© pearson education, inc. publishing as prentice hall20-1 chapter 20: accounting for state and...

TRANSCRIPT

© Pearson Education, Inc. publishing as Prentice Hall 20-1

Chapter 20: Accounting for State and Local Governmental Units –

Proprietary and Fiduciary Fundsby Jeanne M. David, Ph.D., Univ. of Detroit Mercy

to accompany

Advanced Accounting, 10th editionby Floyd A. Beams, Robin P. Clement,

Joseph H. Anthony, and Suzanne Lowensohn

© Pearson Education, Inc. publishing as Prentice Hall 20-2

Proprietary and Fiduciary Funds: Objectives1. Review the appropriate accounting and financial

reporting for proprietary funds.2. Recognize the proper treatment of internal service

funds in the government-wide statements.3. Introduce the differences between a proprietary fund

statement of cash flows and its commercial business counterpart.

4. Prepare journal entries and fund financial statements for fiduciary funds.

5. Learn about GASB guidance for pension fund accounting.

© Pearson Education, Inc. publishing as Prentice Hall 20-3

1: Proprietary Funds1: Proprietary Funds

Accounting for State and Local Governmental Units – Proprietary and Fiduciary Funds

© Pearson Education, Inc. publishing as Prentice Hall 20-4

Accounting for Proprietary Funds

• ModelCA + NCA – CL – NCL = Net assets

• Use accrual accounting• Net assets

– Invested in capital assets net of related debt– Restricted net assets– Unrestricted net assets

• Two types– Internal service funds– Enterprise funds

© Pearson Education, Inc. publishing as Prentice Hall 20-5

Internal Service Funds• Use for government activities that provide goods

and services to other departments or agencies of that same governmental unit

• Central stores/ purchasing• Motor pools• Print shop

• Might be started with transfers from general fund and/or contributed capital from other sources

• Main source of revenues is other funds • Use "Due from …" rather than accounts receivable

© Pearson Education, Inc. publishing as Prentice Hall 20-6

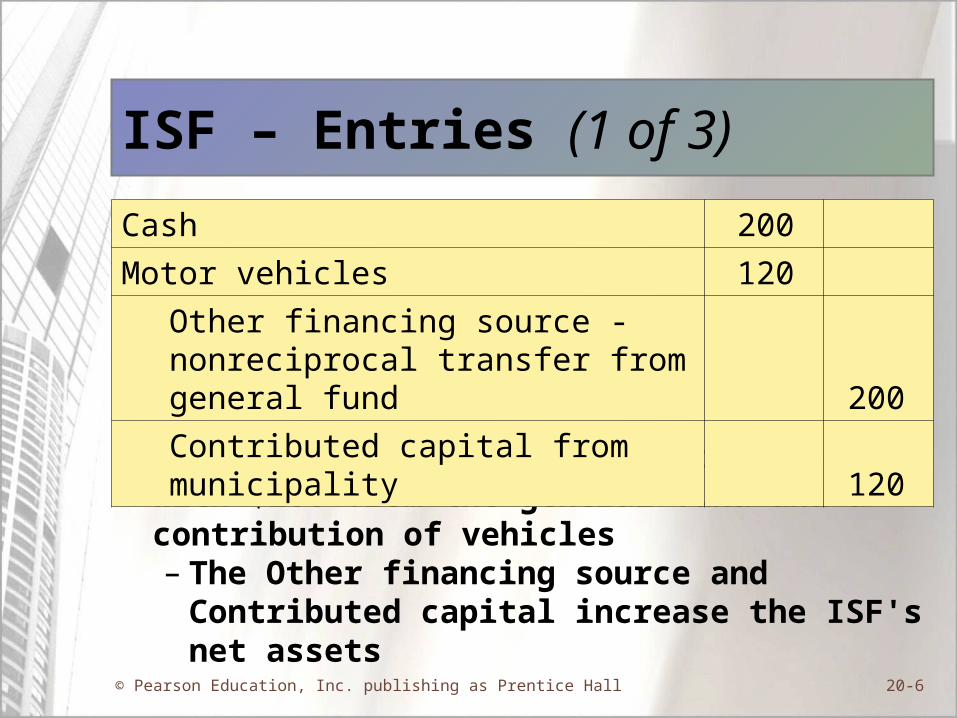

ISF – Entries (1 of 3)

