tiasblogweb.files.wordpress.com€¦ · web viewincome. it was also pleasing to see that this...

TRANSCRIPT

Step 7 – Inventory practises of BOTB

Key Concepts and Questions

Before I began to complete step seven regarding the inventory practises of my firm, BOTB, I knew that I would have quite a lot of content to cover. Before I started delving too deep into the information about my firm, its operations, and before completing the first few steps of this assignment that related to BOTB, I was required to check that my firm definitely had inventory (for step 7) and depreciation (for step 10). Through this process, I discovered that my firm and its inventory practises definitely weren’t straight forward, so I’m looking forward to gaining a deeper understanding of BOTB’s inventory practises and what inventory really means to a firm. I have had previous experience dealing with inventory through my school studies, so the concepts aren’t entirely new to me, but in saying that, I definitely still have a great deal to learn and I’m eager to broaden my knowledge of inventory, which is one of the core assets in accounting for many businesses. My basic understanding of inventory is that it consists of items that are purchased and owned by a firm that are intended for sale.

The first aspect I noticed about BOTB, is that its inventory account was not displayed in the 2017 Consolidated Statement of Financial Position. Immediately I was completely intrigued. Why is there no inventory amount to show in the balance sheet? I thought this was very strange? I then took it upon myself to check my firms inventory practises from the previous three years of annual reports. I was surprised when I discovered that in 2016, 2015 and 2014, that inventory was shown in the balance sheet under current assets. It made complete sense to me that inventories are a current asset because it would be in the hope of most businesses that their inventory is sold within a 12-month period. The inventory account shows a declining trend from having a value of 526,445 in 2014, to 501,137 in 2015, to 315,535 in 2016. In the year of 2016, total inventories made up nearly 19% of total current assets and nearly 10% of total assets, and these figures were very similar in the previous two years. This shows me that BOTB’s inventory amounts were not huge, but did have a reasonable standing when compared to their other assets. I wonder why BOTB’s inventory value is declining at quite a rapid pace through these years? And why in 2017 did BOTB decide to take inventory out of their balance sheet? To draw on my knowledge of my company that I gathered in step three of this assignment, I would question, is it because of the changes of their business structure that the business has decided that inventory is no longer needed as a separate account in the balance sheet? I know that BOTB have developed to mainly operating online and now have less emphasis on their physical presence of their cars and brand in airports, shopping centres, etc? I believe this could definitely be one of the reasons as to why my firm is no longer showing inventories on their statements. But I wonder where these funds went?

I thought it was then time to search through the notes of my annual report to discover more information about their inventory practises, and hopefully find an explanation to this major change in their financial statements. I decided to start from 2014 and work my way through to 2017. From 2014-16, the main note that BOTB wrote to describe inventories was, ‘inventories are valued at the lower of cost and net realisable value, after making due allowance for obsolete and slow-moving items.’ I believe this statement meant that this company is in line with UK’s accounting standards. It’s interesting that this company discloses a lot of its information about its inventory as this is the only note that BOTB has on its inventory practises from 2014-16. Furthermore, I discovered that cost of sales for the last four years (how much inventory the firm sold in the year) for BOTB comprises of the price of the competition prizes (i.e. the cars), along with the rent of the retail display site they utilise to have a physical presence and other related costs of the retail space. I understand that the

cost of sales is recognised as an expense, as shown in the Consolidated Statement of Comprehensive Income. It was also pleasing to see that this amount matched that of the cost of inventories recognised as expense in the note section of profit before income tax, but this was only the case in the years of 2014-16. In terms of BOTB, the cost of goods sold would be constantly changing because there is a range of 180 cars that can be given away each week. Drawing on my knowledge from step three, this range of cars vary from some being much more expensive than others. Additionally, another interesting aspect I noticed about BOTB’s inventory in 2014-16, was that they displayed the sub-classification of inventory as finished goods. Seen as BOTB does not actually manufacture the cars, but purchase them from suppliers, I would question whether this is a clear representation of their inventory practices.

