1 finance school of management chapter 10: an overview of risk management objective risk and...

TRANSCRIPT

1

FinanceFinance School of Management School of Management

Chapter 10: An Overview of Chapter 10: An Overview of Risk ManagementRisk Management

Objective• Risk and Financial Decision Making

• Conceptual Framework for Risk Management

• Efficient Allocation of Risk-Bearing

2

FinanceFinance School of Management School of Management

What is Risk? Risk and Economic Decisions The Risk Management Process The Three Dimensions of Risk Transfer Risk Transfer and Economic Efficiency Institutions for Risk Management Portfolio Theory: Quantitative Analysis for Optimal

Risk Management Probability Distributions of Returns Standard Deviation as a Measure of Risk

ContentsContents

3

FinanceFinance School of Management School of Management

Roles of Risk ManagementRoles of Risk Management

One of the three analytical “pillars” to finance

Risk allocation (redistribution)

4

FinanceFinance School of Management School of Management

Concept of RiskConcept of Risk

Uncertainty that matters Illustration: Preparing foods for your party Gains & losses, “upside” potential & “downside”

possibility

5

FinanceFinance School of Management School of Management

Risk AversionRisk Aversion

A characteristic of an individual’s preference in risk-taking situations− Experiment

Prefer lower risk given same expected value Decreasing marginal utility of income Rational behavior assumed to be risk-averse A measure of willingness to pay to reducing risk

6

FinanceFinance School of Management School of Management

Risk ManagementRisk Management

The process of formulating the benefit-cost trade-offs of risk reduction and deciding on the course of action to take.− The appropriateness of a risk-management decision

should be judged in the light of the information available at the time the decision is made.

− Skill and lucky in risk management.

7

FinanceFinance School of Management School of Management

Risk ExposureRisk Exposure Particular types of risk one faces due to one’s

circumstances (job, business, and pattern of consumption, etc.)

Illustrations – the risk of a crop failure and the risk of a decline in the

price for a farmer

– the risks of fire, theft, storm damage, earthquake damage for a house owner

– the currency risk for a person whose business involves imports or exports of goods

8

FinanceFinance School of Management School of Management

Speculators and HedgersSpeculators and Hedgers

Hedgers: taking positions to reduce their exposures. Speculators: taking positions that increase their

exposure to certain risks in the hope of increasing their wealth.

The riskiness of an asset or a transaction cannot be assessed in isolation or in abstract.

9

FinanceFinance School of Management School of Management

Risks Facing HouseholdsRisks Facing Households

Sickness, disability, and death Unemployment Consumer-durable asset risk Liability risk Financial-asset risk

10

FinanceFinance School of Management School of Management

Risks Facing FirmsRisks Facing Firms

Production risk and R&D risk Price risk of outputs Price risk of inputs

11

FinanceFinance School of Management School of Management

The Risk-Management ProcessThe Risk-Management Process

A systematic attempt to analyze and deal with risk Steps

– Risk identification

– Risk assessment

– Selection of risk-management techniques

– Implementation

– Review

12

FinanceFinance School of Management School of Management

Risk IdentificationRisk Identification

Figuring out what the most important risk exposures are for the unity of analysis.

The perspective of the entity as a whole– Career and stock-market risk

– The net exposure to exchange-rate risk of a firm buying inputs and selling products abroad

– Price risk and quantity risk of farms

13

FinanceFinance School of Management School of Management

Risk AssessmentRisk Assessment

The quantification of the costs associated with the risks that have been identified

Health-insurance and actuaries Professional investment advisors

14

FinanceFinance School of Management School of Management

Risk-Management TechniquesRisk-Management Techniques

Risk avoidance Loss prevention and control Risk retention Risk transfer

15

FinanceFinance School of Management School of Management

Implementation Implementation

The basic principle is to minimize the costs of implementation.– The lowest premium for health insurance

– The costs of investing in the stock market through mutual fund or a broker

16

FinanceFinance School of Management School of Management

Review Review

Risk management is a dynamic “feedback” process, in which decisions are periodically reviewed and revised.

17

FinanceFinance School of Management School of Management

Risk Transfer and Economic EfficiencyRisk Transfer and Economic Efficiency

Transfering some or all of the risk to others is where the financial system plays the greatest role.

18

FinanceFinance School of Management School of Management

Risk Transfer and Economic EfficiencyRisk Transfer and Economic Efficiency

Institutional arrangements for the transfer of risk contribute to economic efficiency in two fundamental ways.

– To reallocate existing risks to those most willing to bear the risks,

– To cause a reallocation of resources to production and consumption in accordance with the new distribution of risk-bearing.

19

FinanceFinance School of Management School of Management

Efficient Bearing of Existing RisksEfficient Bearing of Existing Risks

A retired widow, whose sole source of income is $100,000 in the form of a portfolio of stocks.