• A village begins a central motor pool with $200 from the general fund and a contribution of vehicles– The Other financing source and Contributed

capital increase the ISF's net assets

Cash 200

Motor vehicles 120

Other financing source - nonreciprocal transfer from general fund 200

Contributed capital from municipality 120

© Pearson Education, Inc. publishing as Prentice Hall 20-7

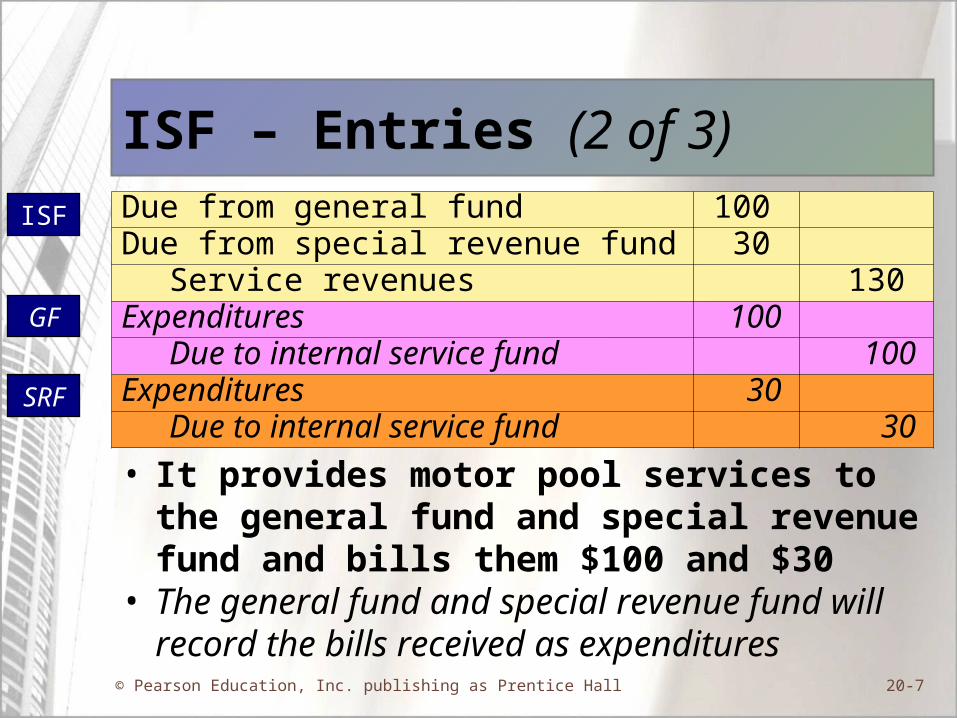

ISF – Entries (2 of 3)

• It provides motor pool services to the general fund and special revenue fund and bills them $100 and $30

• The general fund and special revenue fund will record the bills received as expenditures

Due from general fund 100 Due from special revenue fund 30

Service revenues 130 Expenditures 100

Due to internal service fund 100 Expenditures 30

Due to internal service fund 30

ISF

GF

SRF

© Pearson Education, Inc. publishing as Prentice Hall 20-8

ISF – Entries (3 of 3)

• The internal service fund collects the $100 due from the general fund

• The general fund will record the payment of its liability

Cash 100

Due from general fund 100

Due to internal service fund 100

Cash 100

ISF

GF

© Pearson Education, Inc. publishing as Prentice Hall 20-9

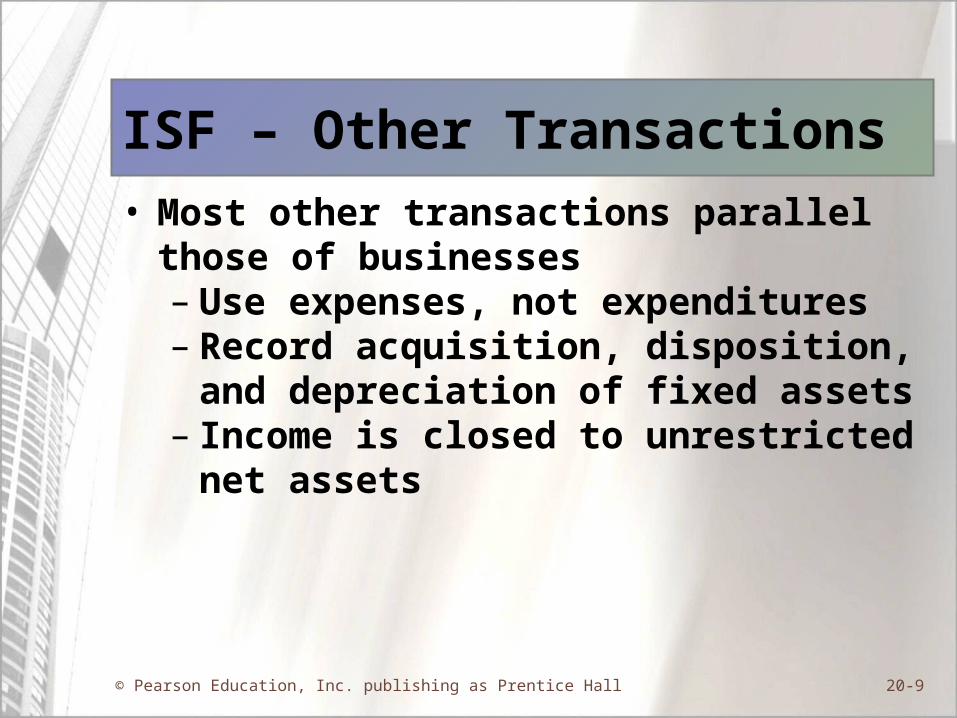

ISF – Other Transactions

• Most other transactions parallel those of businesses– Use expenses, not expenditures– Record acquisition, disposition, and

depreciation of fixed assets– Income is closed to unrestricted net assets

© Pearson Education, Inc. publishing as Prentice Hall 20-10

Enterprise Funds • Use for governmental activities

– Financed and operated like a business– Provide goods and services to general public

