1 capital investment appraisal. 2 introduction as investments involve large resources, wrong...

TRANSCRIPT

1

Capital investment appraisal

2

Introduction

As investments involve large resources, wrong investment decisions are very expensive to correct

Managers are responsible for comparing and evaluating alternative projects so as to allocate limited resources and maximize the firm’s wealth

Basic techniques of making capital investment appraisal for evaluating proposed capital investment projects

3

Investment appraisal methods

Considering the time value of money concept

Ignoring the time value of money concept

•Net present value •Internal rate of return

•Payback period•Accounting rate of return

4

Net present value method

5

Time value of money

When facing different investment proposals, the management should choose the project that can generate the greatest addition of value to the company. For example,

Project A Project BInitial investment $100 $100Cash inflow at end of yearYear 1 $110Year 2 $121

6

At first sight, some may think that project B is better because it has a higher cash inflow.

However, the time value of money concept states that a dollar today is always worth more than a dollar in the future

The two projects are of equal value to the company because their present values are the same

7

After taking timing of cash flow into consideration,

Project A Project B

Present value of cash flow

(interest rate is 10% per annum) 110 121

(1+10%)(1+10%)2

= $100 $100

The two projects are of equal value to the company because their present values are the same

8

Factors leading to the changes in value of money

Opportunity cost of money

Erosion of purchasing power due to inflation

Uncertainty and risk

9

Opportunity cost of money

Opportunity cost of money refers to the cost incurred or income forgone by not using the money for other purpose

For surplus cash, the opportunity cost is the interest income forgone by investing the cash in other investments or depositing it in the bank

10

Erosion of purchasing power due to inflation

Inflation refers to the continual increase in the general price level of goods or services

During a period of inflation, prices of goods increase while the purchasing power of money decrease. The purchasing power of a dollar today is greater than that of the future

11

Uncertainty and risk

Investors tend to avoid risk. The uncertainty involved in future cash inflows is much higher than that in present cash inflows

If the level of risk rises, investors will expect a higher return as compensation.

For example, suppose an investor expects $100 for return now. After adding a 10% risk premium, he will expect $110 one year later

12

Discounting

13

Discounting

According to the time value of money concept, a dollar in one year is not worth the same as a dollar in anther year.

In evaluating a multi-year investment, cash inflows and outflows are generated in different years

It is necessary to convert the cash flows for different years into a common value at a common point of time, either at present or in the future

14

Discounting is the process of reducing future cash flows to present values with the use of an interest rate

Present value = FVn

(1+r)n

Where FV = Future value of an investmentn= Number of yearsr= Appropriate interest rate

15

Example

16

John has won a lucky draw. He is deciding whether to receive the Prize money of $3000 today or the following set of cash flows over the next three years:

Year Cash flow1 $11002 $12103 $1331

Future values Discount processes Present value

Year 1 $1100 $1100/1.1 $1000

Year 2 $1210 $1210/1.12 $1000

Year 3 $1331 $1331/1.13 $1000

17

Net present value method

18

Net present value method

Net present value (NPV) method is a process that uses the discounted cash flow of a project to determine whether the rate of return on that project is equal to, higher than, or lower than the desired rate of return

With the NPV method, we can compare the return on investment in capital projects with the return on an alternative equal risk investment in securities traded in financial market

19

Calculation procedures

1. Determining the discount rate

2. Calculating the NPV:

NPV = FV1 FV2 FV3 FVn

(1+r)1 (1+r)2 (1+r)3 (1+r)n+ + + - I0

where FV = future value of an investmentn = no. of yearsr = Rate of return available on an equivalent risk security in the financial marketI 0= initial investment

20

3. Interpreting the NPV derived as follows:NPVs Comments Reasons

<0 Reject the project The rate of return from the project is small than the rate of return from an equivalent risk investment

=0 Indifferent to accept or reject the project

The rate of return from the project is equal to the rate of return from an equivalent risk investment

>0 Accept the project The rate of return from the project is greater than the rate of return from an equivalent risk investment

Highest Accept the project If various project are considered, the project with highest positive NPV should be chosen

21

Example

22

A company is considering making several investments in the Production facilities for the new products with an estimated usefulLife of four years. The cash inflows and outflows are listed as follows:

ProjectA B C D$ $ $ $

Initial investment 900000 1000000 303730 1500000Cash inflowYear 1 120000 400000 100000 10000Year 2 250000 400000 100000 10000Year 3 400000 400000 100000 1000000Year 4 1300000 400000 100000 1000000

The appropriate discount rate of these investment is 12%

23

Required:(a) Calculate the NPV of each investment and determine whether

to accept it or not (assuming the company has unlimitedresources)

(b) If the company has limited resources, determine which investment should be accepted by referring to the highest NPV