A college student, who has a wealth of $100,000 in a bank CD.

The different attitudes towards future and risk. Exchange (swap) their assets.

20

FinanceFinance School of Management School of Management

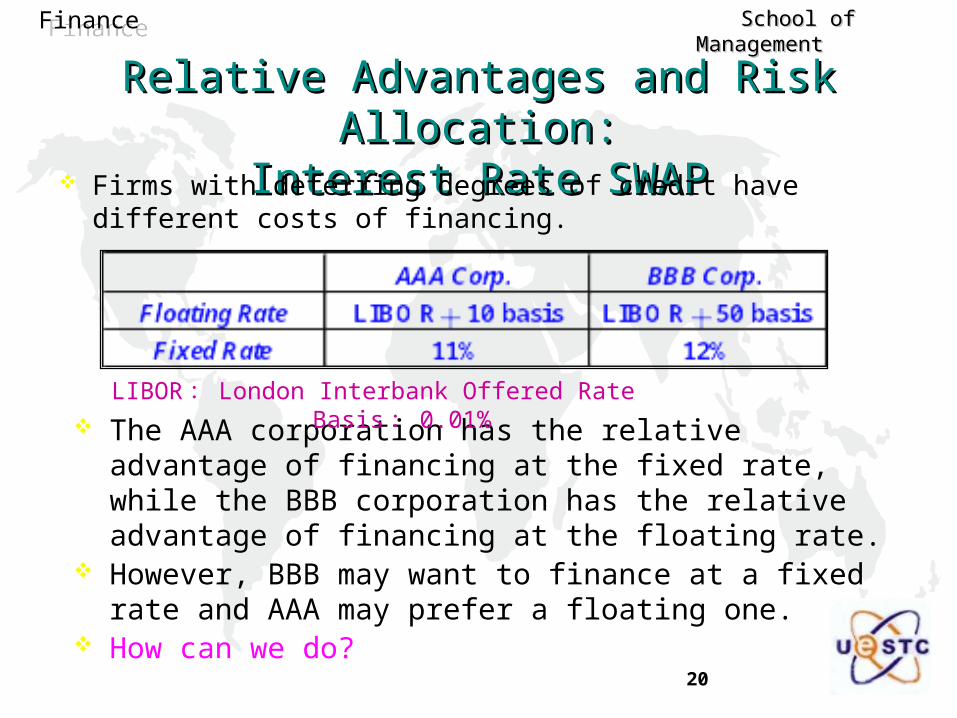

Relative Advantages and Risk Allocation:Relative Advantages and Risk Allocation:Interest Rate SWAPInterest Rate SWAP

Firms with deferring degrees of credit have different costs of financing.

The AAA corporation has the relative advantage of financing at the fixed rate, while the BBB corporation has the relative advantage of financing at the floating rate.

However, BBB may want to finance at a fixed rate and AAA may prefer a floating one.

How can we do?

LIBOR : London Interbank Offered Rate Basis :0.01%

21

FinanceFinance School of Management School of Management

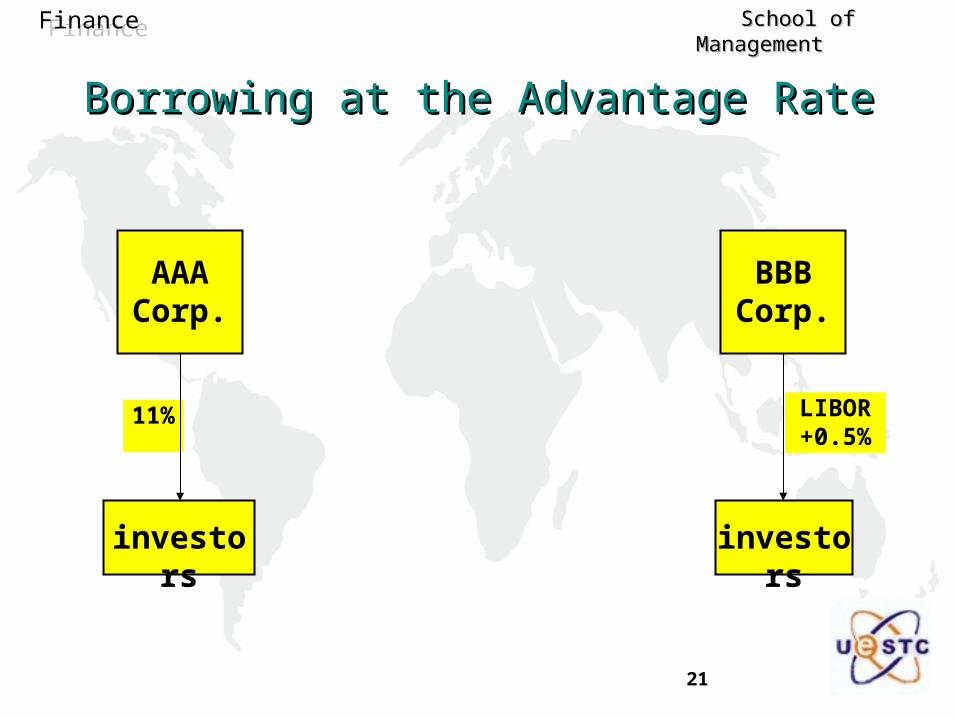

Borrowing at the Advantage RateBorrowing at the Advantage Rate

11%

AAACorp.

