1 chapter 5 inflation and disinflation © pierre-richard agénor the world bank

Post on 20-Dec-2015

221 views

TRANSCRIPT

1

Chapter 5Inflation and Disinflation

© Pierre-Richard Agénor

The World Bank

2

Sources of Inflation Nominal Anchors in Disinflation Money vs. the

Exchange Rate Disinflation Programs: The Role of Credibility Two Recent Stabilization Experiments

3

Sources of Inflation Hyperinflation and chronic Inflation Fiscal Deficits, Seigniorage, and Inflation Other sources of Chronic Inflation

Wage Inertia Exchange Rates and the Terms of Trade The Frequency of Price Adjustment Food Prices Time Inconsistency and the Inflationary Bias

4

Hyperinflation and Chronic Inflation Cagan's criterion: Hyperinflation is defined as an

inflation rate of at least 50% per month, or 12,975% per annum.

Three main features of hyperinflation (Végh, 1992):

It typically has its origin in large fiscal imbalances. Nominal inertia tends to disappear. It brings about a chaotic social and economic

environment.

5

Example of hyperinflation: Zaire. A deep and worsening political crisis led to a drastic

increase in government expenditure. At the peak of the hyperinflation process, in

December 1993, inflation rose to almost 240% a month.

During the whole period, domestic prices were increasingly set in foreign currency.

Figure 5.1: during the whole episode, the monthly rate of depreciation of the parallel exchange rate remained closely correlated with the inflation rate.

6

Figure 5.1aZaire: Money Growth and Inflation, 1990-96

Source: Beaugrand (1997).1/ Monthly rate of change of the stock of currency outside banks.

1990 1991 1992 1993 1994 1995 1996

-50

0

50

100

150

200

250

0

Inflation and Money Growth

Currency outside banks

Inflation

1/

7

Figure 5.1bZaire: Inflation and Exchange Rate Depreciation, 1990-96

Source: Beaugrand (1997).2/ Parallel exchange rate in terms of old zaïres. The new zaïre was introduced in October 1993 at a parity of NZ=Z 3,000,000; later data have been rescaled accordingly.

1990 1991 1992 1993 1994 1995 1996

-100

0

100

200

300

400

500

0

Inflation and Exchange Rate Depreciation

Zaïres per U.S. dollar (parallel market)

Inflation

2/

8

Features of chronic inflation: Fiscal imbalances are often less acute in the short

run than those observed during episodes of hyperinflation; in this case more difficult to mobilize political support for reform.

There is a high degree of inflation inertia resulting from widespread indexation of wages and financial assets.

The public is often skeptical of new attempts to stop inflation, particularly when there is a history of failed stabilization efforts.

Lack of credibility can be a source of inertia.

9

Fiscal Deficits, Seigniorage, and Inflation In countries where the tax collection system, capital

markets, and institutions are underdeveloped, fiscal imbalances are often at the root of hyperinflation and chronic inflation.

Governments often have no other option but to monetize their budget deficits.

Bruno and Fischer (1990): how monetary growth and fiscal deficits affect inflation.

Suppose: real money demand, md, is a function of the expected inflation rate, a.

10

Under perfect foresight expected and actual inflation rates are equal, = a.

Money demand:

md = m0exp(-).

At equilibrium, m = ms = md. This implies:

= - [ ln(m/m0)/ ].

Along an equilibrium path, inflation and real money balances are negatively related.

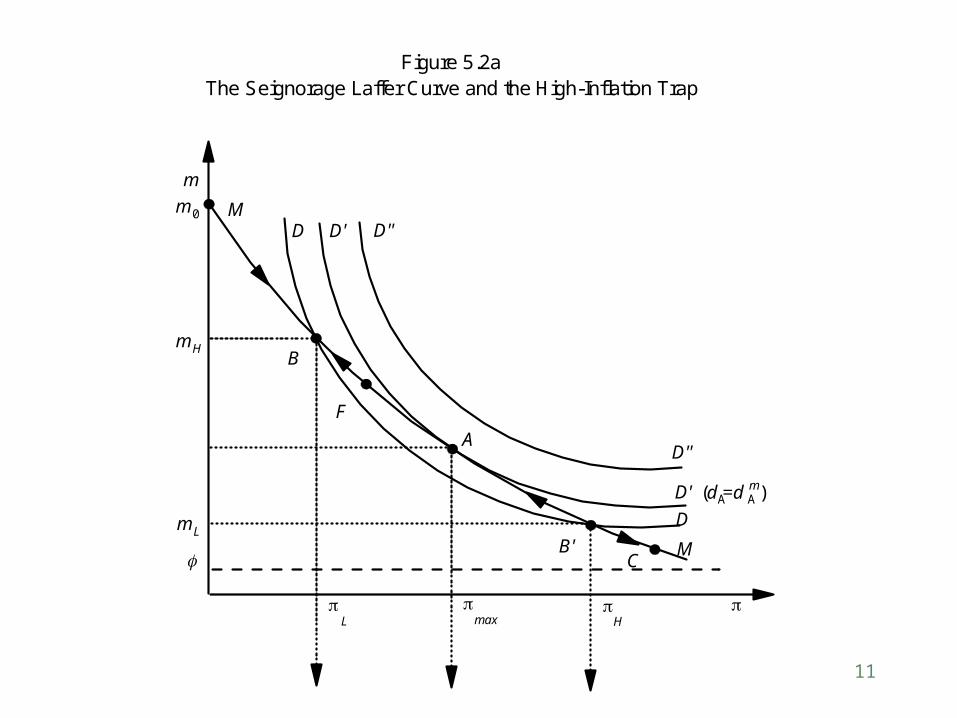

Downward-sloping curve in the -m space, denoted MM in Figure 5.2.

11

Figure 5.2aThe Seignorage Laffer Curve and the High-Inflation Trap

D

B' M

D''

B

D

A

D'

D'

M

D''

F

m

m0

C

L

H

(d =d )Am

A

mL

mH

max

12

Figure 5.2bThe Seignorage Laffer Curve and the High-Inflation Trap

A

B'B

L

H

max

d*A

d Am

Am=d

13

Real fiscal deficit:

d = dA + , > 0,

dA: autonomous component of the deficit;

: measure Olivera-Tanzi effect (rise in the inflation rate lowers the real value of tax revenue as a result of the lag involved in collecting taxes).

