081203 2009 preview - strategy outlook · 2008-12-03 · uralsib research team:...

TRANSCRIPT

URALSIB research team: [email protected]

December 2008

Strategy Russia ’09: Darkest Before Dawn

Investing For a Recovery

Russian Equity Research

STRATEGY RUSSIA ’09: DARKEST BEFORE DAWN

TABLE OF CONTENTS RUSSIA ‘09: DARKEST BEFORE DAWN ...................................................1 INVESTING FOR A RECOVERY.................................................................1 THE BIG PICTURE .................................................................................2 MAIN ASSUMPTIONS FOR 2009..............................................................3 MAIN RISKS FOR 2009 ..........................................................................5 SECTOR THEMES FOR 2009 ..................................................................6 DEFENSIVE PORTFOLIO STOCK PICKS ...................................................7 “PHOENIX RISING” STOCKS ...................................................................9 2008 IN REVIEW .................................................................................10 POSITIVE 1ST HALF – COLLAPSE IN 2ND ..............................................10 RUSSIA RELATIVE TO WORLD/GEM.....................................................11 THEMES .............................................................................................11 STOCK PERFORMANCE .......................................................................12 STRONG FIRST HALF ..........................................................................12 COMPLETE CHANGE IN SECOND HALF .................................................13 GREATER VOLATILITY .........................................................................13 TOUGH 1H09 FOLLOWED BY AN IMPROVEMENT....................................14 MACRO OVERVIEW .............................................................................14 BANKING ............................................................................................17 OIL & GAS..........................................................................................19 UTILITIES............................................................................................25 METALS & MINING ..............................................................................29 FERTILIZERS.......................................................................................32 AUTOMOTIVE ......................................................................................36 TRANSPORT .......................................................................................41 TELECOMS .........................................................................................45 CONSUMER GOODS & RETAIL .............................................................50 REAL ESTATE .....................................................................................54

STRATEGY

RUSSIAN EQUITY RESEARCH

URALSIB does, and seeks to do, business with the companies covered in their research reports. Consequently, investors should be aware that URALSIB may have a conflict of interest that could affect the objectivity of this report. This report should not be used as the only single factor governing investment decisions. Disclosures and analyst certifications are located at the end of the body of this report. © URALSIB Capital 2008

URALSIB research team, [email protected]

RUSSIA ’09: DARKEST

BEFORE DAWN INVESTING FOR A RECOVERY

High beta Russia. Conditions in the Russian economy will get worse before recovering in third or fourth quarter of next year. The equity market will remain weak, with volatility driven by a combination of domestic news and the trend in global – especially emerging – equity markets and commodities. But most of the blue chips and corporate debt issues are now pricing in an even worse case scenario. This is an excessive reaction considering that the country and the largest corporations are well positioned to survive the economic whirlwind, even as growth is collapsing over the medium term. Investing into some equities and debt issues that are now priced at distressed levels will prove very profitable beyond this period of weakness. The current valuations pay investors for the timing uncertainty. At this stage, the most reasonable scenario is for continued weakness in asset prices through the first half of 2009, with a strong recovery in the second half. The downside risk is an even deeper global recession than expected, while the risk to the upside is that investors will anticipate recovery earlier and buy into high-beta markets such as Russia.

Phoenix Rising. We recommend two portfolios for investors: First, the defensive portfolio, which is comprised of high conviction stocks that we believe are very well placed to deliver strong relative performance during the expected tough first half market conditions. These stocks should also be amongst the first to rise in absolute terms when the market rallies. We recommend buying these stocks today. The second portfolio, the phoenix rising portfolio, is comprised of the highest conviction stocks along with others that we expect to remain weak during down markets, but which are well positioned for strong gains when the rally starts. We recommend buying these shares during the down days in the first quarter.

Mirror image of 2008. In 2009 we expect the Russian investment climate to form a mirror image of that seen in 2008. Prices through 1H09 will remain very volatile and, despite some bear market rallies, generally weak. We anticipate very bad economic and corporate news in 1H09 and the equity markets may again test the recent lows in that period. Although the outlook for the start of the year is bad, the case is improving for a much more favorable investment backdrop in 2H09. The massive amount of liquidity that governments around the world are pumping into their economies and the measures being taken to prevent a prolonged recession should have a positive impact in 2H09, in our view. That, plus output cuts that materials and commodities producers are making, should produce a real inflationary boost to economies and commodity prices later in the year.

RTS target ranges. It is very difficult to specify a realistic target for the RTS Index over the next year as there are simply far too many variables and possible scenarios, both externally and for the domestic economy. A year-end rally may yet occur this year given the optimism generated by the US President-elect Barack Obama’s proposals to stimulate the economy and similar packages put in place by other governments. A reality check is inevitable in the first and second quarters of next year. Given recent volatility, the RTS could close out this year anywhere in the range 550 to 800. The trading range in 1H09 is again likely to be very wide, possibly between 500 on the downside and 1,200 on the upside. Although we expect a very volatile and mainly weak 1Q09 we do expect a stronger end to first half. We expect a mid-year level closer to the upper end of that range. How the market closes out the full year will depend on how the global economy performs, how oil and other commodities trade and how investors perceive investment risk in Russia.

Defensive Stocks

AFK Sistema Comstar-UTS

Federal Grid Company Gazprom

Gazprom Neft Magnit

MTS OGK-4

Polyus Gold Raspadskaya Raven Russia

RusHydro Silvinit comm Silvinit pref

TMK * Stocks that we believe are best placed to weather an economic whirlwind during 1H09 (in alphabetical order)

Note: Market data as of 21 November 2008

2

STRATEGY DARKEST BEFORE DAWN

Tough conditions, but survivable. Russia has enough financial resources to weather the economic storm over the winter months, although economic growth will certainly deteriorate very sharply. The country is also sufficiently adaptable to withstand a long period of global downturn, in our view. The fact that the economy has not yet achieved any real trade or investment integration with the rest of the world can be a virtue in such periods. Had the current debt and commodity crisis occurred in, say another three to four years’ time, the destructive effects would have been much greater. For now, the extent of contagion is limited and will allow the country to batten down the hatches to survive the hurricane. Of course the major external contagion is the price of oil. Oil (and gas) revenues are very critical for the Russian economy and to investor perception of currency risk and overall country risk. We expect continued weakness in the oil price into early 2009 before it sees some stability and a recovery later in the year.

Picking the stocks best placed for a recovery. In this note we review the current trading conditions for each sector and set out our macro overview to assess the operating outlook for each in 2009. From this we identify the companies that are best placed today to outperform both the economy and the rest of the stock market through the turbulence expected over the next six months. These stocks are listed in the table above on the right. The investment case for each is set out later in this note. We also identify the stocks that in our opinion are best placed to lead a market rally in 2H09. These are our favored long-term plays and are also set out in the table below on the right.

THE BIG PICTURE Assets now priced at distressed levels. The basic investment case for Russia – the reason to buy assets – is that the country will survive this financial and economic crisis. The economy will experience a severe downturn and many companies will face major difficulties. Not all the current major owners will be able to hold on to their equity, and we are likely to see major restructuring in the banking, real estate and some consumer sectors. But no major bank will fail and no major corporation will default on its debt. At current levels the market is assuming a worst-case scenario, with many companies valued barely above distressed levels. We believe this is a complete exaggeration and these valuations will recover once the financial crisis ends and the shoots of recovery appear in 2H09.

More emphasis on reforms. We hope the Russian government will treat the crisis as a wake-up call and place greater emphasis on reforms once the dust has settled. To maintain the government’s aim of increasing investment in the country and ensuring greater economic diversity, Russia will need to attract greater inflows of foreign investment. This can only be done with a much improved business climate and business practices. The pace of reform has moved far too slowly up until now but will hopefully pick up in 2009. Reform of the financial markets can now be included in the list of much needed, and now obvious, reforms – not just how the markets operate, but why Russia lacks a sizeable domestic investor base (i.e. pension funds). The latter problem has contributed to the extreme volatility in the markets since September. Prime Minister Vladimir Putin’s call for legislation to ban insider trading is a positive indicator of that.

“Phoenix Rising” Stocks

Stocks in defensive portfolio, plus

DIXY Group EVRAZ

LSR Group LUKOIL Mechel NLMK

Norilsk Nickel PIK Group Sberbank

TNK-BP Holding VimpelCom

VTB X5 Retail Group

* Stocks that we believe are well placed to benefit from the expected recovery in commodities, economic activity and investor sentiment through 2H09 (in alphabetical order).

3

STRATEGY DARKEST BEFORE DAWN

MAIN ASSUMPTIONS FOR 2009 Key assumptions. We make a number of assumptions in our analysis and forecast of economic trends and in assessing each sector outlook. These assumptions can be split into two groups: international and domestic.

