· pricing supplement (incorporated with limited liability under the laws of the republic of...

TRANSCRIPT

PRICING SUPPLEMENT

(incorporated with limited liability under the laws of the Republic of Korea) (acting through its principal office in Korea)

Issue of US$300,000,000 Floating Rate Notes due 2023 under the US$8,000,000,000 G l o b a l M e d i u m T e r m N o t e P r o g r a m m e

THE NOTES TO WHICH THIS PRICING SUPPLEMENT RELATES (THE NOTES) HAVE NOT BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE SECURITIES ACT), OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND, UNLESS SO REGISTERED, MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE SECURITIES LAWS. ACCORDINGLY, THE NOTES WILL BE OFFERED AND SOLD ONLY OUTSIDE THE UNITED STATES TO NON-U.S. PERSONS IN RELIANCE ON REGULATION S.

Joint Bookrunner and Lead Manager

STANDARD CHARTERED BANK (TAIWAN) LIMITED

Joint Bookrunner and Manager

SG SECURITIES (HK) LIMITED, TAIPEI BRANCH

Co-Managers

KGI BANK KGI SECURITIES CO. LTD.

CTBC BANK CO., LTD. PRESIDENT SECURITIES CORPORATION

THE SHANGHAI COMMERCIAL & SAVINGS BANK MEGA INTERNATIONAL COMMERCIAL BANK

CO., LTD.

TAIPEI FUBON COMMERCIAL BANK CO., LTD. FUBON SECURITIES CO., LTD.

E.SUN COMMERCIAL BANK, LTD. TAISHIN INTERNATIONAL BANK CO., LTD.

The date of this Pricing Supplement is 12 March 2018.

PRICING SUPPLEMENT 12 March 2018

KOOKMIN BANK

(acting through its principal office in Korea) Issue of US$300,000,000 Floating Rate Notes due 2023

under the US$8,000,000,000 Global Medium Term Note Programme

This document constitutes the Pricing Supplement relating to the issue of Notes described herein. The terms and conditions of the Notes (the “Conditions”) shall consist of the terms and conditions set out under the heading “Terms and Conditions of the Notes” in the Offering Circular dated 3 April 2017, as supplemented by the Supplemental Offering Circular dated 25 August 2017 (together, the “Offering Circular”), as amended or supplemented, as the case may be, in this Pricing Supplement. Terms used herein shall be deemed to be defined as such for the purposes of the Conditions set forth in the Offering Circular. This Pricing Supplement contains the final terms of the Notes and must be read in conjunction with the Offering Circular.

The Notes have not been and will not be registered under the Financial Services Commission of Korea under the Financial Investment Services and Capital Markets Act of Korea. Accordingly, the Notes may not be offered, sold or delivered, directly or indirectly, in Korea or to, or for the account or benefit of, any resident of Korea (as such term is defined under the Foreign Exchange Transaction Law of Korea and its Enforcement Decree), except as otherwise permitted under applicable Korean laws and regulations. In addition, during the first year after the issuance of the Notes, the Notes may not be transferred to any resident of Korea other than a Korean QIB who is registered with KOFIA as a Korean QIB and subject to the requirement of monthly reports with the KOFIA of its holding of Korean QIB bonds as defined in the Regulation on Issuance, Public Disclosure, etc. of Securities of Korea, provided that (a) the Notes are denominated, and the principal and interest payments thereunder are made, in a currency other than Korean won, (b) the amount of the Notes acquired by such Korean QIBs in the primary market is limited to less than 20% of the aggregate issue amount of the Notes, (c) the Notes are listed on one of the major overseas securities markets designated by the Financial Supervisory Service of Korea, or certain procedures, such as registration or report with a foreign financial investment regulator, have been completed for offering of the Notes in a major overseas securities market, (d) the one-year restriction on offering, delivering or selling of Notes to a Korean resident other than a Korean QIB is expressly stated in the Notes, the relevant purchase agreement and offering circular and (e) the Company and the Initial Purchasers shall individually or collectively keep the evidence of fulfillment of conditions (a) through (d) above after having taken necessary actions therefor.

1. Issuer: Kookmin Bank (acting through its principal office in Korea)

2. (i) Series Number: 2018-3

(ii) Tranche Number: 1

3. Specified Currency or Currencies: United States dollars (US$)

4. Aggregate Nominal Amount:

(i) Series: US$300,000,000

(ii) Tranche: US$300,000,000

5. (i) Issue Price: 100.00% of the Aggregate Nominal Amount

(ii) Net Proceeds: US$299,400,000

6. (i) Specified Denominations: (in the case of Registered Notes, this means the minimum integral amount in which transfers can be

US$200,000 and, in excess thereof, integral multiples of US$1,000

made)

(ii) Calculation Amount: US$1,000

7. (i) Issue Date: 3 April 2018

(ii) Interest Commencement Date: Issue Date

8. Maturity Date: Interest Payment Date falling in or nearest to 3 April 2023

9. Interest Basis: Three month US$ LIBOR + 0.78% per annum (further particulars specified below)

10. Redemption/Payment Basis: Redemption at par

11. Change of Interest Basis or Redemption/ Payment Basis:

Not Applicable

12. Put/Call Options: Not Applicable

13. Status of the Notes: Senior

14. Listing: Singapore Exchange Securities Trading Limited (the “Singapore Stock Exchange”)

Taipei Exchange

Application will be made by the Issuer to the Taipei Exchange (the “TPEx”) for the listing and trading of the Notes on the TPEx. TPEx is not responsible for the content of this document and the Offering Circular and any amendment and supplement thereto and no representation is made by TPEx to the accuracy or completeness of this document and the Offering Circular and any amendment and supplement thereto. TPEx expressly disclaims any and all liability for any losses arising from, or as a result of the reliance on, all or part of the contents of this document and the Offering Circular and any amendment and supplement thereto. Admission to the listing and trading of the Notes on the TPEx shall not be taken as an indication of the merits of the Issuer or the Notes. The Notes will be traded on the TPEx pursuant to the applicable rules of the TPEx. Effective date of listing of the Notes is on or about 3 April 2018

15. Method of distribution: Syndicated

Provisions Relating to Interest (if any) Payable

16. Fixed Rate Note Provisions Not Applicable

17. Floating Rate Note Provisions Applicable

(i) Specified Period(s)/ Specified Interest Payment Dates:

3 April, 3 July, 3 October and 3 January of each year, beginning 3 July 2018, up to and including the Maturity Date

(ii) Business Day Convention: Modified Following Business Day Convention

(iii) Additional Business Centre(s): Taipei

(iv) Manner in which the Rate of Interest and Interest Amount are to be determined:

Screen Rate Determination

(v) Party responsible for calculating the Rate of Interest and Interest Amount (if not the Agent):

Not Applicable

(vi) Screen Rate Determination:

—Reference Rate and Relevant Financial Centre:

Reference Rate: Three month US$ LIBOR

Relevant Financial Centre: London

—Interest Determination Date(s): Two London business days prior to the start of each Interest Period

—Relevant Screen Page: Reuters screen page “LIBOR01”

(vii) ISDA Determination: Not Applicable

(viii) Margin(s): + 0.78% per annum

(ix) Minimum Rate of Interest: Not Applicable

(x) Maximum Rate of Interest: Not Applicable

(xi) Day Count Fraction: Actual/360, adjusted

(xii) Fall back provisions, rounding provisions and any other terms relating to the method of calculating interest on Floating Rate Notes, if different from those set out in the Conditions:

Not Applicable

18. Zero Coupon Note Provisions Not Applicable

19. Index Linked Note Provisions Not Applicable

20. Dual Currency Note Provisions Not Applicable

Provisions Relating to Redemption

21. Issuer Call Not Applicable

22. Investor Put Not Applicable

23. Final Redemption Amount of each Note:

Par

24. Early Redemption Amount of each Note payable on redemption for taxation reasons or on event of default and/or the method of calculating the same (if required or if different from

Condition 7(e) applies

that set out in Condition 7(e)):

General Provisions Applicable to the Notes

25. Form of Notes: Registered Notes:

Regulation S Global Note (US$300,000,000 nominal amount) registered in the name of a nominee for a common depositary for Euroclear and Clearstream, Luxembourg

26. Additional Financial Centre(s) or other special provisions relating to Payment Dates:

Seoul, Taipei, London and New York City

27. Talons for future Coupons or Receipts to be attached to Definitive Bearer Notes (and dates on which such Talons mature):

No

28. Details relating to Partly Paid Notes: amount of each payment comprising the Issue Price and date on which each payment is to be made and consequences of failure to pay, including any right of the Issuer to forfeit the Notes and interest due on late payment:

Not Applicable

29. Details relating to Instalment Notes:

(i) Instalment Amount(s): Not Applicable

(ii) Instalment Date(s): Not Applicable

30. Redenomination applicable: Redenomination not applicable

31. Other terms or special conditions: Not Applicable

Distribution

32. (i) If syndicated, names of Managers: Lead ManagerStandard Chartered Bank (Taiwan) Limited

Joint ManagerSG Securities (HK) Limited, Taipei Branch

Co-ManagersKGI Bank KGI Securities Co. Ltd. CTBC Bank Co., Ltd. President Securities Corporation The Shanghai Commercial & Savings Bank, Ltd. Mega International Commercial Bank Co., Ltd. Taipei Fubon Commercial Bank Co., Ltd. Fubon Securities Co., Ltd. E.SUN Commercial Bank, Ltd. Taishin International Bank Co., Ltd.

