1 determinants of the exchange rate 2 determinants of the exchange rate under a flexible rate...

Post on 21-Dec-2015

220 views

TRANSCRIPT

1

Determinants of the Exchange Rate

2

Determinants of the Exchange Rate

• Under a flexible rate system, the exchange rate is determined by supply and demand.

– The dollar demand for foreign exchange originates from American demand for foreign goods, services, & assets (real or financial).

– The supply of foreign exchange originates from sales of goods, services, & assets from Americans to foreigners.

– The foreign exchange market brings the quantity demanded and quantity supplied into balance.

As it does so, it brings the purchases by Americans from foreigners into equality with the sales of Americans to foreigners.

3

Quantity offoreign exchange (pounds)

Q

$1.20

$1.50

$1.80

Dollar price of foreign exchange(for pounds)

Foreign Exchange Market Equilibrium

S(sales to

foreigners)

Excess demandfor pounds

Excess supplyof pounds

• The dollar price of the English pound is measured on the vertical axis. The horizontal axis indicates the flow of pounds to the foreign exchange market.• The demand and supply of pounds

are in equilibrium at the exchange

rate of $1.50 = 1 English pound.• At this price, quantity demanded equals quantity supplied.• A higher price of pounds (like $1.80 = 1 pound), would lead to an excess supply of pounds ... causing the dollar price of the pound to fall (depreciate).• A lower price of pounds (like $1.20 = 1 pound), would lead to an excess demand for pounds … causing the dollar price of the pound to rise (appreciate).

D(purchases from

foreigners)

e

4

Changes in the Exchange Rate

• Factors that cause a currency to depreciate:

– A rapid growth of income (relative to trading partners) that stimulates imports relative to exports.

– A higher rate of inflation than one's trading partners.

– A reduction in domestic real interest rates (relative to rates abroad).

5

Quantity offoreign exchange (pounds)

Q1

$1.50

$1.80

Dollar price of foreign exchange(for pounds)

a

Foreign Exchange Market Equilibrium

S(sales to

foreigners)

• Other things constant, if incomes increase in the United States, U.S.

imports of foreign goods and services will grow.• The increase in imports will increase the demand for pounds (in the foreign exchange market) causing the dollar price of the pound to rise from $1.50 to $1.80.

D1

Q2

D2

b

6

Quantity offoreign exchange (pounds)

Q1

$1.50

Dollar price of foreign exchange(for pounds)

Inflation WithFlexible Exchange Rates

S1

• If prices were stable in England while the price level in the U.S. increased by 50 percent … the

U.S. demand for British goods (and pounds) would increase …

D1

D2

a

$2.25

S2

as U.S. exports to Britain would be relatively more expensive they would decline and thereby cause the supply of pounds to fall.• These forces would cause the dollar to depreciate relative to the pound.

b

7

Changes in the Exchange Rate

• Factors that cause a currency to appreciate:

– A slower growth rate relative to one’s trading partners.

– A lower inflation than one's trading partners.

– An increase in domestic real interest rates

(relative to rates abroad).

8

FOREIGN EXCHANGE TURNOVER AND WORLD EXPORTS Foreign Exchange

Turnover ($ trillion)

World Exports of Goods ($ trillion)

Ratio

1979 $17.5 $1.5 12:1

1986 75.0 2.0 38:1

1989 190.0 3.1 61:1

1992 252.0 4.7 54:1

1995 297.5 5.0 60:1

1998 372.5 5.4 69:1

SOURCES: Held, David, Anthony McGrew, David Goldblatt and Jonathan Perraton, Global Transformations, p. 209; Bank for International Settlements, Central Bank Survey of Foreign Exchange and Derivatives Market Activity, 1998, p. 5; International Monetary Fund, World Economic Outlook, 1998, p. 200.

Growth of Trade and Foreign Exchange Transactions

9

Exchange Rates and Asset Prices

Exchange rates are determined by the relative supplies and demands for currencies.

Since buyers and sellers are ultimately interested in purchasing something with the currency - goods, services, or investments - their prices and returns must indirectly influence the demand for a given currency.

So far, we have focused on the relationship between exchange rates and the demand and supply of goods and services.