International. Our assumptions for the global climate include:

Growth. The IMF projects a severe downturn in the US economy in 4Q08 and through to 1Q09 followed by a gradual climb to a positive growth number in 3Q09 and leading to stronger growth in 4Q09. The fund does warn that the extent of the decline may be worse than it expects and the steepness of the recovery line more shallow, but its expectations for investment markets and commodity prices are generally in line with ours.

Inflation. The huge financial packages put in place in the major economies (with more likely to come) plus drastic cuts in interest rates will inevitably lead to higher inflation across the globe. This would eventually be good for asset price appreciation and for commodities.

US dollar. The US dollar will likely remain relatively strong against the euro and most major currencies into early 2009 but will then weaken significantly through the course of the year as President-elect Obama plans to spend enormous sums of money to bail out stricken industries, such as the auto-makers, and to fund major public projects. Printing money on a large scale will inevitably weaken the dollar. We expect the yen to remain the strongest international currency, with sterling performing better relative to both the dollar and the euro. Even though the UK economy is declining faster than the eurozone, it is likely to emerge quicker due to less contagion and fewer political problems than exist inside the eurozone.

Oil. The price of oil will likely test new lows and generally remain weak over the next few months. This is because demand is falling fast and any move by OPEC and other producers are, of necessity, behind the curve. There are also some holders of oil-derivative instruments that still need to unwind into the year-end and early 2009. But from mid 1Q09 the extent of the demand destruction should be clearer and production better balanced. Our other major assumption is that OPEC discipline will hold and that the cartel will adhere to its promised production levels. In this scenario, price weakness would be followed by a strengthening in 2H09. We assume an average price for Brent of between $70 and $75/bbl through 2009 and 2010, with Urals trailing by between $3 and $4/bbl.

Gold. The price of gold (and to a lesser extent, silver) is set to rise in 1H09 as the dollar weakens and economic and corporate news flow reflects the deteriorating conditions this winter. Gold will emerge as a strong savings haven. Expect to see new record highs in 1H09.

Metals. In keeping with our global macro, inflation and currency assumptions, we expect to see stronger metal prices in 2H09. The fact that many big producers, including in Russia, are cutting output and closing some units will accelerate the pace of the price recovery when it comes.

IMF assumes a decline in global growth until next summer then stability before a late-year recovery.

Gold looks set to shine in 2009

US dollar is expected to weaken in 2009 as the new administration prints dollars to fund the huge bailout packages

We expect Brent to average close to $70/bbl through 2009 but with continued volatility, and price strength only in 2H09

4

STRATEGY DARKEST BEFORE DAWN

Domestic. Our main domestic assumptions include:

Default risk. There is zero risk of a sovereign default or a default by any state owned/controlled company and very low risk of a technical default from any major enterprise. The main risk lies with ruble issues of smaller companies; we expect some technical defaults at least.

Banks. No high-street bank will fail, but the share of non-performing loans will increase significantly. Bad debt write-offs will inevitably increase.

Economic growth. GDP growth will continue to fall through to 1Q09. This will entail further job losses and company closures. Macroeconomic news flow is likely to be at its worst in late 1Q09 and early 2Q. But as commodity prices rally in 2H09 and confidence rebuilds, we expect the economy to improve. (Note: our main economic assumptions are set out in the Macro Overview section later in this note.)

Consumer. The economic crisis spells the end, for a time, to consumption growth in Russia and by Russians in foreign markets.

Real estate. The price of real estate, both commercial and residential, will fall a lot more than already seen. The market will likely reach a bottom in 2Q09.

Ruble. The gradual widening of the CBR’s currency basket will continue and the government will allow the foreign currency reserves to decline until at least mid-January. At that point a major reassessment will be made and any change of course revealed. At present the government appears resolved to hold the ruble steady, albeit with regular widening of the “basket” trading band.

Inflation. The government will not achieve single-digit inflation in 2009 given the massive liquidity injection into the economy. The prospects for inflation far below 10% in 2010 are not too promising, either.

Budget. We anticipate the government will conduct a major review of its budget assumptions for 2009 and 2010, sot likely in February, when there will hopefully be a clearer picture with regard to economic trends and revenue projections (i.e. the oil price).

Oil production. We expect a production decline of at least 2% in 2009, with a drop of up to 5% also possible. This would mean a loss of production and exports of between 200,000 and 500,000 bpd by the end of the year. The lower production will be due to large cuts in oil field spending by the oil majors prompted by lower cash flows, the lower oil price and high taxes.

Equity issuance. Equity issuance will be zero or negligible in 1H09, with volumes picking up in 2H09. Only around $2.6 bln of the $100 bln of new equity originally targeted for 2008 and 2009 has so far been placed. The outlook for 2009 is for around $10 bln; all hopes of that figure being exceeded rest with a bullish 4Q09.

M&A. We anticipate a surge in mergers and acquisitions in 2009 as companies and investors with cash use the opportunity to acquire assets from financially strapped owners. Industry consolidation is already underway in the banking sector and is expected in the consumer sector and others. Many companies will have to combine in order to survive.

Considerable problems to be overcome at home

Chasing oil Ruble/US$ and Urals $/bbl

Source: Bloomberg

22232425262728

01/0

8

02/0

8

03/0

8

04/08

05/0

8

06/08

07/0

8

08/08

09/0

8

10/08

11/0

8

-150-125-100-75-50-250RUB/$ L.H.

OIL Urals*(-1) R.H. Scale

5

STRATEGY DARKEST BEFORE DAWN

MAIN RISKS FOR 2009 Economy. If the financial packages being put in place in the US and elsewhere do not stop the global economy slipping into a deeper, longer recession, the hoped-for bounce in commodity prices would be delayed. This would also have a negative impact on the domestic economy and pull growth lower this winter, which would also mean more job losses and business closures than currently anticipated.

Oil and the ruble. If global economic growth drops by more than expected and/or OPEC does not match lower demand with production cuts, the price of crude will fall closer to the long-run average of $30/bbl. In this event, it is unlikely that Russia would have enough financial reserves, or indeed be willing to burn them at a faster pace, making devaluation inevitable.

Oil spike. A spike cannot be ruled out. This would of course require a supply shock, such as an attack against Iran and it then retaliating or a major conflict in Nigeria. Right now the prospects are low but they cannot be completely ignored.

Political stability. If the ruble undergoes a devaluation and, at the same time, the economy slips into recession with more widespread job losses and company failures, this would be reflected in an inevitable collapse in public confidence in the government and senior ministers. Political instability, and changes, would follow.

China. A sharp drop in Chinese growth would hit the prospects for a rally in commodities, and in Asian economies, through the second half and would push prices much lower in the interim. The risk of social instability would also rise, which would delay any recovery in both China and in commodity-dominated countries such as Russia.

Conflicts. Any conflict similar to that with Georgia would further damage Russia’s position with the EU. Relations between Russia and the EU are likely to be particularly sensitive in the first six months of next year, when the Czech Republic holds the rotating presidency.

Czech presidency. The Czech Republic takes over the EU presidency from 1 January. Although Brussels and the larger EU countries have the greater say in dealings with Moscow, the Czech presidency will give the East European countries a greater voice, with the obvious potential for conflict.

Corporate governance. We have already witnessed a deterioration in corporate governance standards, which is affecting how investors view Russia risk. If this trend continues and minority investors’ interest are harmed, the investment risk premium will rise further. Uralkali. How the issue surrounding Uralkali turns out will have a very direct and long lasting impact on the perception of Russia risk.

Relations with the EU may be tougher next year

Corporate governance standards starting to slip

6

STRATEGY DARKEST BEFORE DAWN

SECTOR THEMES FOR 2009 Main themes. The backdrop of a slowing economy and generally weak commodity prices will of course provide the main investment theme through at least 1H09. The other main themes, which we have incorporated into our review of each industry sector and stock selection, include:

Ruble weakness against the dollar and euro. This factor will increase the value of export earnings for industries such as oil, gas and other commodities. It will also increase the cost of servicing foreign debt and the cost of imported goods. That, in turn, may help companies competing against imported goods, such as food manufacturers.

Cost reduction. Industries with a high cost content in materials, such as cement, coal, pipes and steel, will see a big drop in costs in 2009. We are already seeing evidence of this and it will become much more apparent in the costs of oil companies, for example, in 1H09.

Consolidation. Already evident in the banking and financial sectors, we may see more acquisitions and mergers across other industries, such as the retail sector.

Regional variations. Regions dominated by one large industry will be more obviously affected by the slowdown than other regions that are either are dependant on federal budget support or have a more diversified economy.

Consumer industries. Russia’s retailers are facing into a much tougher 1H09, with already evident slowing in spending expected to get much worse. The trend will be towards lower priced goods, particularly in food retailing, with discounters expected to outperform the higher priced outlets.

