contentsus.imshealth.com/actsonline/acts2013.pdf · overall precision index, ... we supply our...

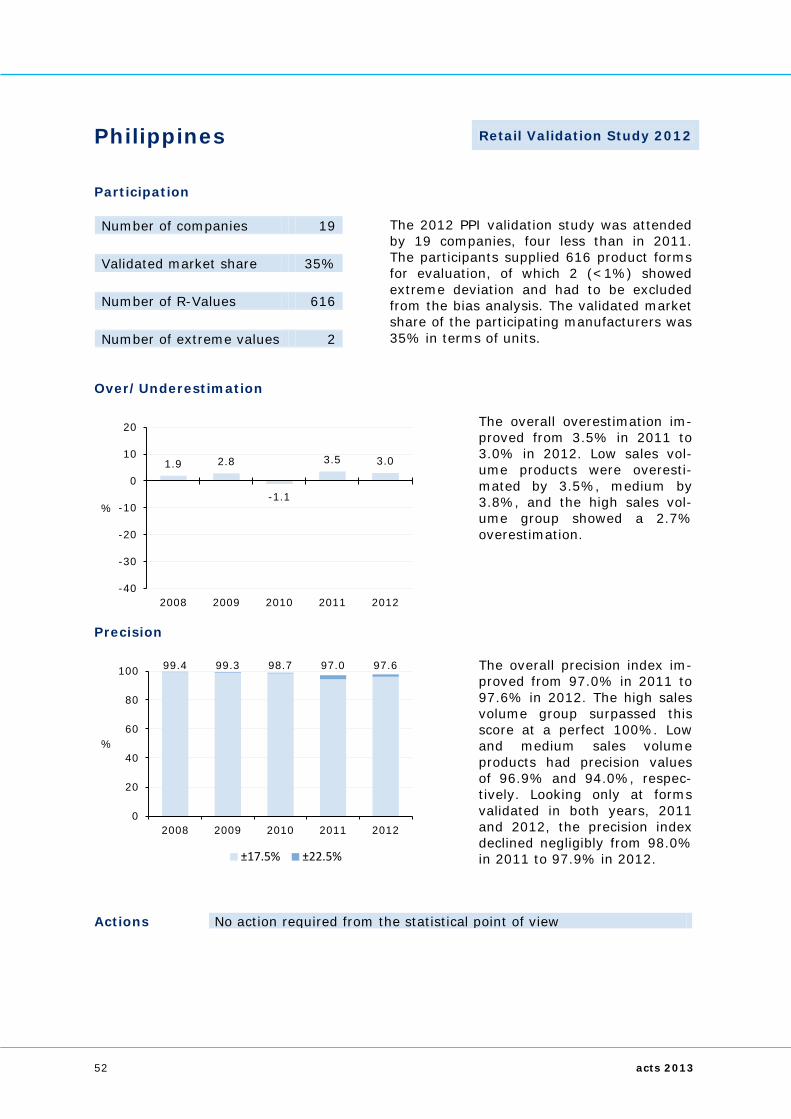

TRANSCRIPT

Contents Abstract 3

Accuracy 5

Retail Validation 7

Algeria 11

Argentina 12

Australia 13

Austria 14

Bangladesh 15

