1 economic environment: weathering the storm? the fairfield county economy, the year ahead december...

TRANSCRIPT

1

Economic Environment: Economic Environment:

Weathering the Storm?Weathering the Storm?

The Fairfield County Economy, The Fairfield County Economy, The Year AheadThe Year Ahead

December 7, 2005 Todd P. Martin Economic Services203-218-9825 [email protected]

2

US Economic Backdrop US Economic Backdrop

• Economic growth remains respectable despite headwinds of Hurricanes, higher energy prices, and rising interest rates. Real GDP should slow to approximately a 3% pace next year.

• The Fed will continue to gradually tightening monetary policy to a “neutral” posture. The targeted fed funds rate is expected to rise to 4.5% by early 2006 (up from 1.0% in June 2004). Ben Bernanke replaces Alan Greenspan as chairman in late January.

• The yield curve continues to flattened as 10-year T-note yields have remained relatively low while short-term rates are up 300 BPs. Long-term yield should move from 4.50% currently to 5.0% by early 2006.

• Core Inflation remains contained, but future price concerns are heightening.

• Risks: Iraq - terrorism - energy prices – interest rates – housing bubble? – Longer-Term: growing budget & trade deficits – consumer leverage

3

The Fed will tighten a bit more “The cumulative rise in energy and other costs has

the potential to add to inflation pressures; however, core inflation has been relatively low in recent months and longer-term inflation expectations remain contained.”

“With underlying inflation expected to be contained, the Committee believes that policy accommodation can be removed at a pace that is likely to be measured.”

Federal Open Market Committee Press Release – 1101/05

4

Smooth Transition at the Fed?

Alan Greenspan Ben Bernanke

Wall Street Journal

Release Date: October 24, 2005

Statement by Federal Reserve Board Chairman Alan Greenspan:

"The President has made a distinguished appointment in Ben Bernanke. Ben comes with superb academic credentials and important insights into the ways our economy functions. I have no doubt that he will be a credit to the nation as Chairman of the Federal Reserve Board."

5

Monetary policy works with a lag of 6-18 monthsMonetary policy works with a lag of 6-18 months

Source: Bloomberg, Federal Reserve,TPM Economic Services

Targeted Fed Funds Rate vs. 10-year T-Note & 30-year Mortgage Yields

0

1

2

3

4

5

6

7

8

9

10

Fed Funds

10-Year T-Note

30-Year Mortgage

6

The economy expanded at a 4.3% pace in the 3rd Q ‘05The economy expanded at a 4.3% pace in the 3rd Q ‘05

Source: The Conference Board, BEA,TPM Economic Services

Gross Domestic Product (CW$)

Transformation: %Chg, AR Source: Bureau of Economic Analysis

-2

0

2

4

6

8

95 96 97 98 99 00 01 02 03 04 05

7

Jobless Claims suggest continued job growthJobless Claims suggest continued job growth

Source: Bloomberg, BLS, TPM Economic Services

US Weekly Initial Jobless Claims - 4 week MA

200.0

250.0

300.0

350.0

400.0

450.0

500.0

550.0Jan-89

Aug-89

Mar-90

Oct-90

May-91

Nov-91

Jun-92

Jan-93

Aug-93

Mar-94

Oct-94

May-95

Dec-95

Jul-9

6Jan-97

Aug-97

Mar-98

Oct-98

May-99

Dec-99

Jul-0

0Feb-01

Sep-01

Apr-02

Nov-02

May-03

Dec-03

Jul-0

4Feb-05

Sep-05

Spike due to Katrina – trend intact

Similar Pattern to early 1990s?

8

CT Economic OutlookCT Economic Outlook

• Connecticut’s economic rebound has lagged the national recovery. While job growth has improved recently, CT employment is still down 25,400 from mid-2000. CT is the only state that hasn’t seen job growth from 1989.

• According to NEEP, the state should add 18,200 jobs in 2005 and 17,600 in 2006. The Unemployment rate has moved above national average.

• Fairfield County’s economic performance is strong, but long-term viability is threatened by high cost of living, transportation woes, and energy issues.