Deficit must be financed by seigniorage revenue:

d = m,

M/M : rate of growth of the nominal money stock. .

14

Rate of change of real money balances:

m/m = - ..

After substitution, in steady state with m/m = 0, = :

= [dA /(m - )],

which implies that inflation and real money balances are negatively related in equilibrium (DD in figure 5.2).

.

15

Economy moves along MM in the short run; MM intersects DD only when the economy reaches its long-run equilibrium position (constant level of real money balances).

Depending on the size of dA, MM and DD may or may not intersect.

Figure 5.2 illustrates three cases: two equilibria, corresponding to curve DD; one equilibrium, corresponding to curve D´D´; no equilibrium, corresponding to curve D´´D´´.

16

Under what conditions is the long-run equilibrium unique?

Suppose = 0. In steady state, m = dA.

As dA increases, steady-state seigniorage revenue (inflation tax) must increase as well.

But the relationship is nonlinear because as inflation rises, real money demand falls.

Exponential form of the money demand function: when inflation begins to rise, real money balances fall by relatively little, and revenue from the inflation tax increases at first.

As inflation continues to rise, real money balances begin to fall at a rate faster than the rate at which inflation rises.

17

Thus, after a phase during which m increases (at a decreasing rate), it starts falling (at an increasing rate) and eventually tends to zero as goes to infinity.

These results define a concave relationship: seigniorage Laffer curve associating the steady-state , and m = dA.

Figure 5.2: for some level of dA, there are two corresponding rates of inflation, one low one high.

MM and DD curves in that case intersect twice. Uniqueness occurs only at the optimal inflation

rate, max: maximizes steady-state seigniorage.

18

Revenue-maximizing rate of inflation is reached:

- [(dm/m)/(d/)] = m/ = 1.

m/: elasticity of real money demand with respect to inflation.

Optimal inflation rate:

max = 1/,

: inflation elasticity of money demand.

19

When < max, increases in raise revenue from the inflation tax: ( d(m) / d > 0 and m/ < 1).

When > max, increases in decrease revenue from the inflation tax: ( d(m) / d < 0 and m/ > 1).

Is the solution stable? Equilibrium with a lower inflation rate is unstable.

Level of dA in this case:

dA = (m0exp(-1) - )/.m

m

20

This means that any disturbance or exogenous shock will lead the economy away from low inflation equilibrium point.

But, high inflation equilibrium is stable. Given the nature of the adjustment process under

perfect foresight, a country can be stuck in a situation in which inflation is persistently high: inflation trap (Bruno and Fischer, 1990).

Any equilibrium characterized by > max is inefficient: the same amount of revenue could be collected at a lower inflation rate.

What can governments do to move the economy away from an inefficient position?

21

Change either dA or , because both affect the position of the economy along the seigniorage Laffer curve.

For instance, a credible reduction in the money growth rate may shift MM and DD in such a way that the MM curve will intersect the DD curve only once.

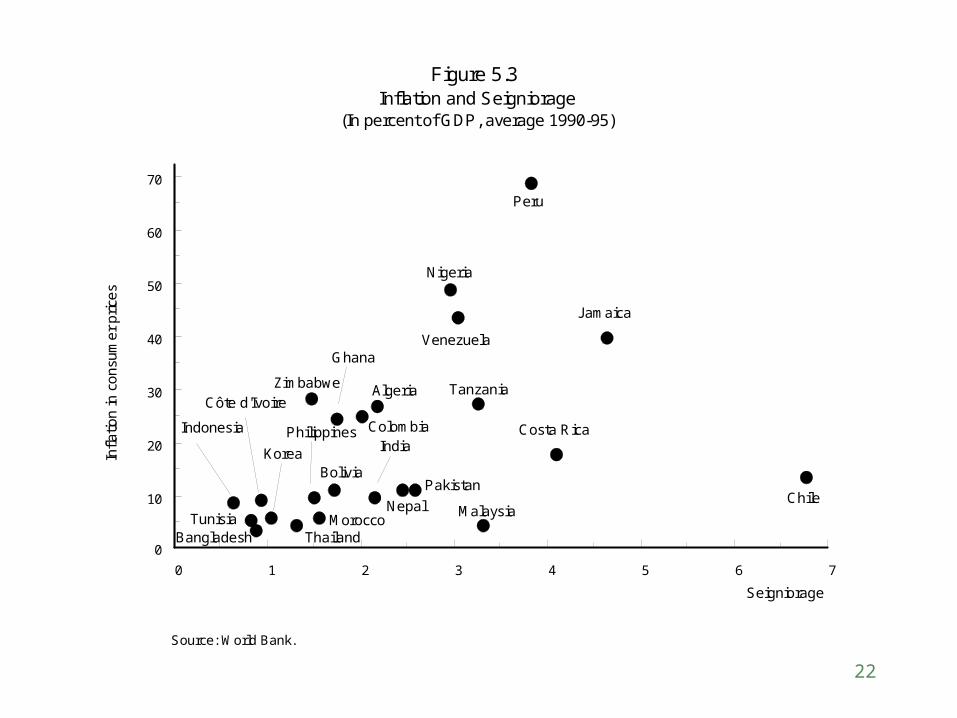

Figure 5.3: positive relation between inflation and seigniorage.

