residential property insurance coverages

TRANSCRIPT

.www.InsuranceCommunityUniversity.com

Residential Property Insurance Coverages

.www.InsuranceCommunityUniversity.com

Insurance forms and endorsements vary based on insurance company; changes in edition dates; regulations; court decisions; and state jurisdiction. The instructional materials provided by The Insurance Community Center and its authors is intended as a general guideline and any interpretations provided by The Community do not modify or revise insurance policy language. •Information which is copyrighted and proprietary to Insurance Services Office, Inc. (“ISO Material”) is included in this publication. Use of the ISO Material is limited to ISO Participating Insurers and their Authorized Representatives. Use by ISO Participating Insurers is limited to use in those jurisdictions for which the insurer has an appropriate participation with ISO. Use of the ISO Material by Authorized Representatives is limited to use solely on behalf of one or more ISO Participating Insurers.•The authors of these materials, Insight Insurance Consulting and The Insurance Community Center assumes neither liability nor responsibility to any person or business with respect to any loss that is alleged to be caused directly or indirectly as a result of the instructional materials provided.

Insight Insurance Consulting714 803-5830

laurie@insightinsuranceconsulting.comwww.insightinsuranceconsulting.com

www.theinsurancecommunity.com Copyright 2010

All Rights Reserved

2

.www.InsuranceCommunityUniversity.com

What this class will cover

Steps in reviewing the residential property and identifying exposures

Underwriting Considerations for the various policies

3

.www.InsuranceCommunityUniversity.com

What this class will cover

Policies reviewed: Dwelling Fire Difference in Conditions and Wrap

Arounds Homeowners Townhouses Tenants Package Cooperatives (Coop) Condominiums

4

.www.InsuranceCommunityUniversity.com

Steps in reviewing residential properties and

identifying exposures

5

.www.InsuranceCommunityUniversity.com

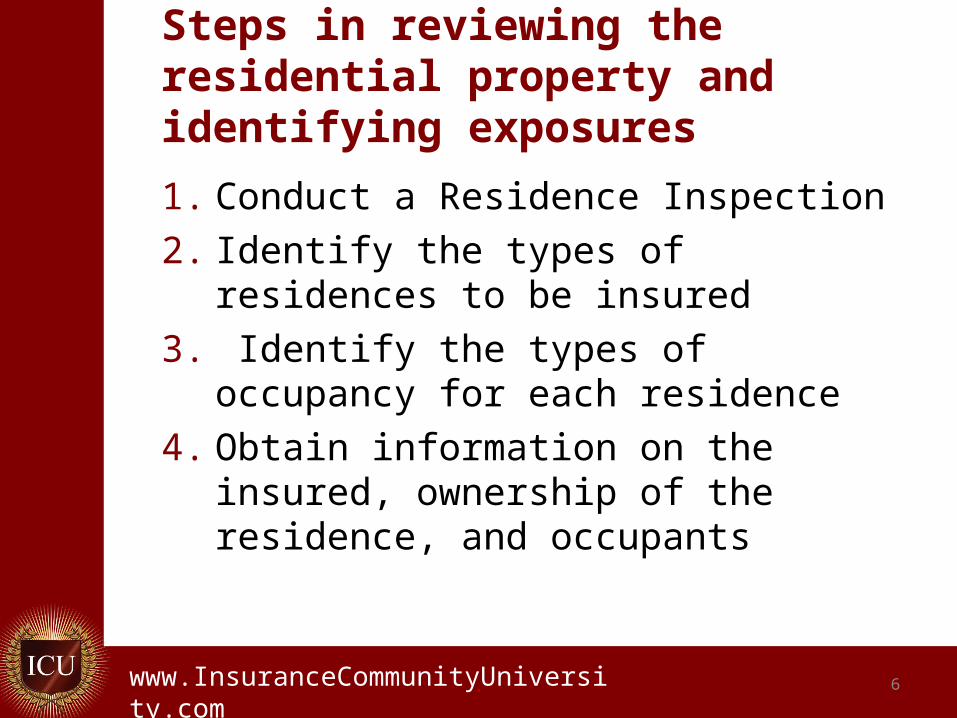

Steps in reviewing the residential property and identifying exposures

1. Conduct a Residence Inspection

2. Identify the types of residences to be insured

3. Identify the types of occupancy for each residence

4. Obtain information on the insured, ownership of the residence, and occupants

6

.www.InsuranceCommunityUniversity.com

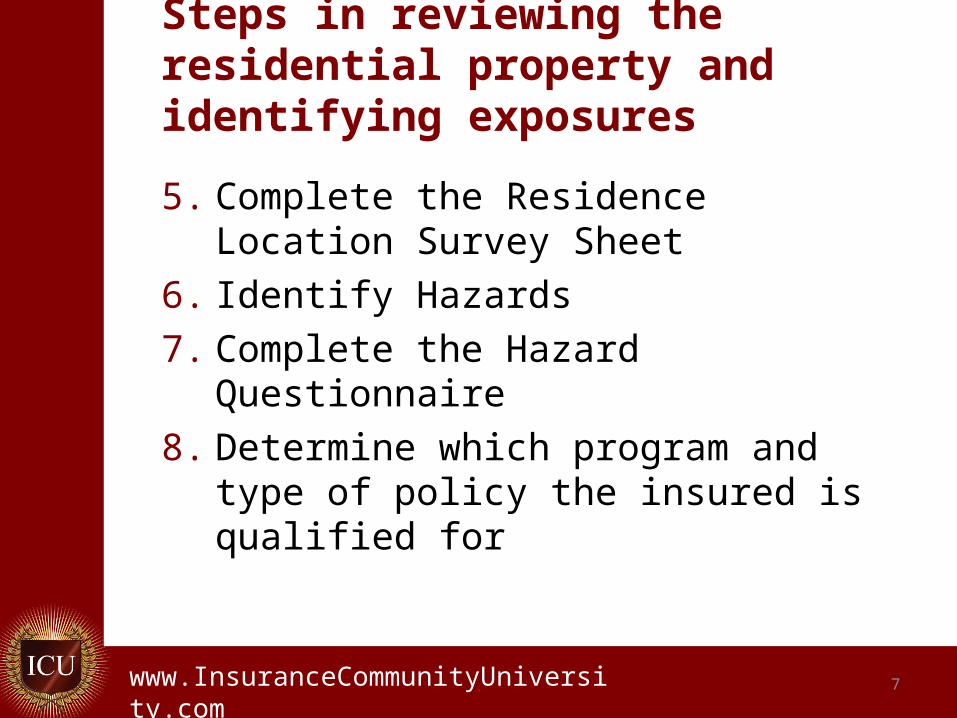

Steps in reviewing the residential property and identifying exposures

5. Complete the Residence Location Survey Sheet

6. Identify Hazards

7. Complete the Hazard Questionnaire

8. Determine which program and type of policy the insured is qualified for

7

.www.InsuranceCommunityUniversity.com

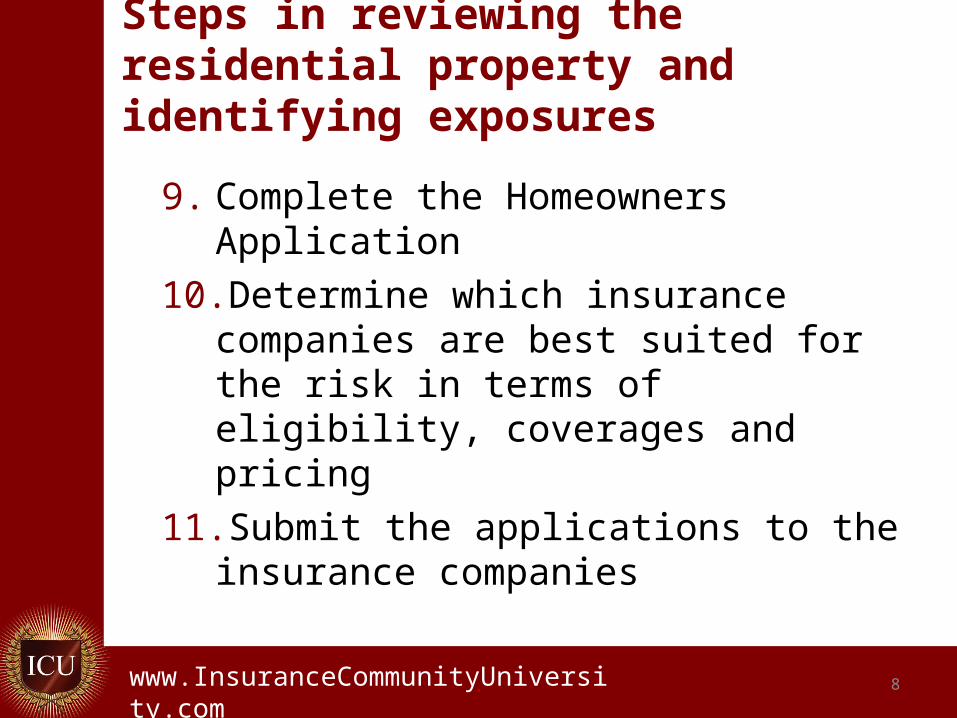

Steps in reviewing the residential property and identifying exposures

9. Complete the Homeowners Application

10.Determine which insurance companies are best suited for the risk in terms of eligibility, coverages and pricing

11.Submit the applications to the insurance companies

8

.www.InsuranceCommunityUniversity.com

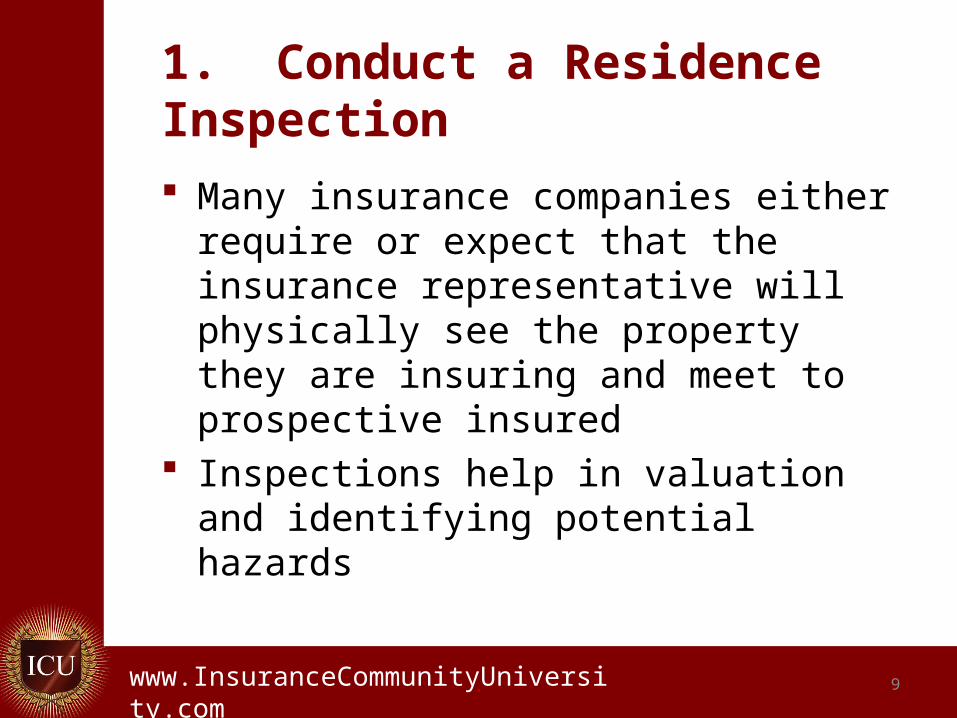

1. Conduct a Residence Inspection

Many insurance companies either require or expect that the insurance representative will physically see the property they are insuring and meet to prospective insured

Inspections help in valuation and identifying potential hazards

9

.www.InsuranceCommunityUniversity.com

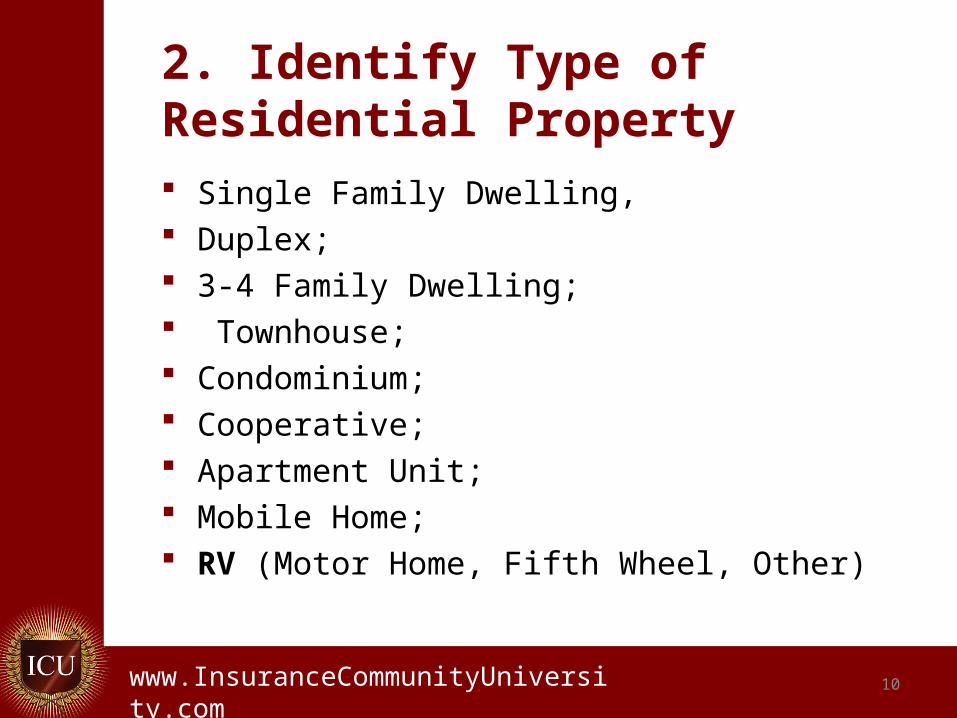

2. Identify Type of Residential Property Single Family Dwelling, Duplex; 3-4 Family Dwelling; Townhouse; Condominium; Cooperative; Apartment Unit; Mobile Home; RV (Motor Home, Fifth Wheel, Other)

10

.www.InsuranceCommunityUniversity.com

2. Identify Type of Residential Property

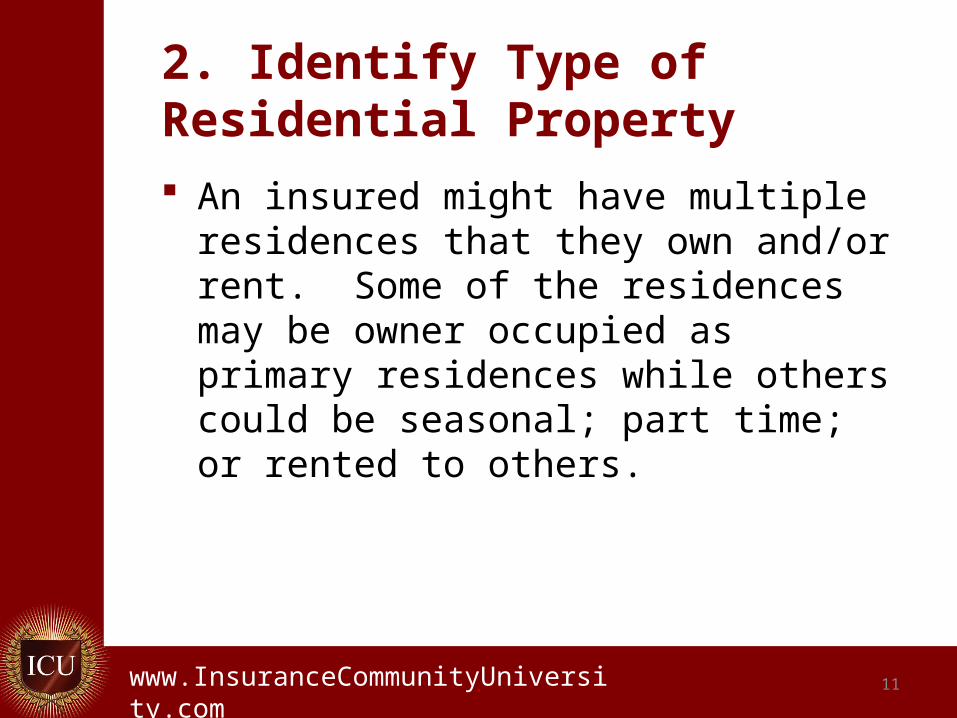

An insured might have multiple residences that they own and/or rent. Some of the residences may be owner occupied as primary residences while others could be seasonal; part time; or rented to others.

11

.www.InsuranceCommunityUniversity.com

3. Identify Type of Occupancy

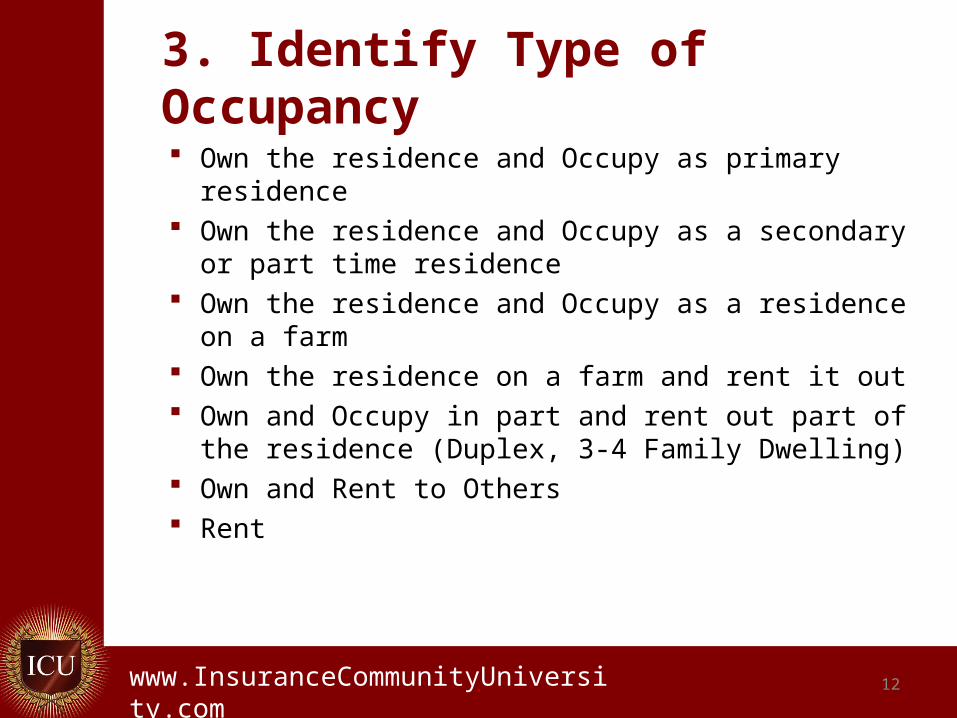

Own the residence and Occupy as primary residence

Own the residence and Occupy as a secondary or part time residence

Own the residence and Occupy as a residence on a farm

Own the residence on a farm and rent it out Own and Occupy in part and rent out part of the

residence (Duplex, 3-4 Family Dwelling) Own and Rent to Others Rent

12

.www.InsuranceCommunityUniversity.com

4. Identify Type of “Ownership”

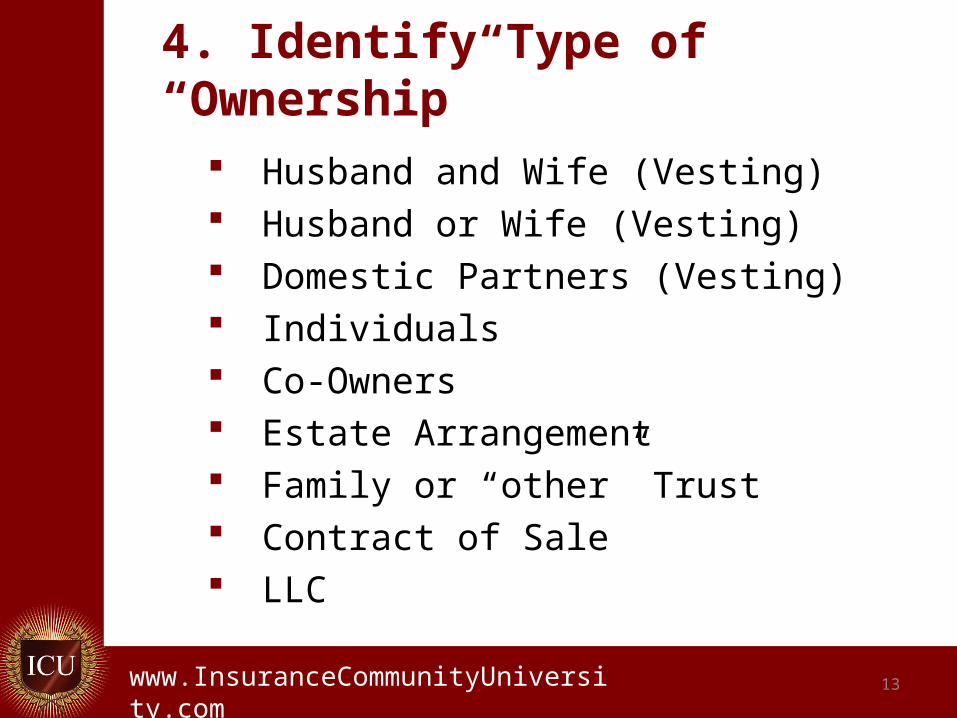

Husband and Wife (Vesting) Husband or Wife (Vesting) Domestic Partners (Vesting) Individuals Co-Owners Estate Arrangement Family or “other” Trust Contract of Sale LLC

13

.www.InsuranceCommunityUniversity.com

5. Complete the Residence Location Survey Sheet

The university has provided a residence location survey sheet in their checklists

14

.www.InsuranceCommunityUniversity.com

6-7 Identify hazards

The residence checklists provides guidelines for checking for hazards

Hazards related to natural hazards and physical hazards of the residence to be insured

15

.www.InsuranceCommunityUniversity.com

8-10 Qualification and Applications Once the field underwriting process is

complete then the correct market for the risk must be determined

It is essential that the application is completed correctly and completely

Supplemental information such as the university residential survey and pictures are helpful in the placement of coverage

16

.www.InsuranceCommunityUniversity.com

Underwriting Considerations

Vary from Company to Company

17

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes Occupancy

Owner Tenant Seasonal Secondary

Condition of the home Age Upgrades Renovations Vacancy

18

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes

Construction Details (such as) Roof Electrical Heating

19

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes Natural Hazards

Location Flood, EQ, Wind Proximity to hazards like distance to

tidal waters Brush Protection Class

20

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes

Hazards Related to Occupancy Trampolines Dogs Swimming Pools Wood Burning Stoves Fuel Tank Storage

21

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes

Hazards relating to the Insured Occupation Financial Stability

Foreclosures/Bankruptcy Pride of Occupancy (Maintenance)

22

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes

Usage of Home Residence Business, Agriculture, etc.

Limits of Insurance Required Insurance to Value

23

.www.InsuranceCommunityUniversity.com

Underwriting Considerations for Homes Security

SL Burglar Alarms Fire Protection Gated Community

24

.www.InsuranceCommunityUniversity.com

Insurance Policies

General Background

25

.www.InsuranceCommunityUniversity.com

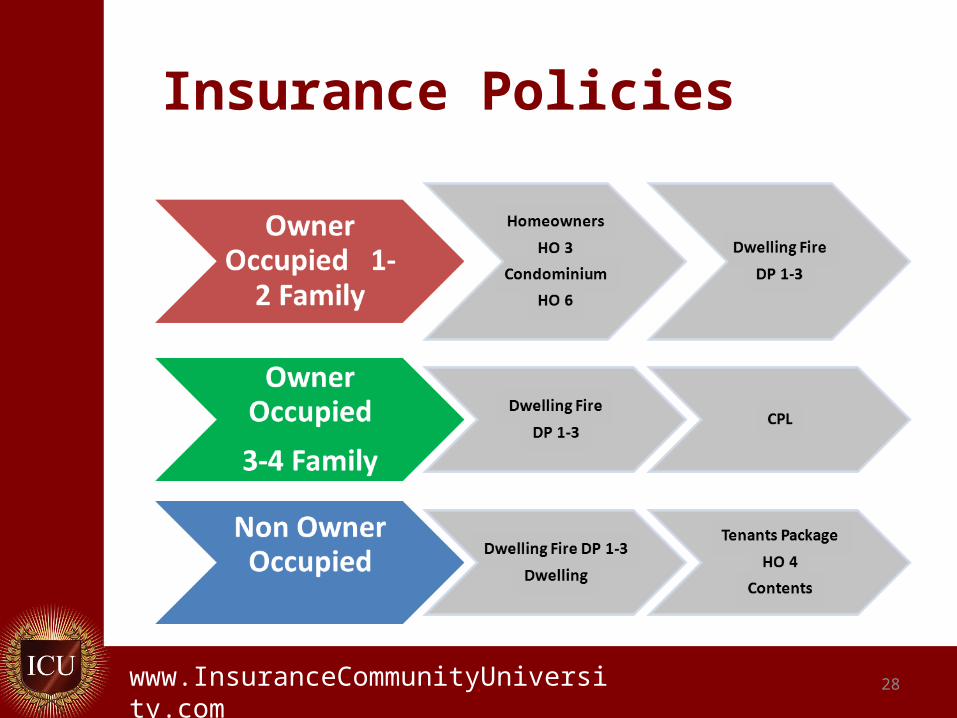

Insurance Policies

There are several forms of insurance for residential properties

The type of policy that should be written on a residence depends on the underwriting considerations discussed in this course

26

.www.InsuranceCommunityUniversity.com

Insurance Policies In general the major considerations that

determine the type of policy to be issued include: Type of Residence Ownership Occupancy Age, Condition and Protection Values

Insurance Companies all have different eligibility requirements for different insurance forms

27

.www.InsuranceCommunityUniversity.com

Insurance Policies

28

.www.InsuranceCommunityUniversity.com

Dwelling Program

DP Series of Forms

29

.www.InsuranceCommunityUniversity.com 30

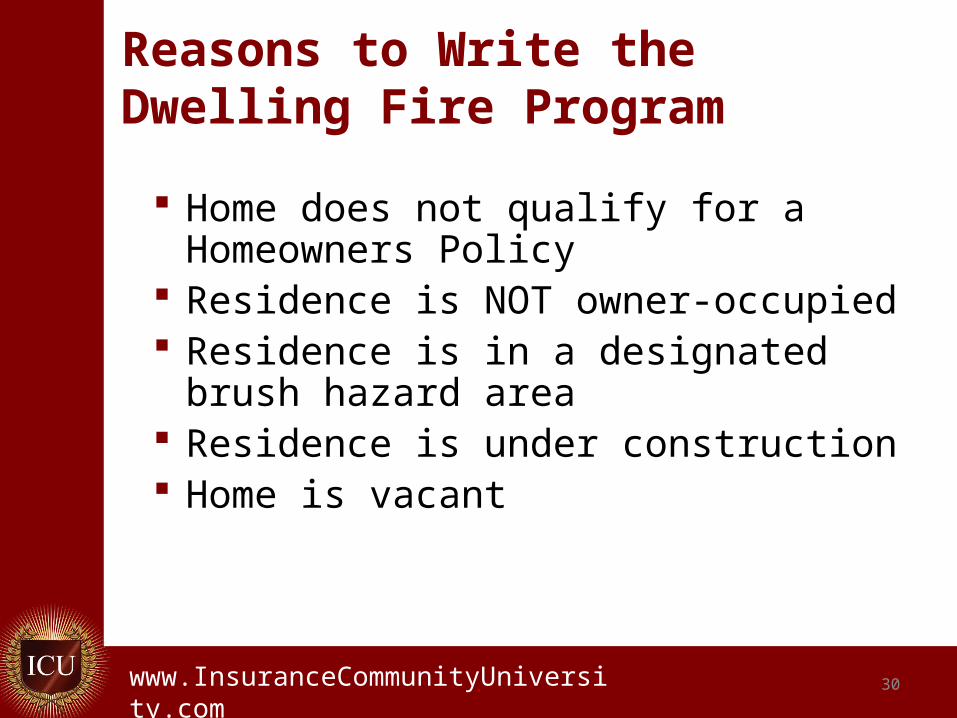

Reasons to Write the Dwelling Fire Program

Home does not qualify for a Homeowners Policy

Residence is NOT owner-occupied Residence is in a designated brush

hazard area Residence is under construction Home is vacant

.www.InsuranceCommunityUniversity.com 31

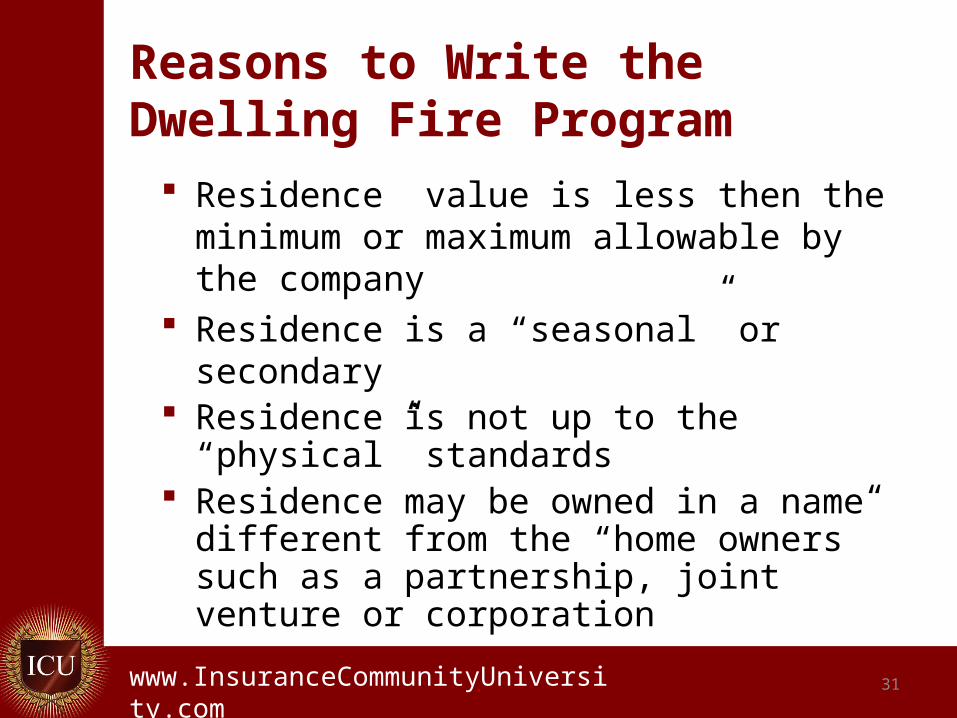

Residence value is less then the minimum or maximum allowable by the company

Residence is a “seasonal” or secondary Residence is not up to the “physical”

standards Residence may be owned in a name

different from the “home owners” such as a partnership, joint venture or corporation

Reasons to Write the Dwelling Fire Program

.www.InsuranceCommunityUniversity.com 32

The insured may prefer having their home issued on a Dwelling Program because: The insured might not want or need the

full range of homeowners coverages The Homeowners Program might be

more expensive than the insured chooses to pay

Reasons to Write the Dwelling Fire Program

.www.InsuranceCommunityUniversity.com 33

Dwelling Program

The Dwelling Program can be written as a Property ONLY policy If written as a property only policy then

the CPL could be written separately or added to an insured’s homeowners policy they have on another property

Some insurance companies will include the Dwelling Fire with the CPL coverages

.www.InsuranceCommunityUniversity.com 34

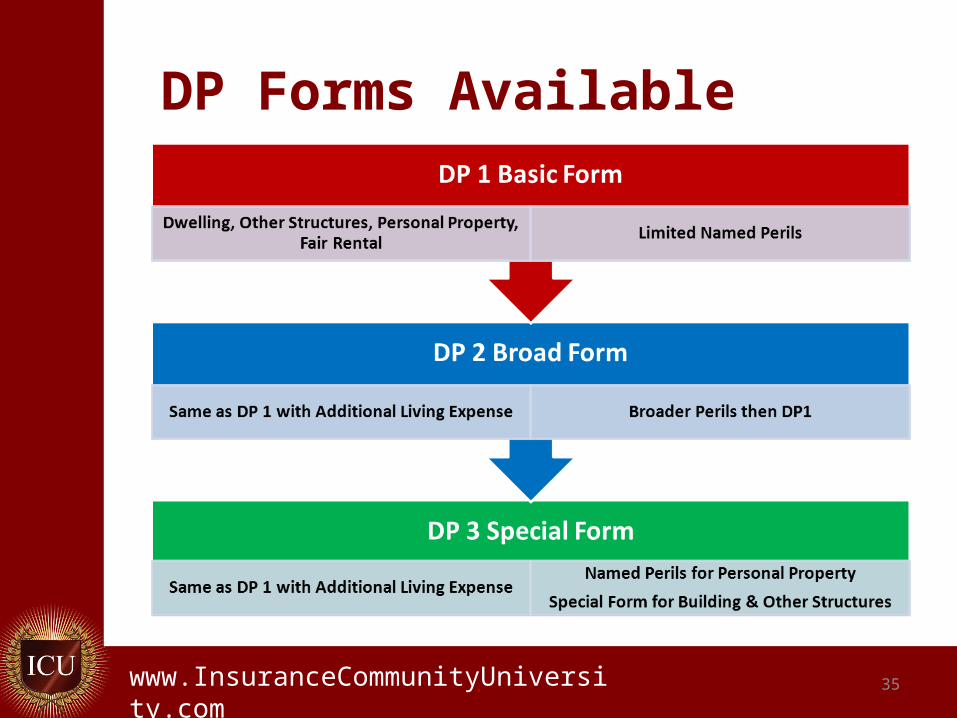

Forms available in the Dwelling Fire Program There are three Coverage Forms available in

the DP series. The DP 00 03 is the most comprehensive of the forms available.

These forms offer property coverages on a dwelling and its contents similar to the coverages under Section I of the Homeowners Form. DP00 01 (DP 1) Basic Form DP00 02 (DP 2) Broad Form DP00 03 (DP 3) Special Form