• Housing remains very strong in the state. Housing permits totaled 11,837 in 2004 -- the strongest since 1989. Not overbuilt like the late 1980s.

• CT vulnerable to national (and global) economy, higher interest rates, energy prices, high cost of living, and complacency

9

CT is still down 25,400 jobs from July 2000 peakCT is still down 25,400 jobs from July 2000 peak

Source: CT Labor Department, BLS, TPM Economic Services

Connecticut, Employment, Total Nonagricultural

Transformation: Level Source: Bureau of Labor Statistics

1500

1550

1600

1650

1700

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

[Thousands]

Up 36,000 jobs from Sept. 2003 low

10

Other states have more than regained jobs lostOther states have more than regained jobs lost

Source: The Conference Board, BLS, TPM Economic Services

[Thousands]NH, RI & NJ Non-Farm Employment

New Hampshire Rhode Island New Jersy

NH &

RI T

hous

ands

NJ T

hous

ands

400.00

450.00

500.00

550.00

600.00

650.00

3000

3500

4000

4500

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

11

CT Employment growth performance sub-parCT Employment growth performance sub-par

YOY% Change in payroll employment (Sept. 2005 vs. Sept. 2004)

0.3

0.91.0

1.11.2 1.2

1.3

1.8

2.1

1.6

0.0

0.5

1.0

1.5

2.0

2.5

MA ME NY CT NJ RI PA VT NH US

Source: CT Labor Dept., TPM Economic Services

12

CT unemployment above US Rate - first time in 8 yearsCT unemployment above US Rate - first time in 8 years

Source: CT Labor Department, BLS, TPM Economic Services

Unemployment Rate CT vs. US

Unemployment Rate CT Unemployment Rate US

2

3

4

5

6

7

00 01 02 03 04 05

% of labor force (SA)

13

Fairfield County Unemployment rates very lowFairfield County Unemployment rates very low

CT Unemployment Rates % Bridgeport-Stamford LMA - Oct. 2005

3.3 3.4 3.4 3.5 3.5 3.5 3.6 3.7 3.8 3.8 3.8 3.9 3.9 3.9 4.0 4.0 4.1 4.2 4.2 4.44.7

5.65.9

6.3

7.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Source: CT Labor Dept., TPM Economic Services

14

CT Construction sector has seen strongest growthCT Construction sector has seen strongest growth

Source: CT Labor Department, BLS, TPM Economic Services

Connecticut, Employment, Construction

Transformation: Level Source: Bureau of Labor Statistics

40

50

60

70

80

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

[YOY Change - Thousands]

15

CT FIRE employment - continued consolidationCT FIRE employment - continued consolidation

Source: CT Labor Department, BLS, TPM Economic Services

Connecticut, Employment, Finance, Insurance, Real Estate

Transformation: Level Source: Bureau of Labor Statistics

125

135

145

155

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

[Thousands]

16

Where CT has lost jobs over the last 12 monthsWhere CT has lost jobs over the last 12 months

-700

-500

-400

-300

-200

-200

-200

-100

-100

-100

-100

-100

-1000 -900 -800 -700 -600 -500 -400 -300 -200 -100 0

Other Retail

Insurance

Computer & Electronic Product

Other Non-Durable Goods

Machinery

Printing & Related

Utilities

Other Durable Goods

Plastics & Rubber

Motor Vehicle & Parts Dealers

Information

Arts, Ent. & Recreation

Change in CT Non-Farm Employment Oct. 2005 vs. Oct. 2004 ( Not SA)

Source: CT Labor Department, TPM Economic Services

17

Where jobs were created last yearWhere jobs were created last year

100

100

200

300

400

400

400

500

500

500

600

700

800

900

1,000

1,300

1,300

2,2003,400

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Fabricated Metal

Food & Beverage Stores

Other Financial

Other Services

Transportation Equipment

Credit Intermediation

Real Estate & Rental & Leasing

Building Materials

General Merchandise

State Gov.

Professional & Business Services

Educational Services

Accommodation & Food Services

Securities & Commodity

Local Gov.