Utilities. The main risks to the sector come from reduced electricity demand as the economy slows and an expected drop in deregulated wholesale prices. We favor the more efficient operators in this environment. We expect the distribution companies to face a tough environment because of a likely drop in connection fees. These fees made up to 22% of total revenues for Moscow distribution companies and 28% for Lenenergo. The Federal Grid Company is the best protected from the expected downturn in revenues.

Banking. The big challenge facing all banks in 2009 will be the rising level of non-performing loans and bad debts. The creditworthiness of corporations and individuals will worsen as the economy slows and unemployment rises. Industry consolidation will step up a pace as the stronger banks take out the weaker/troubled banks.

Manufacturing. This sector is heading for a major downturn with industries such as auto manufacturers already announcing production and staff cuts. A late recovering sector.

Media. Likely to suffer from a drop in advertising as the economy slows and companies scale back spending. RBC took a big hit with stock market investments, an issue that raises corporate governance risk.

Metals & Mining. The industry is suffering from a lack of demand, falling prices, rising bad debts and limited access to trade finance. The outlook for the 1H09 looks dreadful and most companies will report very bad 1H09 results. The major hope is for a recovery in 2H09, if demand picks up a little but against a backdrop of reduced supply, as producers continue to scale back capacity in 1Q09. Gold is expected to be preferred as a safe haven play (silver to a lesser extent), and that will be positive for sentiment towards the gold producers.

Banks will face the challenge of higher non-performing loans

Expected big drop in material costs will help boost profits

7

STRATEGY DARKEST BEFORE DAWN

Oil and gas. The oil stocks are likely to underperform during 1H09, as we expect the present tough operating conditions to affect the financial results for 4Q08 and 1Q09. These results will not be reported until next summer and will affect investor perceptions. Costs are beginning to fall across the industry, as the price of materials such as cement drop. This should provide a more positive backdrop for 2H09. Longer-term drivers include diversification into the more profitable retail segment and the use of new technologies. The big question mark, apart from the oil price, is oil taxation, with the industry continuing to lobby for bigger cuts and the Finance Ministry opposing it.

Real estate. If history repeats itself (in line with other economic slowdowns, e.g. Asia 1997/1999) then this will be the last sector to recover. Raven Russia is in our conviction list because of its unique specialization in industrial warehousing. That segment is very under supplied, leaving the company with plenty of scope for growth even in a declining economy.

Telecoms. The mobile telecom stocks are relatively well positioned in a slowing economy, as the bulk of their revenue is for basic services. The example from other countries that have entered a slowdown earlier than Russia is that basic mobile activity holds up relatively well. That said, 4Q results are usually the weakest for seasonal reasons, and that will be a negative for the sector during late 1Q09 when the results are announced. Sentiment towards the regional telecom shares will continue to be affected by uncertainty over the fate of Svyazinvest. No significant progress is expected during 1H09, at least.

Transport. This is one of the most exposed industries to slowing disposable income and business activity, although this is not yet reflected in the rating of stocks such as Aeroflot. Considerable downside risk exists.

DEFENSIVE PORTFOLIO STOCK PICKS

Stock Ticker Price,* Mkt Cap*, Free Target Upside***, 2009E$ $ mln float, % price, $ % P/E

Comstar-UTS CMST LI 1.8 746 35 13 643 1.3Federal Grid Co FEES 0.004 1,667 20 NR n/a n/aGazprom GSPBEX 3.4 81,292 40 NR n/aGazprom Neft SIBN 1.5 7,230 3 NR n/aMagnit MGNT 10.3 738 19 UR n/aOGK-4 OGKD 0.010 630 1 0 536 21.7MTS MBT US 21.7 8,639 41 94 334 3.0Polyus Gold PLZL 15.0 2,636 45 50 233 7.5Raspadskaya RASP 1.1 859 18 12 991 0.7Raven Russia RUS LN 0.4 192 21 1 192 3.2RusHydro HYDR 0.015 3,749 21 0 684 3.2Silvinit comm SILV 465.0 3,639 11 NR 7.4Silvinit pref SILVP 160.0 85 NR n/aAFK Sistema SSA LI 4.0 1,930 19 42 950 1.8TMK TMKS LI 1.8 393 23 UR - 0.3* priced as of close November 28; ** based on DCF analysis; Source: Bloomberg, URALSIB estimates

High-Conviction Portfolio

*** upside to DCF target price Comstar-UTS. Comstar-UTS’s core business is highly profitable and relatively well protected against a slowdown in the economy. Regional expansion offers good growth potential. The company has a strong management team, a good balance sheet and healthy cash flows. It may benefit from the state buying of its stake in Svyazinvest for cash and MGTS shares.

Federal Grid Co. The Federal Grid Co. does not have any connection fees to worry about (this revenue stream will fall for others) and is looking at a relatively safe 20% increase in transmission revenues for 2009. While cost growth is expected to exceed inflation, the company will still enjoy positive cash flow growth in 2009. It has a good balance sheet.

Oil industry faces a challenge from lower capex spending

8

STRATEGY DARKEST BEFORE DAWN

Gazprom. Gazprom’s business is based on fixed-supply contracts that will secure its income through 1H09. These contracts may be reduced in 2H09 if the oil price remains low. The company is moving ahead with plans to develop major new projects with international partners, who will share the costs.

Gazprom Neft. Gazprom Neft is the best positioned of the oil majors in terms of a balance between costs, output and cash flows. The free float is very small but Gazprom has declared big ambitions for the company. Hence, Buy when any stock is available.

Magnit. Russia’s second-largest food retailer is well prepared for the slowing consumer spending to come. It has the best balance sheet in the sector and no US dollar debt. Its price-sensitive product range should sell well in a downturn and help it win market share from more expensive competitors.

OGK-4. Unlike other generators, OGK-4 and RusHydro are not facing the problem of rising non-performing loans and bad debts. They are the most efficient operators in the industry, with good balance sheets and cash flows for 2009 based on tariff increases.

MTS. Mobile services are much more resilient that other parts of the consumer sector during a downturn, especially basic voice services. The company will generate strong cash flows and will pay a big dividend to its major shareholder (AFK Sistema) and to minorities. Its debt position is much better than that of VimpelCom.

Polyus Gold. The best Russian equity proxy for the gold price. The price of gold is expected to rise as investors buy into it as a haven in the midst of financial turmoil, dollar weakness and general economic uncertainty through 1H09.

Raspadskaya. Raspadskaya has defensive qualities as its cash holdings are five times the size of its short-term debt.

Raven Russia. Russia has a massive shortage of class A warehouse space, even with the expected cooling of economic activity over the next two quarters. The company is on course to add 900,000 sqm of new space by 2010 to bring its total space to 1.2 mln sqm. The company pays a dividend equivalent to a 17% yield and will raise this to a yield equivalent (based on the current share price) of 20% by 2010.

RusHydro. Unlike other generators, OGK-4 and RusHydro are not facing the problem of rising non-performing loans and bad debts. They are the most efficient operators in the industry, with good balance sheets and cash flows for 2009 based on tariff increases.

Silvinit common. Stable potash prices and a 60% EBITDA margin should allow the company to generate positive net income, with a high tolerance, through both halves of 2009, even if output drops.

Silvinit pref. Silvinit is expected to pay out 10% of RAS profit to preferred shareholders – a yield of 15% and 19% for 2008 and 2009, respectively.

AFK Sistema. This stock trades at a very substantial discount to its sum-of-parts because the market is overestimating its short-term debt problems and is linking that with obvious problems at Sistema-HALS. The stock has very big upside once the debt issue is clarified/resolved.

TMK. TMK has a very good business model and demand for pipes is expected to remain high as demand from Gazprom, Transneft and the export market is still high. Net debt is high but very manageable considering anticipated cash flows.

Silvinit will pay a big dividend

OGK 4, RusHydro and Federal Grid Co are best placed in the power utilities sector

9

STRATEGY DARKEST BEFORE DAWN

“PHOENIX RISING” STOCKS These are the shares that we believe are well positioned to lead a rally in the markets during 2H09, along with the defensive portfolio (high-conviction) stocks listed above. See the individual sector summaries for details of our analysts’ view of these stocks.

