pwc tax services, south africa standing committee on finance submissions: draft 2010 taxation laws...

TRANSCRIPT

PwC

PwC Tax Services, South Africa

Standing Committee on Finance

Submissions:

Draft 2010 Taxation Laws Amendment Bills

David Lermer & (Prof) Osman Mollagee

1 June 2010

PricewaterhouseCoopers

• Initial focus today on policy matters

• More detailed technical submissions directly to NT & SARS

• Not EM sequence

• Concern/clarity around NT/SARS strategy

• Applaud initiatives to promote growth (e.g. Gateway into Africa)

Opening remarks

June 2010Slide 2

Submissions on Draft 2010 Taxation Laws Amendment Bills

Submissions

I. Consultation Period

II. Specific V General Anti-avoidance provisions

III. Interest exemption: Natural persons

IV. Interest exemption: Non-residents

V. Denial of interest deductions

VI. Employee share schemes: Denial of Dividend exemption

VII. Regional investment funds

VIII. Rates & Thresholds

IX. Transfer pricing

X. Discretion to waive interest

PricewaterhouseCoopers

• Very short consultation period — AGAIN

• Complexity and volume

– Seasoned tax practitioners require more time. What about average taxpayers

• No chance of further debate after today

– Further submissions to NT/SARS —but not to Standing Committee

– Need for rebuttal acknowledged previously

– Money Bill

I. Consultation Period

June 2010Slide 4

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

• The GAAR (general anti-avoidance rule)

• Substantial time and effort to develop and legislate

• Why the reluctance to apply it?

• Specific anti-avoidance rules

• Complicate our tax law

• Weaken the GAAR

• Notoriously difficult to attack only the specified targets

II. Anti-avoidance Rules– Specific V General

June 2010Slide 5

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

TLAB: cl 19 EM: 2.4 ITA: s10C

• Negative impact on small business access to funds

• Discourages loans from private individuals

• Increases cost of finance

• Perceived “distortion” overstated

• Bigger distortion created by non-deductibility

III. Restriction of Interest Exemption– Natural Persons

June 2010Slide 6

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

TLAB: cl 18 EM: 5.2 ITA: s10B

• Discourages foreign direct investment (& undermines HQ regime)

• Perceived abuses adequately addressed elsewhere

• Likely to be ineffective (double tax treaties & local interest deductions)

• Administratively burdensome and potentially impossible to police

• Consider a Withholding Tax?

IV. Restriction of Interest Exemption– Non-residents

June 2010Slide 7

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

TLAB: cl 42 EM: 4.1 ITA: s23K

• Too broad & far-reaching

• Focus appears to be on banks, but proposed legislation targets taxpayers

in general

• Ignores fundamental income tax principles: Investment in shares can be to

produce taxable income

• Direct allocation based on exempt income unfair and too simplistic

• Discourages repatriation of foreign dividends

V. Denial of Interest Deduction– Prevention of Financial Instrument Mismatches

June 2010Slide 8

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

TLAB: cl 17(1)(l) EM: 2.9 ITA: s10(1)(k)(i)

• Denial of exemption creates a mismatch (double taxation)

• Taxation of employee

• Without any deduction for employer

• Deduction required to preserve equity and fairness

VI. Employee Share Schemes– Denial of dividend exemption

June 2010Slide 9

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

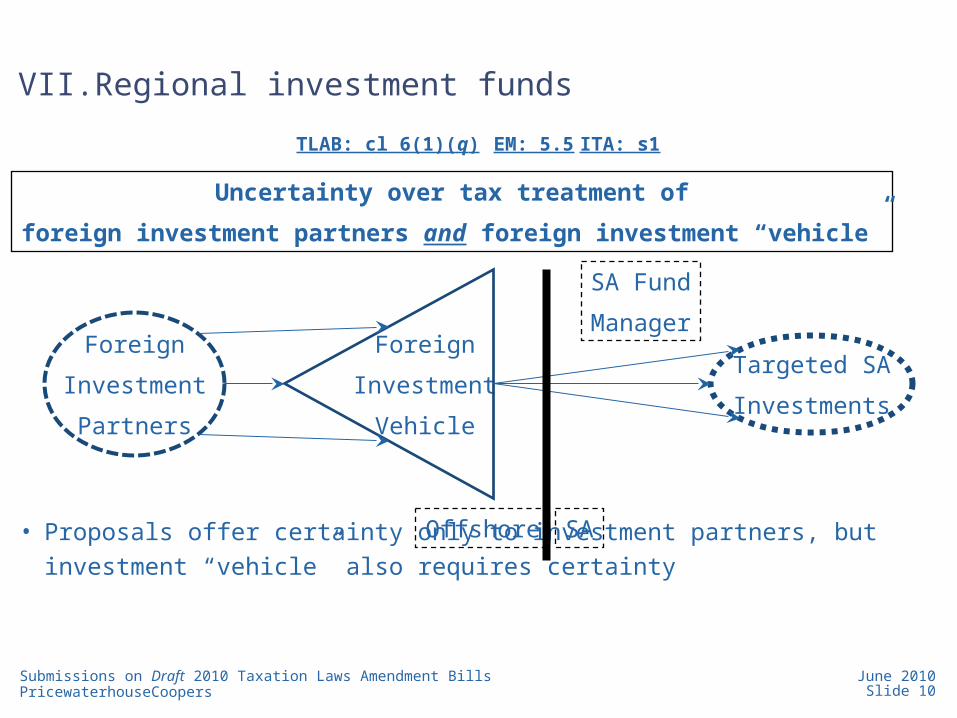

TLAB: cl 6(1)(q) EM: 5.5 ITA: s1

• Proposals offer certainty only to investment partners, but investment “vehicle”

also requires certainty

VII. Regional investment funds

June 2010Slide 10

Submissions on Draft 2010 Taxation Laws Amendment Bills

Foreign

Investment

Vehicle

SA Fund

ManagerForeign

Investment

Partners

Targeted SA

Investments

SAOffshore

Uncertainty over tax treatment of

foreign investment partners and foreign investment “vehicle”

PricewaterhouseCoopers

TLAB: Appendix 1 EM: 1 ITA: s5

• Not doing enough to address fiscal drag

VIII.Rates & Thresholds

June 2010Slide 11

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

TLAB: cl 53 EM: 5.3 ITA: s31

• Applaud modernisation of SA’s TP provisions

• But concern over inflexible penalty on adjustments

• STC

• Interest

IX. Transfer Pricing

June 2010Slide 12

Submissions on Draft 2010 Taxation Laws Amendment Bills

PricewaterhouseCoopers

TL 2nd AB: Part A & cl 17(1) Part B OM: 2.1–2.11 ITA: s89quat

• Removal of possibility of interest-waiver

• Ostensibly in favour of VDP

• Many other scenarios (besides VDP) merit waiver-of-interest

• Outright withdrawal is inappropriate

IX. Discretion to waive interest

June 2010Slide 13

Submissions on Draft 2010 Taxation Laws Amendment Bills

PwC

Thank you

© 2010 PricewaterhouseCoopers Inc. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. PricewaterhouseCoopers Inc is an authorised financial services provider.