0601087 market analysis and new channel development

DESCRIPTION

Hi Friends This is supa bouy I am a mentor, Friend for all Management Aspirants, Any query related to anything in Management, Do write me @ [email protected]. I will try to assist the best way I can. Cheers to lyf…!!! Supa BouyTRANSCRIPT

A

PROJECT REPORT

ON

“MARKET ANALYSIS and NEW CHANNEL DEVELOPMENT”

FOR

HDFC Standard Life Insurance Company

SUBMITTED TO UNIVERSITY OF PUNEIN PARTIAL FULFILLMENT OF 2 YEARS FULL TIME COURSE

MASTERS IN BUSINESS ADMINISTRATION (M.B.A.)

SUBMITTED BY

PAWAN NIGAM

(BATCH - 2006-08)

BRACT’sVishwakarma Institute of Management,

Kodhawa Pune- 411014.

1

COLLEGE CERTIFICATE

TO WHOMSOEVER IT MAY CONCERN

This to certify that Mr. Pawan Nigam is a bonafide student of our

institute. He has successfully carried out his summer project titled “MARKET

ANALYSIS AND NEW CHANNEL DEVELOPMENT” at HDFC Standard

Life Insurance Company.

This is the original study of Mr. Pawan Nigam & important source of

data used have been acknowledge in his report.

This report is submitted in partial fulfilment of two year fulltime course

of M.B.A under University of Pune, batch 2006-2008 as per the rules.

Prof. Mahesh Gadekar Dr. Sharad Joshi

(Project Guide) (Director)

2

ACKNOWLEDGMENT

Unending truth, endeavour never fails. But for hitting target you need weapon of

motivation, enthusiasm precise adviser. So really I am thankful to all of them who lend

their helping hand directly or indirectly.

Firstly I would like to thank Mr. D.M SATWALEKAR is the M D and CEO of the

HDFC Std. Life Insurance Company ltd. for giving me opportunity to work with this

organization

I would like thanks Mr. YUVRAJ SINGH without whose support, this project

would not have been possible. Heartiest thanks for his constant support and motivation.

My gratitude to everyone there at HDFC Standard Life who has helped me directly

or indirectly in the completion of this project.

I am thankful to my Director Dr. SHARAD JOSHI for providing me an

opportunity to do my winter training in such a prestigious company, which has truly been a

learning experience.

I wish to express my gratitude to Prof. MAHESH GADEKAR (project guide),

who gave proper guidance throughout the project, without his guidance and feedback it

would not have been possible for me to under take the research & utilize the research

methodology tools appropriately.

I would also like to convey thanks to all my colleagues who were also summer

trainees like me for being always ready with a helping hand.

3

PREFACE

The two month summer project with HDFC Standard Life was undertaken as a part

of academic curriculum which management students do at the end of second semesters.

As Market Analysis and New Channel Development are the cornerstones for any

industry, its immense significance in Insurance Industry cannot be undermined. It is

through these channels that insurance firms derive the bulk of their business. With

changing times and increase in competition and clutter, firms are finding it a Herculean

task to develop and maintain these channels.

Hence considering the above facts, the project title given by HDFC Standard Life Is

“Market Analysis and New Channel Development”…………Analysis and

Recommendations...

This Title covers the following points…..

1) New Channel Development

2) Maintenance of Existing Channels

3) Revival of Channels That Have Become Dysfunctional

On each of the above mentioned parameters an extensive research has been done by

the use of available data through papers, magazines, and internet and by direct interviews

and administering questionnaires.

Hope the findings and recommendations prove to be of some help for the firm for

deciding on the future course of action.

4

TITLE INDEX

Chapter No. TOPIC PAGE No.

Chapter 1 EXECUTIVE SUMMARY 1

Chapter 2 OBJECTIVE &SCOPE OF THE PROJECT 4

Chapter 3 COMPANY PROFILE 7

Product Range & Varity 9

List of Competitors and there Performance 12

Historical Development of the Company 15

Awards and Recognition 16

Analysis Of HDFC Standard Life Insurance For Strengths And Opportunities

18

Chapter 4 THEROTICAL BECKGROUND 20

Industry Profile 21

About IRDA 22

About FC 23

About HDFC Group 24

Distribution Framework 33

New Opportunity 35

Chapter 5 RESEARCH METHODOLOGY 37

Chapter 6 DATA ANALYSIS 41

Chapter 7 FINDINGS & LIMITATIONS 47

Chapter 8 CONCLUSION 50

Chapter 9 RECOMMENDATIONS 52

Chapter 10 BIBLIOGRAPHY 53

Chapter 11 ABBRIVATIONS 54

Chapter 12 ANNEXURE 55

5

INDEX OF TABLES/GRAPHS

Sr. No. TABLE/GRAPH PAGE No.

1. Organisation Chart 9 & 26

2. Graph showing market share of LIC V/s private players 13

3. Graph showing market share of HDFC V/s other private

companies

15

4. Table showing list of Board of Directors 24

5. Chart for Standard Life plc 27

6. Graph showing Age Group of the Respondents 42

7. Graph showing Income Level of the Respondents 43

8. Graph showing Marital status of the respondents. 44

9. Graph showing awareness of new insurance policies among

the respondents

45

10. Graph showing the rating given to the company by the FC’s 46

6

CHAPTER 1

EXECUTIVE SUMMARY

7

EXECUTIVE SUMMARY

1.1 INTRODUCTION OF THE PROJECT

HDFC Standard Life insurance is India’s premier insurance enabling company. HDFC Standard Life insurance is the one-stop-shop for requirements of services in the areas of insurance, optimum investment, financial coverage and losses, mortality benefit, and health option etc. This is backed by HDFC Standard Life insurance service support infrastructure - the widest in the country.

This project is related with finding out new channels of business for HDFC Standard Life by analyzing the market.

1.2 PROJECT TITLE

“MARKET ANALYSIS AND NEW CHANNEL DEVELOPMENT”

1.3 REASON FOR CHOSING THIS COMPANY & PROJECT

The reason behind choosing this company is – HDFC Standard Life Insurance Company is a giant among the country’s Insurance industries.

HDFC Standard Life is the prestigious units of well know HDFC group. It is one of the leading insurance companies in India.

HDFC Standard Life Insurance Company Ltd. is one of India’s leading private life insurance companies, which offers a range of individual and group insurance solutions. It is a joint venture between Housing Development Finance Corporation Limited (HDFC Ltd.), India’s leading housing finance institution and one of the subsidiaries of Standard Life plc, leading providers of financial services in the United Kingdom.

HDFC Standard Life's cumulative premium income, including the first year premiums and renewal premiums is Rs. 672.3 Crores for the financial year, Apr-Nov 2005. So far the company has covered over 11, 00,000 individuals and has declared 5th consecutive bonus in as many years for its 'with profit' policyholders.

1.4 LOCATION

Gandhi Plaza, CTS No. 47/21,FP No. 70/21, 24, Brandywine, Law College Road, Deccan Gymkhana,

8

Pune. 1.5 DURATION OF THE PROJECT

The duration of the project was 2 months. That is from 1st June to 31st July.

1.6 HOW DID I CARRY OUT THIS PROJECT?

I carried out this project through descriptive research methodology by preparing questionnaire and conducting personal interviews of Charted Accountants, Businessman’s, House Wife’s and Students.

1.7 RESULTS

However much the traditional agent's role be part of the company, the insurer must still be ready to adopt alternative distribution channels not to compete with agents but as a complementary effort to provide customers with an array of products. The insurers must not depend fully on their agents.

9

CHAPTER 2

OBJECTIVE &SCOPE OF THE PROJECT

10

OBJECTIVE & SCOPE OF THE PROJECT

2.1 TITLE OF THE PROJECT

“MARKET ANALYSIS AND NEW CHANNEL DEVELOPMENT”

2.2 DIFFERENT OBJECTIVES BEHIND CONDUCTING THIS PROJECT -

2.2.1 PRIMARY OBJECTIVES :-

1) To find out the new channels for business.

2) To find out whether the FC’s are aware of various new policies which are

available in the market?

3) To check whether the FC’s are satisfied with the different investment plans

available in the market.

4) To check for the FC’s feedback towards the company.

2.2.2 SECONDARY OBJECTIVE :-

1) To check the present situation and actual status of the company in the market.

2) To find out the market share of HDFC Standard Life in Pune.

3) Revival of the dead channels of business.

2.3 SCOPE OF THE PROJECT

To find out new market and opportunities. The study was pertaining to questions like

preferences for a particular product and also the study aims at answering the questions like,

the product preference. To find awareness of the company among people.

11

2.3.1 AREA OF THE PROJECT

Gandhi Plaza, CTS No. 47/21,

FP No. 70/21, 24, Erandwane,

Law College Road, Deccan Gymkhana,

Pune

2.3.2 AREA COVERED, SAMPLE SIZE

Tilak Road, Deccan Gymkhana, Sinhagad Road, F.C College Road, Karve

Nagar, L.B.S Road, Null Stop, etc. are the area covered for the research. The sample

size is of 100.

12

CHAPTER 3

COMPANY PROFILE

13

COMPANY PROFILE

3.1 COMPLETE NAME OF THE COMPANY:-

Company Name: - “HDFC Standard Life Insurance Company”

3.2 MISSION STATEMENT, VISION, SLOGAN, LOGO

3.2.1 MISSION STATEMENT :-

We aim to be the top insurance company in the market. This does not just mean to be the largest or the most productive company in the market; rather it is a combination of several things like –

Customer service of the highest order. Value for money for customers. Professionalism in carrying out business. Innovative product to cater to different needs of different customers. Use of technology to improve service standards. Increasing market share.