Now we turn to the prices that determine the demand for assets - their returns.

10

Law of One Price for Assets

Assume:

Absent frictions, identical goods must trade for identical prices in different countries when converted into a common currency.

The same condition should hold for assets.

One important difference between goods and assets:

Price is not paid immediately - it is paid over time in the form of returns.

This introduces the primary friction for exchanging assets - a friction not found in goods.

Risk

11

Law of One Price for Assets

Hence, there must exist a corresponding version of the Law of One Price for assets which requires returns to be identical across countries once this friction has been removed:

Covered Interest Parity

Covered Interest Parity requires frictionless markets to offer identical rates of returns for identical assets.

12

Law of One Price for AssetsArbitrageurs will guarantee that the following two strategies will generate the exact same common-currency return:

1. a. Purchasing $1 worth of U.S. short-term treasuries.

b. Obtain an n-period return of 1+Rt,t+n.

2. a. Convert $1 into foreign currency at rate 1/st (FC/$).

b. Purchase corresponding foreign short-term treasuries.

c. Receive an n-period foreign currency return of 1+R*t,t+n.

d. Eliminate the currency risk of the foreign return by locking in an exchange rate of Ft,t+n ($/FC).

13

Law of One Price for AssetsArbitrageurs will guarantee that the following two strategies will generate the exact same common-currency return:

1. a. Purchasing $1 worth of U.S. short-term treasuries.

b. Obtain an n-period return of 1+Rt,t+n.

2. a. Convert $1 into foreign currency at rate 1/st (FC/$).

b. Purchase corresponding foreign short-term treasuries.

c. Receive an n-period foreign currency return of 1+R*t,t+n.

d. Eliminate the currency risk of the foreign return by locking in an exchange rate of Ft,t+n ($/FC).

e. Obtain an overall n-period return of: Ft,t+n (1+R*t,t+n)

st

14

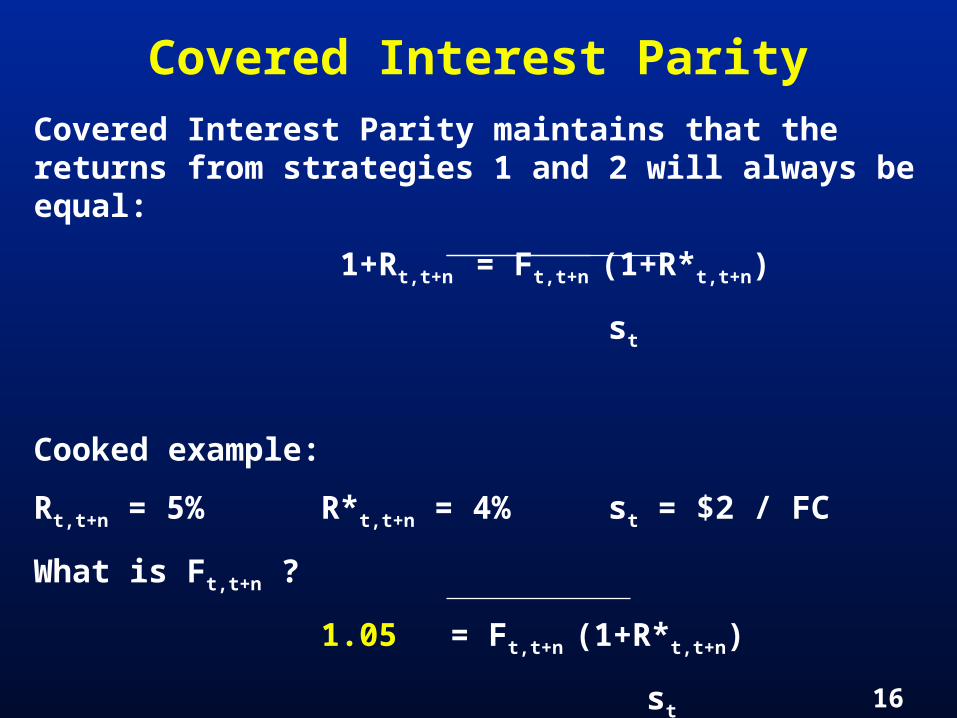

Covered Interest ParityCovered Interest Parity maintains that the returns from strategies 1 and 2 will always be equal:

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

Cooked example:

Rt,t+n = 5% R*t,t+n = 4% st = $2 / FC

What is Ft,t+n ?

