1 i godrej agrovet trend and challenges in indian poultry industry 19 th june, 2015

TRANSCRIPT

1 I Godrej Agrovet

TREND AND CHALLENGES ININDIAN POULTRY INDUSTRY

19th June, 2015

ANIMAL AGRICULTURE AT A GLANCE

3 I Godrej Agrovet

ANIMAL AGRICULTURE HOLDS TREMENDOUS PROMISE FOR THE FUTURE…

2004-05 2012-13 2019-20 -

200,000

400,000

600,000

800,000

1,000,000

1,200,000

638,530

870,896

1,142,625

180,034 261,771

363,218

Agriculture: Value Output Animal Agriculture: Value Output

Agriculture vs Animal Agriculture Value Output (INR ‘000 Crores)

Animal Agriculture Value Output as a % of Agriculture Value

Output

28% 30% 32%

Historically, Animal Agriculture has grown at a faster rate than Overall Agriculture. This trend is expected to continue resulting in faster

growth of Animal Agriculture

CAGR: 4.0%

CAGR: 4.8%

If Animal Agriculture

continues to grow at historical rates,

its size in 2020 would be

~363,000 crores (USD 60 bn)

Source: National Account StatisticsFigures at 2004-05 constant pricesUSD/INR assumed at 61

4 I Godrej Agrovet

Source: Ministry of Agriculture, CSO, GAVL analysisFigures at 2004-05 constant prices

AND …LIVESTOCK WILL ACCOUNT FOR 50% OF THE TOTAL AGRICULTURE OUTPUT BY 2030

72%

28%

FY 2007

71%

29%

FY 2011

Crops Livestock

50%

50%

FY 2030

GVO at constant prices in Rs. ‘ 000 crore

5 I Godrej Agrovet

ANIMAL AGRICULTURE COULD BE A GAME CHANGER FOR INDIAN FARMERS

Particulars (per Ha) Rice Wheat Sugarcane

Total Profit / Ha / Year (INR) 60 to 70 K 70 – 80 K 1.0 – 1.2 Lakh

Profit per Ha per year through Agricultural Crops

Profit per Ha / Year In INR Requirement for a profit of 1 Lakh / Year

Cattle Farming (10) 1.5 – 2.0 Lakh 6 cows

Broiler Farming (10,000) 2.5 – 3.0 Lakh 3,650 broilers

Layer Farming (10,000) 3.0 – 3.5 Lakh 3,100 layers

Shrimps Farming (acre) 5.0 – 6.0 Lakh 0.2 acres of land

Profit per year through Animal Farming

Note: In animal farming, there are other source of income like cow dung, broiler/layer litter etc.

Income of farmers varies depending upon milk, broiler, egg and shrimp prices in the market

Indian farmer can make significantly more money in animal agriculture compared to agriculture. Moreover, even non-agricultural land can be used for animal farming