(ii) Stabilising Manager(s) (if any): Not Applicable

33. If non-syndicated, name of relevant Dealer:

Not Applicable

34. U.S. Selling Restrictions: Reg. S Compliance Category 2, TEFRA not applicable

35. Additional selling restrictions: The Notes have not been, and shall not be, offered, sold or re-sold, directly or indirectly to investors other than "professional investors" as defined under the Article 2-1 of the Taipei Exchange Rules Governing Management of Foreign Currency Denominated International Bonds (the “TPEx Rules”). Purchasers of the Notes are not permitted to sell or otherwise dispose of the Notes except by transfer to a Professional Investor.

Under the TPEx Rules, "professional investors" include "professional institutional investors" as defined under Paragraph 2 of Article 4 of the Financial Consumer Protection Act of the ROC.

Operational Information

36. Any clearing system(s) other than DTC, Euroclear and Clearstream, Luxembourg and the relevant identification number(s):

Not Applicable

37. Delivery: Delivery against payment

38. Additional Paying Agent(s) (if any): Not Applicable

39. Registrar: The Bank of New York Mellon SA/NV, Luxembourg Branch

40. Fiscal Agent and Common Depositary: The Bank of New York Mellon, London Branch

41. ISIN: XS1793243939

Common Code: 179324393

LISTING APPLICATION

This Pricing Supplement comprises the details required to list the issue of Notes described herein pursuant to the US$8,000,000,000 Global Medium Term Note Programme of Kookmin Bank.

The Singapore Stock Exchange assumes no responsibility for the correctness of any of the statements made or opinions expressed or reports contained in this Pricing Supplement. Approval in-principle from, admission to the Official List of, and quotation of any Notes on, the Singapore Stock Exchange is not to be taken as an indication of the merits of Kookmin Bank, the Programme or the Notes.

TPEx is not responsible for the content of this document and the Offering Circular and any amendment and supplement thereto and no representation is made by TPEx to the accuracy or completeness of this document and the Offering Circular and any amendment and supplement thereto. TPEx expressly disclaims any and all liability for any losses arising from, or as a result of the reliance on, all or part of the contents of this document and the Offering Circular and any amendment and supplement thereto. Admission to the listing and trading of the Notes on the TPEx shall not be taken as an indication of the merits of the Issuer or the Notes. The Notes will be traded on the TPEx pursuant to the applicable rules of the TPEx. Effective date of listing of the Notes is on or about 3 April 2018.

RESPONSIBILITY

The Issuer accepts responsibility for the information contained in this Pricing Supplement.

SCHEDULE A – RISK FACTORS RELATING TO THE NOTES AND OTHER INFORMATION

ADDITIONAL RISKS

Application will be made for the listing of the Notes on the TPEx. No assurances can be given as to whether the

Notes will be, or will remain, listing on TPEx or whether a trading market for the Notes will develop or as to the

liquidity of any such trading market. If the Notes fail to or cease to be listed on the TPEx, certain investors may

not invest in, or continue to hold or invest in, the Notes.

ROC TAXATION

The following is a general description of the principal ROC tax consequences for investors receiving interest in

respect of, or disposing of, the Notes and is of a general nature based on the Issuer’s understanding of current

law and practice. It does not purport to be comprehensive and does not constitute legal or tax advice.

This general description is based upon the law as in effect on the date hereof and that the Notes will be issued,

offered, sold and re-sold to professional investors as defined under the Taipei Exchange Rules Governing

Management of Foreign Currency Denominated International Bonds only. This description is subject to change

potentially with retroactive effect. Investors should appreciate that, as a result of changing law or practice, the

tax consequences may be otherwise than as stated below. Investors should consult their professional advisers on

the possible tax consequences of subscribing for, purchasing, holding or selling the Notes.

Interest on the Notes

As the Issuer of the Notes is not a ROC statutory tax withholder, there is no ROC withholding tax on the

interest or deemed interest to be paid by the Issuer on the Notes.

Payments of interest or deemed interest under the Notes to an ROC individual holder are not subject to ROC

income tax as such payments received by him/her are not considered to be ROC-sourced income. However, such

holder must include the interest or deemed interest in calculating his/her basic income for the purpose of

calculating his/her alternative minimum tax (“AMT”), unless the sum of the interest or deemed interest and other

non- ROC-sourced income received by such holder and the person(s) who is (are) required to jointly file the tax

return in a calendar year is below $1 million New Taiwan Dollars ("NT$"). If the amount of the AMT exceeds

the annual income tax calculated pursuant to ROC Income Basic Tax Act (also known as the AMT Act), the

excess becomes such holder’s AMT payable.

ROC corporate holders must include the interest or deemed interest receivable under the Notes as part of

their taxable income and pay income tax at a flat rate of 20% (unless the total taxable income for a fiscal year is

under NT$500,000), as they are subject to income tax on their worldwide income on an accrual basis. The AMT

is not applicable.

Sale of the Notes

In general, the sale of corporate bonds or financial bonds is subject to 0.1% securities transaction tax (“STT”)

on the transaction price. However, Article 2-1 of the Securities Transaction Tax Act prescribes that STT will

cease to be levied on the sale of corporate bonds and financial bonds from 1 January 2010 to 31 December 2026.

Therefore, the sale of the Notes will be exempt from STT if the sale is conducted on or before 31 December 2026.

Starting from 1 January 2027, any sale of the Notes will be subject to STT at 0.1% of the transaction price, unless

otherwise provided by the tax laws that may be in force at that time.

Capital gains generated from the sale of bonds are exempt from income tax. Accordingly, ROC individual

and corporate holders are not subject to income tax on any capital gains generated from the sale of the Notes. In

addition, ROC individual holders are not subject to AMT on any capital gains generated from the sale of the

Notes. However, ROC corporate holders should include the capital gains in calculating their basic income for the

purpose of calculating their AMT. If the amount of the AMT exceeds the annual income tax calculated pursuant

to the ROC Income Basic Tax Act (also known as the AMT Act), the excess becomes the ROC corporate holders’

AMT payable. Capital losses, if any, incurred by such holders could be carried over 5 years to offset against

capital gains of same category of income for the purposes of calculating their AMT.

Non-ROC corporate holders with a fixed place of business (e.g., a branch) or a business agent in the ROC are

not subject to income tax on any capital gains generated from the sale of the Notes. However, their fixed place of

business or business agent should include any such capital gains in calculating their basic income for the purpose

of calculating AMT.

As to non-ROC corporate holders without a fixed place of business and a business agent in the ROC, they are

not subject to income tax or AMT on any capital gains generated from the sale of the Notes.

ROC SETTLEMENT AND TRADING

Investors with a securities book-entry account with an ROC securities broker and a foreign currency deposit

account with an ROC bank, may request the approval of the Taiwan Depositary & Clearing Corporation

("TDCC") for the settlement of the Notes through the account of TDCC with Euroclear or Clearstream,

Luxembourg and if such approval is granted by TDCC, the Notes may be so cleared and settled. In such

circumstances, TDCC will allocate the respective book-entry interest of such investor in the Notes position to the

securities book-entry account designated by such investor in the ROC. The Notes will be traded and settled

pursuant to the applicable rules and operating procedures of TDCC and the TPEx as domestic bonds.

In addition, an investor may apply to TDCC (by filing in a prescribed form) to transfer the Notes in its own

account with Euroclear or Clearstream, Luxembourg to the TDCC account with Euroclear or Clearstream,

Luxembourg for trading in the domestic market or vice versa for trading in overseas markets.

For such investors who hold their interest in the Notes through an account opened and held by TDCC with

Euroclear or Clearstream, Luxembourg, distributions of principal and/or interest for the Notes to such holders

may be made by payment services banks whose systems are connected to TDCC to the foreign currency deposit

accounts of the holders. Such payment is expected to be made on the second Taiwanese business day following

TDCC’s receipt of such payment (due to time difference, the payment is expected to be received by TDCC one

Taiwanese business day after the distribution date). However, when the holders will actually receive such

distributions may vary depending upon the daily operations of the ROC banks with which the holder has the

foreign currency deposit account.

RECENT DEVELOPMENTS

The Issuer’s unaudited and unreviewed preliminary financial data as of and for the year ended 31

December 2017 and the three months ended 31 December 2017 have been publicly released as part of KB

Financial Group, Inc.’s preliminary results announcement and are not included in the Offering Circular or this

pricing supplement. The Issuer’s audited consolidated financial statements as of and for the year ended 31

December 2017 are expected to be released on 30 March 2018. Purchasers of the Notes are deemed to

acknowledge that the settlement of the Notes will occur after the release of the Issuer’s audited consolidated

financial statements as of and for the year ended 31 December 2017.

