

23

Competitive AdvantageCompetitive Advantage

Risk

• Carriers establish a base rate for each rating territory that represents the average expected loss cost.

• In reality there is a distribution of risk and expected loss costs, even within a territory.

• The Prescreen Score more closely follows the actual distribution of risk.

Base Rate

ActualCosts

PrescreenScore

Lo

ss $

24

Competitive AdvantageCompetitive Advantage

Risk

• Carriers establish a base rate for each rating territory that represents the average expected loss cost.

• In reality there is a distribution of risk and expected loss costs, even within a territory.

• The Prescreen Score more closely follows the actual distribution of risk.

Base Rate

ActualCosts

PrescreenScore

Users of Prescreen can let their competitors waste resources chasing these marginal accounts!

Lo

ss $

25

– Marketers can use sophisticated models– Portfolio Management is a key to success – Risk-based pricing helps a lot– It is not a competitive advantage if you don’t use it

– Marketers can use sophisticated models– Portfolio Management is a key to success – Risk-based pricing helps a lot– It is not a competitive advantage if you don’t use it

SummarySummary