1 15 years of re market transition in pl - boom, bust or both? european property institute (pl) ...

TRANSCRIPT

1

15 years of RE Market Transition in PL -boom, bust or both?

European Property Institute (PL)www.ein-epi.eu

15th Annual ERES Conference

Krakow, June 18-21, 2008

2

The European Property Institute (EPI)

Polish Foundation - an independent think tank;

Established 2006 with offices in Warsaw and Kraków

Mission - foster European East-West real property integration;

Modality - exchange of knowledge and experience in real estate;

Activities - promoting better market data, conducting research and trend analyses of

selected segments of the real estate sector;

Pan-European target - work towards creating a cohesive and accessible European system

of information and database covering real estate markets;

Key challenge - initiating and cooperating in activities supporting European integration in

property sector’s institutions building and policy making;

Recent projects - publishing best-selling professional books and manuals; enhancing the

skills of domestic real estate professions.

3

Macroeonomic Revolution Macroeonomic Revolution Shock therapy - biting the bullet

Stabilization - market prices would tell us the truth Free prices showed real shortages / surpluses (misallocations) Free trade helped reduce shortages and export surpluses Positive real interest rates stimulated savings Stable / exchangable currency allowed to transact in PLN

Restructuring - change the way of producing / allocating Reallocation of resources to improve production efficiency Self-financing of State owned enterprises Privatization and restitution - property rights system Financial / capital markets to facilitate competition for resources

Stimulation - produce more with less Taxation reforms - to encourage more economic activity Labor market reforms - to increase labor supply Inflation prevention by monetary policy