Kookmin Bank’s Unaudited Consolidated Interim Financial Statements as of and for the nine months

ended 30 September 2017

The Issuer’s unaudited consolidated interim financial statements as of and for the nine months ended 30

September 2017 are attached to the back of this pricing supplement beginning on the following page.

Kookmin Bank and SubsidiariesIndexSeptember 30, 2017 and 2016

Page(s)

Report on Review of Interim Consolidated Financial Statements......................... 1~2

Interim Consolidated Financial Statements

Interim Consolidated Statements of Financial Position................................................ 3

Interim Consolidated Statements of Comprehensive Income .…………………….…… 4

Interim Consolidated Statements of Changes in Equity................................................ 5

Interim Consolidated Statements of Cash Flows………………….…….........…………. 6

Notes to the Interim Consolidated Financial Statements…..……………………..... 7~161

Report on Review of Interim Consolidated Financial Statements

(English Translation of a Report Originally Issued in Korean)

To the Shareholder and Board of Directors of Kookmin Bank

Reviewed Financial StatementsWe have reviewed the accompanying interim consolidated financial statements of Kookmin Bank and itssubsidiaries (collectively the “Group”). These financial statements consist of the interim consolidatedstatement of financial position of the Group as of September 30, 2017, and the related interim consolidatedstatements of comprehensive income for the three-month and nine-month periods ended September 30,2017 and 2016, and interim consolidated statements of changes in equity and cash flows for the nine-monthperiods ended September 30, 2017 and 2016, and a summary of significant accounting policies and otherexplanatory notes, expressed in Korean won.

Management's Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these interim consolidated financialstatements in accordance with International Financial Reporting Standards as adopted by the Republic ofKorea (“Korean IFRS”) 1034, Interim Financial Reporting, and for such internal control as managementdetermines is necessary to enable the preparation of interim consolidated financial statements that are freefrom material misstatement, whether due to fraud or error.

Auditor's ResponsibilityOur responsibility is to issue a report on these interim consolidated financial statements based on ourreview.

We conducted our review in accordance with quarterly or semi-annual review standards established by theSecurities and Futures Commission of the Republic of Korea. A review of interim financial informationconsists of making inquiries, primarily of persons responsible for financial and accounting matters, andapplying analytical and other review procedures. A review is substantially less in scope than an auditconducted in accordance with Korean Standards on Auditing and consequently does not enable us toobtain assurance that we would become aware of all significant matters that might be identified in an audit.Accordingly, we do not express an audit opinion.

ConclusionBased on our review, nothing has come to our attention that causes us to believe the accompanying interimconsolidated financial statements are not presented fairly, in all material respects, in accordance withKorean IFRS 1034 Interim Financial Reporting.

Other MattersWe have audited the consolidated statement of financial position of the Group as of December 31, 2016,and the related consolidated statements of comprehensive income, changes in equity and cash flows forthe year then ended, in accordance with Korean Standards on Auditing. We expressed an unqualifiedopinion on those financial statements, not presented herein, in our audit report dated March 8, 2017. Theconsolidated statement of financial position as of December 31, 2016, presented herein for comparativepurposes, is consistent, in all material respects, with the above audited statement of financial position as ofDecember 31, 2016.

Review standards and their application in practice vary among countries. The procedures and practicesused in the Republic of Korea to review such financial statements may differ from those generally acceptedand applied in other countries.

November 13, 2017Seoul, Korea

This report is effective as of November 13, 2017, the review report date. Certain subsequentevents or circumstances, which may occur between the review report date and the time of readingthis report, could have a material impact on the accompanying interim consolidated financialstatements and notes thereto. Accordingly, the readers of the review report should understand thatthere is a possibility that the above review report may have to be revised to reflect the impact ofsuch subsequent events or circumstances, if any.

2

Kookmin Bank and SubsidiariesInterim Consolidated Statements of Financial PositionSeptember 30, 2017 and December 31, 2016

(In millions of Korean won) Notes

AssetsCash and due from financial institutions 4,6,7,36 18,739,502 14,681,846

4,6,8,12 8,906,835 7,956,232Derivative financial assets 4,6,9 1,591,665 2,796,445Loans 4,6,8,10,11 247,995,401 236,551,052Financial investments 4,6,8,12 38,630,206 35,732,406

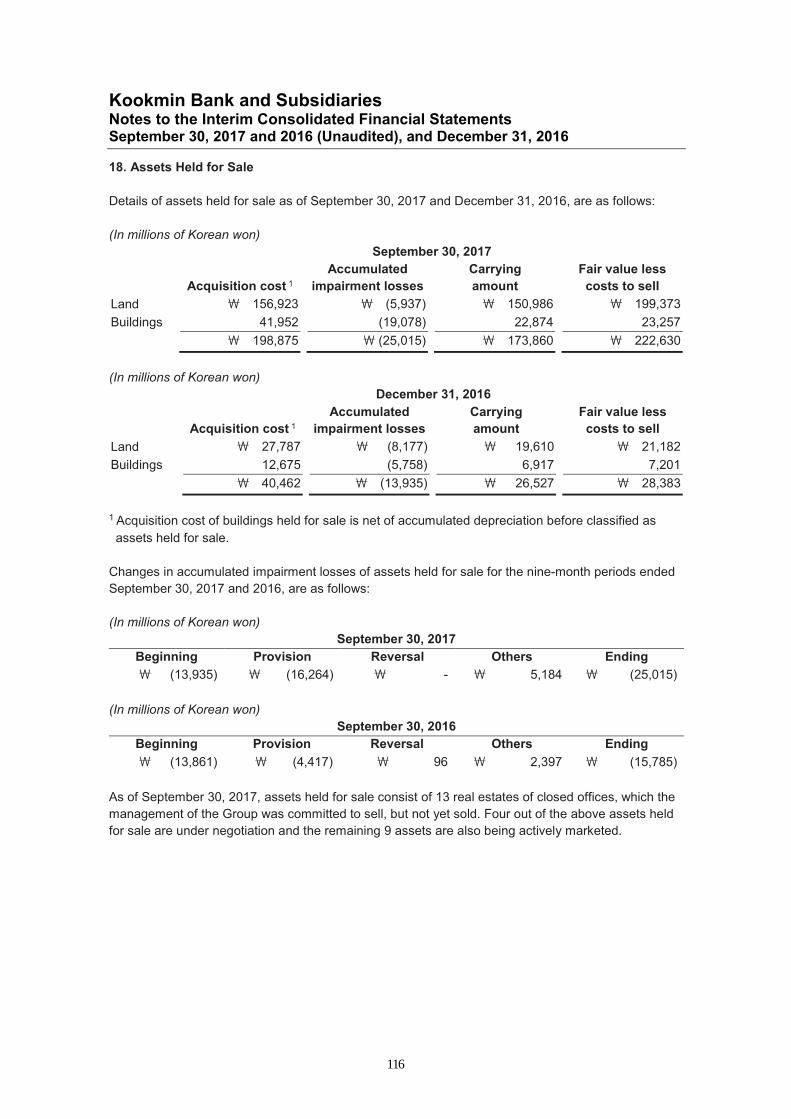

13 340,621 367,976Property and equipment 14 2,971,298 3,117,391Investment property 14 348,034 372,880Intangible assets 15 210,231 210,714Current income tax assets 32 13,905 11,937Deferred income tax assets 16,32 2,202 47,692Assets held for sale 18 173,860 26,527Other assets 4,6,17 6,683,504 5,193,272

Total assets 326,607,264 307,066,370

Liabilities4,6 72,215 73,238

Derivative financial liabilities 4,6,9 1,580,632 2,833,598Deposits 4,6,19 248,700,703 235,736,034Debts 4,6,20 17,776,492 15,934,409Debentures 4,6,21 18,511,721 14,959,692Provisions 22 401,147 425,284Net defined benefit liabilities 23 185,216 71,167Current income tax liabilities 32 2,652 5,357Deferred income tax liabilities 16,32 167,195 19Other liabilities 4,6,24,30 14,155,516 13,702,570

Total liabilities 301,553,489 283,741,368Equity 25

Capital stock 2,021,896 2,021,896Capital surplus 5,219,689 5,219,704Accumulated other comprehensive income 34 741,881 494,863Retained earnings 33 17,070,309 15,588,539(Provision of regulatory reserve for credit losses

September 30, 2017 : 2,001,063 million

December 31, 2016 : 1,835,115 million)(Amounts estimated to be appropriatedSeptember 30, 2017 : 141,477 millionDecember 31, 2016 : 165,948 million)

Equity attributable to the shareholder of the Parent Company 25,053,775 23,325,002Non-controlling interest equity - -Total equity 25,053,775 23,325,002Total liabilities and equity 326,607,264 307,066,370

Financial assets at fair value through profit or loss

Investments in associates

Financial liabilities at fair value through profit or loss

September 30, 2017(Unaudited)

December 31, 2016

The accompanying notes are an integral part of these interim consolidated financial statements.