24

Project A

NPV = 120000 250000 400000 13000001.12 1.122 1.123 1.124

+ + + - 900000

= $517327 (accepting)Project B

NPV = 40000 400000 400000 4000001.12 1.122 1.123 1.124

+ + + - 1000000

= $214920(accepting)

(a)

25

Project C

NPV = 100000 100000 100000 1000001.12 1.122 1.123 1.124

+ + + - 303730

= $0 (indifferent to accept or reject)Project D

NPV = 10000 10000 1000000 10000001.12 1.122 1.123 1.124

+ + + - 1500000

= -$135801(rejecting)

(a)

(b) With limited resources, the company should only accept project A because it generates the highest NPV

26

Advantages of NPV

Consistency with the time value of money concept

Consideration of all cash flows

Adoption of cash flows instead of accounting profit

27

Internal rate of return

28

Internal rate of return

The internal rate of return is the annual percentage return achieved by a project, of which the sum of discounted cash inflow over the life of the project is equal to the sum of discounted cash outflows

If the IRR is used to determine the NPV of a project, the NPV will be zero.

The company will accept this project only if the IRR is equal to or higher than the minimum rate of return or the cost of capital

29

Calculation procedures

1. By trial and error, find out the discount rate that will give a zero NPV

where FV = future value of an investment

n = no. of yearsr = internal rate of return

I 0= initial investment

2. If the NPV is positive, try a higher discount rate in order to give a negative NPV and vice versa

NPV = FV1 FV2 FV3 FVn

(1+r)1 (1+r)2 (1+r)3 (1+r)n+ + + - I0 = 0

30

3. After getting one positive NPV and one negative NPV, use interpolation to find out the rate giving zero NPV

IRR = L + PP – N

(H – L)

Where L = Discount rate of the low trial H = Discount rate of the high trial P = NPV of cash flows of the low trial N = NPV of cash flows of the high trial

31

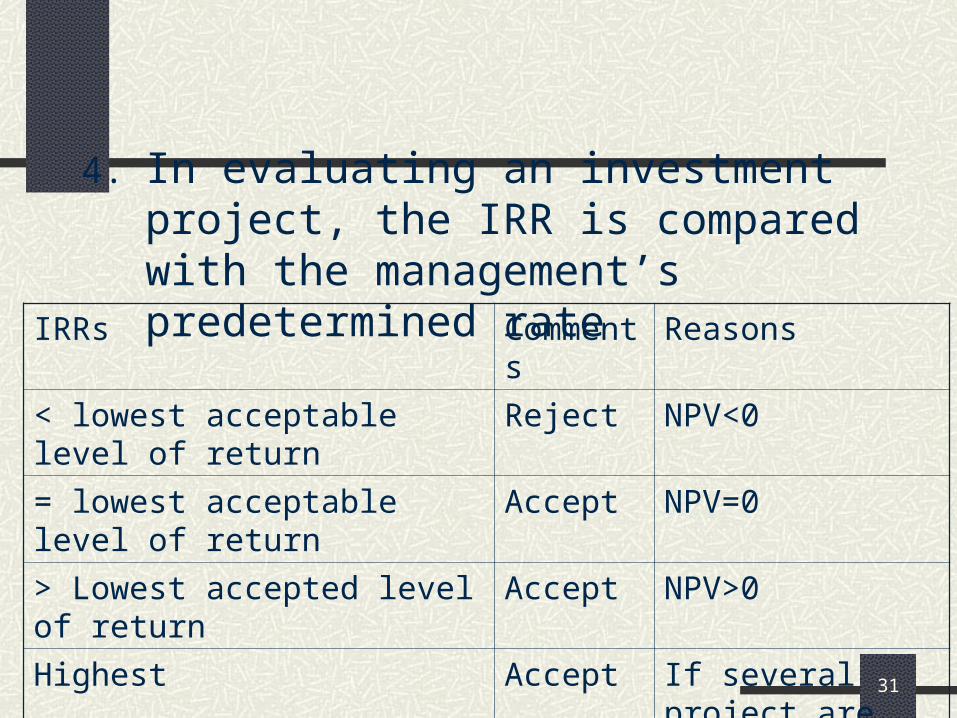

4. In evaluating an investment project, the IRR is compared with the management’s predetermined rate

IRRs Comments Reasons

< lowest acceptable level of return Reject NPV<0

= lowest acceptable level of return Accept NPV=0

> Lowest accepted level of return Accept NPV>0

Highest Accept If several project are considered, the highest IRR should be chosen

32

Example

33

A project costs $400 and produces a regular cash inflow of $200 at the end of each of the next three years. Calculate the IRR. If the minimum rate of return is 15 %, suggest with reason whether you Should accept the project or not.