making full utilization of land resources

6 I Godrej Agrovet

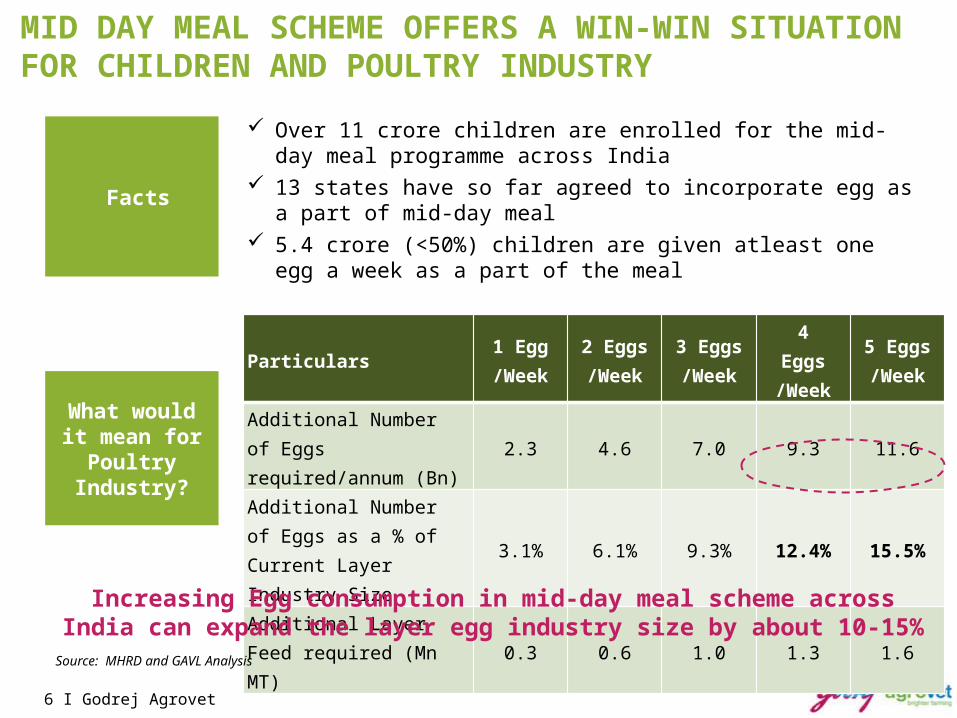

MID DAY MEAL SCHEME OFFERS A WIN-WIN SITUATION FOR CHILDREN AND POULTRY INDUSTRY

Facts

Over 11 crore children are enrolled for the mid-day meal programme across India

13 states have so far agreed to incorporate egg as a part of mid-day meal

5.4 crore (<50%) children are given atleast one egg a week as a part of the meal

What would it mean for Poultry

Industry?

Particulars1 Egg/Week

2 Eggs/Week

3 Eggs/Week

4 Eggs /Week

5 Eggs/Week

Additional Number of Eggs required/annum (Bn)

2.3 4.6 7.0 9.3 11.6

Additional Number of Eggs as a % of Current Layer Industry Size

3.1% 6.1% 9.3% 12.4% 15.5%

Additional Layer Feed required (Mn MT)

0.3 0.6 1.0 1.3 1.6

Increasing Egg consumption in mid-day meal scheme across India can expand the layer egg industry size by about 10-15%

Source: MHRD and GAVL Analysis

7 I Godrej Agrovet

CHICKEN CONSUMPTION HAS BEEN GROWING DUE TO CHANGING CONSUMER PREFERENCES

2007 2008 2009 2010 2011 2012 2013 20141.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2.72.9

3.2 3.4 3.43.7

4.04.2

Gross Consumption (Mn MT)

2007 2008 2009 2010 2011 2012 2013 20141.0

1.5

2.0

2.5

3.0

3.5

2.32.4

2.7 2.7 2.73.0

3.23.3

Per Capita Annual Chicken Consumption (Kg)

On a pan-India basis, Chicken is the most preferred non-vegetarian diet due to its availability and taste. QSR and Food Service businesses are expected to

drive growth in Consumption of Chicken in the future

CAGR:

6.4%

Source: OECD and FAO; GAVL Analysis

Note: Chicken consumption includes meat from Broiler, Layer and Breeder birds

8 I Godrej Agrovet

GROWTH IN POULTRY INDUSTRY WILL BE DRIVEN BY INCREASE IN PERCAPITA CONSUMPTION

Source: MEPDA,, News Articles, GAVL AnalysisNote: For Broiler and Layer, grown in India’s population will also drive the growth in aggregate consumption

Layer Egg Industry

75 Billion Eggs in 2014

Poultry Meat Industry

4.2 Mn MT in 2014

2013-14 2019-20

55

76

Layer: Percapita Annual Consumption of Eggs

CAGR: 5.5%

2013-14 2019-20

2.9

4.5

Broiler: Percapita Annual Consumption (Kg)

CAGR: 8.0%

9 I Godrej Agrovet

FUTURE OF POULTRY INDUSTRY LOOKS SECURE ASGROWTH WILL BE DRIVEN BY RISE IN PERCAPITA INCOMES

Per Capita Poultry Meat Consumption one of the Lowest

Brazil USA Japan Thailand China Vietnam India1

11

21

31

41

51 47.044.0

13.5 13.010.0 7.5

3.0

KG/Annum

Per Capita Poultry Meat Consumption vs.