3

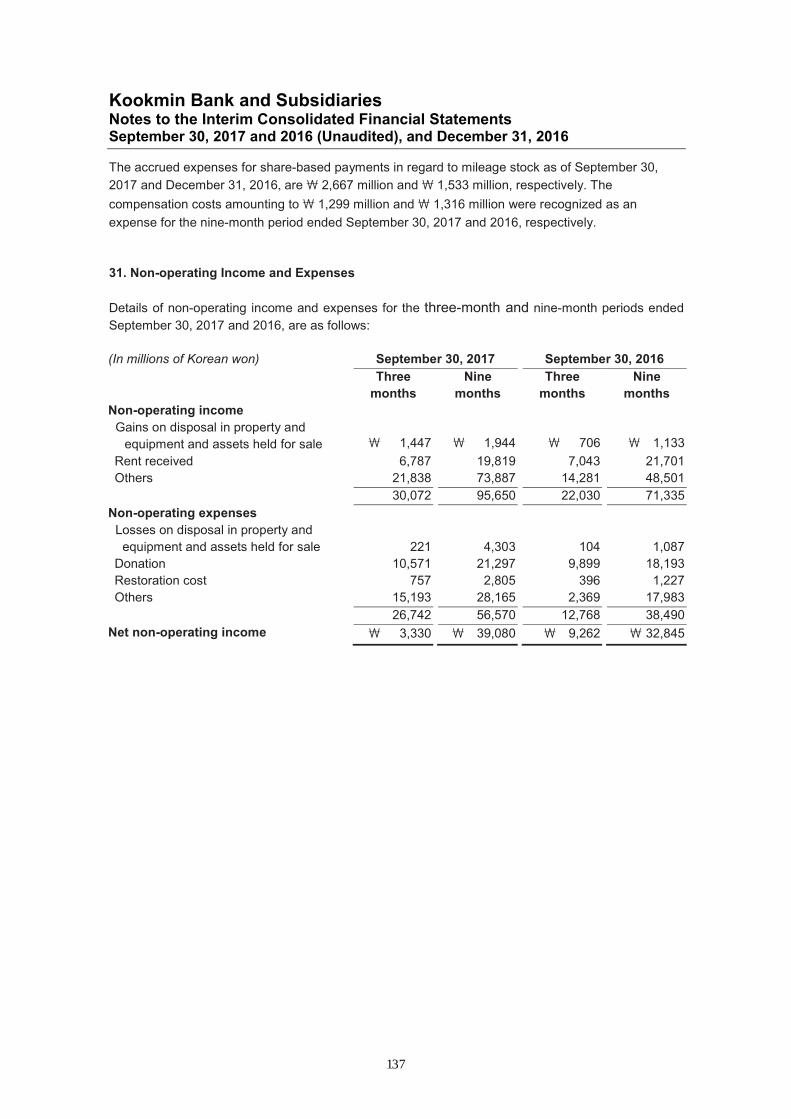

Kookmin Bank and SubsidiariesInterim Consolidated Statements of Comprehensive IncomeThree-Month and Nine-Month Periods Ended September 30, 2017 and 2016

(Unaudited) (Unaudited)Notes

Interest income 2,117,606 6,127,258 1,974,657 5,903,216Interest expense (730,176) (2,154,751) (750,778) (2,373,584)Net interest income 26 1,387,430 3,972,507 1,223,879 3,529,632

Fee and commission income 371,486 1,090,690 334,249 979,372Fee and commission expense (62,356) (180,698) (53,797) (160,039)Net fee and commission income 27 309,130 909,992 280,452 819,333

28 40,797 109,986 (35,371) 18,961

Net other operating income(expenses) 29 (87,587) (283,624) 8,384 (44,697)

General and administrative expenses 14,15,23,30,40 (771,145) (2,416,172) (804,224) (2,549,863)

878,625 2,292,689 673,120 1,773,366

11,17,22 (76,501) (169,053) (125,569) (294,100)

Operating profit 802,124 2,123,636 547,551 1,479,266

Share of profit of associates 13 17,381 31,186 3,413 8,573Other non-operating income 31 3,330 39,080 9,262 32,845Net non-operating income 20,711 70,266 12,675 41,418

Profit before income tax expense 822,835 2,193,902 560,226 1,520,684

Income tax expense 32 (190,801) (352,639) (138,458) (355,730)

Profit for the period 632,034 1,841,263 421,768 1,164,954

25September 30, 2017 (Nine months) : 1,699,786 millionSeptember 30, 2017 (Three months) : 582,811 millionSeptember 30, 2016 (Nine months) : 1,011,751 millionSeptember 30, 2016 (Three months) : 475,352 million)

Other comprehensive incomeItems that will not be reclassified to profit or loss:Remeasurements of net defined benefit liabilities 23 (1,782) (7,490) (1,399) (5,805)

Currency translation differences 13,177 (7,322) (43,143) (51,445)Gain on valuation financial investments 587 169,423 11,215 129,104

(995) 89,494 124 (775)

(3,953) 1,046 8,554 7,2161,442 1,867 164 (175)

34 8,476 247,018 (24,485) 78,120

Total comprehensive income for the period 640,510 2,088,281 397,283 1,243,074

Profit attributable to:Shareholder of the parent company 632,034 1,841,263 421,768 1,164,954Non-controlling interests - - - -

632,034 1,841,263 421,768 1,164,954Total comprehensive income for the period attributable to:Shareholder of the parent company 640,510 2,088,281 397,283 1,243,074Non-controlling interests - - - -

640,510 2,088,281 397,283 1,243,074

Gain(Loss) on cash flow hedging instruments

Net gain(loss) on financial assets/liabilitiesat fair value through profit or loss

Operating profit before provision forcredit losses

Provision for credit losses

(Adjusted profit after provision of regulatoryreserve for credit losses

Share of other comprehensive income(loss) ofassociatesGain(Loss) on hedging instruments ofa net investments in a foreign operations

Other comprehensive income(loss) for theperiod net of tax

Items that may be reclassified subsequently toprofit or loss:

Period Ended September 302017 2016

(In millions of Korean won) Three months Nine months Three months Nine months

The accompanying notes are an integral part of these interim consolidated financial statements.

4

KookminBankandSubsidiaries

Interim

ConsolidatedStatementsofChangesinEquity

Nine-MonthPeriodsEndedSeptember30,2017and2016

Accumulated

Other

(InmillionsofKoreanwon)

Capital

Capital

Com

prehensive

Retained

Non-controlling

Total

Stock

Surplus

Income

Earnings

interests

Equity

BalanceatJanuary1,2016

2,021,896

5,219,704

500,807

15,004,804

-22,747,211

Com

prehensiveincomefortheperiod

Profitfortheperiod

--

-1,164,954

-1,164,954

Remeasurementsofnetdefinedbenefitliabilities

--

(5,805)

--

(5,805)

Currencytranslationadjustments

--

(51,445)

--

(51,445)

Gainonvaluationoffinancialinvestments

--

129,104

--

129,104

Shareofothercomprehensivelossofassociates

--

(775)

--

(775)

Gainonhedginginstrumentsofanetinvestment

inaforeignoperations

--

7,216

--

7,216

Lossoncashflowhedginginstruments

--

(175)

--

(175)

Totalcom

prehensiveincomefortheperiod

--

78,120

1,164,954

-1,243,074

Transactionswith

theshareholder

Dividends

--

-(380,521)

-(380,521)

Totaltransactionswith

theshareholder

--

-(380,521)

-(380,521)

BalanceatSeptember30,2016(Unaudited)

2,021,896

5,219,704

578,927

15,789,237

-23,609,764

BalanceatJanuary1,2017

2,021,896

5,219,704

494,863

15,588,539

-23,325,002

Com

prehensiveincomefortheperiod

Profitfortheperiod

--

-1,841,263

-1,841,263

Remeasurementsofnetdefinedbenefitliabilities

--

(7,490)

--

(7,490)

Currencytranslationadjustments

--

(7,322)

--

(7,322)

Gainonvaluationoffinancialinvestments

--

169,423

--

169,423

Shareofothercomprehensiveincomeofassociates

--

89,494

--

89,494

Gainonhedginginstrumentsofnetinvestments

inforeignoperations

--

1,046

--

1,046

Gainoncashflowhedginginstruments

--

1,867

--

1,867

Totalcom

prehensiveincomefortheperiod

--

247,018

1,841,263

-2,088,281

Transactionswith

theshareholder

Dividends

--

-(359,493)

-(359,493)

Changesinownershipinterestsinsubsidiaries

-(15)

--

-(15)

Totaltransactionswith

theshareholder

-(15)

-(359,493)

-(359,508)

BalanceatSeptember30,2017(Unaudited)

2,021,896

5,219,689

741,881

17,070,309

-25,053,775

AttributabletotheshareholderoftheParentCompany

Theaccompanyingnotesareanintegralpartoftheseinterim

consolidatedfinancialstatements.

