© the mcgraw-hill companies, inc., 2006 mcgraw-hill/irwin1 16-1 reporting the statement of cash...

Post on 20-Dec-2015

214 views

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin1

16-1

Reporting the Statement of Cash Flows(refer to HOU’s)

Chapter

1616

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin2

16-2

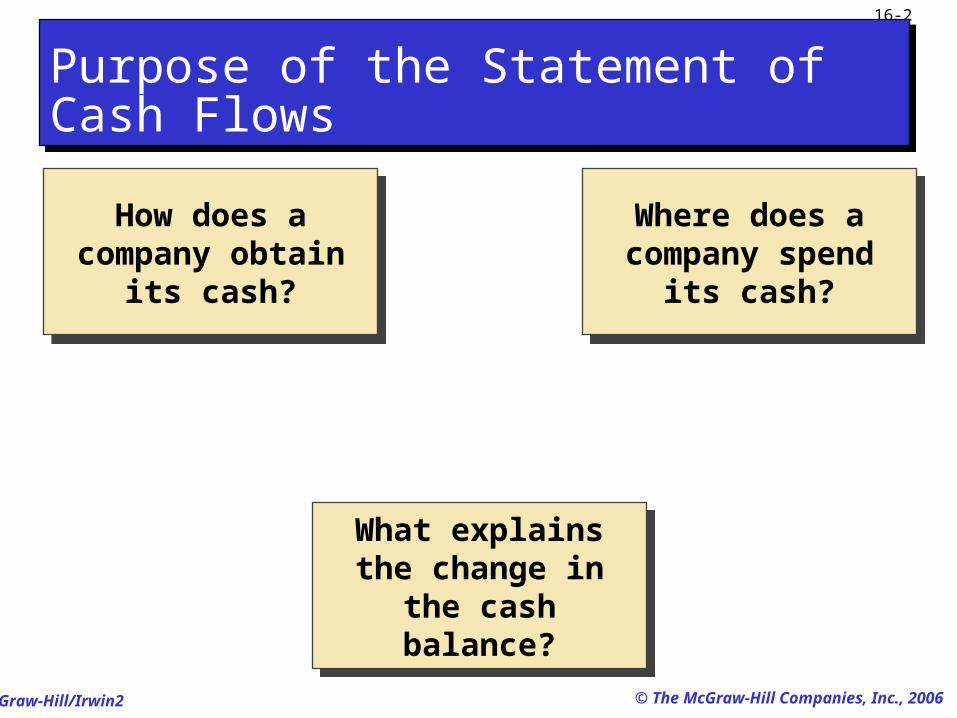

How does a company obtain its

cash?

How does a company obtain its

cash?

Where does a company spend its

cash?

Where does a company spend its

cash?

What explains the change in the cash

balance?

What explains the change in the cash

balance?

Purpose of the Statement of Cash FlowsPurpose of the Statement of Cash Flows

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin3

16-3

How did the business fund its

operations?

How did the business fund its

operations?

Did the business borrow any funds or

repay any loans?

Did the business borrow any funds or

repay any loans?

Does the business have sufficient cash to pay its debts as

they mature?

Does the business have sufficient cash to pay its debts as

they mature?

Did the business make any dividend

payments?

Did the business make any dividend

payments?

Importance of Cash FlowsImportance of Cash Flows

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin4

16-4

CashCashCurrency

Cash Equivalents

Short-term, highly liquid investments. Readily convertible into cash. So near maturity that market value is unaffected by

interest rate changes.

Short-term, highly liquid investments. Readily convertible into cash. So near maturity that market value is unaffected by

interest rate changes.

Measurement of Cash FlowsMeasurement of Cash Flows

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin5

16-5

The Statement of Cash Flows includes the following three sections:

Operating Activities Investing ActivitiesFinancing Activities

Classifying Cash FlowsClassifying Cash Flows

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin6

16-6

Outflows Salaries and wages. Payments to suppliers. Taxes and fines. Interest paid to lenders. Other.

Outflows Salaries and wages. Payments to suppliers. Taxes and fines. Interest paid to lenders. Other.

Inflows Receipts from customers. Cash dividends received. Interest from borrowers. Other.

Inflows Receipts from customers. Cash dividends received. Interest from borrowers. Other.

Operating ActivitiesOperating Activities

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin7

16-7

Outflows Purchasing long-term

productive assets. Purchasing equity

investments. Purchasing debt investments. Other.

Outflows Purchasing long-term

productive assets. Purchasing equity

investments. Purchasing debt investments. Other.

Inflows Selling long-term productive

assets. Selling equity investments. Collecting principal on loans. Other.

Inflows Selling long-term productive

assets. Selling equity investments. Collecting principal on loans. Other.