• Utilities, civic centers, golf clubs• Might start with funds transferred and contributions• Main revenues from general public, but some from

other departments of the government• Use "Accounts Receivable" for general public and

others and "Due from …" for other funds of this governmental unit

© Pearson Education, Inc. publishing as Prentice Hall 20-11

EF – Entries (1 of 4)

• Utility-type enterprise funds often charge customer deposits– Amounts given as deposits are restricted

cash, not included in current assets– Customer deposits are liabilities, may be

current or long term• Deposits may be returned or applied against the

customers accounts receivable

Restricted cash 10

Customer deposits 10

© Pearson Education, Inc. publishing as Prentice Hall 20-12

EF – Entries (2 of 4)

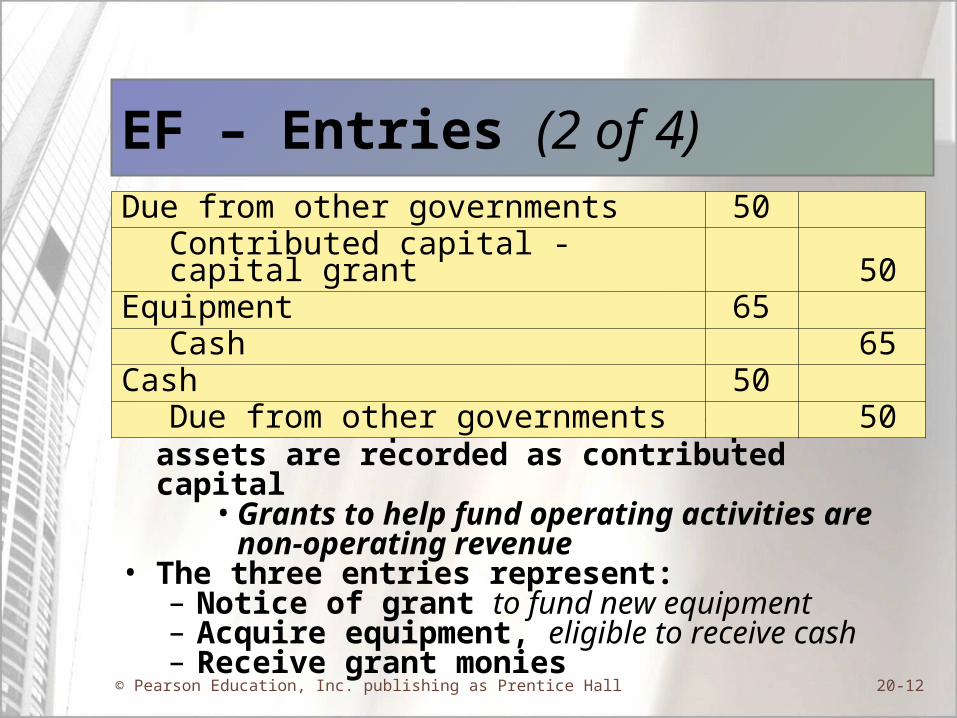

• Grants to acquire or enhance capital assets are recorded as contributed capital

• Grants to help fund operating activities are non-operating revenue

• The three entries represent:– Notice of grant to fund new equipment– Acquire equipment, eligible to receive cash– Receive grant monies

Due from other governments 50 Contributed capital - capital grant 50

Equipment 65 Cash 65

Cash 50 Due from other governments 50

© Pearson Education, Inc. publishing as Prentice Hall 20-13

EF – Entries (3 of 4)