3.2.2 VISION STATEMENT :-

The most successful and admired life insurance company, which mean that we are the most trusted company, the easiest to deal with, offer the best valve for money, and at the standards in the industry. In short “The most obvious choice for all”

3.2.3 COMPANY LOGO :-

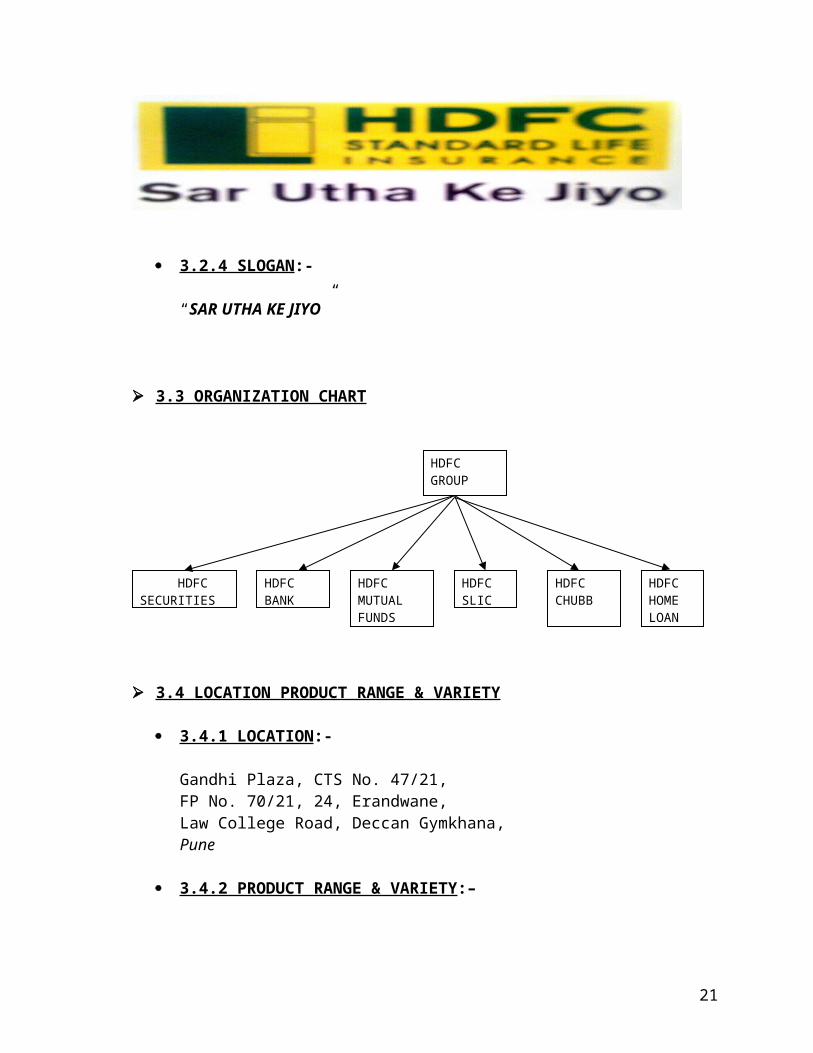

3.2.4 SLOGAN :-

“SAR UTHA KE JIYO”

14

3.3 ORGANIZATION CHART

3.4 LOCATION PRODUCT RANGE & VARIETY

3.4.1 LOCATION :-

Gandhi Plaza, CTS No. 47/21,FP No. 70/21, 24, Erandwane, Law College Road, Deccan Gymkhana,Pune

3.4.2 PRODUCT RANGE & VARIETY :–

There is a wide range of product offered by HDFC Standard Life to its customers. They are as follows-

A) SAVING PLAN

1. Endowment Assurance Plan

It is a participating (with profits) insurance plan that offers the following features: i) It provides financial support to the family by way of a lump sum payment in case of

the unfortunate death of the life assured within the term of the policy.ii) It provides a lump sum payment to the life assures on survival up to maturity. The

lump sum mentioned is the basic sum assured plus any bonus additions.

2. Unit Linked Endowment Plan

The unit linked endowment plan is an insurance policy that is designed to pay a lump sum amount on the maturity or on earlier death. The unit linked endowment plan

HDFCBANK

HDFCMUTUALFUNDS

HDFCSLIC

HDFCCHUBB

HDFC HOMELOAN

HDFCGROUP

HDFCSECURITIES

15

also gives the option of additional protection against common critical illness, as well as additional protection if death is as the result of an accident.

Your premiums are invested in units of the investment fund of your choice, based on the prevailing unit price. On maturity you receive the value of your units. On death (or critical illness, if chosen) you receive the value of your units and your selected basic sum assured.

3. Children’s Plan

A children plan is designed to provide a lump sum amount to the child at maturity. It also provides financial security to the child in the future, even in case of the insured parent’s unfortunate death during the policy term. Children’s plan receives simple bonuses, which are usually added annually. This is a flexible plan with three options for you to choose from, depending on your requirements.

4. Money Back Plan

It is a participating (with profits) insurance plan that offers the features listed below:

i) Payment of cash lump sum, each of which is a proportion of the basic sum assured, at 5-year intervals during the term of policy.

ii) On survival up to maturity, a payment equal to the basic sum assured plus any bonus additions less the cash lump sums paid is provided.

iii) In case of the unfortunate death of the life assuror within the term of the policy, the basic sum assured plus any bonus additions is provided. This is over and above the earlier payouts.

5. Unit Linked Young Star Plan

HDFC Unit linked Young Star plan is designed to provide a lump sum to the child at maturity. It also provides financial security to the child in his future, even in case of the insured parent’s unfortunate death during the policy term. The Unit linked Young Star plan also gives the option of additional protection against the six common critical illnesses. Your premiums are invested in units of the investment funds of your choice, based on the prevailing unit price. On maturity the value of the units will be paid. On death (or critical illness, if chosen) the selected basic sum assured is paid, and the policy continues until maturity. Following a valid death or critical illness claim, we will pay the future premiums (at the level originally chosen at inception) into your policy, as and when they would have fallen due.

16

A) INVESTMENT PLAN

1. Single Premium Whole of Life Plan

Single Premium Whole of Life Plan is well suited to meet your long term investment needs. This participating (with profit) plan offers you the following benefits:

A sound investment:

Your money will be invested in our ‘with profit fund’. The fund aims to provide secure and stable long term growth. Normally, we declare a compound reversionary bonus for your policy every year and add it to your policy on its anniversary. In addition, on death, surrender or on the guaranteed dates, a terminal bonus might be payable. You have to pay a single premium and the policy will pay you a lump sum amount.

Flexibility of term:

Even after choosing your policy, you can decide on the policy term. For 4 weeks after any one of the 10th, 15th, 20th, and subsequent five-year anniversaries, you can choose to receive the sum assured plus any attaching bonuses, in full. Once the money has been received, your policy will cease.

B) PROTECTION PLAN

1. Term Assurance Plan

Under this plan, a sum assured is payable in case of death of the life assured during the term of the contract. One can choose the lump sum that would replace the income lost to one’s family in the unfortunate event of one’s death. Since this no-participating plan is pure risk cover plan, no benefits are payable on the survival to the end of the term of the policy.

2. Loan Covered Term Assurance

This plan provides a lump sum on the unfortunate death of the life assured during the term of the plan. The lump sum will be a decreasing percentage of the initial sum assured. As the outstanding loan decreases as per the loan schedule, the cover under the policy decreases as per the policy schedule. Since this is a non-participating, risk is there, no benefits are payable on survival to the end of the term of the policy.

17

C) RETIREMENT PLAN

1. Personal Pension Plan

This participating plan is basically a saving contract, which is designed to provide an income for life from retirement. It does this by providing a national lump sum on retirement, comprising of sum assured plus any attaching bonus. Subject to the prevailing regulations, part of this lump sum can be taken in form of cash and the rest converted to an annuity at the rate then offered by HDFC Standard Life. Alternately, if it is permitted by the prevailing regulation, the national lump sum can be used to buy an annuity with any other insurance company.

2. Unit Linked Pension Plan

The unit linked pension plan is basically an insurance contract, which is designed to provide a retirement income for life. Your premiums are invested in units of the investment fund of your choice, based on the prevailing unit price. On investing the vale of your units will be used to buy your retirement benefits. On earlier death, the beneficiary receives the value of your units plus a cash lump sum of Rs. 1,000.

3.4 LIST OF MAJOR COMPETITORS

1. ICICI 2. Aviva3. Bajaj Allianz 4. ING Vaisya5. Birla Sun Life Insurance 6. SBI Life6. Tata AIG 7. Max Newyork

3.4.1 PERFORMANCE OF MAJOR COMPETITORS

Private insurance players belonging to both life and non-life insurance segments have significantly improved their market share during the first half of the current fiscal year ended September 30, as per the figures compiled by the Insurance Regulatory and Development Authority (IRDA). The market share of private sector life insurers in terms of premium collections has nearly doubled to 10.95 per cent during the first half of current fiscal compared to 5.66 per cent during the corresponding period of last fiscal year.

In the case of non-life insurance players, their market share rose to 13.7 per cent, recording a growth of 86.72 per cent on an annual basis, while the market share of public sector majors stood at 86.3 per cent, registering a marginal growth of 6.03 per cent. The overall market has recorded a growth of 12.71 per cent. As per the figures compiled by IRDA, the life insurance industry recorded a total premium underwritten of Rs 5,435.95 crore for the six months period under review. Of this, private players contributed to Rs 595.33 crore.

18

The public sector giant Life Insurance Corporation of India (LIC) continued to lead with a premium collection of Rs 4,840.62 crore, translating into a market share of 89.05 per cent.