Belgium 16

Bolivia 17

Brazil 18

Bulgaria 19

Canada 20

Central America 21

Chile 22

Colombia 23

Croatia 24

Czech Republic 25

Dominican Republic 26

Ecuador 27

Egypt 28

Estonia 29

Germany 30

Greece 31

Hong Kong 32

Hungary 33

India 34

Indonesia 35

Ireland 36

Italy 37

Japan 38

Jordan 39

Korea 40

Kuwait 41

Latvia 42

Lebanon 43

Lithuania 44

Malaysia 45

Mexico 46

Morocco 47

New Zealand 48

Pakistan 49

Paraguay 50

Peru 51

Philippines 52

Poland 53

Portugal 54

Saudi Arabia 55

Serbia 56

Singapore 57

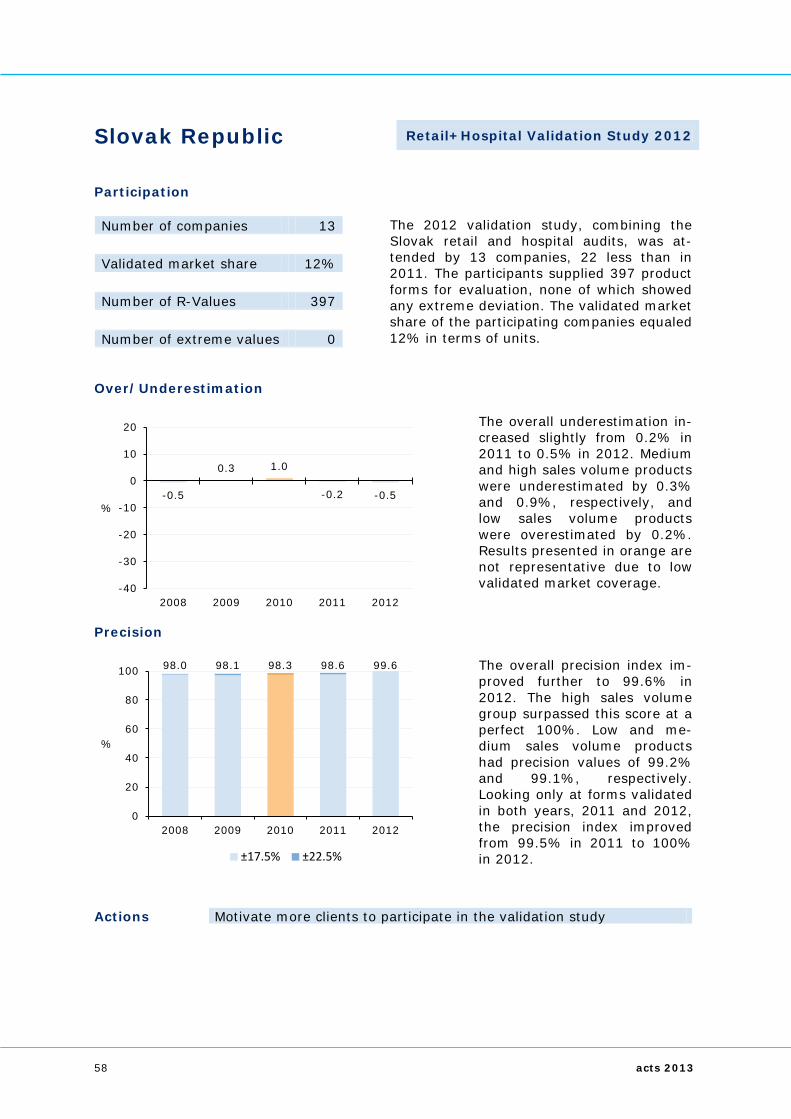

Slovak Republic 58

Slovenia 59

Spain 60

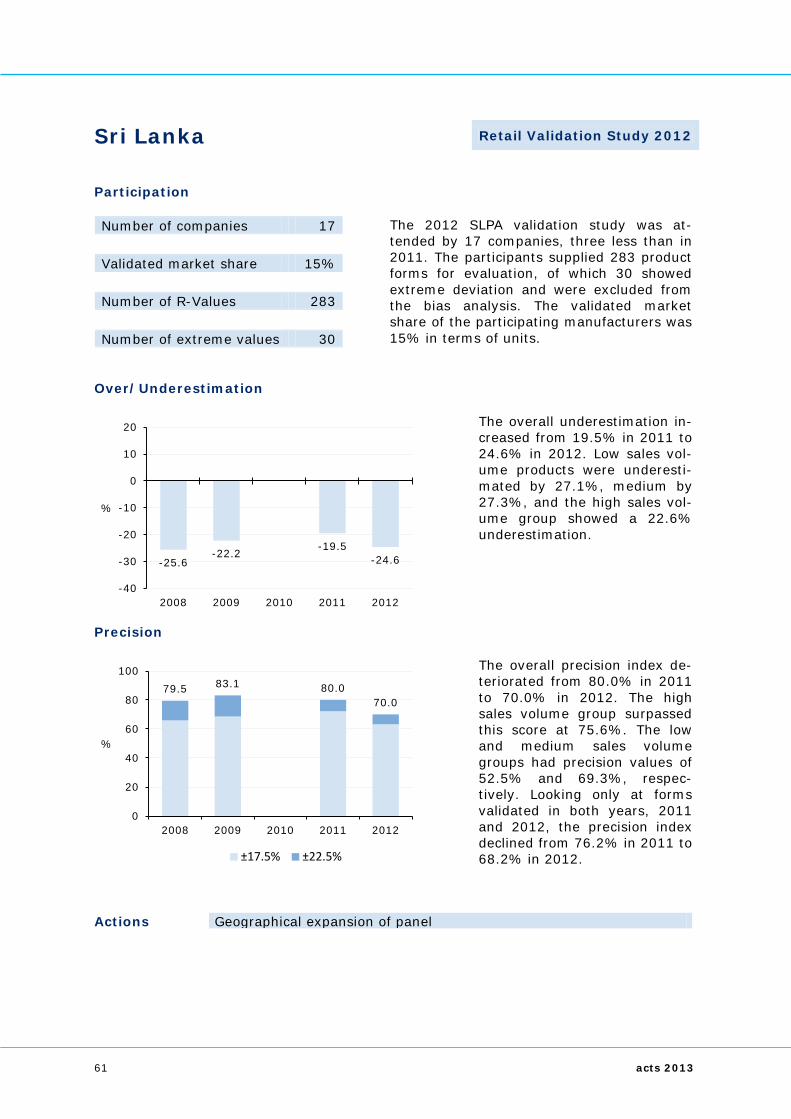

Sri Lanka 61

Switzerland 62

Thailand 63

Tunisia 64

Turkey 65

Un. Arab Emirates 66

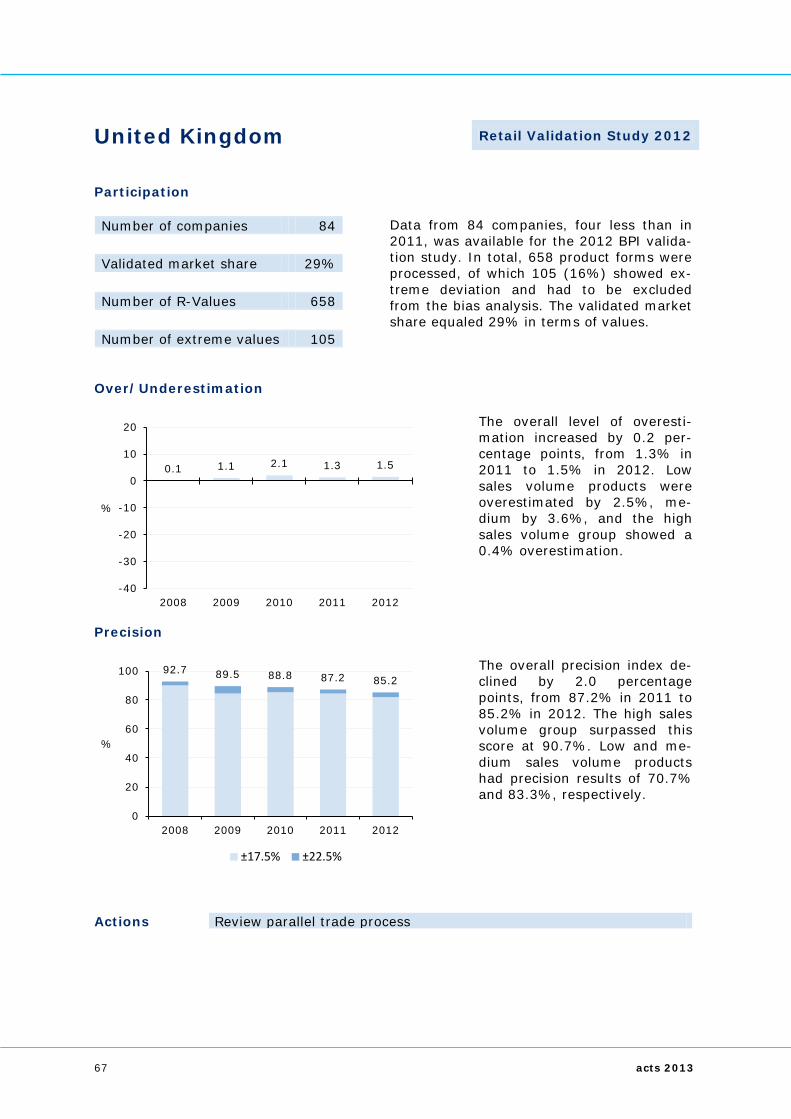

United Kingdom 67

Uruguay 68

USA 69