Biting the bullet worked - economy started growing 1993

4

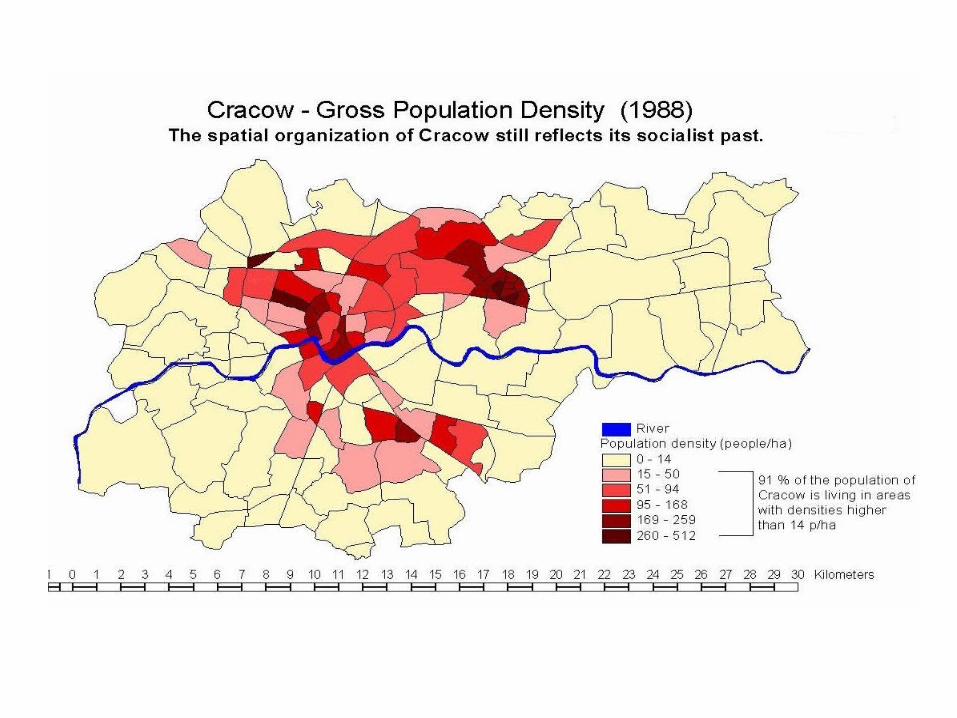

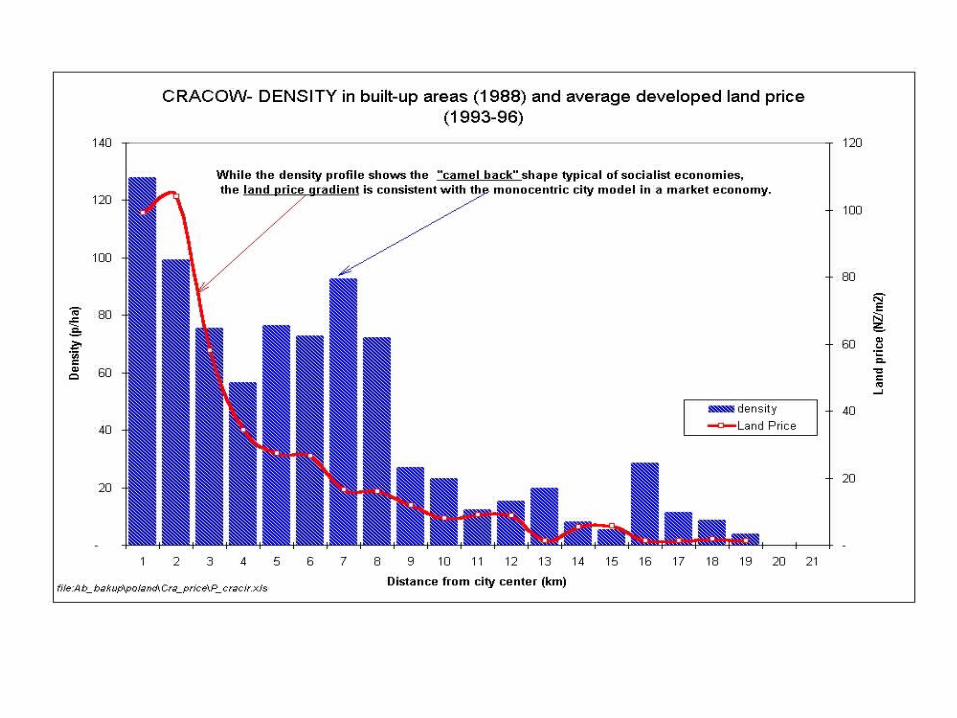

Inherited Profound Land MisallocationsMarket prices revealed inefficiencies of urban land use

Spatial misallocations - urban dispersion and sprawl # Many „empty runs” of expensive infrastructure Excessive energy / environmental costs Very expensive for local governments to maintain

Functional misallocations - grossly wrong proportions Too much industrial and agricultural land allocations # Not enough commercial and residential land allocations

Locational misallocations - inverted density gradient # Valuable land used for low-density functions Inexpensive land used for high-density functions

User misallocations - inefficient users sit on valuable land Administrative land allocation based on merit, not competition No land-use succession and recycling for 50 years

Inefficient land use compromises urban productivity

0

5

10

15

20

25

30

35

40

45 St. Petersburg

Moscow

Cracow

New York

Paris

Seoul

Curitiba

Hong Kong

Seattle

Share (%)of Industrial Land in Urban Areas

8

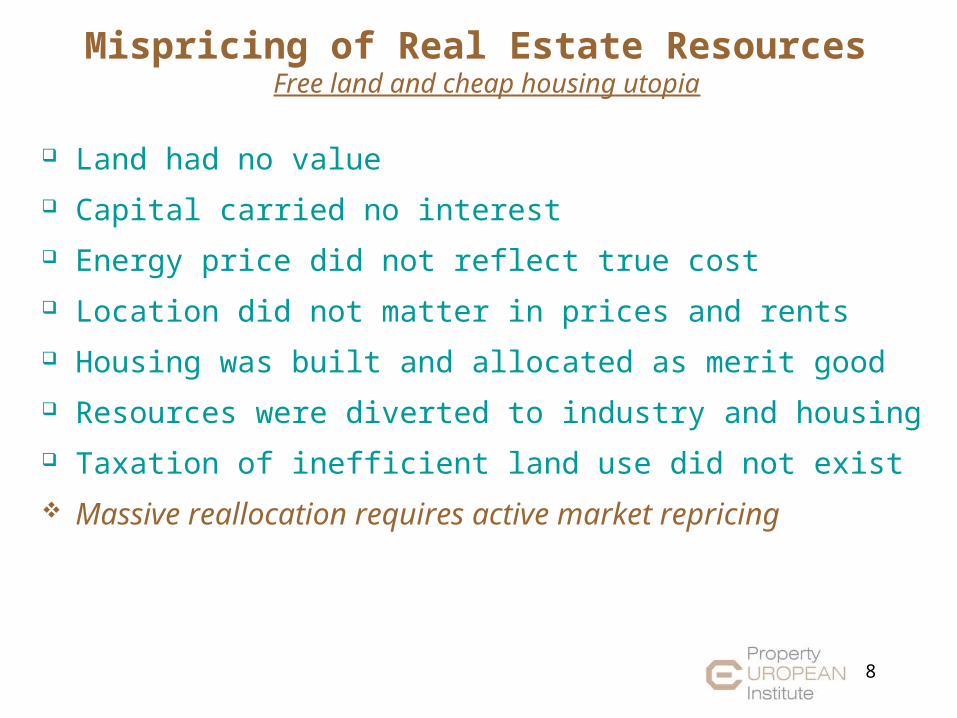

Mispricing of Real Estate Resources Free land and cheap housing utopia

Land had no value

Capital carried no interest

Energy price did not reflect true cost

Location did not matter in prices and rents

Housing was built and allocated as merit good

Resources were diverted to industry and housing

Taxation of inefficient land use did not exist

Massive reallocation requires active market repricing

9

Reform Directions and EffortsLearning to pay what it costs

Land is a capital and housing is a commodity - the Market Market needs clear / strong property rights Market needs efficient trading mechanism Market needs accessible / reliable information Market needs affordable credit system Market needs cost-recovery asset maintenance Market needs stable rules of the game Government needs to protect public interest Government needs market to produce the right product Government needs to help those who need it Enable the market + protect public interest = Big Challenge