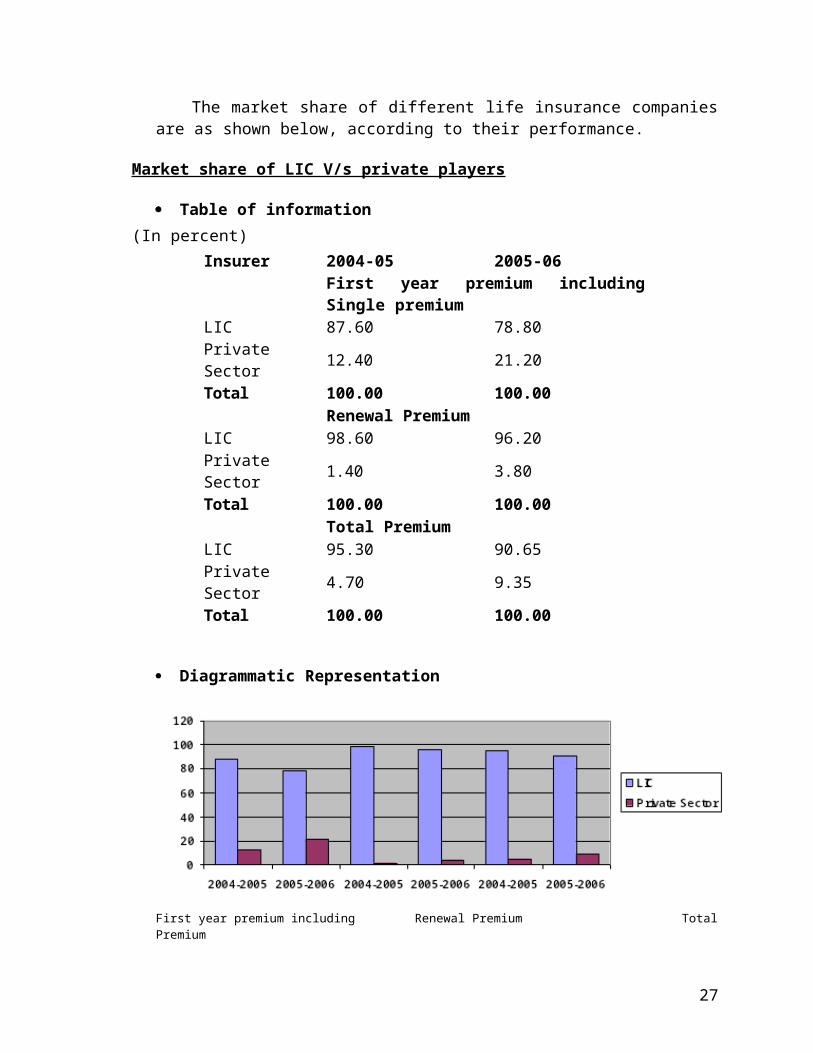

The market share of different life insurance companies are as shown below, according to their performance.

Market share of LIC V/s private players

Table of information

(In percent)

Insurer 2004-05 2005-06

First year premium including Single premium

LIC 87.60 78.80

Private Sector 12.40 21.20

Total 100.00 100.00

Renewal Premium

LIC 98.60 96.20

Private Sector 1.40 3.80

Total 100.00 100.00

Total Premium

LIC 95.30 90.65

Private Sector 4.70 9.35

Total 100.00 100.00

Diagrammatic Representation

First year premium including Renewal Premium Total Premium

Single premium

19

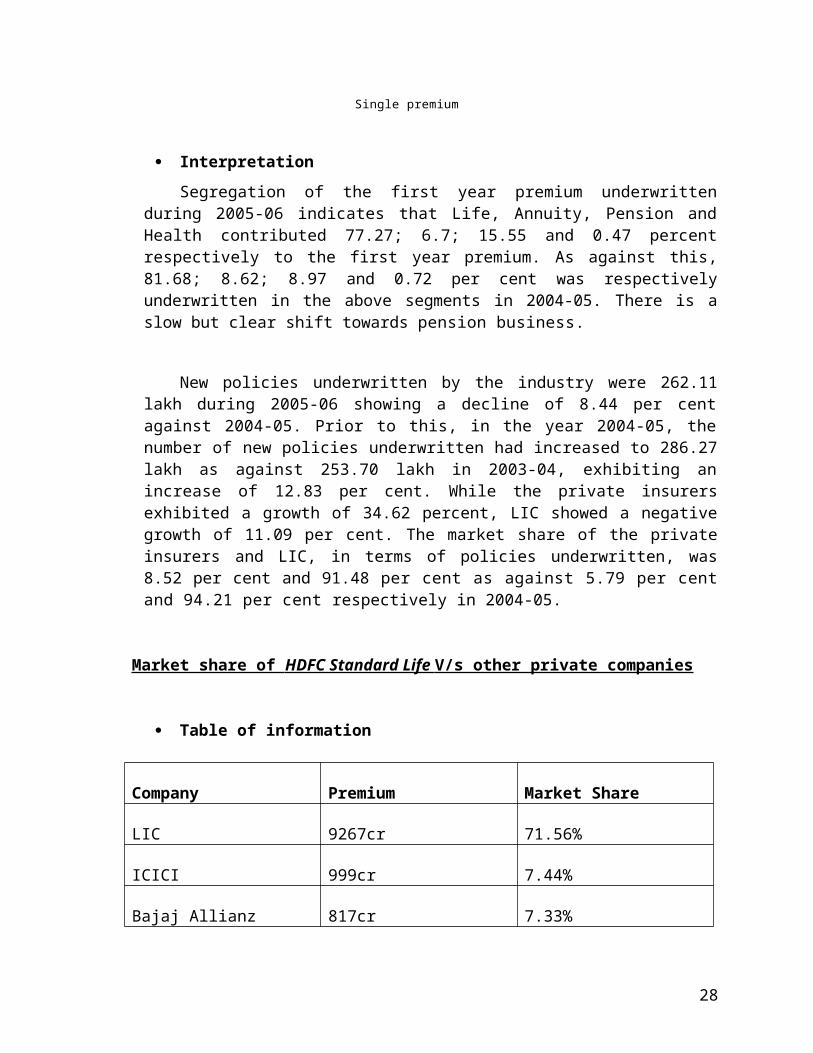

Interpretation

Segregation of the first year premium underwritten during 2005-06 indicates that Life, Annuity, Pension and Health contributed 77.27; 6.7; 15.55 and 0.47 percent respectively to the first year premium. As against this, 81.68; 8.62; 8.97 and 0.72 per cent was respectively underwritten in the above segments in 2004-05. There is a slow but clear shift towards pension business.

New policies underwritten by the industry were 262.11 lakh during 2005-06 showing a decline of 8.44 per cent against 2004-05. Prior to this, in the year 2004-05, the number of new policies underwritten had increased to 286.27 lakh as against 253.70 lakh in 2003-04, exhibiting an increase of 12.83 per cent. While the private insurers exhibited a growth of 34.62 percent, LIC showed a negative growth of 11.09 per cent. The market share of the private insurers and LIC, in terms of policies underwritten, was 8.52 per cent and 91.48 per cent as against 5.79 per cent and 94.21 per cent respectively in 2004-05.

Market share of HDFC Standard Life V/s other private companies

Table of information

Company Premium Market Share

LIC 9267cr 71.56%

ICICI 999cr 7.44%

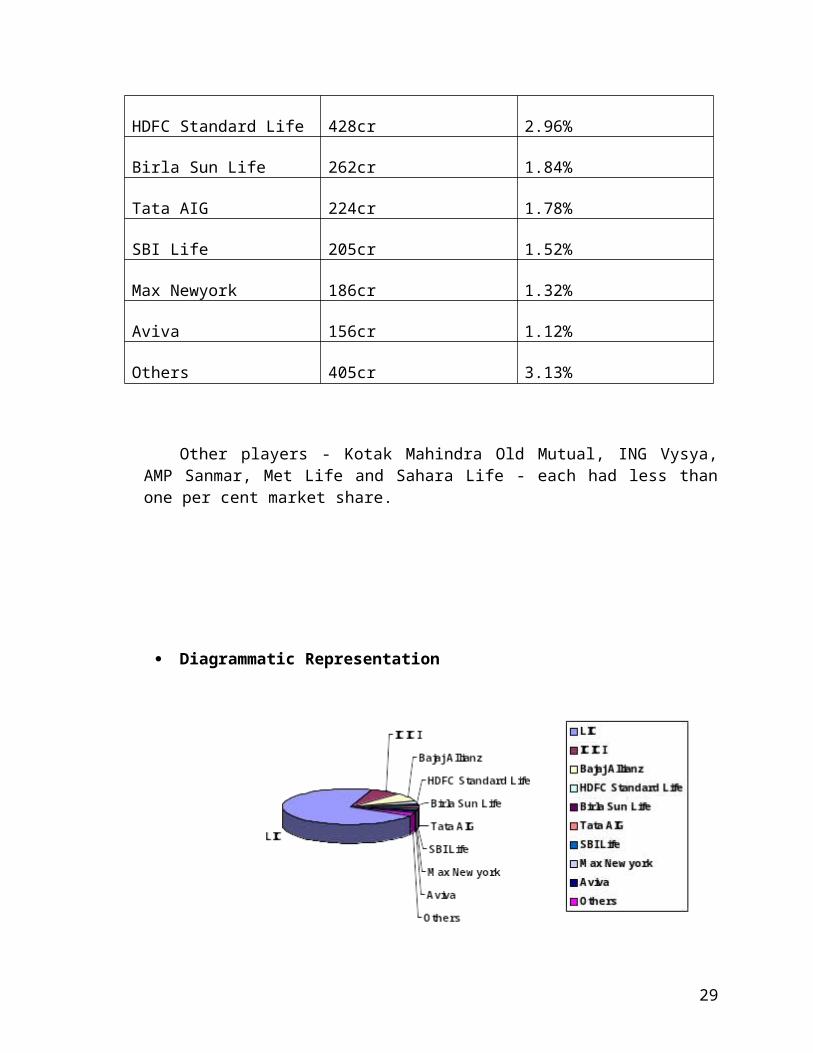

Bajaj Allianz 817cr 7.33%

HDFC Standard Life 428cr 2.96%

Birla Sun Life 262cr 1.84%

Tata AIG 224cr 1.78%

SBI Life 205cr 1.52%

Max Newyork 186cr 1.32%

Aviva 156cr 1.12%

Others 405cr 3.13%

20

Other players - Kotak Mahindra Old Mutual, ING Vysya, AMP Sanmar, Met Life and Sahara Life - each had less than one per cent market share.