Investing ActivitiesInvesting Activities

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin8

16-8

Outflows Pay dividends. Purchasing treasury stock Repaying cash loans. Paying owners’ withdrawals.

Outflows Pay dividends. Purchasing treasury stock Repaying cash loans. Paying owners’ withdrawals.

Inflows Issuing its own equity

securities. Issuing bonds and notes. Issuing short- and long-term

liabilities.

Inflows Issuing its own equity

securities. Issuing bonds and notes. Issuing short- and long-term

liabilities.

Financing ActivitiesFinancing Activities

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin9

16-9

Items requiring separate disclosure include:

Retirement of debt by issuing equity securities.

Conversion of preferred stock to common stock.

Leasing of assets in a capital lease transaction.

Items requiring separate disclosure include:

Retirement of debt by issuing equity securities.

Conversion of preferred stock to common stock.

Leasing of assets in a capital lease transaction.

Noncash Investing and FinancingNoncash Investing and Financing

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin10

16-10

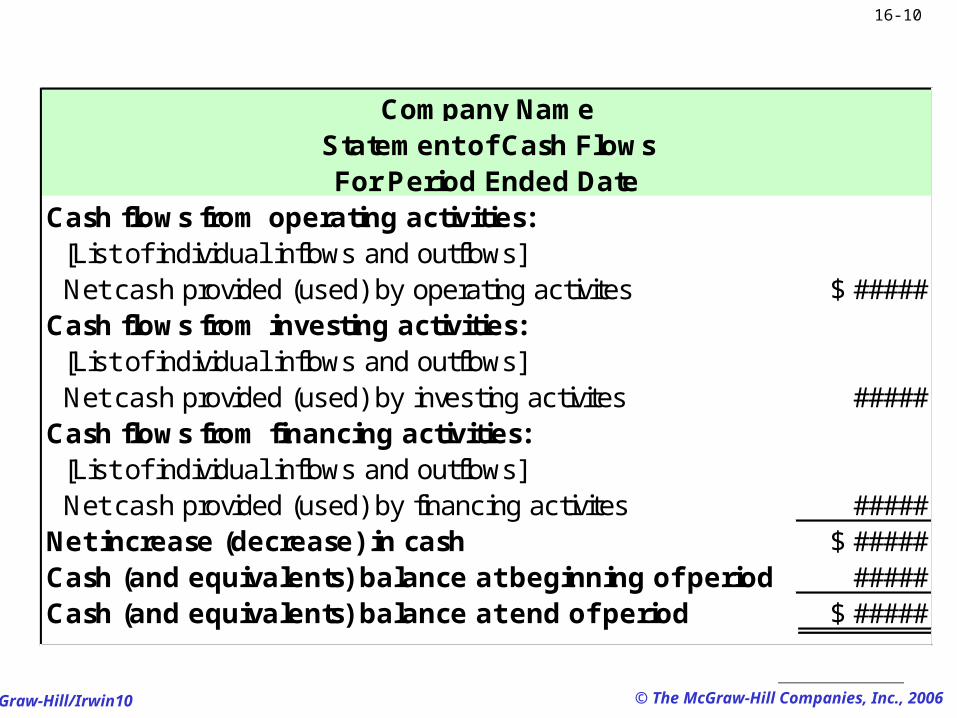

Cash flows from operating activities: [List of individual inflows and outflows] Net cash provided (used) by operating activites $ #####Cash flows from investing activities: [List of individual inflows and outflows] Net cash provided (used) by investing activites #####Cash flows from financing activities: [List of individual inflows and outflows] Net cash provided (used) by financing activites #####Net increase (decrease) in cash $ #####Cash (and equivalents) balance at beginning of period #####Cash (and equivalents) balance at end of period $ #####

Company NameStatement of Cash FlowsFor Period Ended Date

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin11

16-11

Cash flows from operating activities: [List of individual inflows and outflows] Net cash provided (used) by operating activites $ #####Cash flows from investing activities: [List of individual inflows and outflows] Net cash provided (used) by investing activites #####Cash flows from financing activities: [List of individual inflows and outflows] Net cash provided (used) by financing activites #####Net increase (decrease) in cash $ #####Cash (and equivalents) balance at beginning of period #####Cash (and equivalents) balance at end of period $ #####

Company NameStatement of Cash FlowsFor Period Ended Date

There are two acceptable methods to determine Cash Flows from Operating Activities:

Direct Method

Indirect Method

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin12

16-12

Let’s look at the Direct Method for preparing

the Cash Flows from Operating

Activities section.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin13

16-13

Analyzing the Cash AccountAnalyzing the Cash Account

Balance, Jan. 1, 2005 22,000 Payments for merchandise 150,000 Receipts from customers 466,000 Payments for wages 145,000 Receipts from sale of land 25,000 Payments for interest 10,000 Receipts from stock issuance 35,000 Payments for taxes 20,000