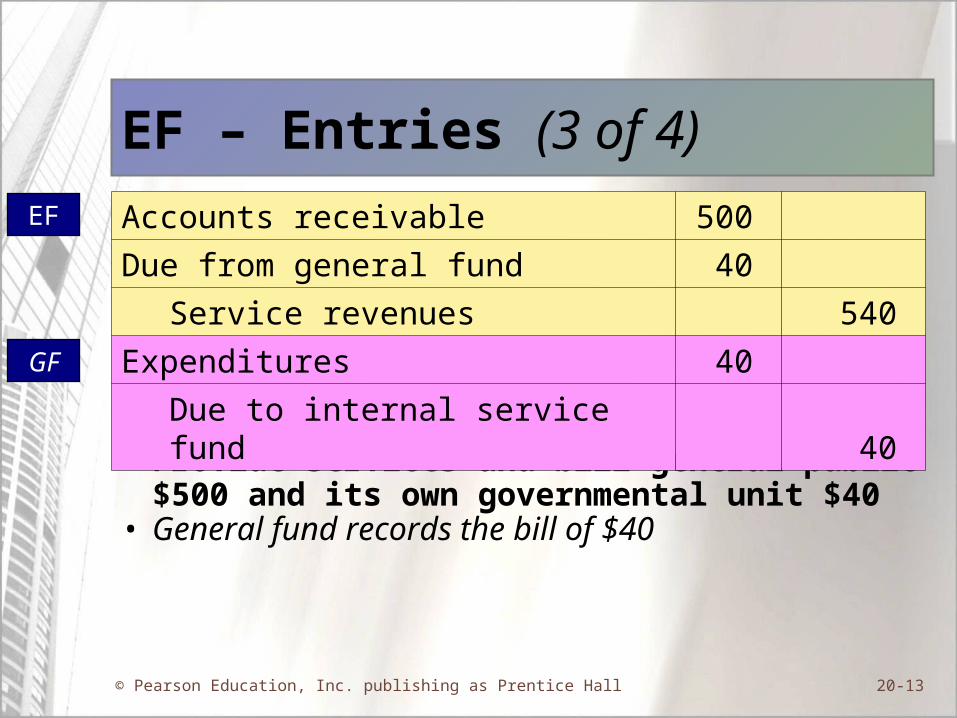

• Provide services and bill general public $500 and its own governmental unit $40

• General fund records the bill of $40

Accounts receivable 500

Due from general fund 40

Service revenues 540

Expenditures 40

Due to internal service fund 40

EF

GF

© Pearson Education, Inc. publishing as Prentice Hall 20-14

EF – Entries (4 of 4)

• Collect from general public and the general fund• The general fund records the payment• The enterprise fund will use allowances for uncollectibles and bad debt

expense, like business enterprises

Cash 490

Accounts receivable 450

Due from general fund 40

Due to internal service fund 40

Cash 40

EF

GF

© Pearson Education, Inc. publishing as Prentice Hall 20-15

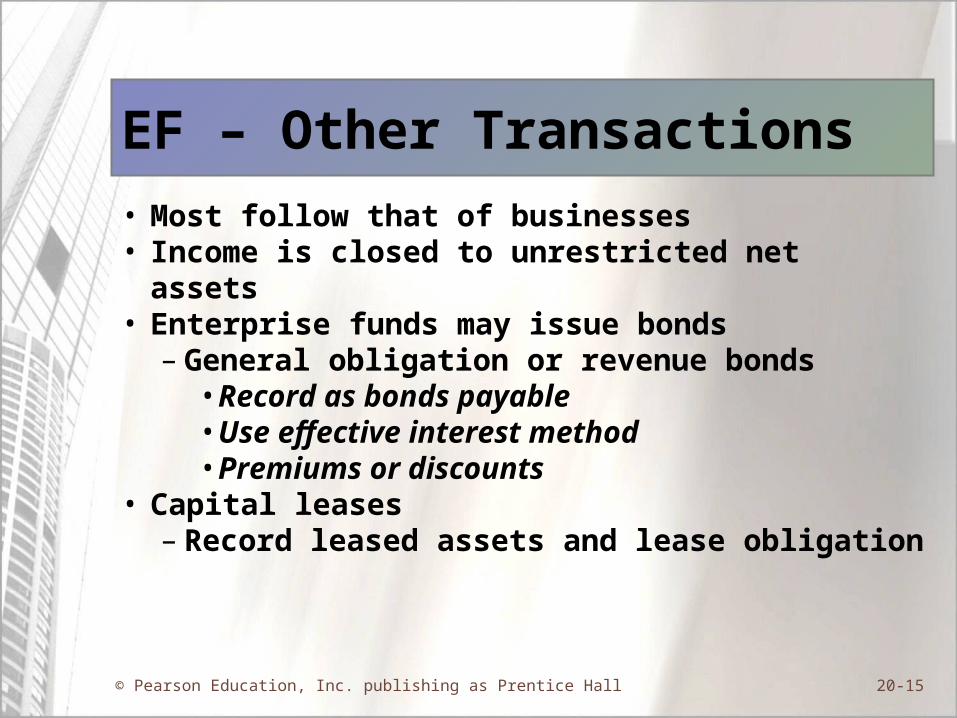

EF – Other Transactions

• Most follow that of businesses• Income is closed to unrestricted net assets• Enterprise funds may issue bonds

– General obligation or revenue bonds• Record as bonds payable• Use effective interest method • Premiums or discounts

• Capital leases – Record leased assets and lease obligation

© Pearson Education, Inc. publishing as Prentice Hall 20-16

2: Internal Service Funds in 2: Internal Service Funds in Government-wide StatementsGovernment-wide Statements

Accounting for State and Local Governmental Units – Proprietary and Fiduciary Funds