Diagrammatic Representation

Interpretation

HDFC Standard Life has the 3rd highest market share of 3.11% among the other private insurance company. Among the private sector players in terms of premium collections, ICICI Prudential topped the list.

It recorded a premium of Rs 185.2 crore and a market share of 3.41 per cent, followed by Birla Sun Life with a premium underwritten of Rs 82.41 crore (1.52 per cent market share), HDFC Standard with Rs 66.18 crore premium (1.22 per cent share), Tata AIG with Rs 63.04 crore (1.16 per cent) and Allianz Bajaj with Rs 47.17 crore premium (0.87 per cent share).

3.5 HISTORICAL DEVELOMENT OF THE COMPANY

HDFC Standard Life Insurance Company Ltd. is one of India’s leading private insurance companies, which offers a range of individual and group insurance solutions.

21

It is a joint venture between Housing Development Finance Corporation Limited (HDFC Ltd.), India’s leading housing finance institution and one of the subsidiaries of Standard life plc, leading providers of financial services in United Kingdom. Both the promoters are well known for their ethical dealings and financial strength and are thus committed to being a long-term player in the life insurance industry.

3.5.1 KEY STRENGTHS

Financial Expertise

As a joint venture of leading financial services groups, HDFC Standard Life has the financial expertise required to manage the long-term investments safely and efficiently.

Range of Solutions HDFC Standard Life Insurance Company has a range of individual and group

solutions, which can be easily customized to specific needs. The group solutions have been designed to offer complete flexibility combined with a low charging structure.

3.5.2 TRACK RECORD SO FAR

HDFC Standard Life has been recording consistent growth since its inception and is today one of the leading insurance companies in India. Till December 2006, the company has covered over 22.5 lakh individuals and achieved a total sum assured of over Rs. 1,25,700 crore.

For the period April – Dec 06, the company recorded new business first year premium of Rs. 984 crore with growth of 64% over April – Dec 05. The total premium income also grew to Rs. 1651 crore during the same period on the back of a high persistency of regular premium policies. HDFC Standard life’s Effective Premium income grew to Rs. 803 crore in April – Dec06, highlighting the stress that the company puts on regular products as opposed to single premium products.

The company has covered over 1.6 million individuals out of which over 5, 00,000 lives have been covered through our group business tie-ups.

The Standard Life Assurance Company ("Standard Life") was established in 1825 and the first Standard Life Assurance Company Act was passed by Parliament in 1832. Standard Life was reincorporated as a mutual assurance company in 1925.

22

3.6 AWARDS AND RECOGNITION

Year Award

• 2003 Company of the Year• 2002 Company of the Year• 2001 Best Personal Pension Provider• 2000 Company of the Year• 1999 Company of the Decade• 1996-99 Company of the year• 1995 4 star service award• 1992-94 Overall best company• 1991 3 star service award• Standard Life has been awarded the "Raising Standards" quality mark.

This shows that the Company:

uses clear language to describe their products on key documents, have appropriate products and Provide a quality service for the customers.

3.6.1 Money Marketing Awards

Company of the Year every year from 1999 to 2005 Best Pension Provider 2004 and 2005 Best Group Pension Provider every year from 1998 to 2003 Best Personal Pension Provider every year since 1998 to 2003 Best Life Investment Product Provider 2003 and 2004 Gold Award in the Poster Campaign Category (Advertising) 2004

3.6.2 Money facts Investment, Life & Pensions Awards

Best Pension Product 2003, 2004 and 2005 Best Pension Service 2003, 2004 and 2005

3.6.3 Bank hall Achievement Awards

Pension Provider of the Year 2003 and 2004

3.6.4 Financial Adviser Provider Awards

Overall Winner in 1999, 2000, 2001 and 2002 Pensions Provider of the Year 1999, 2000, 2001, 2002 and 2003 Pensions Company of the Year 2004 Individual Pensions Company of the Year 2004 Group Pensions Provider of the Year 2004

23

Health Insurance Company of the Year 2004

3.6.5 Financial Adviser Service Awards

Company of the Year every year from 1997 to 2001 5 Star Life and Pensions Provider every year from 1996 to 2004 5 Star Investment Provider every year from 1996 to 2002 and 2004

3.6.6 Pensions Management Administration and Service Awards

Overall Winner - Personal Pensions 2003 Overall Winner - Stakeholder Pensions 2002 and 2003 Overall Winner - Group Personal Pensions 2002 and 2004 Member Communications - Personal Pensions, Group Personal Pensions &

Stakeholder Pensions 2003 Backup (branch office) - Personal Pensions 2003 Backup (head office technical support) - Personal Pensions & Stakeholder

Pensions 2003

3.6.7 Pensions Management Technology Awards

Best extranet accessibility 2004

3.6.8 Guardian & Observer Consumer Finance Awards

Overall Winner in Personal & Stakeholder Pension Provider 2003

3.6.9 Professional Adviser Awards

Best Product Provider Website (adviser zone) 2005 3.6.10 Online Finance Awards

Best online Product Provider (ifazone) 2003 Best online Financial Adviser (ifazone) 2002

3.7 ANALYSIS OF HDFC STANDARD LIFE INSURANCE COMPANY FOR STRENGTHS AND OPPORTUNITIES

STRENGTHS:

Having good network Having good brand image

24

HDFC has one of the highest brand recall of around 80% (source:AC Neilson ORG MARG)

HDFC has different types of training methods for their FC’s, Agents or Advisor. For Example Disha training, IRDA training, Basic training and induction, Advanced training.

Financial Expertise. Range of solutions.

OPPORTUNITIES

In India still there is a big market for insurance field. The new employer employee plan has a big scope in the market.

75% of Indian market is still untapped. By their ULIP plans they can compete with LIC Company.

WEAKNESSES

Less advertisement & publicity Poor awareness for new products in consumers They are unable to target rural area as compare to LIC.

THREATHS

Some brands in the market gives there product with more features. ICICI & Bajaj Allianz is the major competitor with better network. Many private players are coming into the market.

25

CHAPTER 4

THEROTICAL BECKGROUND

26

THEROTICAL BECKGROUND

A) INDUSTRY PROFILE

Nature of Insurance Industry

The insurance provides protection or safeguard against financial losses or failure from a variety of perils. By purchasing policies, individuals and businesses can receive reimbursement for losses due to car accident, theft of property, fire and storm damage; medical expenses; and loss of income due to disability or death.

The insurance industry consists mainly of insurance carriers (or insurers), insurance agencies, advisors and consultants. In general, insurance carriers or insurers are large companies that provide insurance and assume the risks covered by the policy. Insurance agencies and consultants sell insurance policies for the carriers. While some of these establishments are directly affiliated with a particular insurer and sell only that carrier’s policies, many are independent and are thus free to market the policies of a variety of insurance carriers.

Insurance carriers assume the risk associated with annuities and insurance policies and assign premiums to be paid for the policies. In the policy, the carrier states the length and conditions of the agreement, exactly which losses it will provide compensation for, and how mush will be awarded. The premium charged foe the policy is based primarily on the amount to be awarded in case of loss, as well as the likelihood that the insurance carrier will actually have to pay. In order to be able t compensate policy holders for their losses, insurance companies invest the money (which they receive) in building up a portfolio of financial assets and income-producing real estate, which can be used to pay off any claims that may be brought.

Definition of Insurance & Types of Insurance:

DefinitionInsurance is a contract by which insurer agrees to pay the insured compensation for

a specified damage an injury or safeguard in exchange for periodic payment. Insurance is a safeguard against losses or failure.

TypesMainly insurance is of two types i.e. Life Insurance & General Insurance

a) Life Insurance1) Insurance for Life

b) General Insurance1) Fire Insurance2) Marine Insurance3) Miscellaneous Insurance

27

B) INSURANCE REGULATORY AND DEVELOPMENT ATHORITY

Insurance Regulatory and Development Authority (IRDA) was constituted in 1999 by

an Act of Parliament to protect the interests of the policyholders and to regulate, promote

and ensure orderly growth of the insurance industry. IRDA consists of a ten member team

that comprises a Chairman, five whole-time members and four part-time members. IRDA

allows registration of new players in the insurance field. It also has the authority to renew,

modify, withdraw, suspend or cancel such registration. IRDA ensures protection of the

interests of the policy holders in matters concerning assigning of policy, nomination by

policy holders, insurable interest, settlement of insurance claim, surrender value of policy

and other terms and conditions of contracts of insurance. It specifies requisite

qualifications, code of conduct and practical training for intermediary or insurance

intermediaries and agents.

After creation of IRDA, insurance sector has seen tremendous growth. Before IRDA

came into force there were only players in the insurance field, namely, Life Insurance

Corporation of India (LIC) and General Insurance Corporation of India (GIC). Since then

23 new players have entered in the insurance sector.

B1 Composition of Authority under IRDA Act, 1999

As per the section 4 of IRDA Act' 1999, Insurance Regulatory and Development

Authority (IRDA, which was constituted by an act of parliament) specify the composition

of Authority

The Authority is a ten member team consisting of

(a) A Chairman;

(b) Five whole-time members;

(c) Four part-time members,

(all appointed by the Government of India)

28

C) ABOUT FINANCIAL CONSULTANTS

C1 Definition

FC is business associates of HDFC Standard Life who are able to recommend the best solution based upon the individual customers need. Basically FC is an individual who provides financial solutions to his clients by drawing his insurance policy i.e. the policy holder is provided with the option of choosing the area of investment where he wants to invest his premium money.