Stock Ticker Price,* Mkt Cap*, Free Target Upside***, 2009E$ $ mln float, % price, $ % P/E

Dixy Group DIXY 1.72 103 18 UR n/a n/aEvraz EVR LI 3.9 1,433 14 - - 0.3 LSR Group LSRG LI 1.45 679 13 - - 1.1 LUKOIL LKOH 27.3 23,220 50 NR n/a n/aMechel MTL US 3.66 1,524 24 - - 0.4 NLMK NLMK LI 5.2 3,116 18 - - 0.7 Norilsk Nickel GMKN 68 12,963 45 - - 2.3 PIK Group PIK LI 0.49 242 17 33 0.2 Sberbank SBER 0.82 18,128 44 5 510 2.6 TNK-BP TNBP 0.515 8,316 3 NR n/a n/aVimpelCom VIP US 6.99 7,169 26 32 358 3.1 VTB VTBR LI 1.98 6,876 23 NR n/a n/aX5 FIVE LI 4.01 868 25 UR n/a n/a* priced as of close November 28; ** based on DCF analysis; Source: Bloomberg, URALSIB estimates

"Phoenix Rising" Portfolio

*** upside to DCF target price

10

STRATEGY DARKEST BEFORE DAWN

2008 IN REVIEW POSITIVE 1ST HALF – COLLAPSE IN 2ND

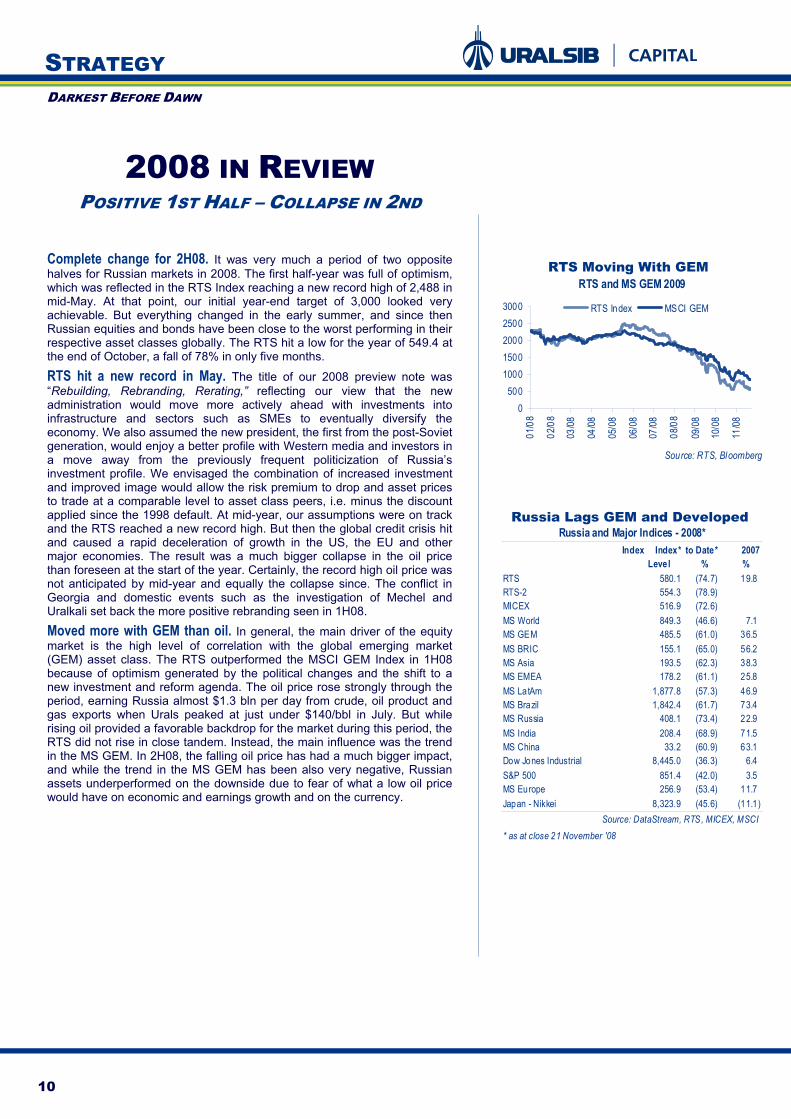

Complete change for 2H08. It was very much a period of two opposite halves for Russian markets in 2008. The first half-year was full of optimism, which was reflected in the RTS Index reaching a new record high of 2,488 in mid-May. At that point, our initial year-end target of 3,000 looked very achievable. But everything changed in the early summer, and since then Russian equities and bonds have been close to the worst performing in their respective asset classes globally. The RTS hit a low for the year of 549.4 at the end of October, a fall of 78% in only five months.

RTS hit a new record in May. The title of our 2008 preview note was “Rebuilding, Rebranding, Rerating,” reflecting our view that the new administration would move more actively ahead with investments into infrastructure and sectors such as SMEs to eventually diversify the economy. We also assumed the new president, the first from the post-Soviet generation, would enjoy a better profile with Western media and investors in a move away from the previously frequent politicization of Russia’s investment profile. We envisaged the combination of increased investment and improved image would allow the risk premium to drop and asset prices to trade at a comparable level to asset class peers, i.e. minus the discount applied since the 1998 default. At mid-year, our assumptions were on track and the RTS reached a new record high. But then the global credit crisis hit and caused a rapid deceleration of growth in the US, the EU and other major economies. The result was a much bigger collapse in the oil price than foreseen at the start of the year. Certainly, the record high oil price was not anticipated by mid-year and equally the collapse since. The conflict in Georgia and domestic events such as the investigation of Mechel and Uralkali set back the more positive rebranding seen in 1H08.

Moved more with GEM than oil. In general, the main driver of the equity market is the high level of correlation with the global emerging market (GEM) asset class. The RTS outperformed the MSCI GEM Index in 1H08 because of optimism generated by the political changes and the shift to a new investment and reform agenda. The oil price rose strongly through the period, earning Russia almost $1.3 bln per day from crude, oil product and gas exports when Urals peaked at just under $140/bbl in July. But while rising oil provided a favorable backdrop for the market during this period, the RTS did not rise in close tandem. Instead, the main influence was the trend in the MS GEM. In 2H08, the falling oil price has had a much bigger impact, and while the trend in the MS GEM has been also very negative, Russian assets underperformed on the downside due to fear of what a low oil price would have on economic and earnings growth and on the currency.

RTS and MS GEM 2009

Source: RTS, Bloomberg

0500

10001500200025003000

01/0

8

02/0

8

03/08

04/08

05/0

8

06/0

8

07/08

08/0

8

09/0

8

10/0

8

11/08

RTS Index MSCI GEM

RTS Moving With GEM

Index Index* to Date* 2007Level % %

RTS 580.1 (74.7) 19.8RTS-2 554.3 (78.9)MICEX 516.9 (72.6)MS World 849.3 (46.6) 7.1MS GEM 485.5 (61.0) 36.5MS BRIC 155.1 (65.0) 56.2MS Asia 193.5 (62.3) 38.3MS EMEA 178.2 (61.1) 25.8MS LatAm 1,877.8 (57.3) 46.9MS Brazil 1,842.4 (61.7) 73.4MS Russia 408.1 (73.4) 22.9MS India 208.4 (68.9) 71.5MS China 33.2 (60.9) 63.1Dow Jones Industrial 8,445.0 (36.3) 6.4S&P 500 851.4 (42.0) 3.5MS Europe 256.9 (53.4) 11.7Japan - Nikkei 8,323.9 (45.6) (11.1)

Russia and Major Indices - 2008*

Source: DataStream, RTS, MICEX, MSCI* as at close 21 November '08

Russia Lags GEM and Developed

11

STRATEGY DARKEST BEFORE DAWN

RUSSIA RELATIVE TO WORLD/GEM Big under-performance in 2H08. The table on the previous page shows the performance of Russian equities and the major emerging market and world indices in 2007 and year-to-date. In 1H08 the RTS performance was almost neutral, outperforming the MS GEM Index by almost 20%. Year-to-date the index is down almost 75%, while the MS GEM Index is off 61% and the world average down 47%. Hence, global equities are having a bad year on credit losses and growth concerns, emerging markets are worse because of the perception of higher risk in developing economies (and less developed financial structures), the contagion effects from a global slowing and, especially, the hit on commodity prices. Russia under-performed even more due its high dependency on commodities and a higher risk perception, which resulted from events associated with Georgia and Mechel.

THEMES Power utilities was bad all year. All industry sectors have been hit badly this year. But consistently the worst performing theme throughout the year has been the power utilities sector. It underperformed by 24% in the first half against an almost flat market. Since 1 July, the industry sector index is down another 82% to bring the year-to-date decline to 86.5%. The breakup of UES, the very complicated industry restructuring that resulted and the uncertainty over future tariffs, led most investors to avoid the theme in the first half. Traders did get involved with the sum-of-the-parts play, and many did so with borrowed cash. Hence, when the shares from the dissolution of UES started to arrive from July, when those traders were forced to dump them into a falling market. Since then, concerns over the future tariff regime, capex costs and a deterioration of corporate governance (as deals are cancelled) have also weighed on the sector.

Metals rolled over. The metals and mining sector was the best performing of the first half as the price of commodities, including steel and coal, reached new records. But it has been the second-worst performer since July, as commodity prices have been collapsing and demand falling away. Many companies have already announced capacity cuts and job losses. The banks have mirrored the problems in the global financial sector and, even though Russian banks are not exposed to the sort of mortgage and derivative losses of their western counterparts, the share prices have tracked lower with them. The telecom sector tracked lower in the first half as the mobiles moved down with the US equity markets and the fixed line operators were hit with uncertainties over Svyazinvest, etc.

