1 information markets & decision makers yiling chen anthony kwasnica tracy mullen penn state...

Post on 20-Dec-2015

214 views

TRANSCRIPT

1

Information Markets & Decision Makers

Yiling ChenAnthony Kwasnica

Tracy MullenPenn State University

This research was supported by the Defense Advanced Research Projects Agency (DARPA) and the Laboratory for Economic Management and Auctions (LEMA)

2

Two Features of Information Markets

1. Information is revealed over time.– As security maturity approaches better

information becomes available.

2. Information provided by the market can be used to improve decision making.

– If the market is aggregating information, a decision maker can treat the market as a new source of information.

3

Timing v. Decisions

There is a potential tradeoff between information refinement and decision making.

– Delay is costly. Decision makers often prefer to make decisions earlier.

• It is more expensive to move resources quickly.• Low cost options can disappear.

– If delay is costly, a decision maker must decide between making a decision earlier with less accuracy but low cost and a decision later with higher accuracy but high cost.

4

This Research

We examine experimentally the interaction between decision makers and information markets when delay is costly and new information is revealed over time.– What is the optimal decision making strategy?– What do human decision makers do?

• Do decision makers make systematic errors when utilizing information market data?

– How does the information market perform with multiple decision makers?

5

Experiment Design

• Two states of the world: Good, Bad– Prior probability of Good and Bad is .5

• One state contingent asset:

100 if Good

0 if BadAvìïï=íïïî

6

Experiment Design (cont’d)

• 8 traders endowed with 5 units of the asset and cash.

• Can buy or sell in a standard asset double auction market.

• Each auction period consists of 5 discrete rounds lasting 3-4 minutes.

• 5-6 auction periods per experimental session.

7

Trading

• Traders can buy or sell units of the asset.

• Traders are given an informative signal about the likelihood of the two states.– Signal g is more likely in Good and signal b

is more likely in Bad.– Observe one new signal in each round

8

Trading

Since traders observe an additional signal at the beginning of each round, the information in the market improves over time.

Example of how information might change overtimeRound

1 2 3 4 5

g 1 2 2 3 4

b 0 0 1 1 1

Pr(G) .6 .69 .6 .69 .77

Pr(B) .4 .21 .4 .21 .23

9

Decision Making

All traders must make a decision (1 or 2)– The value of the decision depends upon

the state (Good or Bad).– There is a cost c associated with delaying

the decision (to later rounds).– Decision must be reached before

resolution of the state.

10

Decision Making

Decision 1 is preferred when the state is Good and 2 when the state is Bad.

All payoffs decrease by c for each round of delay.