The number of certified financial consultants appointed by HDFC Standard Life increased from 10645 in the year 2003 to 18296 in the year 2004. The company continues to concentrates its efforts on to ensure the quality of its consultants through process of screening, personal interviews and training.

C2 Role of FC

1. Every FC has to work under a sales development manager, who reports to a Business development Manager.

2. He can pursue it as a part time or full time job & can even operate from HDFC Standard Life’s office or at his own convenient premises.

3. They are required to meet certain targets depending upon his potential.4. They receive commission for the business they provide the company.

To summaries, it’s a part time opportunity for those who have good networking skill & has the urge to earn through extra sources of income.

C3 Nature of work

Agents increasingly offer comprehensive financial planning services, including retirement and estate planning; as a result, in addition to offering insurance policies, agents sell mutual funds, annuities, and securities. Agents must obtain a license in the States where they plan to do their selling.

Despite slower than average growth, job opportunities are good for college graduates who have sales ability, excellent interpersonal skills, and expertise in a wide range of insurance and financial services.

C4 Eligibility

Regulation 4 of the regulations requires that a person desiring to obtain a license to become an agent should fulfill the following obligations:-

1) Shall possess a minimum qualification of a pass in 12 standard conducted by a recognized board or university. However if the resident resides in a place where the population is less than 5000, a pass in 10 standard will do.

29

2) According to regulation 5 of the regulations an aspiring agent needs to-: complete from an approved institution, at least 100 hrs of practical training in life or general insurance which may spread over 4 to 5 weeks to act as an insurance agent.

3) Complete from an approved institution, at least 150 hrs of practical training in life and general insurance this may spread over 4 to 5 weeks to act as a composite insurance agent.

C5 Training and Support programs at HDFC Standard Life IRDA specified 100 hr training(Training options are available) FC induction Program Disha Training on products, Competition analysis, Sales tools, Sales Pitches, Handling

customer objections and Expanding customer base. Business Development sessions. Training and workshops for enhancing skills.

D) ABOUT HDFC GROUP

Helping Indians Experience the joy of home ownership, HDFC was started in the year 1977 as home loan providers. Their objective, from the beginning, has been to enhance residential housing stock and promote home ownership.

Now, their offerings range from hassle-free home loans and deposit products, to property related services and a training facility. They also offer specialized financial services to their customer base through partnerships with some of the best financial institutions worldwide.

HDFC is a professionally managed organization with a board of directors consisting of eminent persons who represent various fields including finance, taxation, construction and urban policy & development. The board primarily focuses on strategy formulation, policy and control, designed to deliver increasing value to shareholders.

Board of Directors

Mr. Deepak S Parekh is the Chairman of the Company. He is also the Executive Chairman of Housing Development Finance Corporation Limited (HDFC Limited). He joined HDFC Limited in a senior management position in 1978. He was inducted as a whole-time director of HDFC Limited in 1985 and was appointed as its Executive Chairman in 1993. He is the Chief Executive Officer of HDFC Limited. Mr. Parekh is a Fellow of the Institute of Chartered Accountants (England & Wales).

Mr. Keki M Mistry joined the Board of Directors of the Company in December, 2000. He is currently the Managing Director of HDFC Limited. He joined HDFC Limited in 1981 and became an Executive Director in 1993. He was appointed as its

30

Managing Director in November, 2000. Mr. Mistry is a Fellow of the Institute of Chartered Accountants of India and a member of the Michigan Association of Certified Public Accountants.

Mr. Alexander M Crombie joined the Board of Directors of the Company the Standard Life Group in March 2004 and is also the Chief Executive of Standard Life Investments Limited. Mr. Crombie is a fellow of the Faculty of Actuaries in Scotland.

Ms. Marcia D Campbell is currently the Group Operations Director in The Standard Life Assurance Company and is responsible for Group Operations, Asia Pacific in April, 2002. He has been with the Standard Life Group for 34 years holding various senior management positions. He was appointed as the Group Chief Executive of Development, Strategy & Planning, Corporate Responsibility and Shared Services Centre. Ms. Campbell joined the Board of Directors in November 2005.

Mr. Keith N Skeoch is currently the Chief Executive in Standard Life Investments Limited and is responsible for overseeing Investment Process & Chief Executive Officer Function. Prior to this, Mr. Skeoch was working with M/s. James Capel & Co. holding the positions of UK Economist, Chief Economist, Executive Director, Director of Controls and Strategy HSBS Securities and Managing Director International Equities. He was also responsible for Economic and Investment Strategy research produced on a worldwide basis. Mr. Skeoch joined the Board of Directors in November 2005.

Mr. G N Bajpai was the former chairman of Life Insurance Corporation of India and Securities and Exchange Board of India. Mr. Bajpai retired from Life Insurance Corporation of India with more than 3 decades of experience and further served SEBI as its chairman for 3 years, during which time he had strengthened the compliance enforcement in SEBI.

Mr. Gautam R Divan is a practicing Chartered Accountant and is a Fellow of the Institute of Chartered Accountants of India. Mr. Divan was the Former Chairman and Managing Committee Member of Midsnell Group International, an International Association of Independent Accounting Firms and has authored several papers of professional interest. Mr. Divan has wide experience in auditing accounts of large public limited companies and nationalized banks, financial and taxation planning of individuals and limited companies and also has substantial experience in structuring overseas investments to and from India.

Mr. Ranjan Pant is a global Management Consultant advising CEO/Boards on Strategy and Change Management. Mr. Pant, until 2002 was a Partner & Vice-President at Bain & Company, Inc., Boston, where he led the worldwide Utility Practice. He was also Director, Corporate Business Development at General Electric headquarters in Fairfield, USA. Mr. Pant has an MBA from The Wharton

31

School and BE (Honors) from Birla Institute of Technology and Sciences.

Mr. Ravi Narain is the Managing Director & CEO of National Stock Exchange of India Limited. Mr. Ravi Narain was a member of the core team to set-up the Securities & Exchange Board of India (SEBI) and is also associated with various committees of SEBI and the Reserve Bank of India (RBI).

Mr. Deepak M Satwalekar is the Managing Director and CEO of the Company since November, 2000. Prior to this, he was the Managing Director of HDFC Limited since 1993. Mr. Satwalekar obtained a Bachelors Degree in Technology from the Indian Institute of Technology, Bombay and a Masters Degree in Business Administration from The American University, Washington DC.

HDFC has a staff strength of 1370 (as on 31st July, 2006), which includes professionals from the fields of finance, law, accountancy, engineering and marketing.