5

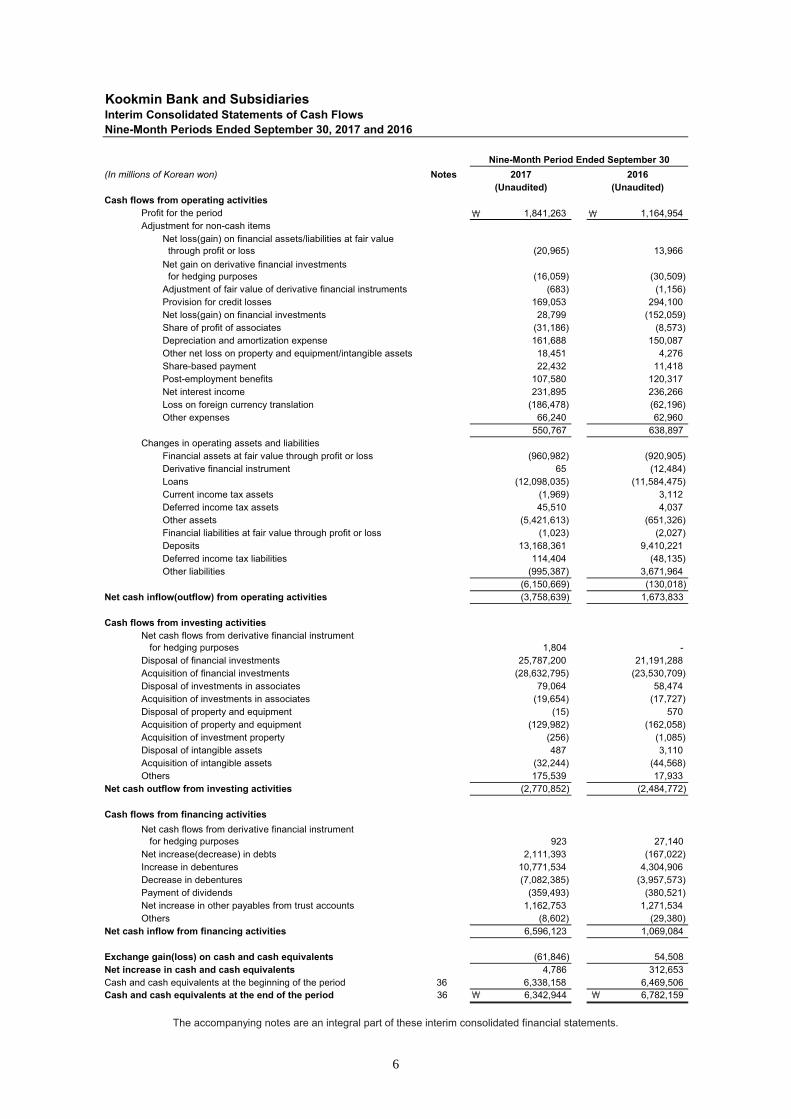

Kookmin Bank and SubsidiariesInterim Consolidated Statements of Cash FlowsNine-Month Periods Ended September 30, 2017 and 2016

(In millions of Korean won) Notes

Cash flows from operating activitiesProfit for the period 1,841,263 1,164,954Adjustment for non-cash items

Net loss(gain) on financial assets/liabilities at fair valuethrough profit or loss (20,965) 13,966Net gain on derivative financial investmentsfor hedging purposes (16,059) (30,509)Adjustment of fair value of derivative financial instruments (683) (1,156)Provision for credit losses 169,053 294,100Net loss(gain) on financial investments 28,799 (152,059)Share of profit of associates (31,186) (8,573)Depreciation and amortization expense 161,688 150,087Other net loss on property and equipment/intangible assets 18,451 4,276Share-based payment 22,432 11,418Post-employment benefits 107,580 120,317Net interest income 231,895 236,266Loss on foreign currency translation (186,478) (62,196)Other expenses 66,240 62,960

550,767 638,897Changes in operating assets and liabilities

Financial assets at fair value through profit or loss (960,982) (920,905)Derivative financial instrument 65 (12,484)Loans (12,098,035) (11,584,475)Current income tax assets (1,969) 3,112Deferred income tax assets 45,510 4,037Other assets (5,421,613) (651,326)Financial liabilities at fair value through profit or loss (1,023) (2,027)Deposits 13,168,361 9,410,221Deferred income tax liabilities 114,404 (48,135)Other liabilities (995,387) 3,671,964

(6,150,669) (130,018)Net cash inflow(outflow) from operating activities (3,758,639) 1,673,833

Cash flows from investing activities

1,804 -Disposal of financial investments 25,787,200 21,191,288Acquisition of financial investments (28,632,795) (23,530,709)Disposal of investments in associates 79,064 58,474Acquisition of investments in associates (19,654) (17,727)Disposal of property and equipment (15) 570Acquisition of property and equipment (129,982) (162,058)Acquisition of investment property (256) (1,085)Disposal of intangible assets 487 3,110Acquisition of intangible assets (32,244) (44,568)Others 175,539 17,933

Net cash outflow from investing activities (2,770,852) (2,484,772)

Cash flows from financing activities

923 27,140Net increase(decrease) in debts 2,111,393 (167,022)Increase in debentures 10,771,534 4,304,906Decrease in debentures (7,082,385) (3,957,573)Payment of dividends (359,493) (380,521)Net increase in other payables from trust accounts 1,162,753 1,271,534Others (8,602) (29,380)

Net cash inflow from financing activities 6,596,123 1,069,084

Exchange gain(loss) on cash and cash equivalents (61,846) 54,508Net increase in cash and cash equivalents 4,786 312,653Cash and cash equivalents at the beginning of the period 36 6,338,158 6,469,506Cash and cash equivalents at the end of the period 36 6,342,944 6,782,159

Net cash flows from derivative financial instrumentfor hedging purposes

Net cash flows from derivative financial instrumentfor hedging purposes

Nine-Month Period Ended September 30

(Unaudited) (Unaudited)2017 2016

The accompanying notes are an integral part of these interim consolidated financial statements.

6

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

1. The Bank

Kookmin Bank (the “Bank”) was incorporated in 1963 under the Citizens National Bank Act to providebanking services to the general public and to small and medium-sized enterprises. Pursuant to theRepeal Act of the Citizens National Bank Act, effective January 5, 1995, the Bank’s status changed toa financial institution which operates under the Banking Act and Commercial Act.

The Bank merged with Korea Long Term Credit Bank on December 31, 1998, and with itssubsidiaries, Daegu, Busan, Jeonnam Kookmin Mutual Savings & Finance Co., Ltd., on August 22,1999. Pursuant to the directive from the Financial Services Commission related to the StructuralImprovement of the Financial Industry Act, the Bank acquired certain assets, including performingloans, and assumed most of the liabilities of Daedong Bank on June 29, 1998. Also, the Bankcompleted the merger with Housing and Commercial Bank (“H&CB”) on October 31, 2001, andmerged with Kookmin Credit Card Co., Ltd., a majority-owned subsidiary, on September 30, 2003.Meanwhile, the Bank spun off its credit card business segment on February 28, 2011, and KBKookmin Card Co., Ltd. became a subsidiary of KB Financial Group Inc.

The Bank listed its shares on the Stock Market Division of the Korea Exchange (“KRX,” formerlyKorea Stock Exchange) in September 1994. As a result of the merger with H&CB, the shareholder ofthe former Kookmin Bank and H&CB received new common shares of the Bank which were relistedon the KRX on November 9, 2001. In addition, H&CB listed its American Depositary Shares (“ADS”)on the New York Stock Exchange (“NYSE”) on October 3, 2000, prior to the merger. Following themerger with H&CB, the Bank listed its ADS on the NYSE on November 1, 2001. The Bank became awholly owned subsidiary of KB Financial Group Inc. through a comprehensive stock transfer onSeptember 29, 2008. Subsequently, the Bank’s shares and its ADS, each listed on the KRX and theNYSE, were delisted on October 10, 2008 and September 26, 2008, respectively. As of September30, 2017, the Bank’s paid-in capital is 2,021,896 million.

The Bank engages in the banking business in accordance with the Banking Act, trust business inaccordance with the Financial Investment Services and Capital Markets Act, and other relevantbusinesses. As of September 30, 2017, the Bank operates 1,062 domestic branches and offices, andfive overseas branches (excluding five subsidiaries and three offices).

7

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

2. Basis of Preparation

2.1 Application of Korean IFRS

The Group maintains its accounting records in Korean won and prepares statutory financialstatements in the Korean language (Hangul) in accordance with Korean IFRS. The accompanyinginterim consolidated financial statements have been condensed, restructured and translated intoEnglish from the Korean language financial statements.

The interim consolidated financial statements of the Bank and its subsidiaries (collectively the“Group”) have been prepared in accordance with Korean IFRS. These are the standards and relatedinterpretations issued by the International Accounting Standards Board (“IASB”) that have beenadopted by the Republic of Korea.

The preparation of the interim consolidated financial statements requires the use of certain criticalaccounting estimates. It also requires management to exercise judgment in the process of applyingthe Group’s accounting policies. The areas involving a higher degree of judgment or complexity, orareas where assumptions and estimates are significant to the interim consolidated financialstatements are disclosed in Note 2.4.

The Group’s interim consolidated financial statements for the nine-month period ended September30, 2017, have been prepared in accordance with Korean IFRS 1034 Interim Financial Reporting.These interim consolidated financial statements have been prepared in accordance with Korean IFRSstandards issued and early adopted at the end of the reporting period.