So, as it is evident to see, there are many differences between the years 2014-16 and the year of 2017 in terms of their inventory practises. This relates back to the issue of BOTB removing the inventory account from their balance sheet. It was now time to read the note section on inventory in the 2017 annual report. I was hoping that BOTB didn’t chose to disclose as much of their inventory information like they did the previous years because then, I will be left stranded with many questions. It was very pleasing to discover that BOTB was kind enough to provide an explanation to why their inventory practises have faced a major change, and this change is due to the reasons I questioned previously. I discovered that what was previously classed as inventory was the cars on display in their retail spaces. However, due to the recent change in business structure in how people can choose from a range of 180 cars, and from most of the businesses revenues coming from online ticket purchasing, BOTB has removed inventory from their financial statements and its operations. Because of this, the inventory funds have now been reclassified as property plant and equipment. After learning this about my firm I had to question, was their inventory management and strategy towards their inventory right? It seems so strange that a firm that has always been operating with an inventory account decides to completely remove such account? I wonder what impact this would have on BOTB’s financial statements, if any? Well from my knowledge about property, plant, and equipment is that all items classed under this account whether it be equipment, vehicles, and in BOTB’s case, display equipment, must be depreciated. This means that these display cars will now be subject to depreciation, so I thought I would have a look to see if there were any differences in depreciation in the notes section of the annual report. It was to my surprise to see that ‘depreciation and impairment of property, plant and equipment’ under the profit before income tax section had increased from 141,463 in 2016 to 228,894 in 2017. This quite substantial increase is clearly due to reclassification on inventory. I found this to be very interesting as it shows how changing one account and its practices can affect other accounts in a firm’s financial statements and shows how they link together.

Through BOTB’s annual reports, nowhere did it state or indicate what type of inventory recording system it used. I made the assumption that BOTB, in the years previous to 2017, would have used the perpetual system. I made this assumption because I believe that this is the preffered inventory system as it is more accurate and is always up-to-date as it keeps continuous records of all inventory transactions. Based on this, I was provided with another reason to assume that BOTB used the perpetual inventory system as cost of sales is listed on one line in the consolidated statement of comprehensive income. Additionally, BOTB uses the specific identification inventory method as each unit sold on hand are identified with a specific invoice and is consistent with the actual movement of inventory. This method applies to motor vehicles, being BOTB’s core product. Seen as BOTB has decided to remove inventory from their accounts, I am unable to identify any areas that they could improve their inventory management. Moreover, as BOTB is such a unique business, their inventory practises are also very unique. Seen as their inventory only consisted of the retail display cars in the

years prior to 2017, the costs associated with the inventory management would have most likely been part of the cost of sales account (i.e. cost of renting retail space etc.).

Therefore, I found this step to be very beneficial to my accounting studies and learning journey. Despite BOTB having entirely different inventory practices from a typical manufacturing or retail firm, it was enlightening to analyse their accounting processes and changes to these processes. I understand that inventory plays a major role in most business, so I believe it is very important to gain an understanding through the early stages of my university study of inventory practices and what it means to a firm. I thought analysing a firm’s annual report to discover all you can about their inventory practices was a great process to complete, and it highlighted to me the importance of effective inventory management.

Step 8 – Learning how to use MYOB Account Right

MYOB set up

Figure 1: Last transaction screen - reconciling accounts

Figure 2: Last screen – changing preferences

MYOB training

Figure 3: Last screen - print/email invoices

MYOB Quiz – Screenshot of 13 questions

Step 9

10 transactions of Best of the Best PLC

Best of the Best PLC (BOTB) sells tickets to their customers to enter weekly competition in which they can win a car. BOTB has an online presence where they sell tickets and they also have a physical presence in retail spaces (airports, shopping centres etc.) where tickets are sold to people and their cars are displayed. As a person wins a car at the end of every week and there is a range of 180 cars to choose from, the cars are purchased at the end of each given week to suit each winner. The winner of the car is based on a competition called spot the ball which contestants can complete online or in the retail spaces. While BOTB is a UK company with pound dollar values and which uses the tax amount of 20%, for the purpose of this step, the Australian dollar value and the GST of 10% will be applied. The following are 10 hypothetical transactions for BOTB that have occurred during the one-month period of September:

2nd September

Transaction 1:

Cash collected from ticket sales at retail spaces (30 days) to undeposited funds account.