BBBCorp.

investors investors

LIBOR+0.5%

22

FinanceFinance School of Management School of Management

SWAPSWAP

LIBOR-0.20 % 11.70 %

11%

LIBORAAACorp.

BBBCorp.

investors investors

11.20%

LIBOR+0.5%

23

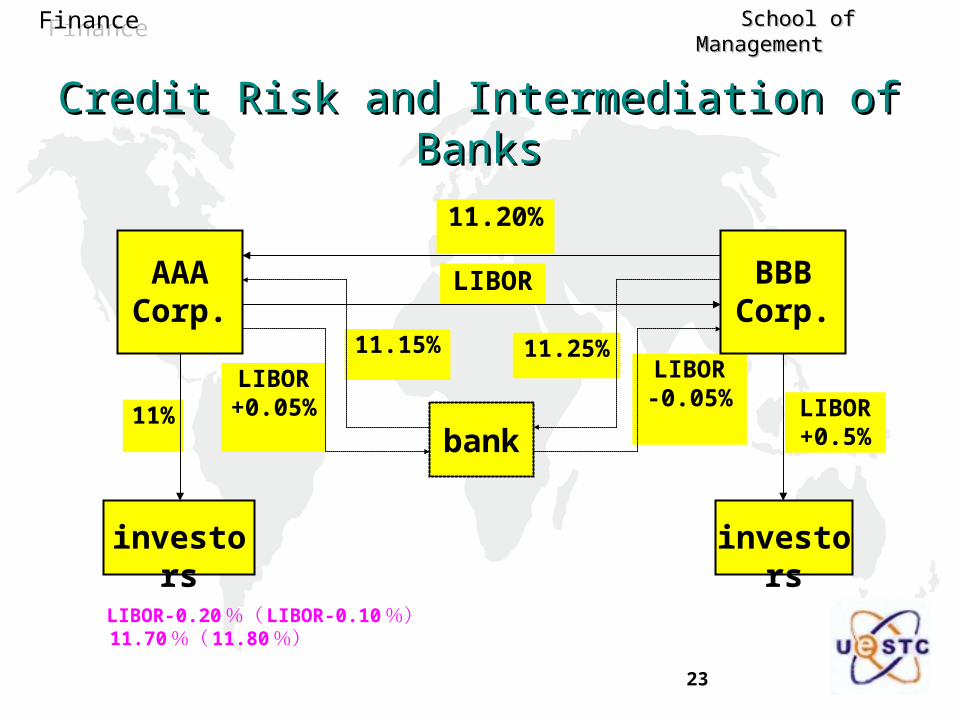

FinanceFinance School of Management School of Management

Credit Risk and Intermediation of BanksCredit Risk and Intermediation of Banks

LIBOR-0.20 %( LIBOR-0.10 %) 11.70 %( 11.80 %)

LIBOR+0.05%

LIBOR-0.05%

11%

11.25%11.15%

LIBORAAACorp.

BBBCorp.

investors investors

bank

11.20%

LIBOR+0.5%

24

FinanceFinance School of Management School of Management

Risk and Resource AllocationRisk and Resource Allocation

A scientist discovers a new drug designed to treat the common cold.

She requires $1,000,000 to develop, test and produce it. At this stage, the drug has a small probability of

commercial success. Using her own money or setting up a firm?

25

FinanceFinance School of Management School of Management

Risk and Resource AllocationRisk and Resource Allocation

risk pooling and sharing/specialization in the bearing of risks.

By allowing people to reduce their exposure to the risk of undertaking certain business ventures, the function of the financial system to facilitate the transfer of risks may encourage entrepreneurial behavior that can have a benefit to society.

26

FinanceFinance School of Management School of Management

Complete Markets for RiskComplete Markets for Risk

A world in which there exist such a wide range of institutional mechanisms that people can pick and choose exactly those risks they wish to bear and those they want to shed.

Kenneth Arrow, 1953

– A hypothetical, ideal world

– Limiting case for efficient risk allocation

– Separation: production and risk bearing

27

FinanceFinance School of Management School of Management

Acceleration of Financial InnovationsAcceleration of Financial Innovations

Insurance, stock, and future markets (400 yrs) Debt or equity: design of securities (400 yrs) The supply side New discoveries in telecommunications, information processing,

and finance theory have significantly lowered the costs of achieving global diversification and specialization in the bearing of risks.