Oil and gas has been relatively good. The consumer sector held up well in the first half year, as the industry was viewed as defensive and enjoyed steady growth in the expanding domestic economy. That changed in recent months as worries grow over operating margins and business growth. Many of the owners/major shareholders of the main operators are also highly leveraged and that has added to the risk in the sector. The oil and gas theme has been the best this year (up until the end of November pricing date). The announcement, in May, that the government was to cut oil taxes, boosted the sector by almost 20% through May and helped the first half performance. In the second half, even though the price of oil has collapsed, state buying of shares in Gazprom and Rosneft has helped prevent a collapse similar to that of the metals and mining sector.

Real estate the worst. The worst performing sector has been real-estate. Falling prices of residential and commercial properties, project closures as demand dries up and high leverage in some companies has led to a major stock market value collapse for almost all companies.

Index 1H '08 2H '08*r to Date*Level* % % %

Oil & Gas 376.5 3.6 (71.5) (70.5)Metals & Mining 213.5 9.8 (86.4) (85.1)Consumer 280.2 (10.0) (74.3) (76.9)Power Utilities 134.1 (24.4) (82.1) (86.5)Telecom 321.8 (21.4) (72.3) (78.2)Banks** 152.3 (16.0) (77.1) (80.8)

Industry Sector Performance

Source: Uralsib Research, RTS

Power Utilities consistently bad

Real Estate Props The Table

Price* Year to Date* $ p/s %

Chelyabinsk Steel 340 (5.8)Chelyabinsk Pipe 3.5 (16.9)Lebedyansky 73 (20.7)TGK-2 0.00074 (26.0)TGK-10 2.9 (29.1)TGK-4 0.0008 (35.5)Aeroflot 2 .12 (42.5)Baltika 27 (46.0)Irkutskenergo 0.55 (53.8)Surgutneftegas 0.54 (56.5)RTS 580.12 (74.7)LSR Group 1.01 (92.5)Yuzhuraln ickel 100 (92.9)OGK-6 0.0085 (93.3)OGK-1 0.008 (93.5)Evraz 4.5 (94.2)Pharmacy 36.6 4 (94.5)Integra 0.91 (94.6)OGK-2 0.006 (96.1)PIK Group 0.5 (98.4)Sistema-Hals 0.112 (98.9)

Leaders & Laggards in 2008*

Source: RTS, Bloomberg

* Prices as at close 21 November '08

12

STRATEGY DARKEST BEFORE DAWN

STOCK PERFORMANCE Surgutneftegas the best performer among oils. The table in the side column shows the ten best and worst share price performances so far this year. The top of the list is a collection of companies that have traded little, in volume terms. The only major stock is Surgutneftegaz as investors hope that its large cash/investment portfolio places it in a relatively better position to that of its peers. The bottom of the list reflects the problems in the real-estate sector, in the steel companies and also the fears over Integra’s debt position.

Sistema-HALS was worst. The second table in the side column shows the performance of the most liquid blue chip stocks. Sistema-HALS loss of almost 99% of its market value since January reflects investor expectations that the company cannot survive. Evraz’s loss of 94% reflects the fear that the company might have problems refinancing its debt. However, the recently announced loan of $1.8 bln from VEB has addressed that.

STRONG FIRST HALF Global market influence. The main drivers of the relatively favorable – compared to global markets – first half performance were:

The political transition that took place very seamlessly with Vladimir Putin’s favored candidate easily winning a majority of the public vote in the March election. To investors that represented the ideal combination of the young reformer (Dmitry Medvedev) in the Kremlin and political stabilizer (Putin) in the Prime Minister’s role in the White House.

Apart from the political stability that ensued from the “managed” transition, the program for government adopted by the new President and his team was viewed as very investment friendly and growth orientated. He promised to substantially increase spending in infrastructure and to develop new industries, especially technology. He also promised to more actively push reforms in the judiciary and the bureaucracy and to tackle corruption.

The surging price of oil, gas and most other commodities was directly favorable for the Russian economy and the outlook for earnings growth. As the graph on the side shows, the rising price did not directly pull the RTS higher but it did provide the favorable backdrop that allowed the market to outperform other markets.

That contributed to the strong growth in the economy during the first half with GDP growing 8.5% in the 1Q08 and 7.5% in the 2Q08. Earnings growth across most industries was comfortably in double digits and well above the global average.

Strong fund flows. That combination of political stability, rising oil and a growing economy led to high levels of fund flows into Russia in the first half, as global investors increased exposure via Russia dedicated funds. In the first six months of the year, over $3 bln was invested into those funds that report their flows on a weekly basis. That compares, for example, with over $7 bln withdrawn from China funds for the period. Other capital flows into Russia were also net positive. Having suffered a net outflow of $24 bln in the first quarter, flows in the second quarter were positive by $34 bln.

Russia China** Brazil India GEM BRIC $ mln $ mln $ mln $ mln $ mln $ mln

2007 1,348 (2,028) 4,041 (629) 12,551 2,7381H '08 3,030 (7,230) 597 (620) (536) (577)2H '08* (1,349) 1,406 (1,097) (2,222) (3,272) (3,182)

Fund Flows 2008*

Source: EPFR Global* year to 21 November '08

Price* Year to Date* $/Sh %

Surgutneftegaz 0.54 (56.5)Rostelecom 5.1 (56.6)Polyus 15 (67.3)LUKoil 28.3 (67.5)Rosneft 2.98 (68.9)Novatek GDR 22 (71.4)Gazpromneft 1.775 (72.0)Tatneft 1.6 (73.6)Norilsk Nickel 67 (74.7)RTS 580.12 (74.7)Gazprom 3.32 (76.4)MTS 22.96 (77.4)TNK-BP 0.5 (77.6)RusHydro 0.0183 (78.0)Novolipetsk 0.87 (78.5)Magnit 10.5 (79.2)VTB 2.1 (79.4)Sberbank 0.84 (80.1)Vimpelcom 7.67 (81.6)Comstar 2 (84.1)Eurasia Drilling 4.1 (84.8)TMK 1.5 (86.3)Mechel 4.06 (87.5)X5 Retail Group 4.39 (88.0)Magnitogorsk Steel 0.15 (88.5)AFI Development 1 (89.0)WBD 13.68 (89.6)Uralkali 0.8 (89.7)Severstal 2.2 (90.3)Sistema 4 (90.4)LSR Group 1.01 (92.5)Evraz 4.5 (94.2)Integra 0.91 (94.6)PIK Group 0.5 (98.4)Sistema Hals 0.112 (98.9)

Blue Chip Leaders & Laggards in 2008*

Source: RTS, Bloomberg

* Prices as at close 21 Novemner '08

Main Traded Shares

RTS and Urals 2H'09

Source: RTS, Bloomberg

200

700

1200

1700

2200

2700

07/0

8

07/08

07/0

8

08/0

8

08/0

8

09/0

8

09/08

10/0

8

10/08

11/0

8

11/08

RTS Index OIL Ura ls

Equities Follow Oil Lower

Russia Was Best in 1H09

13

STRATEGY DARKEST BEFORE DAWN

COMPLETE CHANGE IN SECOND HALF More domestic in the second half. All that changed in 2H08 for the following reasons:

The situation in the global financial markets deteriorated quickly with institutions such as Freddie Mac, Fannie Mae, Bear Stearns and AIG having to be bailed out, while Lehman Brothers failed. Similar problems and rescues across Europe undermined investor confidence in all markets, hitting those with a higher risk profile, i.e. developing economies, the hardest. In recent months, the Russian government has put over $230 bln in place to ensure that no high-street banks fail and that the country’s most important enterprises can refinance their debts.

Fears over recession in the US and in most major economies hit valuations everywhere and undermined the high commodity prices as demand destruction started.

The domestic economy was in danger of overheating in the early summer with PPI at over 30% and consumer inflation at 15%. The very big fall in industrial production (to + less than 1.0%) at the end of June was a big surprise and reflected just how expensive the cost base in Russia had become.

The price of Brent crude peaked at just under $140/bbl on 11 July and since then it has fallen by 161% to $53.6/bbl. That has led to widespread fears over currency stability, much slower growth and has under-mined the key assumptions that had supported the more favorable first half view. The government has committed itself to a stable ruble policy, but as the price of oil falls and the dollar strengthens, the cost of that policy has jumped to over $20 bln per week.

The BP / AAR dispute over TNK grabbed headlines across the world for many months, with a lot investors viewing it as a sign of either a lack of power by the pro-business, reformer President, or a lack of interest.

The Prime Minister’s July attack against Mechel, in particular, and against the spiraling cost of materials was interpreted by investors as meaning that the state would impose price, aka profit, controls in the major sectors of the economy. Of course, that was not an issue for long as the price of metals collapsed globally. That event resulted in a drop of about 5% for the market and a spike in the withdrawal of money from Russia funds.