.www.InsuranceCommunityUniversity.com

DP Forms Available

35

.www.InsuranceCommunityUniversity.com

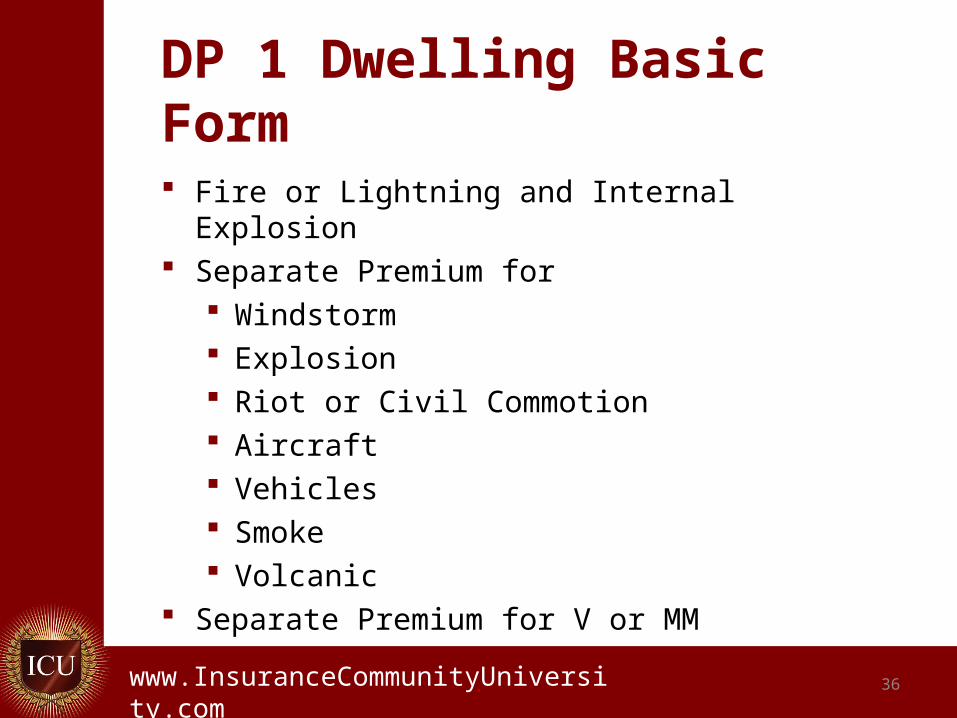

DP 1 Dwelling Basic Form

Fire or Lightning and Internal Explosion Separate Premium for

Windstorm Explosion Riot or Civil Commotion Aircraft Vehicles Smoke Volcanic

Separate Premium for V or MM

36

.www.InsuranceCommunityUniversity.com

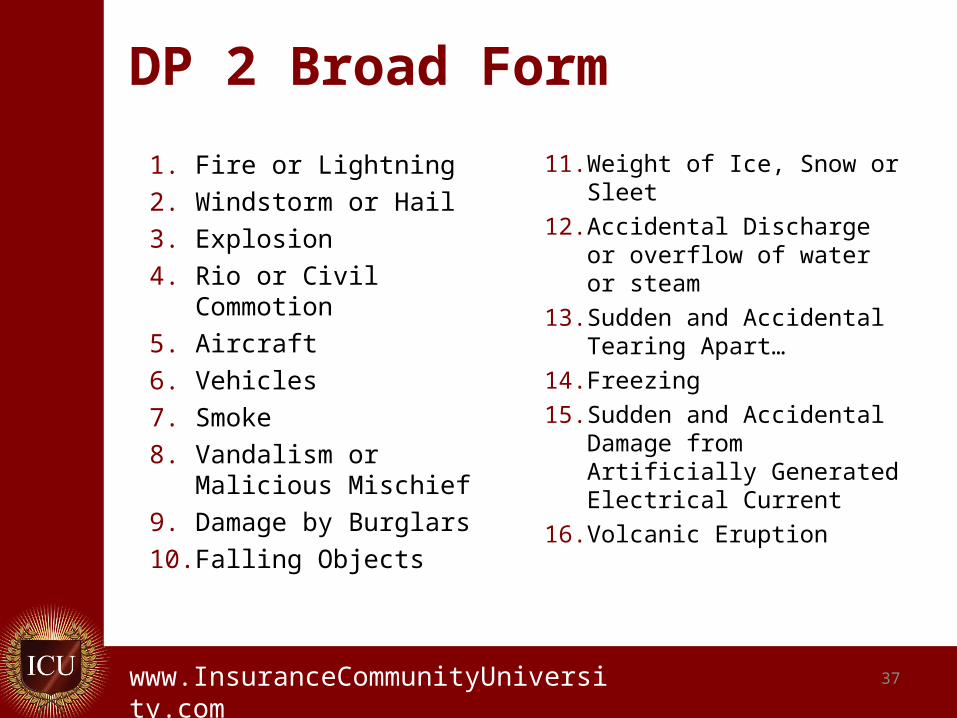

DP 2 Broad Form

1. Fire or Lightning

2. Windstorm or Hail

3. Explosion

4. Rio or Civil Commotion

5. Aircraft

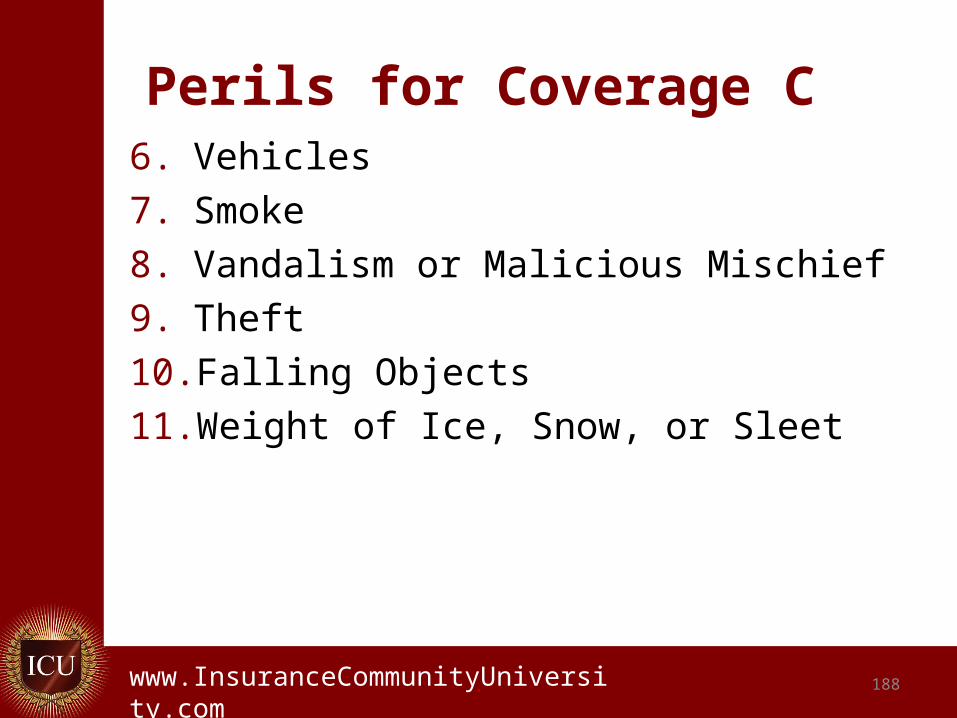

6. Vehicles

7. Smoke

8. Vandalism or Malicious Mischief

9. Damage by Burglars10. Falling Objects

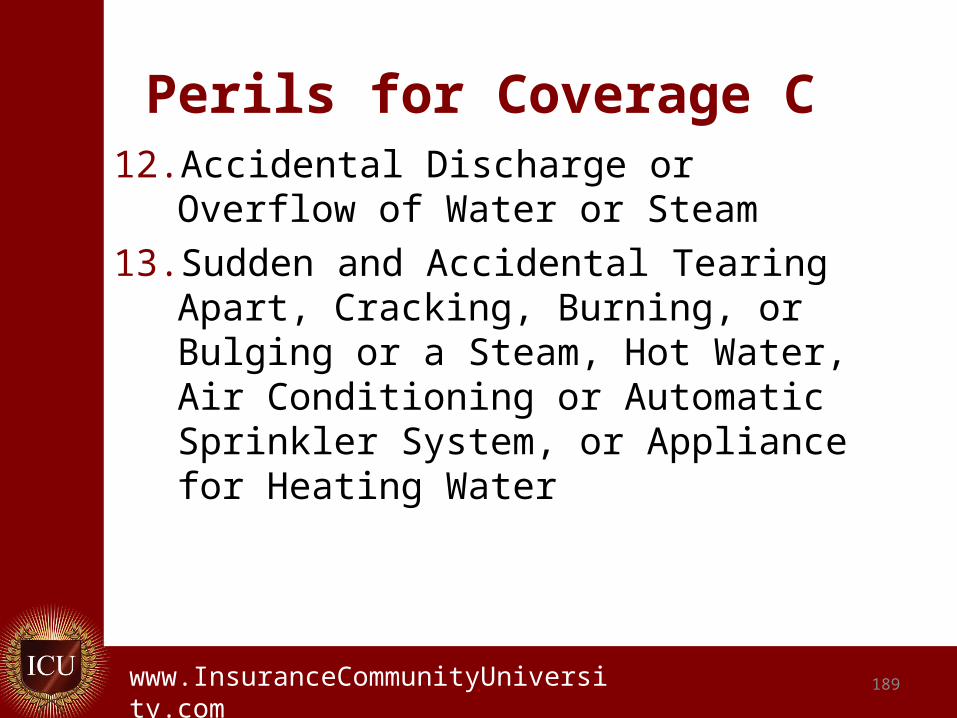

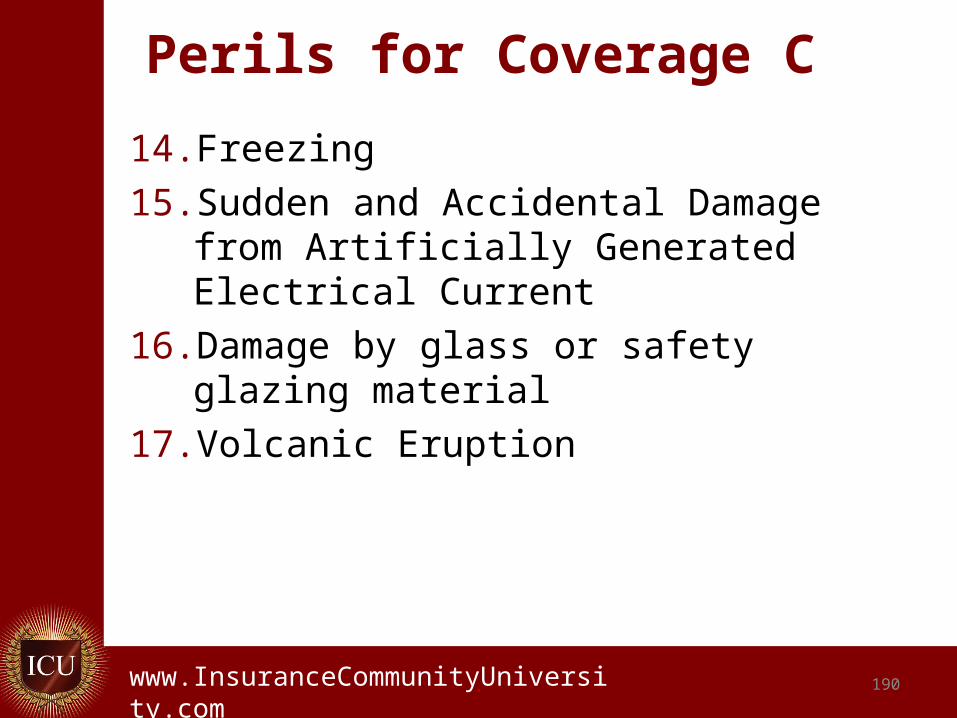

11. Weight of Ice, Snow or Sleet12. Accidental Discharge or

overflow of water or steam13. Sudden and Accidental

Tearing Apart…14. Freezing15. Sudden and Accidental

Damage from Artificially Generated Electrical Current

16. Volcanic Eruption

37

.www.InsuranceCommunityUniversity.com 38

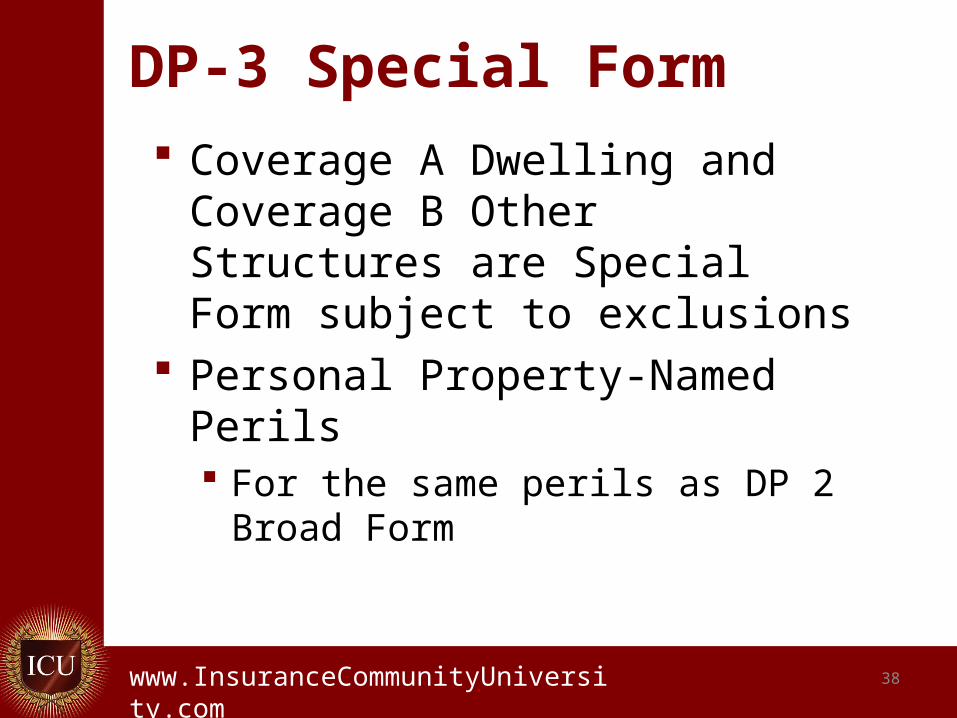

DP-3 Special Form Coverage A Dwelling and

Coverage B Other Structures are Special Form subject to exclusions

Personal Property-Named Perils For the same perils as DP 2 Broad

Form

.www.InsuranceCommunityUniversity.com

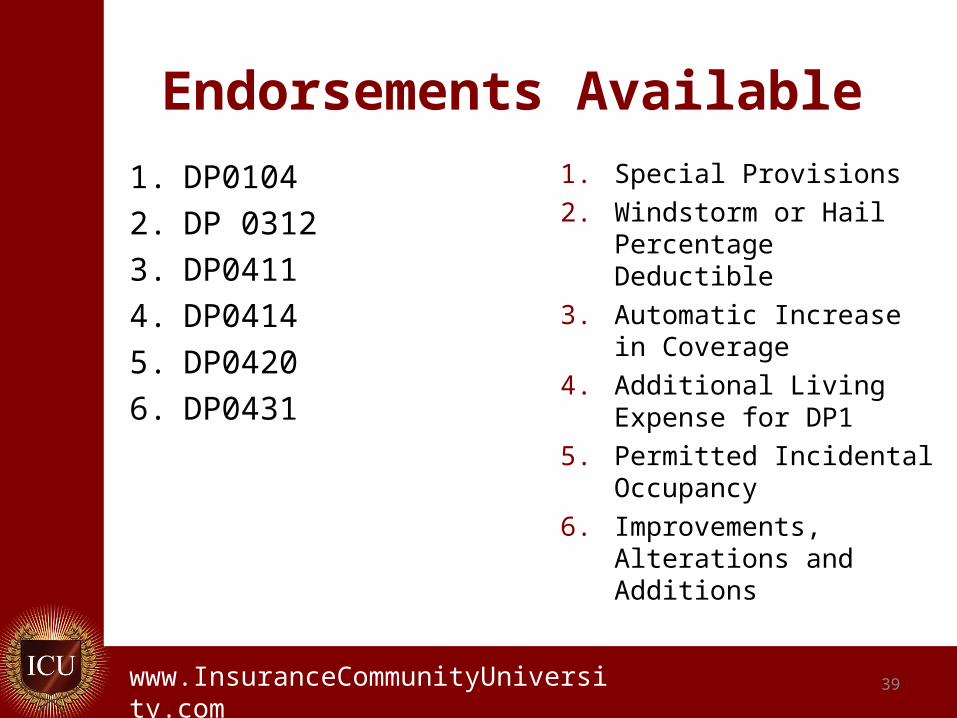

Endorsements Available

1. DP0104

2. DP 0312

3. DP0411

4. DP0414

5. DP0420

6. DP0431

1. Special Provisions

2. Windstorm or Hail Percentage Deductible

3. Automatic Increase in Coverage

4. Additional Living Expense for DP1

5. Permitted Incidental Occupancy

6. Improvements, Alterations and Additions

39

.www.InsuranceCommunityUniversity.com

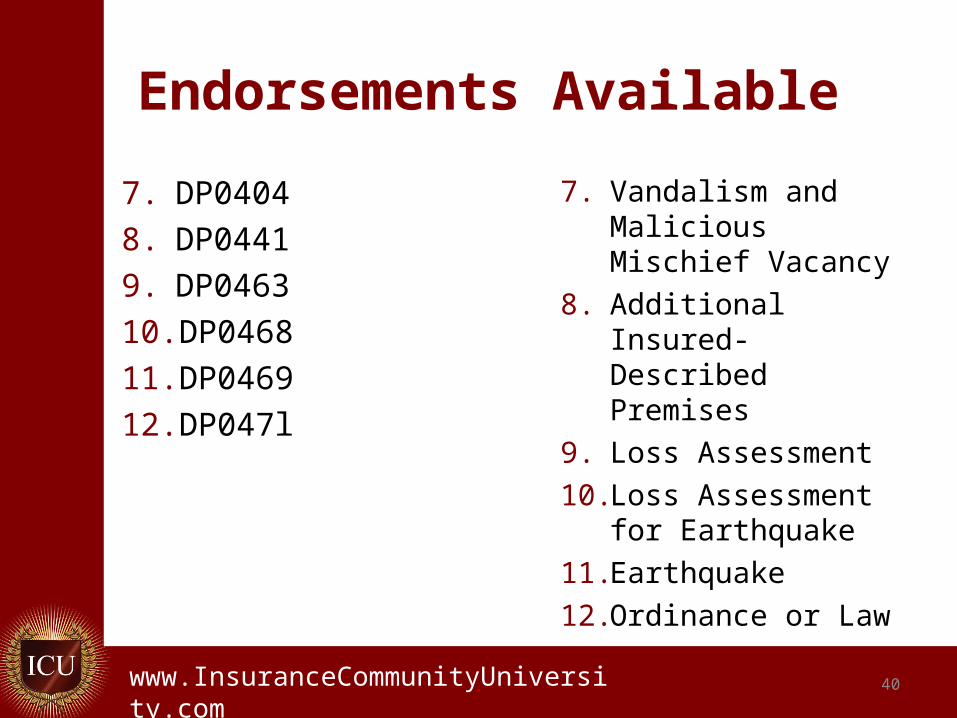

Endorsements Available

7. DP0404

8. DP0441

9. DP0463

10. DP0468

11. DP0469

12. DP047l

7. Vandalism and Malicious Mischief Vacancy

8. Additional Insured-Described Premises

9. Loss Assessment

10. Loss Assessment for Earthquake

11. Earthquake

12. Ordinance or Law

40

.www.InsuranceCommunityUniversity.com

Endorsements Available

13. DP0472

14. DP0473

15. DP0495

16. DP0499

17. DP0530

18. DP1143

19. DP1766

13. Broad Form Theft

14. Limited Theft

15. Water Back Up and Sump Pump Overflow

16. Sinkhole Collapse

17. Functional Replacement Cost

18. Dwelling Under Construction

19. Unit Owners Coverage

41

.www.InsuranceCommunityUniversity.com

Liability Coverages

Comprehensive Personal Liability CPL

42

.www.InsuranceCommunityUniversity.com 43

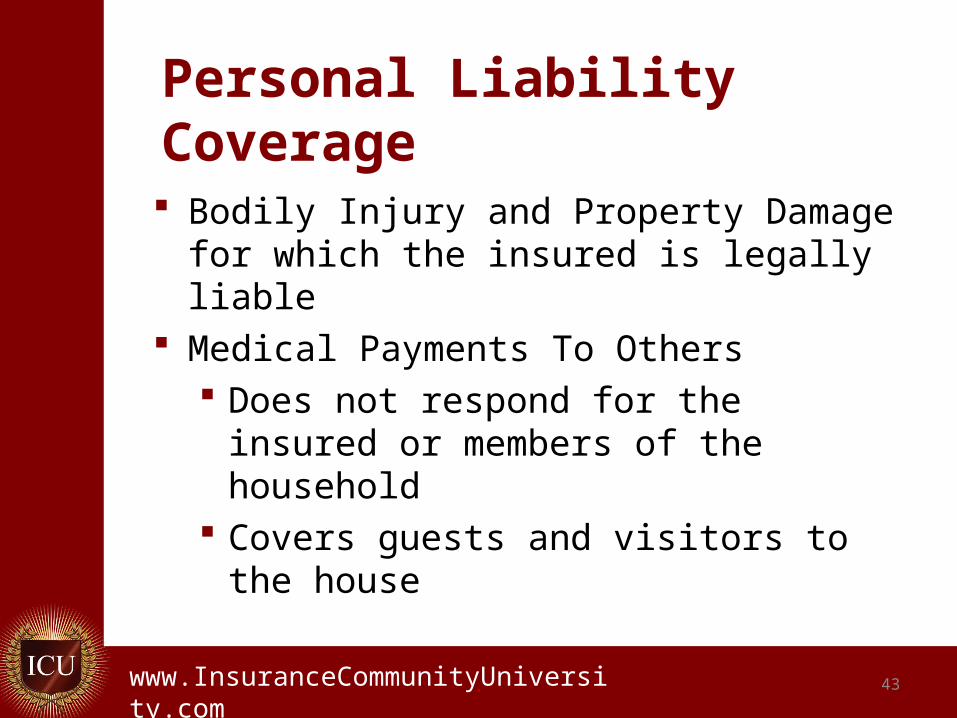

Personal Liability Coverage

Bodily Injury and Property Damage for which the insured is legally liable

Medical Payments To Others Does not respond for the insured or

members of the household Covers guests and visitors to the house

.www.InsuranceCommunityUniversity.com 44

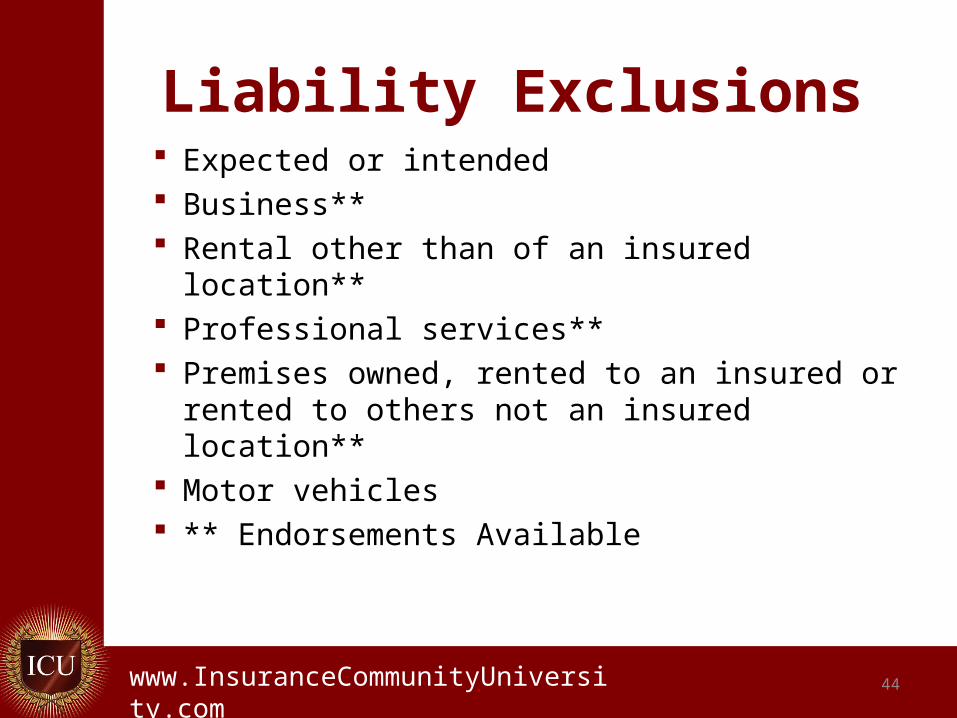

Liability Exclusions Expected or intended Business** Rental other than of an insured location** Professional services** Premises owned, rented to an insured or

rented to others not an insured location** Motor vehicles ** Endorsements Available

.www.InsuranceCommunityUniversity.com 45

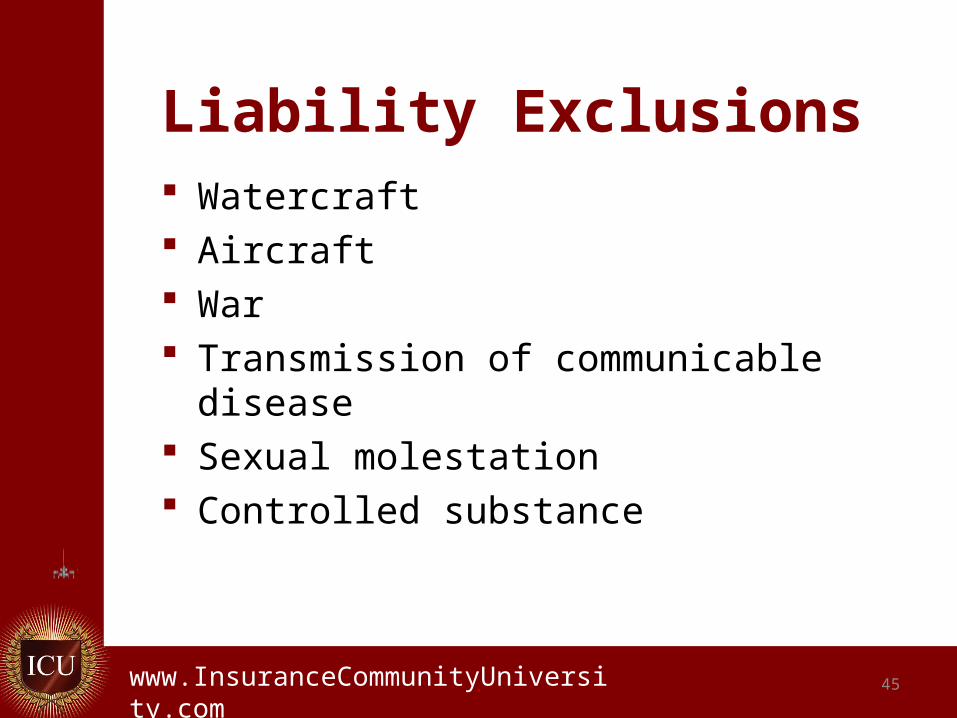

Watercraft Aircraft War Transmission of communicable disease Sexual molestation Controlled substance

Liability Exclusions

.www.InsuranceCommunityUniversity.com 46

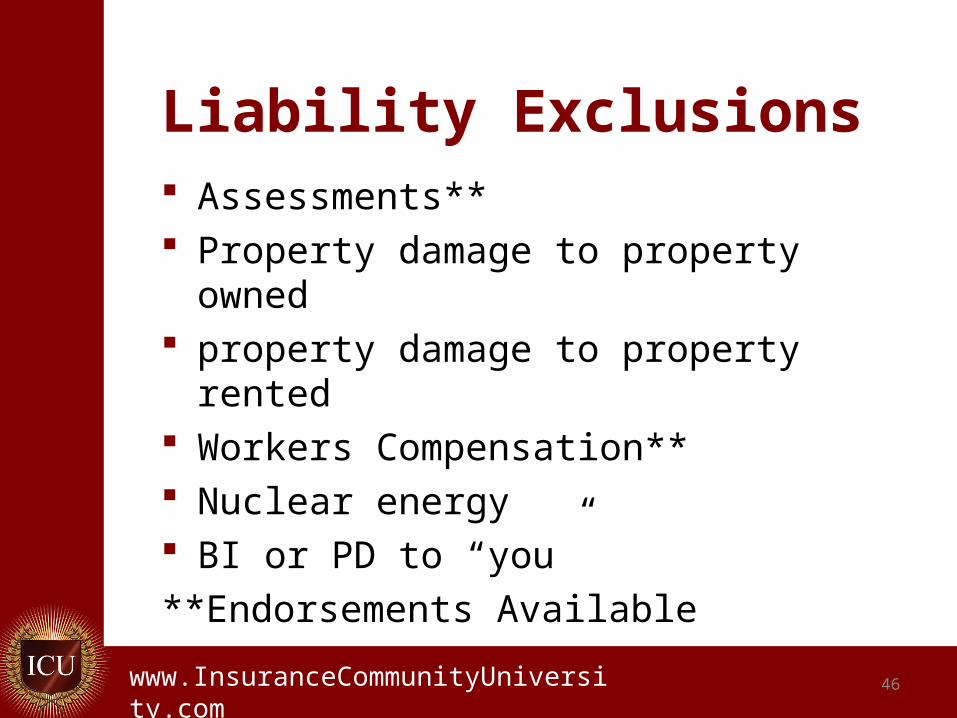

Assessments** Property damage to property owned property damage to property rented Workers Compensation** Nuclear energy BI or PD to “you”

**Endorsements Available

Liability Exclusions

.www.InsuranceCommunityUniversity.com 47

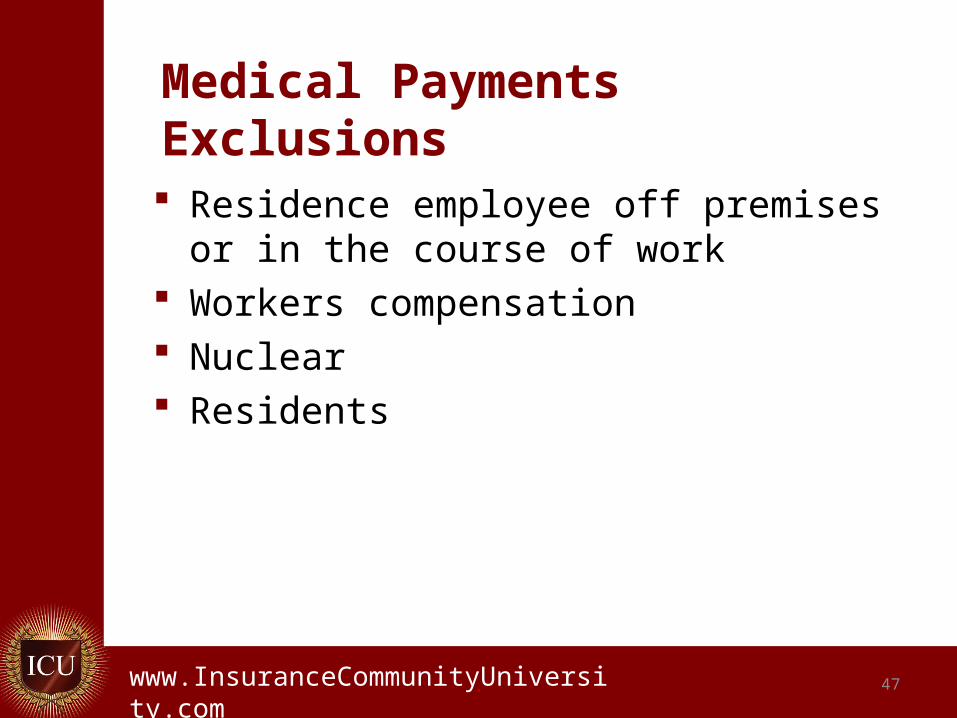

Medical Payments Exclusions

Residence employee off premises or in the course of work

Workers compensation Nuclear Residents

.www.InsuranceCommunityUniversity.com

Difference in Conditions (DIC)

and Wrap Around Insurance

48

.www.InsuranceCommunityUniversity.com

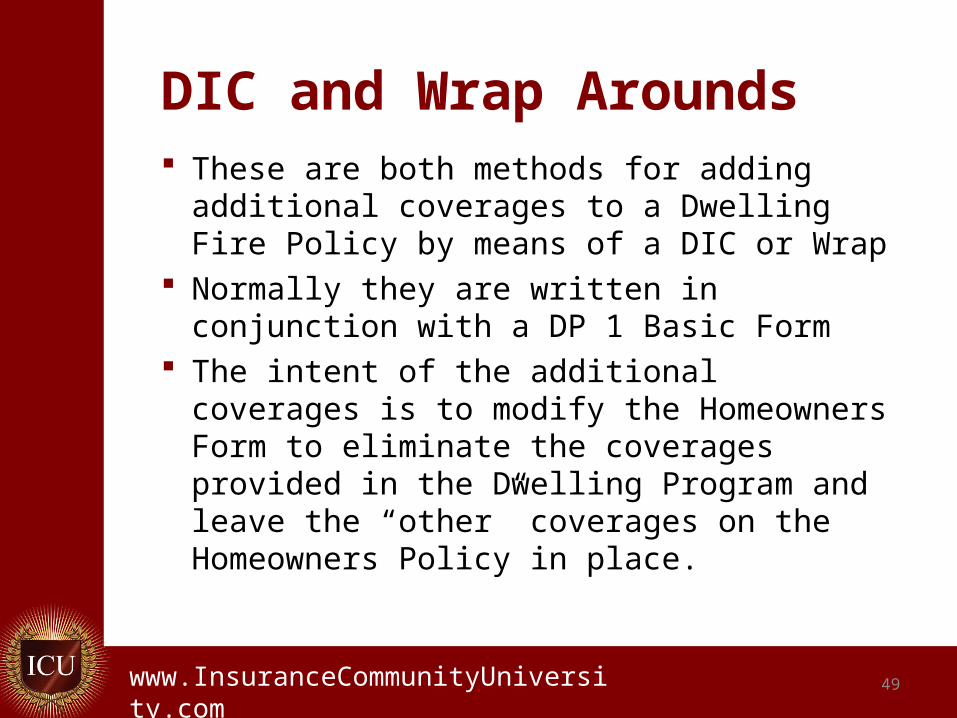

DIC and Wrap Arounds These are both methods for adding

additional coverages to a Dwelling Fire Policy by means of a DIC or Wrap

Normally they are written in conjunction with a DP 1 Basic Form

The intent of the additional coverages is to modify the Homeowners Form to eliminate the coverages provided in the Dwelling Program and leave the “other” coverages on the Homeowners Policy in place.

49

.www.InsuranceCommunityUniversity.com 50

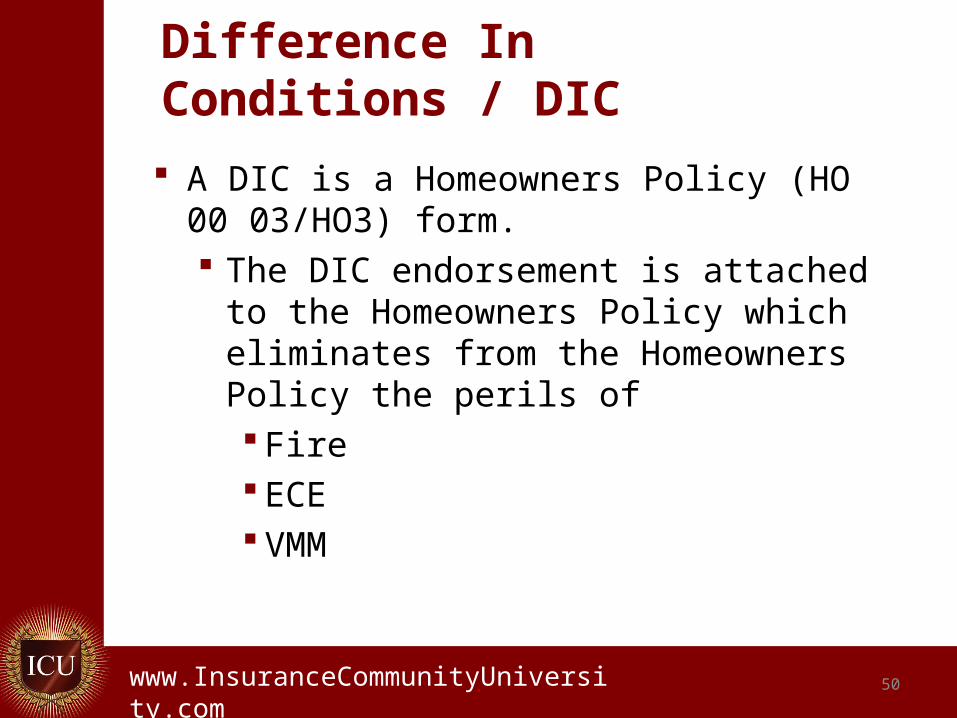

Difference In Conditions / DIC

A DIC is a Homeowners Policy (HO 00 03/HO3) form. The DIC endorsement is attached to the

Homeowners Policy which eliminates from the Homeowners Policy the perils of Fire ECE VMM

.www.InsuranceCommunityUniversity.com 51

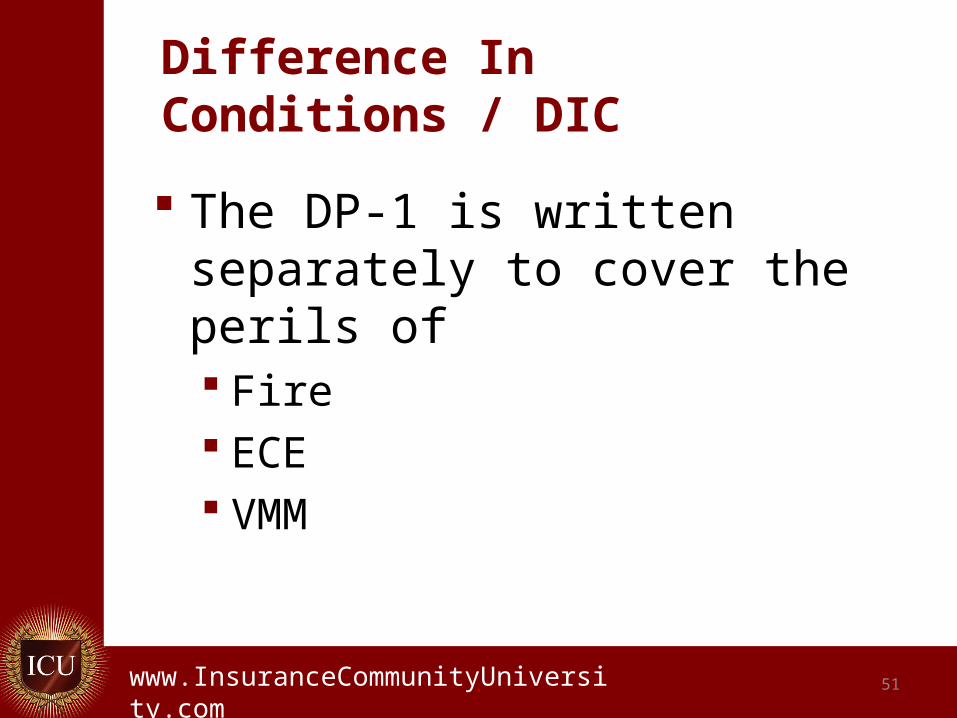

Difference In Conditions / DIC

The DP-1 is written separately to cover the perils of Fire ECE VMM

.www.InsuranceCommunityUniversity.com 52

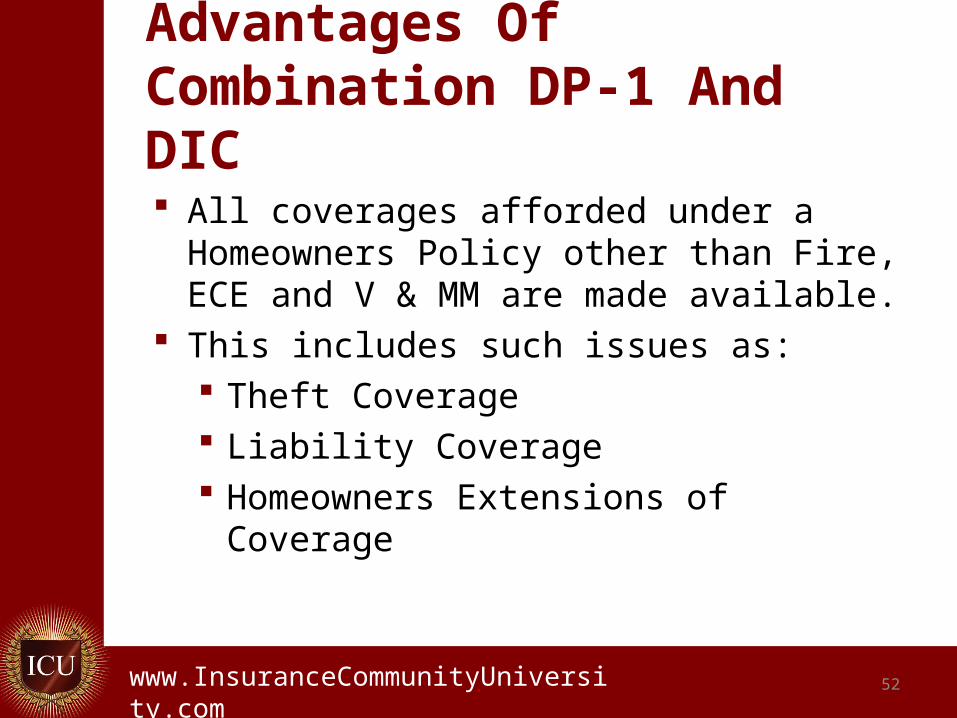

Advantages Of Combination DP-1 And DIC

All coverages afforded under a Homeowners Policy other than Fire, ECE and V & MM are made available.

This includes such issues as: Theft Coverage Liability Coverage Homeowners Extensions of Coverage

.www.InsuranceCommunityUniversity.com 53

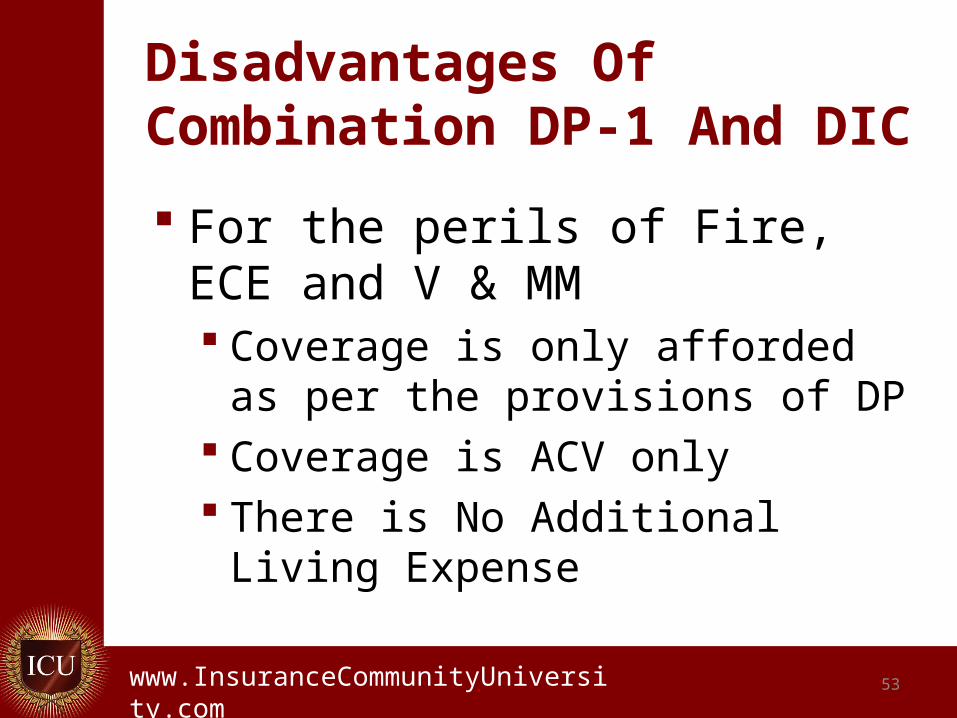

Disadvantages Of Combination DP-1 And DIC

For the perils of Fire, ECE and V & MM Coverage is only afforded as per

the provisions of DP Coverage is ACV only There is No Additional Living

Expense

.www.InsuranceCommunityUniversity.com 54

Wrap Around Policies

A Wrap Around is a Homeowners Policy (HO 00 03/HO3) form The Wrap Around endorsement is

attached to the Homeowners Policy which eliminates from the Homeowners Policy Fire, ECE & VMM

.www.InsuranceCommunityUniversity.com 55

Wrap Around Policies To the extent they are covered on the DP

form. The Wrap pays excess over the DP coverages

The DP 00 01/DP1 is written to cover the perils of Fire ECE VMM

.www.InsuranceCommunityUniversity.com 56

Wrap Around Policies The difference between the DIC and Wrap

is that the Wrap eliminates the perils of the DP 1 only to the extent they are covered under that form

.www.InsuranceCommunityUniversity.com 57

Wrap Around Policies The Wrap is therefore EXCESS Fire, ECE,

and V & MM Provides potential for higher limits DP 1 is ACV only so the Wrap picks up the

difference between ACV and Replacement Cost Wrap Around provides first dollar Additional Living

Expense in that it is not a coverage provided on a DP 1. The Additional Living Expense on the Wrap would apply even to the Fire, ECE & V& MM loss

.www.InsuranceCommunityUniversity.com

Homeowners Insurance

58

.www.InsuranceCommunityUniversity.com

Homeowners

Homeowners Policies are the premier policy for the owner of a home who occupies it as their residence.

It is a package policy of Property and Liability and includes a lot of enhanced coverages and numerous endorsements.

Every company has their own eligibility and their own form and endorsements

ISO provides a guideline for homeowners coverages

59

.www.InsuranceCommunityUniversity.com 60

What Types of Properties Are Insured On A Homeowner’s Policy

A Single Family Dwelling A Multiple Family Dwelling (1-2 units) A Townhouse Unit

.www.InsuranceCommunityUniversity.com 61

Townhouse

Similar to an individual home Two or more units Sharing of a common wall with individual

ownership up to the middle There is joint ownership of common

property and a property owners association

.www.InsuranceCommunityUniversity.com 62

Townhouse

The owner owns the land beneath the home and the air above.