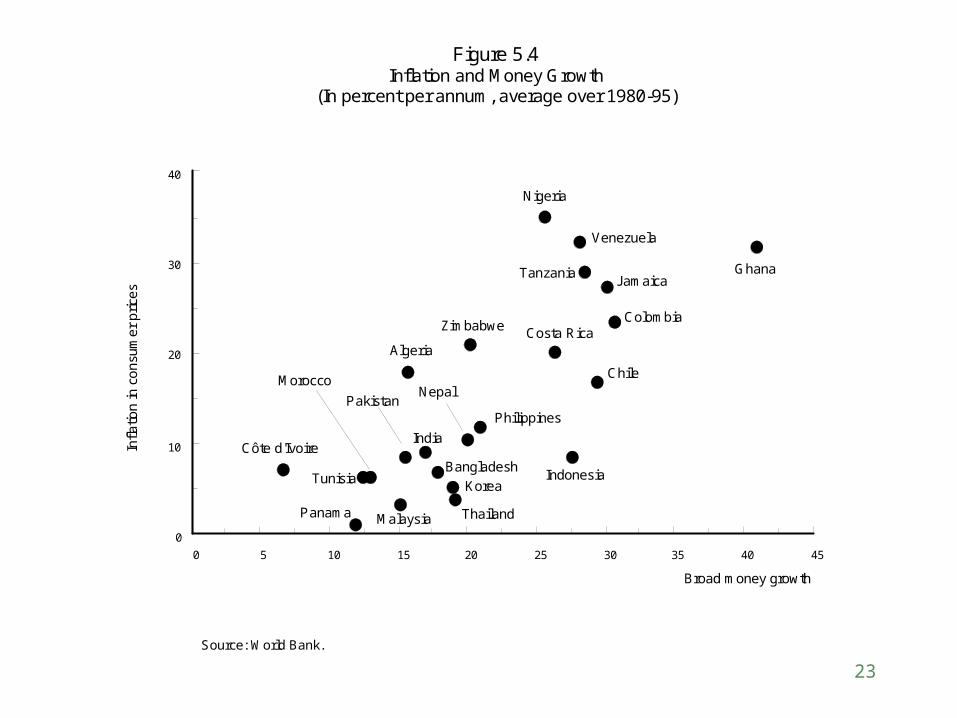

Figure 5.4: positive relation between inflation and broad money growth.

De Haan and Zelhorst (1990) and Karras (1994b): link between monetary growth and budget deficits in developing countries.

22

Figure 5.3 Inflation and Seigniorage

(In percent of GDP, average 1990-95)

Source: World Bank.

0 1 2 3 4 5 6 7

0

10

20

30

40

50

60

70

Infla

tion

in c

on

sum

er

pri

ces

Seigniorage

Bangladesh

Malaysia

ThailandTunisia Morocco

Korea

Indonesia

Côte d'Ivoire

PhilippinesIndia

Nepal

PakistanBolivia

Chile

Costa Rica

Ghana

Colombia

Algeria TanzaniaZimbabwe

Jamaica

Venezuela

Nigeria

Peru

23

Figure 5.4Inflation and Money Growth

(In percent per annum, average over 1980-95)

Source: World Bank.

Infla

tion

in c

ons

umer

pric

es

Broad money growth

0 5 10 15 20 25 30 35 40 45

0

10

20

30

40

Panama Malaysia Thailand

Korea

Morocco

TunisiaBangladesh

Côte d'Ivoire

Indonesia

PakistanNepal

India

Philippines

Chile

AlgeriaCosta RicaZimbabwe

Colombia

JamaicaTanzania Ghana

Venezuela

Nigeria

24

Conclusion: only in a small number of cases does a close, positive relationship exist.

Explanation: role played by expectations about future policy changes (Kawai and Maccini, 1990).

Criticism for public finance approach to inflation:

Since taxation is an alternative to money creation; marginal cost of taxation is moderate relative to

the welfare costs of extreme inflation;

high money growth (and therefore high inflation) is not optimal.

25

Other Sources of Chronic Inflation In addition to fiscal deficits and money growth,

other factors that can affect the inflationary process in the short run:

Wage inertia Exchange rates and the terms of trade The frequency of price adjustment Food prices Time inconsistency and the inflation bias

26

Wage Inertia Backward-looking wage formation mechanisms (e.g.

wage indexation on past inflation rates) can play an important role in inflation persistence.

Model: economy produces home goods and tradable goods.

27

The inflation rate, , is given by a weighted average of changes in prices of both categories of goods:

= N + (1 - ) ( + T) 0 < < 1,

: share of home goods in the price index,

N: rate of change in prices of home goods,

T: rate of change in prices of tradables,

: devaluation rate.

*

*

28

Changes in prices of home goods are set as a mark-up over nominal wage growth, w, and the level of excess demand for home goods, dN:

N = w + dN.

^

^

Nominal wage growth is determined through indexation on past inflation as follows:

w = -1 0 < 1,

with = 1 denoting full indexation.

^

29

Inflation:

= -1+ dN + (1 - )( + T),

inflation inertia exists as long as is positive.

*

Agénor and Montiel (1999): experience of countries like Chile in the early 1980s and more recently Brazil has shown that backward-looking wage indexation can contribute to inflation inertia.

In some countries: frequency at which nominal wages are adjusted tends to increase with the inflationary pressures generated by exchange rate movements.

30

Exogenous shocks in the wage bargaining process could also exert independent impulse effects on inflation.

This could persist over time in the presence of an accommodative monetary policy.

31

Exchange rates and the terms of trade Nominal exchange rate depreciation can exert direct

effects on the fiscal deficit through two channels: by affecting the domestic-currency value of

foreign exchange receipts by the government and foreign exchange outlays;

by affecting the revenue derived from ad valorem taxes on imports.

Since depreciation raises the prices of import-competing goods and exportables, it may exert pressure on wages due to its effect on the cost of living.

32

This is likely to occur in a setting in which indexation mechanisms are pervasive.

Example: a country facing a sharp deterioration in competitiveness and a large current account deficit and policymakers decide to devalue the exchange rate.

Devaluation will increase both the domestic-currency price of imported final goods as well as imported inputs. This puts upward pressure on domestic prices.

Increase in prices can be large enough to outweigh the effect of the initial devaluation on competitiveness---thereby prompting policymakers to devalue again.

33

The process can therefore turn into a devaluation-inflation spiral.

If wages are indexed on the cost of living, they will increase also, putting further upward pressure on prices of domestic goods.

Evidence: Onis and Ozmucur (1990) for Turkey; Alba and Papell (1998) for Malaysia, the Philippines, and Singapore.

Similar process can be seen in countries where the official exchange rate is fixed but the parallel market for foreign exchange is large.

Deterioration in external accounts leads agents to expect a devaluation of the official exchange rate to restore competitiveness.

34

Such expectations will be translated immediately into a depreciation of the parallel exchange rate.

Because the parallel rate measures the marginal cost of foreign exchange, domestic prices will tend to increase.

This increase in prices will further erode competitiveness, leading agents to expect an even larger devaluation of the official exchange rate.