Wholesale Trade

Transportation & Warehousing

Health Care & Social Assistance

Construction & Mining

Change in CT Non-Farm Employment Oct. 2005 vs. Oct. 2004 ( Not SA)

Source: CT Labor Department, TPM Economic Services

18

Sectors with largest % change last yearSectors with largest % change last year

-2.60%

-2.40%

-2.30%

-1.70%

-1.30%

-1.10%

-0.80%

-0.80%

-0.40%

-0.40%

-0.40%

-0.30%

-3.0% -2.5% -2.0% -1.5% -1.0% -0.5% 0.0%

Computer & Electronic Product

Printing & Related

Utilities

Other Non-Durable Goods

Plastics & Rubber

Machinery

Other Retail

Insurance

Motor Vehicle & Parts Dealers

Arts, Ent. & Recreation

Other Durable Goods

Information

% Change in CT Non-Farm Employment Oct. 2005 vs. Oct. 2004 ( Not SA)

Source: CT Labor Department, TPM Economic Services

19

Sectors with the strongest % job growthSectors with the strongest % job growth

0.30%

0.30%

0.50%

0.60%

0.80%

0.80%

0.90%

1.00%

1.30%

1.30%

1.90%

2.00%

2.00%

3.10%

3.10%

4.30%

4.80%

4.80%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Fabricated Metal

Professional & Business Services

Other Services

Local Gov.

Accommodation & Food Services

State Gov.

Transportation Equipment

Health Care & Social Assistance

Credit Intermediation

Educational Services

General Merchandise

Real Estate & Rental & Leasing

Wholesale Trade

Transportation & Warehousing

Building Materials

Other Financial

Securities & Commodity

Construction & Mining

% Change in CT Non-Farm Employment Oct. 2005 vs. Oct. 2004 ( Not SA)

Source: CT Labor Department, TPM Economic Services

20

Job gains & losses in SW CT – last 12 mo. Job gains & losses in SW CT – last 12 mo.