Per Capita GDP

Low per capita in India is holding back poultry meat consumption

Significantly high consumption in developed countries

Source: Rabo Bank; figures as of 2012

KEY CHALLENGES

11 I Godrej Agrovet

VOLATILITY IN BROILER PRICES IS HERE TO STAY

Oct

-11

Dec-1

1

Feb-1

2

Apr-1

2

Jun-

12

Aug-1

2

Oct

-12

Dec-1

2

Feb-1

3

Apr-1

3

Jun-

13

Aug-1

3

Oct

-13

Dec-1

3

Feb-1

4

Apr-1

4

Jun-

14

Aug-1

4

Oct

-14

Dec-1

4

Feb-1

5

Apr-1

50

10

20

30

40

50

60

70

80

90

5757

Live Prices (INR) for West Region

Live Price

Live Prices have been highly volatile and remained almost flat on yearly basisVolatility in prices results in Yo-Yo profits for integrators

Source: poultrybazaar.net

1

12 I Godrej Agrovet

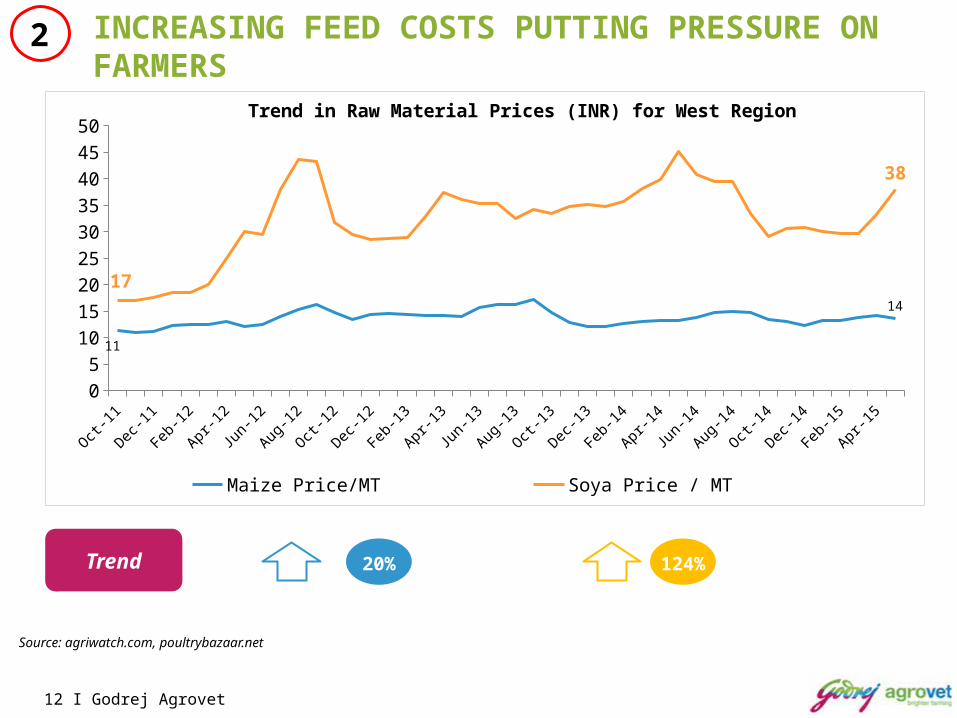

INCREASING FEED COSTS PUTTING PRESSURE ON FARMERS

20%

Oct

-11

Dec-1

1

Feb-1

2

Apr-1

2

Jun-

12

Aug-1

2

Oct

-12

Dec-1

2

Feb-1

3

Apr-1

3

Jun-

13

Aug-1

3

Oct

-13

Dec-1

3

Feb-1

4

Apr-1

4

Jun-

14

Aug-1

4

Oct

-14

Dec-1

4

Feb-1

5

Apr-1

50

5

10

15

20

25

30

35

40

45

50

11

14

17

38

Trend in Raw Material Prices (INR) for West Region

Maize Price/MT Soya Price / MT

Trend 124%

Source: agriwatch.com, poultrybazaar.net

2

13 I Godrej Agrovet

POOR DISEASE MANAGEMENT IN FARMS ADDS TO THE VOLATILITY

• Farmers: Revenue loss resulting in lower profits

• Feed Players: Decrease in cash with farmer resulting in decline in sales

• Food Processing: Lower utilization of plants during culling

• End Consumers: Wide swings in prices during outbreak of diseases

2006 2008 2015

10.44

61.62

72.46

No. of birds culled in major bird flu outbreaks[Lakhs]