Decision Payoffs

Good Bad

Round 1 2 1 2

0 550 50 50 550

1 540 40 40 540

2 530 30 30 530

3 520 20 20 520

4 510 10 10 510

5 500 0 0 500

11

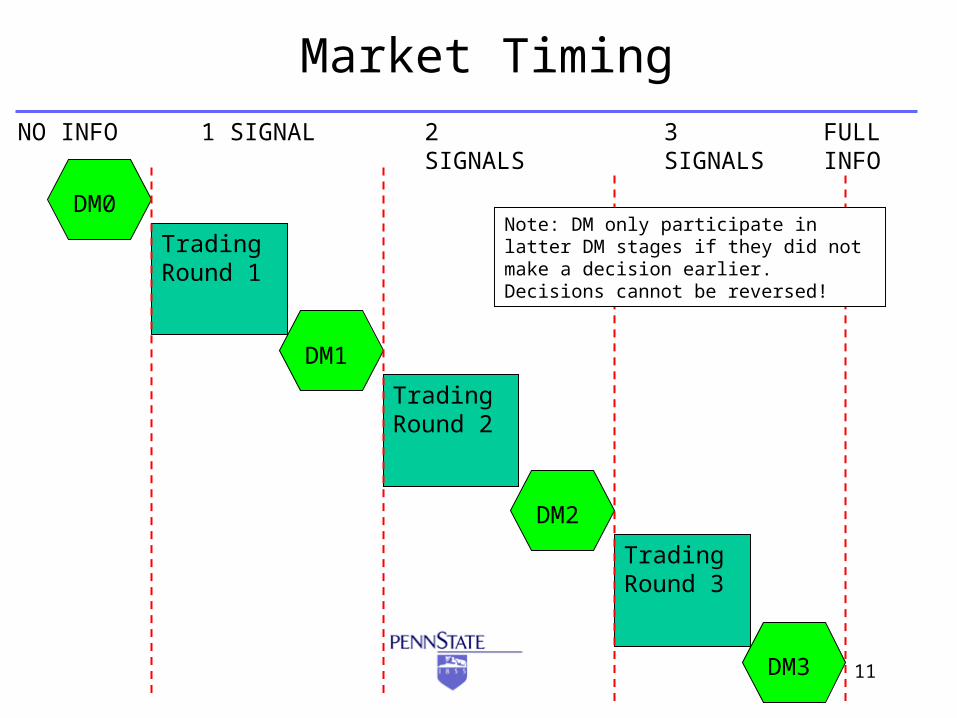

Market Timing

Trading Round 1

Trading Round 2

Trading Round 3

NO INFO 1 SIGNAL 2 SIGNALS 3 SIGNALS FULL INFO

DM0

DM1

DM2

DM3

Note: DM only participate in latter DM stages if they did not make a decision earlier. Decisions cannot be reversed!

12

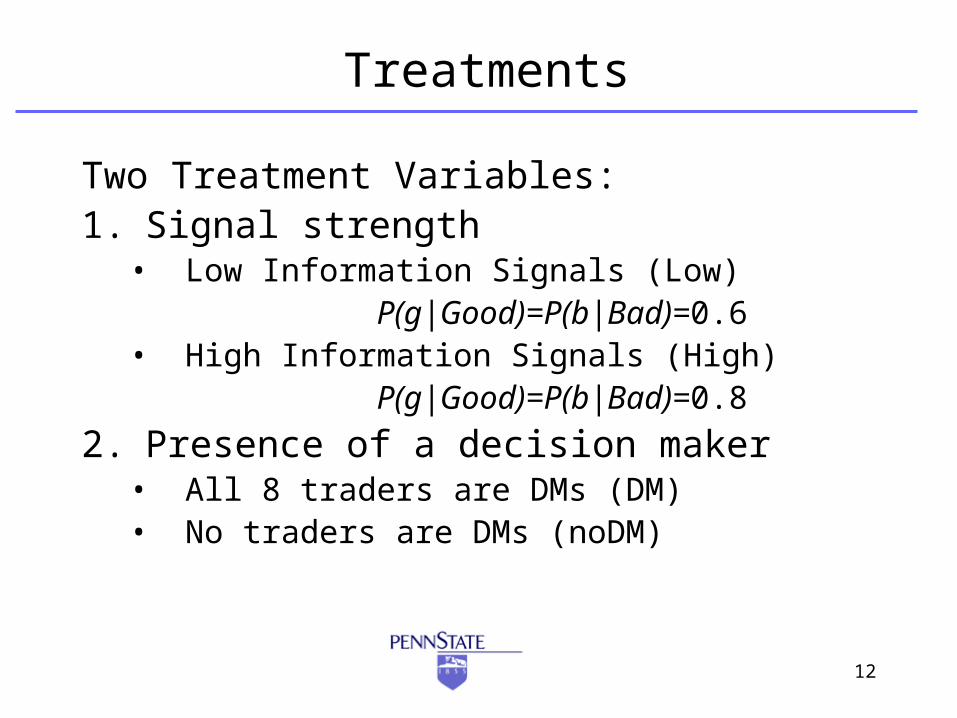

Treatments

Two Treatment Variables:1. Signal strength

• Low Information Signals (Low)P(g|Good)=P(b|Bad)=0.6

• High Information Signals (High)P(g|Good)=P(b|Bad)=0.8

2. Presence of a decision maker• All 8 traders are DMs (DM)• No traders are DMs (noDM)

13

Treatments

Decision Makers

DM noDM

SignalsLow 3 (24) 2 (16)

High 3 (24)

Sessions Completed

All sessions conducted at the LEMA lab at Penn State University.