© Pearson Education, Inc. publishing as Prentice Hall 20-17

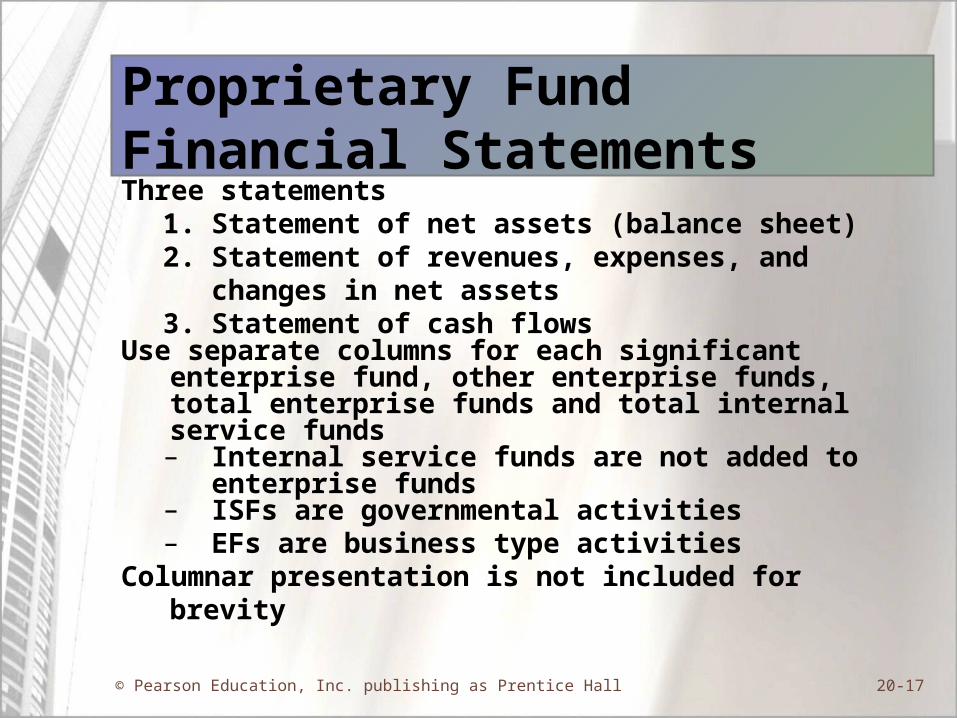

Proprietary Fund Financial StatementsThree statements

1. Statement of net assets (balance sheet)2. Statement of revenues, expenses, and changes in

net assets3. Statement of cash flows

Use separate columns for each significant enterprise fund, other enterprise funds, total enterprise funds and total internal service funds

– Internal service funds are not added to enterprise funds

– ISFs are governmental activities– EFs are business type activities

Columnar presentation is not included for brevity

© Pearson Education, Inc. publishing as Prentice Hall 20-18

Statement of Net AssetsCash $720 Receivables, net 261 Due from other funds 32 Supplies 62 Total current assets $1,075 Restricted cash $185 Land 95 Buildings and equipment 1,990 Vehicles 220 Accumulated depreciation (1,005) Total noncurrent assets $1,485 Total assets $2,560

Accounts payable $68 Due to other funds 4 Other current liabilities 129 $201 Customer deposits $185 Compensated absences 295 Bonds and notes payable 465 945 Total liabilities $1,146 Net assets: Invested in capital assets, net of related debt $575 Restricted 270 Unrestricted 569 Total net assets $1,414

© Pearson Education, Inc. publishing as Prentice Hall 20-19

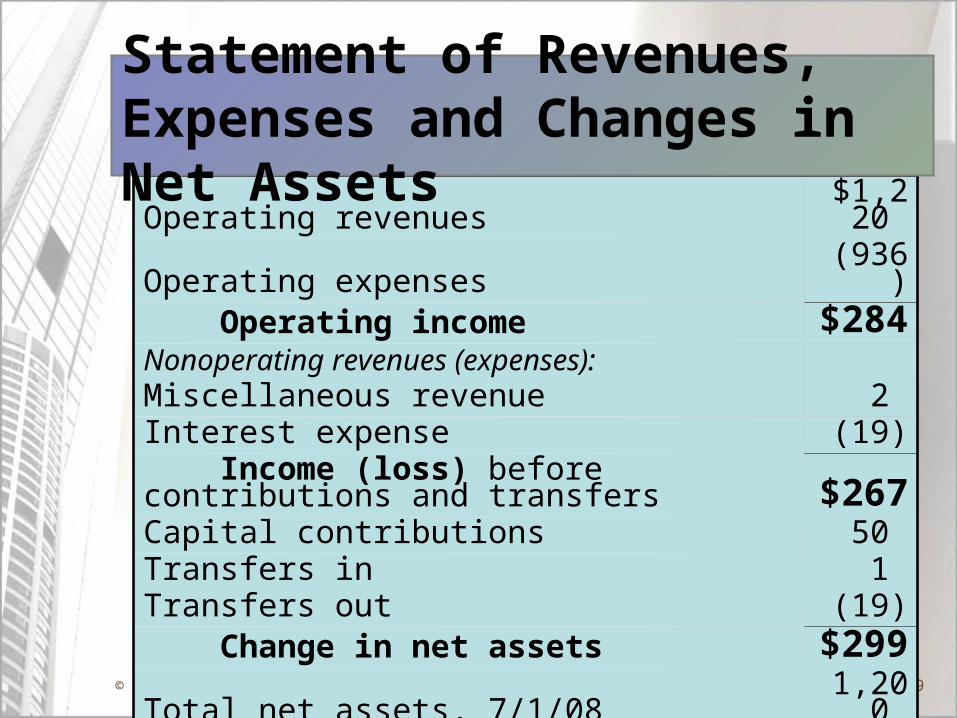

Operating revenues $1,220 Operating expenses (936) Operating income $284 Nonoperating revenues (expenses): Miscellaneous revenue 2 Interest expense (19) Income (loss) before contributions and transfers $267 Capital contributions 50 Transfers in 1 Transfers out (19) Change in net assets $299 Total net assets, 7/1/08 1,200 Total net assets, 6/30/09 $1,499