2011 2012 2013

100% 100%

73%

Death rate of Avian influenza [bird flu]

INCIDENTLOSS [NO.OF

BIRDS IN LAKHS]

LOSS OF OUTPUT VALUE

[Rs crores]

BIRD FLU 72.46 86.94

HEAT WAVE 50.0 57.0

YEAR 2014 HAS ACCOUNTED FOR MORE LOSS THAN EVER

Source: Economic times, animal husbandry statistics 2014, GOI

3

14 I Godrej Agrovet

OUR ABILITY TO LOBBY AS A GROUP LIMITED

Chicken leg price (Rs/kg)

0 20 40 60 80 100 120 140 160 180

45

170

Chicken Legs Avg Price comparison (Rs/kg)

India USA

• WTO has ruled in favour of USA forcing India to allow imports of chicken legs from USA

• Currently, fresh chicken in retail was selling for Rs 180 a kg and chicken legs for Rs 240 a kg.

• On the other hand, chicken drumsticks from US come in at around Rs 50-60 a kg.

COUNTRY REASON FOR BAN

China Avian Flu

European UnionChlorine treatment of chicken

South Africa Chicken fed with GM feed

OTHER COUNTRIES THAT RESTRICT USA CHICKEN IMPORTS

Source: Economic times, various news articles

4

India has challenged the verdict, Are we doing enough as a

group

15 I Godrej Agrovet

WE ARE NOT THE PREFERRED EMPLOYERS FOR THE TALENT OF THE COUNTRY

Best Companies to Work For, India 2013

Hardly any Organization features in the “ Best Employer” Surveys

Godrej Agrovet Godrej Agrovet No poultry business companies

Critical to manage talent in the business

Attracting Talent Retaining Talent Nurturing Talent

5

FUTURE TRENDS

17 I Godrej Agrovet

INCREASE IN INTEGRATION AUGURS WELL FOR THE FUTURE OF POULTRY INDUSTRY ONLY IF BACKED BY VALUE ADDITION

60%

40%

FY 2011

68%

32%

FY 2013

75%

25%

FY 2015

Integration

Open Market

Source: Extent of integration in Poultry Industry; GAVL Analysis

18 I Godrej Agrovet

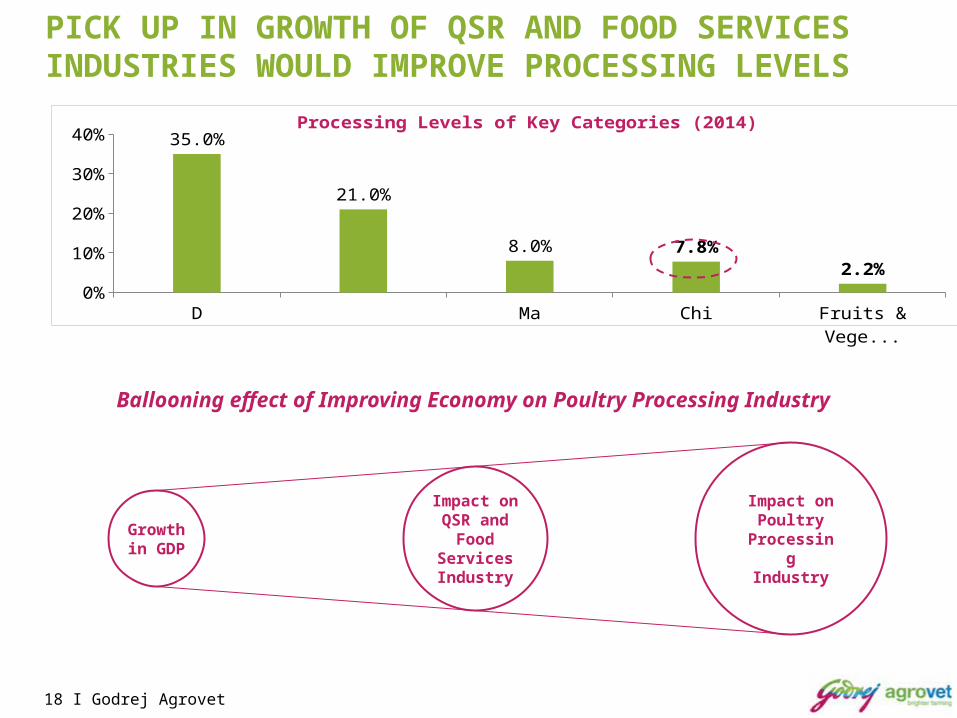

PICK UP IN GROWTH OF QSR AND FOOD SERVICES INDUSTRIES WOULD IMPROVE PROCESSING LEVELS

Dairy Meat Marine Chicken Fruits & Vegetables0%5%

10%15%20%25%30%35%40% 35.0%

21.0%

8.0% 7.8%2.2%

Processing Levels of Key Categories (2014)

Growth in GDP

Impact on QSR and

Food Services Industry

Impact on Poultry