Payments for equipment 70,000 Payments for bond retirement 50,000 Payments for dividends 40,000

Balance, Dec. 31, 2005 63,000

Cash

Let’s use this Cash account to prepare B&G Company’s Statement of Cash

Flows under the Direct Method.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin14

16-14

Cash flows from operating activities Cash received from customers 466,000$

Cash paid for merchandise (150,000) Cash paid for wages (145,000) Cash paid for interest (10,000) Cash paid for taxes (20,000)

Net cash provided by operating activities 141,000 Cash flows from investing activities

Proceeds from sale of land 25,000

Purchase of equipment (70,000) Net cash used by investing activities (45,000) Cash flows from financing activities

Proceeds from issuance of common stock 35,000 Redemption of bonds (50,000) Payment of dividends (40,000)

Net cash used by financing activities (55,000) Net increase in cash 41,000 Cash, January 1, 2005 22,000 Cash, December 31, 2005 63,000$

B&G CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin15

16-15

Let’s look at the Indirect Method

for preparing the Cash Flows from Operating

Activities section.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin16

16-16

Net Income

Net Income

Cash Flows from Operating

Activities

Cash Flows from Operating

Activities

97.5% of all companies use the indirect method.97.5% of all companies use the indirect method.

Changes in current assets and current liabilities.

Changes in current assets and current liabilities.

+ Losses and - Gains

+ Losses and - Gains

+ Noncash expenses such as depreciation and

amortization.

+ Noncash expenses such as depreciation and

amortization.

Indirect Method of Reporting Operating Cash FlowsIndirect Method of Reporting Operating Cash Flows

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin17

16-17

Use this table when adjusting Net Income to Operating Cash Flows.

Indirect Method of Reporting Operating Cash FlowsIndirect Method of Reporting Operating Cash Flows

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin18

16-18

East, Inc. reports $125,000 net income for the year ended December 31, 2005.

Accounts Receivable increased by $7,500 during the year and Accounts Payable

increased by $10,000.

During 2005, East reported $12,500 of Depreciation Expense.

East, Inc. reports $125,000 net income for the year ended December 31, 2005.

Accounts Receivable increased by $7,500 during the year and Accounts Payable

increased by $10,000.

During 2005, East reported $12,500 of Depreciation Expense.

What is East, Inc.’s Operating Cash Flow for 2005?

Indirect MethodExampleIndirect MethodExample

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin19

16-19

Net income 125,000$

Deduct: Increase in accounts receivable

Cash provided by operating activities

Net income 125,000$

Deduct: Increase in accounts receivable

Cash provided by operating activities

For the indirect method, start with

net income.

For the indirect method, start with

net income.

Indirect MethodExampleIndirect MethodExample

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin20

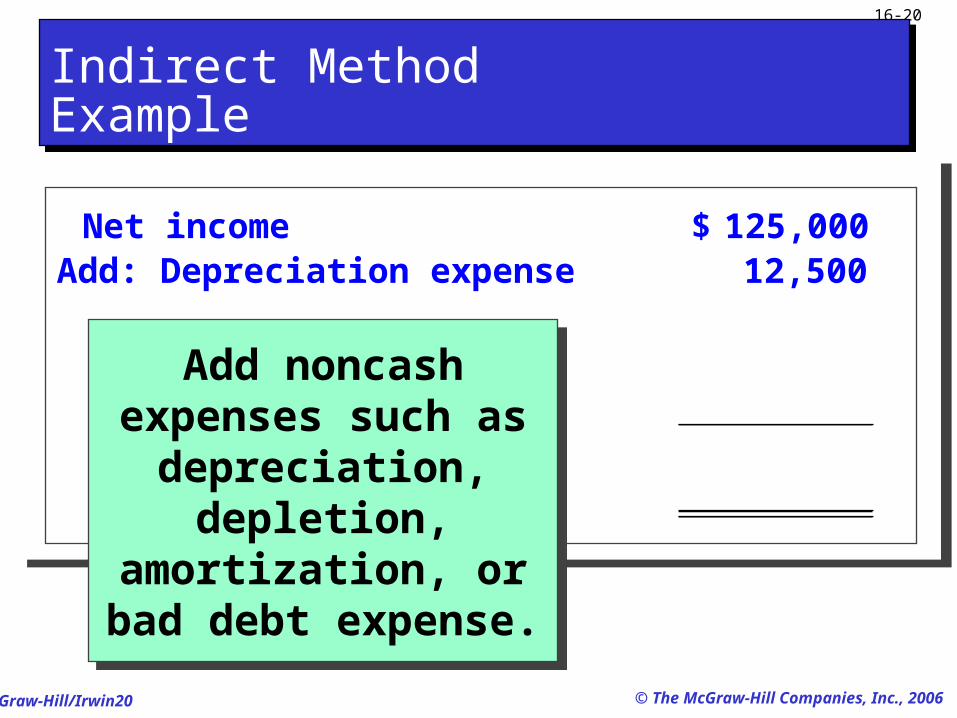

16-20

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable

Cash provided by operating activities

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable

Cash provided by operating activities

Add noncash expenses such as

depreciation, depletion,

amortization, or bad debt expense.