Venezuela 70

Vietnam 71

OTC Validation 72

Argentina 74

Austria 75

Belgium 76

Brazil 77

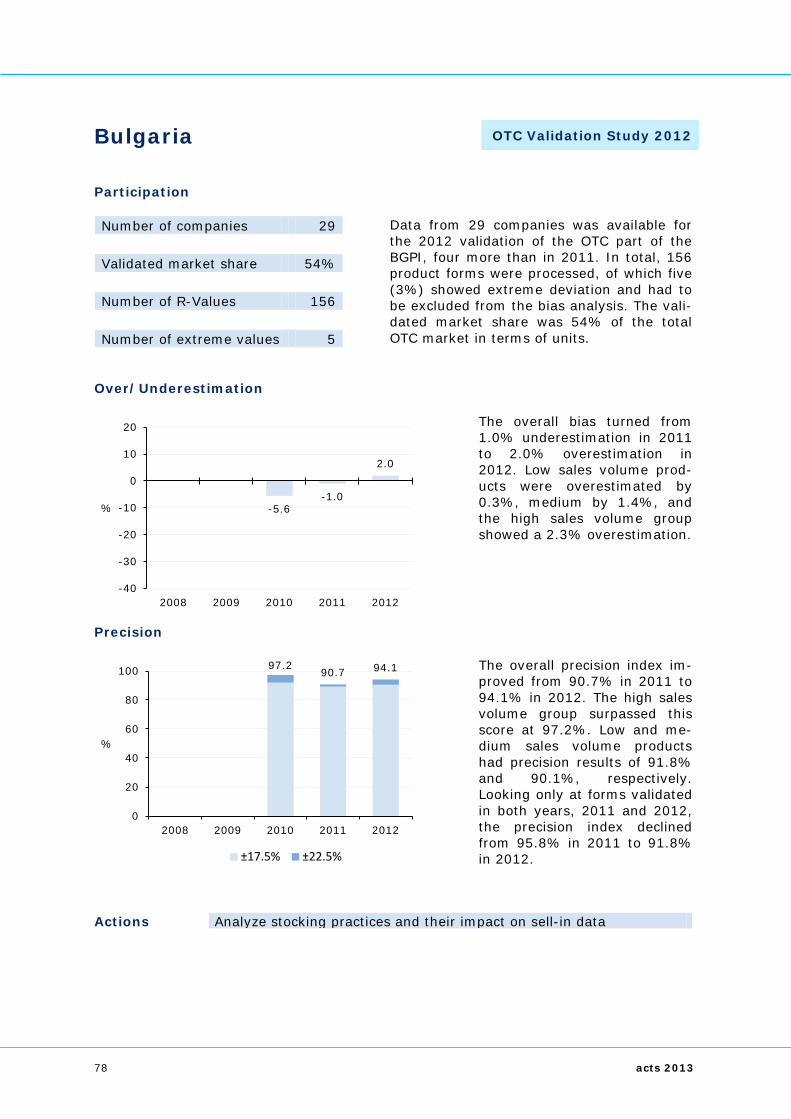

Bulgaria 78

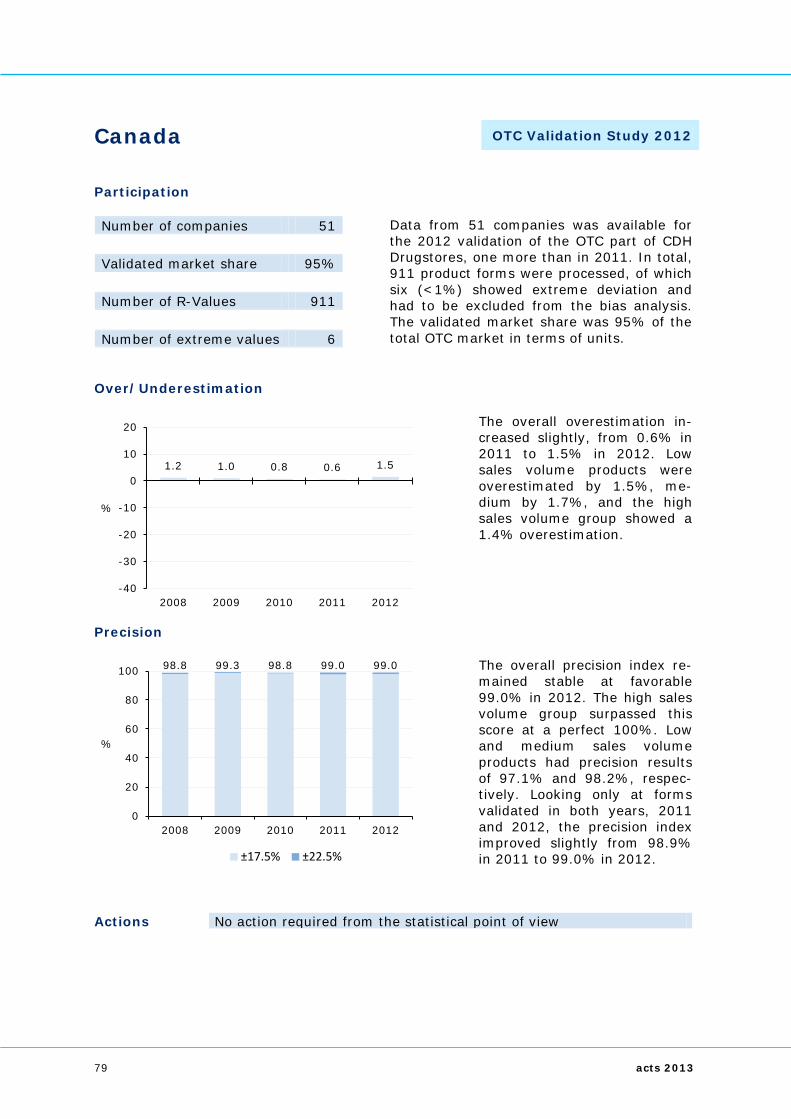

Canada 79

Czech Republic 80

Finland 81

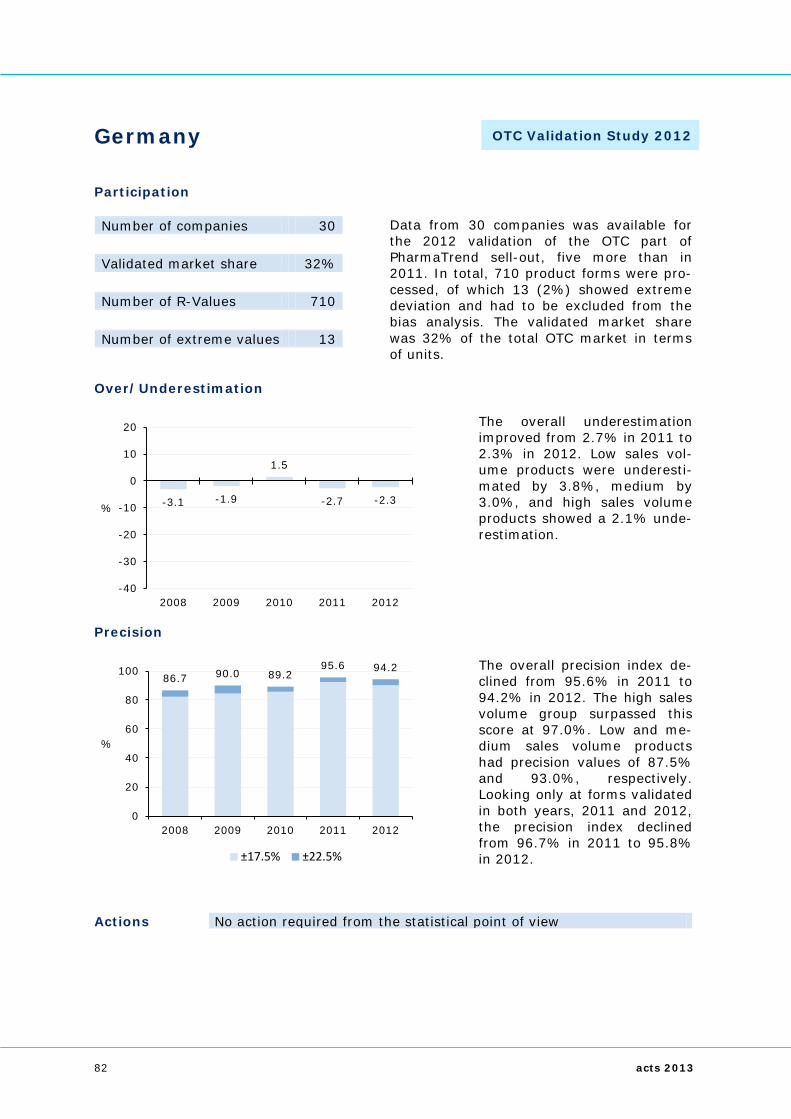