Processing Industry

Ballooning effect of Improving Economy on Poultry Processing Industry

19 I Godrej Agrovet

PROCESSING INDUSTRY HAS SHOWN IMPRESSIVE GROWTH AND WILL CONTINUE TO DO SO

FY11 FY12 FY13 FY14 FY15P FY16E FY17E0.0

0.5

1.0

1.5

2.0

2.5

0%

2%

4%

6%

8%

1.2 1.3 1.5 1.72.0 2.2 2.3

6.6%

4.7% 5.0%5.6%

6.4% 6.8% 7.3%

India is Expected to Show Strong Recovery in the EconomyUSD Tn

2011-12 2012-13 2013-1470%75%80%85%90%95%

100%

94.3% 93.4% 92.3%

5.7% 6.6% 7.8%

Chicken: Processed market is growing at a very high rate and has increased its share in the overall market

Processed Market

Wet Market

CAGR

24.0%

5.2%

Processing Industry grew at > 4x the GDP growth rate during the last 3 years. With improving macro economy, outperformance of processing industry will continue

Source: IMF and HSBC

GDP figures are calculated with the base year as 2004-05

20 I Godrej Agrovet

THOUGH RAW MATERIAL REQUIREMENT FOR FEED PRODUCTION IS EXPECTED TO SIGNIFICANTLY GO UP…

Cattle Feed(9.8 Mn MT)

DORBMaize

1.0 Mn MT

3.9 Mn MT

(33.8 Mn MT)

Maize

Soymeal

16.9 Mn MT

6.8 Mn MT

Fish Feed(2.1 Mn MT)

1.0 Mn MT

Poultry Feed

DORBSource: GAVL Analysis (2014)

Requirement by 2020

21 I Godrej Agrovet

Feed Raw Material

Actual Raw Material

Requirement of Actual Raw

Material for 2014Production for 2013

Requirement of Actual Raw

Material by 2020

Production for 2019 (CAGR of 3%)

Maize Maize 10.8 Mn MT 23 Mn MT 17.9 Mn MT 27.5 Mn MT

Soymeal (73.8% of

Soya Bean)

Soya Bean (1.36x of Soymeal)

5.6 Mn MT 12.5 Mn MT 9.2 Mn MT 14.9 Mn MT

DORB (5.3% of Paddy)

Paddy (19x of DORB)

47.6 Mn MT 155 Mn MT 94.2 Mn MT 185.1 Mn MT

All the raw material requirements for Animal Feed can be satisfactorily met by 2020

INDIA WILL BE ABLE TO MEET ALL RAW MATERIAL REQUIREMENT BY LOCAL SOURCING ITSELF

Source: Directorate of Economics and Statistics, Department of Agriculture and Cooperation, Ministry of Agriculture GAVL AnalysisNote: Soya Bean to Soymeal Conversion Formula: 10% goes towards seed & human consumption and from the rest 18% oil is extracted