Total cash = $305,340 GST inc

GST amount = $27,758.18

5th September

Transaction 2:

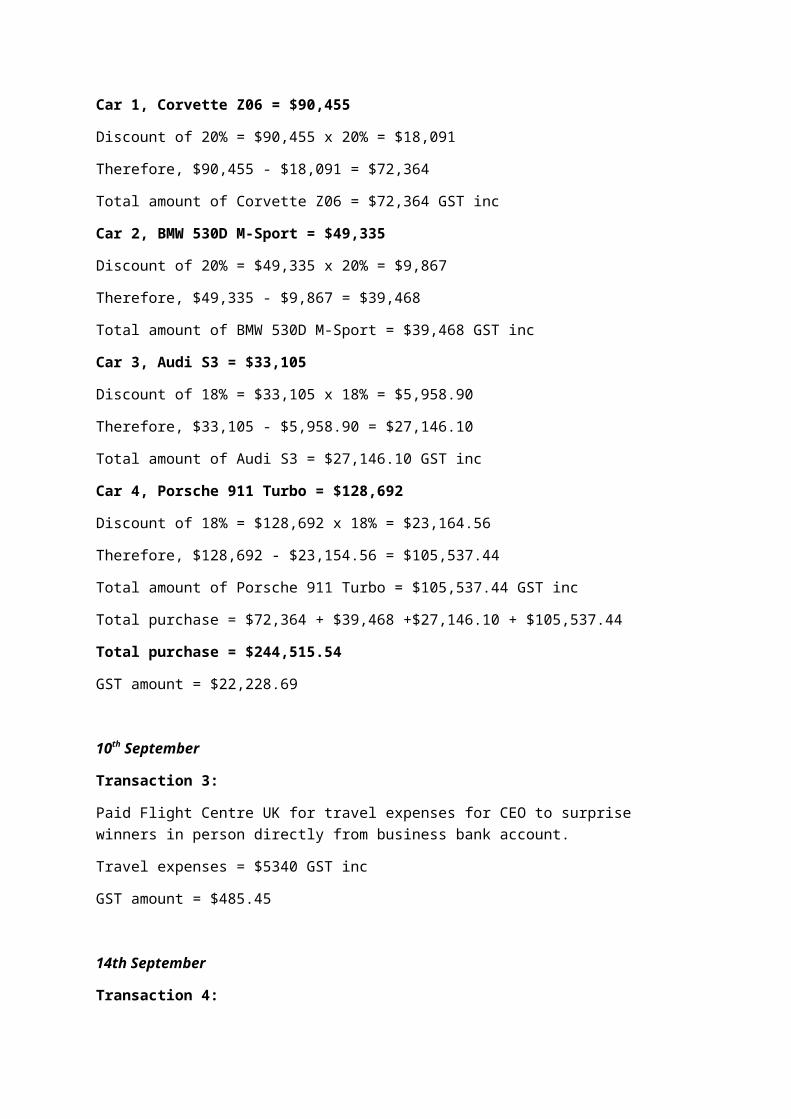

Purchased winning car prizes from previous month from car retailer Arnold Clark. A Corvette Z06 was one of the models which was included in this invoice. The retail price of this car $90,455, but there has been a discount negotiated as the volume of cars being purchased has increase recently, as a car is now given away every week. Clark happily offers this discount as they consider the relationship with BOTB to be a positive marketing strategy. The other cars which were included in this purchase were a BMW 530D M-Sport with a retail selling price of $49,335, an Audi S3 with the retail price of $33,105, and a Porsche 911 Turbo with the retail price of $128,692. This purchased will be paid on a later date.

Car 1, Corvette Z06 = $90,455

Discount of 20% = $90,455 x 20% = $18,091

Therefore, $90,455 - $18,091 = $72,364

Total amount of Corvette Z06 = $72,364 GST inc

Car 2, BMW 530D M-Sport = $49,335

Discount of 20% = $49,335 x 20% = $9,867

Therefore, $49,335 - $9,867 = $39,468

Total amount of BMW 530D M-Sport = $39,468 GST inc

Car 3, Audi S3 = $33,105

Discount of 18% = $33,105 x 18% = $5,958.90

Therefore, $33,105 - $5,958.90 = $27,146.10

Total amount of Audi S3 = $27,146.10 GST inc

Car 4, Porsche 911 Turbo = $128,692

Discount of 18% = $128,692 x 18% = $23,164.56

Therefore, $128,692 - $23,154.56 = $105,537.44

Total amount of Porsche 911 Turbo = $105,537.44 GST inc

Total purchase = $72,364 + $39,468 +$27,146.10 + $105,537.44

Total purchase = $244,515.54

GST amount = $22,228.69

10th September

Transaction 3:

Paid Flight Centre UK for travel expenses for CEO to surprise winners in person directly from business bank account.

Travel expenses = $5340 GST inc

GST amount = $485.45

14th September

Transaction 4:

Revenue collected from online ticket sales to direct bank account (30 days).

