1 chapter 5 presented by group 6 nick feiler xiaohan hu john langsdorf wes matthews steve potts

TRANSCRIPT

1

Chapter 5 Chapter 5 Presented by Group 6Presented by Group 6

Nick Feiler

Xiaohan Hu

John Langsdorf

Wes Matthews

Steve Potts

2

Building a Profit PlanBuilding a Profit Plan

Budget – Plan to generate or consume resources; cost center or profit center.

Profit Plan – Budgets of Profit Centers that generate profits and are accountable for both revenues and expenses.

3

Three Objectives of theThree Objectives of thePlanning ProcessPlanning Process

Translate the strategy of the business into a detailed plan to create value.

Evaluate whether sufficient resources are available to implement the intended strategy.

Create a foundation to link economic goals with leading indicators of strategy implementation.

4

Managers’ 3 Profit Plan QuestionsManagers’ 3 Profit Plan Questions

Does the organization’s strategy create economic value?

Does the organization have the cash to fund their strategy and remain solvent?

Does the organization create enough value to attract the financial resources that it needs to fund long-term investment in new assets?

5

Three Wheels of Profit PlanningThree Wheels of Profit Planning

Profit Wheel

Cash Wheel

ROE Wheel

6

Three Wheels of Profit PlanningThree Wheels of Profit PlanningOperating

Cash

AccountsReceivable

Inventory

Sales*

Cash Wheel

Sales*

Profits**

Investment in Assets

Operating Expenses

ProfitWheel

Profits**

Return on Equity

Asset Utilization

Stockholders’Equity

ROE Wheel

7

Profit Wheel/3WheelsProfit Wheel/3Wheels

The profit plan summarizes the expected revenue inflows and expense outflows for a specified future accounting period.

Usually managers go back and forth, projecting sales, operating expenses, profits, and required investment in assets.

Then they work on the cash wheel and the ROE wheel to ensure resources will be available to implement the profit wheel.

8

Profit Wheel – 5 stepsProfit Wheel – 5 steps

1) Estimate the Level of Sales

2) Forecast Operating Expenses

3) Calculate Expected Profit

4) Price the Investment in New Assets

5) Close the Profit Wheel and Test Key Assumptions.

9

Profit Wheel – Step 1Profit Wheel – Step 1Estimate the Level of SalesEstimate the Level of Sales

External Variables1. Macroeconomic factors2. Government regulations3. Competitor moves4. Customer demand

Internal Decisions1. Product mix and pricing2. Marketing programs3. New Product Introduction and 4. Change in product quality and feature5. Manufacturing and distribution capacity6. Customer service levels

10

Profit Wheel – Step 2Profit Wheel – Step 2Forecast Operating ExpensesForecast Operating Expenses

Variable costs forecast and reduction1. Economic of scales

2. Operating efficiency

3. Bargaining power with suppliers

4. Redesigning of products

5. Increase price

Non-variable costs1. Committed costs

2. Discretionary costs

3. Activity-based indirect costs

11

Profit Wheel – Step 3Profit Wheel – Step 3Calculate Expected ProfitCalculate Expected Profit

Profit defined- The residual economic value after interest expense and

income taxes

Calculating Profit- NOPAT: Net Operating Profit after Taxes- EBIAT: Earnings before Interest and after Taxes

12

Profit Wheel – Step 4Profit Wheel – Step 4Price the Investment in New Price the Investment in New

AssetsAssets

Assets to Consider for Investment:

1) Operating Assets

2) Long-Term Assets

Most common investment evaluation technique is net present value.

13

Profit Wheel – Step 5Profit Wheel – Step 5Close the Profit Wheel and Test Close the Profit Wheel and Test

Key AssumptionsKey Assumptions

Perform a Sensitivity Analysis

Objective: Estimate how profit might change when assumptions prove to be under- or overstated.

14

Cash WheelCash Wheel

The cash wheel illustrates the operating cash flow cycle of a business.

Important as companies have limited cash reserves and borrowing capacity.

Operating cash = Cash Rec’d – Cash PaidDirect (Short Term) & Indirect (Long Term)

Methods

15

Cash Wheel – 4 StepsCash Wheel – 4 Steps

1) Estimate Net Cash Flows from Operations

2) Estimate Cash Needed to Fund Growth in Operating Assets

3) Price the Acquisition and Divestiture of Long-Term Assets

4) Estimate Financing Needs and Interest Payments

16

Cash Wheel – Step 1Cash Wheel – Step 1Estimate Net Cash Flows from Estimate Net Cash Flows from

OperationsOperations

The calculation of EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a simple technique to estimate operating cash flow.

Refer to Exhibit 2.

17

Cash Wheel – Step 2Cash Wheel – Step 2Estimate Cash Needed to Fund Estimate Cash Needed to Fund

Growth in Operating AssetsGrowth in Operating Assets

EBITDA is a rough measure that ignores any changes in working capital needed to operate the business.

Examples include: A/R (accounts receivable), Inventory, and A/P (accounts payable).

Refer to Exhibit 2.

18

Cash Wheel – Step 3Cash Wheel – Step 3Price the Acquisition and Price the Acquisition and

Divestiture of Long-Term AssetsDivestiture of Long-Term Assets

Different strategies and initiatives will require different levels of investment and cash.

Examples here are Fixed Asset purchases, such as computer equipment or machinery.

Refer to Exhibit 2.

19

Cash Wheel – Step 4Cash Wheel – Step 4Estimate Financing Needs and Estimate Financing Needs and

Interest PaymentsInterest Payments

Lastly, need to account for cash needed or generated by financing and income tax.