-1,100

-500

-200

-100

0

100

200

200

700

800

1,200

1,300

-1,500 -1,000 -500 0 500 1,000 1,500

MANUFACTURING

PROFESSIONAL & BUSINESS SERVICES

Wholesale Trade

Transportation, Warehousing, & Utilities

INFORMATION

CONSTRUCTION

Retail Trade

OTHER SERVICES

LEISURE AND HOSPITALITY

FINANCIAL ACTIVITIES

GOVERNMENT

EDUCATIONAL AND HEALTH SERVICES

Change in Employment, Bridgeport-Stamford LMA – Oct. 2005 vs. Oct. 2004 - NSA

Source: CT Labor Department, TPM Economic Services

21

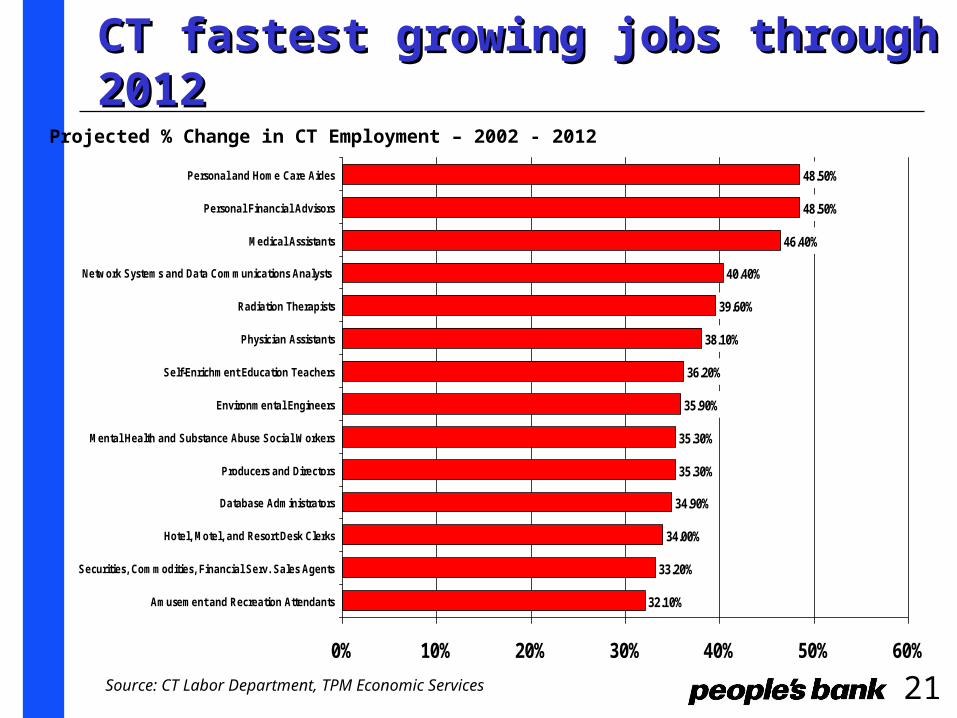

CT fastest growing jobs through 2012 CT fastest growing jobs through 2012

32.10%

33.20%

34.00%

34.90%

35.30%

35.30%

35.90%

36.20%

38.10%

39.60%

40.40%

46.40%

48.50%

48.50%

0% 10% 20% 30% 40% 50% 60%

Amusement and Recreation Attendants

Securities, Commodities, Financial Serv. Sales Agents

Hotel, Motel, and Resort Desk Clerks

Database Administrators

Producers and Directors

Mental Health and Substance Abuse Social Workers

Environmental Engineers

Self-Enrichment Education Teachers

Physician Assistants

Radiation Therapists

Network Systems and Data Communications Analysts

Medical Assistants

Personal Financial Advisors

Personal and Home Care Aides

Projected % Change in CT Employment – 2002 - 2012

Source: CT Labor Department, TPM Economic Services

22

CT jobs with largest growth through 2012CT jobs with largest growth through 2012

2,360

2,469

2,475

2,495

2,548

2,583

2,678

3,045

3,106

3,751

4,306

4,399

4,460

5,248

0 1,000 2,000 3,000 4,000 5,000 6,000

Receptionists and Information Clerks

Landscaping and Groundskeeping Workers

Social and Human Service Assistants

Computer Systems Analysts

Teacher Assistants

Accountants and Auditors

Personal and Home Care Aides

Combined Food Preparation and Serving Workers

Janitors & Cleaners, exc.Maids, Housekeeping Cleaners

Customer Service Representatives

Waiters and Waitresses

Retail Salespersons

Cashiers

Registered Nurses

Projected Change in CT Employment – 2002 - 2012

Source: CT Labor Department, TPM Economic Services

23

Highest paid, fastest growing CT occupationsHighest paid, fastest growing CT occupations

$65,718

$65,915

$67,642

$67,995

$70,658

$72,051

$73,091

$74,818

$77,584

$85,842

$107,078

$111,779

$129,667

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000

Producers and Directors

Architects, Except Landscape and Naval

Network & Computer Systems Administrators

Environmental Engineers

Computer Systems Analysts

Network Systems and Data Communications Analysts

Physician Assistants

Computer Software Engineers, Applications

Computer Software Engineers, Systems Software

Medical Scientists, Except Epidemiologists

Personal Financial Advisors

Computer and Information Systems Managers

Securities, Commodities, Financial Serv. Sales Agents

Microbiologists

Biochemists and Biophysicists

Average CT Salaries in 2003

Source: CT Labor Department, TPM Economic Services

Salaries N/A

24

Housing is booming – Is there a Bubble?Housing is booming – Is there a Bubble?

Source: Conference Board, Census Bureau, TPM Economic Services

Housing Sales, New and Existing Homes

Transformation: Level Source: Bureau of the Census

3

4

5

6

7

8

9

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

25

Overvalued Housing MarketsOvervalued Housing Markets

Source: Wall Street Journal, PMI Mtg. Insurance Co.

Home prices, percent overvalued relative to long-term trend

33.7%

31.3%

27.4%

25.6%

25.5%

25.5%

23.2%

22.2%

22.0%

20.5%

20.4%

19.6%

19.6%

19.5%

19.1%

18.5%

18.2%

30.7%

26.4%

26.5%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0%

Los Angeles-Long Beach, Calf.

Sacramento-Arden, Calf.

Riverside-San Bernadino, Calf.