Add noncash expenses such as

depreciation, depletion,

amortization, or bad debt expense.

Indirect MethodExampleIndirect MethodExample

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin21

16-21

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable (7,500)

Cash provided by operating activities

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable (7,500)

Cash provided by operating activities

Indirect MethodExampleIndirect MethodExample

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin22

16-22

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable (7,500) Add: Increase in accounts payable 10,000 Cash provided by operating activities

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable (7,500) Add: Increase in accounts payable 10,000 Cash provided by operating activities

Indirect MethodExampleIndirect MethodExample

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin23

16-23

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable (7,500) Add: Increase in accounts payable 10,000 Cash provided by operating activities 140,000$

Net income 125,000$ Add: Depreciation expense 12,500 Deduct: Increase in accounts receivable (7,500) Add: Increase in accounts payable 10,000 Cash provided by operating activities 140,000$

Indirect MethodExampleIndirect MethodExample

If we used the Direct Method, we would get the same $140,000 for Cash Provided by Operating Activities.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin24

16-24

Let’s prepare a Statement of

Cash Flows for B&G Company

using the Indirect Method.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin25

16-25

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin26

16-26

Additional Information for 2005:• Net income was $105,000.• Cash dividends declared and paid

were $40,000.• Bonds payable of $50,000 were

redeemed for $50,000 cash.• Common stock was issued for

$35,000 cash.

Additional Information for 2005:• Net income was $105,000.• Cash dividends declared and paid

were $40,000.• Bonds payable of $50,000 were

redeemed for $50,000 cash.• Common stock was issued for

$35,000 cash.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin27

16-27

Cash flows from operating activitiesNet income 105,000$

Adjustments to accrual-basis net income:

B&G CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

Add noncash expenses and

losses.

Subtract noncash revenues and gains.

Add noncash expenses and

losses.

Subtract noncash revenues and gains.

Start with accrual-basis net income.

Start with accrual-basis net income.

Then, analyze the changes in current assets and current

liabilities.

Then, analyze the changes in current assets and current

liabilities.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin28

16-28

Cash flows from operating activitiesNet income 105,000$

Adjustments to accrual-basis net income: Depreciation expense 34,000$

Increase in accounts receivable (9,000) Decrease in inventory 19,000 Decrease in accounts payable (8,000) Total adjustments 36,000

Net cash provided by operating activities 141,000 Cash flows from investing activities

B&G CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin29

16-29

Cash flows from operating activitiesNet income 105,000$

Adjustments to accrual-basis net income: Depreciation expense 34,000$

Increase in accounts receivable (9,000) Decrease in inventory 19,000 Decrease in accounts payable (8,000) Total adjustments 36,000

Net cash provided by operating activities 141,000 Cash flows from investing activities

B&G CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

Now, let’s complete the

investing section.

Now, let’s complete the

investing section.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin30

16-30

Cash flows from operating activitiesNet income 105,000$

Adjustments to accrual-basis net income: Depreciation expense 34,000$

Increase in accounts receivable (9,000) Decrease in inventory 19,000 Decrease in accounts payable (8,000) Total adjustments 36,000

Net cash provided by operating activities 141,000 Cash flows from investing activities

Proceeds from sale of land 25,000

Purchase of equipment (70,000) Net cash used by investing activities (45,000) Cash flows from financing activities

B&G CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

Now, let’s complete the

financing section.