The Group newly applied the following amended and enacted standards and interpretations for theannual period beginning on January 1, 2017, and this application does not have a material impact onthe interim consolidated financial statements.

- Amendments to Korean IFRS 1007 Statement of Cash Flows- Amendments to Korean IFRS 1012 Income Tax- Amendments to Korean IFRS 1112 Disclosure of Interests in Other Entities: Exemption forconsolidation of investee

Also, new standards and interpretations issued but not effective for the financial period beginningJanuary 1, 2017, and not early adopted are as follows:

- Amendments to Korean IFRS 1028 Investments in Associates and Joint Ventures

When an investment in an associate or a joint venture is held by, or it held indirectly through, an entitythat is a venture capital organization, or a mutual fund and similar entities, the entity may elect tomeasure that investment at fair value through profit or loss. The amendments clarify that an entityshall make this election separately for each associate of joint venture, at initial recognition of theassociate or joint venture. The Group will apply these amendments retrospectively for annual periodsbeginning on or after January 1, 2018, and early adoption is permitted. The Group does not expectthe amendments to have a significant impact on the consolidated financial statements.

8

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

- Amendments to Korean IFRS 1102 Share-based Payment

This amendment clarifies accounting for a modification to the terms and conditions of a share-basedpayment that changes the classification of the transaction from cash-settled to equity-settled. Also,clarifies that the measurement approach should treat the terms and conditions of a cash-settledaward in the same way as for an equity-settled award. The Group will apply the amendments forannual periods beginning on or after January 1, 2018 with early application permitted. The Groupdoes not expect the amendment to have a significant impact on the consolidated financial statements.

- Enactments of Interpretation 2122 Foreign Currency Transactions and Advance Consideration

According to these enactments, the date of the transaction for the purpose of determining theexchange rate to use on initial recognition of the related asset, expense or income (or part of it) is thedate on which an entity initially recognizes the non-monetary asset or non-monetary liability arisingfrom the payment or receipt of advance consideration. If there are multiple payments or receipts inadvance, the entity shall determine a date of the transaction for each payment or receipt of advanceconsideration. These enactments will be effective for annual periods beginning on or after January 1,2018, with early adoption permitted. The Group does not expect the enactments to have a significantimpact on the consolidated financial statements.

- Korean IFRS 1109 Financial Instruments

The new standard for financial instruments issued on September 25, 2015 is effective for annualperiods beginning on or after January 1, 2018 with early application permitted. This standard willreplace Korean IFRS 1039 Financial Instruments: Recognition and Measurement. The Group willapply the standards for annual periods beginning on or after January 1, 2018.

The standard requires retrospective application with some exceptions. For example, the entity is notrequired to restate prior periods in relation to classification and measurement (including impairment)of financial instruments. The standard requires prospective application of its hedge accountingrequirements for all hedging relationships except the accounting for time value of options and otherexceptions.

Korean IFRS 1109 Financial Instruments requires all financial assets to be classified and measuredon the basis of the entity’s business model for managing financial assets and the contractual cashflow characteristics of the financial assets. A new impairment model, an expected credit loss model, isintroduced and any subsequent changes in expected credit losses will be recognized in profit or loss.Also, hedge accounting rules amended to extend the hedging relationship, which consists only ofeligible hedging instruments and hedged items, qualifies for hedge accounting.

An effective implementation of Korean IFRS 1109 requires preparation processes including financialimpact assessment, accounting policy establishment, accounting system development and thesystem stabilization. The impact on the Group’s financial statements due to the application of thestandard is dependent on judgements made in applying the standard, financial instruments held bythe Group and macroeconomic variables.

9

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

Within the Group, Korean IFRS 1109 Task Force Team ('TFT') has been set up to prepare forimplementation of Korean IFRS 1109 since October 2015. There are three stages for implementationof Korean IFRS, such as analysis, design and implementation, and preparation for application. TheGroup is analyzing financial impacts of Korean IFRS 1109 on its consolidated financial statements.

The Group performed an impact assessment to identify potential financial effects of applying KoreanIFRS 1109. The assessment was performed based on retainable information as of June 30, 2017,and the results of the assessment are explained as below. The Group plans to perform more detailedanalysis on financial effects base on additional information in the future; therefore, the results of theassessment may change due to additional information that the Group may obtain after theassessment.

(a) Classification and Measurement of Financial Assets

When implementing Korean IFRS 1109, the classification of financial assets will be driven by theGroup’s business model for managing the financial assets and contractual terms of cash flow. Thefollowing table shows the classification of financial assets measured subsequently at amortized cost,at fair value through other comprehensive income and at fair value through profit or loss. If a hybridcontract contains a host that is a financial asset, the classification of the hybrid contract shall bedetermined for the entire contract without separating the embedded derivative.

Business modelContractual cash flows characteristics

Solely represent payments ofprincipal and interest All other

Hold the financial assetfor the collection of thecontractual cash flows

Measured at amortized cost 1

Recognized at fair valuethrough profit or loss 2

Hold the financial assetfor the collection of thecontractual cash flowsand trading

Recognized at fair value throughother comprehensive income 1

Hold for trading Recognized at fair value throughprofit or loss

1 A designation at fair value through profit or loss is allowed only if such designation mitigates anaccounting mismatch (irrevocable).

2 Equity investments not held for trading can be recorded in other comprehensive income (irrevocable).

Stage Period Process

1 From Oct. to Dec. 2015(for 3 months)

Analysis of GAAP differences and development ofmethodology

2 From Jan. to Dec. 2016(for 12 months)

Development of methodology, definition of businessrequirement, and the system development and test.

3From Jan. 2017to Mar. 2018(for 15 months)

Preparation for opening balances of the financial statements

10

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

With the implementation of Korean IFRS 1109, the criteria to classify the financial assets at amortizedcost or at fair value through other comprehensive income are more strictly applied than the criteriaapplied with Korean IFRS 1039. Accordingly, the financial assets at fair value through profit or loss mayincrease by implementing Korean IFRS 1109 and may result in an increased fluctuation in profit or loss.

According to Korean IFRS 1109, debt securities those contractual cash flows do not represent solelypayments of principal and interest and held for trading, and equity securities that are not designatedas instruments measured at fair value through other comprehensive income are measured at fairvalue through profit or loss. As of June 30, 2017, the Group holds debt securities, equity securitiesand other financial assets classified as financial assets at fair value through profit or loss that amountto 8,501,216 million, 155,387 million and 208,390 million, respectively.

Based on results from the impact assessment, if the Group applies Korean IFRS 1109 to the financialassets measured at fair value through profit or loss as of June 30, 2017, the application will not havea material impact on the financial statements because the majority of the financial assets will still beclassified as at fair value through profit or loss.

According to Korean IFRS 1109, a debt security is measured at fair value through othercomprehensive income if the objective of the business model is achieved both by collectingcontractual cash flows and selling financial assets; and the contractual cash flows represents solelypayments of principal and interest on a specific date under contract terms. As of June 30, 2017, theGroup holds debt securities and beneficiary securities of 26,289,316 million classified as financialassets available-for-sale.

Based on results from the impact assessment of Korean IFRS 1109, if Korean IFRS 1109 is appliedfor the above debt securities classified as financial assets available-for-sale, the Group expects themajority of the financial assets to be measured at fair value through other comprehensive income.Meanwhile, the beneficiary securities amounting to 3,994,282 million which of the contractual cashflows under the instrument do not solely represent payments of principal and interest on the principalamount, are measured at fair value through profit or loss, accordingly, the Group expects volatility inprofit or loss may be increased.

According to Korean IFRS 1109, equity securities that are not held for trading, the Group can makean irrevocable election at initial recognition to classify the instruments as assets measured at fairvalue through other comprehensive income, which all subsequent changes in fair value beingrecognized in other comprehensive income and not recycled to profit or loss. As of June 30, 2017, theGroup holds equity securities of 2,034,962 million classified as financial assets available-for-sale.

Based on results from the impact assessment of Korean IFRS 1109, the Group plans to designatemost equity securities as instruments measured at fair value through profit or loss except some equityinstruments, which are classified in financial assets available-for-sale, held for business agreementand investment purpose. Therefore, the Group expects the application of Korean IFRS 1109 on thesefinancial assets may increase volatility in profit or loss.

According to Korean IFRS 1109, a debt instrument is measured at amortized cost if: a) the objective ofthe business model is to hold the financial asset for the collection of the contractual cash flows, and b)the contractual cash flows under the instrument solely represent payments of principal and interest. Asof June 30, 2017, the Group measured loans and receivables of 242,661,130 million, cash and duefrom financial institutions of 15,237,433 million and financial assets held-to-maturity of 8,849,879million at amortized costs.

11

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

Based on results from the impact assessment, if the Group applies Korean IFRS 1109 to the abovefinancial assets, the application will not have a material impact on the financial statements. This isbecause the Group holds the majority of financial assets measured at amortized cost that meets theboth criteria: a) the objective of the business model is to hold the financial asset for the collection ofthe contractual cash flows, and b) the contractual cash flows under the instrument solely representpayments of principal and interest, although loans with conversion right and a part of due fromfinancial institutions which of contractual cash flows do not represent solely payments of principal andinterest are recognized at fair value through profit or loss.