Revenue = $760,300 GST inc

GST amount = $69,118.18

17th September

Transaction 5:

BOTB paid electricity bill for office space for the period (30 days) to British Gas directly from the business bank account.

Total cost = $2550 GST inc

GST amount = $231.82

19rd September

Transaction 6:

BOTB paid wages to Lucy Marshall for the week

Total wages = $22.0975 per hour x 40 hour of work per week

Total wages = $883.90

22nd September

Transaction 7:

Paid owing full amount to Arnold Clark for purchase of winning car prizes (from the 5 th of September) directly from business bank account.

25th September

Transaction 8:

New large desktop screen was purchased from Superfi on credit (with 30-day credit term) which is used for the sporting experts to determine the winner of the competition (who got closest to determining where the ball is). This will be paid at a later date next month.

Total cost = $6450 GST inc

GST amount = 586.36

27th September

Transaction 9:

BOTB paid for retail rent space to Birmingham airport for the previous month (month of August) directly from the business bank account.

Retail rent space = $10,120 GST inc

GST amount = $920

30th September

Transaction 10: Prepared bank deposit of cash collected from ticket sales at retail spaces from the 2nd of September (transferring cash from undeposited funds account to the business bank account).

Analysis/Discussion – Financial Statements

Step nine of this assignment has definitely tested my limits and I have found it to be one of the most challenging steps that I have completed at university. I was challenged when creating the hypothetical transactions for my business as I struggled to think of interesting transactions BOTB could have. As they are a very unique company, and their sales and revenue only consist of ticket sales, I was unable to create any transactions which related to customers returning items, damaged items, quotes for services, or many others that I would have like to experiment with. These were some functions of MYOB that I was quite familiar with as I have used this program in one term of school in years 10, 11 and 12 during my accounting studies. However, I made do with the company I was assigned, and attempted making up transactions for BOTB’s practises as best as I could. The transactions I have made are all realistic transactions that are unique for BOTB. From these transactions, a profit and loss statement, a balance sheet and a statement of cash flow has been created for the month of September. It is imperative to analyse these statements to gain an understanding of BOTB’s financial position and performance in this period. In saying this, it is also important to remember that a true representation of a firm’s financial health, performance and position cannot be determined from analysing a period of only 10 transactions in a one-month period.

One way that these financial statements can by analysed is through the calculation of ratios

UNFINISHED

Step 10 – Depreciation policies

Before I began to complete this step, I was very excited to learn more about my firm and its depreciation policies and was very eager to attack this step, which is ultimately the last step of the assignment (apart from feedback of course). Over the duration of this unit, my feelings towards my firm have greatly evolved. I started off the term despising my firm as it was so different and it was a UK company so this frightened me, and I wished I would have received a more familiar Australian company. However, after completing all the steps of this assignment, and through my in-depth research about my firm, Best of the Best PLC, I have become quite fond of this firm and really enjoy accumulating more knowledge about their policies and operations.

Depreciation must be allocated systematically over the useful life of all physical non-current assets as it must be recorded how much economic benefit each asset is earning over time (2 or more periods). Physical non-current assets account for mainly items under property, plant and equipment. Depreciation represents a decline in the asset and is an estimate of the allocation of the cost of the asset, over the expected useful life of the asset to the business. It is also important to note that depreciation does not represent real cash flow. I have had quite significant exposure to depreciation from my three-year accounting studies in school and my initial understanding was that there are two main methods to calculate depreciation. I found learning about depreciation through Maria’s lecture this term to be like a complete refresher because, while I feel like I still know the basics of depreciation, I have forgotten lots of the key concepts and information I need to know. Through my school studies, we only ever dealt with two depreciation methods but I was very intrigued when Maria started to lecture about a third method, known as the units-of-production method. The first method for calculating depreciation is known as the straight-line method, and is also the method which is more straight forward and easier to calculate. The straight-line method uses an equal amount that is applied to each full year to the useful life of the asset. Whereas, the diminishing balance method uses an accumulated amount each year as it recognises that the asset uses up more economic benefit in the early years and generates more revenue in the earlier years. The units of production method depreciates an asset according to its actual use (units, hours, kilometres), however, this method is not utilised by BOTB.