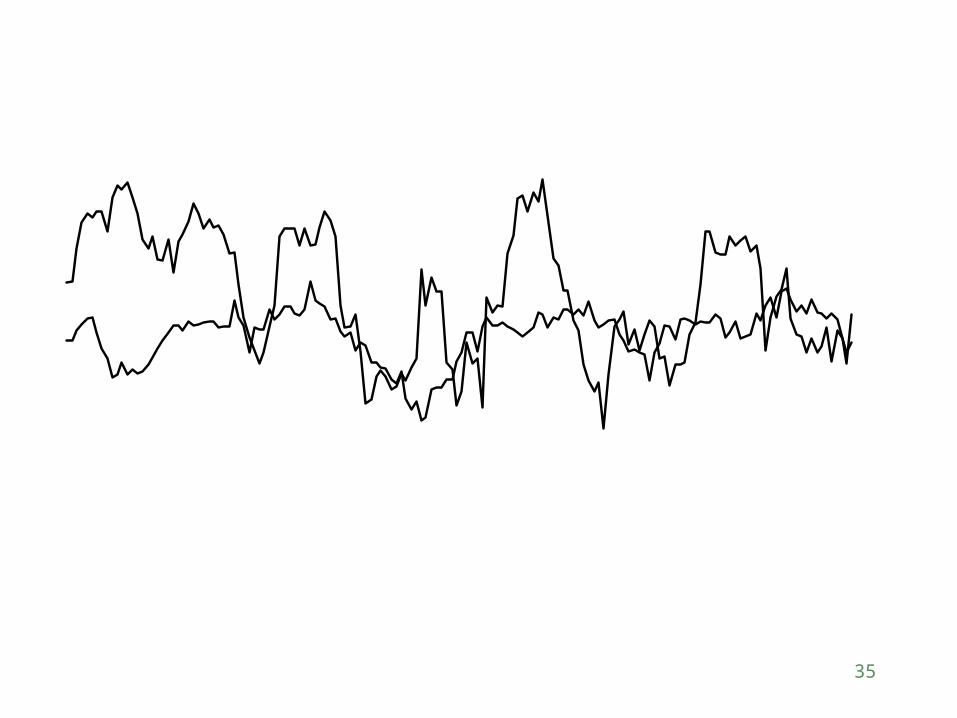

Figure 5.5: although parallel exchange rates display a higher degree of variability than prices, the correlation is positive in the case of Morocco and Nigeria during the 1980s and early 1990s.

When the government is directly involved in controlling exports of commodity, there may be:

35

Figure 5.5aMalawi: Parallel Market Exchange Rate and Inflation

(In percent)

Sources: International Monetary Fund.

Depreciation rate of the parallel exchange rateInflation

Jan81Jan84Jan87Jan90Jan93-40

-30

-20

-10

0

10

20

30

40

50

60

0

Malawi

36

Figure 5.5b Morocco: Parallel Market Exchange Rate and Inflation

(In percent)

Sources: International Monetary Fund.

Depreciation rate of the parallel exchange rate Inflation

Jan81 Jan84 Jan87 Jan90 Jan93-20

-10

0

10

20

30

40

50

60

0

Morocco

37

Figure 5.5c Nigeia: Parallel Market Exchange Rate and Inflation

(In percent)

Sources: International Monetary Fund.

Depreciation rate of the parallel exchange rate Inflation

Jan81 Jan84 Jan87 Jan90 Jan93-50

0

50

100

150

200

250

300

0

-50

Nigeria

38

direct effect of changes in the terms of trade on the budget;

indirect effect through taxes on corporate profits and domestic sales.

Reduction in government revenue due to negative shock causes pressure for monetizing the fiscal deficit.

Improvement in the terms of trade may lead to higher inflation in the future: if government spending has increased sharply in

response to temporary commodity price booms and;

if such increases are difficult to reverse when commodity prices fall.

39

The frequency of price adjustment When high inflation is associated with highly

variable inflation and uncertainty over the pricing horizon of price setters, the frequency of price adjustment becomes endogenous and tends to accelerate.

Shortening of the adjustment interval raises inflation, leading to a further shortening of the adjustment interval.

So price setters will be more and more opting to denominate their prices in a foreign currency.

40

Dornbusch, Sturzenegger, and Wolf (1990): increased synchronization between domestic prices and the nominal exchange rate as inflation rises in Bolivia, Israel, Argentina, and Brazil.

41

Food prices In many developing countries food items comprise

the bulk of the goods included in consumer price indices.

Consumer price index in Nigeria: food items representing 69% of the total basket.

So supply-side factors affecting food prices have an important effect on the behavior of prices.

Moser (1995): rainfall had a significant effect on the rate of price increases, in addition to money growth and exchange rate changes in Nigeria.

Figure 5.6: close correlation between inflation in food prices and inflation in consumer prices.

42

Figure 5.6Inflation and Food Prices

(In percent per annum, average over 1980-95)

Source: World Bank.

Infla

tion

in c

onsu

mer

pric

es

Inflation in food prices

0 10 20 30 40

0

10

20

30

40

Panama

Malaysia

Thailand

KoreaMorocco

Tunisia

Bangladesh

Côte d'Ivoire

Indonesia

India

Nepal

Philippines

Chile

Algeria

Costa Rica

Zimbabwe

Colombia Jamaica

Tanzania

Ghana

Venezuela

Nigeria

43

Time inconsistency and the inflation bias Lack of credibility may impart an inflation bias to

monetary policy. This lack of credibility may result from the time

inconsistency problem faced by policy announcements: a policy that is optimal ex ante may no longer be optimal ex post.

Reason: policymakers are concern about inflation as a policy goal and with the fact that inflation may carry benefits.

44

Barro and Gordon (1983): policymakers are concerned about both inflation and unemployment, with a loss function:

L = (1/2)(y - y)2 + (/2)( - )2, > 0,

y: current output, y: its desired level,

: actual inflation, : desired inflation rate,

: relative importance of deviations of inflation from its target value in the loss function.

(13)

~

~ ~

~

45

Expectations-augmented Phillips curve:

y = yL + ( - a) + u, > 0, yL < y

yL: long-term level of output,

a: expected inflation,

u: disturbance term with zero mean and constant variance,

yL < y: ensures that the policymakers have an incentive to raise output above its long-run value.