NPV = $200 $200 $200(1+r)1 (1+r)2 (1+r)3

+ + - $400 = 0

NPV = $200 $200 $200

1.22 1.222 1.223+ + - $400 = 8.4

Assuming the discount rate is 22%

NPV = $200 $200 $200

1.24 1.242 1.243+ + - $400 = -3.8

Assuming the discount rate is 24%

34

IRR = L + PP – N

(H – L)

Where L = Discount rate of the low trial H = Discount rate of the high trial P = NPV of cash flows of the low trial N = NPV of cash flows of the high trial

IRR = 22% + 8.4 8.4 – (-3.8)

(24 – 22)%

= 23.38%

Since the IRR (23.38%) is higher than the minimum rate of return (15%),The project should be accepted

35

Payback period

36

Payback period

Payback period is the period of time it takes for a company to recover its initial investment in a project

The method measures the time required for a project’s cash flow to equalize the initial investment

37

Acceptance criterion

< predetermined cutoff period Accept the project

> Predetermined cutoff period Reject the project

38

Example

39

A company is considering making the following mutually exclusiveInvestments in the production facilities for the new products with an Estimated useful life of four years. The cash inflow and outflows areListed as follows:

Project A Project B$ $

Initial investment 900000 1000000Cash inflow at the end of yearYear 1 700000 600000Year 2 100000 400000Year 3 100000 400000Year 4 1300000 400000

Project A : 3 years Project B: 2 yearsProject B takes only two years to recover its initial investment. With The shortest payback period, the company will accept project B

40

Advantages of payback period

Easy to adopt

Facilities further evaluation After obtaining an acceptable payback period,

the project will be evaluated by other financial capital budgeting techniques

41

Disadvantages of Payback period

Ignore the cash flows after payback period

Adopt an arbitrary standard for the payback period

Ignores the timing of cash flow

42

Discounted payback period

The payback period method is criticized for ignoring the timing of cash flows, therefore discounted cash flows are used to calculate the discounted payback period

43

Example

44

A company is considering making the following mutually exclusive

investments in the production facilities for the new products with an

estimated useful life of four years. The cash inflow and outflows are

listed as follows:

Project A Project B

Initial investment 900000 1000000

Cash inflow at the end of year

Year 1 700000 600000

Year 2 100000 400000

Year 3 100000 400000

Year 4 1300000 400000

Discount cash inflow (20%)

45

Project A Project B$ $

Initial investment 900000 1000000Discounted cash flowYear 1 700000 400000

1.21 1.21

Year 2 100000 400000 1.22 1.22

Year 3 100000 400000 1.23 1.23

Year 4 100000 400000 1.24 1.24

Discount payback periodProject A 900000-710647

626929

= 583333 = 500000

3+ = 3.3 years

Project B 100000-777778 231481

2+ = 2.96 years

= 69444 = 277778

= 57870 = 231481

= 626929 = 192901

46

Accounting rate of return

47

Accounting rate of return

The accounting rate of return compares the average accounting profit with the average investment cost of project

The accounting profit can be expressed either before tax or after tax

48

Calculation procedures

ARR = Average net profit per year (over the life of the project)

Average investment cost

Average net profit per year =Total profit

No. of life of the project

Average investment cost = Initial investment 2

49

In evaluating an investment project, the ARR of the project is compared with a predetermined minimum acceptable accounting Rate of return:

ARRs Comments

< minimum acceptable rate Reject project

= minimum acceptable rate Accept project

> minimum acceptable rate Accept project

Highest Choose highest ARR

Acceptance criterion

50

Example

51

A company is considering whether to buy specialized machinesFor a new production line. The purchase price of machinery is $400000 and its estimated useful life is four years. There is no scrap Value after four yearsThe project income statements:

Year1 Year 2 Year 3 Year 4$ $ $ $

Revenue 310000 280000 280000 310000Depreciation 10000 100000 100000 100000Other expenses150000 100000 110000 120000Profit before tax 60000 80000 70000 90000Taxation (15%) 9000 12000 10500 13500

51000 68000 59500 76500

Should the company buy the new machinery if the minimum acceptableRate of return is 20%?

52

Average net income = 51000+68000+59500+76500

4= $63750

Average investment = 400000+0 2

= $200000

The cost of machinery is $400000 at the beginningThe cost of machinery is $0 at the end as depreciation is provided On straight line method and there is no scrap value

ARR = $63750$200000 = 31.875%

Since the ARR is 31.875%, which is higher than the minimum Acceptable rate of 20%, the company should invest in the new machinery.

53

Advantages of ARR

It is easy to understand and compute

It avoids using gross figures. Therefore, it enables comparisons to be made between projects with different useful lives

54

Disadvantages of ARR

It ignores the time value of money

ARR method seems to be less reliable than the NPV method. It adopts the accounting profit instead of cash flows calculation. The change of depreciation method may also alter the accounting profit