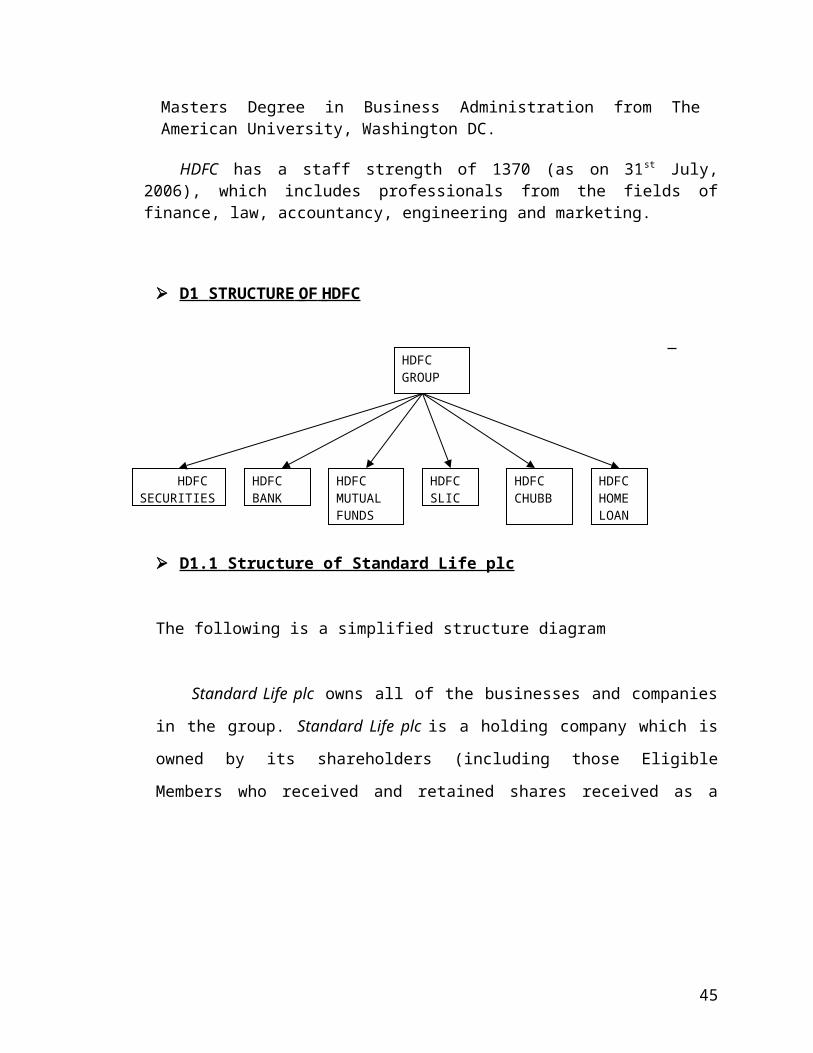

D1 STRUCTURE OF HDFC

D1.1 Structure of Standard Life plc

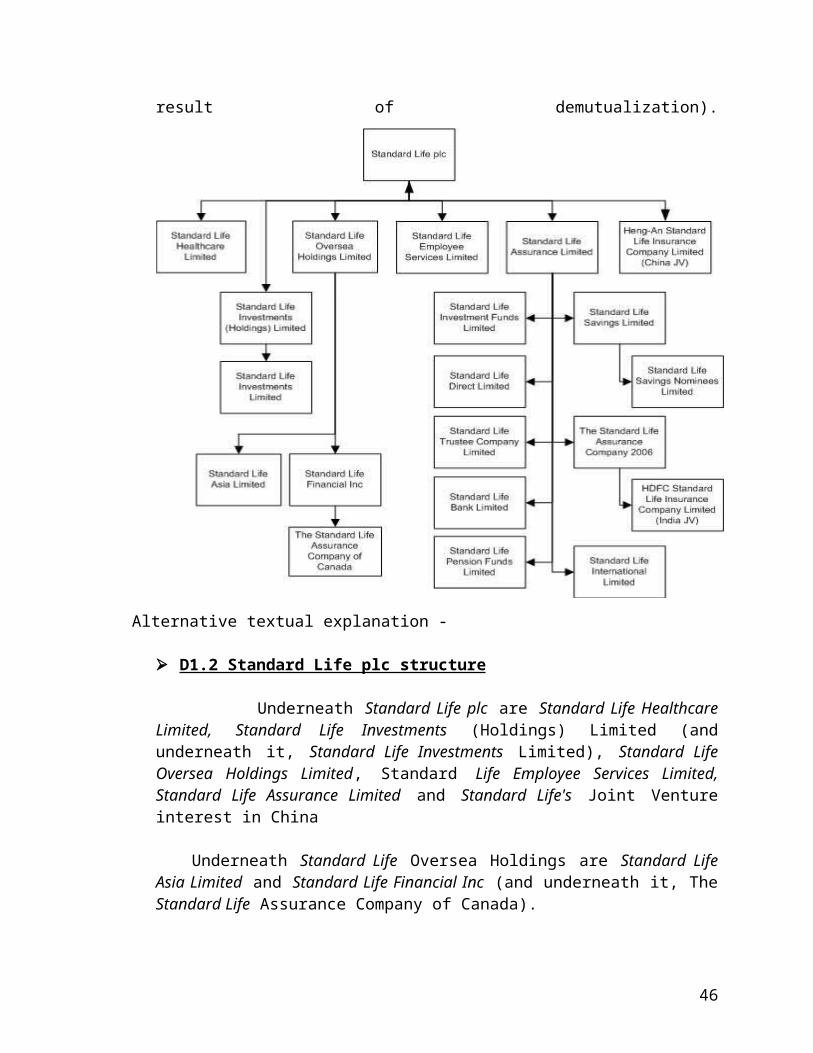

The following is a simplified structure diagram

Standard Life plc owns all of the businesses and companies in the group.

Standard Life plc is a holding company which is owned by its shareholders (including

those Eligible Members who received and retained shares received as a result of

HDFCBANK

HDFCMUTUALFUNDS

HDFCSLIC

HDFCCHUBB

HDFC HOMELOAN

HDFCGROUP

HDFCSECURITIES

32

demutualization).

Alternative textual explanation -

D1.2 Standard Life plc structure

Underneath Standard Life plc are Standard Life Healthcare Limited, Standard Life Investments (Holdings) Limited (and underneath it, Standard Life Investments Limited), Standard Life Oversea Holdings Limited, Standard Life Employee Services Limited, Standard Life Assurance Limited and Standard Life's Joint Venture interest in China

Underneath Standard Life Oversea Holdings are Standard Life Asia Limited and Standard Life Financial Inc (and underneath it, The Standard Life Assurance Company of Canada).

Underneath Standard Life Assurance Limited are Standard Life Direct Limited, Standard Life Savings Limited, Standard Life Direct Limited, Standard Life Trustee Company Limited, Standard Life Bank Limited, Standard Life Pensions Funds Limited,

33

Standard Life International Limited and The Standard Life Assurance Company 2006, which currently holds Standard Life's Joint Venture interests in India.

E) Various Channels through which Insurance is sold in India

In India basically there are two channels through which insurance is sold. These are namely:-

1] Bancassurance

2] Retail insurance (Agency Model)

E1 Bancassurance

In this channel insurance firms have a tie up with various banks .It is through these banks which act as their channel partners that insurance is sold. BANCASSURANCE is poised for big growth as insurance companies prefer corporate agency tie-ups with banks, as against referral arrangements. Corporate agency contracts are better because in such an arrangement customers deal with the bank employees whom they know well. Therefore, there is an element of trust. Bank employees are in a better position to understand the needs of the customer and serve them better. On the contrary, referral arrangements do not add value to the bank — it only lends its database to the insurer.

This model is based on the fact that usually banks have a large pool of clientele. Hence the insurance firms make use of this database to sell their products. But with time this channel has proved to be a costly affair.

E2 Retail Channel

In this channel which is based on the agency model, the insurance firms go on to recruit business partners or agents for the firm to sell insurance. There are properly defined rules from IRDA (Insurance Regulatory Development Authority of India). For the recruitment, selection and working of these agents .The major points of consideration for this channel are:-

1. Development of new Channels.(new recruitments)

2. Revival of Channels that have become dysfunctional.

3. Maintenance of existing Channels.

34

F) Role of Distribution Channels in Value Creation in insurance companies Distribution accounts for the largest element in insurers’ costs and impact the

profitability. Distribution capabilities strongly influence product design in insurance. Distribution channels have a direct impact on the insurers’ market image. Integrity of distribution channel is the key concern of the regulatory mechanism. F1 Emergence of alternative channels such as Bancassurance and Corporate

Agents is reshaping the insurance industry. Insurance penetration levels will rise sharply with multi distribution channel. Widespread recognition of the need for qualified, trained sales forces to serve

the increasingly discerning insurance buyers. Emergence of online and offline insurance education and training initiatives is

changing the range and quality of insurance services. Emergence of new channels will have positive impact on rebating and such

undesirable practices in the industry. Widening choice of distribution channels will eventually drive down the

premium level. F2 Evolution of alternate Distribution channels in India : Areas of supportive

official measures Need to encourage and nurture new channels such as Banc assurance to utilize

the existing infrastructure to optimum extent. Policy measures should encourage insurers to take full responsibility for

training and skill building. Encouraging self-regulation. Strengthening the consumer grievance redressal mechanism.

G) Importance of Distribution Channels

In Sum:

We need more alternative channels in India to sharply increase penetration levels. Emergence of new channels is in the interest of consumers. Widening and strengthening the channels will help the insurance industry to

become more competitive and healthy G1 Developing New Channels(recruitment of agents)

Agents increasingly offer comprehensive financial planning services, including retirement and estate planning; as a result, in addition to offering insurance policies, agents sell mutual funds, annuities, and securities. Agents must obtain a license in the States where they plan to do their selling.

Despite slower than average growth, job opportunities should be good for college graduates who have sales ability, excellent interpersonal skills, and expertise in a wide range of insurance and financial services.

35

Successful agents often have high earnings, but many beginning agents fail to earn enough from commissions to meet their income goals and eventually transfer to other careers.

G2 Maintenance of existing Channels

It is a known fact that more than developing new channels it is a far more Herculean task to maintain them In most markets, except Asia, insurance carriers generate more than 80% of their business through alternative distribution channels such as banc assurance, broker-dealers, wire houses and IFAs. The key challenge for insurers is to attract and retain these distribution channels. Some of the points are given below for maintenance of existing channels.

Quick closure of sales:

To begin with, agents need tools and calculators to produce accurate quotations on the fly. They also need tools that can help them perform a financial need analysis of the customer and suggest suitable products based on the customer’s profile. To further speed up the process, it would help if agents can perform basic suitability tests and underwriting at source.

Reduction in proposal turnaround time:

Insurers must aim to reduce the time it takes to turnaround proposals. They must give agents the ability to submit applications online through a portal, which is seamlessly integrated with the back office. An underwriting engine, which is based on pre-defined rules, can automatically handle many of the proposals, flagging only those proposals that do not meet the basic criteria for manual underwriting. In such a system, insurers can also use straight through processing (STP) to greatly reduce the turnaround times.

Proactive service:

A good system will allow insurers to be proactive in the kind of service they deliver to their distribution partners. For instance, they can provide alerts to agents on policies that are likely to lapse or about defaults on premiums through producer-defined or system alerts. When it comes to wealth management products, an insurer must be able to provide its channels with portfolio management tools such as tools to generate simulated ‘what if’ scenarios or perform financial need analysis. These tools can help agents maximize the asset value of their customers and, since commissions are based on asset value, their income as well.

Enhanced service:

36

Once agents submit a proposal, they are keen to know the status of the proposal. Insurers can enable their agents to directly communicate with underwriters through chat sessions. Insurers can also provide agents with access to a transaction portal, where they can perform basic changes to policies and submit and manage claims.

Value-added services:

An important service that insurers can render channels is lead generation. If insurers can get a single view or a household-centric of the customer, they can alert agents about cross-selling and up-selling opportunities. Insurers can help agents identify profitable customers and segment their customer base, thus giving them the ability to provide differentiated service.

Innovative commission and incentive packaging

Agents sell insurance products so that they can maximize their commissions. To become a preferred partner with profitable producers, insurers must be able to pay differentiated commission rates based on performance and disburse these commissions at different frequencies. For instance, a ‘platinum’ producer could be given commissions fortnightly, whereas a ‘gold’ producer could get it once a month.

Evaluating performance

A critical aspect of managing the insurance distribution network is evaluating performance. Because performance data is what will help insurers offer differentiated service to their channels and design better products. For instance, a channel may be writing a large number of policies, but its lapse rate may be high. Or an agent may be very successful in booking business, but the claims rate on his/her policies may be higher than average.