Germany 82

Greece 83

Hungary 84

Italy 85

Korea 86

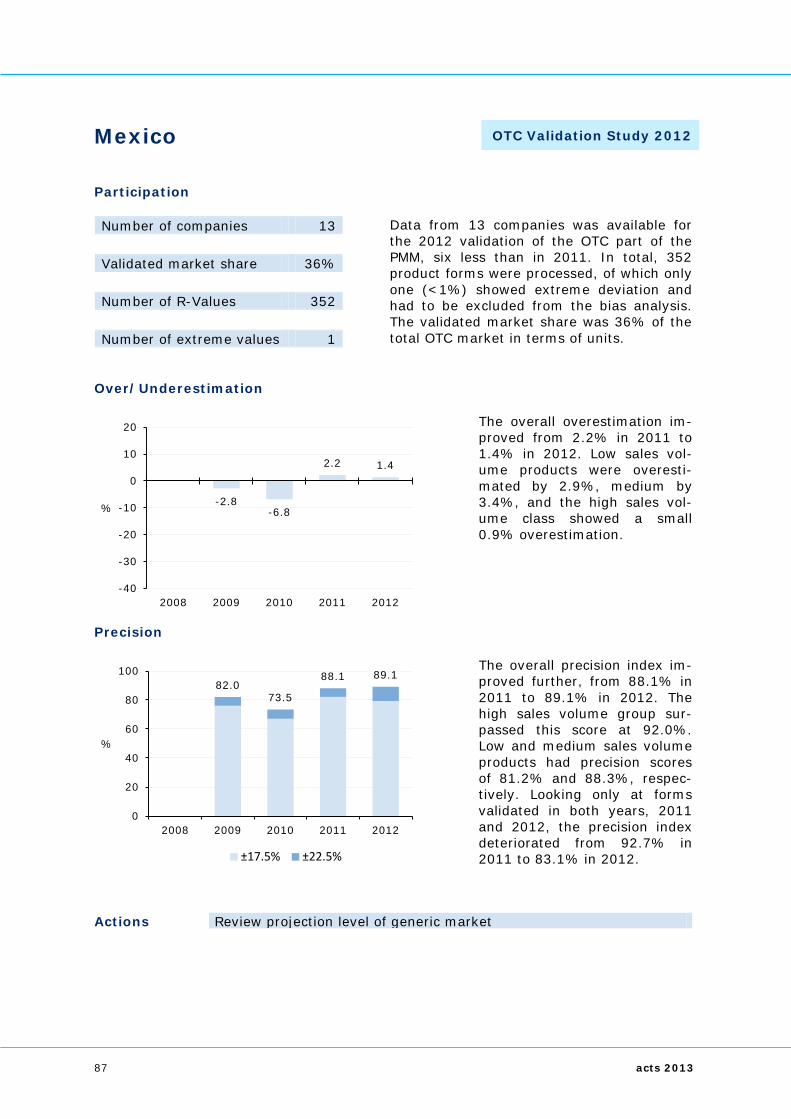

Mexico 87

Poland 88

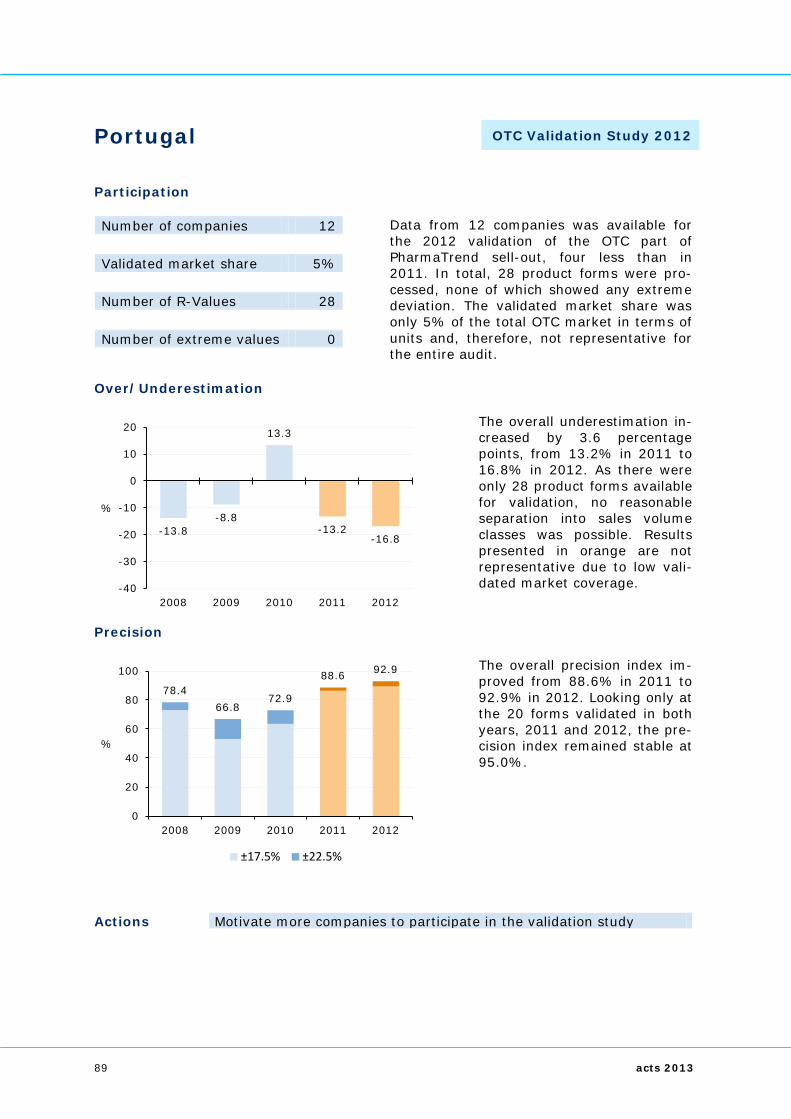

Portugal 89

Spain 90

Switzerland 91

Venezuela 92

PharmaTrend Validation 93

Austria 95

Belgium 96

Czech Republic 97