Statement of Revenues, Expenses and Changes in Net Assets

© Pearson Education, Inc. publishing as Prentice Hall 20-20

Government-wide Statements• Internal service funds are included with

governmental funds– All represent governmental activities

• Enterprise funds displayed in a single column labeled Business-type activities

• ISF and EF already use accrual accounting• Interfund balances: either

• Eliminate• Show interfund balances separate from

other assets/ liabilities• No reconciliations needed for ISF and EF

© Pearson Education, Inc. publishing as Prentice Hall 20-21

ISF in Financial Statements• In the Proprietary fund statements:

– Internal service funds are in a separate column• Separately, to the side of the total for business-

type/ enterprise funds• Not added to those enterprise funds

• In the Government-wide statements:– Internal service funds plus governmental funds

are shown as one total• Labeled as governmental-type activities• Governmental-type and business-type activities

are the added together

© Pearson Education, Inc. publishing as Prentice Hall 20-22

3: Proprietary Funds Statement of 3: Proprietary Funds Statement of Cash FlowsCash Flows

Accounting for State and Local Governmental Units – Proprietary and Fiduciary Funds

© Pearson Education, Inc. publishing as Prentice Hall 20-23

Cash Flow CategoriesFour cash flow categories:

1. Cash flows from operations2. Cash flows from noncapital financing activities3. Cash flows from capital and related financing activities4. Cash flows from investing activities

Compared to for-profit enterprises– Capital expenditures are removed from other investing

activities– Their related financing activities are taken from other

financing activities– Capital expenditures and related financing have their

own category

© Pearson Education, Inc. publishing as Prentice Hall 20-24

Cash flows from operations: Cash received from customers $1,161 Cash paid to suppliers (326) Cash paid for other expenses (471) Net cash provided by operations $364 Cash flows from noncapital financing activities: Cash from general fund 3 Cash flows from capital and related financing activities: Purchase of equipment ($18) Payment on capital debt (87) Net cash provided by capital and related financing (105)Cash flows from investing activities: Interest and dividends 1 Net increase in unrestricted cash $263 Cash balance, 7/1/08 457 Cash balance, 6/30/08 $720

Statement of Cash Flows

© Pearson Education, Inc. publishing as Prentice Hall 20-25

4: Fiduciary Funds4: Fiduciary Funds

Accounting for State and Local Governmental Units – Proprietary and Fiduciary Funds

© Pearson Education, Inc. publishing as Prentice Hall 20-26

Accounting for Fiduciary Funds• Account for assets held in a trust or agency capacity

– Not used for government's own programs• Fiduciary funds

– Private purpose trust funds– Investment trust funds– Pension trust funds– Agency funds

• Focus on demonstrating fulfillment of fiduciary responsibilities– Accrual accounting