The conflict with Georgia in early August had a similar effect in terms of the market and fund outflows, as investors feared that the conflict would damage Russia’s international relationships and, therefore, trade and investment flows.

The reinvestigation of Uralkali over a mine accident in 2006, with a possible fine of $50 bln in the offing, has been interpreted as a second YUKOS, i.e. an attempted at nationalization or forced ownership change in a profitable enterprise. How this plays out will have a major impact on how investors view Russia risk and the credibility of President Medvedev’s reformist government.

GREATER VOLATILITY Spike from August. The table below shows the volatility trend for the RTS and especially the spike from August to September. The big increase in volatility is one reason why investors have been shy of Russia investment over recent months.

Risk Perception Spikes VolatilityRTS Volatility vs RTS Index

Source:RTS

0

50

100

150

200

1/1/2

007

4/1/

2007

7/1/2

007

10/1

/200

7

1/1/

2008

4/1/

2008

7/1/20

08

10/1

/200

8

050010001500200025003000RTS Volatility (GARCH)

Long Run VolatilityLower boundaryUpper boundaryRTS Index

14

STRATEGY DARKEST BEFORE DAWN

TOUGH 1H09 FOLLOWED

BY AN IMPROVEMENT MACRO OVERVIEW

Few countries likely to escape the credit crisis. The level of uncertainty that currently surrounds the global economic outlook leaves a lot of room for gloomy forecasts. Indeed, many of these forecasts may well prove correct, particularly since we have yet to witness the impact of the credit crisis on the real global economy. Anecdotal evidence suggests that this impact will be strong and few countries – if any – will be spared.

LOW CRUDE OIL PRICES WILL HURT, BUT NOT

THAT BADLY Crisis may only have a mild impact on Russia ... With its heavy dependence on global commodity markets as a source of the bulk of government and private sector revenues, there is little doubt that Russia is also going to share the pain. The big issue is how strong and protracted this crisis will be for Russia. We believe that Russia will endure a relatively mild crisis and its economy may escape recession and suffer only limited negative consequences for its social and political stability.

… thanks to strong growth momentum … There are three main reasons which lead us to support this view. Firstly, in previous years Russia has managed to gain significant growth momentum – in 2006 GDP grew by 7.4%YoY and by 8.1% in 2007 and 2008 growth is likely to come in at 7.2%. Even under the most pessimistic macroeconomic scenario it would require a significant amount of time to force an economy moving at such speed to a complete standstill. Given the inertia of macroeconomic trends we believe that even under the most unfavorable scenario for Russia, it would take at least 2-3 quarters for this growth to completely vanish (also, this scenario does not factor in any existing or future government measures to support growth).

… and government support … Secondly, the vulnerability of Russia’s growth pattern, which has been almost totally depended on external factors, might be offset by conservative RF Government fiscal policies. For a number of years the government has opted for quite stringent budgetary planning policy and has managed to accumulate a significant reserve fund. A large amount of Russia’s economic growth of the past few years has been funded via two sources: high returns from commodity exports and cheap global credit. However, both of these sources are no longer available. That said, growth has also been driven to a large extent by purely domestic factors such as, construction and consumption, services which could be – and are being – supported by targeted injections of state funds. While we are not holding our breath in expectation of extremely effective government investment or crisis management policies, we do think that the already-announced aid package which is equal in size to 15-20% of Russia’s GDP is capable of halting the development of the current crisis in Russia. Furthermore, it may even be sufficient to prevent the Russian economy slipping into the doldrums during the severest part of the ongoing global crisis.

Growth Could Accelerate in 2010GDP growth rate, YoY %

Source: Rosstat, URALSIB estimates

0.0

2.0

4.0

6.0

8.0

10.0

1Q04

4Q04

3Q05

2Q06

1Q07

4Q07

3Q08

2Q09

1Q10

4Q10

2006 2007 1H08 2008F 2009FGDP (% YoY) 7.4 8.1 8.0 7.2 4.3Industrial output (% YoY) 6.3 6.3 5.9 4.8 3.4Fixed investment (% YoY) 13.5 21.1 17.9 11.3 -1.8CPI (% YoY) 9.0 11.9 15.1 13.9 10.5Real incomes (% YoY) 10.2 10.7 8.5 7.6 0.5Retail sales (% YoY) 13.9 16.1 15.6 14.2 7.4Exports ($ bln) 303.6 354.4 237.3 459.6 374.7Imports ($ bln) 164.3 223.5 135.4 289.5 212.1Current account ($ bln) 94.3 76.2 63.6 93.6 78.1RUB/USD (eop) 26.3 24.6 23.4 27.5 26.8USD/EUR (eop) 1.32 1.47 1.53 1.20 1.40Urals crude oil average ($/bbl) 61.6 69.7 105.4 97.0 70.0

URALSIB macroeconomic forecast, Nov-08

Sources: Rosstat, Bloomberg, URALSIB estimates

Economic Slowdown Unavoidable

15

STRATEGY DARKEST BEFORE DAWN

…and an economy that remained largely closed to the world. The third reason is the relatively closed nature of the Russian economy which in many ways has not moved that far away from its Soviet heritage. As a result Russia may prove far better positioned to avoid the impact of the most negative external developments than many other emerging market economies. This is not without a certain irony since, Russia’s very low level of integration into the global economy were previously seen as one of the biggest stumbling blocks for its development. However, this very weakness could prove to be one of its biggest strengths in a time of crisis. It is also worth noting that Russia managed to pull through the 1998 crisis in which it was in a far weaker position than today. At that time, the country was lumbered with massive foreign debt and an almost nil level of investor trust following the default. To make matters worse, back in 1998 it had almost depleted reserves, an incapable president, an inexperienced and extremely inefficient bureaucracy and far higher dependence on consumer and food imports. What it did have though was a (albeit very inefficient) working economy and within twelve months of the crisis, the Russian economy was growing at a strong pace and providing its population with essentials.

Russia will be more resilient to crisis than a decade ago. Over the past decade, Russia has managed to modernize key sections of its economy namely, food, retail, and consumer and machinery manufacturing production assets as well as improving in many other areas, particularly within the state sector. All this means that today, Russia is simply far better prepared to withstand the negative fallout from a possible global recession – or a further slide in commodity prices – than it was a decade ago.

MACRO OVERVIEW: GDP GROWTH TO SLOW ON

LOWER DEMAND AMID HIGH INFLATION GDP growth expected to fall from 7.2% to 4.3%YoY. While Russia is, in our view, far better positioned to withstand the global crisis than many other emerging markets, it does not follow that it will emerge entirely unscathed. As a country with a strong dependence on commodity export revenues, Russia will be adversely affected by a downturn in global growth. In fact, it already has been. We anticipate that Russia’s export revenues and correspondingly, budget revenues will fall. This in turn will halt and could even reverse, domestic consumer and investment demand growth. As a consequence, national economic growth rates are likely to contract significantly. Based on a $70/bbl Urals crude oil forecast for 2009, GDP growth rate could fall from an estimated 7.2%YoY this year to only 4.3%. We expect growth dynamics to decelerate right up until mid-2009 with the low point in 2Q09 with 3.9%YoY GDP growth. In the second half of 2009 we expect a gradual improvement on the back of slightly higher crude oil prices (a forecast average of $78/bbl vs. $61/bbl in 1H09).

Softer domestic demand means a larger state role. Weaker global demand and commodity prices would mean some significant changes to the economic growth pattern in Russia. The two key growth drivers of the past 2-3 years – investment and consumer demand – are likely to lose much of their appeal. In 2009 we expect the volume of fixed investment to fall by 1.8%YoY and real income growth to slow dramatically to 0.5%YoY (vs. an estimated 7.6%YoY this year). The outcome is likely to be that the economy will become far more reliant on government spending to support growth and industrial output. Additionally, we forecast that industrial output will remain positive in 2009 at 3.4%YoY.

Lower Domestic Demand ...YoY %

Source: Rosstat, URALSIB estimates

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

2002

2003

2004

2005

2006

2007

2008

F

2009

F

2010

F

Real incomesRetail salesFixed investment

State: 99Foreign 39Ruble 60

Banks: Foreign 193Corporations 741

Foreign 187Domestic 481R.Bonds 73

Individuals 230Total Debt 1263Total Foreign Debt 488

Total Russia Debt ExposureTotal Russian Debt -Official Record*

Source: Central Bank, Uralsib estimates

... Will Support Trade SurplusTrade and current account balances: fact and forecast ($ bln)

Source: Rosstat, CBR, URALSIB estimates

020406080

100120140160180

2000

2001

2002

2003

2004

2005

2006

2007

2008

F

2009

F

2010

F

0

20

40

60

80

100

120Trade balanceCurrent accountUrals crude oil, $/bbl (RHS)

16

STRATEGY DARKEST BEFORE DAWN

Export volumes will fall, but so will imports. In spite of a widely-expected large drop in export volumes – we forecast that gross exports will fall by 18.5%YoY in 2009 to $375bln – we do not anticipate a running deficit in either Russia’s trade or current account balance any time soon. There are two major reasons for this: firstly, we expect a major contraction in import volumes due to falling domestic demand and rising credit costs and secondly, we expect Russia’s current negative capital account balance to gradually shift back into positive territory – a development that is likely to be helped by the stabilization of global credit and commodity markets which is expected to occur by mid-2009. We expect Russia to retain a sizeable current account surplus in 2009 of $78bln (versus an estimated $94bln surplus in 2008).