The demand side Increased volatility of exchange rates, interest rates, and

commodity prices have increased the demand for ways to manage risk.

Complete markets: not possible

28

FinanceFinance School of Management School of Management

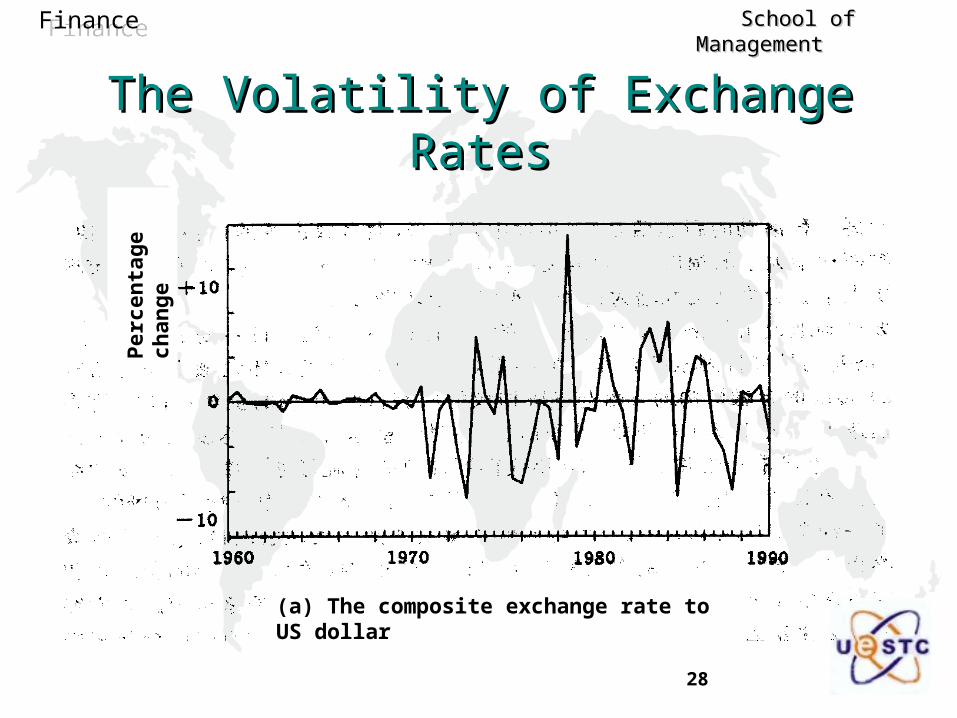

The Volatility of Exchange RatesThe Volatility of Exchange Rates

(a) The composite exchange rate to US dollar

Per

cen

tage

ch

ange

29

FinanceFinance School of Management School of Management

The Volatility of Interest RtesThe Volatility of Interest RtesC

han

ges

in b

asis

p

oin

ts

(b) The changes of rate of return on composite long-term investment grade bond

30

FinanceFinance School of Management School of Management

Real-world Limitations to Efficient Real-world Limitations to Efficient Risk AllocationRisk Allocation

Transactions costs Incentive problems

– moral-hazard: having insurance against some risk causes the insured party to take greater risk or to take less care in preventing the event that gives rise to the loss.

– adverse selection: those who purchase insurance against risk are more likely than the general population to be at risk

31

FinanceFinance School of Management School of Management

Three Dimensions of Risk TransferThree Dimensions of Risk Transfer

The simple way of risk transfer: selling the asset that makes the owner exposed to risk.

The three dimensions of risk transfer: hedging, insuring, and diversifying.

32

FinanceFinance School of Management School of Management

HedgingHedging

The action taken to reduce one’s exposure to a loss but also causing the hedger to give up the possibility of a gain.

Example: farmers Other examples

33

FinanceFinance School of Management School of Management

Insuring Insuring

Paying a premium to avoid losses but retaining the potential for gain.

Example: import/export business Other examples: health insurance, traveling to

Jiuzhaigou.

34

FinanceFinance School of Management School of Management

DiversifyingDiversifying

Holding similar amounts of many risky assets instead of concentrating all of your investment in only one.