All improvements to their land i.e., the dwelling portion to the undivided shared wall and an undivided interest in common areas. Pool, recreation areas, landscaping,

etc. Homeowners Policy HO3

.www.InsuranceCommunityUniversity.com

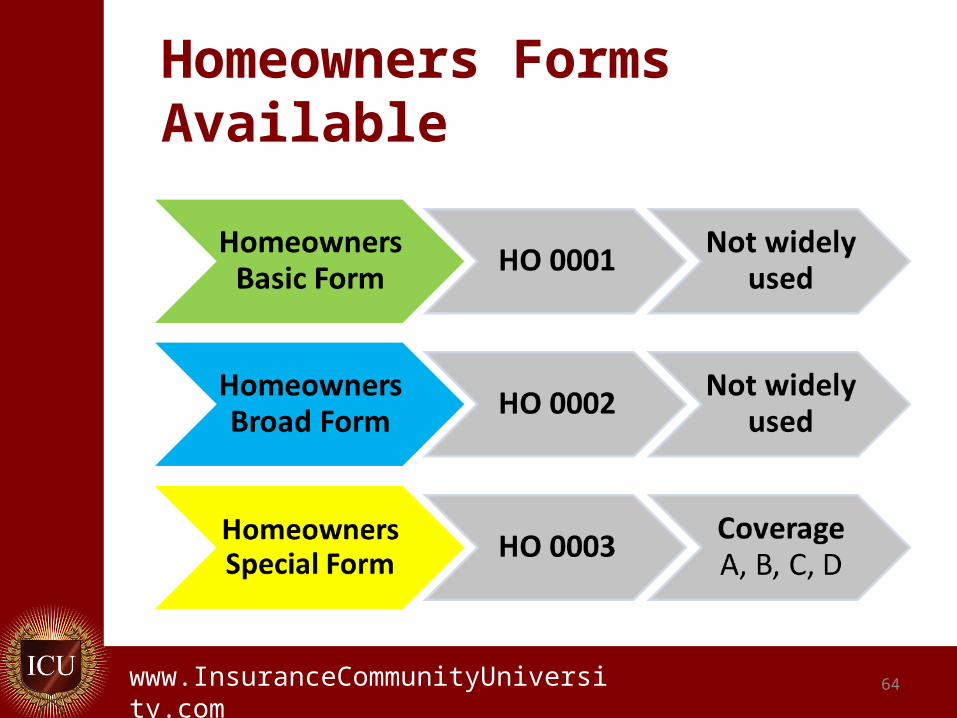

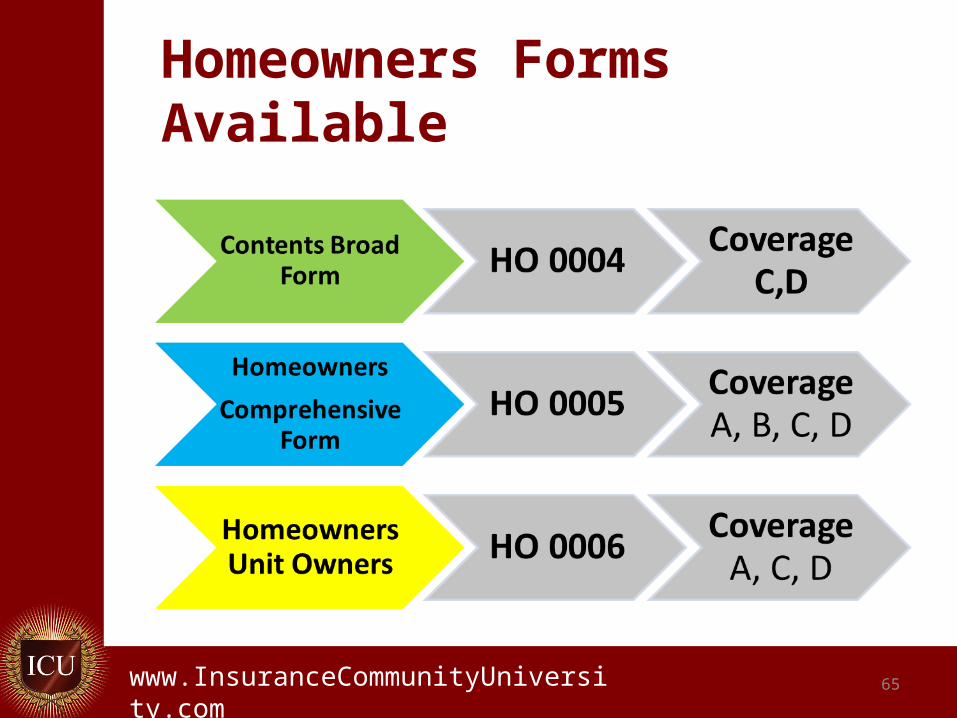

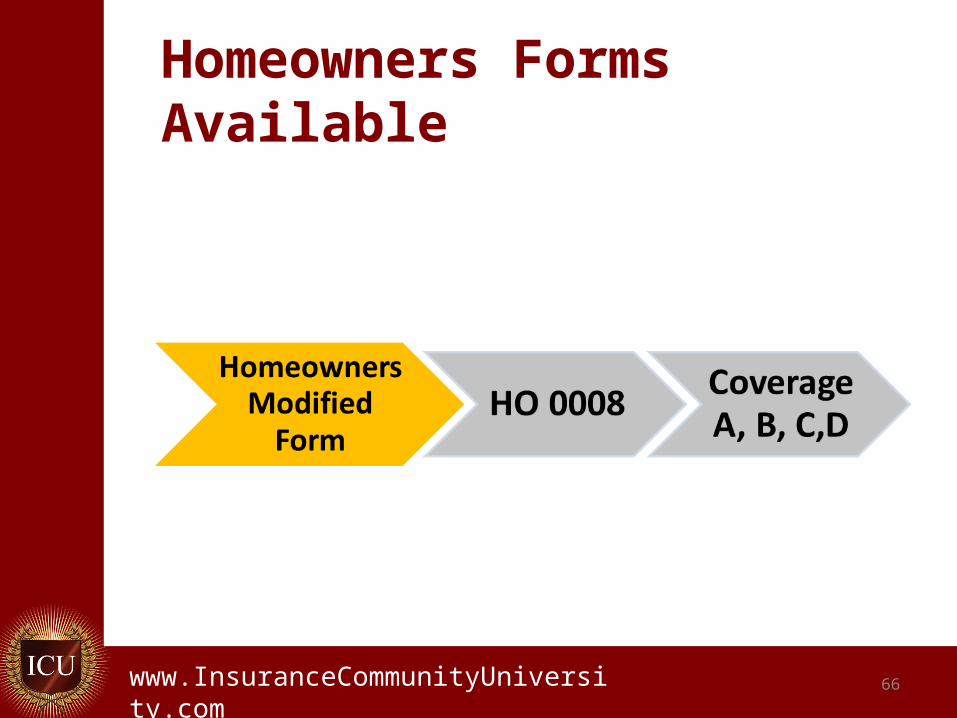

Homeowners Forms Available There are several “homeowners” forms

available. However, not all of the forms listed are

written in all states Specifically the HO 0001, HO 0002, HO

0005, and HO 0008 are written in limited states.

63

.www.InsuranceCommunityUniversity.com

Homeowners Forms Available

64

.www.InsuranceCommunityUniversity.com

Homeowners Forms Available

65

.www.InsuranceCommunityUniversity.com

Homeowners Forms Available

66

.www.InsuranceCommunityUniversity.com 67

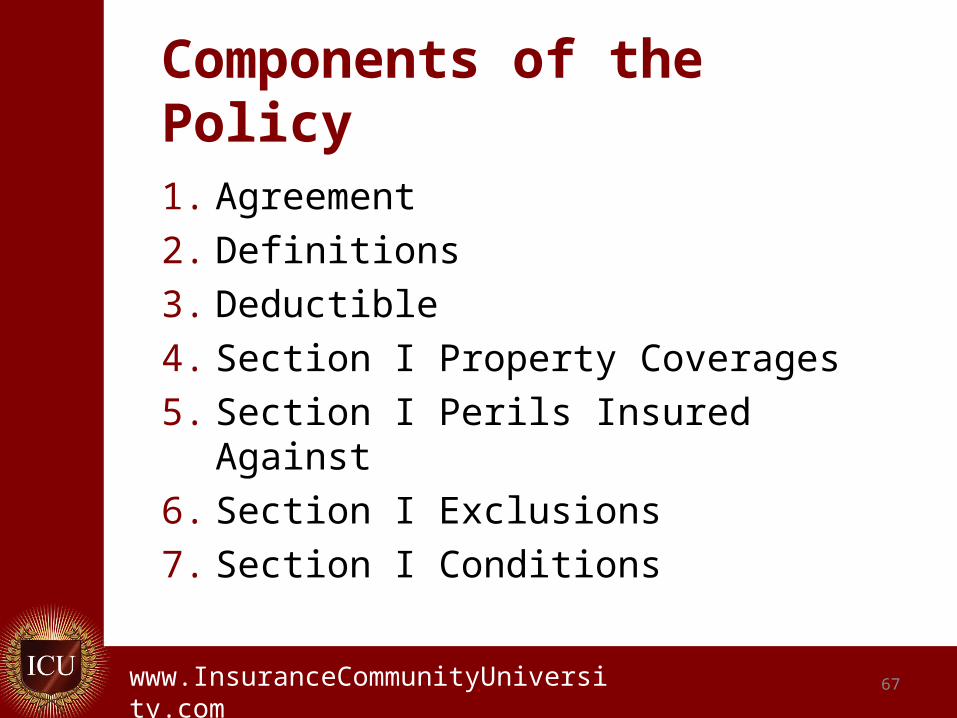

Components of the Policy

1. Agreement

2. Definitions

3. Deductible

4. Section I Property Coverages

5. Section I Perils Insured Against

6. Section I Exclusions

7. Section I Conditions

.www.InsuranceCommunityUniversity.com 68

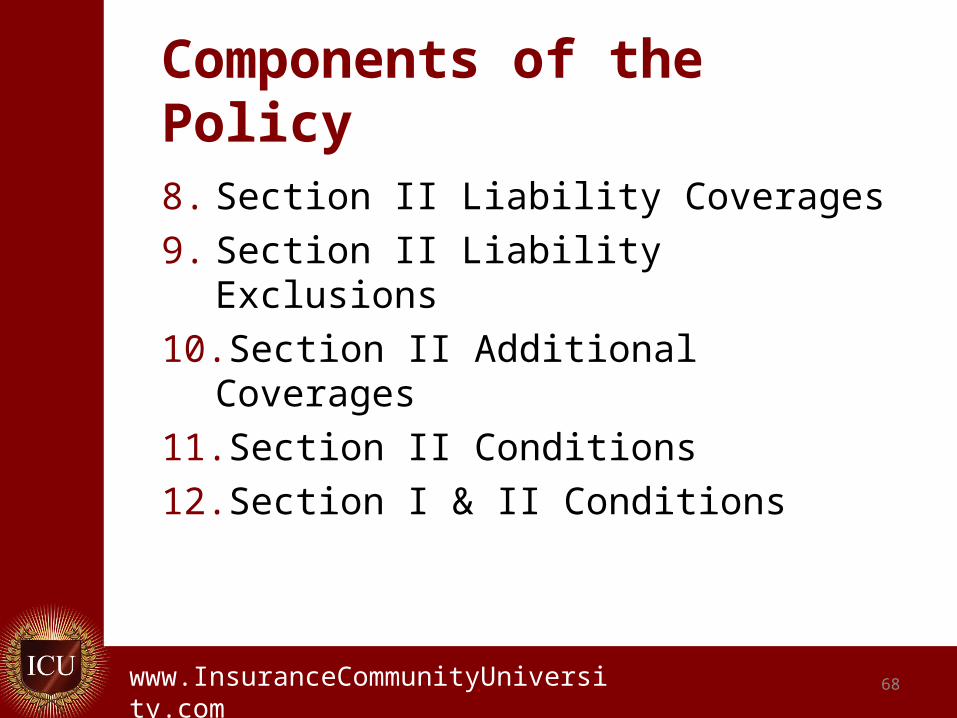

Components of the Policy

8. Section II Liability Coverages

9. Section II Liability Exclusions

10.Section II Additional Coverages

11.Section II Conditions

12.Section I & II Conditions

.www.InsuranceCommunityUniversity.com 69

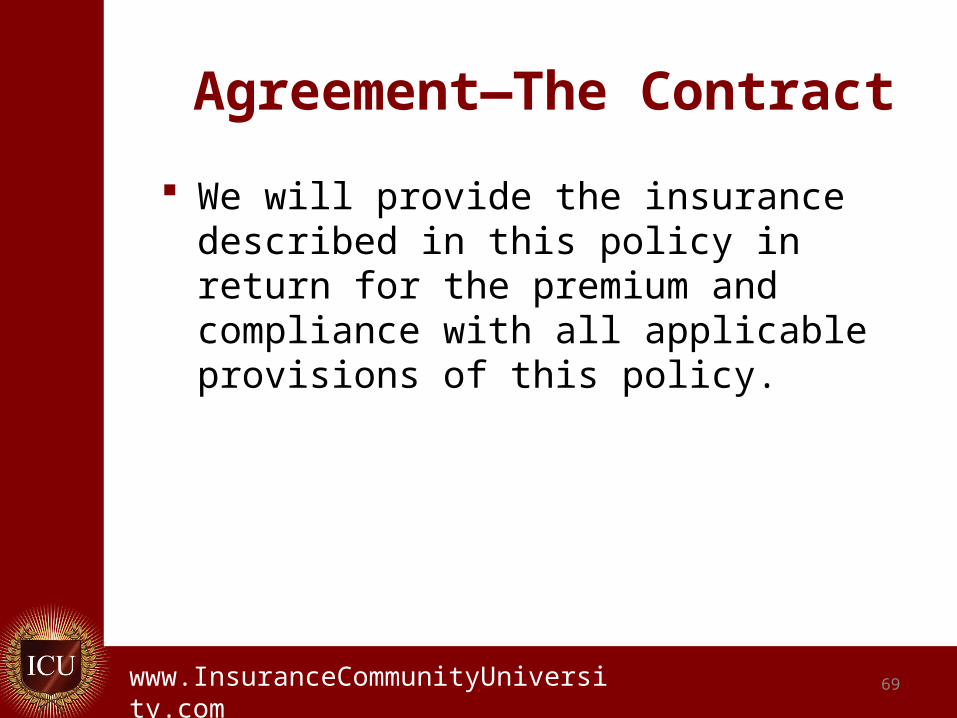

Agreement—The Contract

We will provide the insurance described in this policy in return for the premium and compliance with all applicable provisions of this policy.

.www.InsuranceCommunityUniversity.com 70

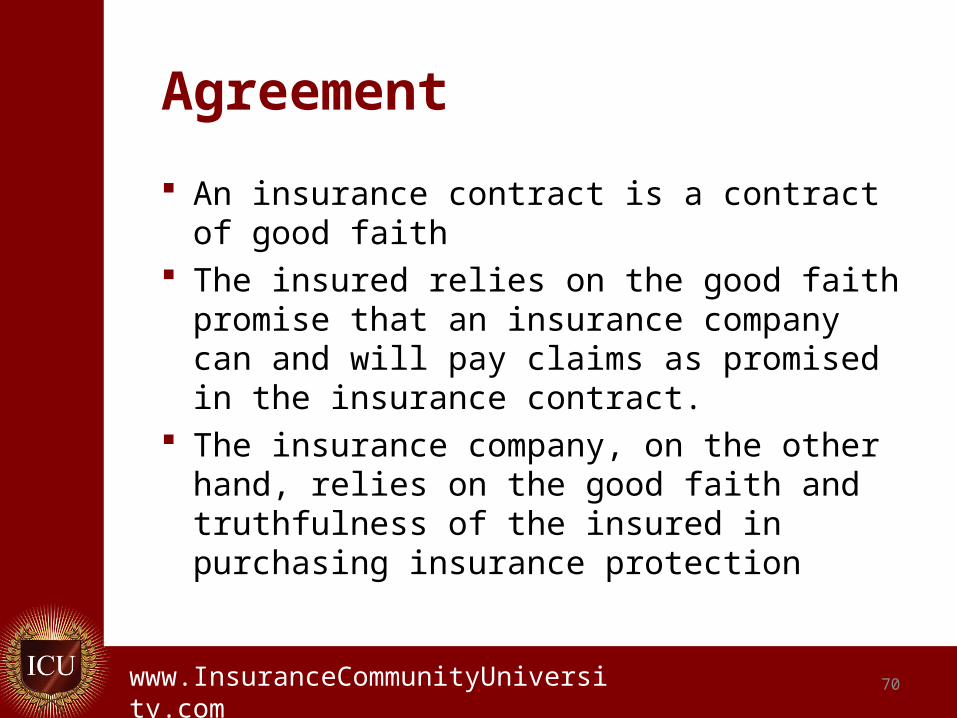

Agreement

An insurance contract is a contract of good faith

The insured relies on the good faith promise that an insurance company can and will pay claims as promised in the insurance contract.

The insurance company, on the other hand, relies on the good faith and truthfulness of the insured in purchasing insurance protection

.www.InsuranceCommunityUniversity.com

Definitions

In the Homeowners Forms whenever a word is defined it is in parentheses in the policy language.

Definitions are key to understanding the intent of the coverage and to determine whether coverage applies and if endorsements are required.

71

.www.InsuranceCommunityUniversity.com 72

“You,” “We,” “Us,” “Our”

In this policy, "you" and "your" refer to the "named insured" shown in the Declarations and the spouse if a resident of the same household. "We," "us," and "our" refer to the Company providing this insurance. Lead-in language to the DEFINITIONS

.www.InsuranceCommunityUniversity.com 73

“You,” “We,” “Us,” “Our”

In this policy, "you" and "your" refer to the "named insured" shown in the Declarations and the spouse if a resident of the same household.

Note: Some carriers will write coverage for domestic partners.

Note: There is a problem when a spouse is not named in the policy as a Named Insured if they are not residing with the spouse named on the policy.

.www.InsuranceCommunityUniversity.com 74

“You”, “We”, “Us”, “Our”

Solution: Name the spouse as a Named Insured. Add the spouse as an Additional

Insured using HO 04 41. Trusts should be listed along with the

individuals making up the trusts

.www.InsuranceCommunityUniversity.com

Definitions (“Aircraft….)

1. Aircraft Liability, Hovercraft Liability, Motor Vehicle Liability and Watercraft Liability All definitions are put into the contract

to define what is NOT covered on a Homeowners Policy

75

.www.InsuranceCommunityUniversity.com 76

Definitions “Bodily Injury”

Bodily injury" means bodily harm, sickness or disease, including required care, loss of services and death that results.

.www.InsuranceCommunityUniversity.com 77

Definitions “Bodily Injury”

Problem: Coverage is limited to only the defined term of

“Bodily Injury”.` An insured who, in addition to the residence

premises on the HO 00 03 has a rental property that liability coverage has been extended to include, in the event of invasion of privacy, wrongful eviction, etc., has coverage gap exists.

An insured who is operating a business as a sole proprietor, employee, or partnership in the event of libel, slander, has a coverage gap.

.www.InsuranceCommunityUniversity.com 78

Definition “Business”

Prior to the Homeowners 2000 form the definition of “business” was: "Business" includes trade, profession or

occupation. The definition was vague and open to

interpretation.

.www.InsuranceCommunityUniversity.com 79

Definition “Business”

Most courts who have examined the issue of defining “business” and “business pursuits” agree that two criteria must be satisfied for a business to exist:

(a) Expectation of gain

(b) At least some degree of continuity

.www.InsuranceCommunityUniversity.com 80

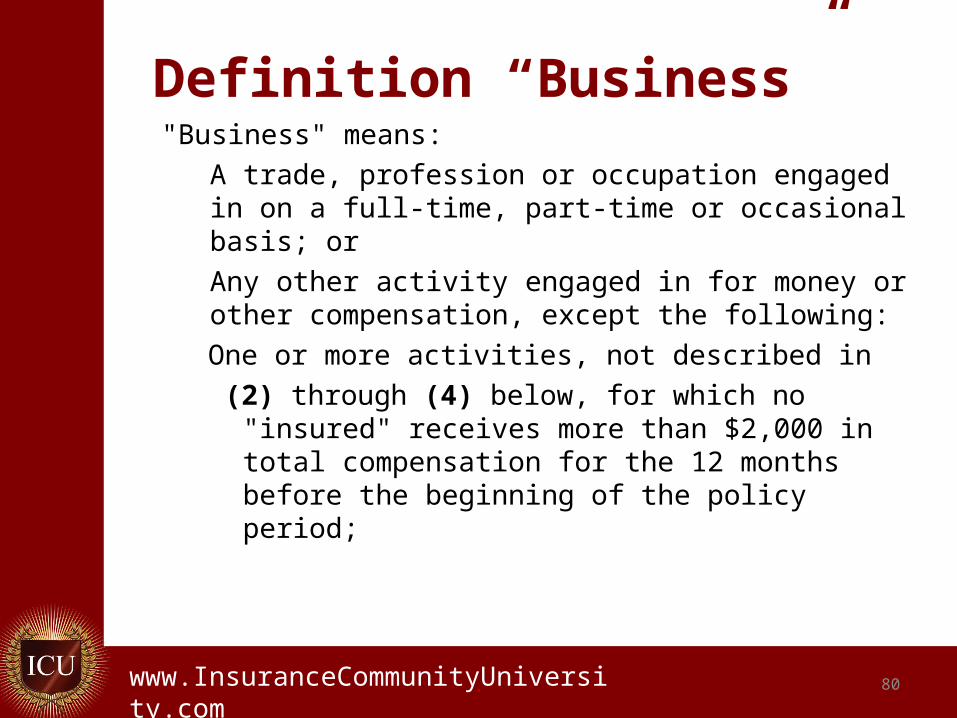

Definition “Business”"Business" means:

A trade, profession or occupation engaged in on a full-time, part-time or occasional basis; or

Any other activity engaged in for money or other compensation, except the following:

One or more activities, not described in

(2) through (4) below, for which no "insured" receives more than $2,000 in total compensation for the 12 months before the beginning of the policy period;

.www.InsuranceCommunityUniversity.com 81

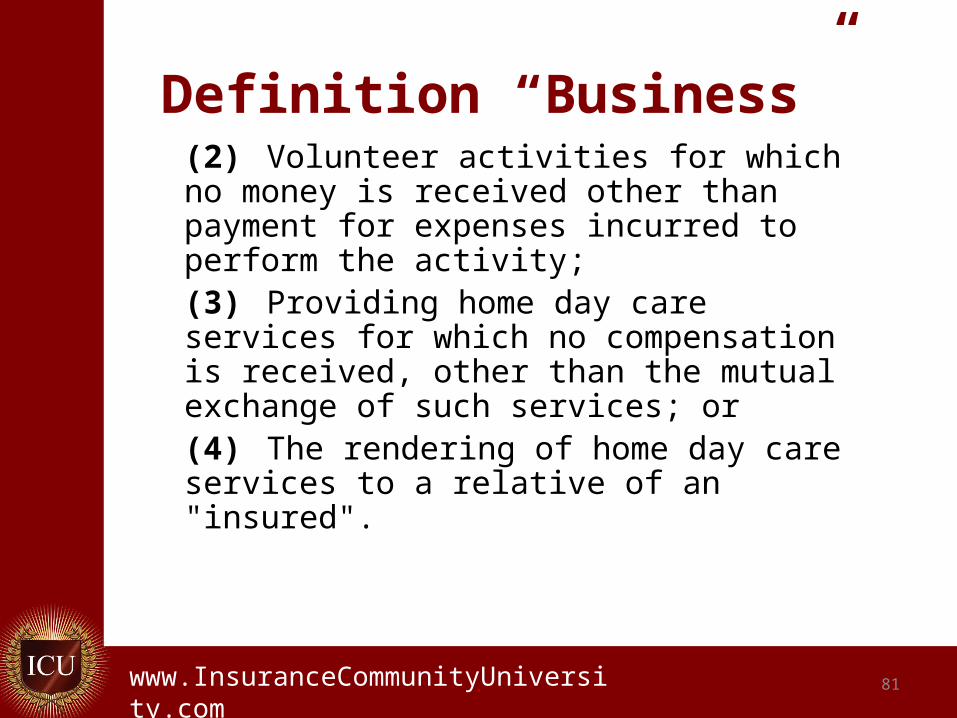

Definition “Business”(2) Volunteer activities for which no money is received other than payment for expenses incurred to perform the activity;(3) Providing home day care services for which no compensation is received, other than the mutual exchange of such services; or(4) The rendering of home day care services to a relative of an "insured".

.www.InsuranceCommunityUniversity.com 82

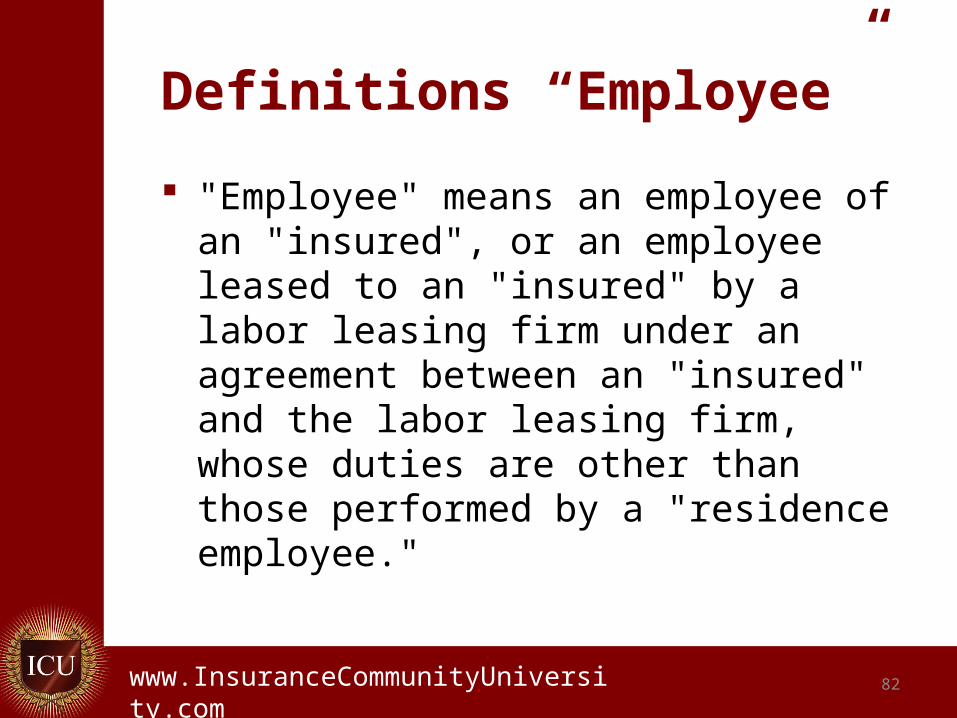

Definitions “Employee”

"Employee" means an employee of an "insured", or an employee leased to an "insured" by a labor leasing firm under an agreement between an "insured" and the labor leasing firm, whose duties are other than those performed by a "residence employee."

.www.InsuranceCommunityUniversity.com 83

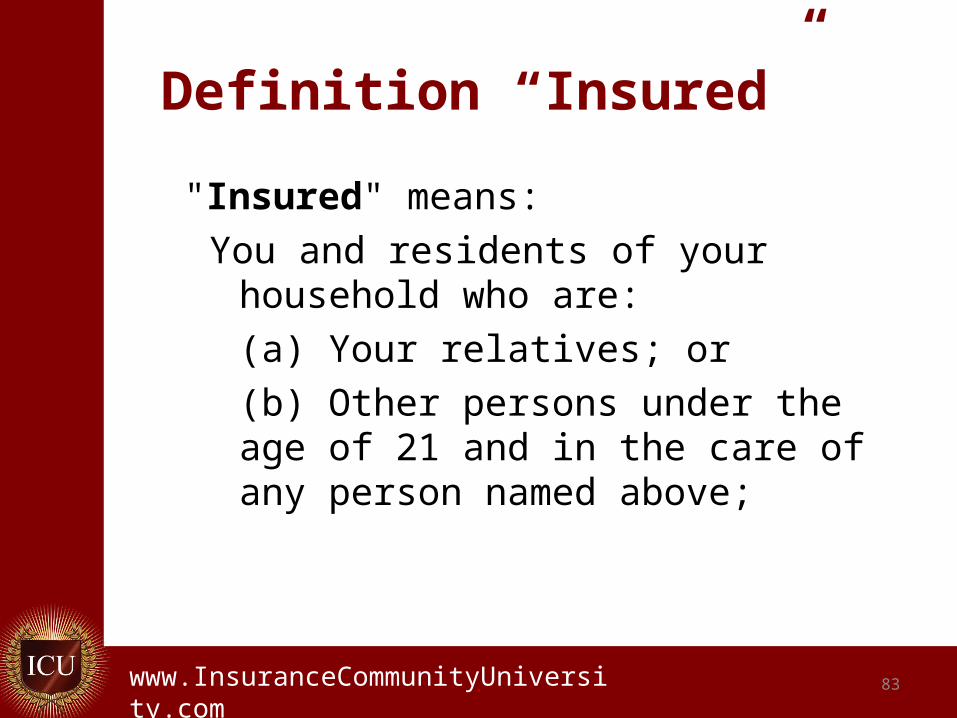

Definition “Insured”

"Insured" means:

You and residents of your household who are:

(a) Your relatives; or

(b) Other persons under the age of 21 and in the care of any person named above;

.www.InsuranceCommunityUniversity.com 84

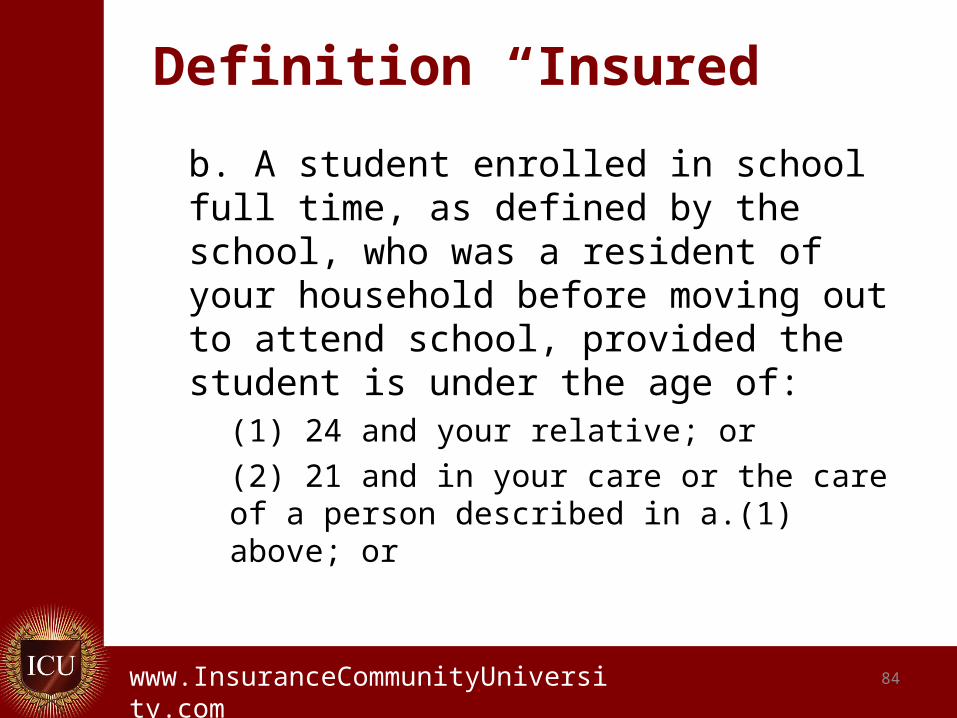

Definition “Insured”

b. A student enrolled in school full time, as defined by the school, who was a resident of your household before moving out to attend school, provided the student is under the age of:

(1) 24 and your relative; or

(2) 21 and in your care or the care of a person described in a.(1) above; or

.www.InsuranceCommunityUniversity.com 85

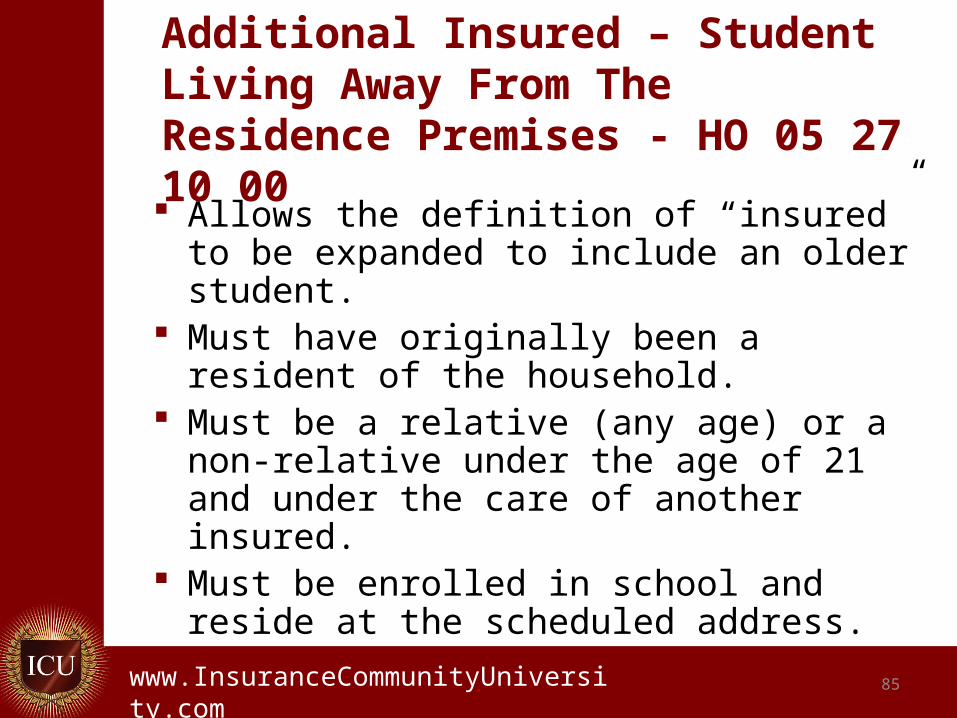

Additional Insured – Student Living Away From The Residence Premises - HO 05 27 10 00 Allows the definition of “insured” to be

expanded to include an older student. Must have originally been a resident of the

household. Must be a relative (any age) or a non-

relative under the age of 21 and under the care of another insured.

Must be enrolled in school and reside at the scheduled address.

.www.InsuranceCommunityUniversity.com 86

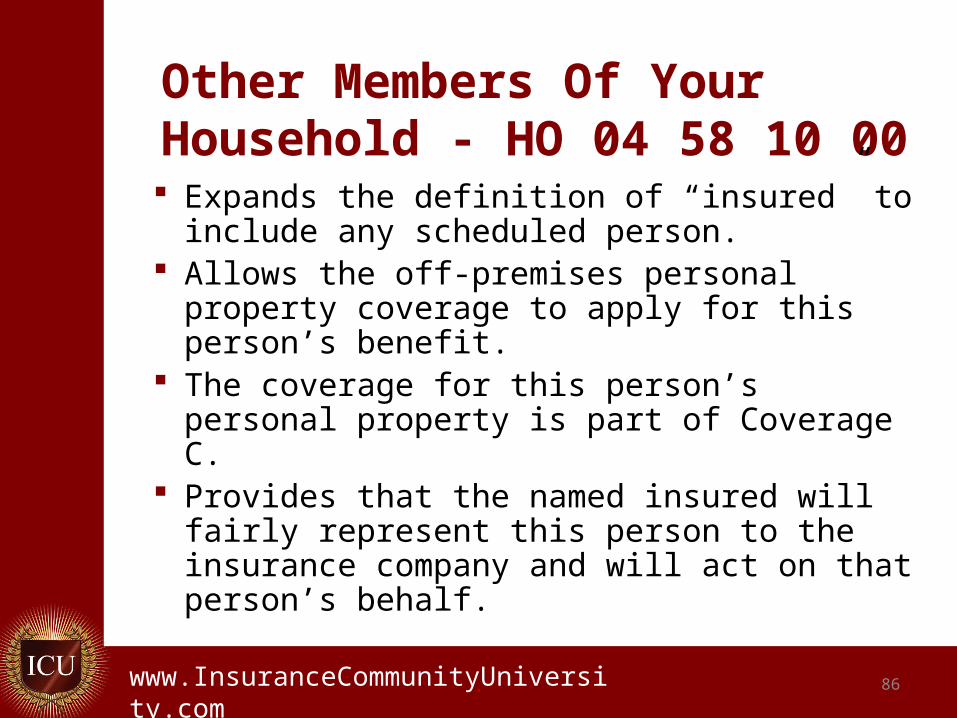

Other Members Of Your Household - HO 04 58 10 00 Expands the definition of “insured” to

include any scheduled person. Allows the off-premises personal property

coverage to apply for this person’s benefit. The coverage for this person’s personal

property is part of Coverage C. Provides that the named insured will fairly

represent this person to the insurance company and will act on that person’s behalf.

.www.InsuranceCommunityUniversity.com 87

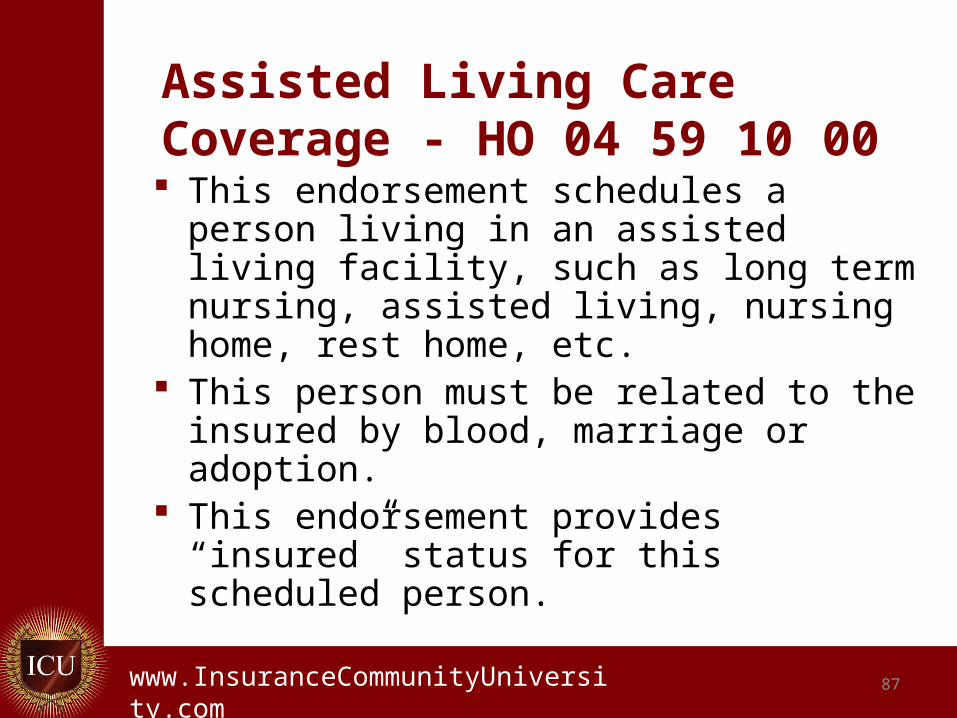

Assisted Living Care Coverage - HO 04 59 10 00 This endorsement schedules a person

living in an assisted living facility, such as long term nursing, assisted living, nursing home, rest home, etc.

This person must be related to the insured by blood, marriage or adoption.

This endorsement provides “insured” status for this scheduled person.

.www.InsuranceCommunityUniversity.com 88

Residence Held In Trust – HO 05 43 10 00 Expands the definition of insured to include

a “trustee”, who is not named in the Declarations page.

Includes specific members of their family.

.www.InsuranceCommunityUniversity.com 89

Other “Insured” considerations

It is very common for a home owner to have a loan on their home or other types of property.

The Lenders Loss Payable Endorsement 438 BFU NS (05 42) is attached to the policy to provide “non-derivative” protection for the lender.

Additionally the lender is named on the declaration page.

.www.InsuranceCommunityUniversity.com

Additional Interests Residence Premises In addition to the Mortgagee this

endorsement allows for other persons or organizations who have an interest in the “residence premises” to be listed on the policy. The form does provide cancellation and non renewal notification to the parties so indicated.