Inflation to remain in double digits in 2009-10. We forecast that next year global inflationary pressures will increase as the large cash injections made into the global financial system finally filter down to the real economy and the markets. Higher inflation would support crude oil prices and the ruble, but it would also make it more difficult for the Russian authorities to pare CPI rates down to single digits. Thus, we believe that Russian consumer inflation will remain at around 10.5%YoY for the bulk of 2009-2010.

EVERY CRISIS HAS A SILVER LINING The crisis could speed up economic restructuring. The speed and global nature of the unfolding crisis make it very difficult to accurately predict the full implications for any single economy. Russia’s high dependence on commodity revenues for maintaining stability and growth – which has over the past few years strengthened – makes it extremely unlikely that the crisis will pass by the national economy and the man in the street. However, we believe there are some potential long-term benefits to be gained as a result of the global crisis.

…kick-starting reform. The first obvious benefit could be the renewal of the state reform process. The recent extended period of rapidly increasing commodity prices has significantly undermined the determination of Russia’s political and economic elite to push forward with much-needed changes to the economy and political system. However, as state coffers start to shrink, attention will start to really focus on Russia’s excessive dependence on the sale of natural resources and the virtually forgotten Dutch disease debate, since this type of development path is extremely risky, particularly in a time of crisis. So as the crisis begins to really bite, we can expect renewed reform efforts across a wide range of areas including, taxation, rule of law, democratization and support for burgeoning industries, etc. We also believe that the relationship between the state and the business community, which have soured in recent years, will undergo something of a revival.

Russia’s previous growth model was doomed anyway. Another positive aspect of the current crisis is its timing. The fact that events began to unfold in the late summer of 2007 has in fact, saved Russia from a much deeper and most likely, far more destructive crisis in the future. The reason why is that throughout 2005-2007 Russia’s development model became almost completely reliant on two factors beyond its control i.e. high commodity prices and easy access to cheap credit. Working in combination these two factors provided a rapid expansion in domestic consumption which boosted Russia’s GDP growth rates. However, if this model were to be left untouched for another few years – i.e. if the next crisis had hit several years later – the impact would have been far graver, since government spending would have reached unsustainable levels and external non-state debt could have ballooned to a level which put the entire private sector at risk of bankruptcy.

Economic imbalances likely to shrink. The crisis will also provide Russia with new opportunities to gradually deflate domestic bubbles in property, prices and wages. It could also help the government to address and perhaps start to resolve some of Russia’s major structural imbalances such as the huge disparities in incomes and regional development.

State Support is CostlyWeekly change in international reserves, $ bln

Source: CBR

-40-30-20-10

01020

04/01

25/01

15/02

07/03

28/03

18/04

09/05

30/05

20/06

11/07

01/08

22/08

12/09

03/10

24/10

But Ruble Stability Ensured,Thus FarCBR's bi-currency basket index: fact and corridor

Source: CBR, URALSIB estimates

28.228.729.229.730.230.7

04/08

05/08

06/08

07/08

08/08

09/08

10/08

11/08

Min. Fact Max.

17

STRATEGY DARKEST BEFORE DAWN

BANKS TO GAIN ONCE THE

WORST IS BEHIND US TRADING AT 50% OF EQUITY; SET TO REBOUND

Situation not as bad as the market has priced in. All of Russia’s listed banks are currently valued by the market below their 2008E shareholders’ equity and are trading below 1.0 on 2008E P/BV. Under normal conditions this would signal that the market expects a marked deterioration in the Russian banking sector – a worst-case scenario consisting of a substantial rise in non-performing loans, a steep slowdown in loan growth, increased market risk and further uncertainty over sources of funding. In our view the Russian banks do not warrant such low valuations as the major players in particular are benefiting from state support which is mitigating risk. For this reason we believe the shares of the most liquid banking names are well set for a strong rebound in 2H09. At present we see risks more on the upside than on the downside.

Low risk profile, liquidity and state support are in focus. The banks best placed to rebound in 2H09 are those with low risk, good share liquidity and access to state support. We believe that as domestic liquidity improves all the Russian banking stocks are set to rebound, with the state-owned behemoths Sberbank and VTB poised to bounce first thanks to their superior share liquidity and higher degree of state support.

LOW DOWNSIDE RISK FOR BANKS, BUT

PRESSURE MAY CONTINUE Sberbank best placed for the rebound. Sberbank, Russia’s largest bank, is the best option for investors looking to take positions ahead of a possible recovery in the equity markets in 2H09 as it is a major recipient of government funds ($20 bln in subordinated loans) and does not bear as much risk as VTB or other private banks. Sberbank shares are trading at a 2008E P/BV of 0.6 vs. 0.4-0.5 for other Russian banks. This 20-40% premium is justified in our view by Sberbank’s lower risk exposure. Meanwhile, taking into account the high equity risk premium of at least 15% that investors are now applying to the Russian market, Sberbank is the only liquid name in the Russian banking universe likely to post profitability above this level in the medium term. State banks best placed to weather the storm in 2009

Comparative Valuations 2008E 2009E* P/E P/BV P/E P/BV Sberbank 3.4 0.6 2.6 0.5 VTB 12.5 0.4 7.5 0.4 Vozrozhdenie 2.6 0.5 1.9 0.4 Bank St. Petersburg 2.1 0.4 1.7 0.4

Source: Bloomberg, URALSIB estimates * Based on the assumptions presented below; may differ from official forecasts

Our 2009 Top Picks Sberbank

VTB

A firm grip on each segmentMarket Shares of Sberbank and VTB, 1H08, %

Source: Sberbank, VTB

30.4

50.2

31.619

114.7 7.5 10.9

0102030405060

Corp

orate

loans

Retai

lde

posit

s

Retai

loans

Corp

orate

depo

sits

Sberbank VTB

18

STRATEGY DARKEST BEFORE DAWN

NPLS TO INCREASE RAPIDLY … Economic downturn raises risk for banks. The crisis of confidence among banks, falling commodity prices and shortage of liquidity have placed significant strain on the Russian economy, which is reflected in our updated macro assumptions for 2009 (see Economics section). We believe the main risk for Russian banks during these tumultuous times comes from the worsening creditworthiness of domestic companies and individuals, especially as interest rates are on the rise. The downsizing of collateral on the back of the equity sell-off and negative revaluation of other assets is an additional issue for Russian banks that is causing them to build additional loan provisions. We believe the market is pricing in a worst-case scenario and that Sberbank and Bank St. Petersburg have the lowest credit risk exposure at present. Sberbank has a more conservative lending policy than the other banks and is therefore less vulnerable to credit risk.

Sberbank has a low risk profile Breakdown of Risks Facing Russia's Listed Banks as of 1H08 (IFRS)

Risks NPLs/gross Securities/ Retail deposits/ Wholesale funding/ Retail loans/ loans, % assets, % liabilities, % liabilities, % loans, % Sberbank 1.5 8.5 60.0 7.70 14.0 VTB 1.7 10.0 13.5 49.0 16.0 Vozrozhdenie 2.3 6.1 46.0 13.7 19.0 Bank St. Petersburg 1.4 16.6 28.0 18.9 10.5

Source: Company data, URALSIB estimates

… BUT WILL BE OFFSET BY MARGIN GROWTH We expect NIM to rise by at least 100 bps. Interest rates are set to increase on the back of huge demand for credit from Russian corporates and stricter lending policies. We believe the Russian banks will be able to pass on the increased costs to borrowers, who have no choice but to refinance debt via local banks and the state. As of end-1H08 Sberbank had the highest NIM of 6.9% among Russian banks, and this figure is set to increase on the back of the rising interest rate environment.