Example: investing in the biotechnology business– initial capital: $100,000

– probability of success: 50%

– uncertainty: quadrupling the investment or losing the entire investment

– independence of successes

35

FinanceFinance School of Management School of Management

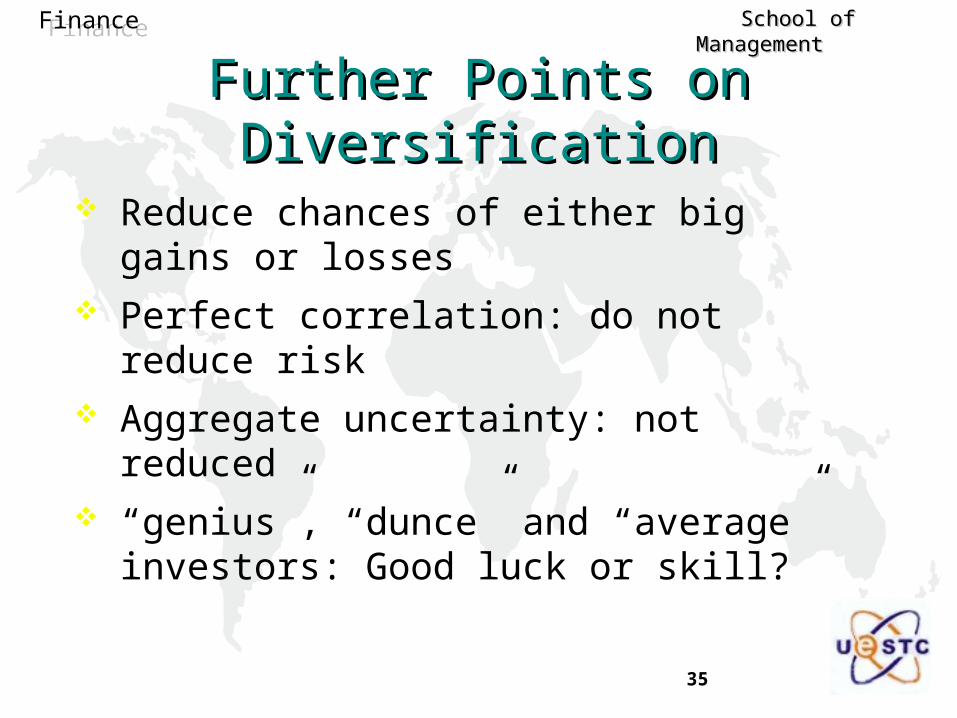

Further Points on DiversificationFurther Points on Diversification

Reduce chances of either big gains or losses Perfect correlation: do not reduce risk Aggregate uncertainty: not reduced “genius”, “dunce” and “average” investors: Good

luck or skill?

36

FinanceFinance School of Management School of Management

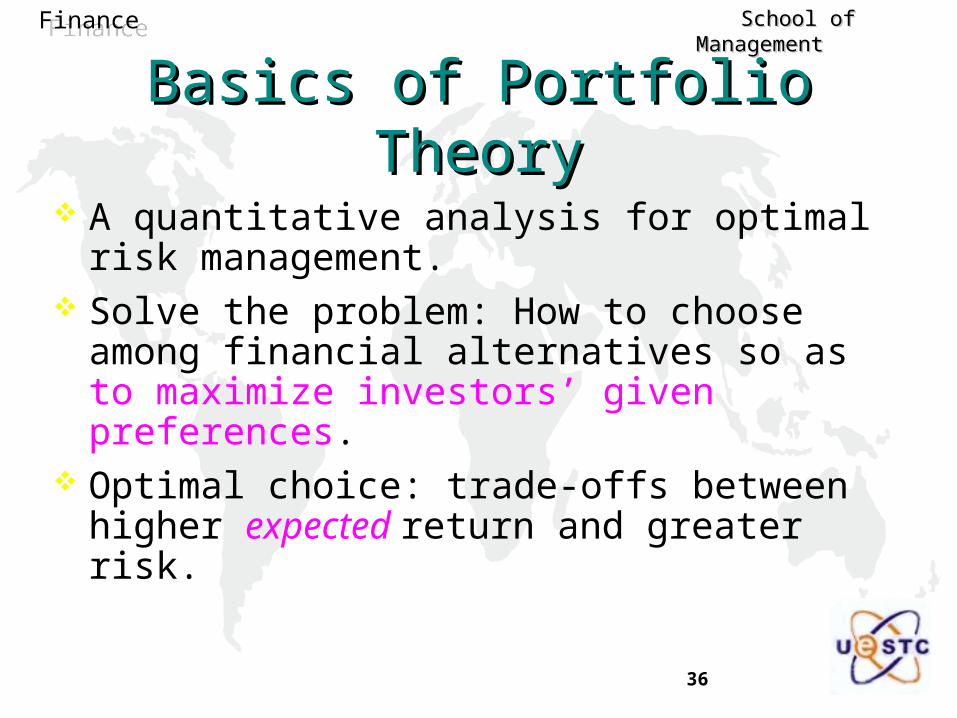

Basics of Portfolio TheoryBasics of Portfolio Theory

A quantitative analysis for optimal risk management. Solve the problem: How to choose among financial

alternatives so as to maximize investors’ given preferences.

Optimal choice: trade-offs between higher expected return and greater risk.

