1 econ 102 the canadian economy chapter 1 the economic problem copyright © 2002 by mcgraw-hill...

Post on 19-Dec-2015

215 views

TRANSCRIPT

1

Econ 102 The Canadian Economy

Chapter 1The Economic Problem

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

2

Chapter Objectives

In this chapter, you will:consider the economic problem that underlies

the definition of economics; learn about the way economists specify

economic choice;examine the production choices an entire

economy faces, as demonstrated by the production possibilities model;

analyze the three basic economic questions and how various economic systems answer them.

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

3

Outline of Topics

1.1 What Economists Do 1.2 Economic Choice 1.3 The Production Possibilities Model 1.4 Economic Systems

4

1.1 What Economists Do The Economic Problem

Economists deal with the economic problem. Economic agents must continually make

choices. Their wants are unlimited. They face a limited supply of economic

resources. Economic resources

including natural, capital, and human resources ( see Definitions on page 3)

5

1.1 What Economists Do Economics Defined

Economics is the study of how to distribute scarce resources among competing ends.Microeconomics focuses on individual

consumers and businesses.Macroeconomics takes a broad view

of the economy.

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

6

1.1 What Economists Do Economic Models

Economic models:simplify economic realityshow how dependent variables are affected by

independent variables include inverse and/or direct relationships incorporate a variety of assumptions such as ceteris

paribusare classified as part of either positive economics

or normative economics (See Definitions on page 5 & 6)

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

7

1.2 Economic Choice Utility Maximization

Economists assume that economic decision-makers maximize their own utility.Utility: the satisfaction gained from any

actionDecision-makers must keep in mind the

opportunity cost of each alternative.Opportunity cost: the utility that could

have been gained by choosing an action’s best alternative.

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

8

1.3 The Production Possibilities Model

The production possibilities model is based on three assumptions:an economy makes only two products resources and technology are fixedall resources are employed to their fullest

capacity

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

9

1.3 The Production Possibilities Model The Production Possibilities Curve (a)

The production possibilities curve shows a range of possible output combinations for an economy. It highlights the scarcity of resources. It has a concave shape, which reflects the

law of increasing opportunity costs.

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

10

The Production Possibilities Curve (b)

Figure 1.1, page 8

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

Production Possibilities Schedule

Hamburgers Computers point on graph

Production Possibilities Curve

0 1 2 3

1000

600

b

c

1000 0 a

900 1 b

600 2 c

0 3 d Computers

Ham

bur

gers

e

f

inefficient

unattainable

d

900

a

11

The Law of Increasing Opportunity CostsFigure 1.2, page 10

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

Production Possibilities Schedule

Hamburgers Opportunity Computers point Cost of on graph Computers

Production Possibilities Curve

0 1 2 3

1000

6001000 0

a 100

900 1 b

300

600 2 c

600

0 3 d Computers

Ham

bur

gers

As the quantityof computers

rises, so does theiropportunity cost.