~

~(14)

46

Policymakers want private agents to expect low inflation, in order to exploit a favorable trade-off between inflation and output.

But the mere announcement of a policy of low inflation is not credible, because policymakers have an incentive to renege to increase output and reduce unemployment and private agents understand this renege.

Result: inflation will in equilibrium be higher than it would be

otherwise; monetary policy suffers from an inflation bias.

47

With a binding commitment to low inflation, = a; the loss function becomes:

L = (1/2)(yL - y + u)2 + (/2)( - )2.

~ ~

Substitute (14) in (13):

L=(1/2) {yL + ( - a) - y + u}2

+ (/2)( - )2

~

~

(15)

48

Under discretion, policymakers take expected inflation as given; the first-order condition for minimizing the expected value of (15) with respect to is:

+ = + (y - yL)

+ 2 + 2

2 (a - )~~~

In equilibrium, = a (Phillips curve) :

= + (y - yL)/.~~

49

In equilibrium output can deviate from its capacity level only as a result of random shocks:

y = yL + u.

The higher (y - yL), the higher the slope of the Phillips curve, and the lower the relative importance of inflation in the loss function, the higher inflation will be.

~

Under discretion, the equilibrium inflation rate will be higher than desired inflation.

50

Credible commitment to a policy rule is welfare enhancing compared with a discretionary policy.

If policymakers can credibly commit themselves to low inflation, the economy will be better off; output will be the same as in the discretionary policy case but inflation will be lower.

51

Nominal Anchors in Disinflation: Money vs. the

Exchange Rate Controllability and Effectiveness Adjustment Paths and Relative Costs Credibility, Fiscal Commitments, and Flexibility The Flexibilization Stage

52

Debated issues in the analysis of disinflation policies: relative merits of exchange-rate-based stabilization versus the targeting of money (or credit) growth in conjunction with exchange rate flexibility.

When information is complete and no distortions or rigidities are present, exchange-rate targets or monetary targets are equivalent policies under perfect capital mobility.

Fischer (1986): when there are multiperiod nominal contracts, exchange-rate targets dominate monetary targets under some configurations of the underlying parameters.

53

Agénor and Montiel (1999): under imperfect capital mobility, disinflation through a reduction in the nominal devaluation rate or a fall in the rate of growth of domestic credit are not equivalent.

Choice between the exchange rate and the money supply as a nominal anchor depends on three main considerations:

degree of controllability and the effectiveness of the instrument in bringing down inflation;

adjustment path of the economy and the relative costs associated with each instrument;

degree of credibility that each instrument commands, and its relationship with fiscal policy.

54

Controllability and Effectiveness Policymakers cannot control directly the money

supply, but fixing the exchange rate can be done relatively fast and without substantial costs.

When money demand is subject to large random shocks and velocity is unstable, the effectiveness of the money supply as an anchor is reduced.

But an exchange rate peg will anchor the price level through its direct impact on prices of tradables.

So fixing the exchange rate rather than the money stock may appear preferable.

55

Monitorable target may bolster the government's commitment to the stabilization effort and help to move new low-inflation equilibrium (Bruno, 1991).

Policymakers must be able to convince private agents that they are willing and able to defend the fixed exchange rate.

Exchange rate management may be difficult to achieve if the current account deficit is large or if official reserves are relatively low.

Speculative attacks may occur.

56

Adjustment paths and relative costs Money-based and exchange-rate-based

stabilization programs differ significantly.

Calvo and Végh (1993): Exchange-rate-based stabilization programs lead to

an initial expansion and a recession later on. Money-based programs cause initial contraction

in output. Former pattern: boom-recession cycle since

credibility of the stabilization program is low and perceived as temporary.

Agents, to take advantage of temporarily low prices of tradable goods, increase spending.

57

Result: current account deficit and real exchange rate appreciation by forcing the authorities eventually to abandon the attempt to fix the exchange rate.

Weak evidence in favor of large intertemporal substitution effects.

Reinhart and Végh (1995): it can explain the behavior of consumption for some of the programs implemented in the 1980s, but not for the tablita experiments of the 1970s in Argentina, Chile, and Uruguay.

Nominal interest rates would have had to fall more than they did to account for a sizable fraction of the consumption boom recorded in the data.

58

Intertemporal effects were not large enough to explain the pattern of output.

Interactions between monetary and supply-side factors.

Roldós (1995): Due to cash-in-advance constraint, inflation

creates a wedge between the real rate of return on foreign-currency-denominated assets and domestic-currency-denominated assets.

When stabilization program based on a permanent reduction in the devaluation rate reduces the wedge and leads to an increase in the desired capital stock in the long run.

59

In the short run, consumption and investment increase, causing a real appreciation, a current account deficit, and an increase in output of home goods.

Over time, the increase in output of tradable goods lowers the initial current account deficit.

Not predict a recession at a later stage. Rebelo and Végh (1997):importance of supply-side

factors (real wages). How do the relative costs of money-based and

exchange-rate-based programs relate to their implications for remonetization?

60

Pegged-exchange rate system: Households and enterprises increase their real

money balances after a period of high inflation. Increase is satisfied automatically through the

balance of payments, as agents repatriate their capital held abroad and convert it costlessly into domestic currency.

Money supply anchor: No automatic mechanism for agents to rebuild their

real money balances. Many central banks refrain from domestic credit

expansion, and the economy remains undermonetized; high real interest rates and an overvalued currency.

61

Result: successful anti-inflation programs under a money supply target (and floating exchange rates) tend to be more contractionary than under pegged exchange rates.

62

Credibility, Fiscal Commitment, and Flexibility Degree of credibility of the money supply and the

exchange rate is important in choosing a nominal anchor.

Credibility depends on: policymakers' ability to convey clear signals about

their policy preferences; degree of controllability of policy instruments and

the dynamic adjustment path of the economy, as discussed earlier.

63

Public observability of the exchange rate as opposed to monetary and credit aggregates enhances the credibility of an exchange rate anchor.

Money-based stabilization by an immediate recession may lose credibility rapidly, if the short-term output and employment cost is high.

When the exchange rate is used as a nominal anchor, residual inflation in home goods prices may remain high combined with the expansion of aggregate demand, it may lead to a real appreciation.