8 traders per session for 5-6 periods

14

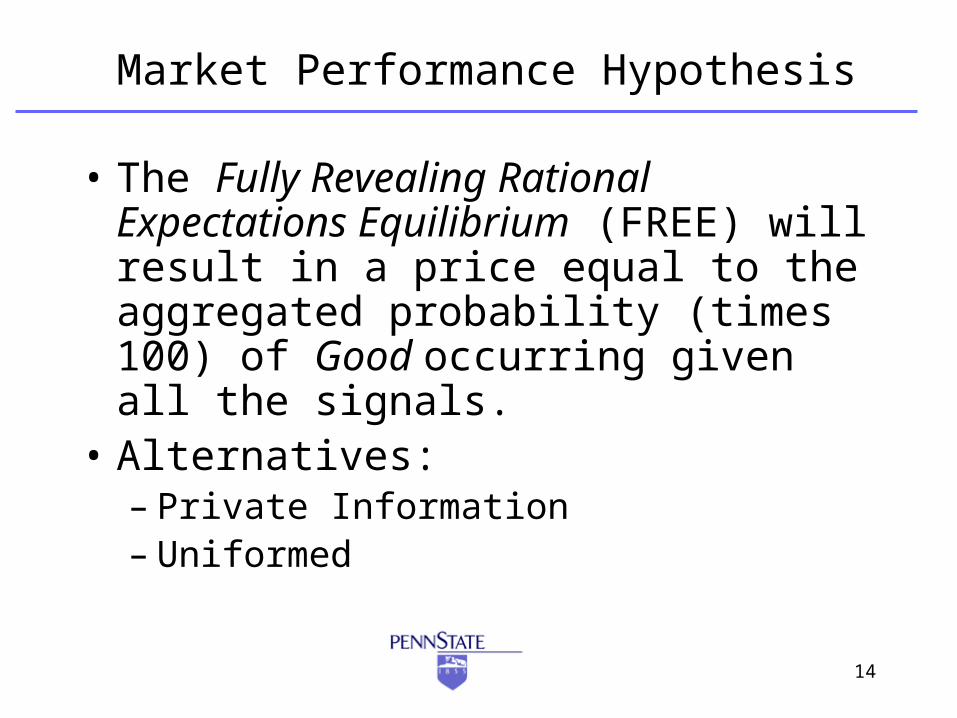

Market Performance Hypothesis

• The Fully Revealing Rational Expectations Equilibrium (FREE) will result in a price equal to the aggregated probability (times 100) of Good occurring given all the signals.