Through step seven of this assignment, I spoke in-depth about how Best of the Best (BOTB) changed its inventory policies from the previous years to 2017, as they reclassified their inventories as property plant and equipment. So, drawing on my previous knowledge, I already knew that there would be some differences in BOTB’s depreciation policies in 2017 to the previous years, as it would now also have to consider the items that were classed as inventories, which were the cars on display in retail spaces. One of the first things I noticed when analysing my firm’s annual reports, was that BOTB didn’t have depreciation listed on the balance sheet. I did know that not all firms show depreciation on their financial statements. However, I wondered, why do some firms that have non-current assets that are depreciated, not display the amounts or account on their balance sheets? I decided to seek insight from the online Facebook accounting group and questioned why some firms decide not to show depreciation on their balance sheet. I have heard balance sheets to be referred to as a ‘snapshot’ of a firm’s financial position at a point in time, so my initial guess was that firms can represent their financial statements how they please, and can pick and choose which elements to show on their statements. Martin Turner replied to my Facebook post and informed me that firms can show depreciation in the balance sheets or in their footnotes, and if they choose to show depreciation in their footnotes, it’s to prevent the balance sheet from being too cluttered. Martin also reminded me that the non-current asset figures that are displayed on the balance sheet are net of depreciation (see screenshot below).

Figure 4: Screenshot of discussion from Facebook group

I was interested to discover the total depreciation amount for BOTB and I was also interested to see where and how this would be displayed, as they didn’t display it on their balance sheets. In the profit before income tax section, it listed ‘depreciation and impairment of property, plant and equipment’ with the amount of 228,894 in 2017 and 141,463 in 2016. I believe that this substantial increase is due to the reclassification of inventories to property, plant and equipment. However, I was very curious as to whether there was also a similar increase in the previous years. Immediately I noticed a significant difference in the 2016 report to the 2017 report, which was very interesting (see figure 2 and 3). In the profit before income tax section, BOTB listed ‘depreciation – owned assets’ with an amount of 62,813. Firstly, obviously the listing name was different and this indicated that in 2016, BOTB didn’t include impairment amounts in the total. Secondly, the 2016 amount of 62,813 was different to the 2016 amount which was in the 2017 report. In the 2017 report, the 2016 amount was 141,463, so I did a simple calculation and assumed that the difference between the two 2016 amounts would be the impairment for the year which was nearly 80,000. I don’t know why BOTB changed the way they displayed this aspect of their annual report in 2017 to also including impairment, but it is intriguing. The 2015 report showed no change to the 2016 report and the amount for depreciation in this year was 90,028, which was consistent with the 2015 amount listed in the 2016 report, and it also displayed the 2014 depreciation amount as 189,396. After comparing the depreciation amounts of BOTB for the last four years with their other expenses listed in the statement of comprehensive income, it is apparent that depreciation accounts for a mere 2% for 2017 of their total expenses, and even less in other years. Therefore, it is clear that depreciation holds limited significance as an expense for this firm.

Figure 5: 2017 annual report

Figure 6: 2016 report

As I reviewed the 2017 annual report and compared it with the 2016 annual report, I noticed that under ‘property, plant and equipment’ in the notes sections, there was an additional listing of display equipment which they state is depreciating at varying rates on cost. This makes sense as the cars which they have on display would vary on cost significantly based on the model and brand of each car the company decides to have on display at different retail spaces. It was interesting to see that BOTB had provided me with the rates of depreciation that was being used for each individual non-current asset, and also indicated that the reducing balance method of depreciation is used. The other assets that BOTB had listed that were being depreciated in 2017 were long leasehold property, improvements to property, fixtures and fittings, motor vehicles and computer equipment, and each gave the rate at which they were being depreciated.

I then decided to compare the rates at which these assets were depreciated and see if there were any variances with the years previous to 2017. To my surprise, I discovered that there were differences in the depreciation rates from 2017 and to the previous years. In 2015-16, the depreciation rate for long leasehold property was ‘not provided’ and improvements to property was ‘not depreciated’. I wonder why BOTB decided to not disclose this information in their most recent year? Was it because they wanted to provide the interested stakeholders with a more accurate view of their business? Was it a change in the company’s accounting processes? Were the rates hard to determine accurately in the previous years? All this information was located in the ‘property, plant and equipment’ note and it was also pleasing to see that BOTB stated at the end of this section, that they review their depreciation policies annually and are reviewed by management at the end of each accounting period as it shows that they are adhering to accounting standards.