What senior managers need is a dashboard that gives them personalized and customized snapshots of performance across the distribution chain. They should have the ability to drill down from the summary views and make deeper analyses of all performance data.

G3 Revival of channels that have become dysfunctional

With time, it has been found hat many channels become dead or dysfunctional. The amount of business that they were generating in the past either declines or completely stop.

37

As prevention is better than cure, hence channels should not be left to themselves but need to be properly tracked and maintained from time to time. The maintenance part comes from performing a through analysis of the channels, finding out their strengths and weaknesses, appreciating them for their good or strong points and motivating them for overcoming their shortcomings.

A list of agents was given who were star performers at one time, but have suddenly stopped performing. An analysis was supposed to be carried out so as to find out the reasons for their non performance.

38

DISTRIBUTION FRAMEWORK

39

The framework

So what would it take for insurance companies to build all this functionality into their systems? What would the framework look like? An ideal channel-facing and customer-centric IT system would have three critical components, all of which must be seamlessly integrated with the back-office platforms. The components are 1) Point of Sale, 2) Channel Portal and 3) Channel Management

Point of Sale

What are the things an agent needs to make a quick sale? To recommend a product that is best suited to a customer’s needs, the agent should have financial tools to perform need and cost-benefit analyses. The agent should be able to simulate and demo a variety of investment scenarios and share with the customer information about the product such as past performance, bonus record etc.

If a prospect shows interest in a product, the agent must get an accurate quote in real-time and be able to generate a proposal on the fly.

After the customer has accepted the proposal, he has to fill the proposal form. If a paper form is used, there will be a delay in the proposal being converted into a policy. Agents would generally prefer to recommend products of those companies that have quicker proposal to policy conversion. So, carriers must provide agents with the ability to submit the forms online.

Once a proposal is submitted, channel partners should be able to track the status of the proposal through an online portal. This will help reduce call-center costs because agents do not need to keep calling up to check on the proposal status.

Channel Portal

If internet gets a way of selling insurance, then portals can be of immense significance. It can prove to be of utmost significance and cost effective measure .For e.g. in foreign countries, a major servicing cost for insurance companies is call centers to support agents.

Here’s where a portal can be particularly handy. Let’s take an example. Today, a large insurance company may get as many as 20,000-30,000 calls a month from agents. On average, each call costs $10 – and that’s just the manpower costs; add communication charges and it is much higher. In a year an insurance company would get around 400,000 such calls, which would, at $10 a call, would cost the insurance company $4 million.

40

A portal that provides information at the click of a mouse to those who want it will lead to a drastic reduction in such calls. Even if it reduces the number of calls by 10%, it means a substantial cost saving for the company.

A portal will also reduce the cost an insurance company spends in producing marketing collateral. Companies keep sending collateral to channels. Each agent may get as many as 100 brochures a month, whether he wants it or not. Insurers can provide these collaterals as downloads or even have a system in place that enables such brochures to be sent on request. The result: big savings in printing and postage costs.

Channel Management

An ideal channel management system will provide insurers with the ability to quickly configure new channels whether it is bank assurance, IFAs or broker-dealers, and add new partners. The system must be flexible enough to accommodate a particular channel’s hierarchical needs and manage each channel through a set of comprehensive business rules.

The system should help insurance companies and its channels evaluate producer performance across products, channels and locations.

The channel management component should allow insurers and channels to perform a variety of analyses such as target variance, KPI evaluation, and performance evaluation of producers for promotion, demotion or transfer and channel performance evaluation.

Insurers should be able to manage different types of commissions across products, channels, producers and regions. They should also be able to launch incentive schemes in a jiffy and then be able to calculate and distribute the benefits to individual producers. To do this, the system should be able to do formula-driven benefit calculations.

41

A NEW OPPORTYNITY ON THE HORIZON…………..

“MICRO INSURANCE”

Micro-insurance can offer innovative ways to combat poverty by providing the poor options to systematically manage life and livelihood risks. So far, insurers have not provided services to the poor because it is not thought profitable. But there is still a way to address the mismatch between the needs of the insurers and the insured.

A Brief Analysis

In India alone, the untapped market is estimated to range between $1.4 billion and $1.9 billion, covering life and non-life services. This is only expected to grow as insurance is better understood among potential clients and a wider range of risks are recognized as insurable. Insurance currently covers only 2% of the poor in India. Up to 90% of the population, or 950 million people, are excluded from services—a huge missing market.

Catalyzing micro-insurance can result in a ‘win-win’, combining commercial profit with social benefits. At the macro level, insurance can provide long-term funds that can be used for infrastructure development. At the micro level, insurance facilitates systematic risk management before an unfortunate event occurs.

What are some of the critical issues inhibiting the development of this niche industry?

There are both demand and supply-side bottlenecks. In India, even among the well-off, there are mixed expectations from insurance—besides covering risk, many expect a ‘return’ on premium. Most non-life products have to be ‘sold’ (often through compulsion). Insurers have tended to limit coverage of the ‘bottom of the pyramid’ population to what is required by regulation, and have only recently started expanding their client base.

Education, training and marketing can overcome that challenge. To begin with, insurers must invest in product development. Most of what is available are standardized products meant for a relatively better-off urban clientele. Products for the rural population do exist, but they are driven by the quota obligations imposed by Insurance Regulatory and Development Authority (IRDA), rather than by market needs. The concerns of the poor include risks like illness; accidents like falling off a tree or suffering a snake bite; natural disasters; man-made disasters like riots and fire; harvest failure; farm animal illness and death.

The affordability of premiums is another inhibitor. Premiums tend to be high in the absence of adequate historical data on risks and claims. Companies use macro data and overcautiously add on ad hoc cushions. Information does exist with NGOs and some insurers. Data pooling could help evolve a system of actuarial pricing that aligns risks with premiums better.

42

Difficulties Faced

Difficulties in distribution because of remote locations and poor infrastructure also add to costs, as doe’s ignorance about potential clients. Here, it would help to build partnerships with intermediaries like NGOs, microfinance institutions, community-based organizations and self-help groups (SHGs), which can offer a knowledge base for the design of new products and procedures. Distribution channels can also be developed through rural branches of banks.

While centralizing services minimizes insurers’ costs, it delays settlements, which, given the complicated procedures, can also frustrate efforts to expand the niche. A solution could be decentralized procedures, especially for low-value claims, in local languages.

Opportunities Ahead

High economic growth coupled with increased financial flows to rural areas is creating new opportunities for multiple enablers to come together. Just look at the spread of SHGs. Or the increase in IT/telecom facilities in rural India would be ideal to make a bigger push.

Today, the micro-insurance sector is at the same turning point that micro-credit was a decade ago. The sector needs a long-term perspective that combines responsiveness to client priorities with market development and financial viability, replacing the current preoccupation with immediate profits. Given the country’s size and diversity, the Indian experience can provide policy lessons for other developing countries, too.

43

CHAPTER 5

RESEARCH METHODOLOGY

44

RESEARCH METHODOLOGY

5.1 RESEARCH METHODOLOGY

Research in common parlance refers to a search for knowledge. One can also define research as a scientific search for pertinent information on a scientific topic. In fact, research is an art of scientific investigation. Research Methodology is the techniques used in carrying out the research. Research Methodology provides the researcher to know about the type of research, type of data research plan and sampling plan used for the project. Research is a scientific and systematic search for pertinent information on a specific topic. Thus when we talk of research methodology we not only talk about research method but also conduct the logic behind the methods we use in the context of our research study

Statement of Problem

Market analysis and new channel development for HDFC Standard Life Insurance and the revival of the dead channels.

Need For Study

Insurance industry scenario having metamorphosed from a seller’s market to a buyer’s market, marketing today gives the cutting edge. Increasingly, companies are trying to make more FC’s for there company for selling there products. The channel members on their side are looking at the company name and brand image as the deciding factor with emphasis on facts like margins, discounts, credits, price levels, delivery regularity and finally advertising promotion.

This project is executed to find out whether the FC’s are aware of various new policies which are available in the market and the preferences for which policy is more. To check whether the FC’s & consumer’s are all satisfied with the different investment plans available in the market. And finally check for the FC’s feedback towards the company.

Research Design

A research design is the specification of the methods and acquiring the information needed. A research design is the arrangement of condition for collection and analysis of data in a manner that aims to combine relevance to the research purpose with economy in procedure. Research design is the plan and structure of investigation so conceived as to obtain answers to research questions the plan is overall schemes or program of the research. It includes an outline of what the

45

investigator will do from writing hypotheses and their operational implication to the final analysis of data. A structure is the framework, organization, or configuration of the relation among variables of a study. A research design expresses both the structure of the research problem and the plan of investigation used to obtain empirical evidence on relations of problem.

5.2 TYPE OF RESEARCH DESIGN

Descriptive Research

Descriptive research includes surveys and fact – finding enquires of different kinds. The major purpose of descriptive research is description of the state of affairs, as it exists at present. This method is undertaken when the researcher is interested in knowledge about the characteristics of certain groups such as people.

5.3 DATA COLLECTION

There may be different types of information and data. Some of the information may be published, while some is unpublished, some is incomplete and some is reliable data and some is biased. It is necessary for the researcher to know of information which is usually employed in marketing research work, and the types of sources from which it is generally collected. The research problem decides the nature of the source of data. There may be secondary data and primary data.

Primary Data Source

Primary data is collected during the course of asking questions by performing survey. Primary data is obtained either through respondent, either through questionnaire or personal interviews. I have collected the primary data through questionnaire.

Secondary Data Source

Information already collected by the company guide on companies and their products, various types of brands in the market etc.

Research Instrument

I have used the structured questionnaire in my research process, which was carefully designed keeping the entire objective in my mind. Most of the questions in my questionnaire were closed ended in nature. I also used interviews for collecting data.