Finland 98

Germany 99

Hungary 100

Italy 101

Poland 102

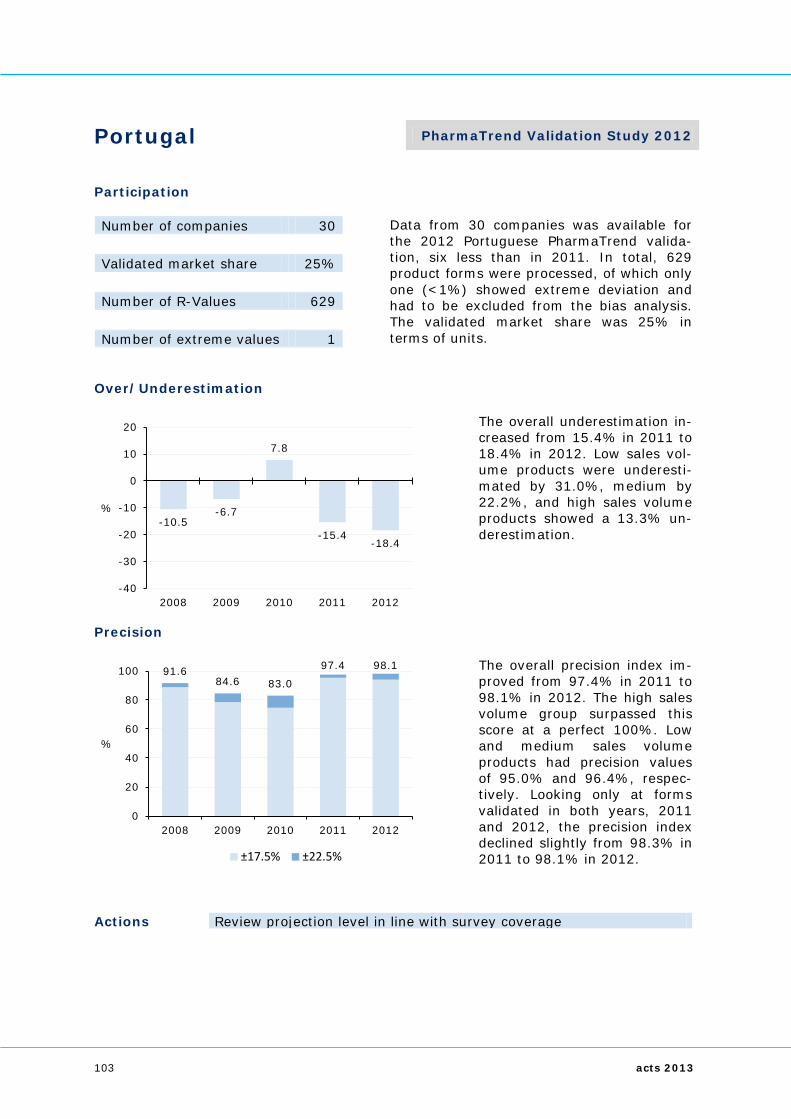

Portugal 103

Spain 104

Switzerland 105

Hospital Validation 106

Austria 108

Belgium 109

Bulgaria 110

Canada 111

China 112

Germany 113

Italy 114