15

Cooked example:

Rt,t+n = 5% R*t,t+n = 4% st = $2 / FC

What is Ft,t+n ?

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

Covered Interest ParityCovered Interest Parity maintains that the returns from strategies 1 and 2 will always be equal:

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

16

Covered Interest ParityCovered Interest Parity maintains that the returns from strategies 1 and 2 will always be equal:

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

Cooked example:

Rt,t+n = 5% R*t,t+n = 4% st = $2 / FC

What is Ft,t+n ?

1.05 = Ft,t+n (1+R*t,t+n)

st

17

Covered Interest ParityCovered Interest Parity maintains that the returns from strategies 1 and 2 will always be equal:

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

Cooked example:

Rt,t+n = 5% R*t,t+n = 4% st = $2 / FC

What is Ft,t+n ?

1.05 = Ft,t+n 1.04

st

18

Covered Interest ParityCovered Interest Parity maintains that the returns from strategies 1 and 2 will always be equal:

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

Cooked example:

Rt,t+n = 5% R*t,t+n = 4% st = $2 / FC

What is Ft,t+n ?

1.05 = Ft,t+n 1.04

$2 / FC

19

Covered Interest ParityCovered Interest Parity maintains that the returns from strategies 1 and 2 will always be equal:

1+Rt,t+n = Ft,t+n (1+R*t,t+n)

st

Cooked example:

Rt,t+n = 5% R*t,t+n = 4% st = $2 / FC

What is Ft,t+n ?

1.05 = Ft,t+n 1.04

$2 / FC

Ft,t+n = $ 2.02 / FC - Investors in R* require a guaranteed currency appreciation to compensate for lower interest rate.

20

Real Example:

Not so long ago, 90-day U.S. and Japanese Treasury Notes had the following returns:

RUS = 5.03% RJ

= 3.77%

The spot exchange rate was st = $.008585 / Yen.

What was the 90-day forward exchange rate F?

$.008689 / Yen.

Investors demanded less compensation for holding Yen-denominated returns since they expected the Yen to appreciate.

21

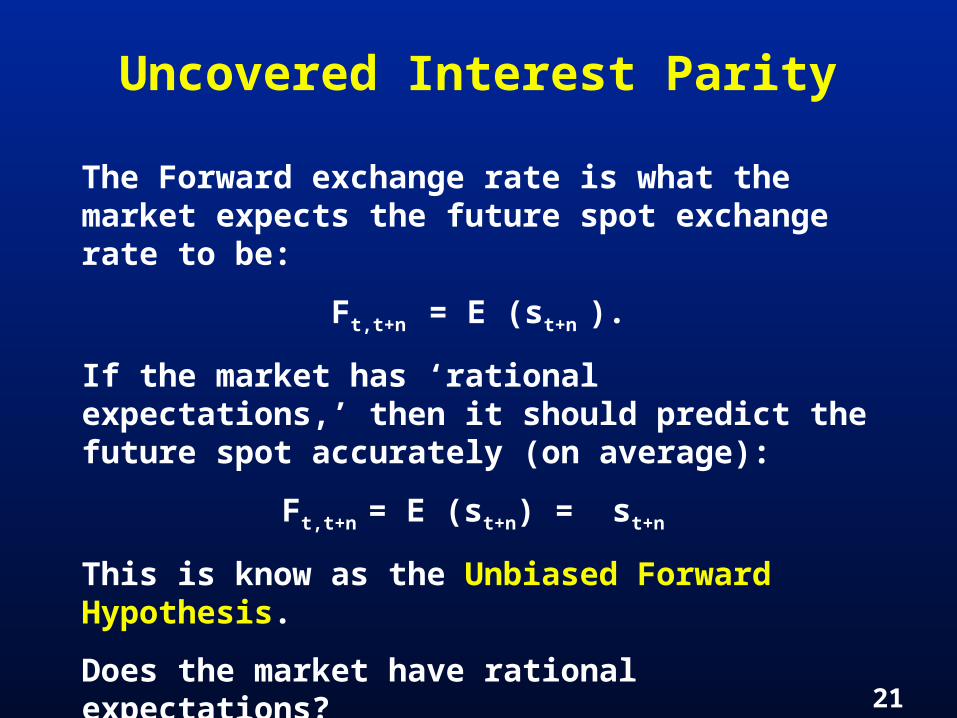

Uncovered Interest Parity

The Forward exchange rate is what the market expects the future spot exchange rate to be:

Ft,t+n = E (st+n ).