Edison, N.J .

Oakland-Freemont-Hayward, Calf.

San J ose-Sunnyvale-Santa Calra, Calf.

Newark-Union, N.J .

Santa Ana-Anaheim-Irvine, Calf.

Las Vegas, Nev.

Tampa-St. Petersburg-C learwater, Fla.

San Diego-Carlsbad-San Marcos, Calf.

Phoenix-Mesa-Scottsdale, Ariz

Miami-Miami Beach-Kendall, Fla.

Nassau-Suff olk, N.Y .

Fort Lauderdale-Pompano Beach, Fla.

Orlando, Fla.

San Fransico-San Mateo, Calf.

Providence, R.I./New Bedford-Fall River, Mass.

Virgina Beach-Norfolk-Newport News, Va.

Washington, DC/Arlington-Alexandria, Va.

26

Riskiest Housing MarketsRiskiest Housing Markets

Source: Wall Street Journal, PMI Mtg. Insurance Co.

Risk Index = biggest chance of housing price declines over the next two years

93

111

197

232

236

288

362

440

456

460

464

466

472

502

522

532

536

133

201

206

0 100 200 300 400 500 600

Phoenix-Mesa-Scottsdale, Ariz

Orlando, Fla.

Virgina Beach-Norfolk-Newport News, Va.

Las Vegas, Nev.

Tampa-St. Petersburg-C learwater, Fla.

Miami-Miami Beach-Kendall, Fla.

Newark-Union, N.J .

Washington, DC/Arlington-Alexandria, Va.

Fort Lauderdale-Pompano Beach, Fla.

Edison, N.J .

San Fransico-San Mateo, Calf.

Sacramento-Arden, Calf.

Los Angeles-Long Beach, Calf.

Providence, R.I./New Bedford-Fall River, Mass.

Riverside-San Bernadino, Calf.

San J ose-Sunnyvale-Santa Calra, Calf.

Oakland-Freemont-Hayward, Calf.

Santa Ana-Anaheim-Irvine, Calf.

Nassau-Suff olk, N.Y .

San Diego-Carlsbad-San Marcos, Calf.

27

Housing still affordable, but falls to 14 year lowHousing still affordable, but falls to 14 year low

Source: Conference Board, WEFA, NAR, TPM Economic Services

Index, Housing Affordability

Transformation: Level Source: WEFA, NAR

100

110

120

130

140

150

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

28

Housing is not overbuild like the mid-1980sHousing is not overbuild like the mid-1980s

Source:CT DECD, New England Economic Partnership, TPM Economic Services

Total housing permits authorized in CT in units

16,9

27 19,3

92

26,2

4630

,163

27,4

15

19,5

47

11,9

70

7,58

0

7,48

0

8,01

09,

250

9,46

0

8,55

0

8,53

7

9,31

1 11,8

6310

,637

9,37

6

9,29

0

9,73

1

10,4

35

11,8

37

11,9

3511

,442

9,60

6

10,0

24

10,7

05

0.0

5,000.0

10,000.0

15,000.0

20,000.0

25,000.0

30,000.0

35,000.01983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2005-2009 is forecast

29

Fairfield County Permits up about 5.5% YTDFairfield County Permits up about 5.5% YTD

-60%

-53%

-39%

-26%

-24%

-19%

-19%

-8%

11%

12%

26%

43%

47%

48%

77%

80%

-80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

Bethel

Norwalk

Trumbull

Stratford

Newtown

Ridgefield

Fairfield

Westport

Danbury

New Canaan

Greenwich

Easton

Stamford

Monroe

Shelton

Bridgeport

% Change in Housing Permits Authorized (Jan-Oct 2005 vs. Jan-Oct 2004)

Source: CT DECD, TPM Economic Services

Excludes: Brookfield, Darien, New Fairfield, Redding, Sherman, Weston & Wilton

30

Teardowns in Fairfield

31

Teardowns in Fairfield (cont.)

32

Teardowns in Fairfield (cont.)

33

Teardowns in Fairfield (cont.)