90

.www.InsuranceCommunityUniversity.com 91

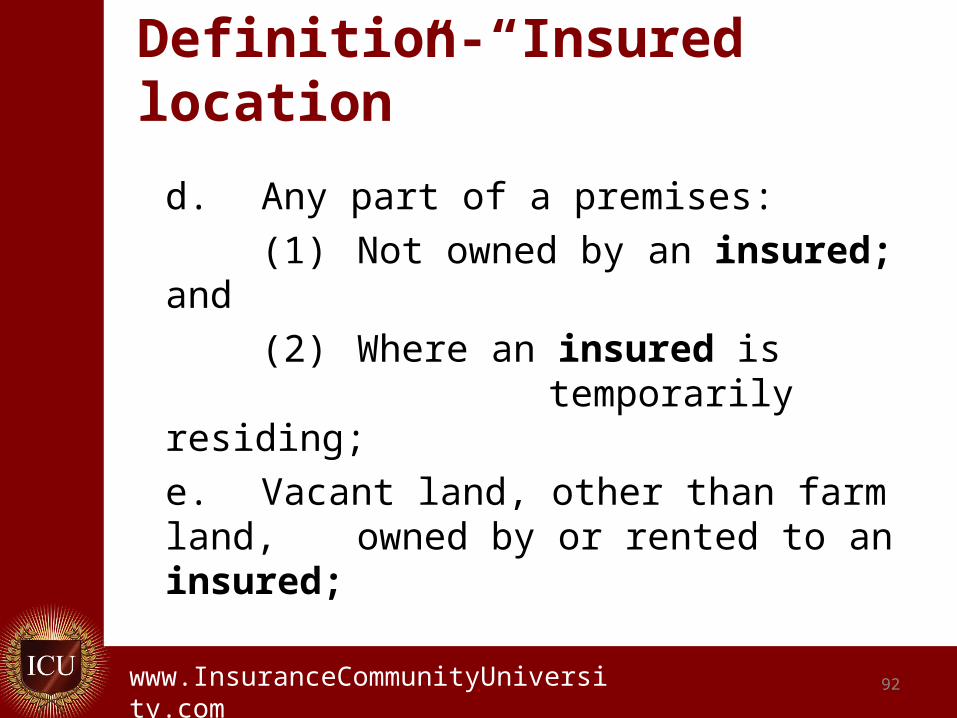

Definition-“Insured location”

“Insured location” means:

a. The residence premises;

b. The part of other premises, other structures and grounds used by you as a residence;

and(1)Which is shown in the Declarations; or

(2)Which is acquired by you during the policy period for your use as a residence;

c. Any premises used by you in connection with a premises described in 4.a. and 4.b. above;

.www.InsuranceCommunityUniversity.com 92

Definition-“Insured location”

d. Any part of a premises:

(1) Not owned by an insured; and

(2) Where an insured is temporarily residing;

e. Vacant land, other than farm land, owned by or rented to an insured;

.www.InsuranceCommunityUniversity.com 93

Definition-“Insured location””

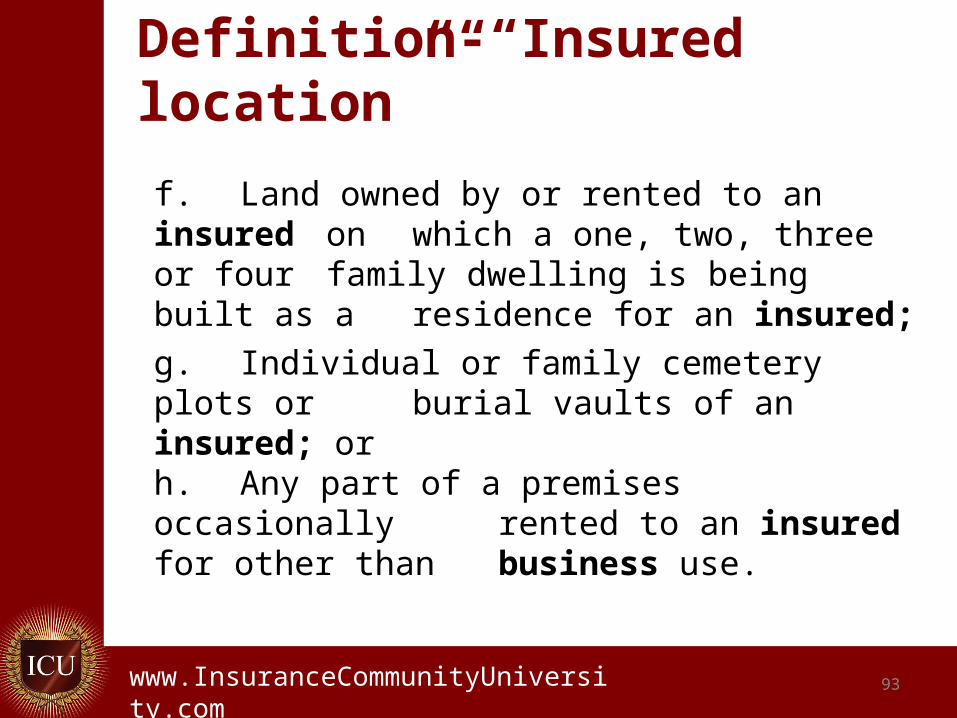

f. Land owned by or rented to an insured on which a one, two, three or four family dwelling is being built as a

residence for an insured;

g. Individual or family cemetery plots or burial vaults of an insured; or

h. Any part of a premises occasionally rented to an insured for other than business use.

.www.InsuranceCommunityUniversity.com 94

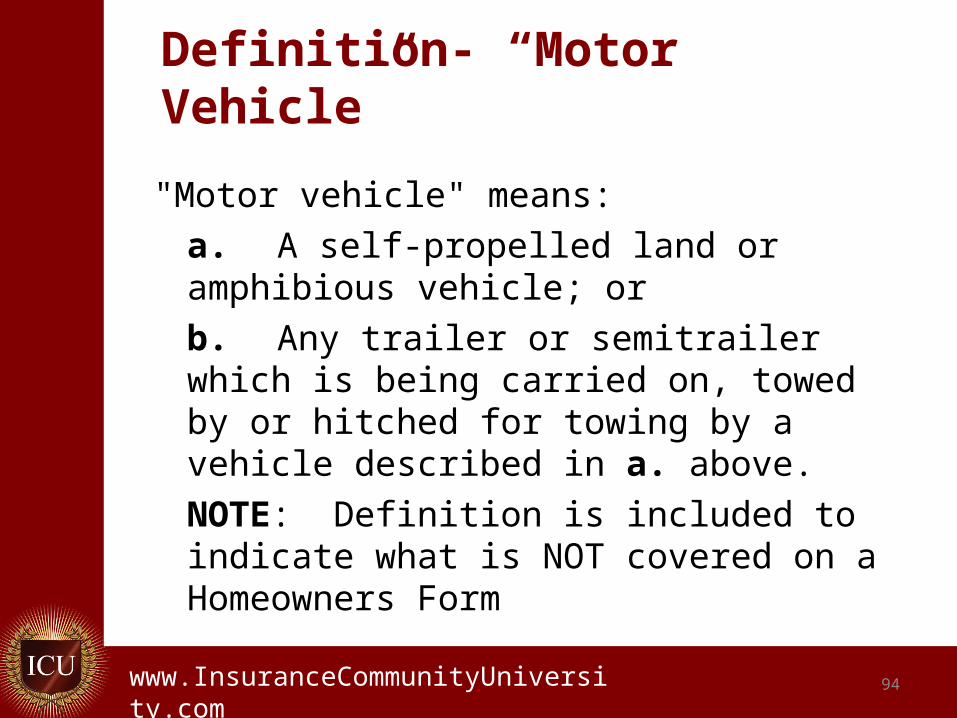

Definition- “Motor Vehicle”

"Motor vehicle" means:

a. A self-propelled land or amphibious vehicle; or

b. Any trailer or semitrailer which is being carried on, towed by or hitched for towing by a vehicle described in a. above.

NOTE: Definition is included to indicate what is NOT covered on a Homeowners Form

.www.InsuranceCommunityUniversity.com 95

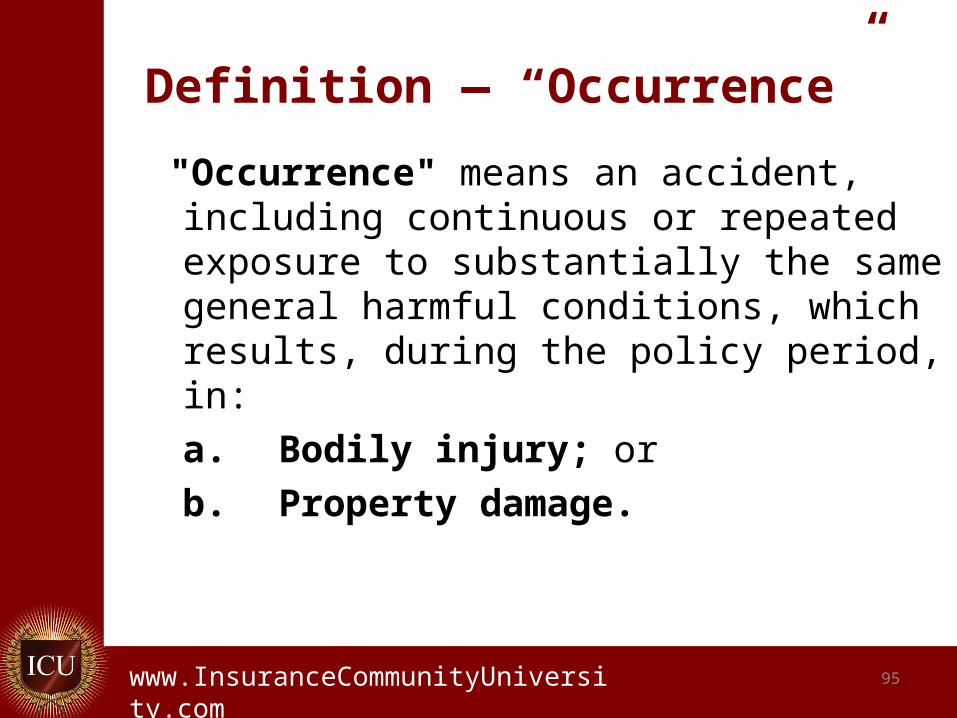

Definition — “Occurrence”

"Occurrence" means an accident, including continuous or repeated exposure to substantially the same general harmful conditions, which results, during the policy period, in:

a. Bodily injury; or

b. Property damage.

.www.InsuranceCommunityUniversity.com 96

Definition— “Property Damage”

"Property damage" means physical injury to, destruction of, or loss of use of tangible property.

.www.InsuranceCommunityUniversity.com

Definition “Residence Employee”

An employee of an “insured” or an employee leased to an "insured” by a labor leasing firm, under an agreement between an “insured” and the labor leasing firm; whose duties are related to the maintenance or use of the “residence premises” including household or domestic services; or

97

.www.InsuranceCommunityUniversity.com

Definition “Residence Employee”

One who performs similar duties elsewhere not related to the “business” of an “insured”.

A “residence employee” does not include a temporary employee who is furnished to an “insured” to substitute for a permanent “residence employee” on leave or to meet seasonal or short tem workload conditions.

98

.www.InsuranceCommunityUniversity.com 99

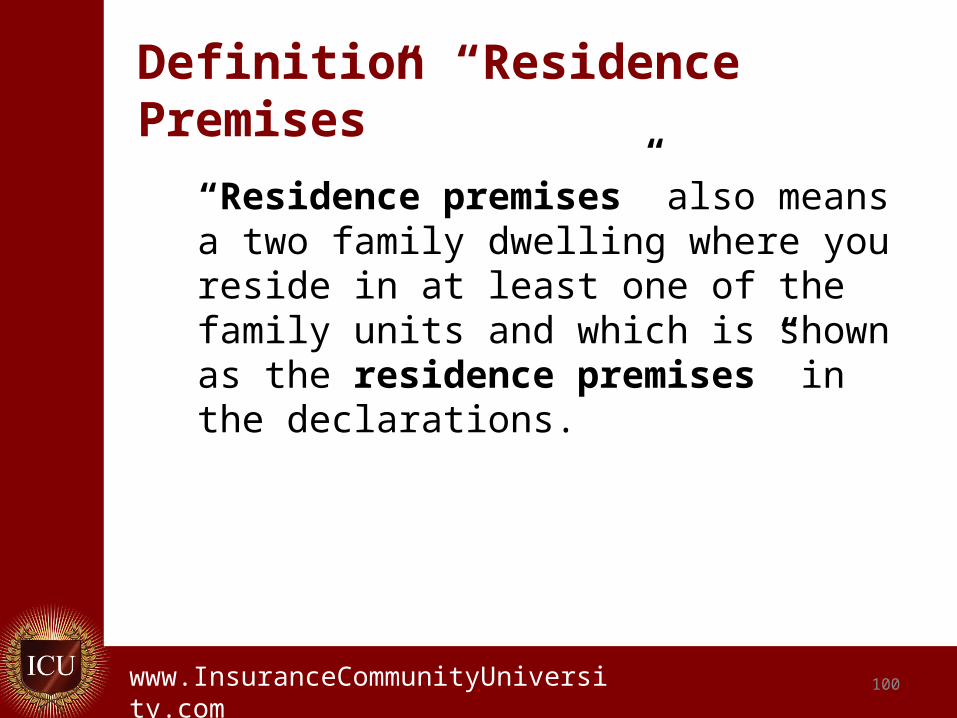

Definition “Residence Premises”

8. "Residence premises" means: a. The one family dwelling, other structures, and grounds; or; b. That part of any other building;where you reside and which is shown as the “residence premises” in the Declarations.

.www.InsuranceCommunityUniversity.com 100

Definition “Residence Premises”

“Residence premises” also means a two family dwelling where you reside in at least one of the family units and which is shown as the residence premises” in the declarations.

.www.InsuranceCommunityUniversity.com

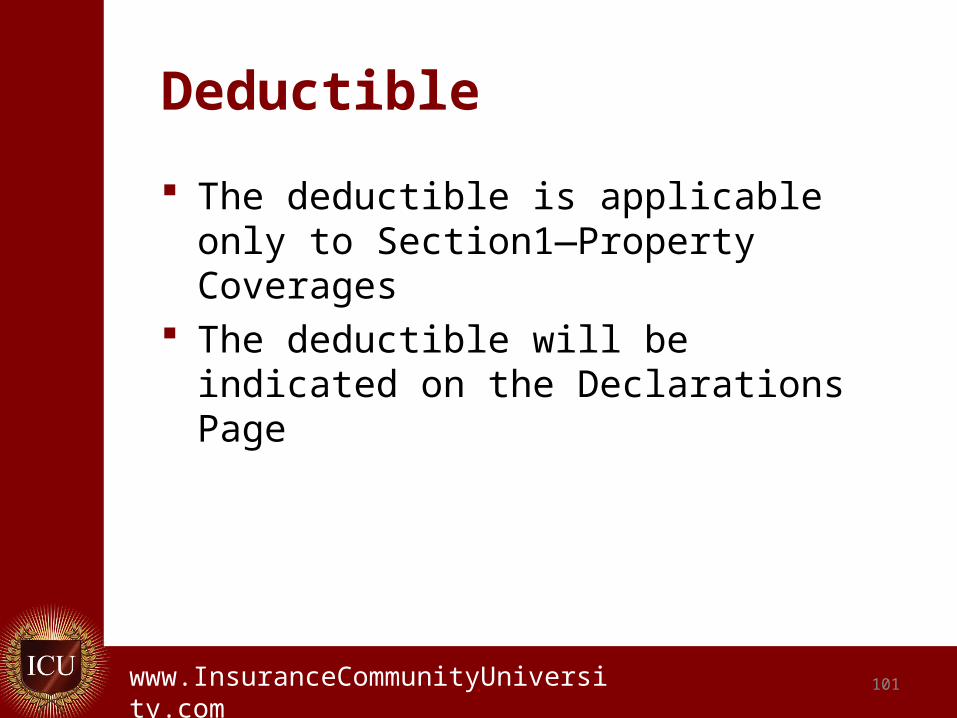

Deductible

The deductible is applicable only to Section1—Property Coverages

The deductible will be indicated on the Declarations Page

101

.www.InsuranceCommunityUniversity.com

Coverages Provided Homeowners HO 0003

102

.www.InsuranceCommunityUniversity.com

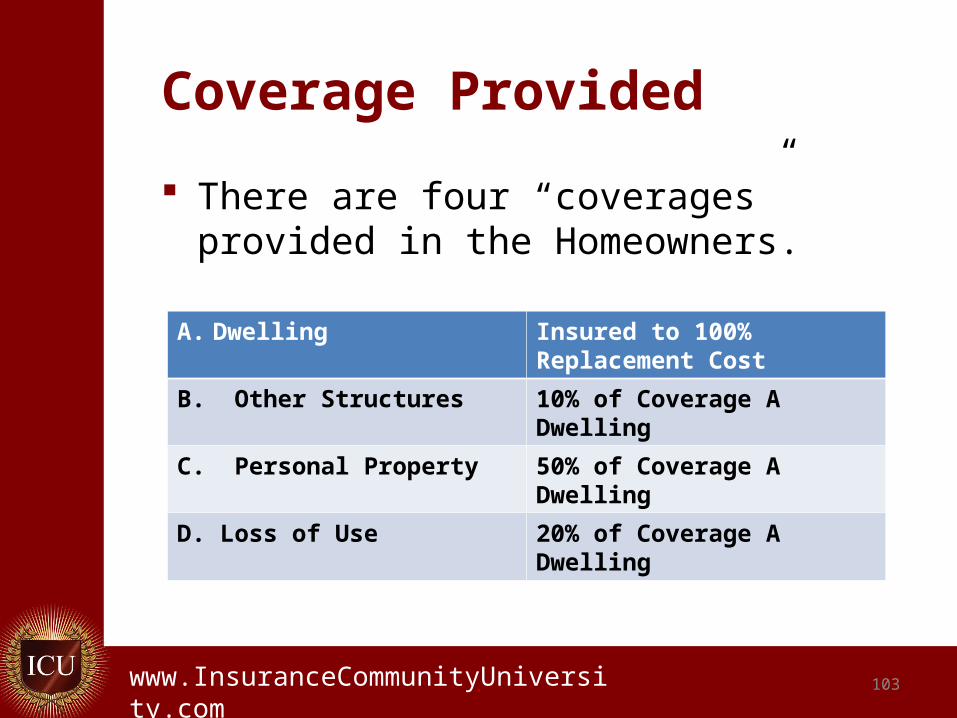

Coverage Provided

There are four “coverages” provided in the Homeowners.

103

A. Dwelling Insured to 100% Replacement Cost

B. Other Structures 10% of Coverage A Dwelling

C. Personal Property 50% of Coverage A Dwelling

D. Loss of Use 20% of Coverage A Dwelling

.www.InsuranceCommunityUniversity.com 104

Additional Limits Of Liability For Coverages A, B, C, And D - HO 04 11 10 00 Used to increase the dwelling limit of

coverage to apply when the loss exceeds the limit shown on the Declarations page.

Specifies that the same policy percentages for Coverages B, C and D apply.

.www.InsuranceCommunityUniversity.com

Section 1 Property Coverage

Coverage A Dwelling Coverage

105

.www.InsuranceCommunityUniversity.com

Dwelling

The dwelling must be used for dwelling purposes to qualify for a Homeowners Policy

It must be occupied for qualification Typically the forms will state will limit recovery if

the building has been vacant for 60 consecutive days for Vandalism and Malicious Mischief and exclude theft to a home under construction

Some forms exclude all coverage if the building has been vacant 60 days.

106

.www.InsuranceCommunityUniversity.com 107

Section I - Property

Property Coverages Explains the categories of property

covered, special limits, excluded property, and additional coverages

Perils Insured Against Describes the perils covered for direct

loss to covered property

.www.InsuranceCommunityUniversity.com 108

Section I - Property

Exclusions Lists the perils that are uniformly

excluded for all covered property Conditions

Establishes the insurer’s and policyholder’s responsibilities, and defines how losses will be settled

.www.InsuranceCommunityUniversity.com 109

Coverage A - Dwelling

The dwelling must be insured for 100% of the replacement cost.

The dwelling amount is used to determine the coverages under B, C, and D as they are percentages of Coverage A

.www.InsuranceCommunityUniversity.com

Extended Replacement Cost (ERC)

Many homeowners carriers are including Extended Replacement Cost for Coverage “A” on the policies.

The ERC can be expressed as a percentage such as 125% or 150% of the coverage “A” limit.

Or the ERC can be expressed in an additional amount of insurance on the Declarations Page

110

.www.InsuranceCommunityUniversity.com 111

Inflation Guard

H0 243 (04-84)-Inflation Guard Endorsement Allows coverages A, B, C, D to be increased

annually by a stated percentage.

.www.InsuranceCommunityUniversity.com 112

Coverage A - Dwelling

Dwelling provides coverage on the dwelling structure located on the residence premises including structures attached to the dwelling for the amount indicated on the declarations page

.www.InsuranceCommunityUniversity.com 113

Coverage A - Dwelling

Under Coverage “Dwelling:” materials and supplies located on or next to the residence premises used to construct, alter, or repair the dwelling or other structure on the residence premises.

Land is not covered.

.www.InsuranceCommunityUniversity.com 114

Coverage A - Dwelling

Problem: Definition of construction. There is no coverage for “theft in or to a

dwelling under construction, or of materials and supplies for use in the construction until the dwelling is finished and occupied.

.www.InsuranceCommunityUniversity.com 115

Coverage A - Dwelling

Coverage “A “is generally provided on a replacement cost basis. The limit for coverage a must be at least 80%

of the current replacement cost of the dwelling in order for losses to be settled at replacement cost.

Replacement cost means the cost of replacing property without a reduction for depreciation.

You must replace property or valuation reverts to actually cash value.

.www.InsuranceCommunityUniversity.com

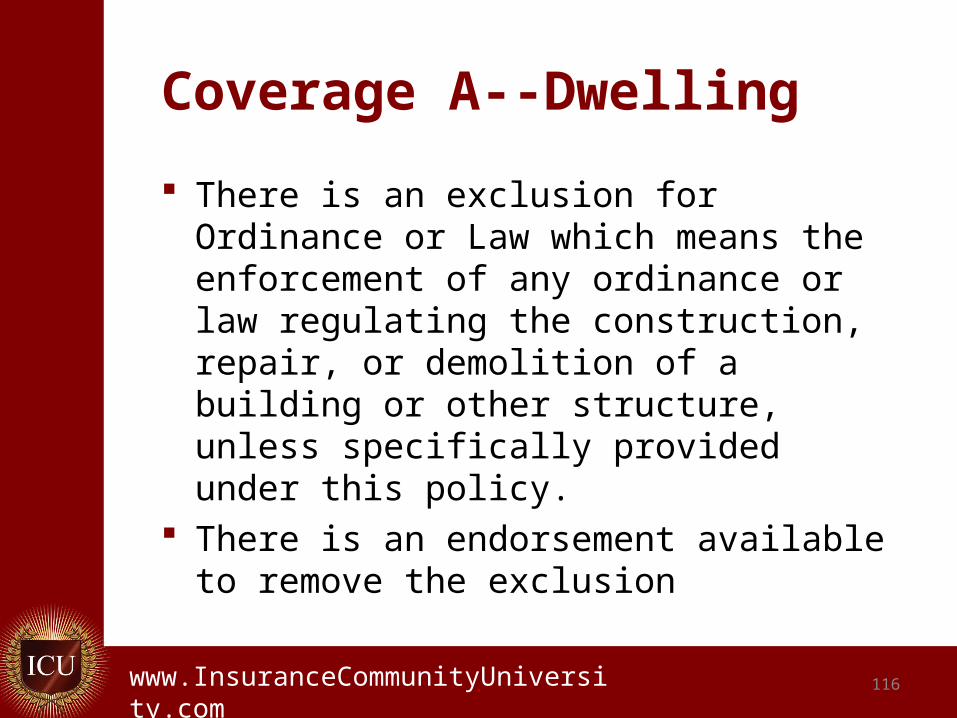

Coverage A--Dwelling

There is an exclusion for Ordinance or Law which means the enforcement of any ordinance or law regulating the construction, repair, or demolition of a building or other structure, unless specifically provided under this policy.

There is an endorsement available to remove the exclusion

116

.www.InsuranceCommunityUniversity.com 117

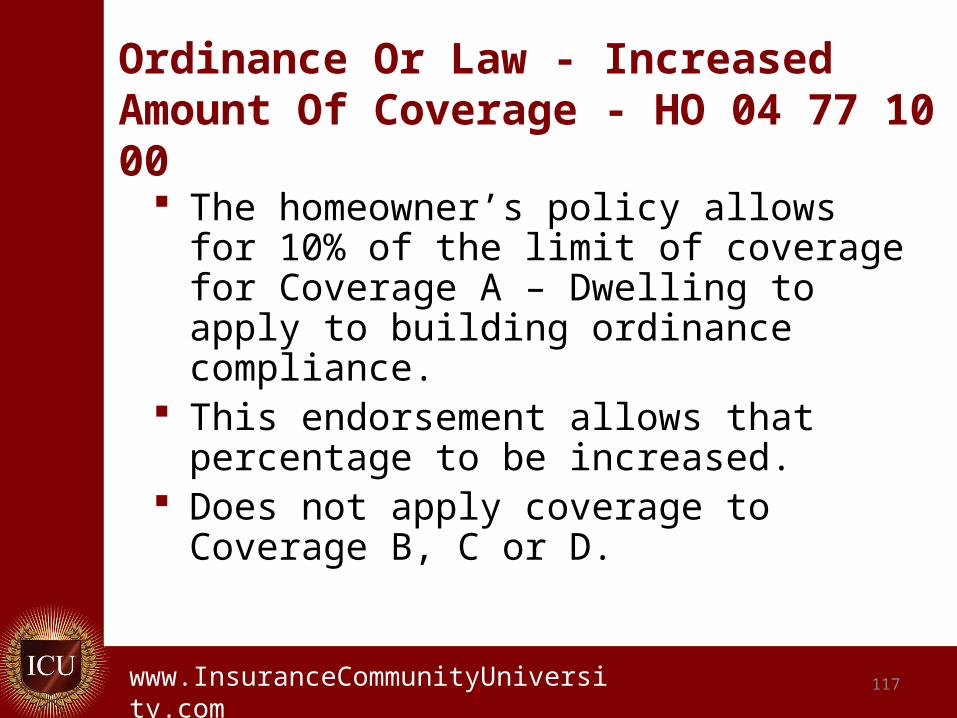

Ordinance Or Law - Increased Amount Of Coverage - HO 04 77 10 00

The homeowner’s policy allows for 10% of the limit of coverage for Coverage A – Dwelling to apply to building ordinance compliance.

This endorsement allows that percentage to be increased.

Does not apply coverage to Coverage B, C or D.

.www.InsuranceCommunityUniversity.com 118

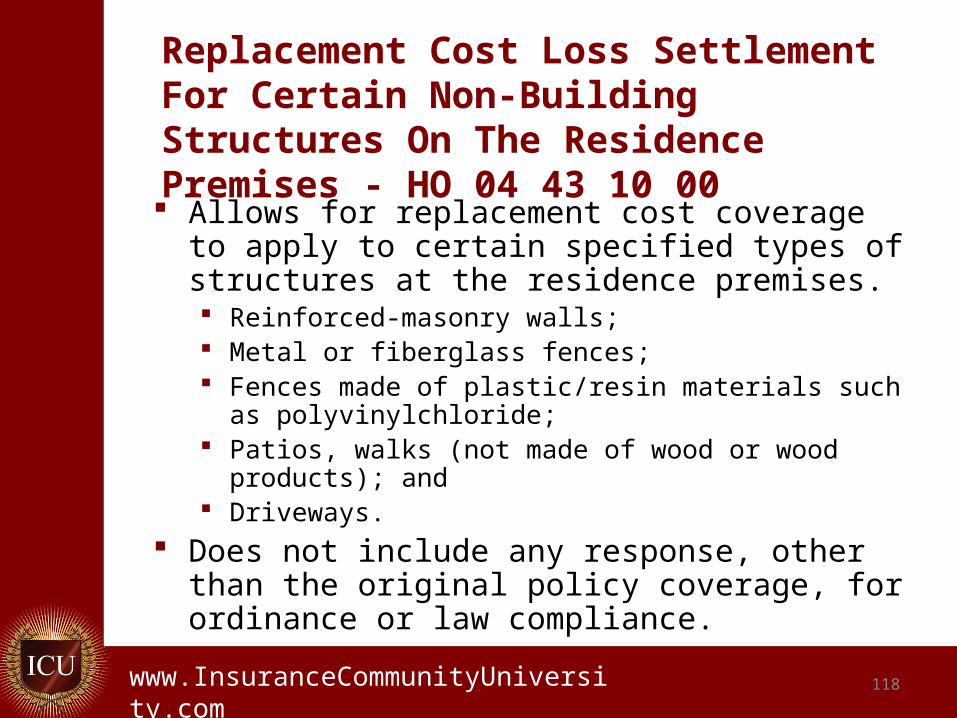

Replacement Cost Loss Settlement For Certain Non-Building Structures On The Residence Premises - HO 04 43 10 00 Allows for replacement cost coverage to apply to

certain specified types of structures at the residence premises. Reinforced-masonry walls; Metal or fiberglass fences; Fences made of plastic/resin materials such as

polyvinylchloride; Patios, walks (not made of wood or wood products); and Driveways.

Does not include any response, other than the original policy coverage, for ordinance or law compliance.

.www.InsuranceCommunityUniversity.com 119

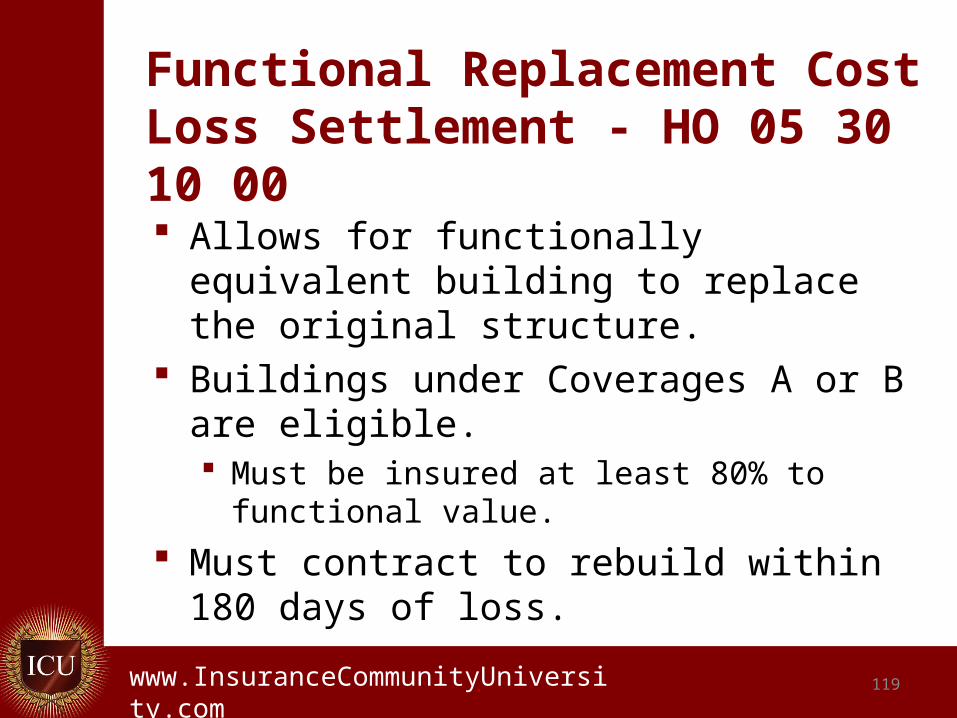

Functional Replacement Cost Loss Settlement - HO 05 30 10 00

Allows for functionally equivalent building to replace the original structure.

Buildings under Coverages A or B are eligible. Must be insured at least 80% to functional

value.

Must contract to rebuild within 180 days of loss.

.www.InsuranceCommunityUniversity.com

Coverage A - Dwelling

Some companies have special reproduction provisions for older homes especially those on the registry

120

.www.InsuranceCommunityUniversity.com

Coverage B Other Structures

Provided for Automatically for 10% of the Coverage A

Dwelling Amount

121

.www.InsuranceCommunityUniversity.com 122

Coverage B – Other Structures

Coverage on a garage or other private structures not attached to or part of the dwelling.

Includes such things as swimming pools, fences, tool sheds, tennis courts, and greenhouses.

.www.InsuranceCommunityUniversity.com 123

Coverage B – Other Structures

We cover other structures on the residence premises set apart from the dwelling by clear space. This includes structures connected to the dwelling by only a fence, utility line, or similar connection.

.www.InsuranceCommunityUniversity.com

Coverage B – Other Structures

We do not cover: Land… Other structures rented or held for

rental to any person not a tenant of the dwelling unless used solely as a private garage

Other structures from which any “business” is conducted; or

124

.www.InsuranceCommunityUniversity.com

Coverage B – Other Structures

Other structures used to store “business” property. However, we do cover a structure that contains “business” property solely owned by an “insured” or a tenant of the dwelling provided that “business property” does not include gaseous or liquid fuel other than fuel in a permanently installed fuel tank of a vehicle or craft parked or stored in the structure.

125

.www.InsuranceCommunityUniversity.com 126

Coverage B – Other Structures

The 10% of coverage “A” that is automatically provided as a coverage “B” limit is increased by some carriers or specific coverage on scheduled structures can be obtained by endorsement.

.www.InsuranceCommunityUniversity.com 127

Coverage B – Other Structures

The limit of liability for this coverage will not be more than 10% of the limit of liability that applies to Coverage A. Use of this coverage does not reduce the Coverage A limit of liability.

.www.InsuranceCommunityUniversity.com 128

Coverage B – Other Structures

Problem: If the insured operates an incidental business

in the home, coverage for the dwelling is provided.

If the insured operates an incidental business or stores business personal property in the “other structure” the “other structure” is not covered.”

.www.InsuranceCommunityUniversity.com 129

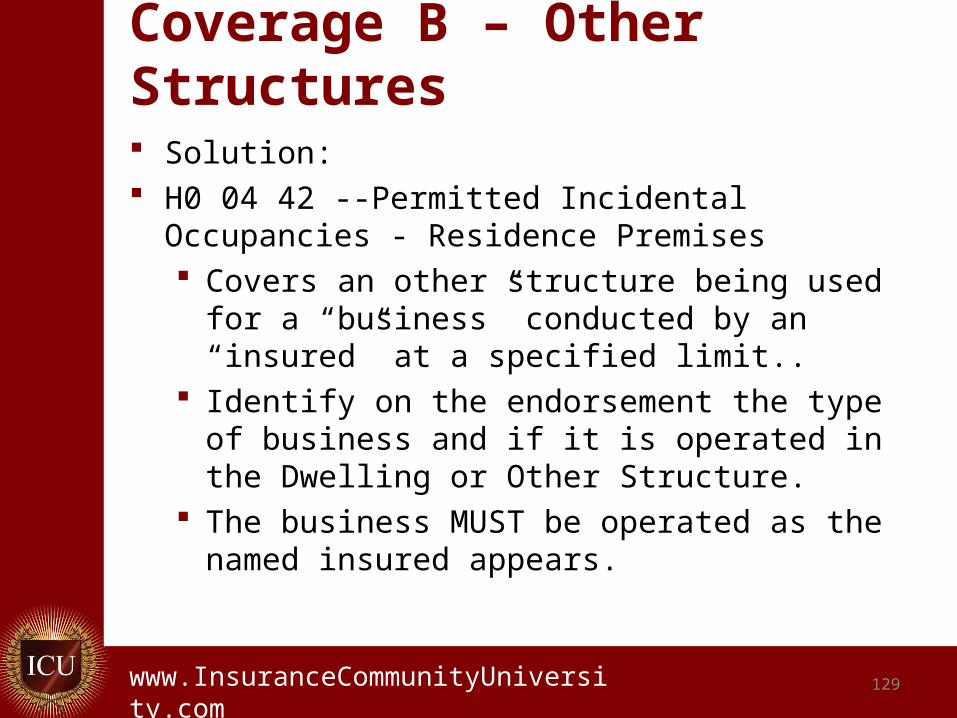

Coverage B – Other Structures

Solution: H0 04 42 --Permitted Incidental Occupancies -

Residence Premises Covers an other structure being used for a

“business” conducted by an “insured” at a specified limit..

Identify on the endorsement the type of business and if it is operated in the Dwelling or Other Structure.

The business MUST be operated as the named insured appears.

.www.InsuranceCommunityUniversity.com 130

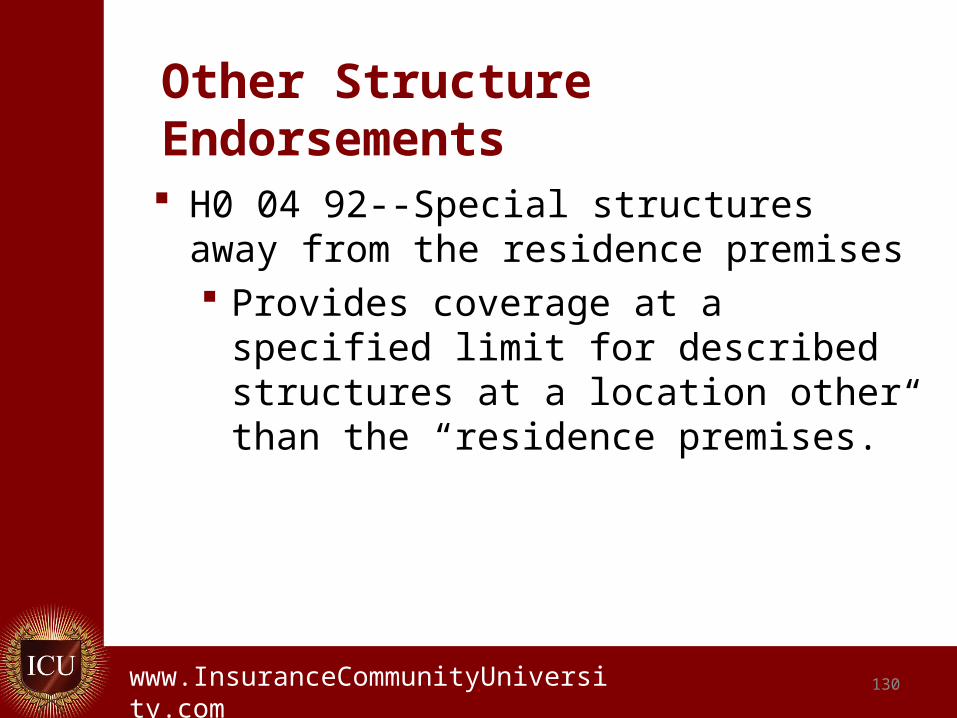

Other Structure Endorsements

H0 04 92--Special structures away from the residence premises Provides coverage at a specified limit for

described structures at a location other than the “residence premises.”

.www.InsuranceCommunityUniversity.com 131

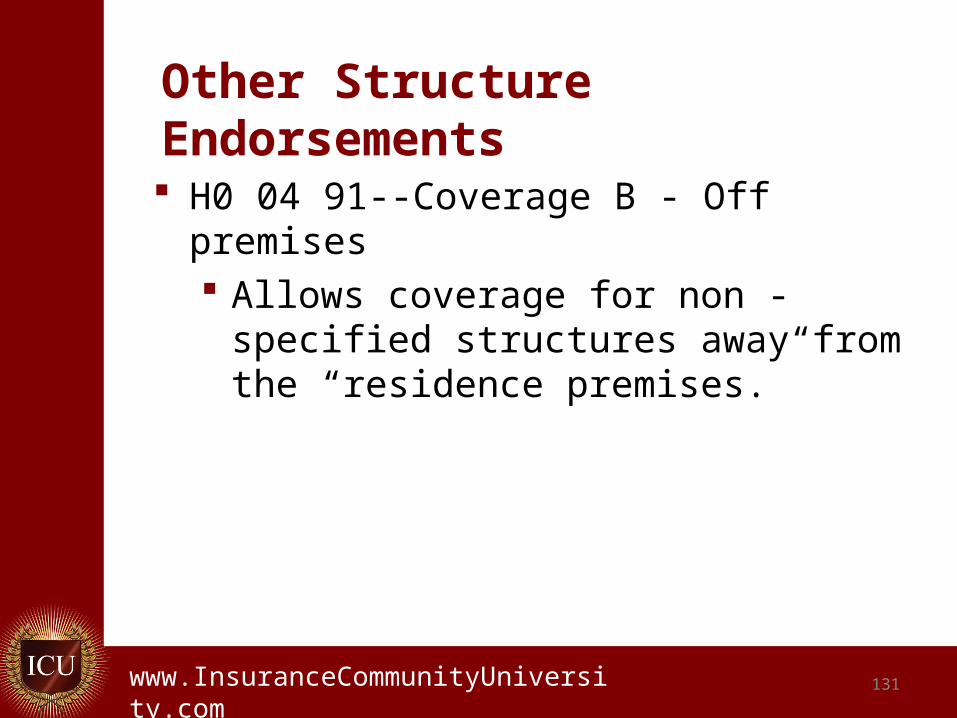

Other Structure Endorsements

H0 04 91--Coverage B - Off premises Allows coverage for non - specified

structures away from the “residence premises.”