This immediately weakens the credibility.

64

When lack of credibility is pervasive, the choice between money and the exchange rate may not matter; inflation will remain high regardless of the anchor.

An exchange-rate rule is, however, more successful in reducing inflation if there is some degree of credibility; initial expansion and the upward pressure on the real exchange rate will be dampened.

Exchange rate anchor may induce a higher commitment to undertake stabilization measures: fiscal adjustment.

65

If there are doubts about the government's commitment to fiscal restraint, an exchange rate peg would also lack credibility.

Végh (1992): ten exchange-rate-based programs aimed at stopping high chronic inflation.

Seven of them were failures: Two cases: failure was due to real appreciation of

the currency following slow convergence of inflation, in spite of achieving fiscal balance.

Remaining five: failure to implement a lasting fiscal adjustment was the main factor.

66

Flexibilization stage Although a pegged exchange rate is beneficial in

stopping high inflation, maintaining it for too long can become problematic.

Fixed nominal exchange rate, continued inflation higher than that prevailing in trading partners implies an appreciation of the real exchange rate erode external competitiveness and hinder export.

Deteriorating trade performance may force the authorities to depreciate the exchange rate and reignite inflationary pressures.

67

Shift toward a more flexible exchange rate regime once macroeconomic stability is achieved, is important to adjust to internal and external shocks.

Reduced commitment to low inflation must be renewed by fiscal and monetary discipline to maintain credibility.

68

Disinflation Programs: The Role of Credibility

Sources of Credibility Problems Enhancing Credibility

Big Bang and Gradualism Central Bank Independence Price Controls Aid as a Commitment Mechanism

69

Sources of credibility problemsFour different sources of credibility problems

in disinflation programs: Inconsistency between the objective of

disinflation and the policy instruments to achieve this objective, or sequencing of policy measures in a reform program.

Uncertainty associated with the policy environment and exogenous shocks.

Time inconsistency of policy announcements: program is optimal ex ante may not be ex post.

Incomplete or asymmetric information about policymakers' preferences.

70

Over time private agents will get to believe that policymakers are serious about their policy goal (learning process).

If policymakers have a long tradition of stop-and-go policies and the rotation of policymakers in office tends to be high, learning process will be slow.

Imperfect monitoring capability makes building reputation by policymakers more difficult; private agents may learn only gradually, through a backward-induction process.

71

Agénor and Taylor (1992): two methods for assessing the relative importance of the various sources of lack of credibility.

Specify a model of the inflationary process in which lagged inflation appears and estimate it with recursive least-squares techniques: changes in the behavior of the coefficient of the

lagged inflation rate (inertia or persistence) can be used to assess changes in the degree of credibility;

increased credibility will translate into a lower coefficient.

72

Study of changes in the behavior of the coefficient of a variable measuring the opportunity cost of holding domestic money.

Assumption: increased credibility will translate into a lower degree of persistence in the inflationary process and in a shift toward domestic-currency-denominated assets.

73

Enhancing credibilityFour ways:

adoption of a drastic (big bang) program as a way to signal the policymaker's commitment to disinflation;

central bank independence; imposition of price controls; conditional foreign assistance.

74

Big bang and gradualism Early phase of overadjustment as a means to

signal to skeptical agents the policymakers' commitment to inflation stabilization.

Easier to implement in countries where a new government with a broad anti-inflation mandate is just being put in place.

Although initial costs of a big bang program is high, it may be less than the costs of inflation continuing at a higher level for a long period of time.

Adopting an overly tight policy stance may exacerbate it because it may create expectations of future policy reversals.

75

Such expectations may result from the conjunction of two factors:

large short-run output and employment costs and a consequent loss of political support;

fact that the future benefits of disinflation are heavily discounted by the public.

In such conditions, enhancing the credibility may require to implement politically and economically sustainable measures instead of shock therapy.

76

Central bank independence Independence may be critical in countries where

central bank financing of government budget deficits is often the main source of inflation.

Factors that may mitigate the credibility gain by central bank independence:

Legal independence does not guarantee the absence of freedom from political interference and pressure on the central bank's policy decisions.

Blackburn and Christensen (1989): even an independent central bank may be willing to make concessions to the government in order to retain its autonomy.

77

Adhering to a rigid anti-inflation policy stance implemented by an independent central bank may be suboptimal in an economy subject to adverse economic shocks.

Credibility of monetary policy may depend on the overall stance of macroeconomic policy, rather than on the degree of central bank independence per se.

Independent monetary and fiscal authorities may adopt policies that generate coordination problems and costs that may outweigh the gain resulting from central bank autonomy alone.

78

Alesina and Tabellini (1990): Ambiguity of the net benefits from central bank

precommitment to low inflation. Reason: lower inflation reduces the revenue from

inflationary finance and forces the fiscal authority to resort to a higher level of distortionary taxation.

Early empirical studies focusing mostly on industrial countries: whenever central banks had the highest degree of autonomy also had the lowest levels of inflation.

79

Measuring central bank independence (Cukierman, 1992):

appointment mechanisms for the governor and board of directors;

turnover of central bank governors; approval mechanism for conducting monetary policy statutory requirements of the central bank regarding

its basic aim and financing of the budget deficit existence of a ceiling on total government borrowing

from the central bank.

80

Recent empirical literature: no robust association between central bank independence and inflation performance in industrial countries (Forder (1998)).

Sikken and De Haan (1998): For developing countries.

Measuring central bank independence using various indicators:

Synthetic legal measure (Cukierman, 1992): variables related to the appointment, dismissal,

and term of office of the governor of the central bank;

81

variables related to the resolution of conflicts between the executive branch and the central bank over monetary policy and the participation of the central bank in the budgetary process;

final objectives of the central bank, as stated in its charter;

legal restrictions on the ability of the public sector to borrow from the central bank.

Turnover rate of central bank governors, which attempts to capture actual independence.

Political vulnerability index: fraction of political transitions that are followed within six months by a replacement of the central bank governor.

82

Sikken and de Haan: no evidence that central bank independence creates an incentive for governments to maintain low fiscal deficits.

Found: measures of independence are not clearly related to the degree of monetization of government budget deficits by the central bank.