If the market has ‘rational expectations,’ then it should predict the future spot accurately (on average):

Ft,t+n = E (st+n) = st+n

This is know as the Unbiased Forward Hypothesis.

Does the market have rational expectations?

Robert Lucas said ‘yes’ and won a prize (Nobel).

22

Uncovered Interest Parity

If so, this implies that an ‘unhedged’ version of covered interest parity should hold as well.

23

Uncovered Interest Parity

If so, this implies that an ‘unhedged’ version of covered interest parity should hold as well. If this is the case:

1+Rt,t+n = E(st,t+n)(1+R*t,t+n)

st

24

Uncovered Interest Parity

If so, this implies that an ‘unhedged’ version of covered interest parity should hold as well. On average:

1+Rt,t+n = st,t+n (1+R*t,t+n)

st

25

Uncovered Interest Parity

If so, this implies that an ‘unhedged’ version of covered interest parity should hold as well. On average:

1+Rt,t+n = st,t+n (1+R*t,t+n)

st

Which can be closely approximated by the Uncovered Interest Parity equation:

Rt,t+n - R*t,t+n = % st,t+n.

26

Uncovered Interest Parity

Example (cooked):

If British short-term interest rates are 5%, German short-term interest rates are 10%, and the current exchange rate is 0.5 P/ Euro, what will be the Pound/Euro exchange rate one year from now?

Rt,t+n - R*t,t+n = % st,t+n.

The Euro should depreciate by 5% to 0.475 P / Euro.

Also, the one-year forward exchange rate better be 0.475 P / Euro

27

To Review: Exchange Rate Arbitrage

Two kinds of Arbitrage:

1. Riskless arbitrage will ensure:

Covered Interest Parity:

1+Rt,t+n = Ft,t+n(1+R*t,t+n)/st

or:

Rt,t+n - R*t,t+n = Ft,t+n - st

If difference between forward and spot rates do not equal differences in interest rates, arbitrageurs will make money every time - relationship holds instantaneously and therefore is risk-free.

28

Exchange Rate Arbitrage

2. Risky arbitrage should ensure:

A. Forward rate is unbiased - it differs from spot by expected exchange rate changes:

Ft,t+n - st = E(%st,t+n),

B. That these expectations are rational:

E(%st,t+n) = %st,t+n

C. So that Uncovered Interest Parity holds on average:

Rt,t+n - R*t,t+n = Ft,t+n - st = E(%st,t+n) = %st,t+n

29

Exchange Rate Arbitrage

2. Risky arbitrage should ensure:

A. Forward rate is unbiased - it differs from spot by expected exchange rate changes:

Ft,t+n - st = E(%st,t+n),

B. That these expectations are rational:

E(%st,t+n) = %st,t+n

C. So that Uncovered Interest Parity holds on average:

Rt,t+n - R*t,t+n = Ft,t+n - st = E(%st,t+n) = %st,t+n

Differences between interest rates forecast exchange rate changes.

30

Exchange Rate Arbitrage

2. Risky arbitrage should ensure:

A. Forward rate is unbiased - it differs from spot by expected exchange rate changes:

Ft,t+n - st = E(%st,t+n),

B. That these expectations are rational:

E(%st,t+n) = %st,t+n

C. So that Uncovered Interest Parity holds on average:

Rt,t+n - R*t,t+n = Ft,t+n - st = E(%st,t+n) = %st,t+n

Differences between interest rates forecast exchange rate changes. Why?