.www.InsuranceCommunityUniversity.com 132

Other Structure Endorsements

H0 04 40 --Structures Rented to Others Residence Premises Covers described rental structures for a

specified limit.

.www.InsuranceCommunityUniversity.com 133

Other Structure Endorsements

H0 04 48 -Other Structures - Increased Limits Increases coverage on detached

structures for an amount excess of the policy amount.

The structure(s) that necessitates the increase must be described.

.www.InsuranceCommunityUniversity.com

Coverage CPersonal Property

Provided for Automatically for 50% of the Coverage A

Dwelling Amount

134

.www.InsuranceCommunityUniversity.com

Coverage C—Personal Property The ISO Homeowners Form provides for

the percentage of Coverage A to be 50% There are insurance companies who will

issue the coverage with a higher percentage automatically

Some carriers will allow the percentage to be higher by endorsement

135

.www.InsuranceCommunityUniversity.com 136

Coverage C—Personal Property

We cover personal property owned or used by an insured while it is anywhere in the world. Covers the insured’s personal property

worldwide, with no territorial restrictions

.www.InsuranceCommunityUniversity.com 137

Coverage C—Personal PropertyAfter a loss and at your request, we will

cover personal property owned by:a. Others while the property is on the

part of the residence premises occupied by an insured;

b. A guest or residence employee, while the property is in any residence occupied by an insured.

.www.InsuranceCommunityUniversity.com 138

Coverage C – Limit for Property at Other Residences

Our limit of liability for personal property usually located at an insured’s residence other than the residence premises is 10% of the limit of liability for Coverage C, or $1000, whichever is greater. However, this limitation does not apply to personal property:

.www.InsuranceCommunityUniversity.com

Coverage C – Limit for Property at Other Residences

a. Moved from the “residence premises” because it is being repaired, renovated or rebuilt and is not fit to live in or store property in; or

b. In a newly acquired principal residence for 30 days from the time you begin to move the property there.

139

.www.InsuranceCommunityUniversity.com 140

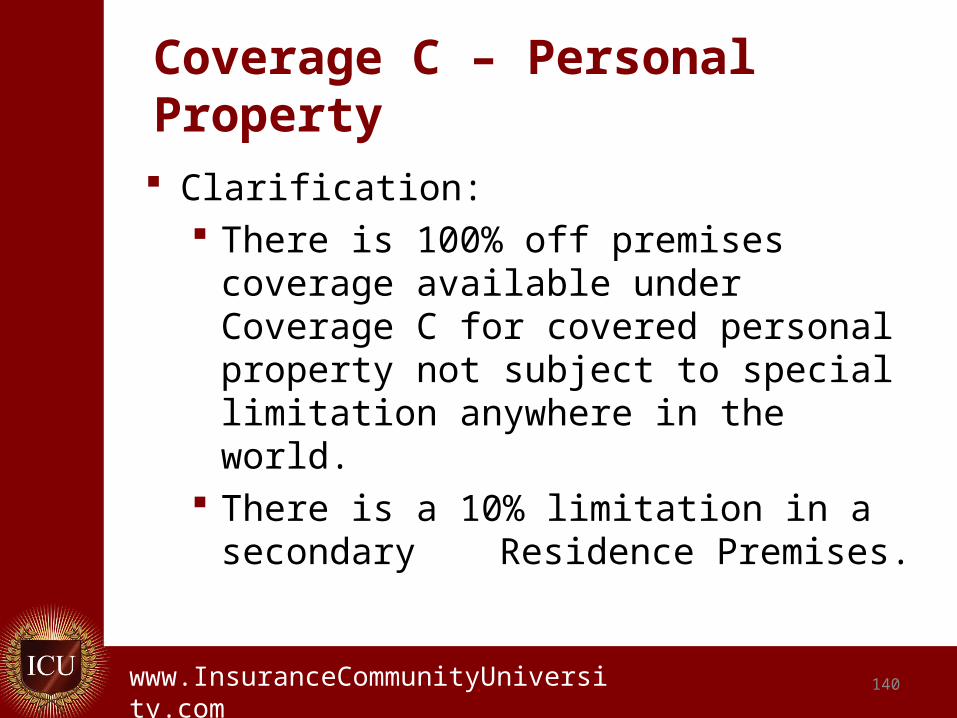

Coverage C – Personal Property

Clarification: There is 100% off premises coverage

available under Coverage C for covered personal property not subject to special limitation anywhere in the world.

There is a 10% limitation in a secondary Residence Premises.

.www.InsuranceCommunityUniversity.com 141

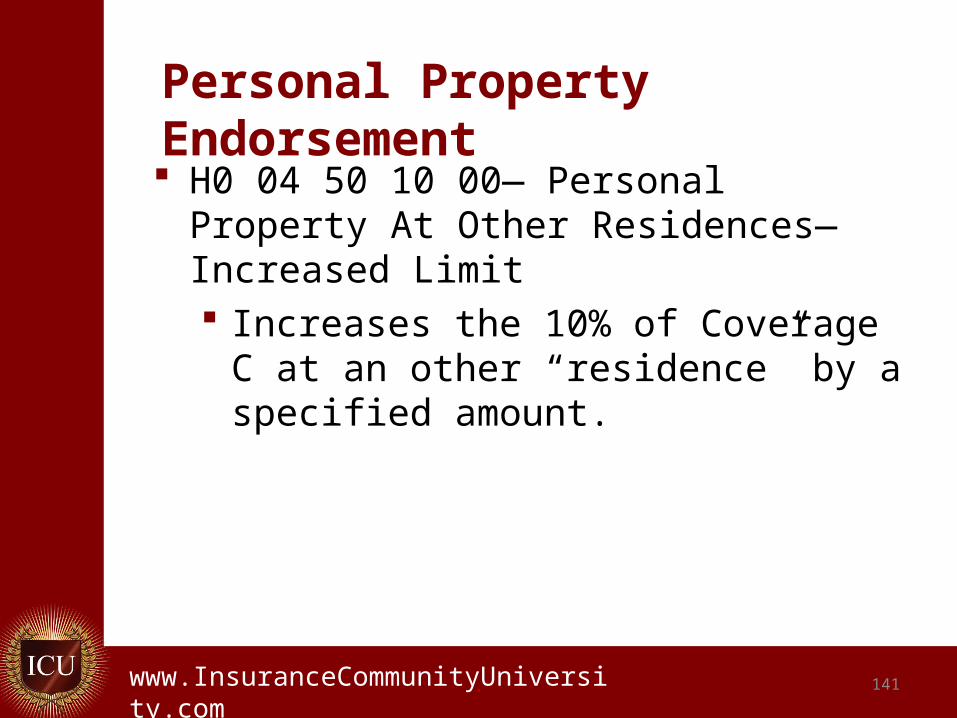

Personal Property Endorsement H0 04 50 10 00— Personal Property At

Other Residences—Increased Limit Increases the 10% of Coverage C at an

other “residence” by a specified amount.

.www.InsuranceCommunityUniversity.com 142

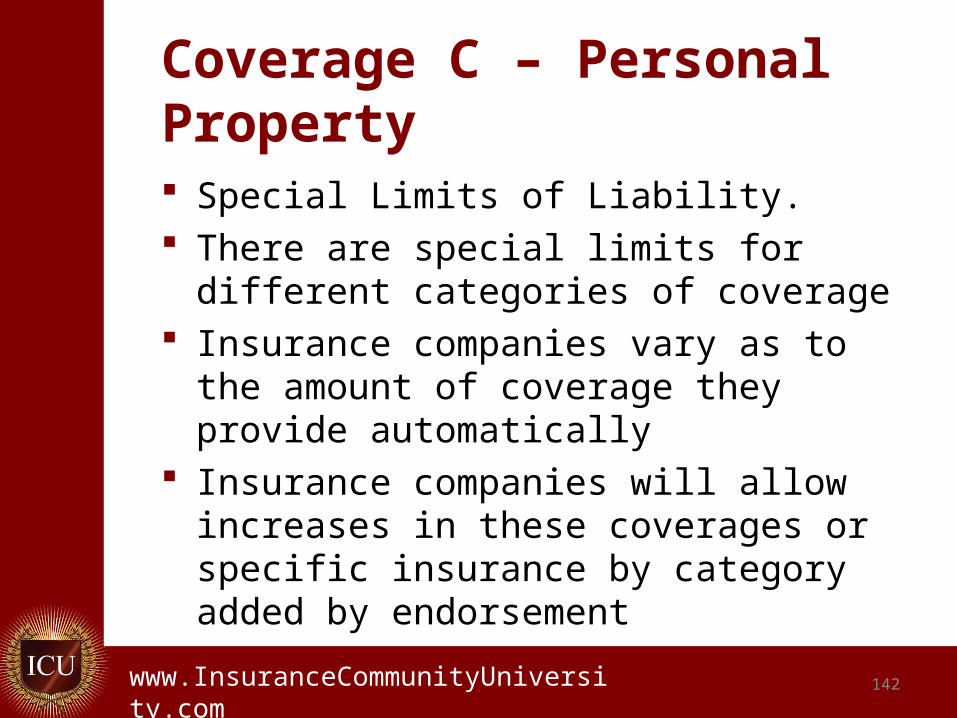

Coverage C – Personal Property Special Limits of Liability. There are special limits for different

categories of coverage Insurance companies vary as to the

amount of coverage they provide automatically

Insurance companies will allow increases in these coverages or specific insurance by category added by endorsement

.www.InsuranceCommunityUniversity.com

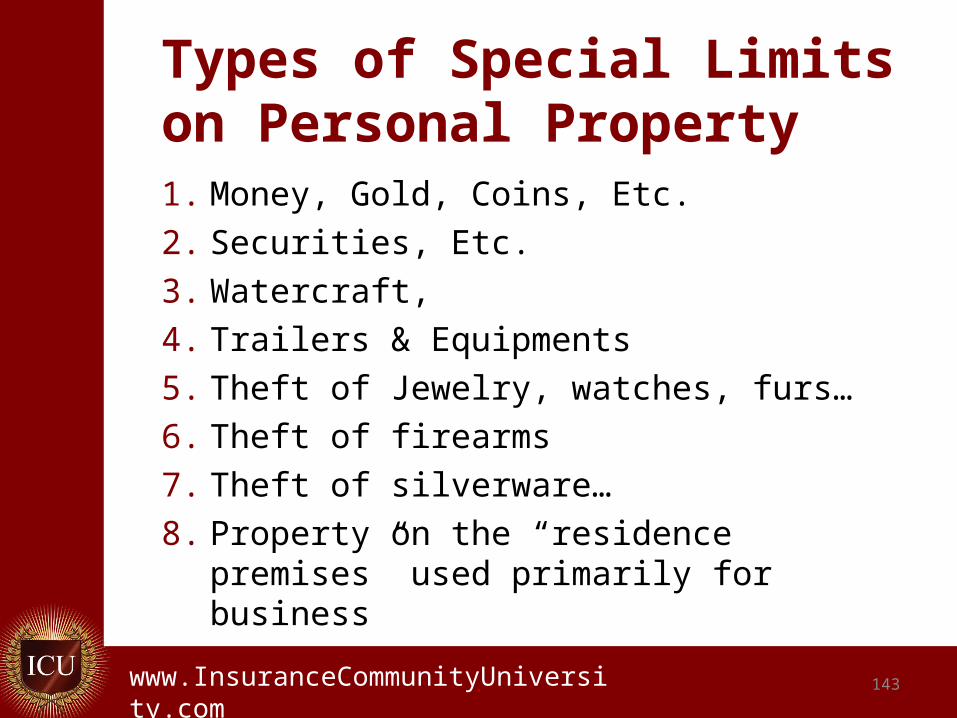

Types of Special Limits on Personal Property1. Money, Gold, Coins, Etc.

2. Securities, Etc.

3. Watercraft,

4. Trailers & Equipments

5. Theft of Jewelry, watches, furs…

6. Theft of firearms

7. Theft of silverware…

8. Property on the “residence premises” used primarily for business

143

.www.InsuranceCommunityUniversity.com 144

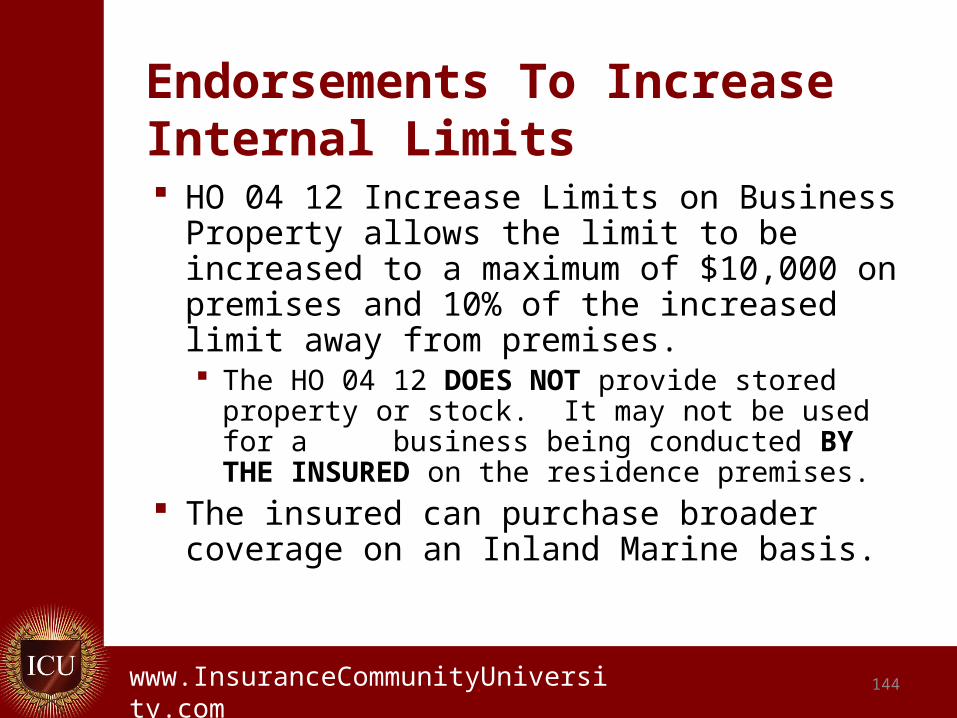

Endorsements To Increase Internal Limits HO 04 12 Increase Limits on Business

Property allows the limit to be increased to a maximum of $10,000 on premises and 10% of the increased limit away from premises. The HO 04 12 DOES NOT provide stored

property or stock. It may not be used for a business being conducted BY THE INSURED on the residence premises.

The insured can purchase broader coverage on an Inland Marine basis.

.www.InsuranceCommunityUniversity.com

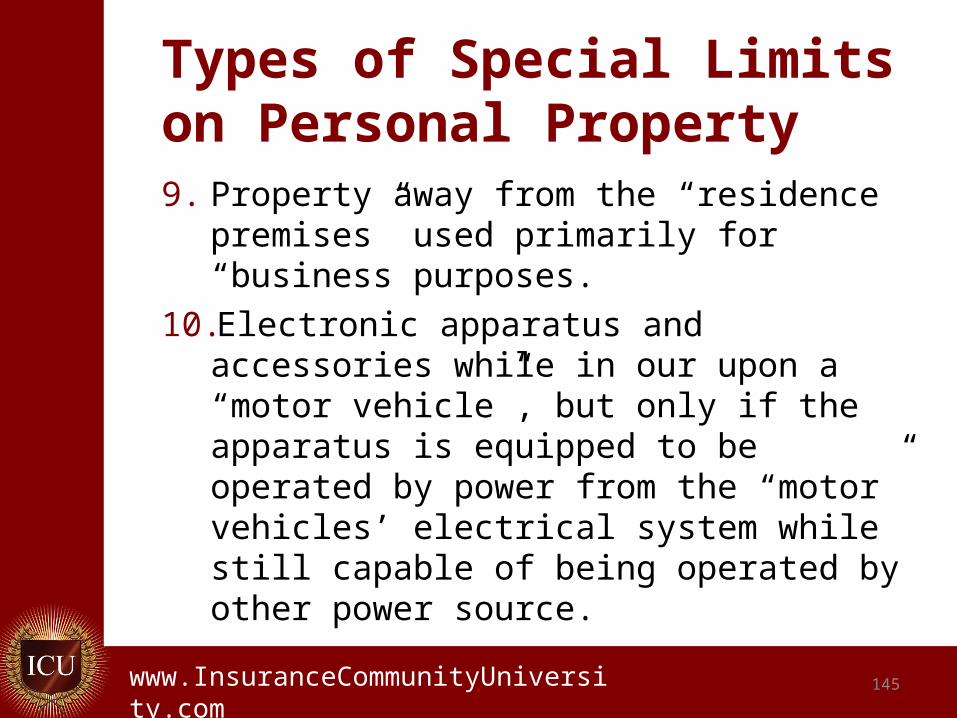

Types of Special Limits on Personal Property9. Property away from the “residence

premises” used primarily for “business purposes.

10.Electronic apparatus and accessories while in our upon a “motor vehicle”, but only if the apparatus is equipped to be operated by power from the “motor” vehicles’ electrical system while still capable of being operated by other power source.

145

.www.InsuranceCommunityUniversity.com 146

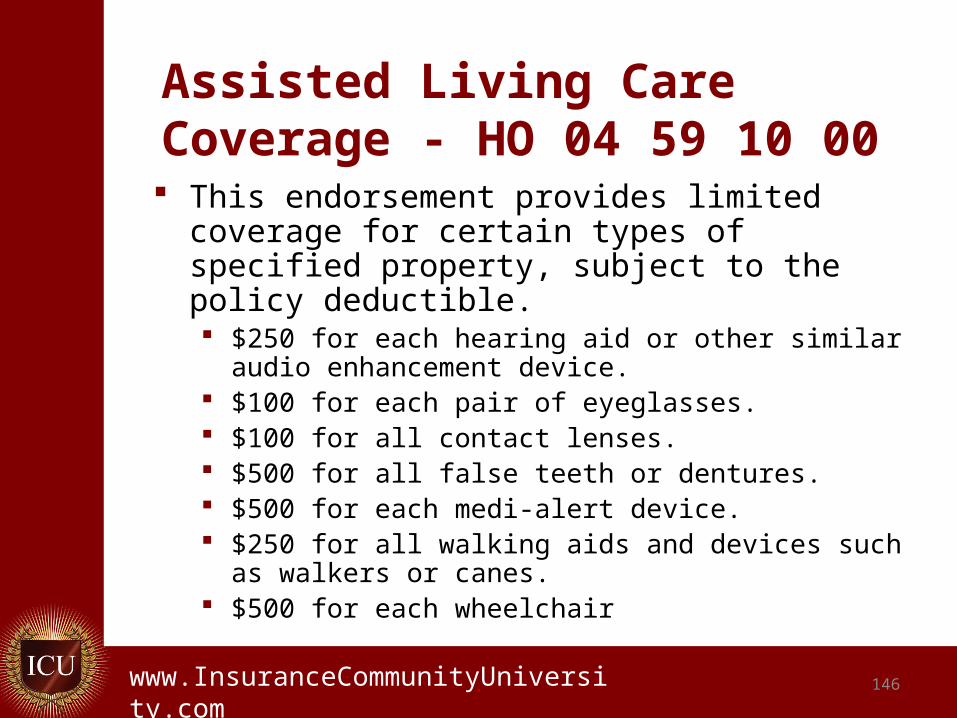

Assisted Living Care Coverage - HO 04 59 10 00 This endorsement provides limited coverage for

certain types of specified property, subject to the policy deductible. $250 for each hearing aid or other similar audio

enhancement device. $100 for each pair of eyeglasses. $100 for all contact lenses. $500 for all false teeth or dentures. $500 for each medi-alert device. $250 for all walking aids and devices such as walkers or

canes. $500 for each wheelchair

.www.InsuranceCommunityUniversity.com 147

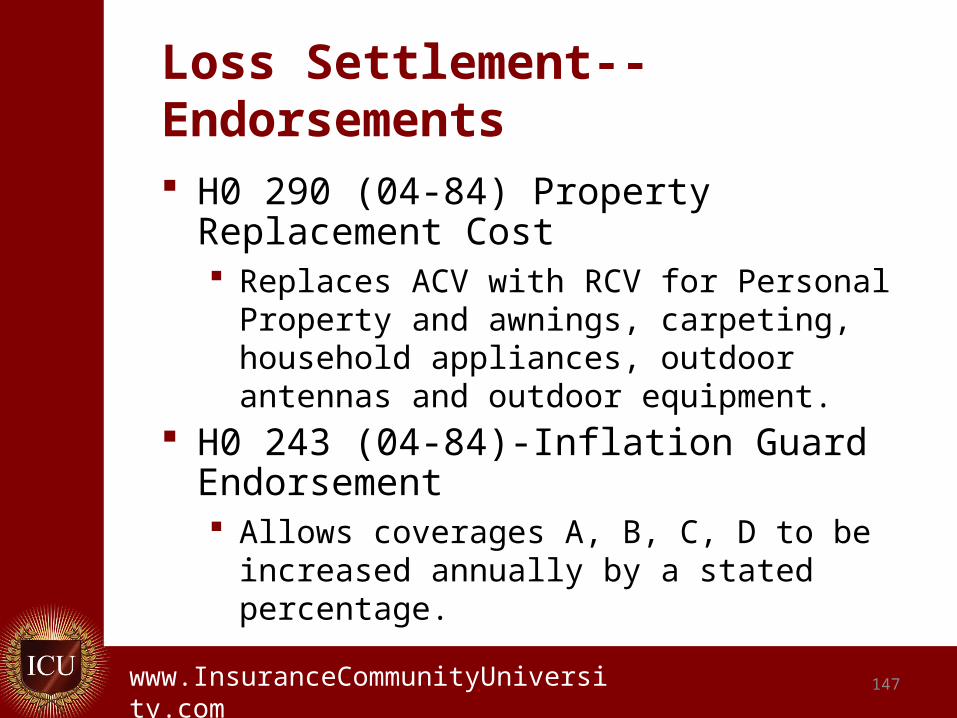

Loss Settlement--Endorsements

H0 290 (04-84) Property Replacement Cost Replaces ACV with RCV for Personal Property

and awnings, carpeting, household appliances, outdoor antennas and outdoor equipment.

H0 243 (04-84)-Inflation Guard Endorsement Allows coverages A, B, C, D to be increased

annually by a stated percentage.

.www.InsuranceCommunityUniversity.com 148

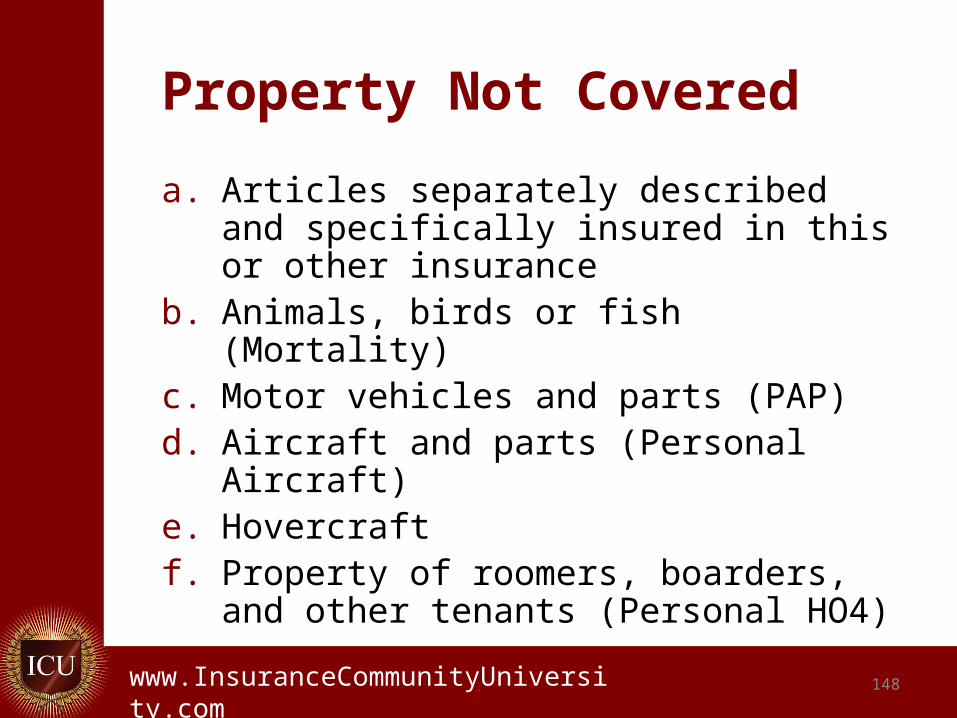

Property Not Covered

a. Articles separately described and specifically insured in this or other insurance

b. Animals, birds or fish (Mortality)c. Motor vehicles and parts (PAP)d. Aircraft and parts (Personal Aircraft)e. Hovercraftf. Property of roomers, boarders, and

other tenants (Personal HO4)

.www.InsuranceCommunityUniversity.com

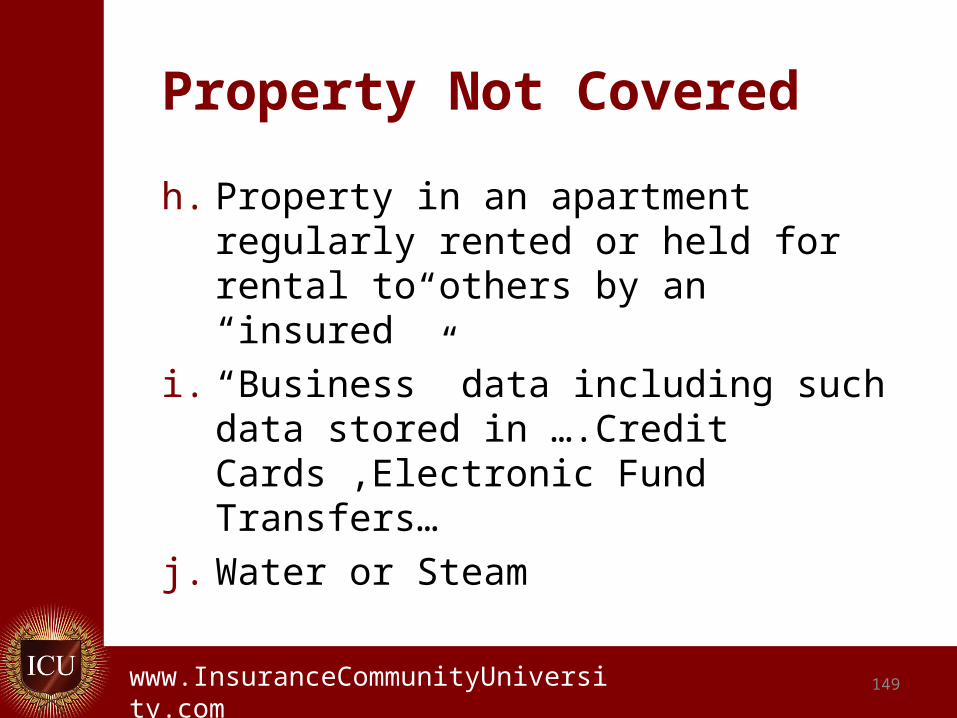

Property Not Covered

h. Property in an apartment regularly rented or held for rental to others by an “insured”

i. “Business” data including such data stored in ….Credit Cards ,Electronic Fund Transfers…

j. Water or Steam

149

.www.InsuranceCommunityUniversity.com 150

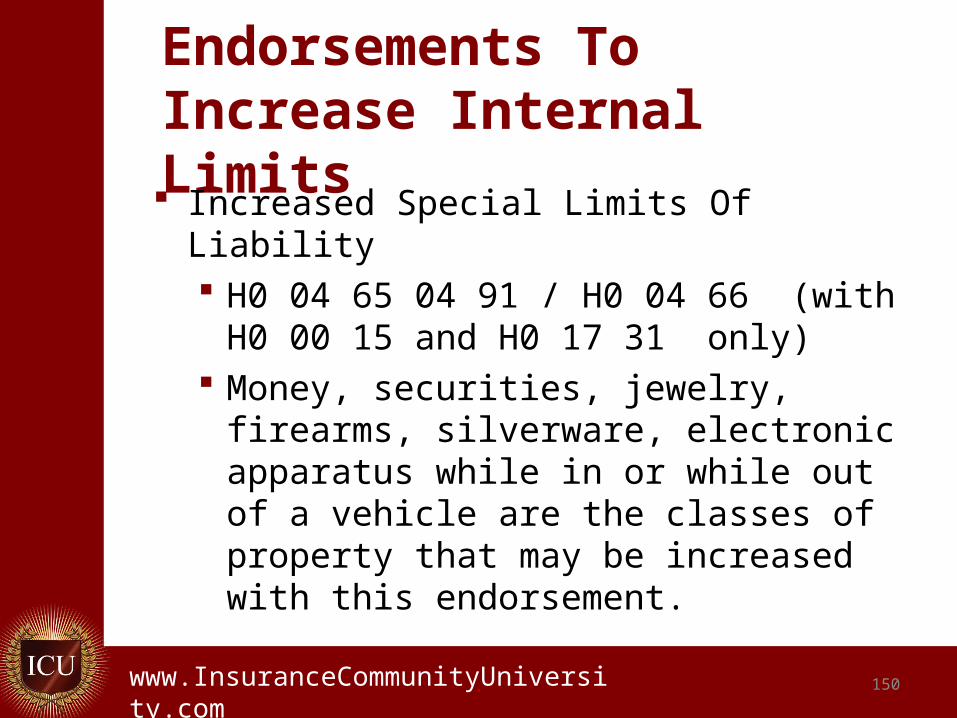

Endorsements To Increase Internal Limits Increased Special Limits Of Liability

H0 04 65 04 91 / H0 04 66 (with H0 00 15 and H0 17 31 only)

Money, securities, jewelry, firearms, silverware, electronic apparatus while in or while out of a vehicle are the classes of property that may be increased with this endorsement.

.www.InsuranceCommunityUniversity.com 151

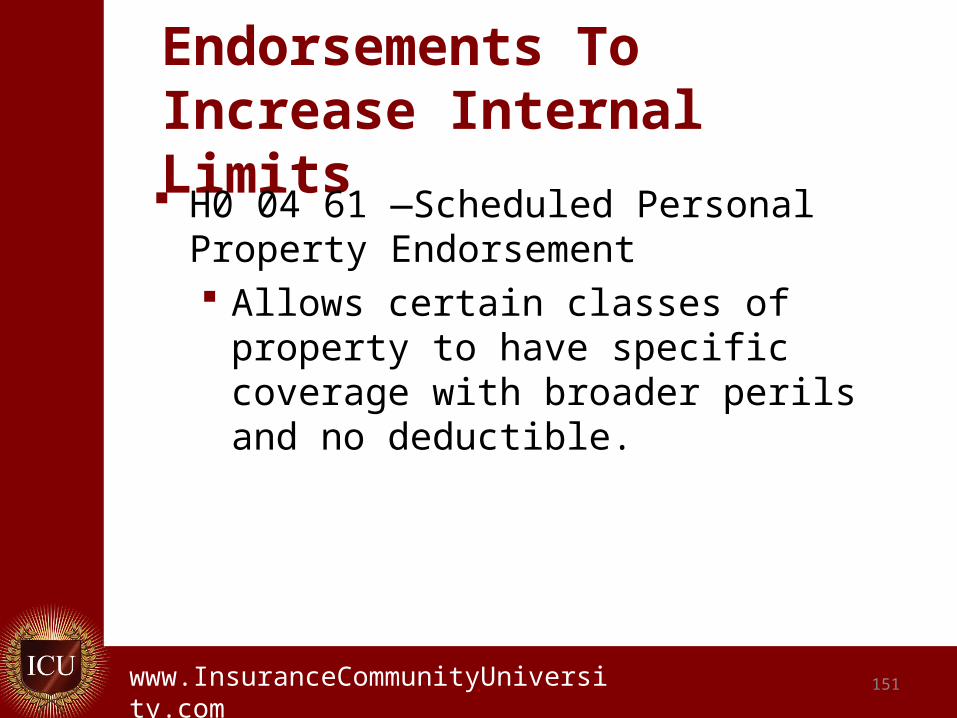

Endorsements To Increase Internal Limits H0 04 61 —Scheduled Personal Property

Endorsement Allows certain classes of property to

have specific coverage with broader perils and no deductible.

.www.InsuranceCommunityUniversity.com 152

Scheduled Personal Property Endorsement The Scheduled Personal Property

Endorsement Provides Coverage for a Schedule (List) of Specific Items.

.www.InsuranceCommunityUniversity.com 153

Scheduled Personal Property Endorsement A Loss to a Scheduled Item (Other Than

Fine Art) Is Settled at the Lesser Of: Actual Cash Value The Cost to Repair the Item The Amount for Which the Item Could Be

Replaced With on Substantially Identical to the Lost or Damaged Item.

.www.InsuranceCommunityUniversity.com 154

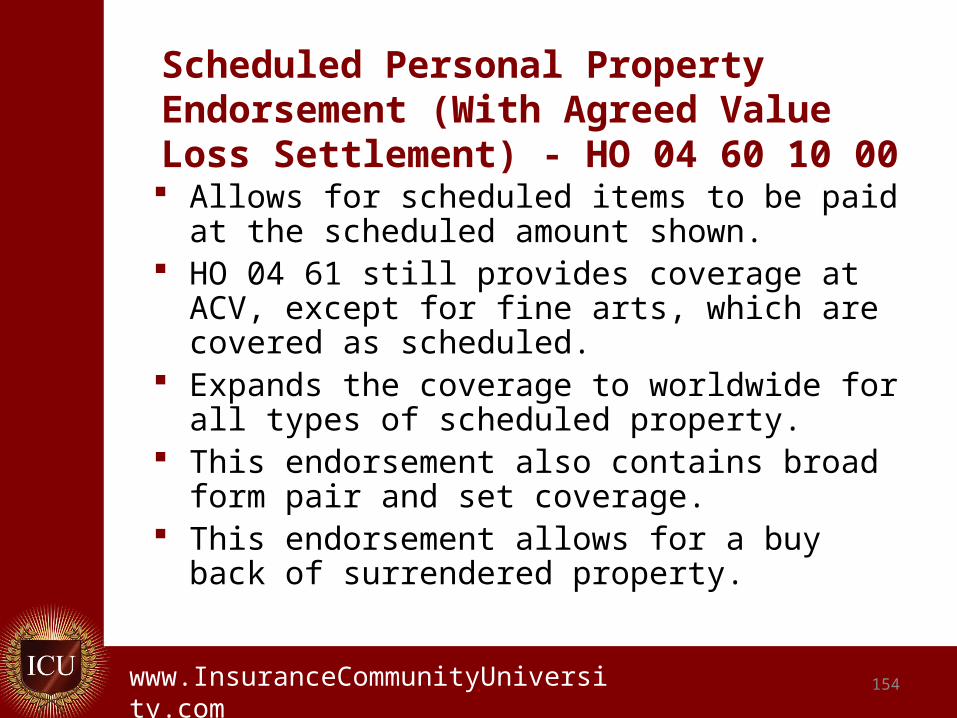

Scheduled Personal Property Endorsement (With Agreed Value Loss Settlement) - HO 04 60 10 00 Allows for scheduled items to be paid at the

scheduled amount shown. HO 04 61 still provides coverage at ACV, except

for fine arts, which are covered as scheduled. Expands the coverage to worldwide for all types of

scheduled property. This endorsement also contains broad form pair

and set coverage. This endorsement allows for a buy back of

surrendered property.

.www.InsuranceCommunityUniversity.com

Identity Fraud Expense Coverage HO 04 55 03 03 The endorsement provides up to $15,000

for “expenses” incurred by an “insured” as the direct result of any one “identity fraud” first discovered or learned of during the policy period.

155

.www.InsuranceCommunityUniversity.com

Loss of UseAdditional Living Expense

Provided for Automatically for 20% of the Coverage A

Dwelling Amount

156

.www.InsuranceCommunityUniversity.com

Coverage D—Loss of Use

There are four insuring agreements

1. Additional Living Expense

2. Fair Rental Value

3. Civil Authority Prohibits Use

4. Loss or Expense Not Covered

157

.www.InsuranceCommunityUniversity.com 158

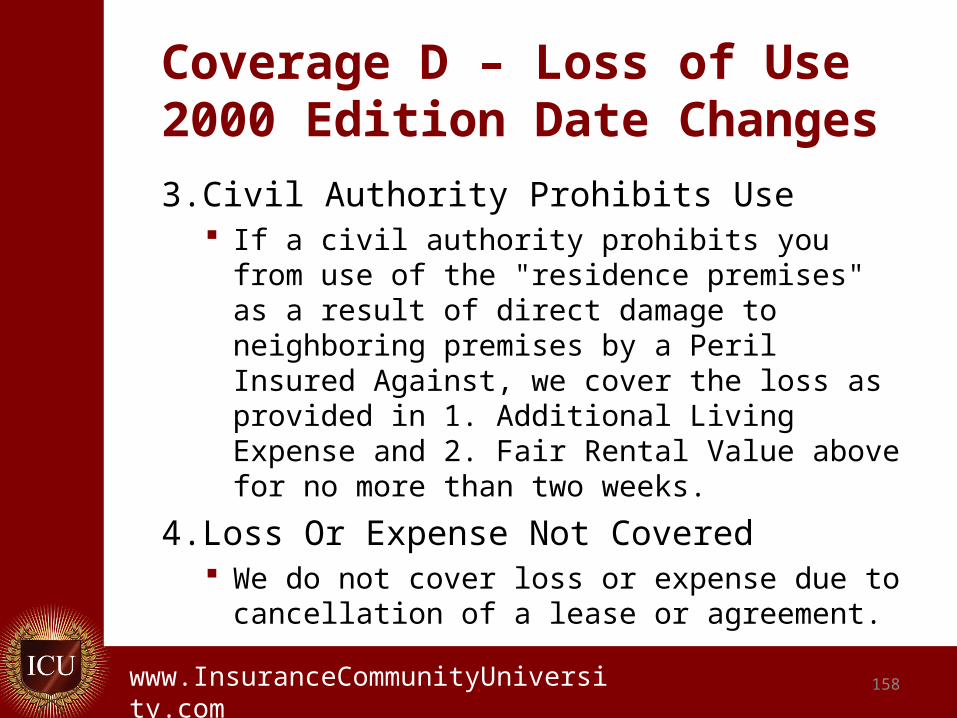

Coverage D – Loss of Use 2000 Edition Date Changes

3.Civil Authority Prohibits Use If a civil authority prohibits you from use of the

"residence premises" as a result of direct damage to neighboring premises by a Peril Insured Against, we cover the loss as provided in 1. Additional Living Expense and 2. Fair Rental Value above for no more than two weeks.

4.Loss Or Expense Not Covered We do not cover loss or expense due to

cancellation of a lease or agreement.

.www.InsuranceCommunityUniversity.com 159

Coverage D – Loss of Use

Loss of Use is provided for 20% of the dwelling amount

If a covered loss makes the insured dwelling uninhabitable, the policy allows two methods of compensation for such loss:

.www.InsuranceCommunityUniversity.com

Coverage D – Loss of Use

Some insurance companies do limit Loss of Use with a percentage.

Some companies will provide for unlimited Loss of Use but will specify the length of time they will pay for example 18 months.

160

.www.InsuranceCommunityUniversity.com 161

Coverage D – Loss of Use Additional Living Expenses- the necessary

increase in living expenses incurred by the insured to maintain the insured’s normal standard of living.

Fair Rental Value- the amount of rent that could reasonably be charged for the premises, less any expenses that do not continue while the premises are uninhabitable.

.www.InsuranceCommunityUniversity.com 162

Coverage D – Loss of Use

4. We will pay for the necessary increase in your normal living expense if:

a. Your residence is made untenantable by an off-premises power stoppage; and

b. This power stoppage is caused by a peril insured against under Coverage A, B, or C

.www.InsuranceCommunityUniversity.com 163

Coverage D – Loss of Use

This coverage extension will not start until the residence premises has been untenantable for 48 hours and will continue for no longer than 7 days.