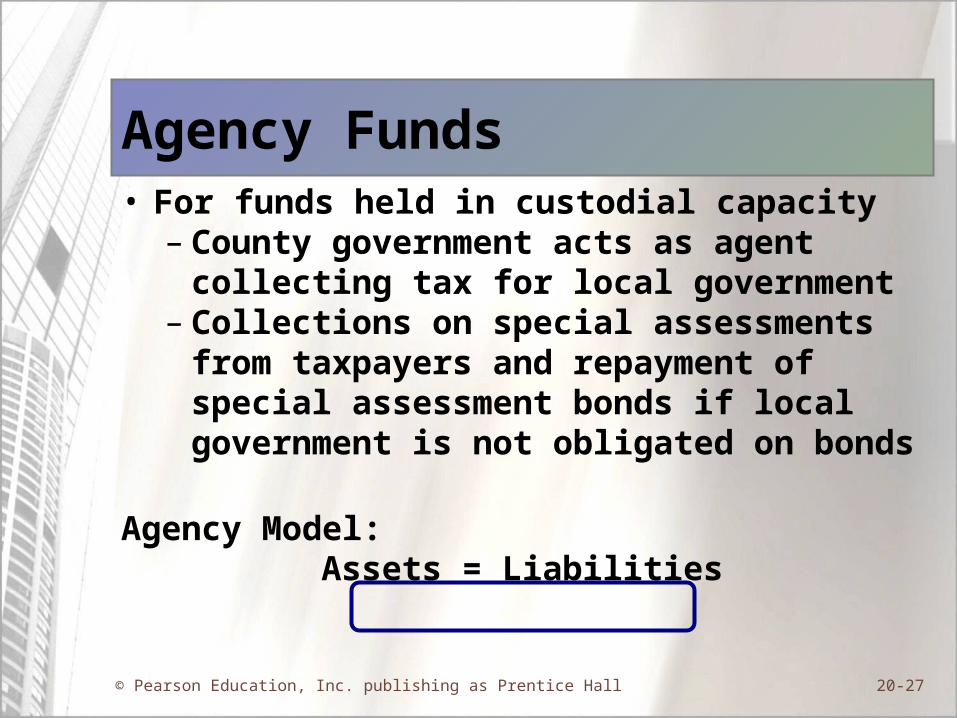

© Pearson Education, Inc. publishing as Prentice Hall 20-27

Agency Funds• For funds held in custodial capacity

– County government acts as agent collecting tax for local government

– Collections on special assessments from taxpayers and repayment of special assessment bonds if local government is not obligated on bonds

Agency Model:Assets = Liabilities

© Pearson Education, Inc. publishing as Prentice Hall 20-28

Agency Transactions

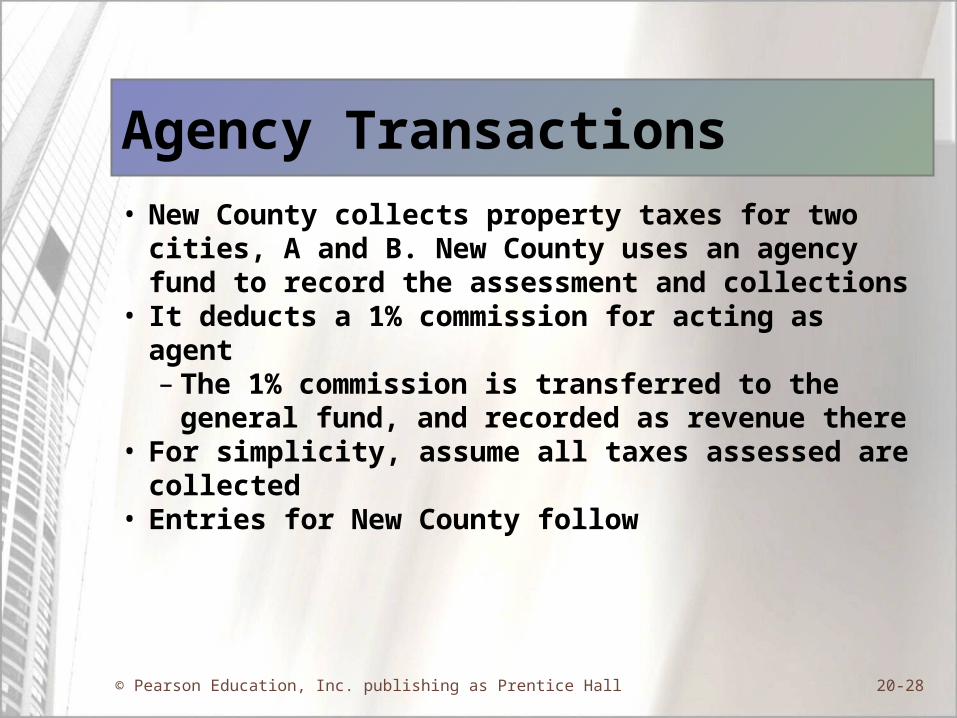

• New County collects property taxes for two cities, A and B. New County uses an agency fund to record the assessment and collections

• It deducts a 1% commission for acting as agent– The 1% commission is transferred to the

general fund, and recorded as revenue there• For simplicity, assume all taxes assessed are