31

Exchange Rate Arbitrage

Rt,t+n - R*t,t+n = %st,t+n

If s generally doesn’t change sufficiently to offset interest differential, (say RUS

t,t+n > RJt,t+n and RUS

t,t+n -RJt,t+n > % st,t+n)

arbitrageurs will:

1. Borrow in low-interest rate currency (Yen).

2. Convert to the high-interest rate currency (Dollars).

3. Deposit in the high-interest rate currency.

4. Convert back to repay low-interest rate loan at an insufficiently appreciated exchange rate.

5. Earn a profit - on average - of:

RUSt,t+n - RJ

t,t+n - %st,t+n

32

Exchange Rate ArbitrageRt,t+n - R*t,t+n = %st,t+n

Example:

RUS = 5.03% RJ

= 3.77% st = $.008585 / Yen.

Ft,t+n says Yen should appreciate to: $.008689 / Yen.

But if, on average, st+n = st, can a speculator can make profits, on average?

Of course: By borrowing in Yen at 3.77%, depositing in Dollars at 5.03%, and converting after 1 year back into yen at the same exchange rate.

This will earn - on average - 1.26% on a zero-wealth investment.

33

Exchange Rate Arbitrage

This activity - if widespread - will have the following effects:

1. Increase demand for dollars currency at time t -causing st ($/Yen) to decline.

2. Increase demand for U.S. deposits - causing RUS

t,t+n to decline.

3. Increase demand for Japanese borrowing - causing RJ

t,t+n to increase.

4. Increase demand for Yen at time t+n - causing st+n to increase.

34

Key International Relationships

35

Exchange Rate

Change

Relative Inflation

Rates

Key International Relationships

36

RPPP: - * = %s

Inflation differentials are offset by changes in spot exchange rate.

Relative Inflation

Rates

Key International Relationships

Exchange Rate

Change

37

Relative Inflation

Rates

Key International Relationships

Purchasing Power Parity

Exchange Rate

Change

38

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Purchasing Power Parity

Exchange Rate

Change

39

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

CIP: Ft,t+n - st = R - R*

Forward differs from spot by interest rate

differential

Purchasing Power Parity

Exchange Rate

Change

40

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

41

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

42

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Unbiased Forward: Ft,t+n - st = E(%st,t+n)

Forward differs from spot by expected

change in spot

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

43

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

44

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

45

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Fisher Effect: 1+R = (1+r)(1+E())

Nominal interest rate equals real rate plus

expected inflation

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

46

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

1+R = (1+r)(1+E())

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

R - R* = E() - E(*) With RIP, interest rates

reflect expected inflation differential.

47

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Fisher Effect and

Real Interest Parity

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

48

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Ft,t+n - st = R - R*

Unbiased Forward

Rate

Purchasing Power Parity

Exchange Rate

Change

Fisher Effect and

Real Interest Parity

49

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Ft,t+n - st = R - R* Ft,t+n - st = E(%st,t+n)

Purchasing Power Parity

Exchange Rate

Change

Fisher Effect and

Real Interest Parity

50

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Ft,t+n - st = R - R*

Uncovered Interest Parity:R - R* = %s

Exchange rate changes offset interest differentials

Purchasing Power Parity

Exchange Rate

Change

Fisher Effect and

Real Interest Parity

Ft,t+n - st = E(%st,t+n)

51

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

1+R = (1+r)(1+E())R - R* = E() - E(*)

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

52

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

- * = %s1+R = (1+r)(1+E())R - R* = E() - E(*)

Unbiased Forward

Rate

Covered Interest Parity

Exchange Rate

Change

53

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

1+R = (1+r)(1+E())R - R* = E() - E(*)

Uncovered Interest Parity:R - R* = %s

Exchange rate changes offset interest differentials

- * = %s

Unbiased Forward

Rate

Covered Interest Parity

Exchange Rate

Change

54

Relative Inflation

Rates

Forward Exchange Premium

Relative Interest Rates

Key International Relationships

Uncovered Interest Parity

Unbiased Forward

Rate

Covered Interest Parity

Purchasing Power Parity

Exchange Rate

Change

Fisher Effect and

Real Interest Parity

55

Key International Relationships

These relationships are at the heart of international financial management. They are used in many dimensions of a multinational’s operations.

1. Deciding which currency to borrow or lend in.

2. Determining an appropriate project rate of return.

3. Analyzing a firm’s foreign exchange exposure.

4. etc...