Now, let’s complete the

financing section.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin31

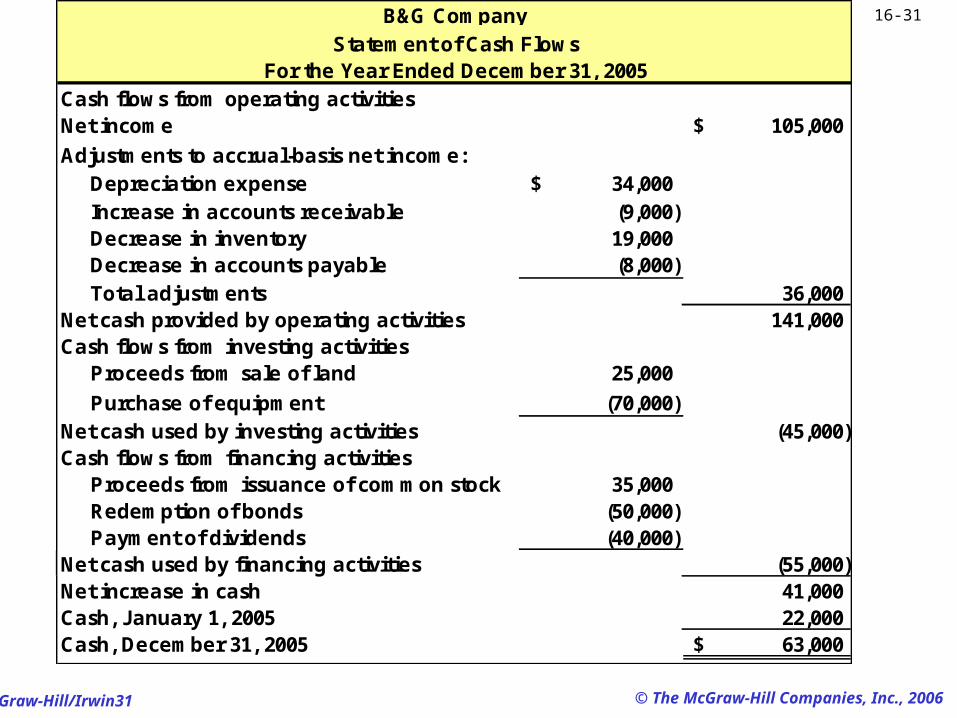

16-31

Cash flows from operating activitiesNet income 105,000$

Adjustments to accrual-basis net income: Depreciation expense 34,000$

Increase in accounts receivable (9,000) Decrease in inventory 19,000 Decrease in accounts payable (8,000) Total adjustments 36,000

Net cash provided by operating activities 141,000 Cash flows from investing activities

Proceeds from sale of land 25,000

Purchase of equipment (70,000) Net cash used by investing activities (45,000) Cash flows from financing activities

Proceeds from issuance of common stock 35,000 Redemption of bonds (50,000) Payment of dividends (40,000)

Net cash used by financing activities (55,000) Net increase in cash 41,000 Cash, January 1, 2005 22,000 Cash, December 31, 2005 63,000$

B&G CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin32

16-32

CASE TWOCASE TWO

Prepare a statement of cash flow using the indirect method

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin33

16-33

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin34

16-34

Additional Information for 2005:• Net income was $38,000.a. The accounts payable balances result from

merchandise inventory purchases. b. Purchased plant assets costing $70,000 by

paying $10,000 cash and issuing $60,000 of bonds payable.

c. Sold plant assets with an original cost of $30,000 and accumulated depreciation of $12,000 for $12,000 cash, yielding a $6,000 loss.

d. Received cash of $15,000 from issuing 3,000 shares of common stock.

e. Paid $18,000 cash to retire bonds with a $34000 book value, yielding a $16000 gain.

f. Cash dividends declared and paid were $14,000.

Additional Information for 2005:• Net income was $38,000.a. The accounts payable balances result from

merchandise inventory purchases. b. Purchased plant assets costing $70,000 by

paying $10,000 cash and issuing $60,000 of bonds payable.

c. Sold plant assets with an original cost of $30,000 and accumulated depreciation of $12,000 for $12,000 cash, yielding a $6,000 loss.

d. Received cash of $15,000 from issuing 3,000 shares of common stock.

e. Paid $18,000 cash to retire bonds with a $34000 book value, yielding a $16000 gain.

f. Cash dividends declared and paid were $14,000.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin35

16-35

Cash flows from operating activitiesNet income 38,000$

Adjustments to accrual-basis net income:

Genesis CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

Add noncash expenses and

losses.

Subtract noncash revenues and gains.

Add noncash expenses and

losses.

Subtract noncash revenues and gains.

Start with accrual-basis net income.

Start with accrual-basis net income.

Then, analyze the changes in current assets and current

liabilities.

Then, analyze the changes in current assets and current

liabilities.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin36

16-36

Adjustments for changes in current assets and current liabilitiesAdjustments for changes in current assets and current liabilities