.www.InsuranceCommunityUniversity.com

Additional Coverages

Subject to Certain Limitations for

Specific Perils and Types of Losses

164

.www.InsuranceCommunityUniversity.com 165

Additional Coverages

1. Debris Removal

2. Reasonable Repairs

3. Trees, Shrubs, and Other Plants

4. Fire Department Service Charge

5. Property Removed

6. Credit Card, Fund Transfer Card, Forgery, and Counterfeit Money

.www.InsuranceCommunityUniversity.com 166

Additional Coverages

7. Loss Assessment

8. Collapse

9. Glass or Safety Glazing Material

10.Landlord’s Furnishings

11.Ordinance or Law**

12.Grave Markers **New in 2000

.www.InsuranceCommunityUniversity.com 167

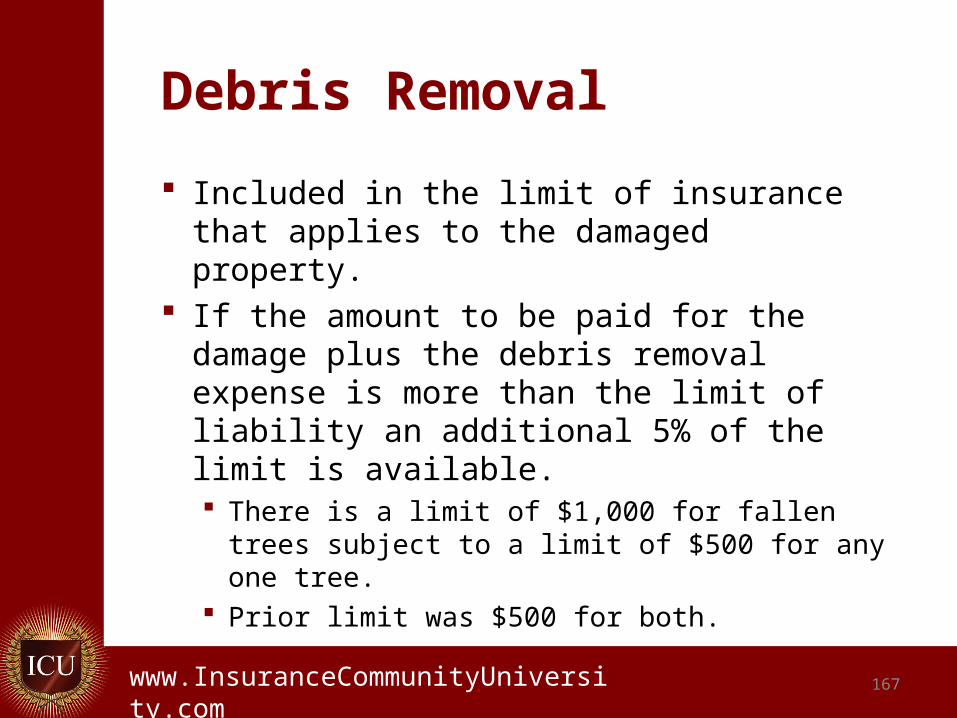

Debris Removal

Included in the limit of insurance that applies to the damaged property.

If the amount to be paid for the damage plus the debris removal expense is more than the limit of liability an additional 5% of the limit is available. There is a limit of $1,000 for fallen trees

subject to a limit of $500 for any one tree. Prior limit was $500 for both.

.www.InsuranceCommunityUniversity.com 168

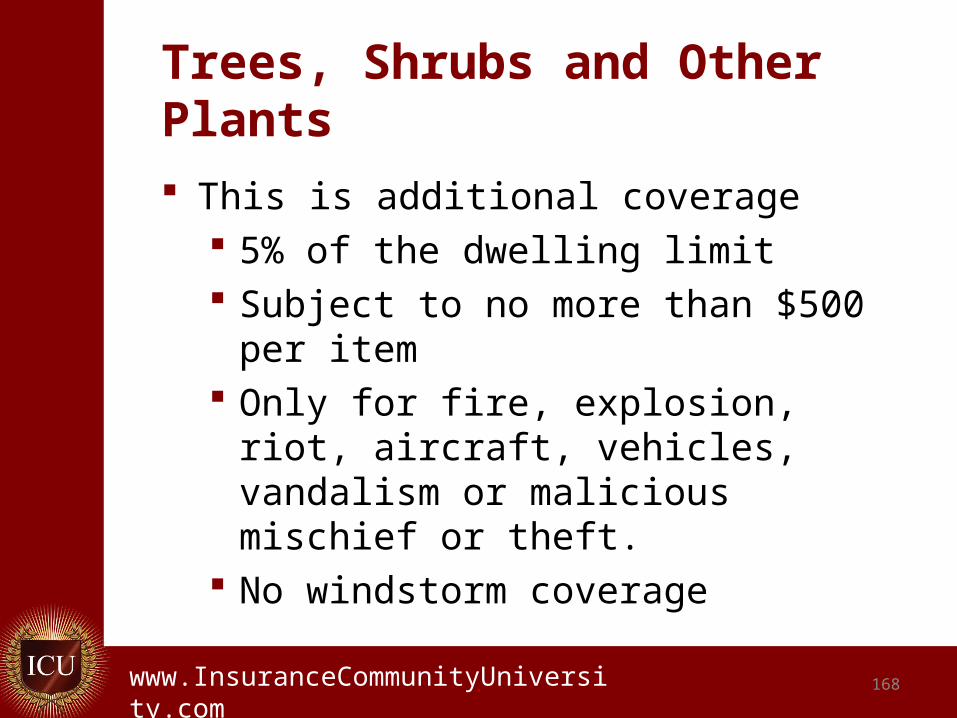

Trees, Shrubs and Other Plants

This is additional coverage 5% of the dwelling limit Subject to no more than $500 per item Only for fire, explosion, riot, aircraft,

vehicles, vandalism or malicious mischief or theft.

No windstorm coverage

.www.InsuranceCommunityUniversity.com 169

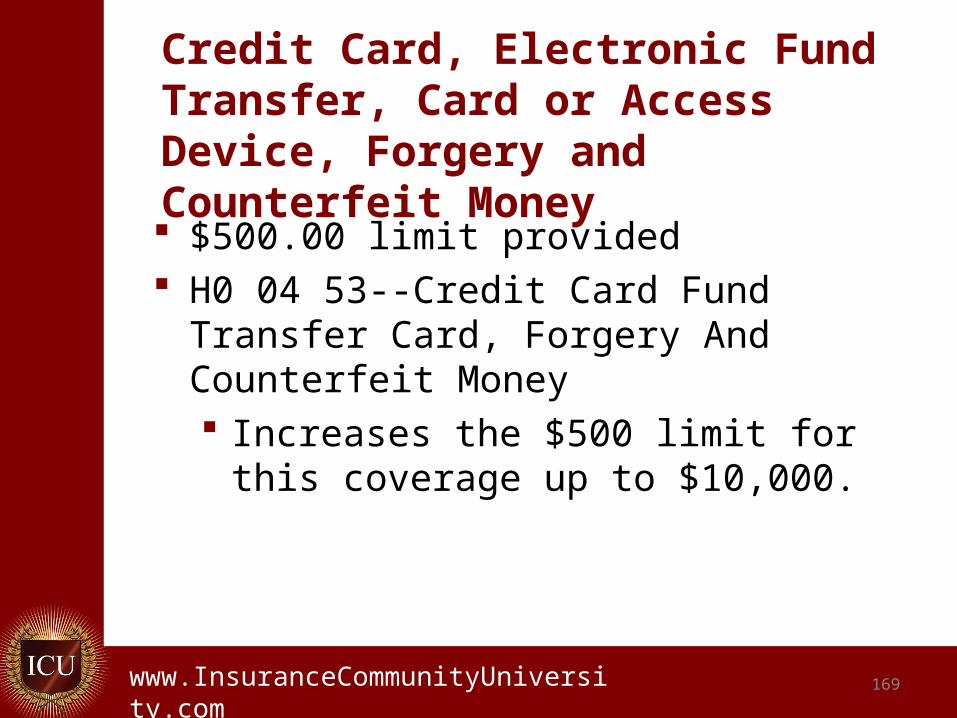

Credit Card, Electronic Fund Transfer, Card or Access Device, Forgery and Counterfeit Money $500.00 limit provided H0 04 53--Credit Card Fund Transfer Card,

Forgery And Counterfeit Money Increases the $500 limit for this coverage

up to $10,000.

.www.InsuranceCommunityUniversity.com 170

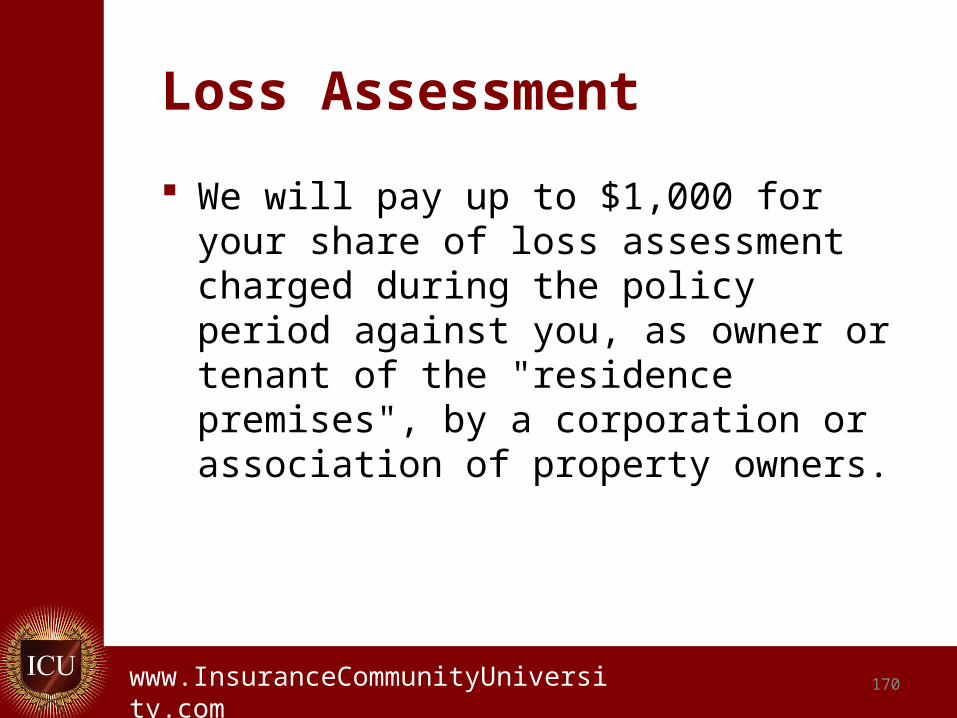

Loss Assessment

We will pay up to $1,000 for your share of loss assessment charged during the policy period against you, as owner or tenant of the "residence premises", by a corporation or association of property owners.

.www.InsuranceCommunityUniversity.com 171

Loss Assessment

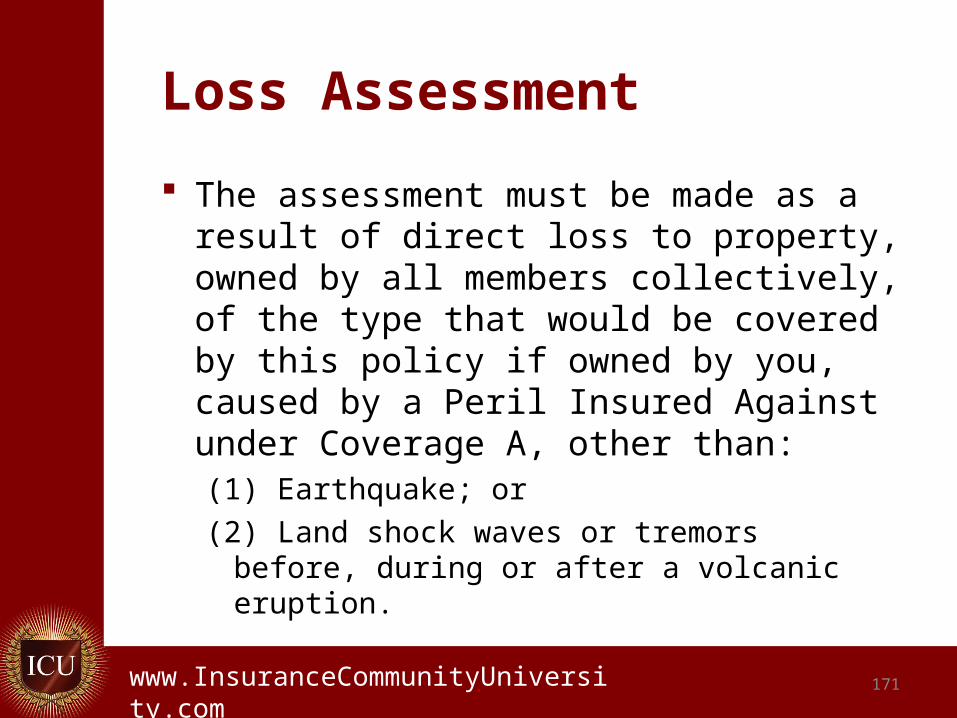

The assessment must be made as a result of direct loss to property, owned by all members collectively, of the type that would be covered by this policy if owned by you, caused by a Peril Insured Against under Coverage A, other than:(1) Earthquake; or

(2) Land shock waves or tremors before, during or after a volcanic eruption.

.www.InsuranceCommunityUniversity.com 172

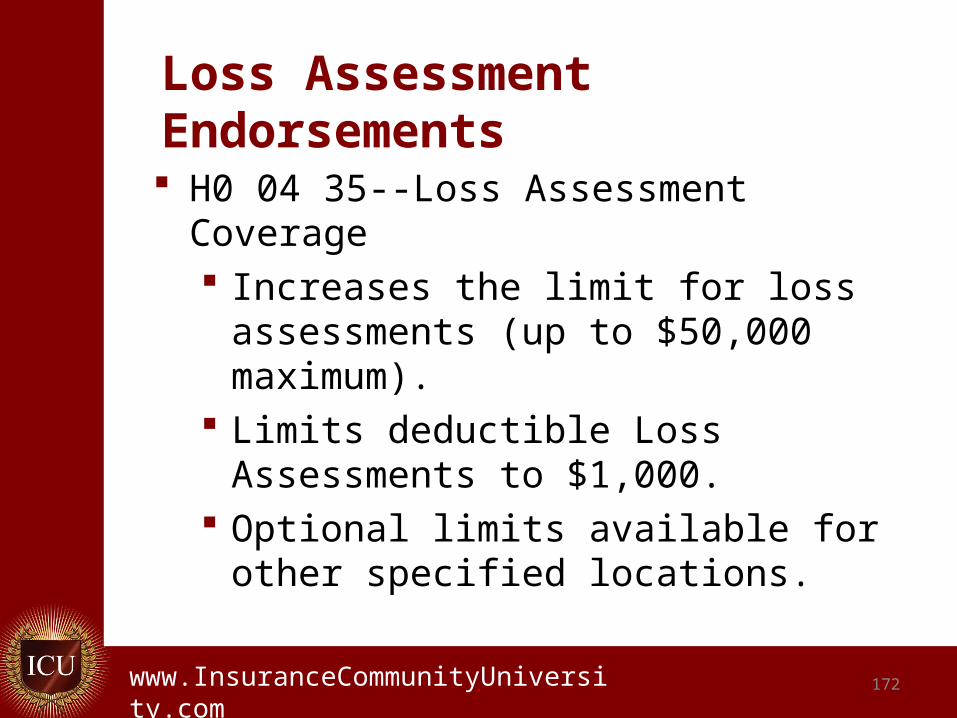

Loss Assessment Endorsements H0 04 35--Loss Assessment Coverage

Increases the limit for loss assessments (up to $50,000 maximum).

Limits deductible Loss Assessments to $1,000.

Optional limits available for other specified locations.

.www.InsuranceCommunityUniversity.com 173

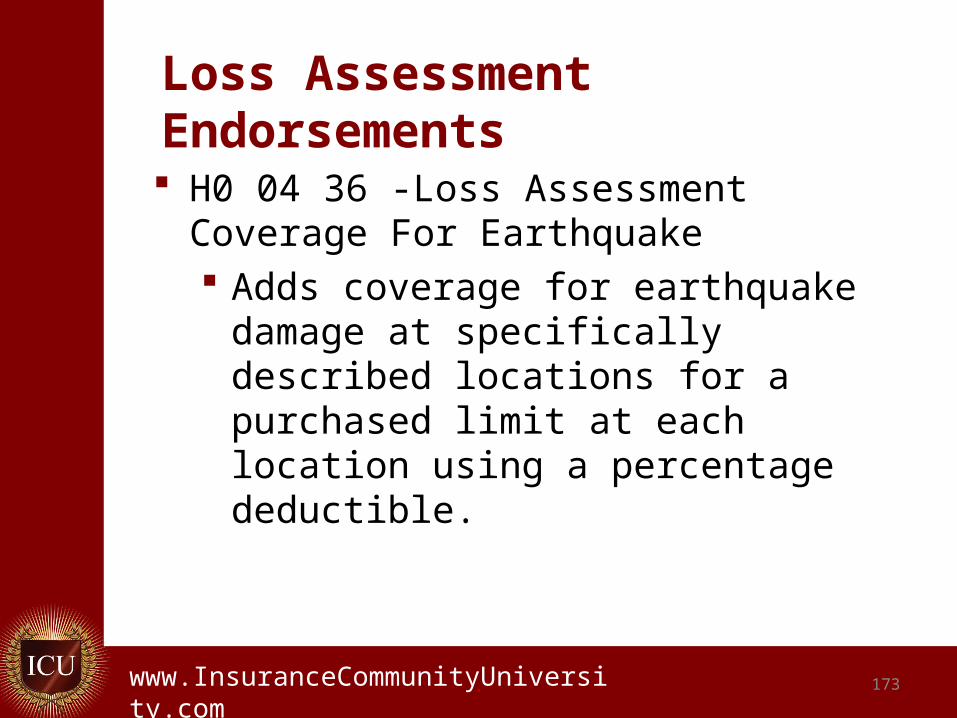

Loss Assessment Endorsements H0 04 36 -Loss Assessment Coverage For

Earthquake Adds coverage for earthquake damage

at specifically described locations for a purchased limit at each location using a percentage deductible.

.www.InsuranceCommunityUniversity.com 174

Collapse

Collapse means an abrupt falling down or caving in of a building or any part of a building with the result that the building or part of the building cannot be occupied for its current intended purpose.

.www.InsuranceCommunityUniversity.com 175

Collapse

A building or any part of a building that is in danger of falling down or caving in is not considered to be in a state of collapse.

.www.InsuranceCommunityUniversity.com 176

Collapse

A part of a building that is standing is not considered to be in a state of collapse even if it has separated from another part of the building.

A building or any part of a building that is standing is not considered to be in a state of collapse even if it shows evidence of cracking, bulging, sagging, bending, leaning, settling, shrinkage or expansion.

The last three are new language as of the 2000 form.

.www.InsuranceCommunityUniversity.com 177

Ordinance or Law

You may use up to 10% of the limit of liability that applies to Coverage A for the increased costs you incur due to the enforcement of any ordinance or law which requires or regulates This is new to the 2000 series. This can be increased with the HO 04

77 Ordinance or Law Increased Amount of Coverage.

.www.InsuranceCommunityUniversity.com 178

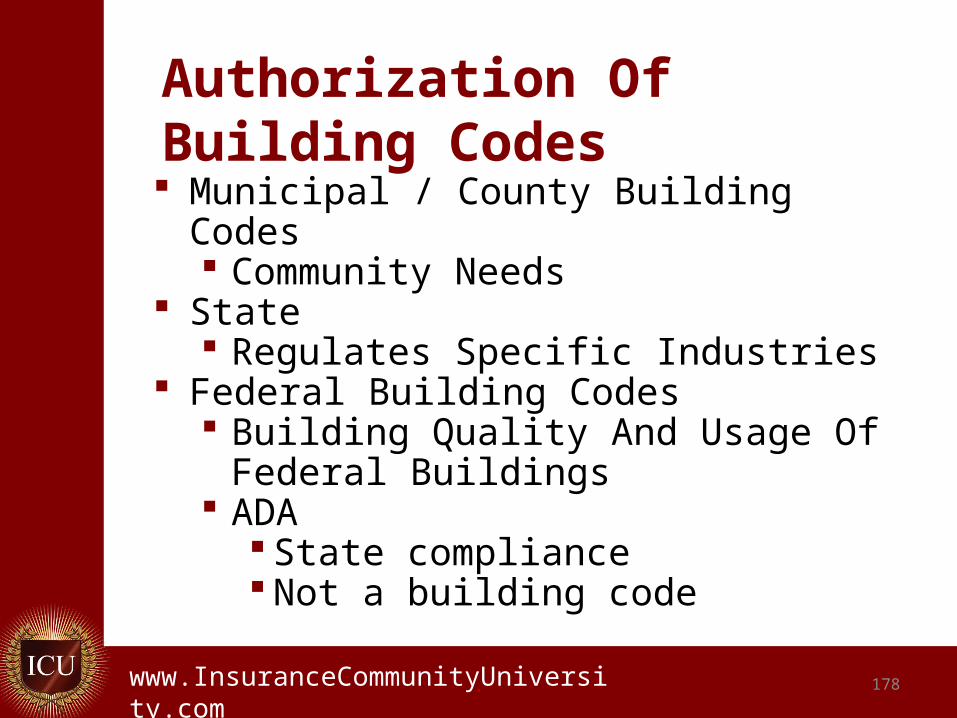

Authorization Of Building Codes Municipal / County Building Codes

Community Needs State

Regulates Specific Industries Federal Building Codes

Building Quality And Usage Of Federal Buildings

ADA State compliance Not a building code

.www.InsuranceCommunityUniversity.com 179

What Are Building Codes? Insulation Landscaping Signs Materials Used -

Occupancy Impact Parking ADA

Regulate Everything About Construction Plumbing Electrical Structural Support Grading Sloping Roofing Flooring

.www.InsuranceCommunityUniversity.com 180

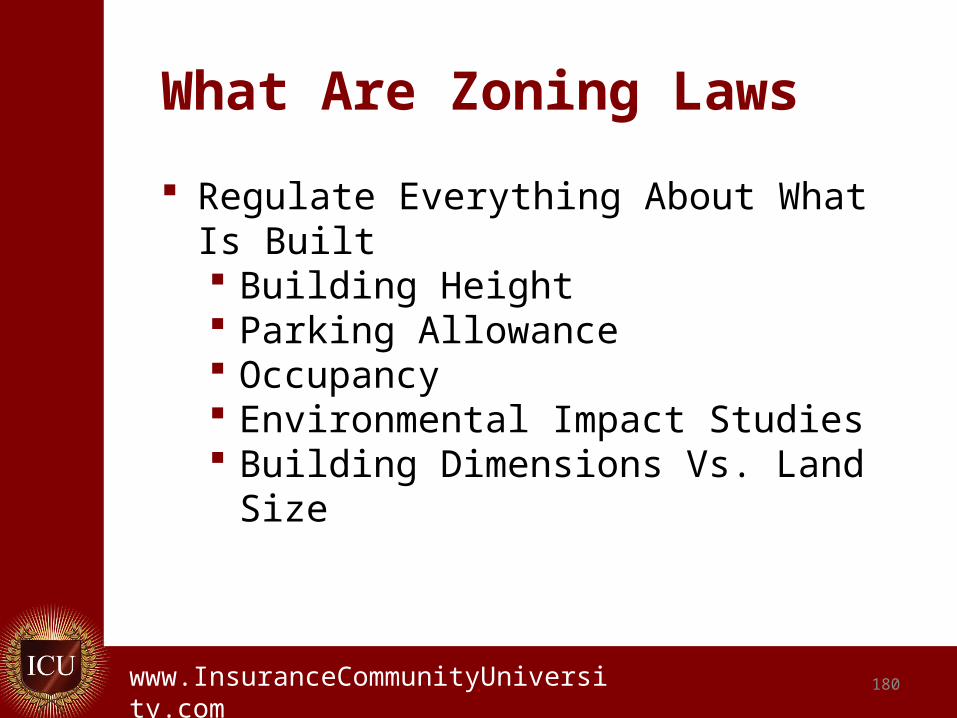

What Are Zoning Laws

Regulate Everything About What Is Built Building Height Parking Allowance Occupancy Environmental Impact Studies Building Dimensions Vs. Land Size

.www.InsuranceCommunityUniversity.com 181

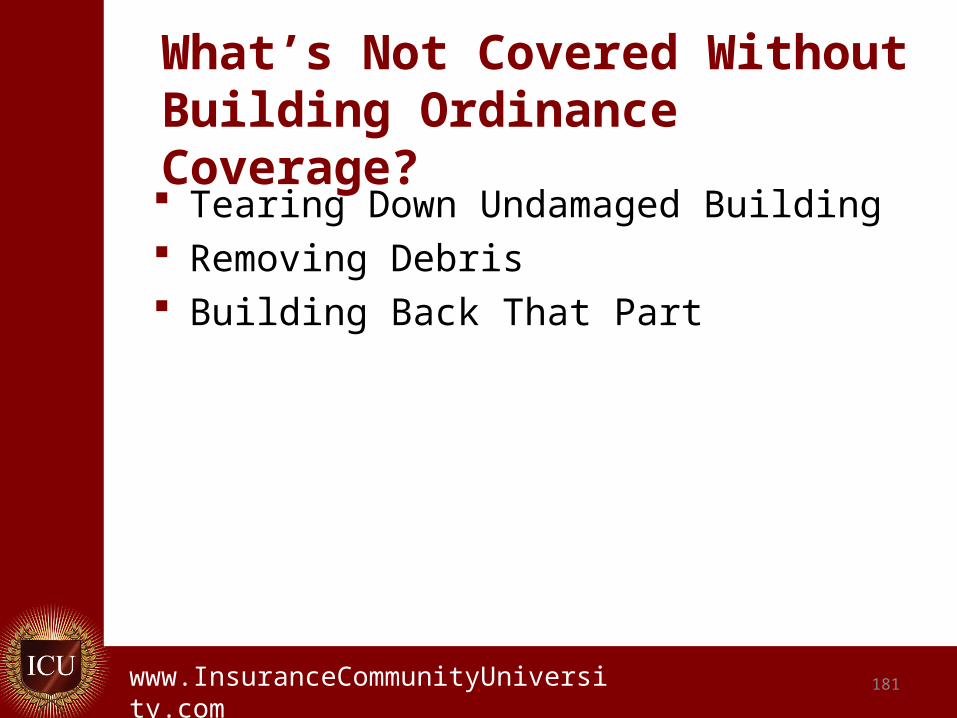

What’s Not Covered Without Building Ordinance Coverage? Tearing Down Undamaged Building Removing Debris Building Back That Part

.www.InsuranceCommunityUniversity.com 182

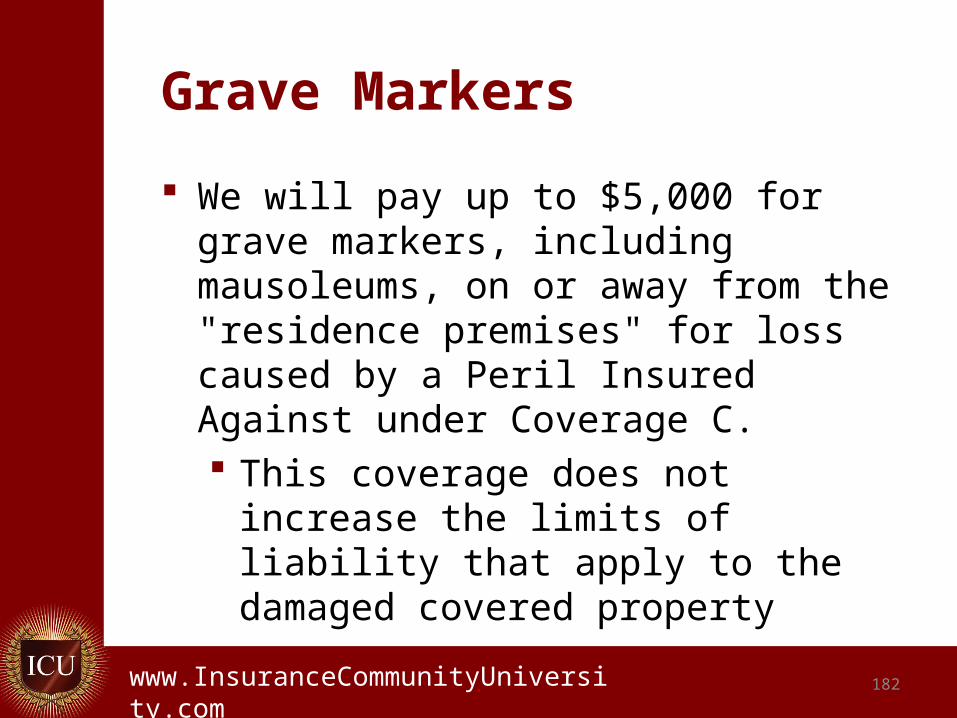

Grave Markers

We will pay up to $5,000 for grave markers, including mausoleums, on or away from the "residence premises" for loss caused by a Peril Insured Against under Coverage C. This coverage does not increase the

limits of liability that apply to the damaged covered property

.www.InsuranceCommunityUniversity.com

Perils of Insurance

183

.www.InsuranceCommunityUniversity.com 184

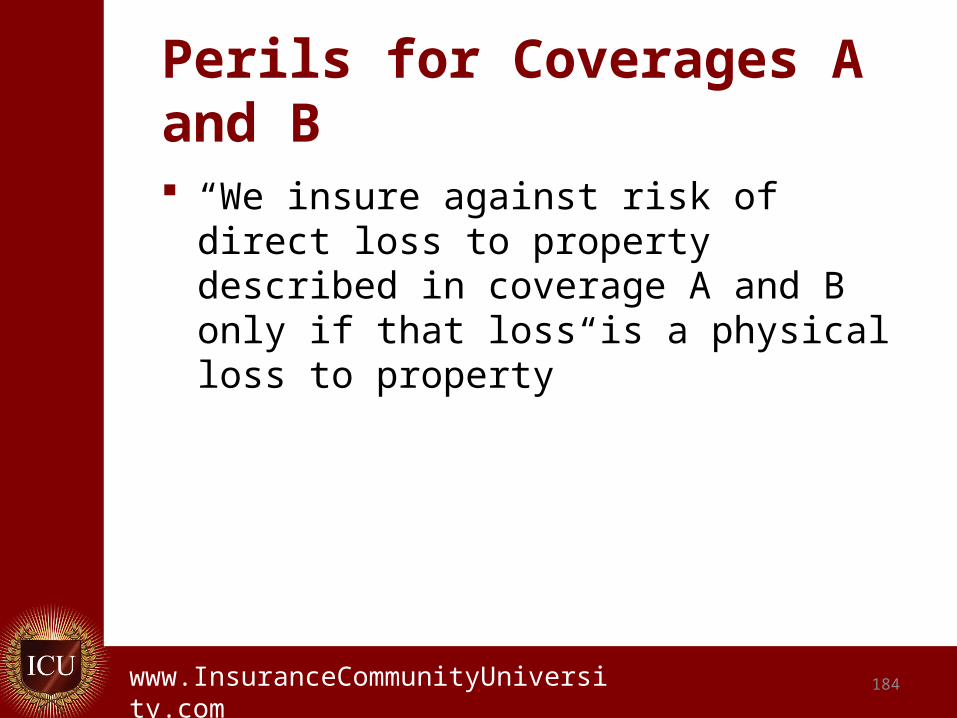

Perils for Coverages A and B

“We insure against risk of direct loss to property described in coverage A and B only if that loss is a physical loss to property”

.www.InsuranceCommunityUniversity.com 185

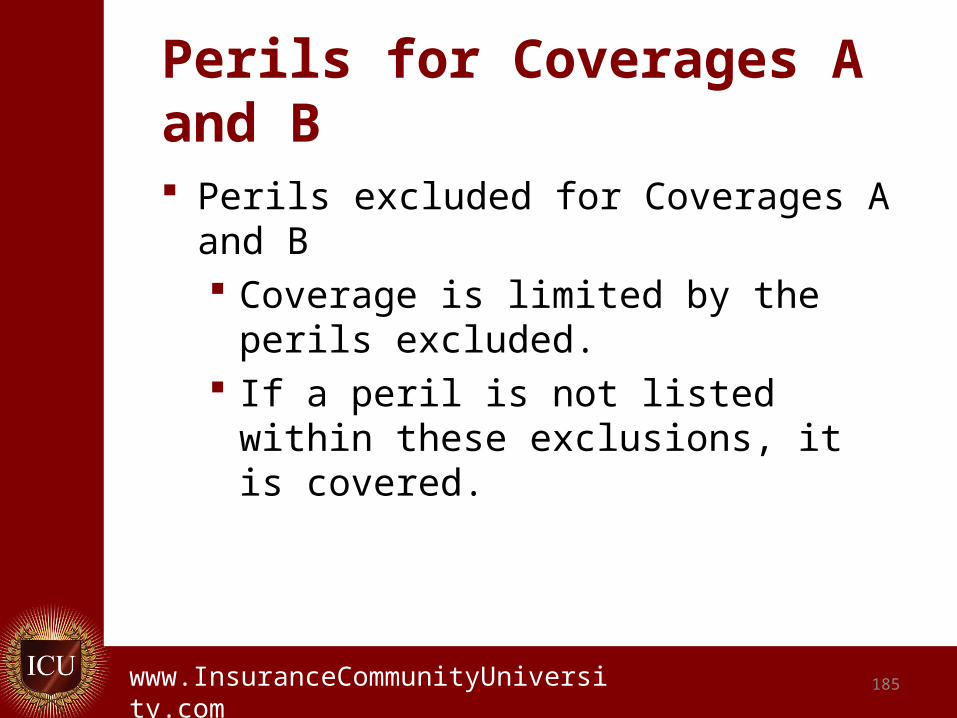

Perils for Coverages A and B

Perils excluded for Coverages A and B Coverage is limited by the perils

excluded. If a peril is not listed within these

exclusions, it is covered.

.www.InsuranceCommunityUniversity.com 186

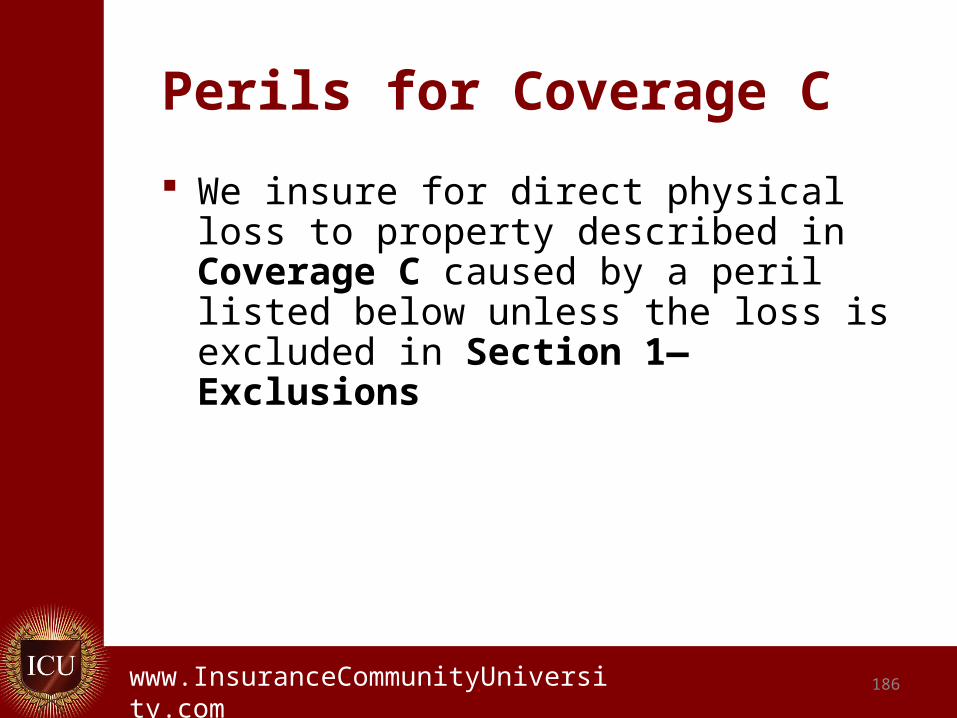

Perils for Coverage C

We insure for direct physical loss to property described in Coverage C caused by a peril listed below unless the loss is excluded in Section 1—Exclusions

.www.InsuranceCommunityUniversity.com 187

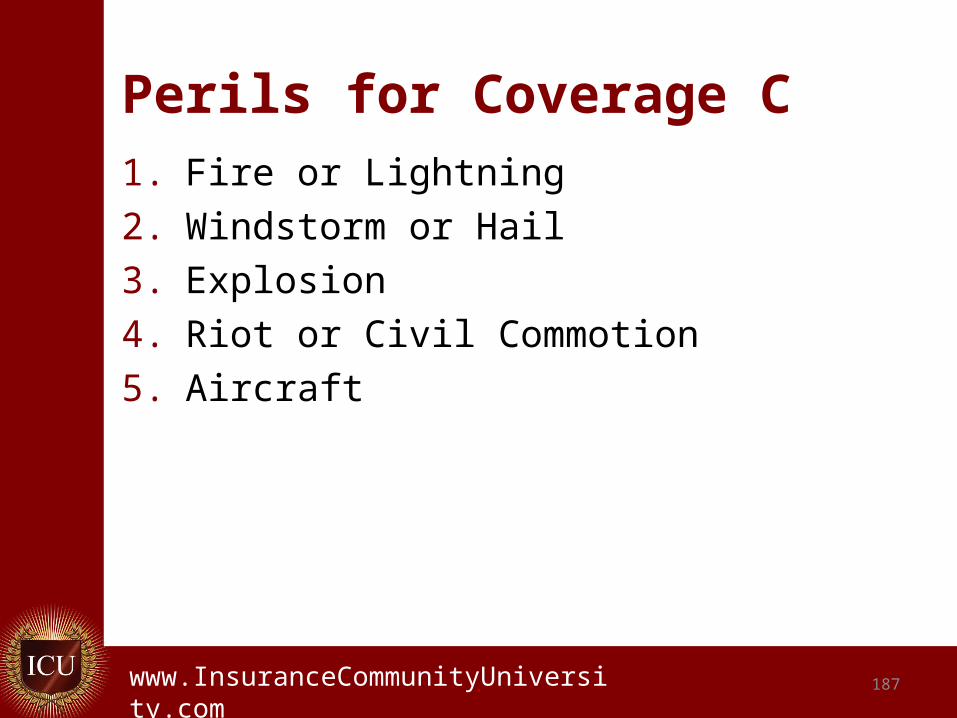

Perils for Coverage C1. Fire or Lightning

2. Windstorm or Hail

3. Explosion

4. Riot or Civil Commotion

5. Aircraft

.www.InsuranceCommunityUniversity.com 188

Perils for Coverage C6. Vehicles

7. Smoke

8. Vandalism or Malicious Mischief

9. Theft

10. Falling Objects

11. Weight of Ice, Snow, or Sleet

.www.InsuranceCommunityUniversity.com 189

Perils for Coverage C12. Accidental Discharge or Overflow of

Water or Steam

13. Sudden and Accidental Tearing Apart, Cracking, Burning, or Bulging or a Steam, Hot Water, Air Conditioning or Automatic Sprinkler System, or Appliance for Heating Water

.www.InsuranceCommunityUniversity.com 190

Perils for Coverage C

14. Freezing

15. Sudden and Accidental Damage from Artificially Generated Electrical Current

16. Damage by glass or safety glazing material

17. Volcanic Eruption

.www.InsuranceCommunityUniversity.com

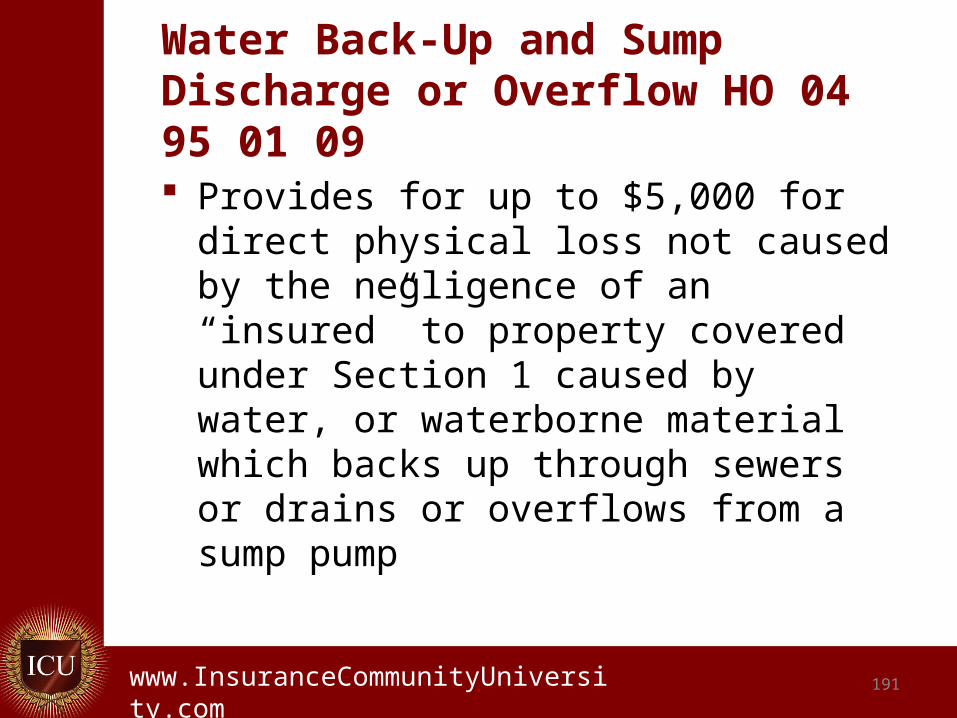

Water Back-Up and Sump Discharge or Overflow HO 04 95 01 09

Provides for up to $5,000 for direct physical loss not caused by the negligence of an “insured” to property covered under Section 1 caused by water, or waterborne material which backs up through sewers or drains or overflows from a sump pump

191

.www.InsuranceCommunityUniversity.com 192

Theft Peril Limitations and Exclusions

Theft committed by an insured. Theft in or to a building under

construction, including construction materials and supplies, that occurs before the building is completed and occupied.