(b) Classification and Measurement of Financial Liabilities

Korean IFRS 1109 requires the amount of the change in the liability’s fair value attributable tochanges in the credit risk to be recognized in other comprehensive income, unless this treatment ofthe credit risk component creates or enlarges a measurement mismatch. Amounts presented in othercomprehensive income are not subsequently transferred to profit or loss.

Based on results from the impact assessment of Korean IFRS 1109, the Group expects that theapplication will have no impact on the financial statements because the Group had no financialliabilities designated as at fair value through profit or loss as of June 30, 2017.

(c) Impairment: Financial Assets and Contract Assets

Korean IFRS 1109 sets out a new forward looking ‘expected loss’ impairment model which replacesthe incurred loss model under Korean IFRS 1039 that impaired assets if there is an objectiveevidence and applies to:

- Financial assets measured at amortized cost,- Debt investments measured at fair value through other comprehensive income- Lease receivables, and- Certain loan commitments and financial guaranteed contracts.

Under Korean IFRS 1109 ‘expected loss’ model, a credit event (or impairment ‘trigger’) no longer hasto occur before credit losses are recognized. The Group will always recognize (at a minimum) 12-month expected credit losses in profit or loss. Lifetime expected losses will be recognized on assetsfor which there is a significant increase in credit risk after initial recognition.

Stage Loss allowance

1 No significant increase in creditrisk after initial recognition

12-month expected credit losses (expected credit lossesthat result from those default events on the financialinstrument that are possible within 12 months after thereporting date)

2 Significant increase in credit riskafter initial recognition

Lifetime expected credit losses (expected credit lossesthat result from all possible default events over the life ofthe financial instrument)3 Credit-impaired

Under Korean IFRS 1109, the asset that is credit-impaired at initial recognition would recognize allchanges in lifetime expected credit losses since the initial recognition as a loss allowance with anychanges recognized in profit or loss.

12

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

Based on results from the impact assessment, the balances subject to loss allowances and the lossallowance amounts under Korean IFRS 1109 as of June 30, 2017 were as follows:

(In millions of Korean won) Carrying amount

BalanceLoss allowance in accordance

with Korean IFRS 1109Loans 1 Stage 1 221,565,485 301,514

Stage 2 20,183,037 308,081Stage 3 1,695,315 934,134

Debt securities / Due fromFinancial Institutions 42,031,940 6,490

285,475,777 1,550,219

1 Balance includes other liabilities.

Based on results from the impact assessment, the amount of the provisions under Korean IFRS 1109as of June 30, 2017 were as follows:

(In millions of Korean won) Carrying amountLoss allowance in accordance

with Korean IFRS 1109Provisions Stage 1 100,797

Stage 2 55,703Stage 3 21,342

177,842

Based on results from the impact assessment, the Bank estimated that equity capital ratio inaccordance with Basel standards will be decreased by 0.05%p from 16.54% to 16.49%.

The results of the assessment may be changed due to additional information that the Group mayobtain after the assessment and related decisions.

(d) Hedge Accounting

Hedge accounting mechanics (fair value hedges, cash flow hedges and hedge of net investments in aforeign operations) required by Korean IFRS 1039 remains unchanged in Korean IFRS 1109,however, the new hedge accounting rules will align the accounting for hedging instruments moreclosely with the Group’s risk management practices. As a general rule, more hedge relationshipsmight be eligible for hedge accounting, as the standard introduces a more principles-based approach.Korean IFRS 1109 allows more hedging instruments and hedged items to qualify for hedgeaccounting, and relaxes the hedge accounting requirement by removing two hedge effectivenesstests that are a prospective test to ensure that the hedging relationship is expected to be highlyeffective and a quantitative retrospective test (within range of 80-125 %) to ensure that the hedgingrelationship has been highly effective throughout the reporting period.

With implementation of Korean IFRS 1109, volatility in profit or loss may be reduced as some itemsthat were not eligible as hedged items or hedging instruments under Korean IFRS 1039 are noweligible under Korean IFRS 1109.

13

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

As of June 30, 2017, the Group applies the hedge accounting to its assets and liabilities that amountto 5,363,324 million. With applying the hedge accounting, the Group recognized the changes in fairvalue of fair value hedging instruments for 20,575 million in loss, and reclassified the fair valuechanges of cash flow hedging instruments amounting to 31 million, which were previouslyrecognized in other comprehensive income, to loss. As of June 30, 2017, the changes in fair values ofcash flow hedging instruments and hedging instruments of a net investments in a foreign operationswhich have been recognized in accumulated other comprehensive income, amount to 1,005 millionand 36,009 million, respectively.

Furthermore, when the Group first applies Korean IFRS 1109, it may choose as its accounting policyto continue to apply all of the hedge accounting requirements of Korean IFRS 1039 instead of therequirements of Korean IFRS 1109.

- Korean IFRS 1115 Revenue from Contracts with Customers

Korean IFRS 1115 Revenue from Contracts with Customers issued on November 6, 2015 replacesKorean IFRS 1018 Revenue, Korean IFRS 1011 Construction Contracts, Interpretation 2031Revenue-Barter Transactions Involving Advertising Services, Interpretation 2113 Customer LoyaltyPrograms, Interpretation 2115 Agreements for the Construction of Real Estate and Interpretation 2118Transfers of assets from customers.

Korean IFRS 1018 and other, the current standard, provide revenue recognition criteria by type oftransactions; such as, sales goods, the rendering of services, interest income, royalty income,dividend income, and construction contracts. However, Korean IFRS 1115, the new standard, isbased on the principle that revenue is recognized when control of a good or service transfers to acustomer – so the notion of control replaces the existing notion of risks and rewards. A new five-stepprocess must be applied before revenue from contract with customer can be recognized:

- Identify contracts with customers- Identify the separate performance obligation- Determine the transaction price of the contract- Allocate the transaction price to each of the separate performance obligations, and- Recognize the revenue as each performance obligation is satisfied.

The new standard is effective for annual periods beginning on or after January 1, 2018 with earlyapplication permitted.

2.2 Measurement Basis

The interim consolidated financial statements have been prepared under the historical costconvention unless otherwise specified.

2.3 Functional and Presentation Currency

Items included in the financial statements of each of the Group's entities are measured using thecurrency of the primary economic environment in which the entity operates (the “functional currency”).The interim consolidated financial statements are presented in Korean won, which is the parentcompany’s functional and presentation currency. Refer to Notes 3.2

14

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

2.4 Critical Accounting Estimates

The preparation of interim consolidated financial statements requires the application of accountingpolicies, certain critical accounting estimates and assumptions that may have a significant impact onthe assets (liabilities) and incomes (expenses). Management’s estimates of outcomes may differ fromactual outcomes if management’s estimates and assumptions based on management’s bestjudgment at the reporting date are different from the actual environment.

Estimates and assumptions are continually evaluated and any change in an accounting estimate isrecognized prospectively by including it in profit or loss in the period of the change, if the changeaffects that period only. Alternatively if the change in accounting estimate affects both the period ofchange and future periods, that change is recognized in the profit or loss of all those periods.

Uncertainty in estimates and assumptions with significant risk that may result in material adjustmentto the interim consolidated financial statements are as follows:

2.4.1 Income Taxes

The Group is operating in numerous countries and the income generated from these operations issubject to income taxes based on tax laws and interpretations of tax authorities in numerousjurisdictions. There are many transactions and calculations for which the ultimate tax determination isuncertain.

If a certain portion of the taxable income is not used for investments, increase in wages, or dividendsin accordance with the Tax System For Recirculation of Corporate Income, the Group is liable to payadditional income tax calculated based on the tax laws. The new tax system is effective for threeyears from 2015. Accordingly, the measurement of current and deferred income tax is affected by thetax effects from the new system. As the Group’s income tax is dependent on the investments,increase in wages and dividends, there exists uncertainty with regard to measuring the final taxeffects.

2.4.2 Fair Value of Financial Instruments

The fair value of financial instruments that are not traded in an active market is determined by usingvaluation techniques. The Group uses its judgment to select a variety of methods and makeassumptions that are mainly based on market conditions existing at the end of each reporting period.Refer to Note 6 for details on valuation techniques and inputs used to determine the fair value offinancial instruments.

2.4.3 Provisions for Credit Losses (allowances for loan losses, provisions for acceptances andguarantees, and unused loan commitments)

The Group determines and recognizes allowances for losses on loans through impairment testing andrecognizes provisions for guarantees, and unused loan commitments. The accuracy of provisions forcredit losses is determined by the methodology and assumptions used for estimating expected cashflows of the borrower for individually assessed allowances of loans, collectively assessed allowancesfor groups of loans, guarantees and unused loan commitments.

15

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

2.4.4 Net Defined Benefit Liability

The present value of net defined benefit liability depends on a number of factors that are determinedon an actuarial basis using a number of assumptions (Note 23).