Furthermore, in the 2017 annual report of note 15, ‘Property, plant and equipment – group and company’, the depreciation and impairment amounts were listed for each asset as charge for the year. For example, the depreciation and impairment charge for the year for long leasehold was 3,500 and was 42,511 for computer equipment. It was interesting to see that in the year of 2017, fixtures and fittings had the highest amount of depreciation and impairment of 97,130 and in 2016, computer equipment had the highest amount of 29,467. This significant depreciation of computer equipment would be in line with the considerable ‘additions’ with the purchase of 185,000 worth of computer equipment, which is reflective of their increasing online presence. However, it is

important to remember that in 2016, all depreciation figures for the assets do not include impairment. As mentioned previously, in 2017 BOTB changed their statements to also display

along with the depreciation amounts, and this was consistent in this section of the annual report. To my understanding, impairment refers to the actual loss of value of a firm’s assets, and is usually conducted through a test by firms. Moreover, in the notes relating to income tax, there is a listing of ‘depreciation in excess of/(less than) capital allowances with the amount of 4,499 in 2017. This would appear to be the impairment amount, but it is concerning that it is not listed as impairment, so this leaves me with some questions. Over the four years, this figure fluctuates significantly from excess of 6,924 in 2014, to a short-fall of (42,901) in 2016. While this figure fluctuates, it is very small in the context of the size of the company’s financial position.

While depreciation focusses on the physical non-current assets that a business owns, I thought it would be beneficial to my studies if I also looked at how BOTB amortises their intangible assets. Intangible assets are non-current and do not have a physical substance. I found it interesting to discover that BOTB’s intangible assets consisted of their IT platform, infrastructure and website, which is growing rapidly. From the 2017 annual report, I discovered in the note section that the amortisation of intangible assets amount was 89,067 and the 2016 amount for this was blank. The only element of intangible assets that was listed with the full amount was classed as development costs, which I assume consists of the aspects of the online website, IT platform and infrastructure, as mentioned above. I found this interesting and decided to analyse the 2016 report as to why there is no amount listed and I identified that it was because their website was not yet operational, therefore, amortisation on the businesses intangible assets were not recognised. I became even more intrigued when I searched for ‘amortisation’ and ‘intangible assets’ in the 2015 report, and there were no results. I wonder why BOTB never had any other types of intangible assets until they established their online presence? I wonder why BOTB never had any of the intangible assets that I know of (which are the well-known types) such as patents, copyright, or goodwill? Additionally, reading through the note section on intangible assets, I discovered that BOTB’s managers estimated that the intangible assets had a useful economic life of three years, and that they are amortised over this period, using the straight-line method. This indicated to me that BOTB expects to invest in new IT platforms, website and infrastructure after three years. Moreover, the intangible asset value was listed in the 2017 balance sheet as 178,133 and in the 2016 report, the value was 267,200, which represents the amortisation of 89,067.

3 journal entries for BOTB depreciation:

General JournalDate Particulars Debit £ Credit £30 June Depreciation expense – display equipment

Accumulated depreciation – display equipment (depreciation expense for the year, at varying rates on cost)

74,401

74,401

30 June Amortisation expense – development costs (online platform)

Accumulated amortisation – development costs (online platform)(amortisation expense for the year, straight-line method)

89,067

89,067

30 June Depreciation expense – motor vehicles 10,312

Accumulated depreciation – motor vehicles (depreciation expense for the year, at 25% on reducing balance)

10,312

The above general journal entries are based on the actual 2017 annual report figures and rates. The above journal entry figures represent an expense and do have an effect on the firm’s profit, although, it has reasonably limited effect on BOTB’s overall financial position as the expense is quite small in comparison to other costs. Depreciation and amortisation is based on the useful life of the asset and this will vary in different businesses due to their use of the asset and policies regarding asset management. Therefore, this leaves room for manipulation to occur as businesses are able to have differing methods, rates, and timelines for the depreciation and amortisation of assets. For example, BOTB, may judge that their website needs rebuilding in two years rather than three, and amortise this intangible asset as 50% rather than 33.3%.

I have found this step to be extremely interesting and beneficial to my understanding of the accounting process relating to depreciation. It was pleasing to discover many changes between the years of BOTB’s annual reports relating to depreciation, impairment, intangibles and its other non-current assets, as I was able to challenge myself to delve deeper into their reports. Initially, I had many concerns with depreciation not being listed on the financial statements as I was worried I would not have enough content to cover. However, as I come to the conclusion of this step, I feel a sense of accomplishment as I discovered and analysed enough substance relating to BOTB’s depreciation policies and financial data, which enabled me to successfully complete this task.