a

b900

c

d

12

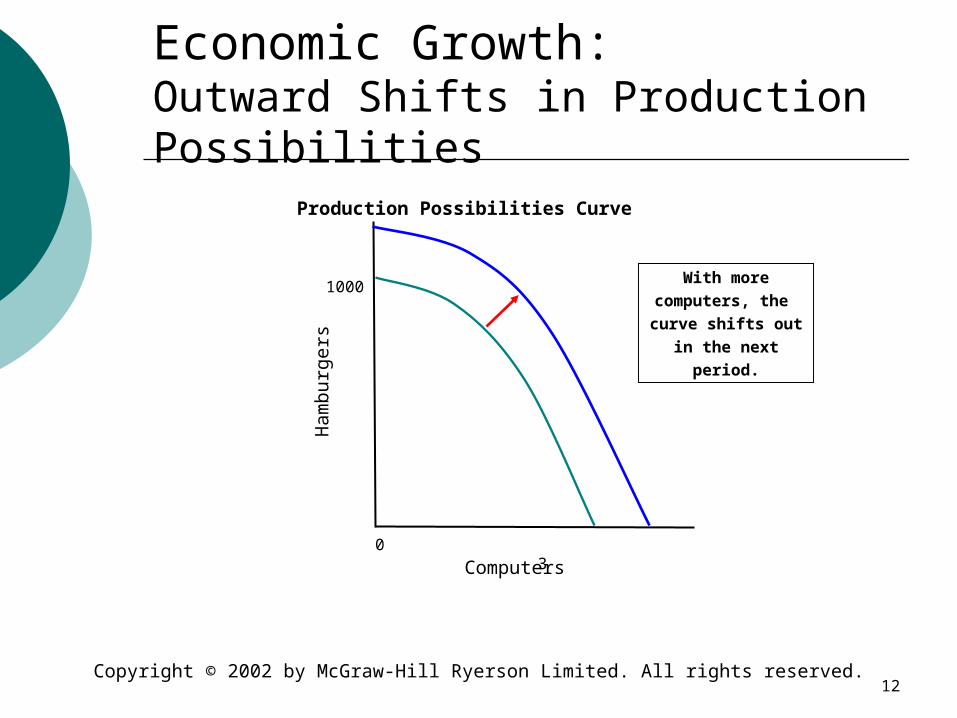

Economic Growth:Outward Shifts in Production Possibilities

Production Possibilities Curve

0 3

1000

Computers

Ham

bur

gers

With morecomputers, the curve shifts out

in the nextperiod.

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

13

1.4 Economic Systems

Economic Systems: the organization of an economy, which represents a country’s distinct set of social customs, political institutions, and economic practicesThe Basic Economic Questions: There are three basic questions any society must answer:what to producehow to produce for whom to produce

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

14

1.4 Economic Systems

There are three systems to choose from: Traditional Economy: an economic system in

which economic decisions are made on the basis of custom.

Traditional economies focus on non-economic concerns and have tight social constraints.

15

1.4 Economic Systems

Market Economy: an economic system based on private ownership and the use of markets in economic decision-making

Market economies are consumer-centered and innovative but create inequality and instability.

Benefits: Consumer sovereignty: the decision of what to

produce is ultimately guided by the needs and wants of household in their role as consumers

InnovationCopyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

16

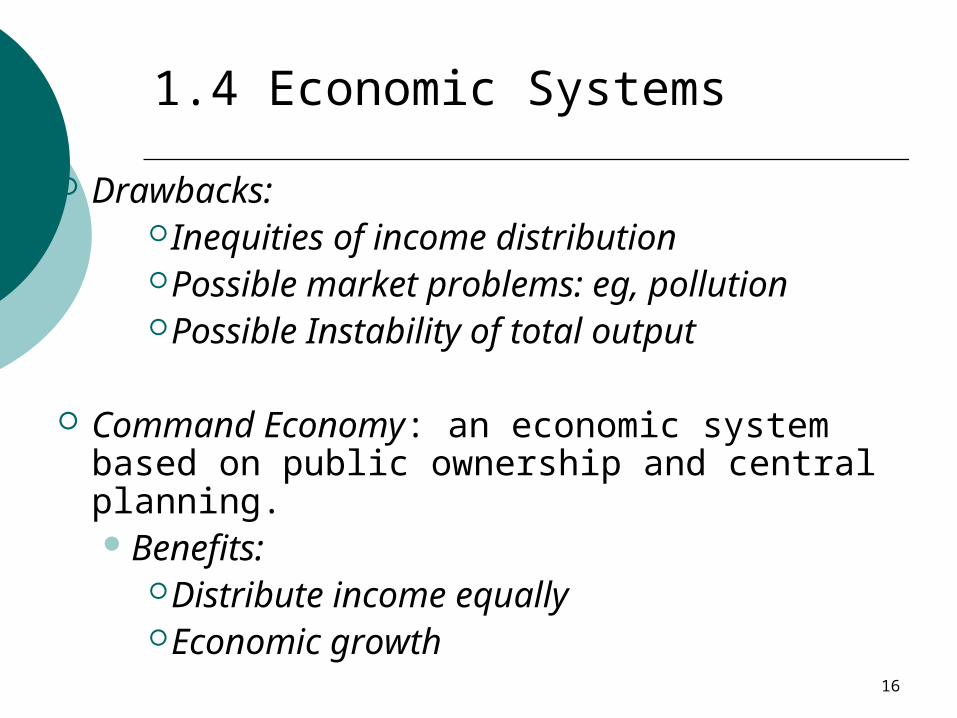

1.4 Economic Systems

Drawbacks:Inequities of income distributionPossible market problems: eg, pollutionPossible Instability of total output