Decreases in noncash current assets are added to net income

Increases in noncash assets are subtracted from net income

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin37

16-37

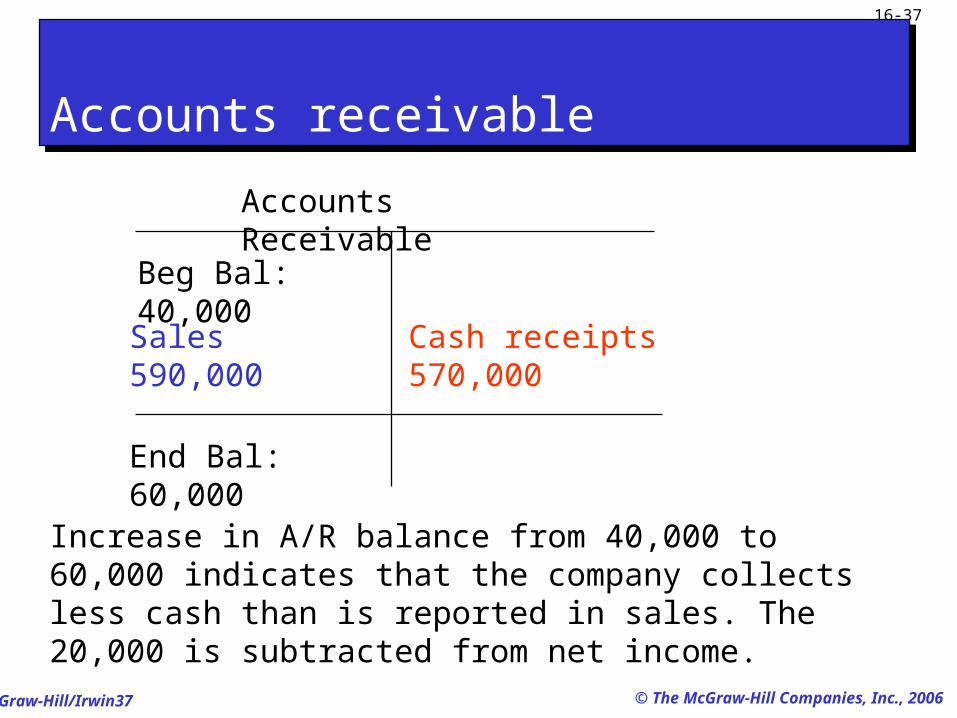

Accounts receivable Accounts receivable

Accounts Receivable

Beg Bal: 40,000

End Bal: 60,000

Sales 590,000 Cash receipts 570,000

Increase in A/R balance from 40,000 to 60,000 indicates that the company collects less cash than is reported in sales. The 20,000 is subtracted from net income.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin38

16-38

Merchandise InventoryMerchandise Inventory

Merchandise inventory

Beg Bal: 70,000

End Bal: 84,000

Purchases 314,000 Cost of goods sold 300,000

Increase in merchandise inventory balance from 70,000 to 84,000 indicates that the company has a larger amount of cash purchase than cost of goods sold. The 14,000 increase is subtracted from net income.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin39

16-39

Prepaid expensePrepaid expense

Beg Bal 4,000

Prepaid expense

End Bal 6,000

Cash payment 218,000Wages and other operating exp 216,000

Increase in prepaid expense balance from 4,000 to 6,000 indicates the company’s cash payments exceed its recorded prepaid expense. The 2,000 increase is subtracted from net income.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin40

16-40

Cash flows from operating activitiesNet income 38,000$

Adjustments to accrual-basis net income: Depreciation expense 24,000$

Increase in accounts receivable (20,000) Increase in inventory (14,000) Increase in prepaid expenses (2,000)

GENESIS CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin41

16-41

Adjustments for changes in current liabilitiesAdjustments for changes in current liabilities

Increases in current liabilities are added to net income

Decreases in current liabilities are subtracted from net income

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin42

16-42

Accounts payableAccounts payable

The decrease in A/P balance from 40,000 to 35,000 indicates that cash payments to suppliers exceed purchases by $5,000 for the period. The 5,000 is subtracted from net income.

Accounts payable

Cash payment

319,000

Beg Bal 40,000

Purchases 314,000

End Bal 35,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin43

16-43

Interest payableInterest payable

The decrease in interest payable balance from 4,000 to 3,000 indicates that cash paid for interest exceeds interest

expense. The 1,000 is subtracted from net income.