34

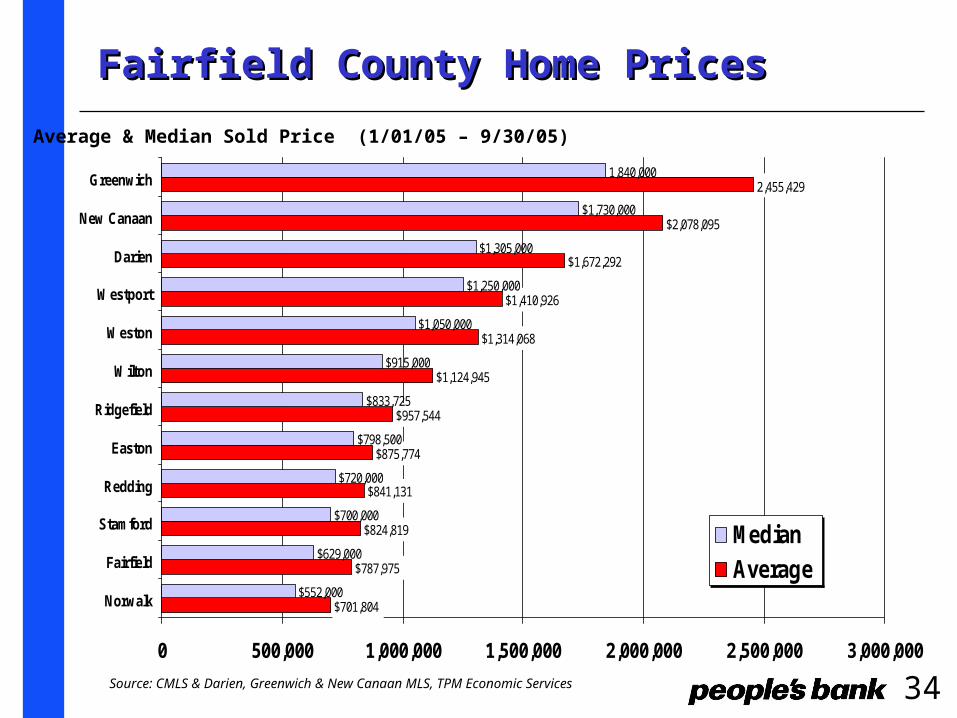

Fairfield County Home PricesFairfield County Home Prices

$701,804

$787,975

$824,819

$841,131

$875,774

$957,544

$1,124,945

$1,314,068

$1,410,926

$1,672,292

$2,078,095

2,455,429

$552,000

$629,000

$700,000

$720,000

$798,500

$833,725

$915,000

$1,050,000

$1,250,000

$1,305,000

$1,730,000

1,840,000

0 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

Norwalk

Fairfield

Stamford

Redding

Easton

Ridgefield

Wilton

Weston

Westport

Darien

New Canaan

Greenwich

Median

Average

Average & Median Sold Price (1/01/05 – 9/30/05)

Source: CMLS & Darien, Greenwich & New Canaan MLS, TPM Economic Services

35

Fairfield County Home PricesFairfield County Home Prices still rising still rising

7%

7%

10%

10%

11%

12%

12%

13%

15%

17%

17%

36%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Greenwich

Westport

Redding

Wilton

Stamford

Darien

Ridgefield

Easton

Fairfield

New Canaan

Norwalk

Weston

Average % change in sold price (Jan-Sept 2005 vs. Jan-Sept 2004)