Command Economy: an economic system based on public ownership and central planning.Benefits:

Distribute income equallyEconomic growth

17

1.4 Economic Systems

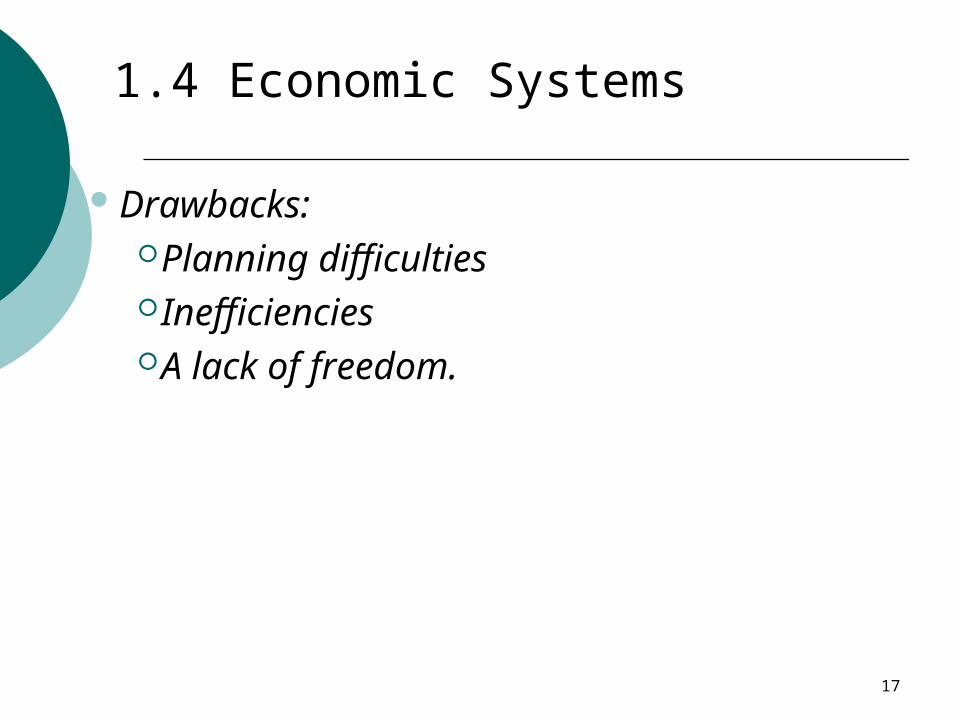

Drawbacks:Planning difficultiesInefficienciesA lack of freedom.