Interest payable

Cash paid for interest 8,000

Beg Bal 4,000

Interest expense 7,000

End Bal 3,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin44

16-44

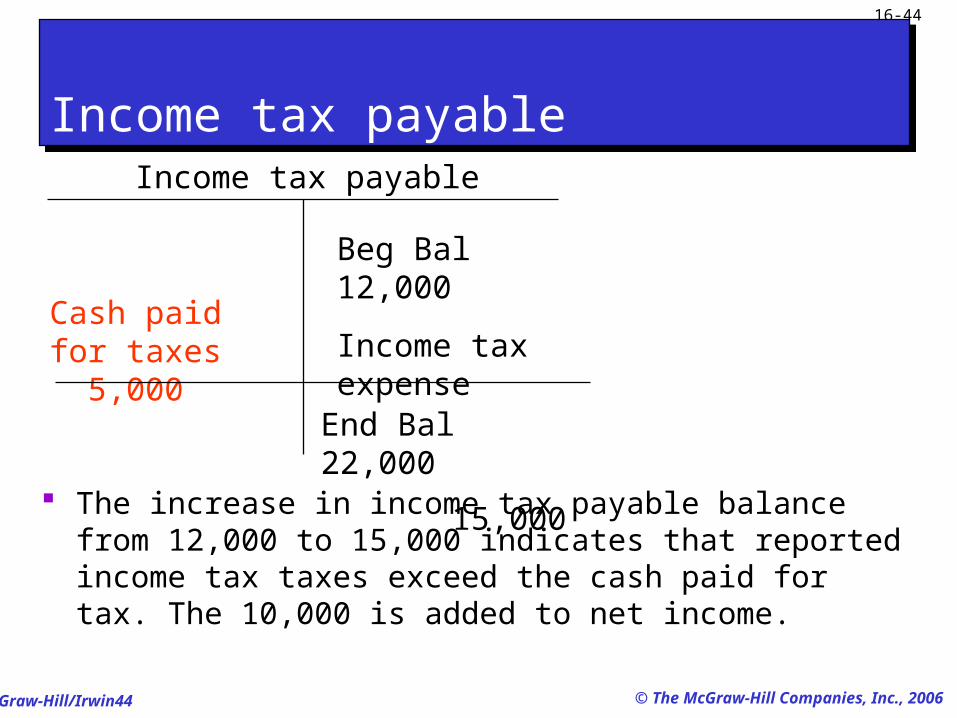

Income tax payableIncome tax payable

The increase in income tax payable balance from 12,000 to 15,000 indicates that reported income tax taxes exceed the cash paid for tax. The 10,000 is added to net income.

Income tax payable

Beg Bal 12,000

Income tax expense

15,000

Cash paid for taxes 5,000

End Bal 22,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin45

16-45

Cash flows from operating activitiesNet income 38,000$

Adjustments to accrual-basis net income: Depreciation expense 24,000$

Increase in accounts receivable (20,000) Increase in inventory (14,000) Increase in prepaid expenses (2,000) Decrease in accounts payable (5,000) Decrease in interest payable (1,000) Increase in income taxes payable 10,000

GENESIS CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin46

16-46

Adjustments for operating items not providing or using cashAdjustments for operating items not providing or using cash

Expenses with no cash outflows are added back to net income

Revenues with no cash inflows are subtracted from net income

Depreciation expense is the only operating item that has no effect on cash flows in the period. The 24,000 is added to net income.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin47

16-47

Adjustments for nonoperating itemsAdjustments for nonoperating items

Nonoperating losses are added back to net income

Nonoperating gains are subtracted from net income

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin48

16-48

Loss on sale of plant assetsLoss on sale of plant assets

c.Sold plant assets with an original cost of $30,000 and accumulated depreciation of $12,000 for $12,000 cash, yielding a $6,000 loss.

The loss is not part of operating activities. The sale of plant assets is part of investing activities. Thus, the 6,000 loss is added back to net income.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin49

16-49

e. Paid $18,000 cash to retire bonds with a $34000 book value, yielding a $16000 gain.

A gain on retirement of debt is not part of operating activities, but financing activities. Thus, the 16,000 nonoperating gain is subtracted from net income.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin50

16-50

Cash flows from operating activitiesNet income 38,000$

Adjustments to accrual-basis net income: Depreciation expense 24,000$

Increase in accounts receivable (20,000) Increase in inventory (14,000) Increase in prepaid expenses (2,000) Decrease in accounts payable (5,000) Decrease in interest payable (1,000) Increase in income taxes payable 10,000 Loss on sale of plant assets 6,000 Gain on retirement of bonds (16,000) Total adjustments (18,000)

Net cash provided by operating activities 20,000

GENESIS CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin51

16-51

Cash Flow from InvestingCash Flow from Investing

(1) Identify changes in investing related accounts.

(2) Report their cash flow effects.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin52

16-52

Cash Flow from InvestingCash Flow from Investing

b. Purchased plant assets costing $70,000 by paying $10,000 cash and issuing $60,000 of bonds payable.

Dr. Plant assets 70,000 Cr. Bonds payable 60,000 Cr. Cash 10,000 Cash outflow for purchase of plant assets =