Supportive factors for Sberbank Comparison of Supportive Ratios as of 1H08 (IFRS)

NIM ROAE,% CAR,% Cost/income ratio,% State support Sberbank 6.9 20.2 13.4 50.9 High VTB 4.8 8.0 15.8 57.1 High Vozrozhdenie 6.4 25.0 14.4 57.5 Moderate Bank St. Petersburg 6.0 21.0 12.8 35.7 Moderate

Source: Company data, URALSIB estimates

… AND STATE SUPPORT Focus on the state-owned liquid names. Our top picks in the sector are Sberbank and VTB – both of which are state-owned and have the highest levels of share liquidity. Both banks are benefiting from state support, which in addition to widening interest margins will likely offset rising credit risk. Sberbank is in line to receive $20 bln in subordinated loans from the CBR and VTB will receive $7.3 bln from VEB, which should boost their capital ratios to above 20%. These loans will amount to more than 10% of Sberbank’s liabilities and 8% of VTB’s. We recommend that investors focus on Sberbank and VTB as best placed for a rebound in 2H09. We prefer Sberbank over VTB due to its lower risk profile.

Sberbank boosted by the stateSubordinated Loans as % of Liabilities

Source: URALSIB estimates

10.2%

8.0%

0%2%4%6%8%

10%12%

Sberbank VTB

19

STRATEGY DARKEST BEFORE DAWN

OIL & GAS SECTOR COST CONTROL, IMPROVED RETAIL, STRONG

CASH AND LOW DEBT

Value drivers in 2009: cost control and diversification into retail. In 2009 the domestic oil companies will create value mainly by lowering costs: either directly by reducing operating costs (which they can control) or indirectly by lobbying for lower taxes and tariffs for the industry. The era when valuations skyrocketed in tandem with the oil price is over. The key valuation drivers in the years to come will be increased use of modern technology, optimization of business processes (field development planning, effective logistics to maximize netbacks, diversification into retail, etc.) and effective cost control.

Timing during 2009. We believe 2Q-3Q09 will be the best time to invest in Russian oil stocks as the sector should by then be benefiting from a better macroeconomic outlook and improved investment climate in the sector, which will create strong buying opportunities for investors. These changes include:

the government revisiting the question of taxation on the sector, including mineral extraction tax (MET) and export tax formulas;

price declines in other sectors (metals, concrete, services) and lower fuel prices will likely have picked up and duly reflected in lifting and direct refining costs;

oil price stabilization, with the impact of Kudrin’s scissors disappearing; stabilization on the debt markets, which will open up new funding

opportunities; ruble depreciation against the US dollar, though inflation will remain

stable. We believe 1Q09 will be dominated by a wave of poor financials for 2H08 and will thus not provide an optimal time to accumulate positions in the stocks.

Oil stocks may drop furtherBrent Price and URALSIB O&G Index Performance

Source: Bloomberg, URALSIB estimates

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

01/08

02/08

03/08

04/08

05/08

06/08

07/08

08/08

09/08

10/08

11/08

12/08

01/09

02/09

03/09

04/09

05/09

06/09

07/09

08/09

08/09

09/09

URALSIB Oil&Gas IndexBrent, $/bbl

Russian oils to publish 3Q08

financials

End of financial storm, oil prices stabilize

MET cut-off rate changed from $9/bbl to

$15/bbl

Oil prices flat: Buy into efficiencyValue Creation Principle, 2009-10

Source: URALSIB estimates

Value creation in 2009-2010

Crude oil prices line

Costs line

Oil prices rocket: Buy if costs lagValue Creation Principle, 2007-1H08

Source: URALSIB estimates

Value creation in 2007-1H08

Crude oil prices line

Costs line

URALSIB oil&gas index vs RTS

Source: URALSIB estimates

0500

10001500200025003000

07/07

09/0

7

11/0

7

01/0

8

03/0

8

05/0

8

07/0

8

09/0

8

11/0

8

USIB O&G RTSI

20

STRATEGY DARKEST BEFORE DAWN

Oil price is set flat at $70/bbl. We set our long-term Brent price flat at $70/bbl; we also assume Brent will remain flat in 2009-10. We do not share the argument that prices will return to $100-150/bbl levels in the long term as cheap reserves are depleted and extraction costs are growing. We believe these trends will be countered by the increased use of more modern extraction methods and improved geological surveys, interpretation and modeling. We also do not believe that anticipated production cuts across the globe will eventually drive prices to high levels within the next 3-5 years as we expect demand to adjust accordingly. Nevertheless, we will continue to monitor the USD/EUR rate, as a weakening dollar could trigger a rebound in the oil price. Our Urals forecast is based on Urals/Brent discount analysis and assumes a flat discount of 2%.

2009E YoY 2009E to spot price

Value drivers YtD Average Spot Scenario estimate % %RUB/USD 24.4 27.4 26.14 7 (5)PPI, % 22.3 n/a 15.5 (30) n/aBrent, $/bbl 104 47 70 (33) 50Urals NW, $/bb l 101 44 68 (32) 57Gasoline, $/ton 903 409 617 (32) 51Jet fue l, $/ton 1,045 587 668 (36) 14Diesel, $/ton 1,013 576 601 (41) 4Fuel o il, $/ton 470 184 291 (38) 58

Forecast of core oil macroeconomic data No return to 2008 levels, but we may see a rebound

2008E

Source: URALSIB estimates

THE INVESTMENT CASE FOR 2009 Value gains through cost control and efficient retail. We believe the valuation paradigm will change in the years to come. In recent years the oil price has been the core value driver, but going forward we expect further valuation gains on the cost side from lower taxes, milder tariffs and improved control of operating costs. We also believe the companies diversified into retail oil product sales will benefit in the current environment of oil price volatility as domestic retail prices remain less volatile, the retail market itself is poorly penetrated by integrated companies and demand is inelastic.

AMBITIOUS PRE-CRISIS STRATEGY… Clarity over oil sector taxation. We believe the government will

review the tax burden on the oil sector next year. The oil companies have been fighting not just for tax cuts but for fundamental changes to the way in which MET and export duties are calculated. Sector taxes currently comprise up to 50% of total costs, hence profitability is highly dependant upon the companies’ lobbying ability and the government’s willingness to cut the tax burden.

Ruble weakening. A mild weakening of the ruble vs. the US dollar will increase sector profitability in dollar terms.

Deflation in other sectors set to seep through to oils. The oil companies have yet to benefit from a recent drop in domestic prices for metals, cement, etc as the goods, materials and services they are using in their operating activities were stocked before the crisis. We believe the effect of declining prices in the other sectors will feed into lower operating costs in the oil sector within six months.

Valuations P/E EV/EBITDA P/E EV/EBITDAGazprom 2.1 2.3 1.7 2.3Rosneft 2.8 2.5 2.7 4.2LUKoil 1.6 1.7 1.8 3.5TNK-BP 1.0 1.5 1.4 3.9Surgutneftegas 4.3 1.9 4.5 5.1Gazprom Neft 1.4 1.2 1.7 3.1Tatneft 1.5 1.6 2.0 1.5Average 2.1 1.7 2.3 3.6Median 1.5 1.7 1.9 3.7

2008E

Source: Company data, Bloomberg, URALSIB estimates

* Based on the assumptions presented below, may differ from official forecasts

Sector revaluation aheadComparative Valuations

2009E*

21

STRATEGY DARKEST BEFORE DAWN

Tariffs. We expect the oil companies will try to lobby for slower growth in tariffs or even a decrease for certain transportation routes. As we understand the oil companies have particularly targeted railroad tariffs and Transneft tariffs. In 2008 exports continued to decline due to falling demand and a relative drop in prices. Exports via railroad and pipeline decreased substantially in 4Q08. In the first half of November crude oil exports via pipeline declined as much as by 25% relative to October, according to Transneft.

Direct costs. Direct costs (controllable costs) should be the oil companies’ main priority. In light of the crisis many companies have already announced substantial cost cuts. We believe 2009-10 will see the companies applying the very latest technology to benefit first place.

GROWTH VIA RETAIL Retail segment is fragmented. The domestic retail market will provide additional shareholder value on the revenue side. The retail market is highly underpenetrated, so although we may see a slowdown in the consumption of petrol products next year, the oil companies have substantial scope to grow by raising their share of the domestic retail market. The integrated oil companies account for only 50% of the retail business. Over each of the last five years the integrated companies have posted double-digit growth in domestic retail sales of petroleum products, and we believe they could double the size of this business again over the next five years. In terms of filling stations, the oil companies control about 40% of the retail market. Other stations are operated by independents, which rarely control more then 10 outlets. Their efficiency varies substantially, depending upon several unpredictable factors. We believe the market share of the most inefficient independent retailers will be captured by the integrated oil companies.

TOP PICKS We like Gazprom, whatever the weather. In our view Gazprom will outperform the domestic oil peer group in 1Q09 as it is likely to be the only company capable of demonstrating strong results for 3Q-4Q08.

The company stands to benefit from a financial standpoint as the calculation for European export gas prices is based on oil, diesel and fuel oil prices and follows them with a lag of 6-9 months.

The planned deregulation of the domestic gas market will lead to rising prices on the domestic market.

The presence of the Russian government as Gazprom’s main shareholder implicitly guarantees the company’s obligations and allows it to borrow at low rates, which is extremely important during these testing times.