37

FinanceFinance School of Management School of Management

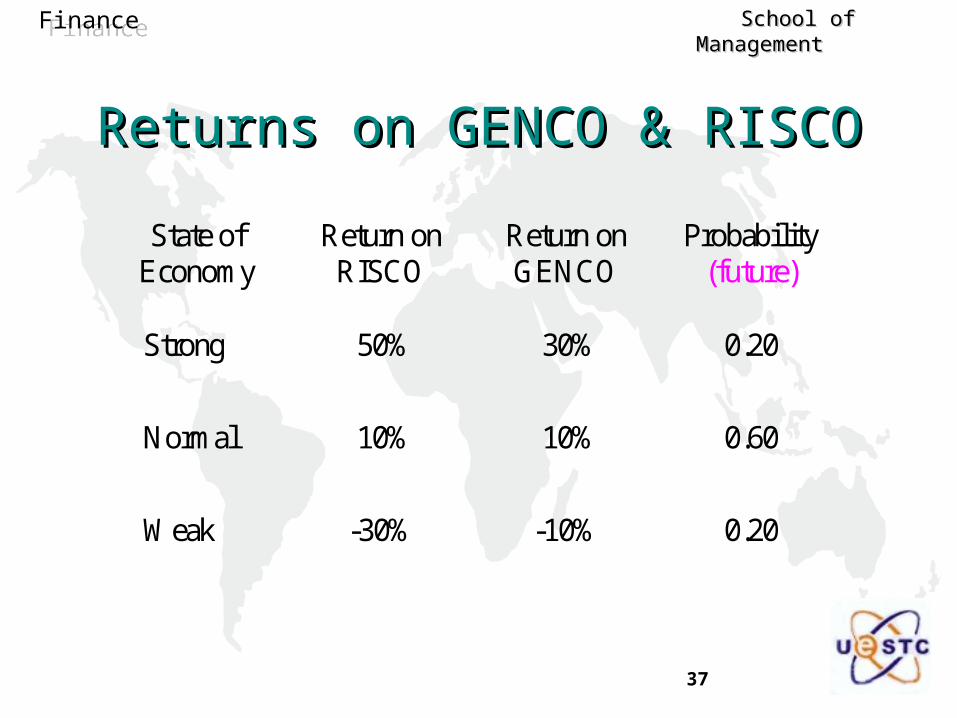

Returns on GENCO & RISCOReturns on GENCO & RISCO

State of Economy

Return on RISCO

Return on GENCO

Probability (future)

Strong 50% 30% 0.20

Normal 10% 10% 0.60

Weak -30% -10% 0.20

38

FinanceFinance School of Management School of Management

50%30%

10%-10%

-30%

Risco

Genco0

0.1

0.2

0.3

0.4

0.5

0.6

Probability

Return

Probability Distributions of Returns of Genco and Risco

Return Distribution: GraphReturn Distribution: Graph

39

FinanceFinance School of Management School of Management

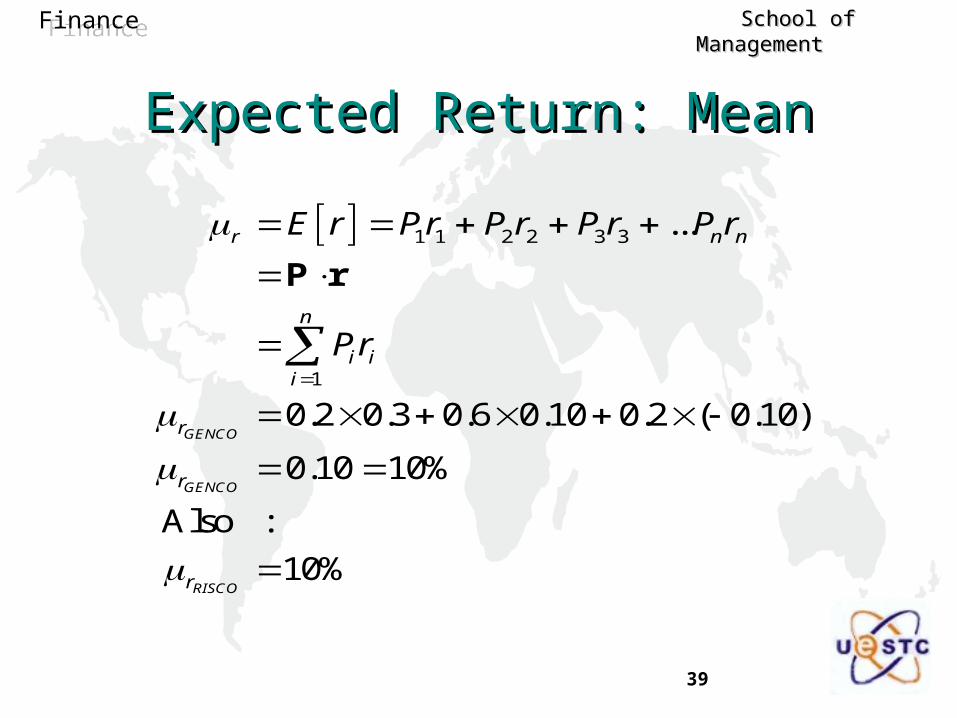

Expected Return: MeanExpected Return: Mean

1 1 2 2 3 3

1

...