10,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin53

16-53

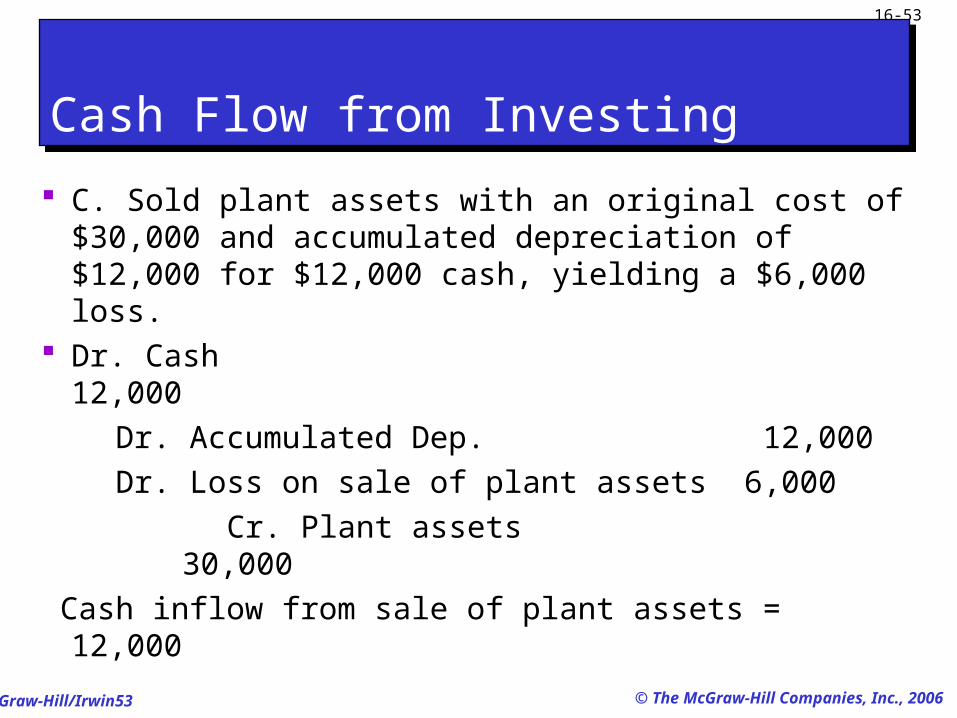

Cash Flow from InvestingCash Flow from Investing

C. Sold plant assets with an original cost of $30,000 and accumulated depreciation of $12,000 for $12,000 cash, yielding a $6,000 loss.

Dr. Cash 12,000 Dr. Accumulated Dep. 12,000 Dr. Loss on sale of plant assets 6,000 Cr. Plant assets 30,000 Cash inflow from sale of plant assets =

12,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin54

16-54

Cash flows from operating activitiesNet cash provided by operating activities 20,000 Cash flows from investing activities

Cash received from sale of plant assets 12,000

Purchase of plant assets (10,000) Net cash used by investing activities 2,000 Cash flows from financing activities

Genesis CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

Now, let’s complete the

financing section.

Now, let’s complete the

financing section.

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin55

16-55

Cash Flow from FinancingCash Flow from Financing

(1) Identify changes in financing related accounts.

(2) Report their cash flow effects

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin56

16-56

Cash Flow from FinancingCash Flow from Financing

Analysis of noncurrent liabilities e. Paid $18,000 cash to retire bonds with a

$34000 book value, yielding a $16,000 gain.

Dr. Bonds payable 34,000 Cr. Gain on retirement of debt 16,000 Cr. Cash 18,000 Cash paid to retire bonds = 18,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin57

16-57

Cash Flow from FinancingCash Flow from Financing

Analysis of equity d. Received cash of $15,000 from issuing

3,000 shares of common stock. Dr. Cash 15,000 Cr. Common Stock 15,000

Cash received from issuing stock = 15,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin58

16-58

Cash Flow from FinancingCash Flow from Financing

f. Cash dividends declared and paid were $14,000.

Dr. Retained earnings 14,000

Cr. Cash 14,000

Cash paid for dividends = 14,000

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin59

16-59

Cash flows from operating activitiesNet cash provided by operating activities 20,000 Cash flows from investing activities

Cash received from sale of plant assets 12,000

Purchase of plant assets (10,000) Net cash used by investing activities 2,000 Cash flows from financing activities

Cash received from issuing stock 15,000 Cash paid to retire bonds (18,000) Cash paid for dividends (14,000) Net cash used in financing activities (17,000)

Net increase in cash 5,000 Cash balance at the beginning of year 12,000 Cash balance at the end of year 17,000$

Genesis CompanyStatement of Cash Flows

For the Year Ended December 31, 2005

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin60

16-60

Analyzing Cash Sources and UsesAnalyzing Cash Sources and Uses

BMX ATV Trex

90,000$ 40,000$ (24,000)$

26,000 (48,000) (25,000)

13,000 (27,000) 15,000$ 15,000$ 15,000$

Cash Flows of Competing Companiesall numbers in thousandsCash provided (used) by operating activities

Cash provided (used) by investing activities:

Repayment of debtNet increase (decrease) in cash

Proceeds from sale of operating assetsPurchase of operating assets

Cash provided (used) by financing activities:

Proceeds from issuance of debt

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin61

16-61

Homework for Chap 16Homework for Chap 16

Ex 16-1, 16-2 Problem 16-4A

© The McGraw-Hill Companies, Inc., 2006McGraw-Hill/Irwin62

16-62

End of Chapter 16End of Chapter 16