Examples here are dividends, interest expense, interest received, and repayment of debt principal.

Refer to Exhibit 2.

20

ROE WheelROE Wheel

Return on Investment (ROI): a ratio measurement of the profit output of the business as a percentage of financial investment inputs.

Return on Equity (ROE): the appropriate internal measure of ROI for managers.

ROE = Net Income / Shareholder’s Equity

21

ROE Wheel – 3 StepsROE Wheel – 3 Steps

Calculate Overall Return on Equity

Estimate Asset Utilization

Compare Projected ROE with Industry Benchmarks and Investor Expectations

22

ROE Wheel – Step 1ROE Wheel – Step 1Calculate Overall Return on EquityCalculate Overall Return on Equity

ROE = (Net Income/Sales)*(Sales/Assets)*

(Assets/Shareholder’s Equity) Net Income/Sales = Profitability Ratio Sales/Assets = Asset Turnover Ratio Assets/Shareholder’s Equity = Financial

Leverage Ratio

23

ROE Wheel – Step 2ROE Wheel – Step 2Estimate Asset UtilizationEstimate Asset Utilization

ROCE = Return on Capital Employed: Measures the effective utilization of capital and assets.

= (Net Income/sales)*(Sales/Capital Employed)

Capital Employed = Assets within a manager’s direct span of control.

24

ROE Wheel – Step 2ROE Wheel – Step 2Asset Utilization MeasuresAsset Utilization Measures

Working Capital Turnover = (Sales) / (Current Assets – Current Liabilities)

Accounts Receivable Turnover = (Net Sales on Credit) / (Average Net Receivables)

Inventory Turnover = (Cost of Goods Sold) / (Average Inventory)

Fixed Asset Turnover = (Sales) / (Property, Plant, and Equipment)

25

ROE Wheel – Step 2ROE Wheel – Step 2ROCE TreeROCE Tree

Sales

Profit (-) COGS

Return/Sales (/)Total Expenses

Selling and Admin. Expenses

Return on Capital Employed (x) Sales

Other Expenses

Cash

Sales/Assets (/)Working Capital Inventories

Total Assets (+)

Accounts Receivable

Productive Assets

26

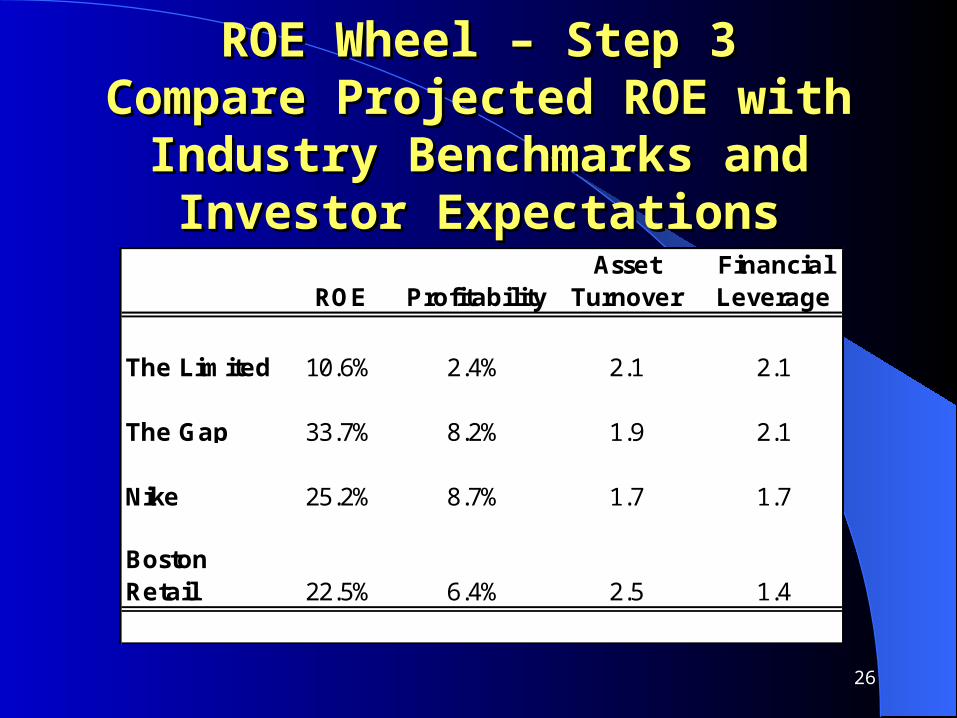

ROE Wheel – Step 3ROE Wheel – Step 3Compare Projected ROE with Compare Projected ROE with

Industry Benchmarks and Investor Industry Benchmarks and Investor ExpectationsExpectations

ROE ProfitabilityAsset

TurnoverFinancial Leverage

The Limited 10.6% 2.4% 2.1 2.1

The Gap 33.7% 8.2% 1.9 2.1

Nike 25.2% 8.7% 1.7 1.7

Boston Retail 22.5% 6.4% 2.5 1.4

27

Using the Profit Wheels to Using the Profit Wheels to Test StrategyTest Strategy

Profit Wheel

- Prepare profit planCash Wheel

- Ensure cash will be adequateROE Wheel

- Compare each alternative

28

Chapter SummaryChapter Summary

Profit plan describes business strategy in economic terms

Profit plan is used to assess the ability of different strategies to generate value and to estimate whether sufficient resources will be available to implement the chosen strategy