• Alternatives:– Private Information– Uniformed

15

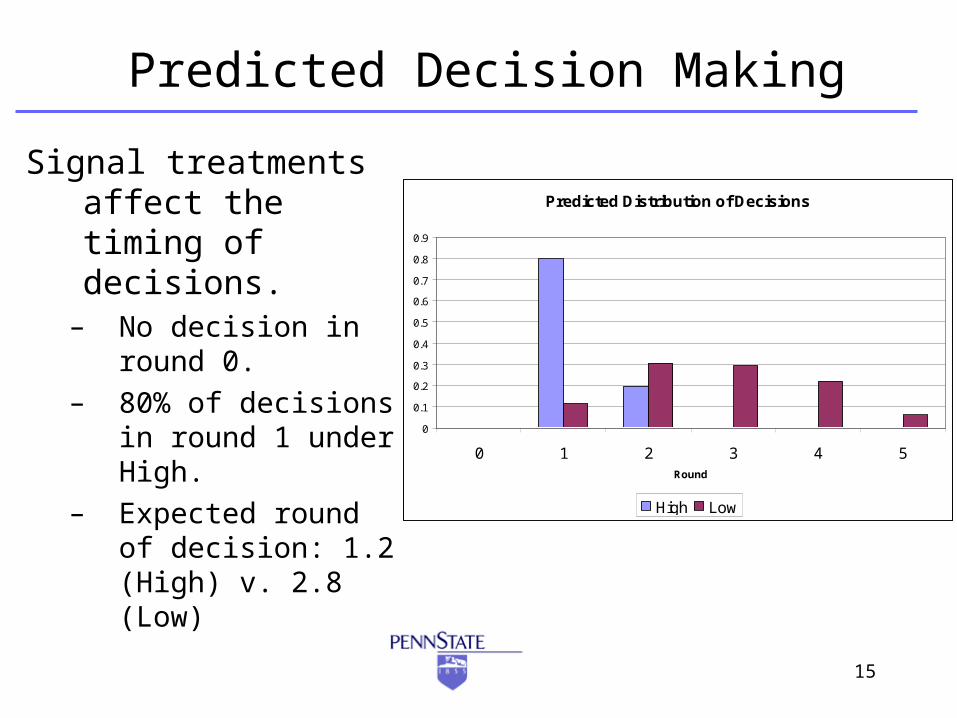

Predicted Decision Making

Signal treatments affect the timing of decisions.

– No decision in round 0.

– 80% of decisions in round 1 under High.

– Expected round of decision: 1.2 (High) v. 2.8 (Low)

Predicted Distribution of Decisions

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0 1 2 3 4 5Round

High Low

16

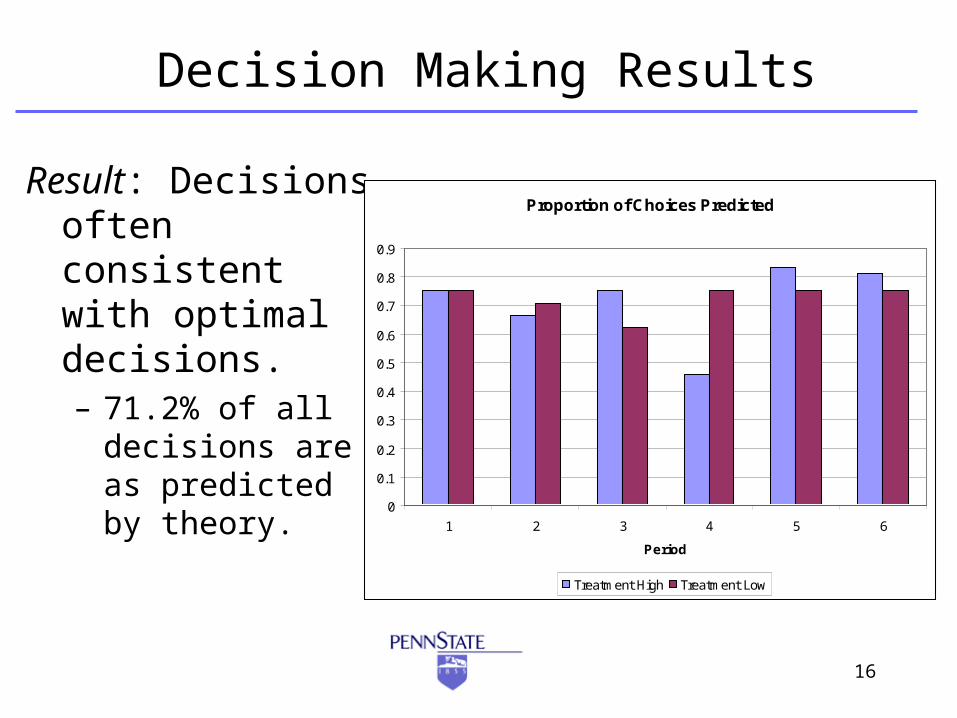

Decision Making Results

Result: Decisions often consistent with optimal decisions.– 71.2% of all

decisions are as predicted by theory.

Proportion of Choices Predicted

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1 2 3 4 5 6

Period

Treatment High Treatment Low

17

Decision Making Results

Result: Timing of decisions is rarely consistent with optimal decisions.– 12.1% of all decisions are placed at the

time predicted.– Mean Decision Time: 2.02 (High)

1.83(Low)• Significantly different from predicted: t=5.49

(High) t=5.65 (Low)• Direction is flipped.

18

Decision Making Results

Result: Decisions are often made before any information is acquired.– 34.5% in High and

44.5% in Low– This is never

predicted by the theory!