2.4.5 Estimated Impairment of Goodwill

The Group tests annually whether goodwill has suffered any impairment. The recoverable amounts ofcash-generating units have been determined based on value-in-use calculations (Note 15).

3. Significant Accounting Policies

The significant accounting policies applied in the preparation of these interim consolidated financialstatements are set out below. These policies have been consistently applied to all periods presented,unless otherwise stated.

3.1 Consolidation

3.1.1 Subsidiaries

Subsidiaries are companies that are controlled by the Group. The Group controls an investee when itis exposed, or has rights, to variable returns from its involvement with the investee and has the abilityto affect those returns through its power over the investee. The existence and effects of potentialvoting rights that are currently exercisable or convertible are considered when assessing whether theGroup controls another entity. Subsidiaries are fully consolidated from the date when control istransferred to the Group and de-consolidated from the date when control is lost.

If a subsidiary uses accounting policies other than those adopted in the interim consolidated financialstatements for like transactions and events in similar circumstances, appropriate adjustments aremade to make the subsidiary’s accounting policies conform to those of the Group when thesubsidiary’s financial statements are used by the Group in preparing the interim consolidated financialstatements.

Profit or loss and each component of other comprehensive income are attributed to the owners of theparent and to the non-controlling interests, if any. Total comprehensive income is attributed to theowners of the parent and to the non-controlling interests even if this results in the non-controllinginterests having a deficit balance.

Transactions with non-controlling interests that do not result in loss of control are accounted for asequity transactions; that is, as transactions with the owners in their capacity as owners. Thedifference between fair value of any consideration paid and the relevant share acquired of thecarrying value of net assets of the subsidiary is recorded in equity. Gains or losses on disposals tonon-controlling interests are also recorded in equity.

16

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

When the Group ceases to have control, any retained interest in the entity is re-measured to its fairvalue at the date when control is lost, with the change in carrying amount recognized in profit or loss.The fair value is the initial carrying amount for the purposes of subsequently accounting for theretained interest as an associate, joint venture or financial asset. In addition, any amounts previouslyrecognized in other comprehensive income in respect of that entity are accounted for as if the Grouphad directly disposed of the related assets or liabilities. This may mean that amounts previouslyrecognized in other comprehensive income are reclassified to profit or loss.

3.1.2 Associates

Associates are entities over which the Group has significant influence in the financial and operatingpolicy decisions. If the Group holds 20% or more of the voting power of the investee, it is presumedthat the Group has significant influence.

Under the equity method, investments in associates are initially recognized at cost and the carryingamount is increased or decreased to recognize the Group’s share of the profit or loss of the investeeand changes in the investee’s equity after the date of acquisition. The Group’s share of the profit orloss of the investee is recognized in the Group’s profit or loss. Distributions received from an investeereduce the carrying amount of the investment. Profit and loss resulting from ‘upstream’ and‘downstream’ transactions between the Group and associates are eliminated to the extent at theGroup’s interest in associates. Unrealized losses are eliminated in the same way as unrealized gainsexcept that they are only eliminated to the extent that there is no evidence of impairment.

If associates use accounting policies other than those adopted in the interim consolidated financialstatements for like transactions and events in similar circumstances, appropriate adjustments aremade to make the associate’s accounting policies conform to those of the Group when theassociate’s financial statements are used by the Group in applying equity method.

After the carrying amount of the investment is reduced to zero, additional losses are provided for, anda liability is recognized, only to the extent that the Group has incurred legal or constructive obligationsor made payments on behalf of the investee.

The Group determines at each reporting period whether there is any objective evidence that theinvestments in the associates are impaired. If this is the case, the Group calculates the amount ofimpairment as the difference between the recoverable amount of the associates and its carrying valueand recognizes the amount as ‘non-operating income(expense)’ in the statement of comprehensiveincome.

3.1.3 Structured Entity

A structured entity is an entity that has been designed so that voting or similar rights are not thedominant factor in deciding who controls the entity. When the Group decides whether it has power tothe structured entities in which the Group has interests, it considers factors such as the purpose, theform, the practical ability to direct the relevant activities of a structured entity, the nature of itsrelationship with a structured entity and the amount of exposure to variable returns.

17

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

3.1.4 Trusts and Funds

The Group provides management services for trust assets, collective investment and other funds.These trusts and funds are not consolidated in the Group’s interim consolidated financial statements,except for trusts and funds over which the Group has control.

3.1.5 Intra-group Transactions

All intra-group balances and transactions, and any unrealized gains arising on intra-grouptransactions, are eliminated in preparing the interim consolidated financial statements. Unrealizedlosses are eliminated in the same way as unrealized gains except that they are only eliminated to theextent that there is no evidence of impairment.

3.2 Foreign Currency

3.2.1 Foreign Currency Transactions and Balances

A foreign currency transaction is recorded, on initial recognition in the functional currency, by applyingthe spot exchange rate between the functional currency and the foreign currency at the date of thetransaction. At the end of each reporting period, foreign currency monetary items are translated usingthe closing rate which is the spot exchange rate at the end of the reporting period. Non-monetaryitems that are measured at fair value in a foreign currency are translated using the spot exchangerates at the date when the fair value was determined and non-monetary items that are measured interms of historical cost in a foreign currency are translated using the spot exchange rate at the date ofthe transaction. Exchange differences arising on the settlement of monetary items or on translatingmonetary items at rates different from those at which they were translated on initial recognition duringthe period or in previous financial statements are recognized in profit or loss in the period in whichthey arise, except for exchange differences arising on net investments in a foreign operation andfinancial liability designated as a hedge of the net investment. When gains or losses on a non-monetary item are recognized in other comprehensive income, any exchange component of thosegains or losses are also recognized in other comprehensive income. Conversely, when gains orlosses on a non-monetary item are recognized in profit or loss, any exchange component of thosegains or losses are also recognized in profit or loss.

3.2.2 Foreign Operations

The financial performance and financial position of all foreign operations, whose functional currenciesdiffer from the Group’s presentation currency, are translated into the Group’s presentation currencyusing the following procedures.

Assets and liabilities for each consolidated statement of financial position presented are translated atthe closing rate at the end of the reporting period. Income and expenses in the statement ofcomprehensive income presented are translated at average exchange rates for the period. Allresulting exchange differences are recognized in other comprehensive income.

Any goodwill arising from the acquisition of a foreign operation and any fair value adjustments to thecarrying amounts of assets and liabilities arising from the acquisition of that foreign operation aretreated as assets and liabilities of the foreign operation. Thus, they are expressed in the functionalcurrency of the foreign operation and are translated into the presentation currency at the closing rate.

18

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

On the disposal of a foreign operation, the cumulative amount of the exchange differences relating tothat foreign operation, recognized in other comprehensive income and accumulated in the separatecomponent of equity, is reclassified from equity to profit or loss (as a reclassification adjustment)when the gains or losses on disposal are recognized. On the partial disposal of a subsidiary thatincludes a foreign operation, the Group re-attributes the proportionate share of the cumulative amountof the exchange differences recognized in other comprehensive income to the non-controllinginterests in that foreign operation. In any other partial disposal of a foreign operation, the Groupreclassifies to profit or loss only the proportionate share of the cumulative amount of the exchangedifferences recognized in other comprehensive income.

3.3 Recognition and Measurement of Financial Instruments

3.3.1 Initial Recognition

The Group recognizes a financial asset or a financial liability in its consolidated statement of financialposition when the Group becomes a party to the contractual provisions of the instrument. A regularway purchase or sale of financial assets (a purchase or sale of a financial asset under a contractwhose terms require delivery of the financial instruments within the time frame established generallyby market regulation or practice) is recognized and derecognized using trade date accounting.

The Group classifies financial assets as financial assets at fair value through profit or loss, available-for-sale financial assets, held-to-maturity financial assets, or loans and receivables, or other financialassets. The Group classifies financial liabilities as financial liabilities at fair value through profit or loss,or other financial liabilities. The classification depends on the nature and holding purpose of thefinancial instrument at initial recognition in the interim consolidated financial statements.

At initial recognition, a financial asset or financial liability is measured at its fair value plus or minus, inthe case of a financial asset or financial liability not at fair value through profit or loss, transactioncosts that are directly attributable to the acquisition or issue of the financial asset or financial liability.The fair value is defined as the price that would be received to sell an asset or paid to transfer aliability in an orderly transaction between market participants. The fair value of a financial instrumenton initial recognition is normally the transaction price (that is, the fair value of the consideration givenor received) in an arm’s length transaction.

3.3.2 Subsequent Measurement

After initial recognition, financial instruments are measured at amortized cost or fair value based onclassification at initial recognition.

Amortized cost

The amortized cost of a financial asset or financial liability is the amount at which the financial assetor financial liability is measured at initial recognition and adjusted to reflect principal repayments,cumulative amortization using the effective interest method and any reduction (directly or through theuse of an allowance account) for impairment or uncollectibility.

19

Kookmin Bank and SubsidiariesNotes to the Interim Consolidated Financial StatementsSeptember 30, 2017 and 2016 (Unaudited), and December 31, 2016

Fair value