46

5.4 SAMPLING

Sample Plan

A sample is a fraction of a subset of population through a valid statistical procedure so it can be regarded as representative of the entire population. The valid statistical procedure of drawing sample from the population is called sampling.

Sample Size

The larger the sample, the more accurate the result would be but practically it is not feasible to target the population. In this project, being aware of the time constraints, sample size is 100.

5.5 SAMPLIMG METHOD

For my research, I have used “Non Random Sampling”. The logic behind this sampling is that certain relevant characteristics describe the dimensions of the population. If a sample has the same distribution on these characteristics, then it is likely to be representative of the population regarding other variables on which we have no control.

Field survey

A method of instrument the respondents from the universe by the help of instrument is questionnaire. Survey is great benefit because of its wide scope.

5.6 TOOLS OF DATA COLLECTION

“QUESTIONNAIRE” was the tool used for data collection. The questionnaire was designed keeping in mind the objectives of the study. It contained a set of questions that gave users as required by the researcher.

Statistical Tools

Percentage method

Weighted average method

47

CHAPTER 6

DATA ANALYSIS

48

DATA ANALYSIS

1) Heading – Classification Based on Age Group of the Respondents

Table of information

Age Group No. of Respondent

25-30 38

30-35 30

35-40 18

40-45 10

45-50 4

Diagrammatic Representation

Interpretation

Highest number of Respondents from Age group below 30, mostly BPO

executives, and students – 38%

49

2) Heading – Income Level of the Respondents

Table of information

Age Group Below 1.5 Lakh 1.5-3 Lakh 3-5 Lakh Above 5 Lakh

Below 30 10 15 10 3

30-40 4 7 27 10

Above 40 1 3 2 8

Diagrammatic Representation

Interpretation

Highest, 27 respondents in income bracket 3 - 5 lakh, which comprises mainly

of age group below 30-40 years. Minimum 1 respondent is in income bracket of

below 1.5 lakh of which are in age group of above 40 years.

3) Heading – Marital status of the respondents.

50

Table of information

Age Group Married Unmarried

Below 30 13 25

30-40 30 8

Above 40 14 0

Diagrammatic Representation

Interpretation

The no. of respondent who are single is 33, and the no. of respondent who are

married is 57.

51

4) Heading - No. of Respondents aware of new insurance policies of the company.

Sample size 50

Table of information

Age Group Awareness

25-35 25

35-45 20

45-55 5

Diagrammatic Representation

Interpretation

Highest awareness is among the age group 25-35, the rating for the company

on an average is 36% of the FC responded the company is average.

52

5) Heading – Rating given to the company by the FC’s.

Sample size 50

Table of information

1 = Very Good, 2 = Good, 3 = Average, 4 = Bad, 5 = Very Bad

Rating for Company

1 2 3 4 5

5 6 10 4 0

4 4 5 5 2

1 0 3 1 0

Diagrammatic Representation

Interpretation

The rating for the company on an average is 36% of the FC responded the

company is average.

53

CHAPTER 7

FINDINGS & LIMITATIONS

54

ANALYSIS AND FINDINGS

Several insurers in Asia, especially in South Korea, are coming up with innovative, multi-channel and direct marketing techniques with successful results

Banc assurance could turn out to be an expensive channel; hence success was all about strong partnership and adjustment and not necessarily the right "model"

Channel conflict may happen but this can be regulated. The agency system is still the most expensive form of distribution. Commission rates

ranging from 40% to 80% on first-year premium for a regular premium savings contract are very high due to the pyramid agency structure that rewards not just the agent but also his managers through overriding commissions and other benefits.

At present the distribution channels that are being utilized are:

Direct selling Corporate agents i.e. pushing the insurance product through the directors or

partners of a company Group selling Worksite marketing Brokers and cooperative societies

Analysis based on responses of the business associatesMajor Findings……………..

After analyzing the responses given by the consultants, the various reasons for non performance are as follows-:

1) Few respondents believed that they themselves are not fit for the job as they lack skills to convince people.

2) Some blamed negligence on part of the office staff in terms of lack of proper product training, knowledge about product and procedures. They believed they did not get the attention they deserve.

3) Frequent changes or job hopping among the SDM’s created a confusion regarding accountability so as to who is their reporting superior.

4) There are also a hand full of consultants whose licenses have expired .Some of these have been great performers and still have the potential of doing great, but completely out of negligence they have not renewed their licenses and no one else stepped forward to sufficiently motivate them to do so.

55

LIMITATIONS OF THE PROJECT

The study covers the part of Pune region only and due to the limited sample size,

the facts revealed in the study may not generalize.

While calculating the percentages, approximations are made to the nearest figures.

The analysis is based on what public & FC’s opinion at the time of survey. The

study may not produce the same findings if done at a later stage of time.

While filling the questionnaires public & FC’s could not provide 100% accurate

information because of their personal limitations.

Biased reply of many people

Time constraints as limited time for the survey.

56

CHAPTER 8

CONCLUSION

57

CONCLUSION

HDFC Standard Life is having good brand image in the market but is still lagging

because poor advertisement and less command over FC’s. There is a lack of

coordination between some of the SDM’s and FC’s i.e. why some of the consultants are

becoming dead.

The company must create awareness for their new products among the FC’s and

the common public by the help of advertising, putting hoardings in main streets of the

cities or by giving audio visual presentation.

It is clear that the only way in which insurance company can address the

challenges and capitalize on the opportunities is by investing in systems that are

customizable, open, and flexible and can be easily integrated with legacy and other

back-office platforms.

Such a system will help them make their distribution chain more effective and

efficient, push new products through the distribution pipeline at a faster pace, reduce

operational costs and inefficiency and position themselves as a preferred partner with

channels.

58

RECOMMENDATIONS

1) Recommendations for developing alternate new channels

With the liberalization of the insurance sector and competition tougher than ever before, companies are increasingly trying to come out with better innovations to stay that one step ahead. Currently, insurance agents are still the main vehicles through which insurance products are sold. But in a huge country like India, one can never be too sure about the levels of penetration of a product. It therefore makes sense to look at well-balanced, alternative channels of distribution.

2) Recommendations for Retaining Existing Channels

Making it easy for channels to do business with them Providing good and quick underwriting support Delivering differentiated service to top performers Providing proactive service Launching incentive plans and contests Managing commissions in a more efficient manner

3) Advertising

Company should increase the level of advertising through wall painting and hoardings for enhancement of sell and also company should advertise their product through bus panels and audiovisuals etc.

HDFC Standard Life should keep attention on working of FC’s. Company should maintain a high degree of motivation between channel member

and dealer. For this the channel members should take participation into company’s activities.

59

BIBLOGRAPHY

BOOKS

1. MARKETING MANAGEMENT 12th ed., Pub: Tata McGraw Hill - PHILIP KOTLER

2. MARKETING MANAGEMENT 2nded., Pub. Macmillan - RAMASWAMI & NAMAKUMARI

3. MARKETING MANAGEMENT 2nd ed., Pub: Tata McGraw - SAXENA

4. MARKETING MANAGEMENT 7th ed. Himalaya Publishing House - S.A.SHERLEKAR

5. MARKETING MANAGEMENT 6th ed., Pub: Tata McGraw - PETER, DONNELLY

6. MARKETING MODALS Pub: Prentice Hall India - ILIEN KOTLER, MOORTHY

JOURNALS

1. BUSINESS STANDERED 2. ICFAI MANAGEMENT RESEARCH Vol. V No. 93. ICFAI MANAGEMENT RESEARCH Vol. V No. 10

INTERNET WEBSITES

1. www.hdfcinsurance.com 2. www.google.com

60

ABBREVIATIONS

HDFC – Hosing Development Financial Corporation

HDFCSLIC – HDFC Standard Life Insurance Company

FC – Financial Consultant

IRDA – Indian Regulatory & Development Authority

SDM – Sales Development Manager

BDM – Branch Development Manager

61

ANNEXURE

Questionnaire Designed To Recruit FC

Name…………………………………….Age………………………………………Qualification……………………………. Occupation………………………………Address…………………………………. Married , Single Phone no………………………………...

1) What kind of occupation are you into?

a) Full time b) Part time

2) What is your income level?

a) Below 1.5 Lakh b) 1.5 – 3 Lakh c) 3 -5 Lakh d) Above 5 Lakh

3) Do you have any other income generating source?

a) Yes b) No

4) Would you like to add any other source to your monthly earnings?

a) Yes b) No

If no, why? ……………………………………………………………If yes, proceed…

5) If such source is added how much do you expect to earn from it?

a) 5000-10,000 b) 11,000-15,000 c) 16,000-25,000 d) 26000 and above

6) If given a chance would you like to work with HDFC Standard Life?

a) Yes b) NoIf yes, proceed…

7) Do you mind if I call you in this regard?

a) Yes b) No

62

Questionnaire Designed To Tab FC’s Responses:-

Name…………………………………….Age………………………………………Qualification……………………………. Occupation………………………………Address…………………………………. Married , Single Phone no…………………………………

1) You are working as an FC for HDFCSLIC

a) Full time b) Part time

If part time, please specify your other engagements…………………………………………………………………………..…………………………………………………………………………..

2) For how long have you been associated with HDFCSLC?

a) Less than 1 yr b) 1-2yr

c) 3-5yrs d) more than 5 yrs

3) On a scale of 1 to 5, rate your performance as an FC where (1=very good, 2=good, 3=average, 4=bad, 5=very bad)

1…………2…………3…………..4……………..5…………..

4) Same as above rate the support facilities provided to you by HDFCSLIC

1…………2…………..3……………4……………5…………..

5) Are you aware of new policies and schemes launched by HDFCSLIC?

a) Yes b) No

6) Any problems faced by you in running business Your comments, please

…………………………………………………………………………………..………………………………………………………………………………….

63