Timing of Decisions

00.05

0.10.15

0.20.25

0.30.35

0.40.45

0.5

0 1 2 3 4 5

Round

Fre

qu

ency

High Low

19

Decision Making Results

Result: There is no evidence of learning.

• High is consistently later than predicted.

• Low is consistently earlier than predicted.

Average Distance from Predicted Time

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

1 2 3 4 5 6Period

High Low

20

Market Data Example (Low)Market Pri ce v. s. Theoreti cal Pri ce

LOW SI GNALS

0

20

40

60

80

100

120

Tradi ng Peri od

Pric

e

Market Pri ce Theoreti cal Pri ce

21

Market Data Example (High)Market Pri ce v. s. Theoret i cal Pri ce

HI GH SI GNALS

0

20

40

60

80

100

120

Tradi ng Peri od

Pric

e

REE Pri ce Tradi ng Pri ce

22

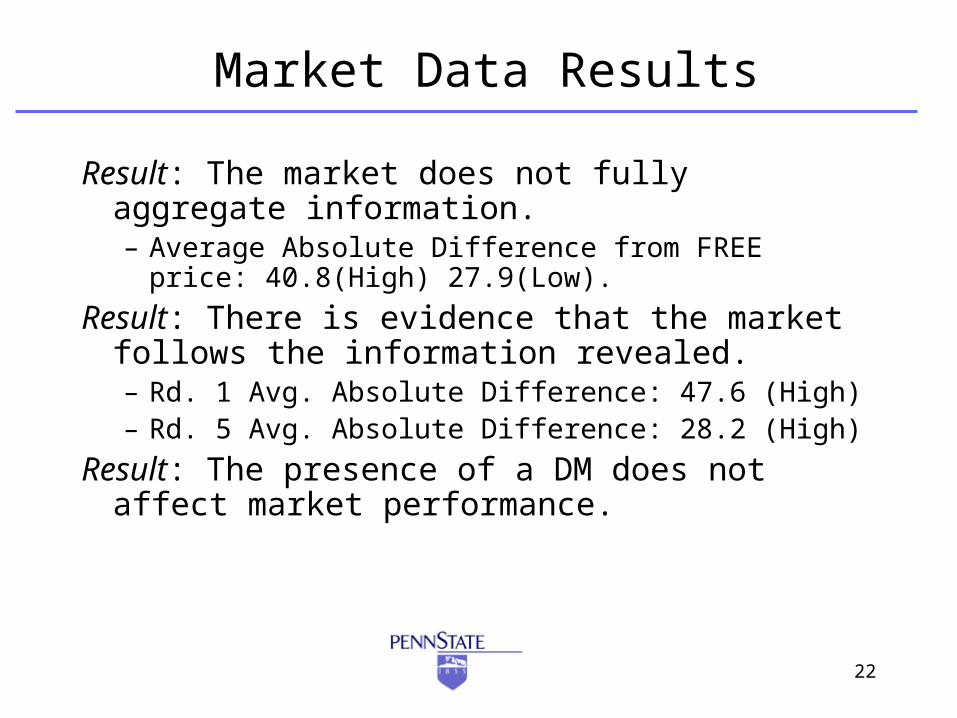

Market Data Results

Result: The market does not fully aggregate information.– Average Absolute Difference from FREE price:

40.8(High) 27.9(Low).

Result: There is evidence that the market follows the information revealed.– Rd. 1 Avg. Absolute Difference: 47.6 (High)– Rd. 5 Avg. Absolute Difference: 28.2 (High)

Result: The presence of a DM does not affect market performance.