10

Legal / Regulatory TransitionFundamentals of property rights

Constitution to recognize / protect private property rights

Civil Code to define real property rights Full ownership rights - freehold Polish Civil Code defines „assets” as ownership and other property

rights

The Real Estate Management Act of 21 August 1997 Real estate management

11

Legal / Regulatory TransitionAttaching / trading property rights

Preliminary contract – final contract

(down payment, earnest money deposit)

Notary public of 14 February 1991

Structure of land and mortgage registers of 6 July 1982

12

Legal / Regulatory TransitionReconciling public-private interests

Legacy of socialist urban planning and spot zoning: State (not local) deterministic monopoly over what is to be where Spot zoning with predetermined exact land use categories

Reforming spatial management during the transition: Planning Act of 1984 lasted till 1995 - new laws 1994, 2003, ??? New Study of conditions and directions of spatial development Old spot-zoning plans lasted till 2002/03 – new local plans on 20% of lands Planning permissions (WZ decisions) and building permits overly complex

Current thinking on planning and building permitting: Dilemma - fine tuning of existing law or revolutionary new law New gov’t effort to simplify planning and limit building permitting

Passive PPP through perpetual usufruct (land leaseholds) Active PPP through joint ventures and long-term leasing Harmonizing public and private interests remains suboptimal

13

Legal / Regulatory TransitionLicensing and taxing for the public interest

Regulating real estate professions Valuers / appraisers Property managers Brokers / agents

Taxing property to mobilize local revenues Recurrent property taxes Transfer taxes on real estate Gift and inheritance taxes

14

Transition of Residential MarketsFocus on demand support rather than on real supply forces

All successive governments in Poland focused on housing affordability: tax credits for purchase of new housing;

mortgage interest deduction from taxable income; and

housing finance skills and institutions to develop mortgage sector.

Supply of new housing has shrank because of hyperinflation, lack of financing and lack of developers …

… because – contrary to almost all other sectors of economy - here was nothing to be privatized in this sector !

Neglected supply side haunts policy makers today

15

Transition of Residential Markets Growth of indvidual investors and developers

0

20

40

60

80

100

120

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

units

co

mpl

eted

('0

00)