collected• Entries for New County follow

© Pearson Education, Inc. publishing as Prentice Hall 20-29

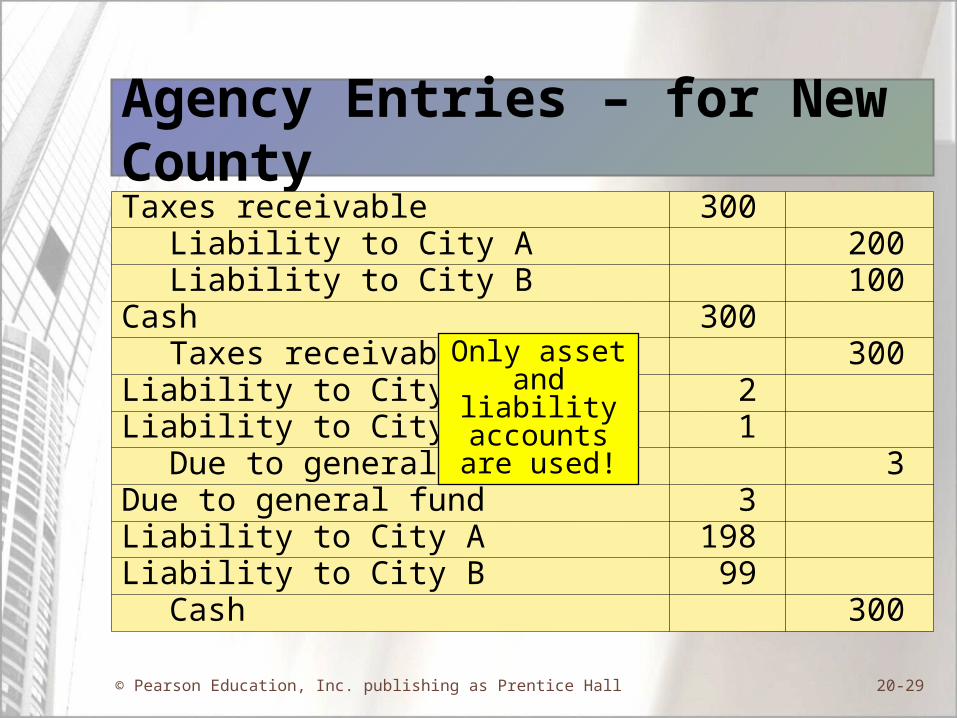

Agency Entries – for New CountyTaxes receivable 300

Liability to City A 200 Liability to City B 100

Cash 300 Taxes receivable 300

Liability to City A 2 Liability to City B 1

Due to general fund 3 Due to general fund 3 Liability to City A 198 Liability to City B 99

Cash 300

Only asset and liability

accounts are used!

© Pearson Education, Inc. publishing as Prentice Hall 20-30

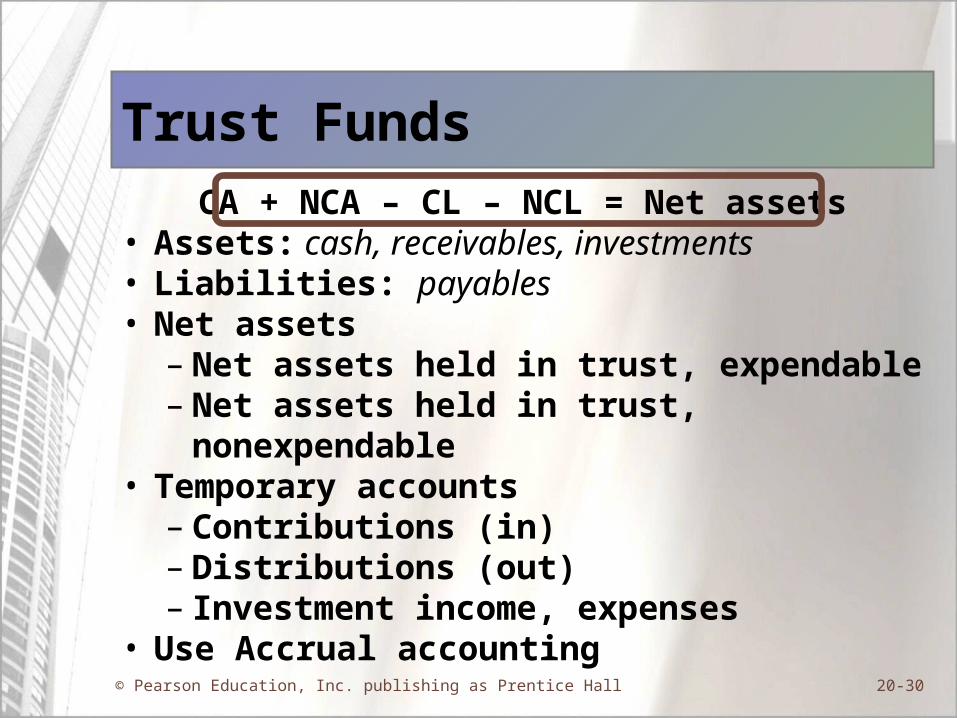

CA + NCA – CL – NCL = Net assets• Assets: cash, receivables, investments • Liabilities: payables• Net assets

– Net assets held in trust, expendable– Net assets held in trust, nonexpendable

• Temporary accounts– Contributions (in)– Distributions (out)– Investment income, expenses

• Use Accrual accounting

Trust Funds

© Pearson Education, Inc. publishing as Prentice Hall 20-31

Fiduciary Fund Financial Statements• Fund Statements

– Statement of fiduciary net assets– Statement of changes in fiduciary net assets

• Fiduciary funds are not included in the government-wide statements

© Pearson Education, Inc. publishing as Prentice Hall 20-32

5: Pension Funds5: Pension Funds

Accounting for State and Local Governmental Units – Proprietary and Fiduciary Funds

© Pearson Education, Inc. publishing as Prentice Hall 20-33

Pension Trust Fund

• Account for Public Employee Retirement Systems (PERS)

• GASB Statement No. 25, 27 and 50• Do not apply FASB pension accounting

• Disclosures– Scheduled of funding progress for defined

benefit, single and multiple employer plans• Also disclose

– Other post-employment benefits

© Pearson Education, Inc. publishing as Prentice Hall 20-34

Copyright © 2009 Pearson Education, Inc. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice HallPublishing as Prentice Hall

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any

means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher.

Printed in the United States of America.