23

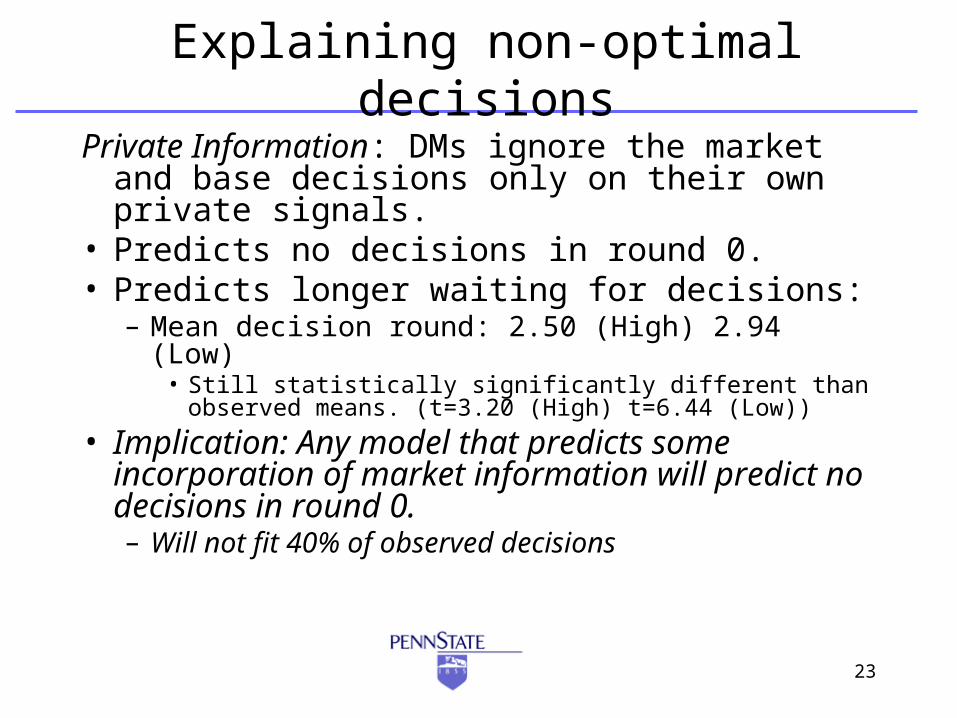

Explaining non-optimal decisions

Private Information: DMs ignore the market and base decisions only on their own private signals.

• Predicts no decisions in round 0.• Predicts longer waiting for decisions:

– Mean decision round: 2.50 (High) 2.94 (Low)• Still statistically significantly different than observed

means. (t=3.20 (High) t=6.44 (Low))

• Implication: Any model that predicts some incorporation of market information will predict no decisions in round 0.– Will not fit 40% of observed decisions

24

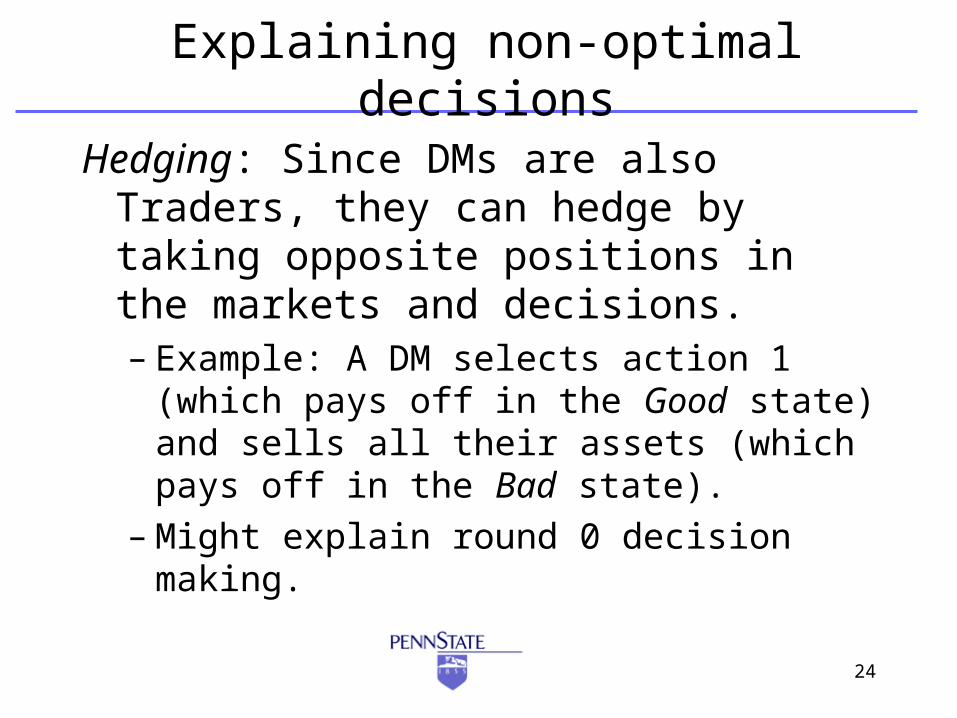

Explaining non-optimal decisions

Hedging: Since DMs are also Traders, they can hedge by taking opposite positions in the markets and decisions.– Example: A DM selects action 1 (which

pays off in the Good state) and sells all their assets (which pays off in the Bad state).