.www.InsuranceCommunityUniversity.com 193

Theft Peril Limitations and Exclusions

Theft from any part of the residence premises rented to someone other than an insured.

Theft of covered property from a secondary residence that the insured owns, rents, or occupies except while an insured is temporarily living there.

.www.InsuranceCommunityUniversity.com 194

Section I--Exclusions

1. Ordinance or law

2. Earth movement

3. Water damage

4. Power failure

5. Neglect

6. War

7. Nuclear hazard

8. Intentional loss

9. Governmental Action

.www.InsuranceCommunityUniversity.com 195

Section I--Exclusions

a. Weather Conditionsb. Acts or decisions including the failure to actc. Faulty, inadequate or defective:

Planning, zoning, development, surveying, siting Design, specifications, workmanship, repair,

construction, renovation, remodeling, grading, compaction

Materials used in repair, construction, renovation or remodeling; or Maintenance

.www.InsuranceCommunityUniversity.com 196

Power Failure

H0 04 98-Refrigerated Property Provides coverage for spoilage due to

power failure or mechanical breakdown of the refrigerator or freezer for a specified dollar amount.

.www.InsuranceCommunityUniversity.com

Conditions

A. Insurable Interest and Limit of Liability

B. Duties After the Loss

C. Loss Settlement

D. Loss to a Pair or Set

E. Appraisals

F. Other Insurance and Service Agreement

G. Suit Against Us

H. Our Option

197

.www.InsuranceCommunityUniversity.com

ConditionsI. Loss Payment

J. Abandonment of Property

K. Mortgagee Clause

L. No Benefit to Bailee

M. Nuclear Hazard Clause

N. Recovered Property

O. Volcanic Eruption Period

198

.www.InsuranceCommunityUniversity.com

Conditions

P. Policy Period

Q. Concealment or Fraud

R. Loss Payable Clause

199

.www.InsuranceCommunityUniversity.com 200

Section II—Liability Coverages

.www.InsuranceCommunityUniversity.com

Section II Liability

Coverage E—Personal Liability If a claim is made or a suit is brought

against an “insured” for damages because of “bodily injury” of “property damage” caused by an “occurrence” to which this coverage applies ,we will

201

.www.InsuranceCommunityUniversity.com

Section II Liability

1. Pay up to our limit of liability for the damages for which an “insured” is legally liable. Damages include prejudgment interest awarded against an “insured” and

2. Provide a defense at our expense by counsel of our choice, even if the suit is groundless, false or fraudulent We may investigate and settle any claim or suit that we decide is appropriate. Our duty to settle or defend ends when our limit of liability for the “occurrence” has been exhausted by payment of a judgment or settlement.

202

.www.InsuranceCommunityUniversity.com 203

Who Is an Insured for Section II - Liability Coverage?

The named insured’s spouse, if a resident of the same household. Note that it is always correct to show

both spouses as named insureds, even if only one of them is on the deed.

Show the “owner” on the first line with the correct trust deed ownership information and then the second spouse.

.www.InsuranceCommunityUniversity.com 204

Who Is an Insured for Section II - Liability Coverage?

Relatives of the named insured, if residents of the same household.

Anyone under the age of 21, if in the care of the named insured or resident relative and if residents of the same household.

.www.InsuranceCommunityUniversity.com 205

Coverage E – Personal Liability

It also may be extended beyond bodily injury and property damage to include liability for personal injury with the personal injury endorsement (HO 24 82).

.www.InsuranceCommunityUniversity.com 206

Liability Coverages

Coverage F—Medical Payments To Others To others Incurred within three years Reasonable charges

On the “insured location”: Persons on the insured location with

the insured’s permission.

.www.InsuranceCommunityUniversity.com 207

Coverage F – Medical Payments to Others Off the “insured location”:

Arises out of a condition on the insured location or adjoining ways.

Is caused by the activities of an insured. Is caused by a residence employee in the

course of employment by an insured. Is caused by an animal owned by or in the care

of an insured.

.www.InsuranceCommunityUniversity.com 208

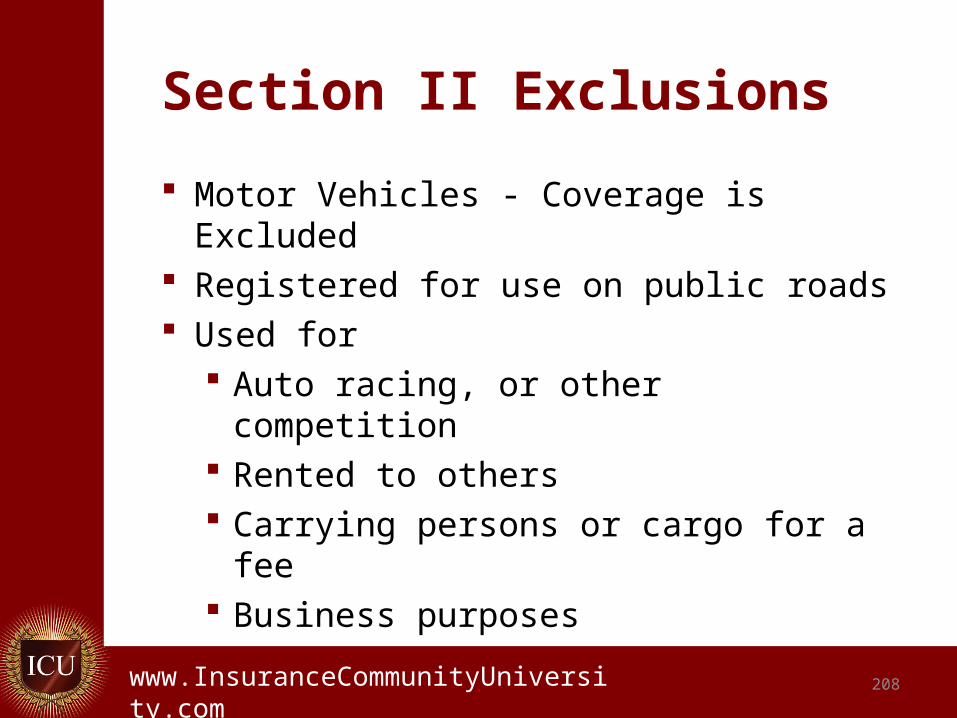

Section II Exclusions

Motor Vehicles - Coverage is Excluded Registered for use on public roads Used for

Auto racing, or other competition Rented to others Carrying persons or cargo for a fee Business purposes

.www.InsuranceCommunityUniversity.com 209

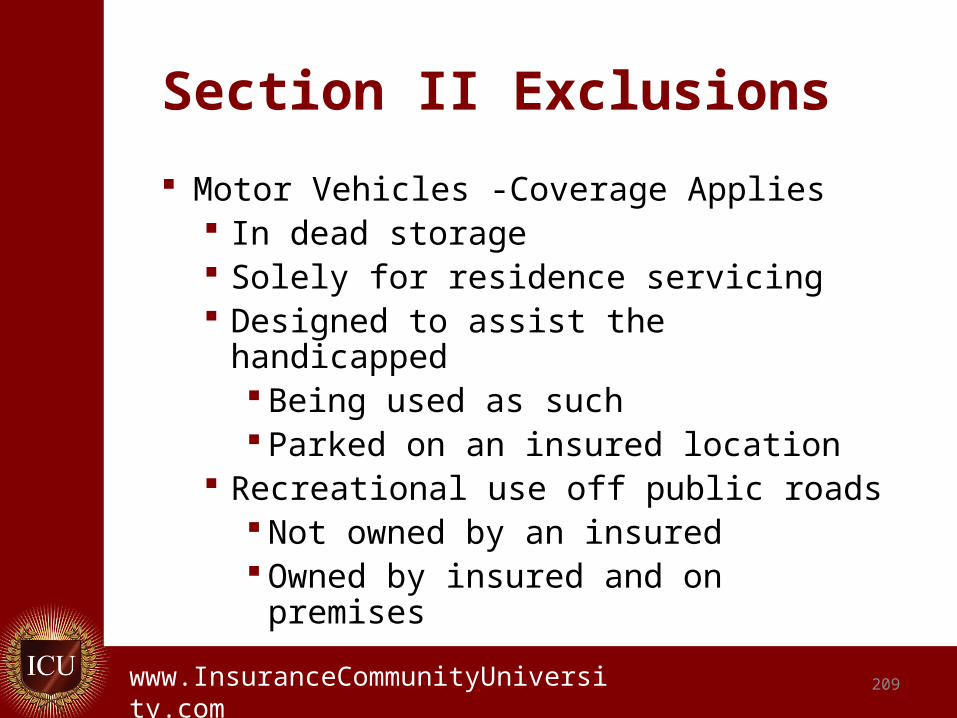

Section II Exclusions

Motor Vehicles -Coverage Applies In dead storage Solely for residence servicing Designed to assist the handicapped

Being used as such Parked on an insured location

Recreational use off public roads Not owned by an insured Owned by insured and on premises

.www.InsuranceCommunityUniversity.com 210

Section II Exclusions

Motorized golf carts – coverage applies Parked at a golf course In use at a golf course Travel to and from the course Crossing roads in the course of play Private residential community

.www.InsuranceCommunityUniversity.com 211

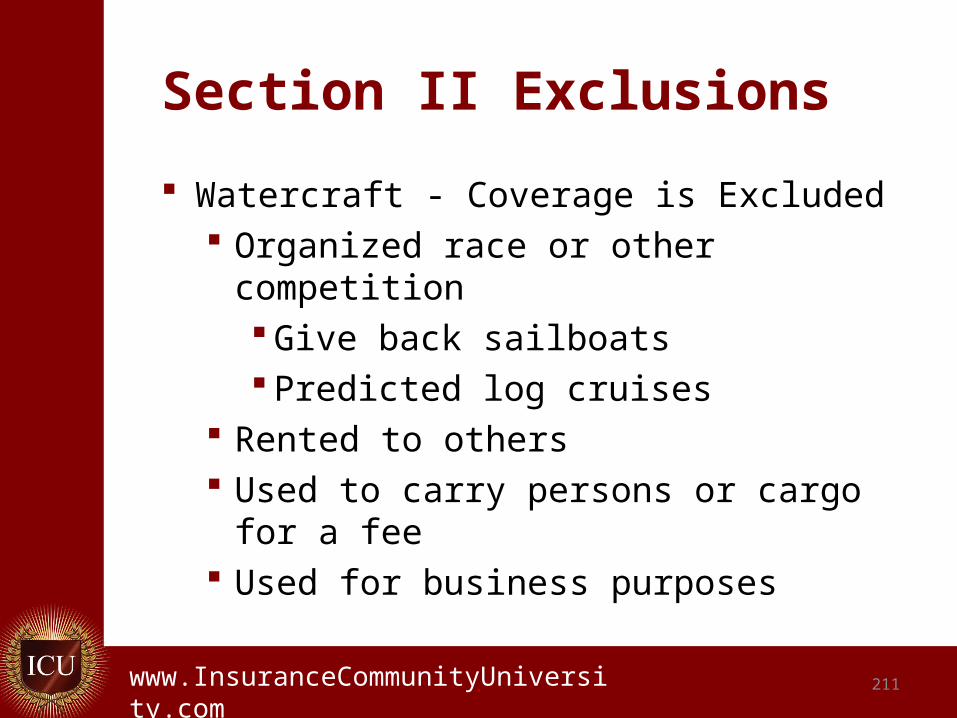

Section II Exclusions

Watercraft - Coverage is Excluded Organized race or other competition

Give back sailboats Predicted log cruises

Rented to others Used to carry persons or cargo for a fee Used for business purposes

.www.InsuranceCommunityUniversity.com 212

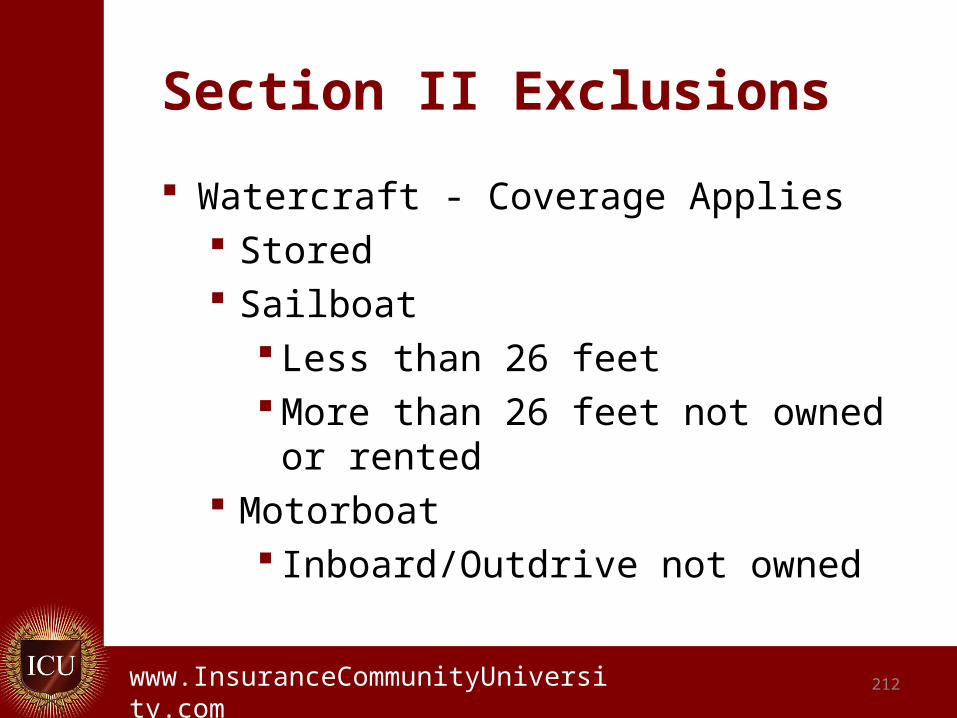

Section II Exclusions

Watercraft - Coverage Applies Stored Sailboat

Less than 26 feet More than 26 feet not owned or

rented Motorboat

Inboard/Outdrive not owned

.www.InsuranceCommunityUniversity.com 213

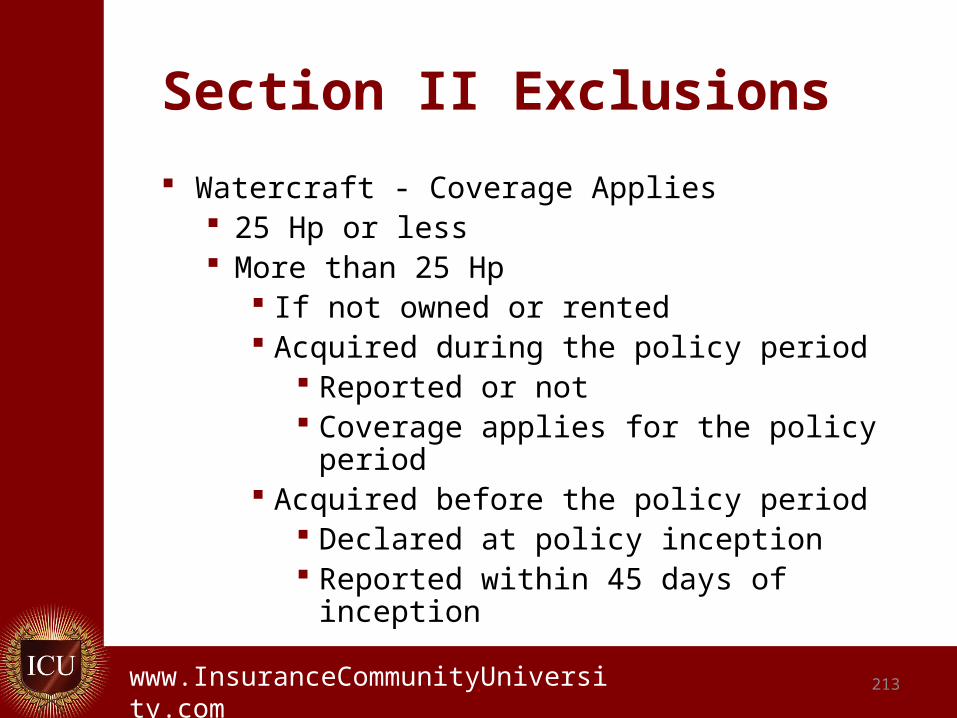

Section II Exclusions

Watercraft - Coverage Applies 25 Hp or less More than 25 Hp

If not owned or rented Acquired during the policy period

Reported or not Coverage applies for the policy period

Acquired before the policy period Declared at policy inception Reported within 45 days of inception

.www.InsuranceCommunityUniversity.com 214

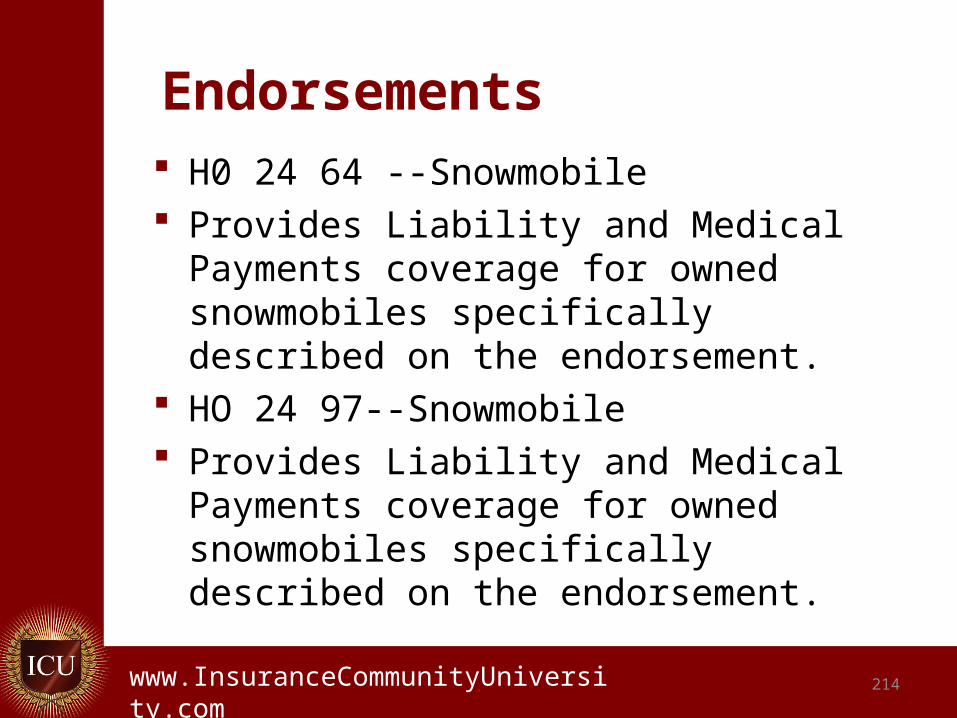

Endorsements H0 24 64 --Snowmobile Provides Liability and Medical Payments

coverage for owned snowmobiles specifically described on the endorsement.

HO 24 97--Snowmobile Provides Liability and Medical Payments

coverage for owned snowmobiles specifically described on the endorsement.

.www.InsuranceCommunityUniversity.com 215

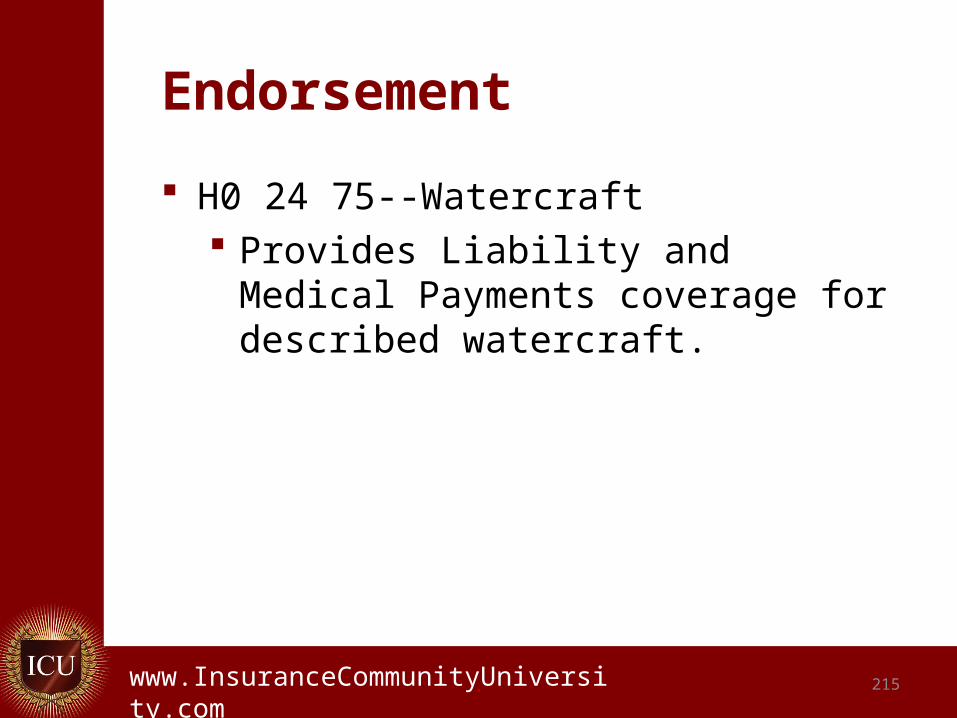

Endorsement

H0 24 75--Watercraft Provides Liability and Medical

Payments coverage for described watercraft.

.www.InsuranceCommunityUniversity.com 216

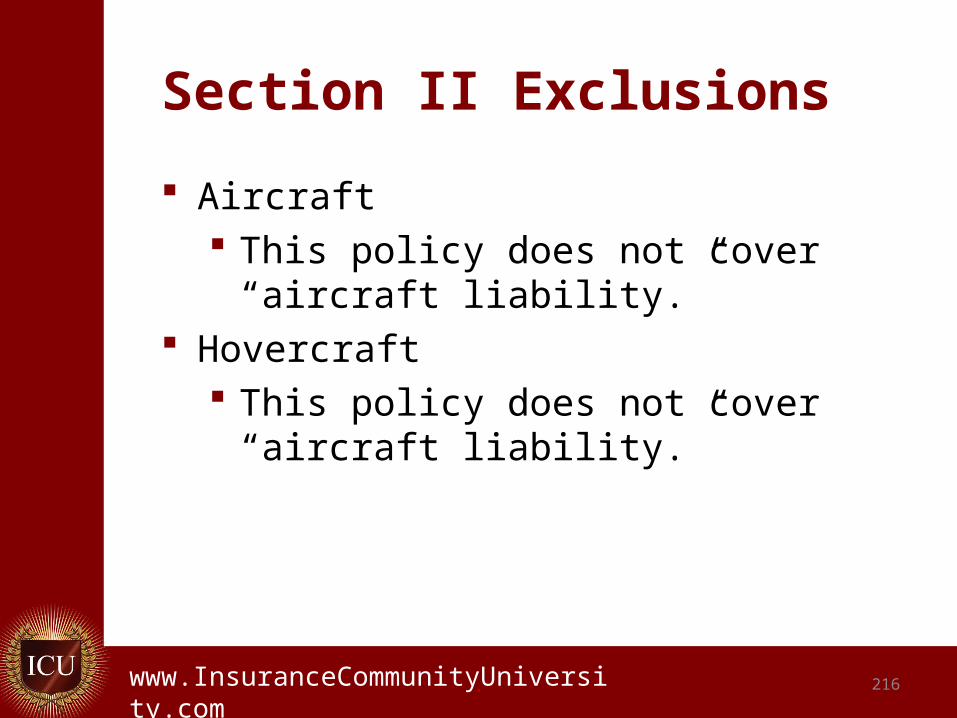

Section II Exclusions

Aircraft This policy does not cover “aircraft

liability.” Hovercraft

This policy does not cover “aircraft liability.”

.www.InsuranceCommunityUniversity.com 217

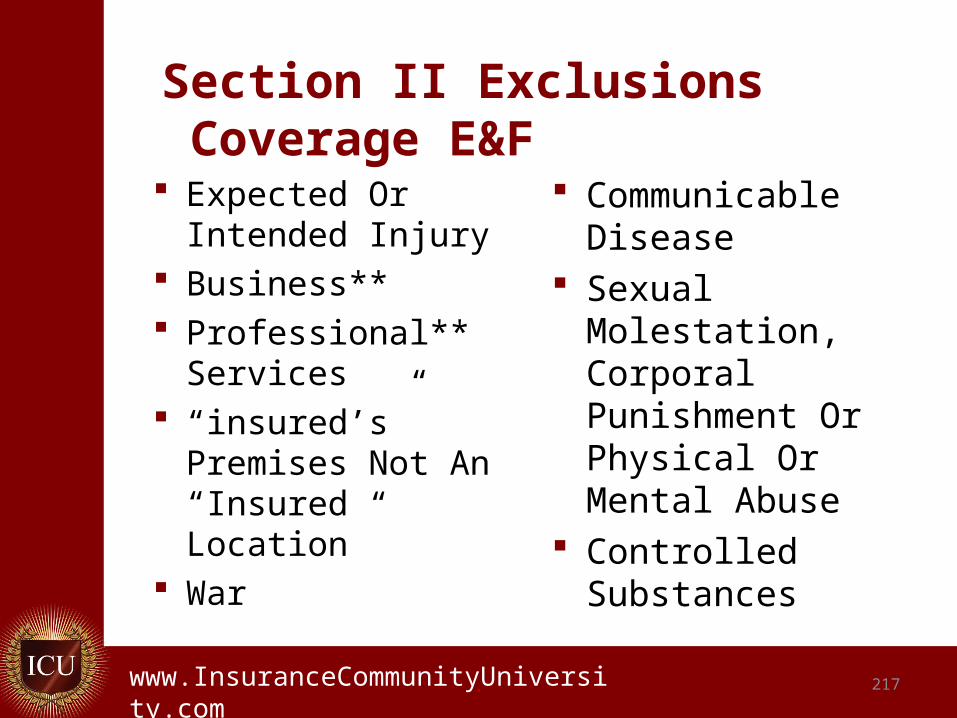

Section II Exclusions Coverage E&F Expected Or

Intended Injury Business** Professional**

Services “insured’s”

Premises Not An “Insured Location”

War

Communicable Disease

Sexual Molestation, Corporal Punishment Or Physical Or Mental Abuse

Controlled Substances

.www.InsuranceCommunityUniversity.com 218

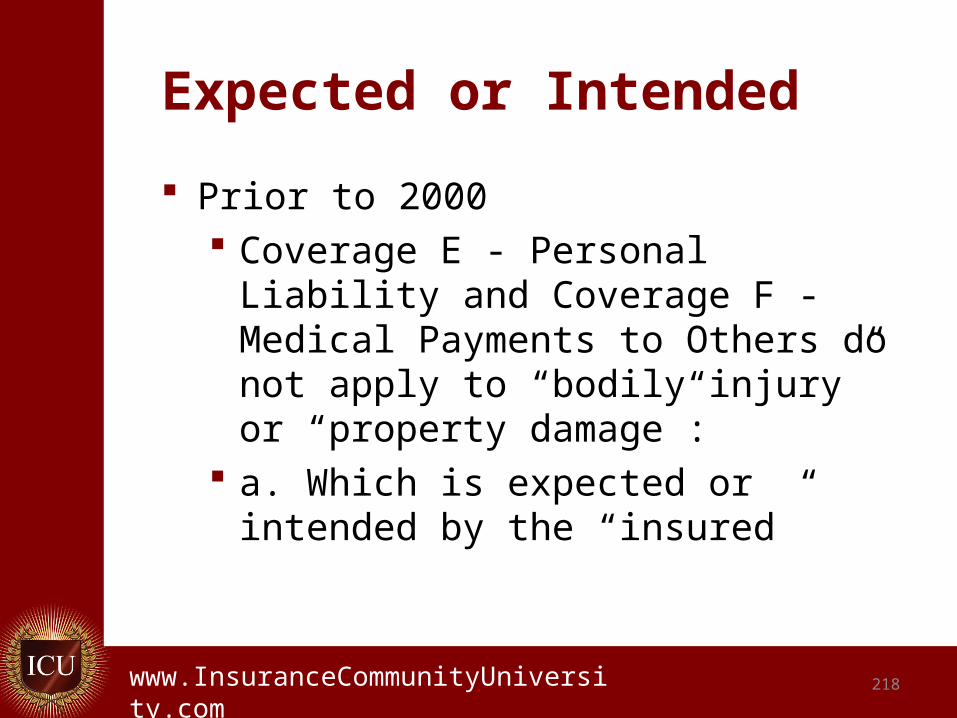

Expected or Intended

Prior to 2000 Coverage E - Personal Liability and

Coverage F - Medical Payments to Others do not apply to “bodily injury” or “property damage”:

a. Which is expected or intended by the “insured”

.www.InsuranceCommunityUniversity.com 219

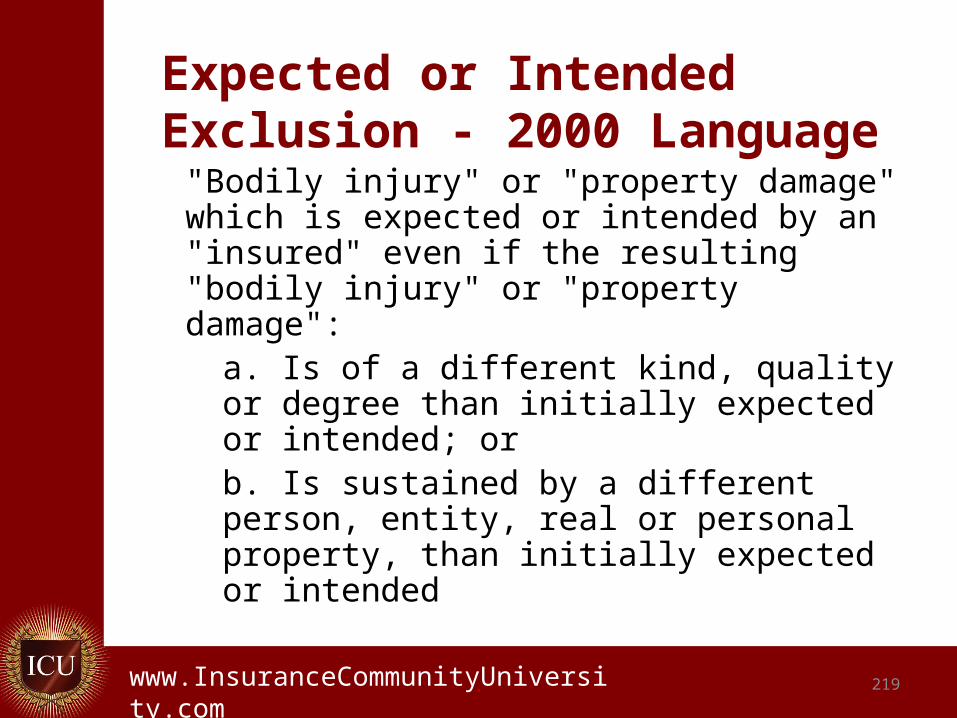

Expected or Intended Exclusion - 2000 Language

"Bodily injury" or "property damage" which is expected or intended by an "insured" even if the resulting "bodily injury" or "property damage":

a. Is of a different kind, quality or degree than initially expected or intended; orb. Is sustained by a different person, entity, real or personal property, than initially expected or intended

.www.InsuranceCommunityUniversity.com 220

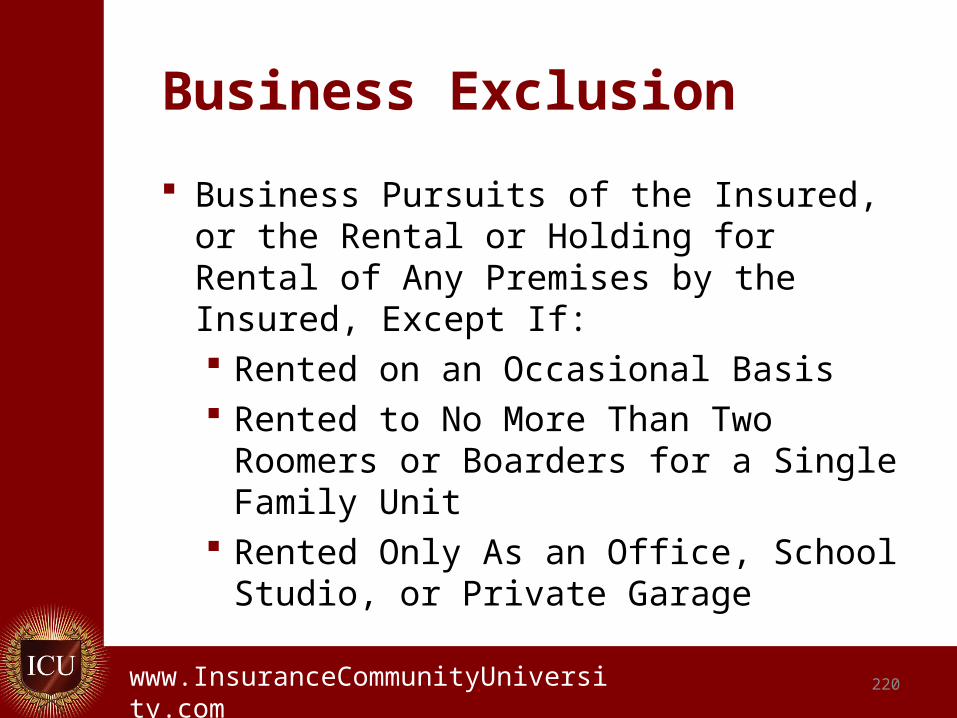

Business Exclusion

Business Pursuits of the Insured, or the Rental or Holding for Rental of Any Premises by the Insured, Except If: Rented on an Occasional Basis Rented to No More Than Two Roomers

or Boarders for a Single Family Unit Rented Only As an Office, School

Studio, or Private Garage

.www.InsuranceCommunityUniversity.com

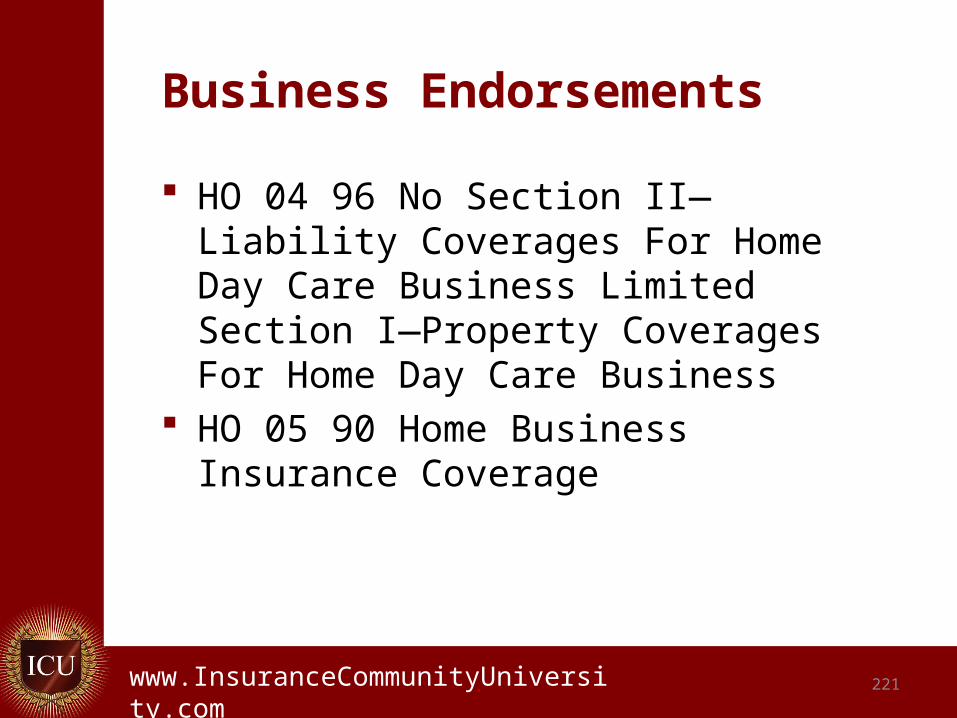

Business Endorsements

HO 04 96 No Section II—Liability Coverages For Home Day Care Business Limited Section I—Property Coverages For Home Day Care Business

HO 05 90 Home Business Insurance Coverage

221

.www.InsuranceCommunityUniversity.com

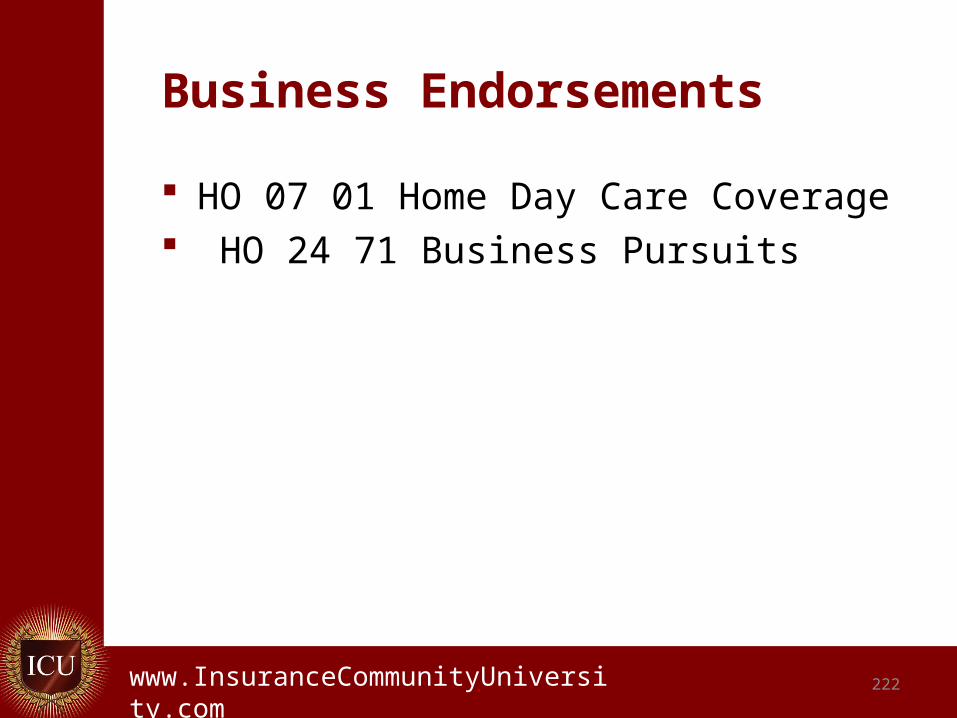

Business Endorsements

HO 07 01 Home Day Care Coverage HO 24 71 Business Pursuits

222

.www.InsuranceCommunityUniversity.com 223

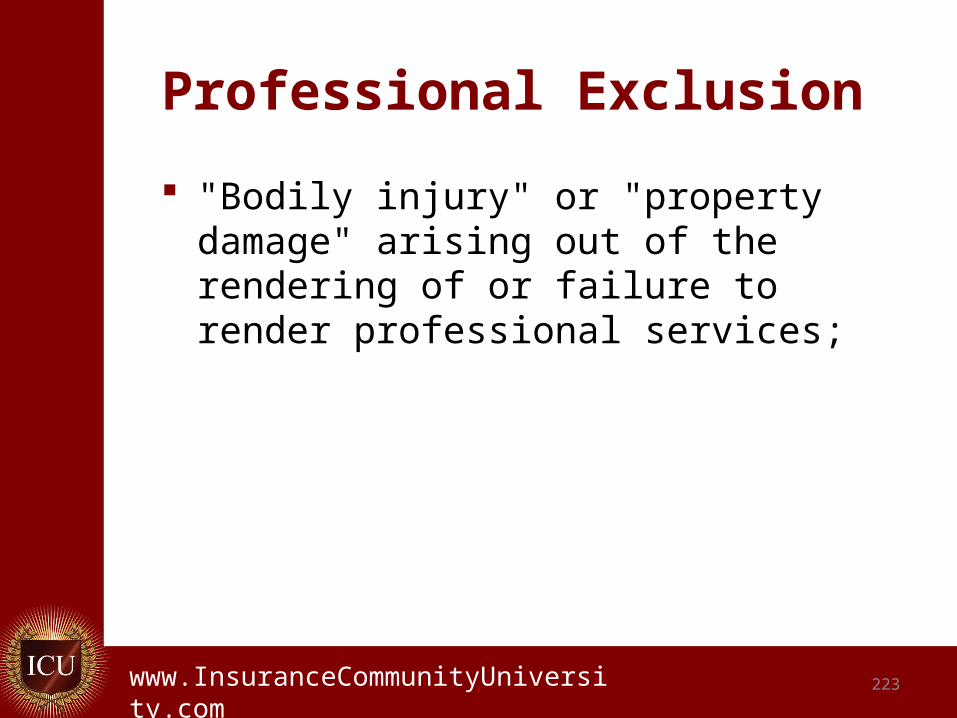

Professional Exclusion

"Bodily injury" or "property damage" arising out of the rendering of or failure to render professional services;

.www.InsuranceCommunityUniversity.com 224

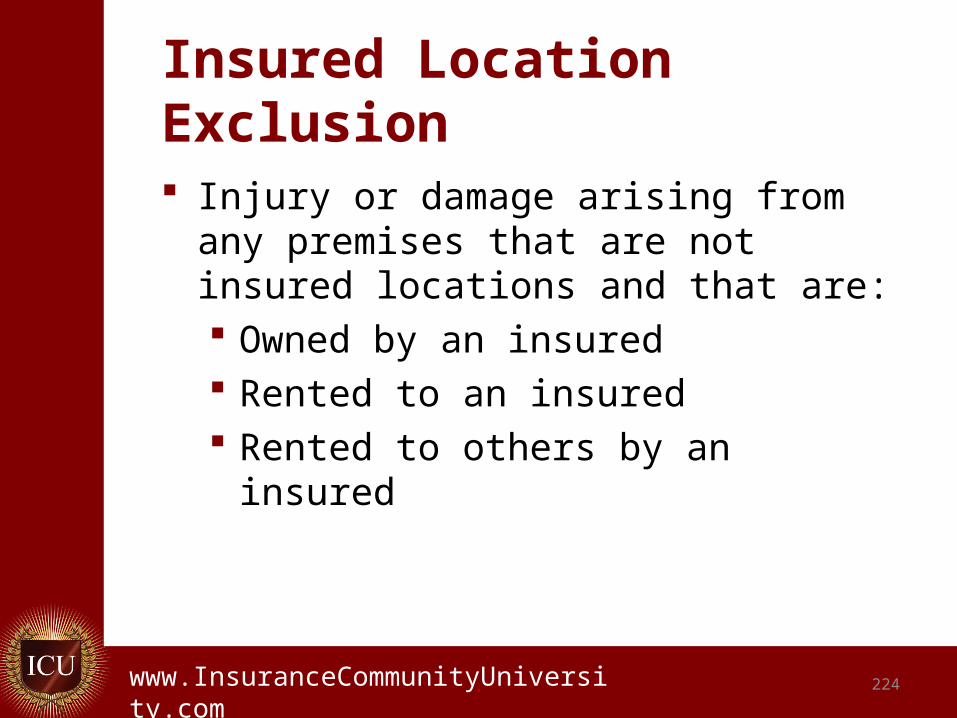

Insured Location Exclusion

Injury or damage arising from any premises that are not insured locations and that are: Owned by an insured Rented to an insured Rented to others by an insured

.www.InsuranceCommunityUniversity.com 225

Communicable Disease Exclusion

Communicable Disease "Bodily injury" or "property damage"

which arises out of the transmission of a communicable disease by an "insured;"

.www.InsuranceCommunityUniversity.com 226

Sexual Molestation Exclusion

Sexual Molestation, Corporal Punishment Or Physical Or Mental Abuse "Bodily injury" or "property damage"

arising out of sexual molestation, corporal punishment or physical or mental abuse; or

.www.InsuranceCommunityUniversity.com 227

Controlled Substances Exclusion

Controlled Substance "Bodily injury" or "property damage" arising out

of the use, sale, manufacture, delivery, transfer or possession by any person of a Controlled Substance as defined by the Federal Food and Drug Law at 21 U.S.C.A. Sections 811 and 812. Controlled Substances include but are not limited to cocaine, LSD, marijuana and all narcotic drugs. However, this exclusion does not apply to the legitimate use of prescription drugs by a person following the orders of a licensed physician.