Source: CMLS & Darien, Greenwich & New Canaan MLS, TPM Economic Services

36

Transportation is a major concern

37

Impact of Higher Energy Costs

38

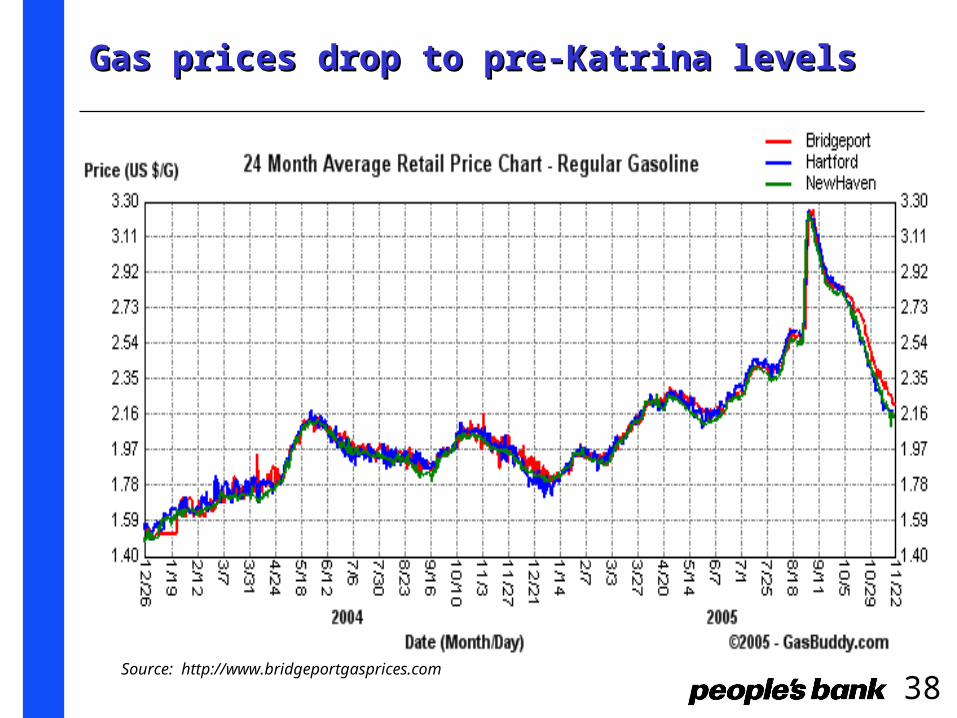

Gas prices drop to pre-Katrina levels Gas prices drop to pre-Katrina levels

Source: http://www.bridgeportgasprices.com

39

Tax revenues total $2.6 billion YTDTax revenues total $2.6 billion YTD

Source: State of CT Dept. of Revenue Services

Year-to-Date CT Tax Revenues ( FY 05-06, July – Oct. $millions)

$55,867

$75,369

$837,055

$2,609,229

$173,509

$1,125,550

$0 $500,000 $1,000,000 $1,500,000 $2,000,000 $2,500,000 $3,000,000

Real Estate Conv.

Petroleum Gross Earnings

Corp & Public Service

Sales & Use

Income

Total

+$210 million, or 8.8%

+$73.5 million or 7.0%

+$29.6 million or 3.7%

+$26.4 million or 26.4%

+$30.1 million or 66.4%

+$10.3 million or 22.5%

40

Focus on the Big Picture

Ten Forces Flattening The World1. 11/9/892. 8/9/953. Work Flow Software4. Open-Sourcing5. Outsourcing6. Offshoring7.Supply-Chaining 8. Insourcing9. In-Forming10. The Steroids

41

CERC Benchmarking Study

• How is Connecticut Positioned in terms of Competitiveness & Innovation in the Knowledge Economy?

• Connecticut Economy at a critical juncture:– Currently scores well in productivity, educated workforce, technology,

etc.

– Losing grounds to other states, urban/suburban disparities, aging population, slow business & job growth, University R&D, etc.

For more information, please see: www.cerc.com/benchmarks

42

SummarySummary• US Economic growth is expected to moderate to 3.0% - 3.5% in

2006 (Hurricanes, energy, interest rates) – job growth improving, but remains sub-par, Inflation pressures building

• Fed moving short-term interest rates toward ‘neutrality’

• Connecticut job growth has lagged the US – NEEP expects 18,200 jobs in 2005. Rising taxes, higher costs, scandals have not helped recovery. Budget battles will continue – 2006 Election Year .

• Fairfield County: remarkably prosperous – Longer-term challenges: transportation, affordable housing, energy problems, high business costs, dealing successfully with the ‘Flattening World’

43

Economic Environment: Economic Environment:

Weathering the Storm?Weathering the Storm?

The Fairfield County Economy, The Fairfield County Economy, The Year AheadThe Year Ahead

December 7, 2005 Todd P. Martin Economic Services203-218-9825 [email protected]