0.2 0.3 0.6 0.10 0.2 ( 0.10)

0.10 10%

Also :

10%

GENCO

GENCO

RISCO

r n n

n

i ii

r

r

r

E r Pr P r P r P r

Pr

P r

40

FinanceFinance School of Management School of Management

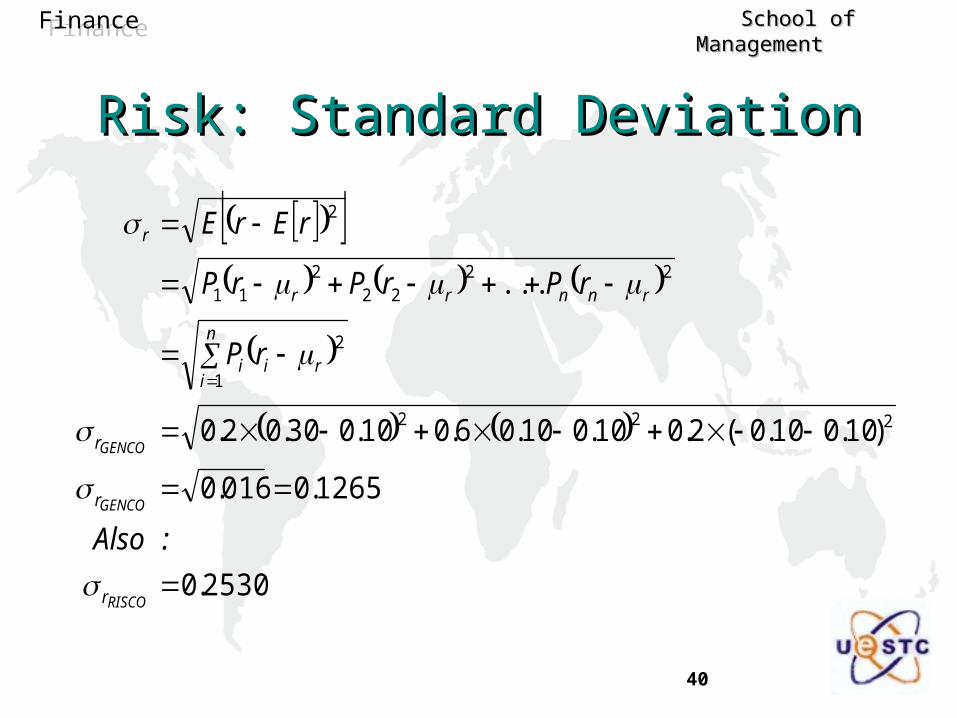

Risk: Standard DeviationRisk: Standard Deviation

2530.0

1265.0016.0

)10.010.0(2.010.010.06.010.030.02.0

...

222

1

2

2222

211

2

RISCO

GENCO

GENCO

r

r

r

n

irii

rnnrr

r

: Also

rP

rPrPrP

rErE

41

FinanceFinance School of Management School of Management

VolatilityVolatility

Standard deviation of returns. A measure of risk (or uncertainty): The first risk

measure (Markowitz, 1952). Volatility is 0: no risk; future return certain. Larger volatility => wider range of returns => more

uncertain (greater risk).

42

FinanceFinance School of Management School of Management

Probability Distribution of ReturnProbability Distribution of Return

Observables: history of prices or returns. Past implies future. Computable: mean & standard deviation. Unknown: distribution of probability. Assumption: Normal distribution of return (from discrete

to continuous). Accuracy depends on assumption!

43

FinanceFinance School of Management School of Management

Distribution of Returns on Two Stocks

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

-100% -50% 0% 50% 100%

Return

Pro

bab

ilit

y D

ensi

ty

NORMCO

VOLCO

44

FinanceFinance School of Management School of Management

Two More Return Densities.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-100.00% -50.00% 0.00% 50.00% 100.00%

Return.

Pro

bab

ilit

y D

ensi

ty.