.www.InsuranceCommunityUniversity.com 228

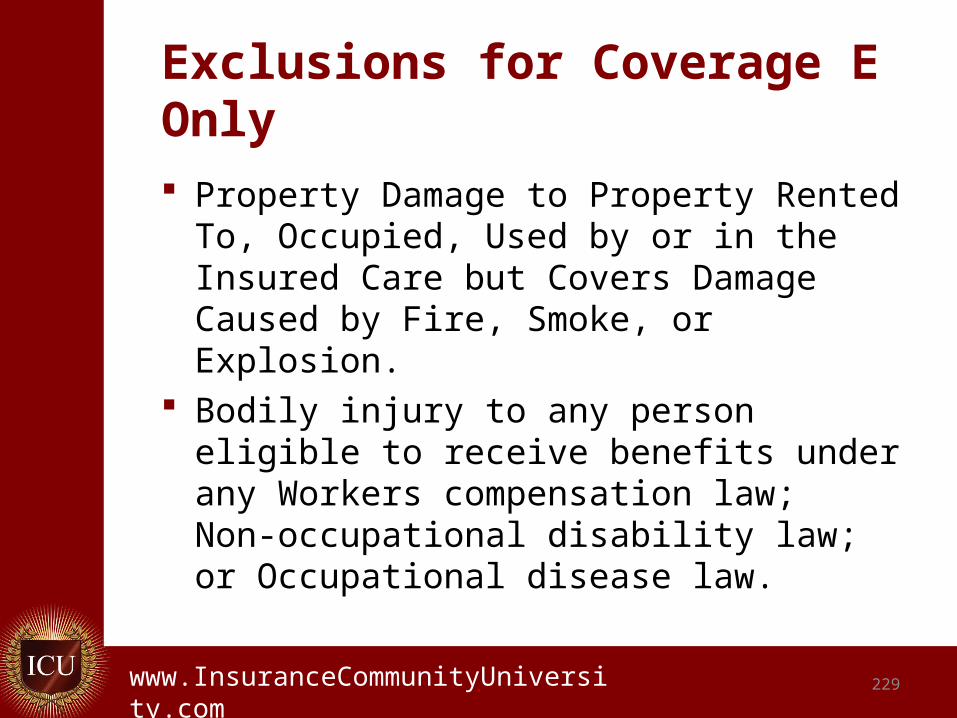

Exclusions for Coverage E Only

Personal Liability Does Not Apply To: Liability for the insured’s share in any

loss assessment as a member of an association, corporation, or community of property owners.

Liability assumed under any contract or agreement.

Property damage to property owned by the insured.

.www.InsuranceCommunityUniversity.com 229

Exclusions for Coverage E Only

Property Damage to Property Rented To, Occupied, Used by or in the Insured Care but Covers Damage Caused by Fire, Smoke, or Explosion.

Bodily injury to any person eligible to receive benefits under any Workers compensation law; Non-occupational disability law; or Occupational disease law.

.www.InsuranceCommunityUniversity.com 230

Exclusions for Coverage E Only

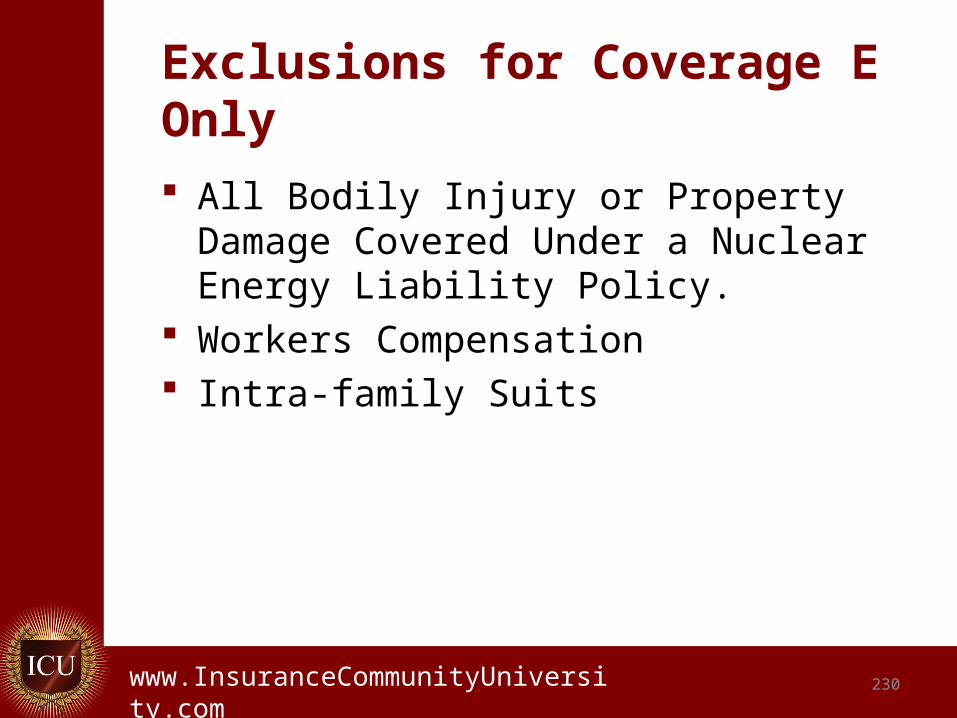

All Bodily Injury or Property Damage Covered Under a Nuclear Energy Liability Policy.

Workers Compensation Intra-family Suits

.www.InsuranceCommunityUniversity.com 231

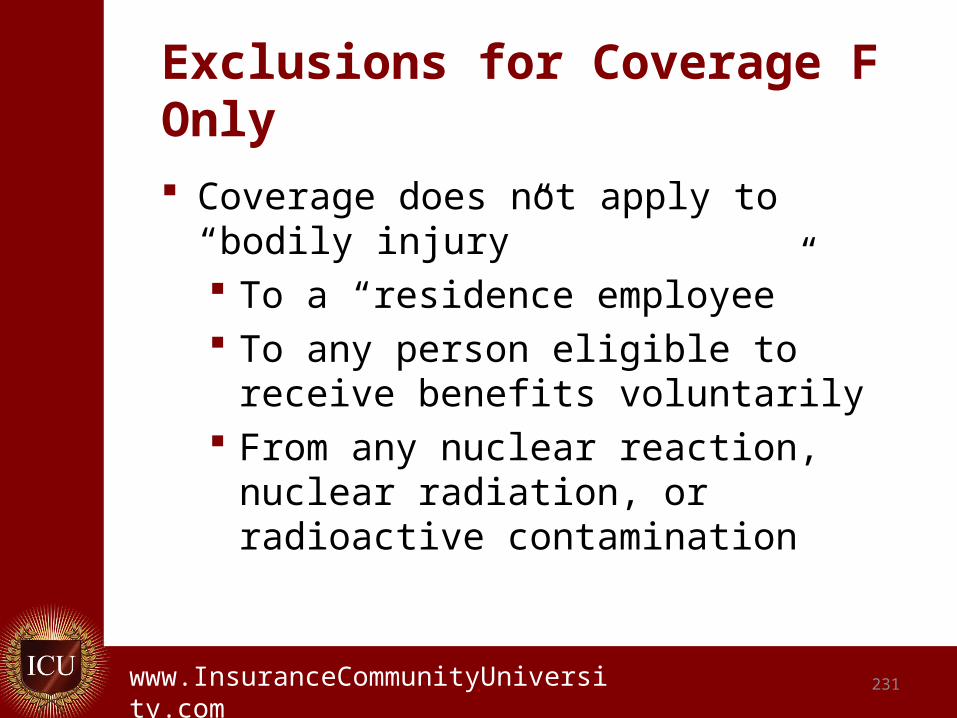

Exclusions for Coverage F Only

Coverage does not apply to “bodily injury” To a “residence employee” To any person eligible to receive

benefits voluntarily From any nuclear reaction, nuclear

radiation, or radioactive contamination

.www.InsuranceCommunityUniversity.com 232

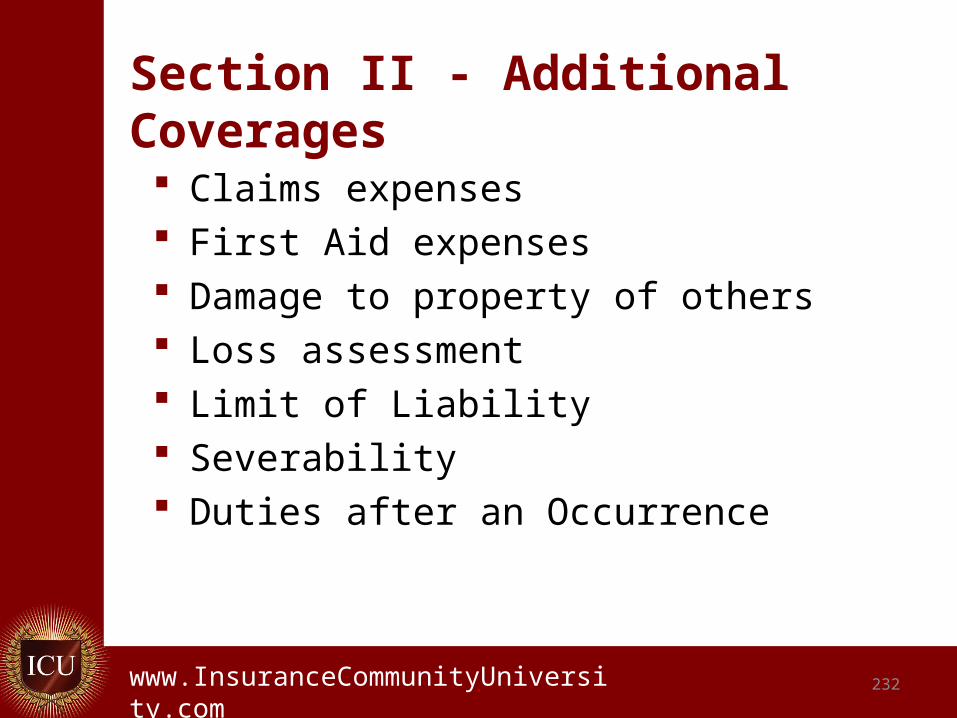

Section II - Additional Coverages

Claims expenses First Aid expenses Damage to property of others Loss assessment Limit of Liability Severability Duties after an Occurrence

.www.InsuranceCommunityUniversity.com 233

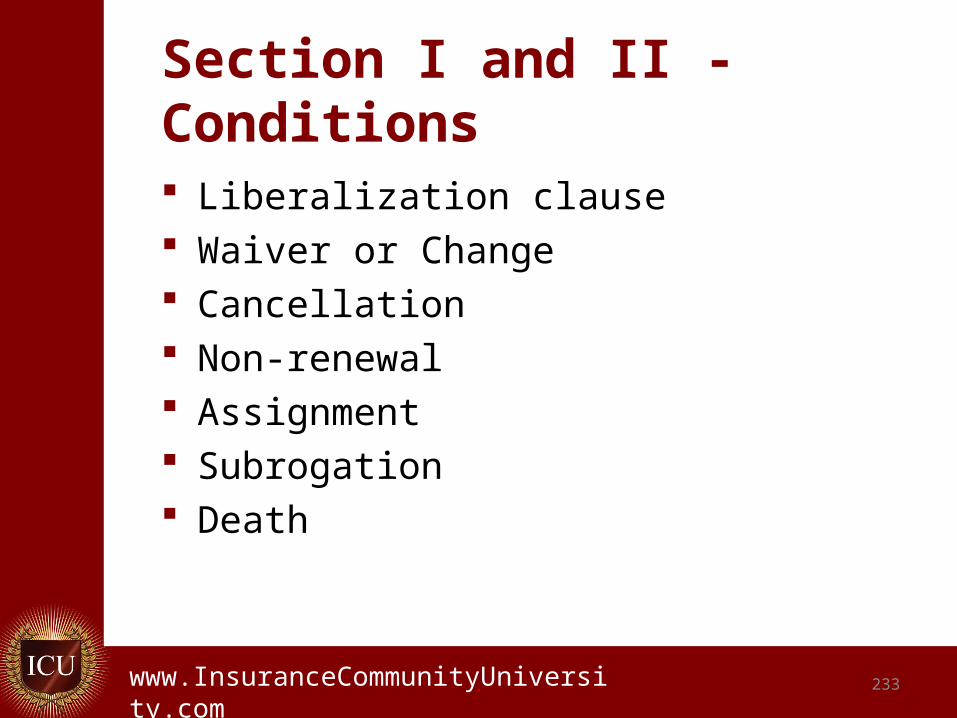

Section I and II - Conditions

Liberalization clause Waiver or Change Cancellation Non-renewal Assignment Subrogation Death

.www.InsuranceCommunityUniversity.com 234

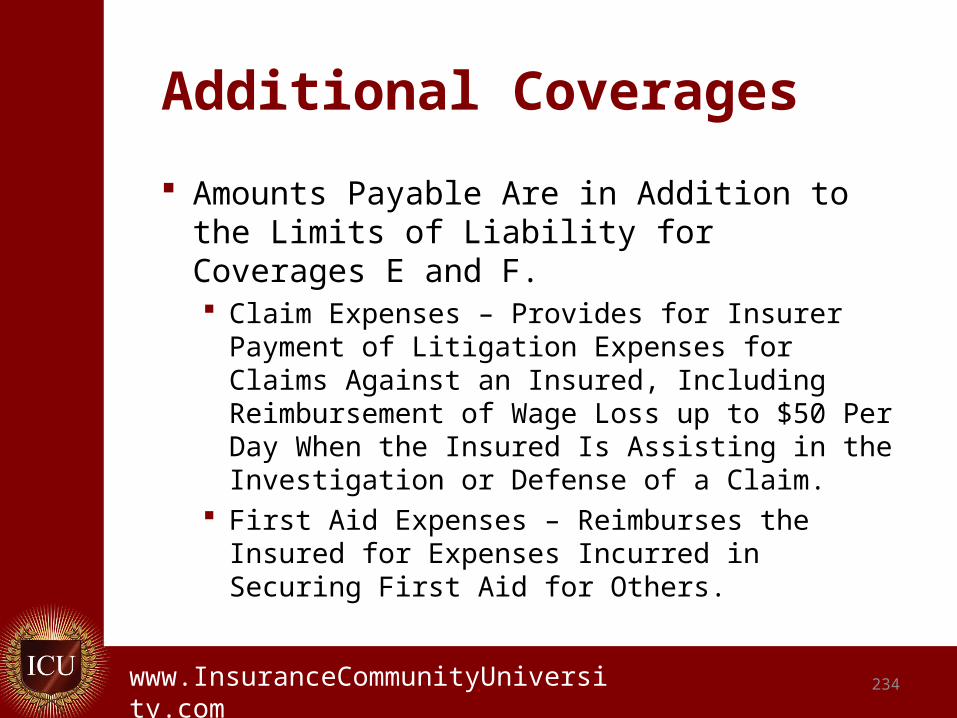

Additional Coverages

Amounts Payable Are in Addition to the Limits of Liability for Coverages E and F. Claim Expenses – Provides for Insurer

Payment of Litigation Expenses for Claims Against an Insured, Including Reimbursement of Wage Loss up to $50 Per Day When the Insured Is Assisting in the Investigation or Defense of a Claim.

First Aid Expenses – Reimburses the Insured for Expenses Incurred in Securing First Aid for Others.

.www.InsuranceCommunityUniversity.com 235

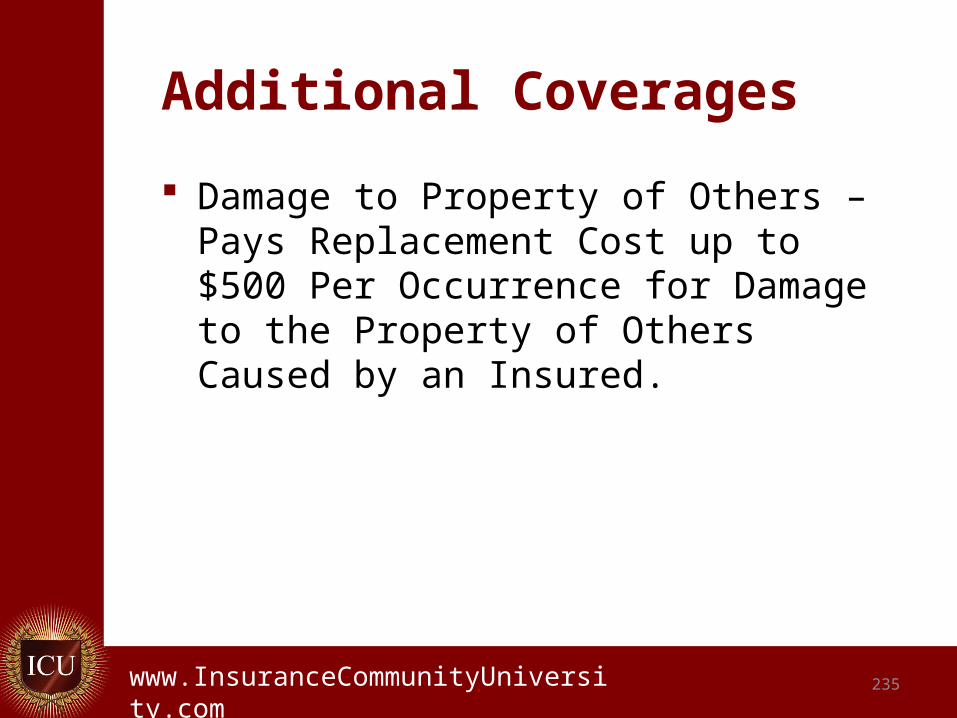

Additional Coverages

Damage to Property of Others – Pays Replacement Cost up to $500 Per Occurrence for Damage to the Property of Others Caused by an Insured.

.www.InsuranceCommunityUniversity.com 236

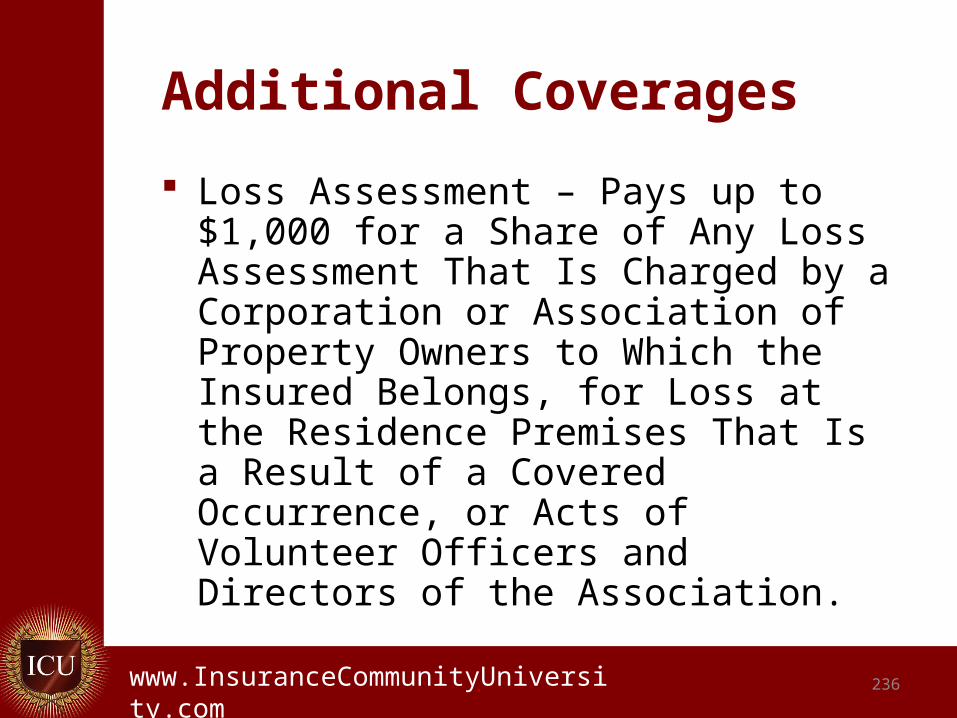

Additional Coverages

Loss Assessment – Pays up to $1,000 for a Share of Any Loss Assessment That Is Charged by a Corporation or Association of Property Owners to Which the Insured Belongs, for Loss at the Residence Premises That Is a Result of a Covered Occurrence, or Acts of Volunteer Officers and Directors of the Association.

.www.InsuranceCommunityUniversity.com 237

Severability of Insurance Conditions of Section II Severability of insurance

States that the insurance applies separately to each insured. Therefore, each insured is treated as

though he or she has separate coverage under the policy.

However, the limit of liability per occurrence remains the same regardless of the number of insureds.

.www.InsuranceCommunityUniversity.com 238

Owned Motorized Golf Cart Physical Loss Coverage - HO 05 28 10 00

Scheduled limit applies. Parts and accessories are covered, but only

up to 10% of the limit for the cart. Golf Cart" means a motorized conveyance

that is: Designed to carry up to four people on a golf

course for the purpose of playing golf. Speed maximum of 25 miles per hour on level

ground.

.www.InsuranceCommunityUniversity.com 239

Home Business Insurance Coverage - HO 07 01 10 00 Additional Definitions of “advertisement” has been

added. "Advertisement" means a notice that is broadcast

or published to the general public or specific market segments about your goods, products or services for the purpose of attracting customers or supporters.

Definition of Personal and Advertising Injury has been added.

This change conforms with the 1998 Commercial General Liability and further limits the response of the liability portion of this endorsement.

.www.InsuranceCommunityUniversity.com 240

Personal Injury - HO 24 82 10 00

This endorsement separates “personal injury” from the original policy definition of “bodily injury”.

The endorsement now contains a separate definition of “personal injury”.

Provides up to $1,000 of coverage for loss assessments.

Specifies that offenses relating to defamation apply to oral and written publications.

.www.InsuranceCommunityUniversity.com 241

Personal Injury - HO 24 82 10 00

Clarifies that the offenses of “wrongful eviction,” “wrongful entry” and “invasion of the right of private occupancy” apply to improper actions regarding a room, dwelling or premises.

New exclusion applies if the insured has knowledge that an action would violate the other person’s rights.

Excludes any loss arising out of pollution. A more detailed exclusion of knowledge of falsity

and loss arising out of a “criminal act” committed by or at the direction of the insured now applies.

.www.InsuranceCommunityUniversity.com

Insuring the Apartment Unit Risk

242

.www.InsuranceCommunityUniversity.com

Apartment

An apartment can pertain to many types of dwelling units. What they have in common is that they are “tenant” occupied. The owner of apartment units could occupy a unit for their own residence premises but they would then be the apartment owner.

243

.www.InsuranceCommunityUniversity.com

Apartment

An apartment building is a multi tenant housing building which has rental units that can be rented on a month to month basis or for a longer period of time.

Tenants may also enter into lease agreements which obligate them for a longer period of time

244

.www.InsuranceCommunityUniversity.com

Apartment

Tenant’s Responsibility Premises Liability Insurance Responsible for their own personal

property May be responsible for any alterations

or additions they add to rental units Insurance is written on an HO 04

245

.www.InsuranceCommunityUniversity.com

Apartment

Apartment Owner is responsible for: All building property All outdoor property All owned indoor property All furniture in furnished apartments All landscaping All common areas Own Liability

Insurance is written on an Apartment Package

246

.www.InsuranceCommunityUniversity.com

Insuring the Cooperative Risk

247

.www.InsuranceCommunityUniversity.com

Cooperatives

Cooperatives may look like an apartment house or a condominium

What distinguishes all of them is the “ownership” of the buildings and units.

In an apartment situation there is no sharing of the ownership of the building and common areas. The apartment owner owns the property solely and has sole responsibility to insure for the property.

248

.www.InsuranceCommunityUniversity.com

Cooperatives (Co-op)

The concept of cooperatives began in 1926 in New York. It is one of the oldest multi family type of housing.

The ownership of the co-op is a non-profit corporation made up of all of the unit owners. Each unit owner has a fractional interest in the ownership of the buildings and the common areas.

249

.www.InsuranceCommunityUniversity.com

Cooperatives (Co-op)

Different from a condo, no one legally owns their own units but owns them all in common.

There is a commercial package placed on the cooperative similar to that placed on the apartment property.

Each individual co op owner insures their own personal property and liability on an HO 04 form

250

.www.InsuranceCommunityUniversity.com

Insuring the Condominium Homeowner Risk

251

.www.InsuranceCommunityUniversity.com

Condominium

The word “condominium comes from the Latin word meaning joint ownership or control. Condominiums were originally developed by the Romans to solve congested living conditions and to promote conservation.

In modern terms it denotes individual ownership of units with the sole right to sell the unit.

252

.www.InsuranceCommunityUniversity.com

Condominiums

In the United States Condos were built as early as 1947 but not legally recognized until 1961.

By 1968 all states in the United States had passed legislation authorizing condominium developments

253

.www.InsuranceCommunityUniversity.com

Condominium

Condominium typically means the unit owners property interest in a multi-unit building.

The unit owner must have A fee-simple title to the unit owned and an undivided interest in common with all other owners of the project in the land, buildings, etc. Which are not deemed to be units by the condominium declarations.

254

.www.InsuranceCommunityUniversity.com

Condominium Condominiums are defined in law in the civil code Additional, the specifics of ownership and

responsibility are detailed in the CC & Rs of the association.

There are four general classifications of residential homeowners associations: Simple Condominiums ( Section 783) A, B, C, D, E, Condominiums Regular Planned Unit Developments Loose Planned Unit Developments

255

.www.InsuranceCommunityUniversity.com 256

Condominium

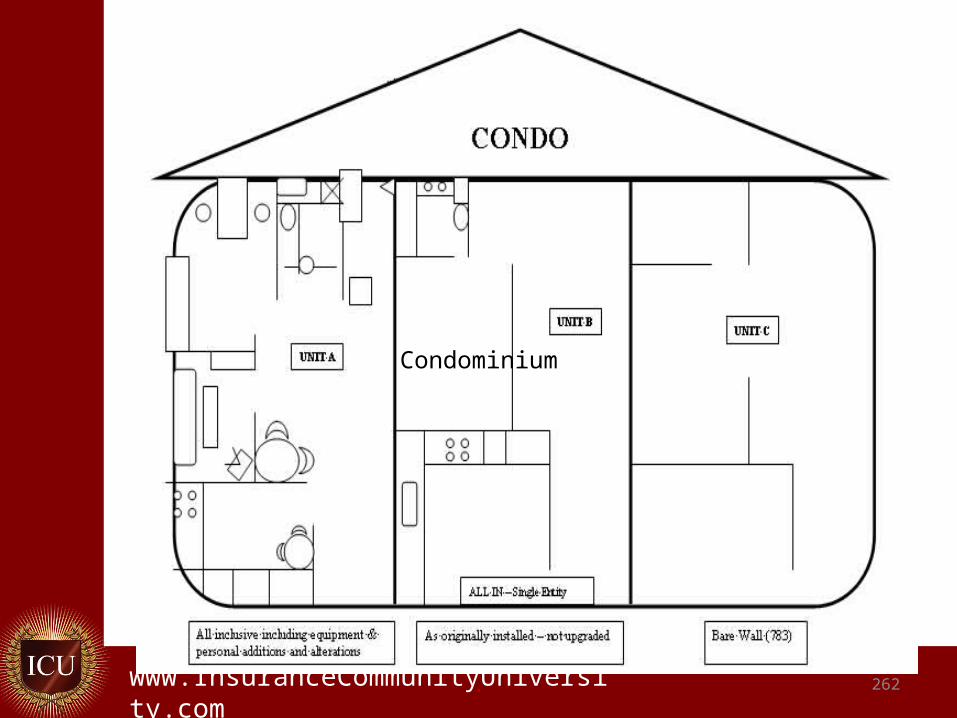

Condominium “unit” Oftentimes referred to as the “air space” within the

unfinished walls, floors and ceilings. Building

The CC &R’s will define “building” for purposes of sole ownership and common ownership. The Association will provide coverage on their association policy for common building elements.

Common Elements Usually defined as the entire projects other than the

units. These would be land, basic building structures, lobbies, corridors, roofs, and similar areas. Also, parking as storage areas.

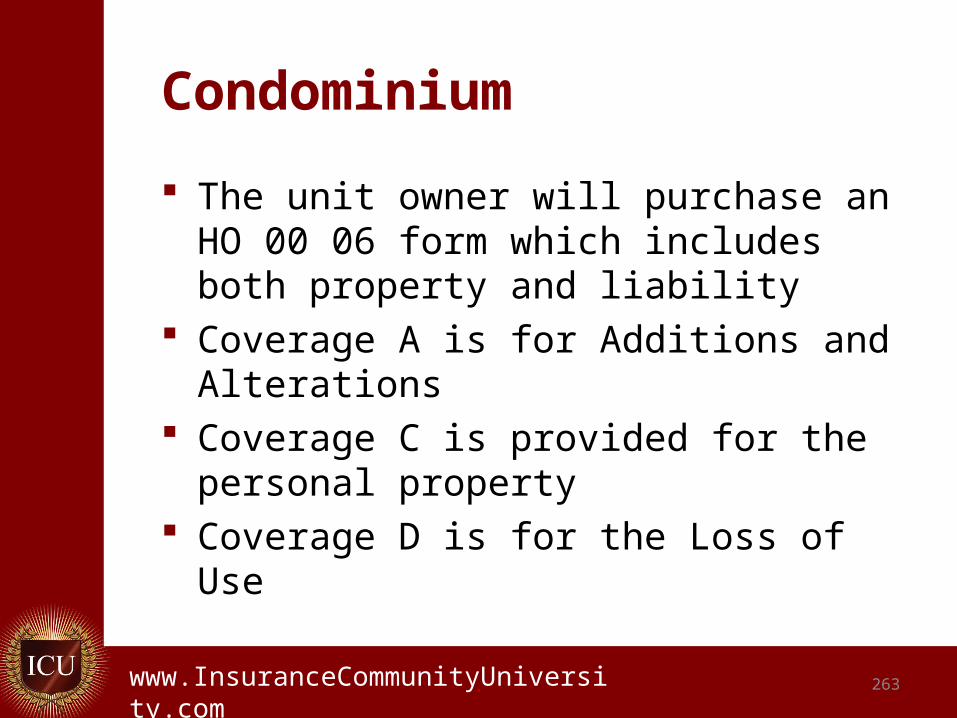

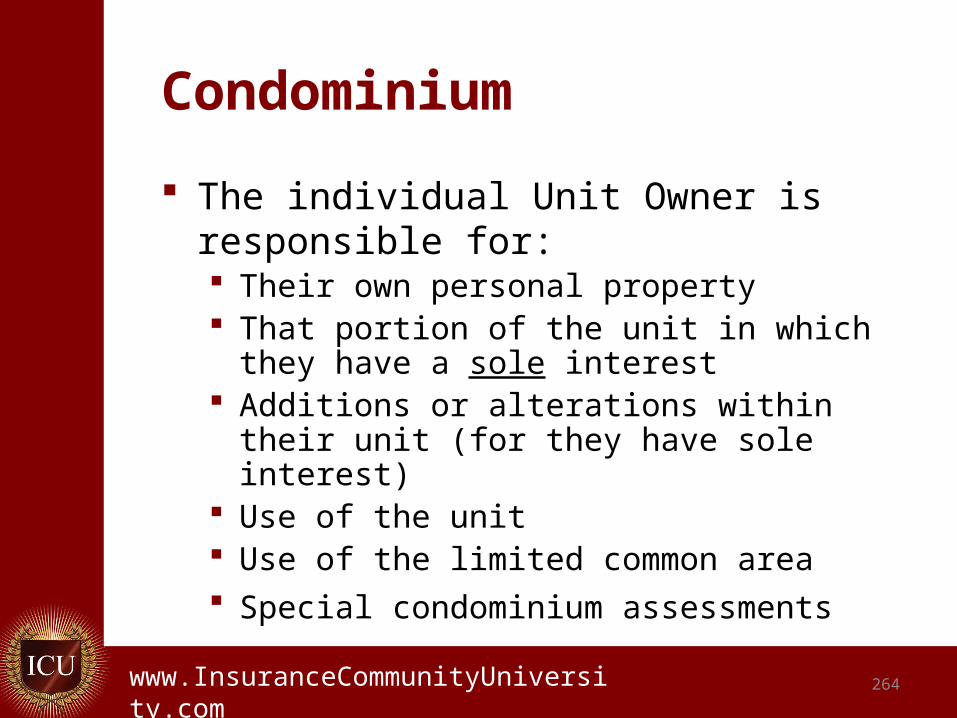

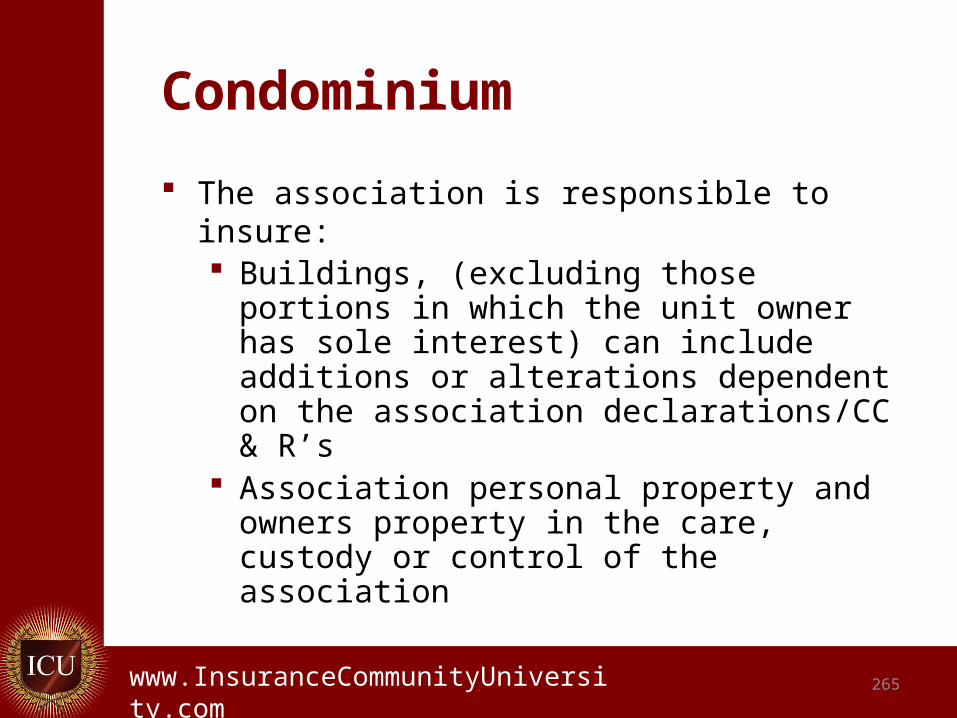

.www.InsuranceCommunityUniversity.com

Condominium