83

Price controls Case when inflationary process is characterized by

substantial inertia, stemming from explicit or implicit indexation.

This is a common feature of economies suffering from chronically high inflation.

Arguments in favor of temporary price controls (Dornbusch, Sturzenegger, and Wolf , 1990):

Realignment device: when pricing decisions are not instantaneous, price controls may help realign prices quickly and correct price distortions.

Coordination device: price controls help coordinate expectations toward a low inflation path.

84

Fiscal device: Reverse Olivera-Tanzi effect: transition from high to low inflation yields an

immediate gain in real revenue from taxation. Lower the borrowing needs of the government

from the central bank. Price controls may help enhance credibility by

serving as an additional nominal anchor. Blejer and Liviatan (1987): price controls may give

policymakers some breathing room. Persson and van Wijnbergen (1993): price controls

may help policymakers to reduce the cost of signaling their commitment to low inflation.

85

Successful temporary application of price controls: Israeli stabilization of 1985.

All nominal variables, including the exchange rate, were frozen.

With a sharp fiscal contraction and a restrictive monetary policy, price controls led to a quick reduction in inflation and enhanced government credibility, without a severe economic contraction.

Criticism of price controls: Use of price controls may be counterproductive

because they do not enable the public to learn whether inflation has really been stopped.

86

Credibility-enhancing effect of price controls may vanish if policymakers are unwilling or unable to control all prices in the economy (Agénor, 1995).

In this case price controls may lead to inflation inertia.

Problems at the practical level: Price controls have often been used as a substitute,

rather than a complement to fiscal and monetary adjustment.

Repeated use of price controls diminished their effectiveness, as economic agents anticipated the price increases that would follow the flexibilization stage.

87

Aid as a commitment mechanism Enhance credibility and the probability of program

success by subjecting to an external enforcement agency whose commitment to low inflation is well established (e.g. IMF).

They provide foreign assistance conditional on attaining specific macroeconomic policy targets.

Difficulties arise in judging the credibility-enhancing effect of foreign assistance:

Political considerations often play a role in deciding whether particular countries should receive external financial assistance support.

88

Conditionality is a double-edged sword. If the degree of conditionality attached to foreign aid is perceived to be excessive, uncertainty about external support may rise (Orphanides (1996)).

89

Two Recent stabilization Experiments

Egypt, 1992-97 Uganda, 1987-95 Egypt: exchange-rate-based stabilization. Uganda: money-based approach. Both show the role of fiscal adjustment in

stabilization programs.

90

Egypt, 1992-97Macroeconomic imbalances faced by Egypt

(Figure 5.7): Although inflation was not high, the fiscal deficit and

money growth rate were high. Dollarization ratio (share of foreign currency

deposits in total bank deposits) grew to about 46% in 1990.

Depreciation of about 30% between 1986 and 1991 of the real effective exchange rate.

Current account deficit reached about 10% in 1990/91.

91

Figure 5.7aEgypt: Macroeconomic Indicators, 1987-96

(In percent per annum, unless otherwise indicated)

Source: International Monetary Fund.

Brazil

1988 1990 1992 1994 1996

0

1

2

3

4

5

6

7 Real GDP growth

1988 1990 1992 1994 19960

10

20

30

Money, credit, and prices

Inflation

Broad money growth

Domestic credit growth

92

Figure 5.7bEgypt: Macroeconomic Indicators, 1987-96

(In percent per annum, unless otherwise indicated)

Source: International Monetary Fund.

2/ U.S. dollar deposits in percent of total deposits.

1988 1990 1992 1994 19960

10

20

30

40

50

60

1988 1990 1992 1994 1996-15

-10

-5

0

5

0

-15

Overall fiscal balance, exc. official grants (in % GDP)

Current account (in % GDP) Dollarization ratio 2/(in percent)

93

Figure 5.7cEgypt: Macroeconomic Indicators, 1987-96

(In percent per annum, unless otherwise indicated)

Source: International Monetary Fund.

3/ 1990=100; a rise is a depreciation.

1988 1990 1992 1994 1996

0

5

10

15

20

25

30

35

1988 1990 1992 1994 1996

50

60

70

80

90

100

110

120

130

100

Real effective exchange rate 3/

Nominal effective exchange rate 3/Total debt service/exports of goods and services

Total debt service/GNP

94

Gross external debt increased to 147% of GDP during the period 1988/89-1990/91.

Program of macroeconomic stabilization and structural reform was implemented in 1991.

Key features: combination of fiscal, monetary, and credit policies

together with an exchange rate anchor policy which was viewed as a way of: signaling the government's commitment to

disinflate; limiting pass-through effects of nominal

exchange rate changes on prices.

95

Substantial adjustment of fiscal accounts through:

general sales tax was introduced and a global income tax reform was implemented;

domestic-currency value of oil revenues and Suez Canal receipts as well as taxes on imports increased;

cuts in public expenditure; debt forgiveness and rescheduling agreement.

96

Results: overall deficit of the government declined sharply; primary fiscal balance of the government improved; gross domestic public debt fell; sharp reduction in broad money growth; rate of inflation declined; improvement in external accounts and a substantial

accumulation of foreign reserves; appreciation of real effective exchange rate; dollarization ratio fell.

97

Output cost of disinflation was a short-lived recession: real GDP growth dropped to 1.1% in 1990/91 but rebounded to 4.6% in 1994/95 and 5% on average for 1995/96-1996/97.

This reflected two factors: Real credit growth to the nongovernment sector

remained positive throughout the stabilization program.

Although interest rates were liberalized in early 1991 and jumped to high levels, they went down very quickly.

98

Key lessons: Importance of fiscal adjustment and external

factors. Debt reduction and write-offs contributed to

significantly to fiscal adjustment and improvements in the country's external accounts---despite an appreciating real exchange rate.

Tighter policies, with a potentially higher output cost, would have been needed otherwise if the external constraint had been more severe.

External assistance played an essential role in helping the program gain credibility rapidly.

99

Uganda, 1987-95Economic problems before applying the

program: In 1986, per capita GDP was estimated to be at

about 50% below the level of 1970. Inflation was high. Fixed exchange rate regime led to a significant real

appreciation and a loss of competitiveness. Foreign exchange shortages led to a considerable

spread between the official exchange rate and the parallel market exchange rate.