VOLCO

ODDCO

45

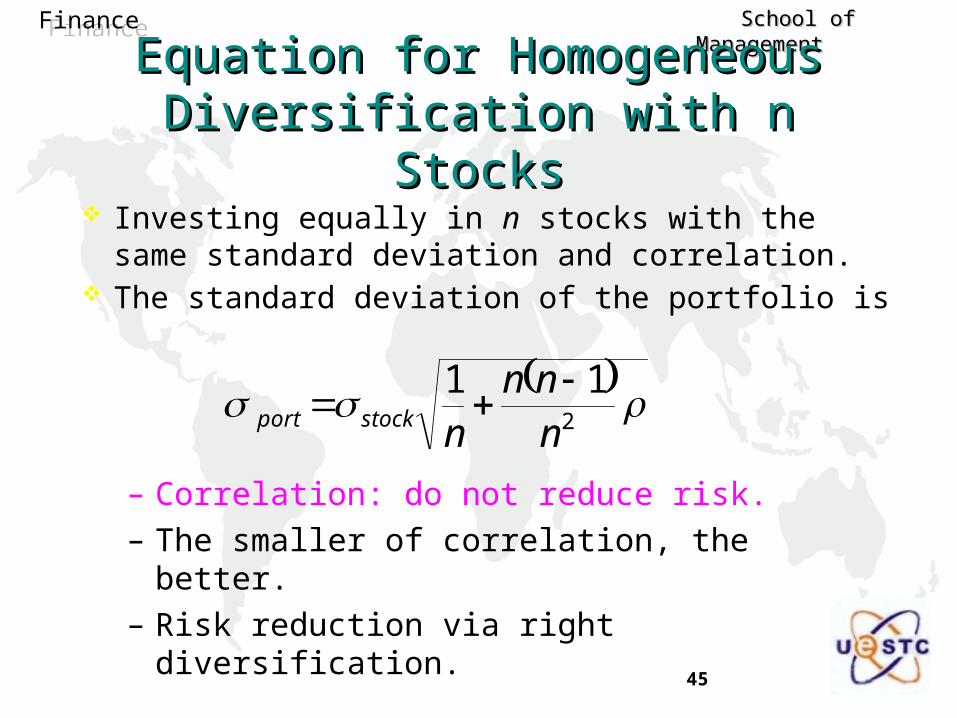

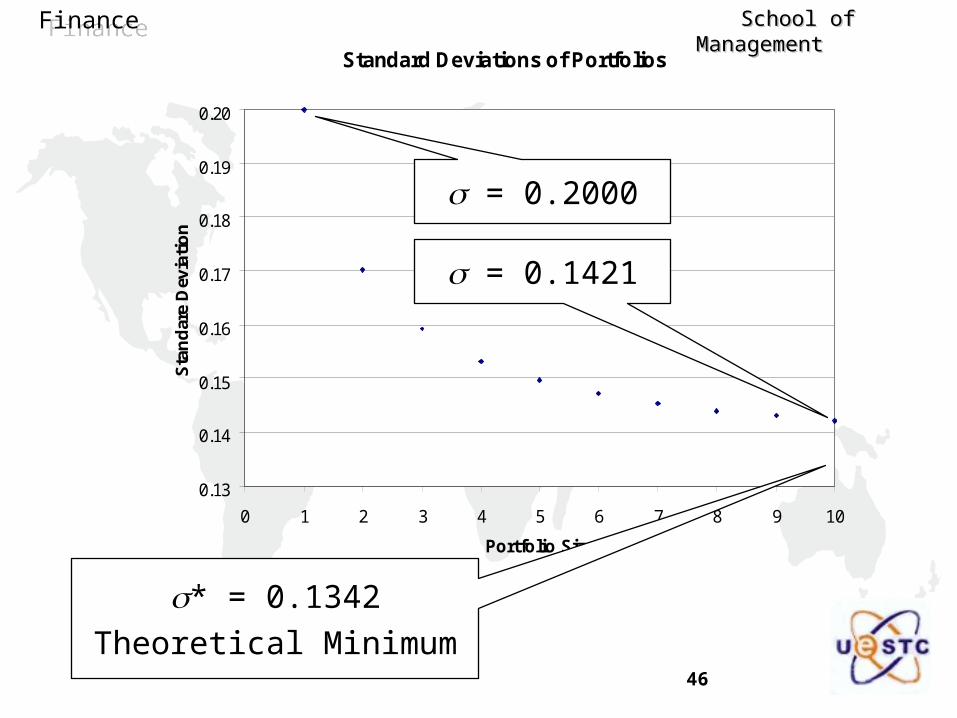

FinanceFinance School of Management School of Management

2

11nnn

nstockport

Equation for Homogeneous Equation for Homogeneous Diversification with n StocksDiversification with n Stocks

Investing equally in n stocks with the same standard deviation and correlation.

The standard deviation of the portfolio is

– Correlation: do not reduce risk.

– The smaller of correlation, the better.

– Risk reduction via right diversification.

46

FinanceFinance School of Management School of Management

Standard Deviations of Portfolios

0.13

0.14

0.15

0.16

0.17

0.18

0.19

0.20

0 1 2 3 4 5 6 7 8 9 10

Portfolio Size

Sta

nd

are

Dev

iati

on

= 0.2000

= 0.1421

* = 0.1342

Theoretical Minimum

47

FinanceFinance School of Management School of Management

Summary: Main PointsSummary: Main Points

Risk: bad uncertainty Risk aversion: prefer lower risk Risk measure: volatility Portfolio: many components Risk mgmt: reduce risks at a reasonable cost Hedge, insure, diversify