– Might explain round 0 decision making.

25

Explaining non-optimal decisions

Hedging: Classify a subject as hedging in a given period if they make decision counter to their strong (at least 5 units) buying or selling habits.

• Proportion of obs. classified as Hedging: 19.8% (High) 14.8% (Low)– Many observations do not involve

decisions in round 0. (41% and 37% in rd. 0).

26

Other Decisions

Remove all 0 round decisions and look only at those that may be consistent with the theory.

• Average decision round now later than predicted and treatment effect now closer to expected.

Avg. Decision Round: 3.09 (High) 3.30 (Low)

t=15.8 t=2.86

– Mean decision round in High treatment appears to be declining with experience.

– 80% of decisions as predicted by theory.– 20% of decision times as predicted by theory.

27

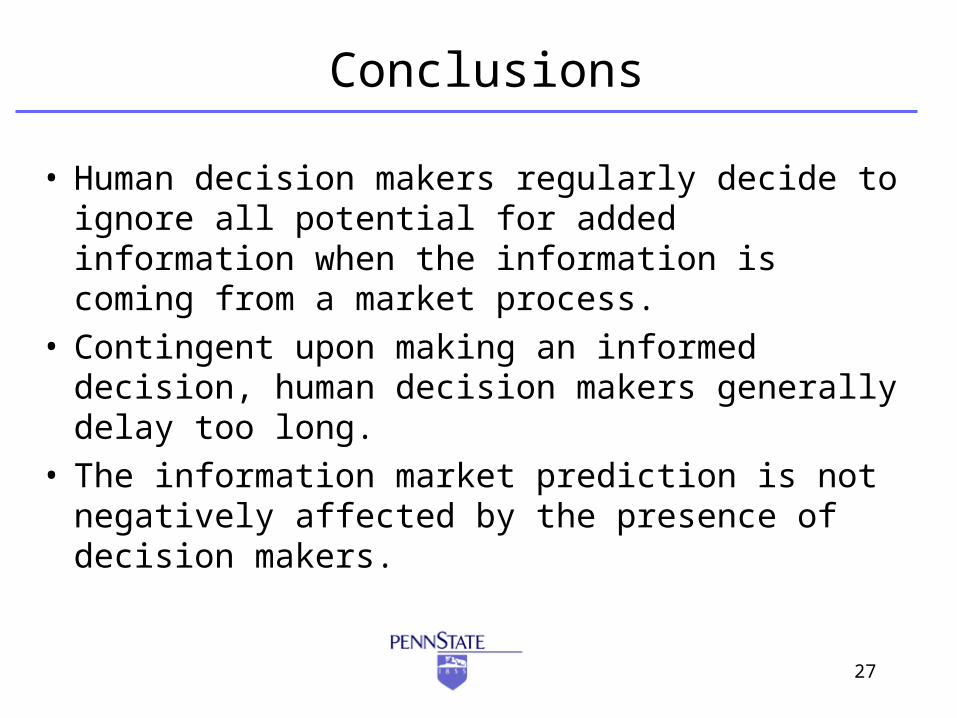

Conclusions

• Human decision makers regularly decide to ignore all potential for added information when the information is coming from a market process.

• Contingent upon making an informed decision, human decision makers generally delay too long.

• The information market prediction is not negatively affected by the presence of decision makers.

28

Next Steps

• Additional treatments to understand decision making biases.– Decisions without the market but same info.– DMs and Traders are different.

• Understanding Market Dynamics– What does the convergence process look like?– Even if decision makers to do the right thing, added

uncertainty comes from the market adjustment process.