18

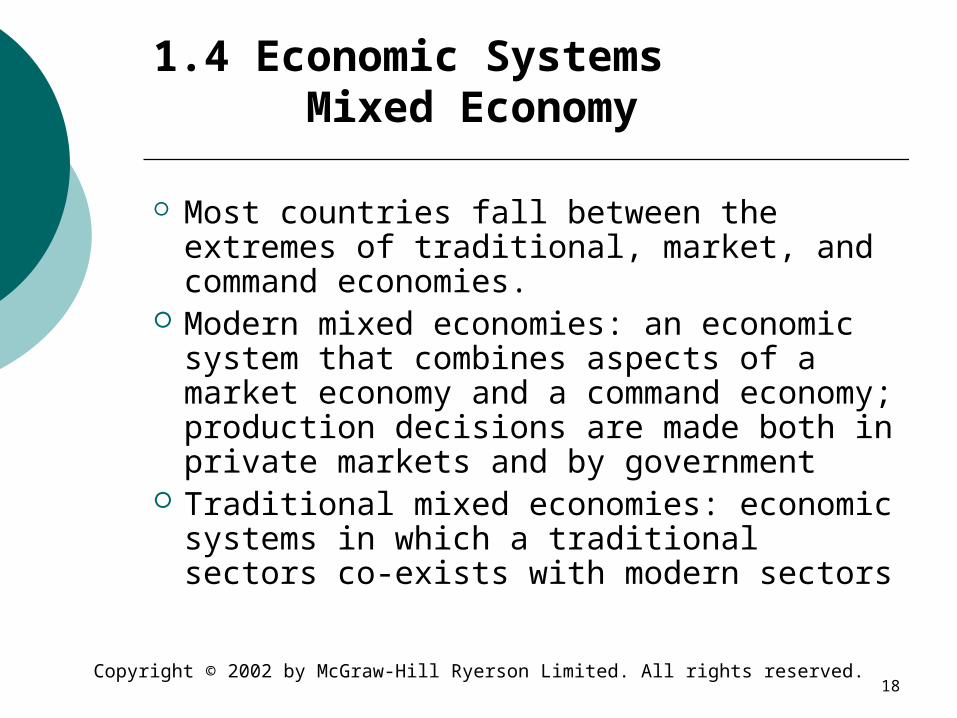

1.4 Economic Systems Mixed Economy

Most countries fall between the extremes of traditional, market, and command economies.

Modern mixed economies: an economic system that combines aspects of a market economy and a command economy; production decisions are made both in private markets and by government

Traditional mixed economies: economic systems in which a traditional sectors co-exists with modern sectors

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

19

The Range of Economic Systems Figure 1.4, page 16

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

20

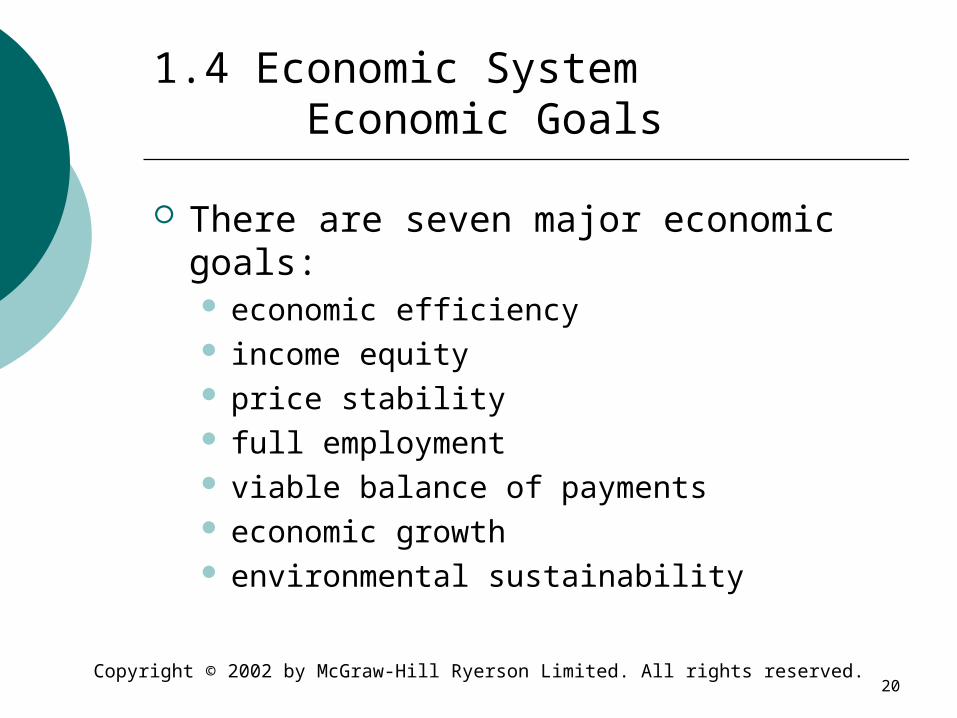

1.4 Economic System Economic Goals

There are seven major economic goals: economic efficiency income equity price stability full employment viable balance of payments economic growth environmental sustainability

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

21

1.4 Economic SystemComplementary and Conflicting Economic Goals

Economic goals may be complementary.An example is the relationship between full

employment and economic growth. Economic goals may be conflicting.

An example is the relationship between price stability and full employment.

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.

22

The Founder of Modern Economics

Adam Smith:explained how the division of labour

increases productionargued that self interest is transformed by

the invisible hand of competition so that it creates significant economic benefits

stressed the principle of laissez faire, which means that governments should not intervene in economic activity

Copyright © 2002 by McGraw-Hill Ryerson Limited. All rights reserved.