CO-OPS DEVELOPERS INDIVIDUALS OTHER

Źródło: GUS

16

Transition of Residential Markets Surprising first market downturn

0

50 000

100 000

150 000

200 000

250 000

300 000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

mie

szka

nia/

dom

y

Permits Starts Completions

Źródło: GUS

17

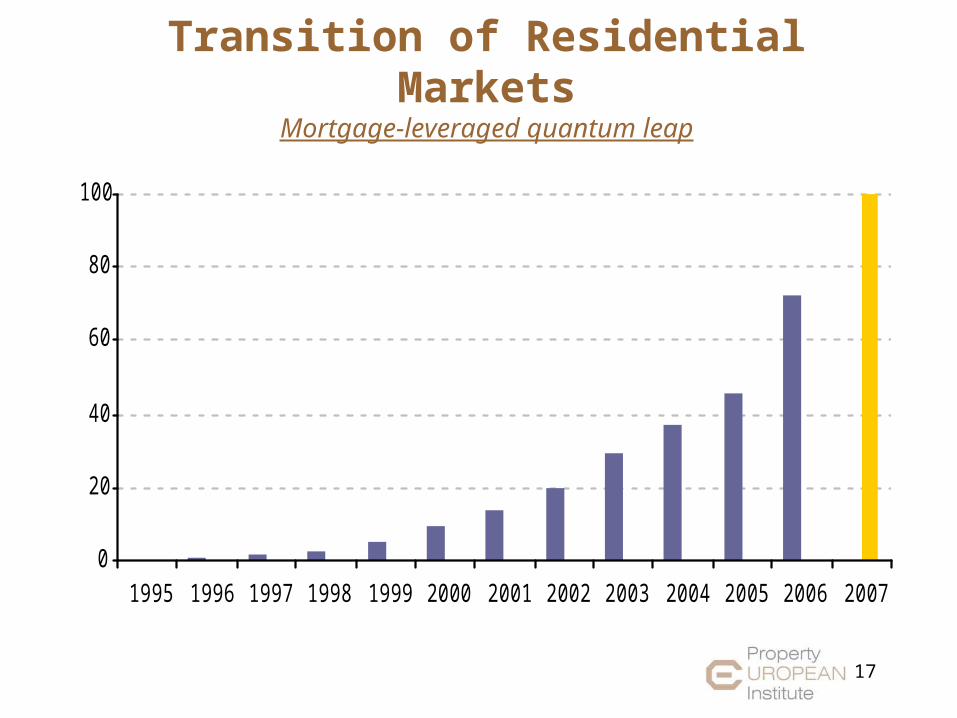

Transition of Residential MarketsMortgage-leveraged quantum leap

0

20

40

60

80

100

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

18

Transition of Residential MarketsMarket boom upon EU accession

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

2001 2002 2003 2004 2005 2006 1Q 2007 2Q 2007 3Q 2007 4Q 2007

PLN/sqm

Trójmiasto

Kraków

Warszawa

Źródło: REAS

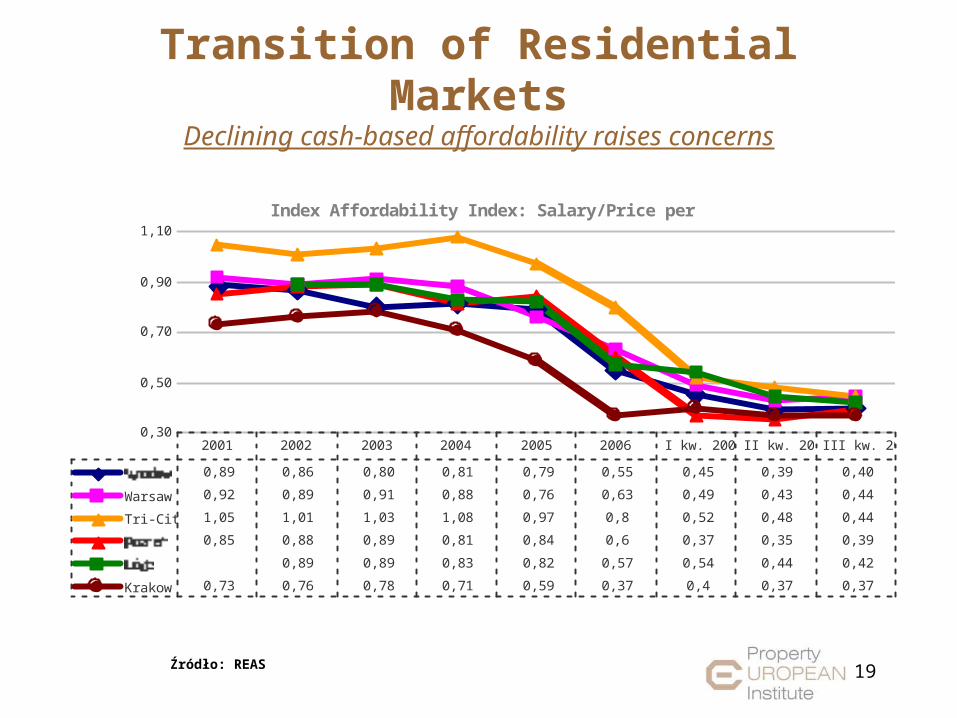

Transition of Residential MarketsDeclining cash-based affordability raises concerns

Index Affordability Index: Salary/Price per sqm.

0,30

0,50

0,70

0,90

1,10

0,89 0,86 0,80 0,81 0,79 0,55 0,45 0,39 0,40

Warsaw 0,92 0,89 0,91 0,88 0,76 0,63 0,49 0,43 0,44

Tri-City 1,05 1,01 1,03 1,08 0,97 0,8 0,52 0,48 0,44

0,85 0,88 0,89 0,81 0,84 0,6 0,37 0,35 0,39

0,89 0,89 0,83 0,82 0,57 0,54 0,44 0,42

Krakow 0,73 0,76 0,78 0,71 0,59 0,37 0,4 0,37 0,37

2001 2002 2003 2004 2005 2006 I kw. 2007 II kw. 2007 III kw. 2007

Źródło: REAS 19

20

Transition of Residential MarketsNeither boom nor bust - current market suspension

0

5.000

10.000

15.000

20.000

25.000

30.000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Supply Demand

Źródło: REAS

21

Transition of Real Estate MarketsPanel discussion

22

Thank you for your keen attention

EUROPEAN PROPERTY INSTITUTE ul. Srebrna 16, 00-810 Warsaw, POLAND

tel. +48 (22) 620 45 84fax. +48 (22) 620 62 89

[email protected] www.ein-epi.eu