Deterioration in terms of trade.

100

In 1987: structural adjustment package, Economic Recovery Program, was applied.

Stabilization took place through a tightening of monetary and fiscal policies.

Currency depreciation was accompanied by a substantial increase in producer prices.

Import restrictions were removed. GDP growth responded quickly to the adjustment

measures (Figure 5.8). But inflation remained high.Main factors behind this

result: insufficient effort to tighten fiscal policy; excessive growth of bank credit to the government.

101

Figure 5.8aUganda: Macroeconomic Indicators, 1987-95 1/

(In percent per annum, unless otherwise indicated)

Source: Sharer et al. (1995), International Monetary Fund and World Bank.

1/ Data refer to the fiscal year (July 1-June30) except for exchange rates. 1988, for instance, refers to 1987/88.

1987 1989 1991 1993 19952

4

6

8

10 Real GDP growth

1987 1989 1991 1993 19950

50

100

150

200

250

0

Inflation

Broad money growth

102

Figure 5.8bUganda: Macroeconomic Indicators, 1987-95 1/

(In percent per annum, unless otherwise indicated)

Source: Sharer et al. (1995), International Monetary Fund and World Bank.

1/ Data refer to the fiscal year (July 1-June30) except for exchange rates. 1988, for instance, refers to 1987/88.

1987 1989 1991 1993 1995-20

-15

-10

-5

0

5

-201987 1989 1991 1993 1995

-50

0

50

100

150

-50

Total domestic credit growth

Government credit growth

Fiscal balance (in % GDP)

Current account balance

(in % GDP)

103

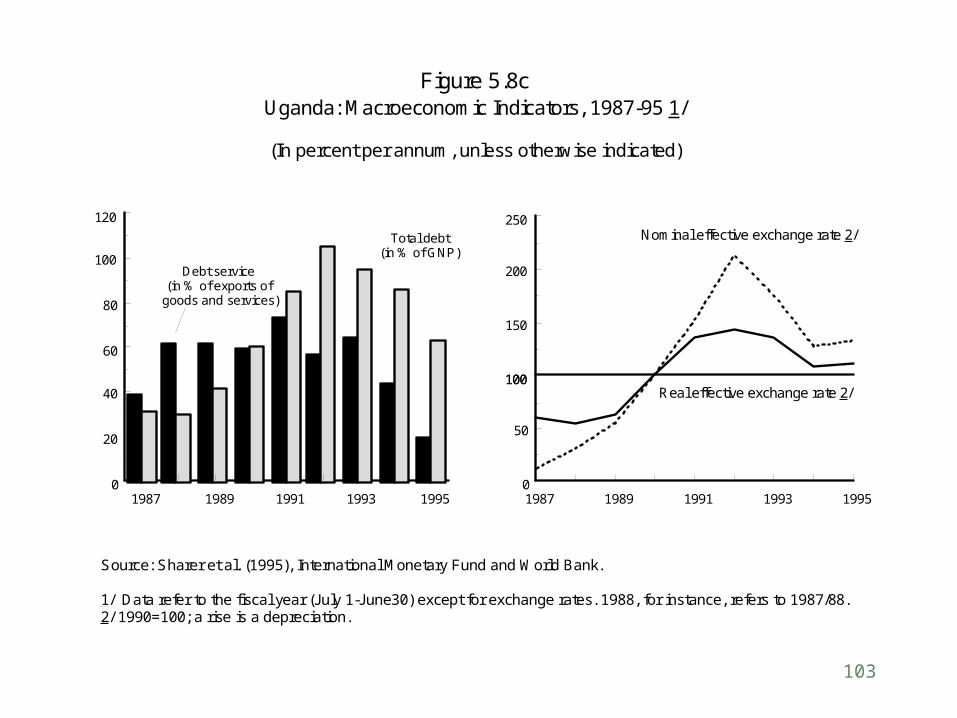

Figure 5.8cUganda: Macroeconomic Indicators, 1987-95 1/

(In percent per annum, unless otherwise indicated)

Source: Sharer et al. (1995), International Monetary Fund and World Bank.

1/ Data refer to the fiscal year (July 1-June30) except for exchange rates. 1988, for instance, refers to 1987/88.2/ 1990=100; a rise is a depreciation.

1987 1989 1991 1993 19950

50

100

150

200

250

100

1987 1989 1991 1993 19950

20

40

60

80

100

120

Real effective exchange rate 2/

Nominal effective exchange rate 2/

Debt service(in % of exports of

goods and services)

Total debt(in % of GNP)

104

Lack of fiscal adjustment and price stabilization and an improvement in external accounts reflected: maintenance of an overvalued exchange rate; difficult external environment.

Major deterioration in terms of trade during 1987/88 to 1992/93.

Lack of foreign exchange led to an accumulation of external arrears and an expansion of parallel currency markets.

105

Corrective actions during 1989/90 and 1990/91:

Devaluation took place. Government spending was cut, tax revenues

increased. Improvement in the fiscal position led to a reduction

in credit expansion and money supply growth. As a result, inflation dropped. Liberalizing domestic prices and the exchange

system led to production of noncoffee products. Current account improved. But inflation increased again because of:

weather-related supply factors;

106

renewed pressure on domestic credit growth to the government.

Fiscal and monetary discipline returned during the period 1992/93 to 1994/95:

strict expenditure control was accompanied with revenue measures and improved tax administration;

foreign exchange market was unified with the introduction of an interbank market;

restrictions on current international transactions were eliminated; this led to strong investment incentives to exporters and to large private capital inflows.

107

Result: prices actually fell; foreign exchange market was further liberalized; real output growth increased; external current account deficit fell.

108

Key results of Egypt and Uganda experiences:

Fiscal adjustment played a key role. This led to maintenance of money supply and

taming of inflation. Without a significant reduction in fiscal imbalances,

stabilization cannot last regardless of the anchor chosen.

109

Other results: Composition of fiscal adjustment has important

implications for growth. Importance of whether the fiscal deficit is reduced

by cutting unproductive expenditure or by raising a tax is that high rates of taxation levied on a narrow tax base foster tax evasion and may lead to an informal economy, exacerbating fiscal constraints in the longer run.