22 I Godrej Agrovet

GST WILL BOOST THE FOOD PROCESSING INDUSTRY – INCLUDING PROCESSED POULTRY

Complex tax structure currently across states in Processed Poultry

Post GST if the rates follow the developed country model , it will give a significant boost the Processed poultry business

COUNTRY OVERALL GST RATEPROCESSED FOOD GST

RATE

Australia 10% 0%

Canada 5% 0%

Singapore 7% 3%

Japan 8% 3%

United Kingdom 20% 0%

TAX RATE

NON-VEG COLD CUTS

NON-VEG BREADED

FRESH FROZEN

…RGC

FROZEN

RGC FRESH

SEALED

RGC FRESH UNSEALED

Max 17.5%(U.P.)

17.5%(U.P.)

17.5%(U.P.)

17.5%(U.P.)

14.5%(Kerala)

14.5%(Kerala)

Min 5%(15 states)

5%(15 states)

5%(16 states)

5%(10 states)

5%(3 states)

Nil(4 states)

Source: GAVL analysis, PHD chamber of Commerce & industry, news articles

23 I Godrej Agrovet

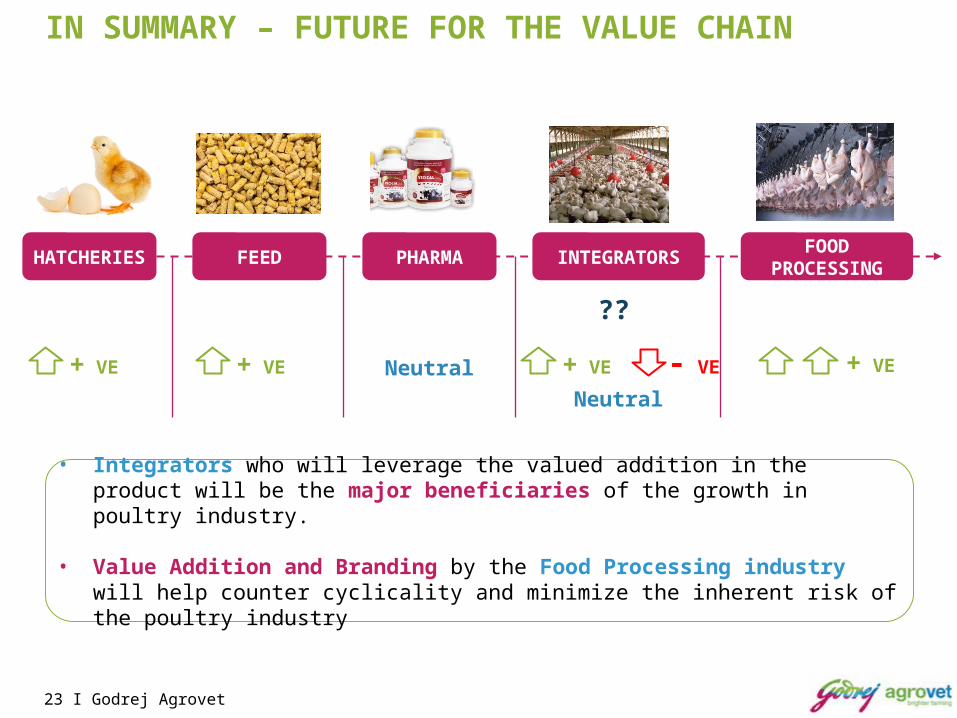

IN SUMMARY – FUTURE FOR THE VALUE CHAIN

HATCHERIES FEED PHARMA INTEGRATORSFOOD

PROCESSING

Neutral + VE

• Integrators who will leverage the valued addition in the product will be the major beneficiaries of the growth in poultry industry.

• Value Addition and Branding by the Food Processing industry will help counter cyclicality and minimize the inherent risk of the poultry industry

??

- VE

Neutral

+ VE+ VE + VE

24 I Godrej Agrovet

THANK YOU FOR YOUR TIME AND CONSIDERATION