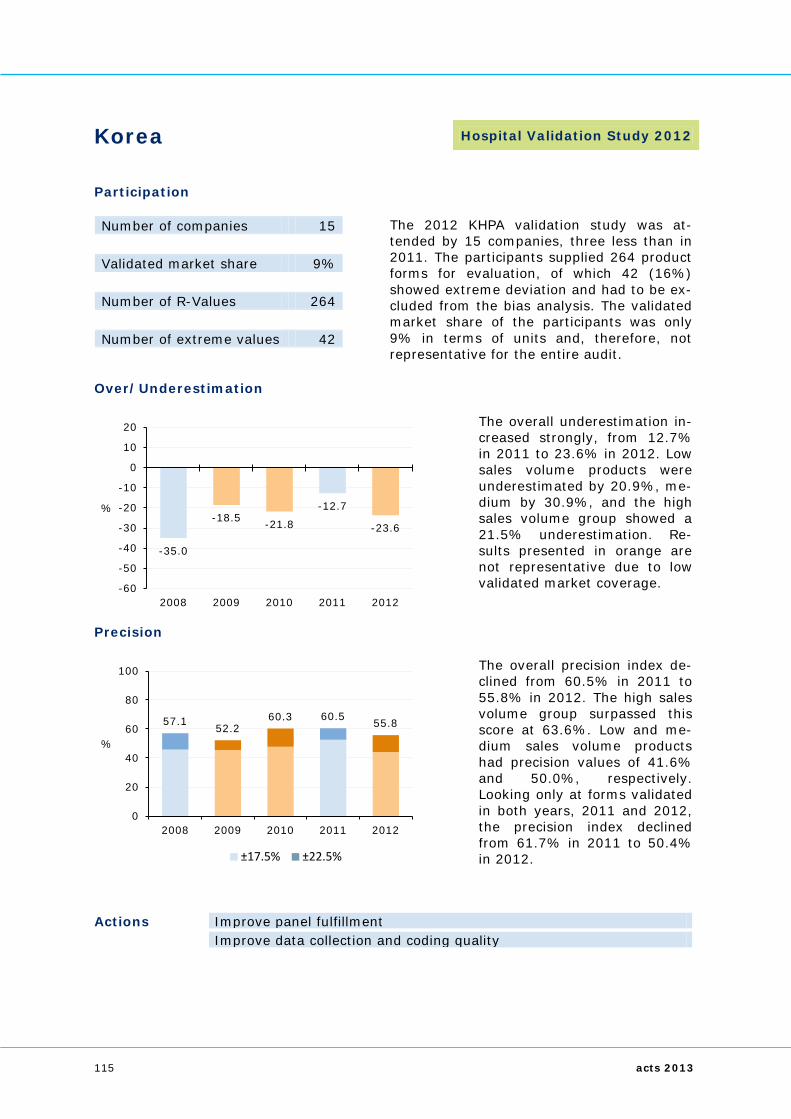

Korea 115

Philippines 116

Spain 117

Switzerland 118

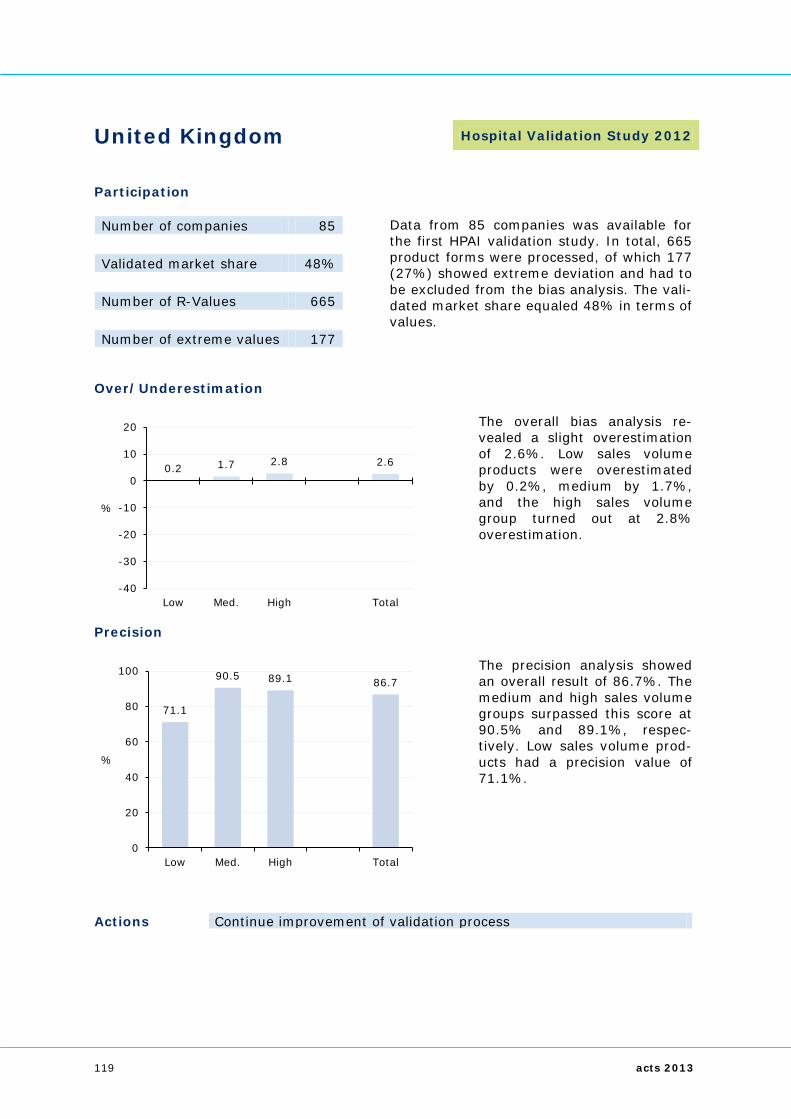

United Kingdom 119

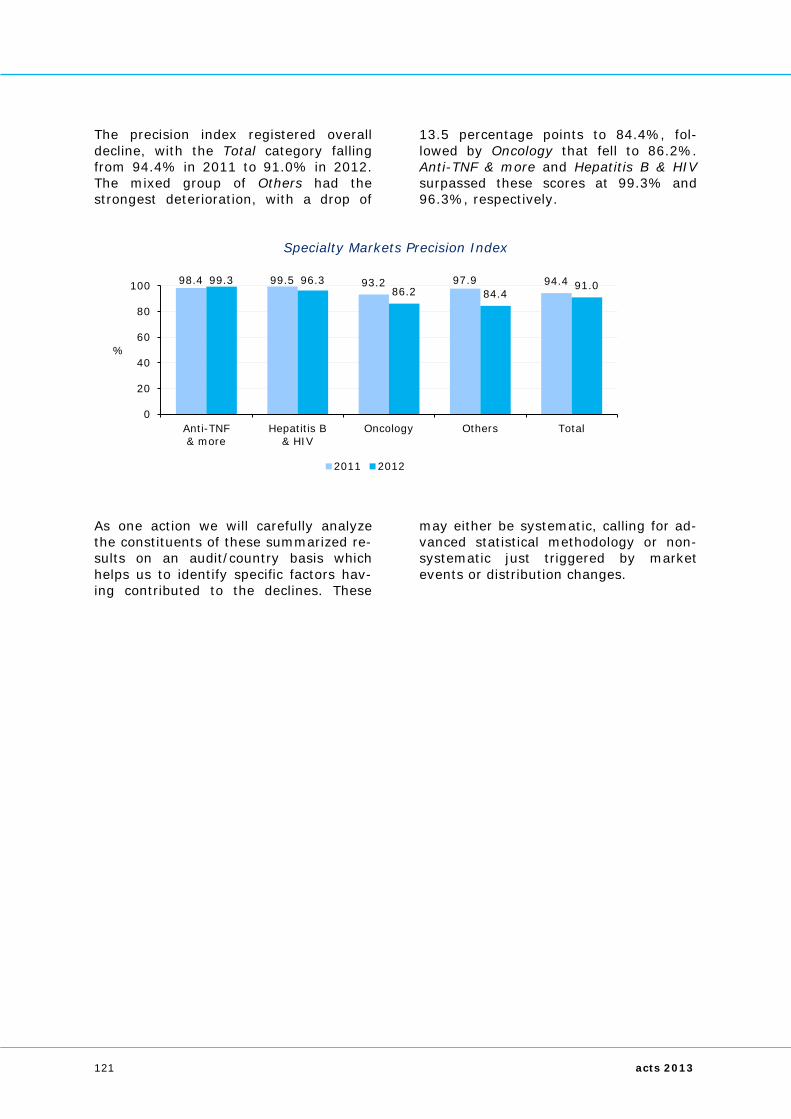

Specialty Mar-kets Validation 120

Forecasting Validation 122

Accuracy (cont’d) 124

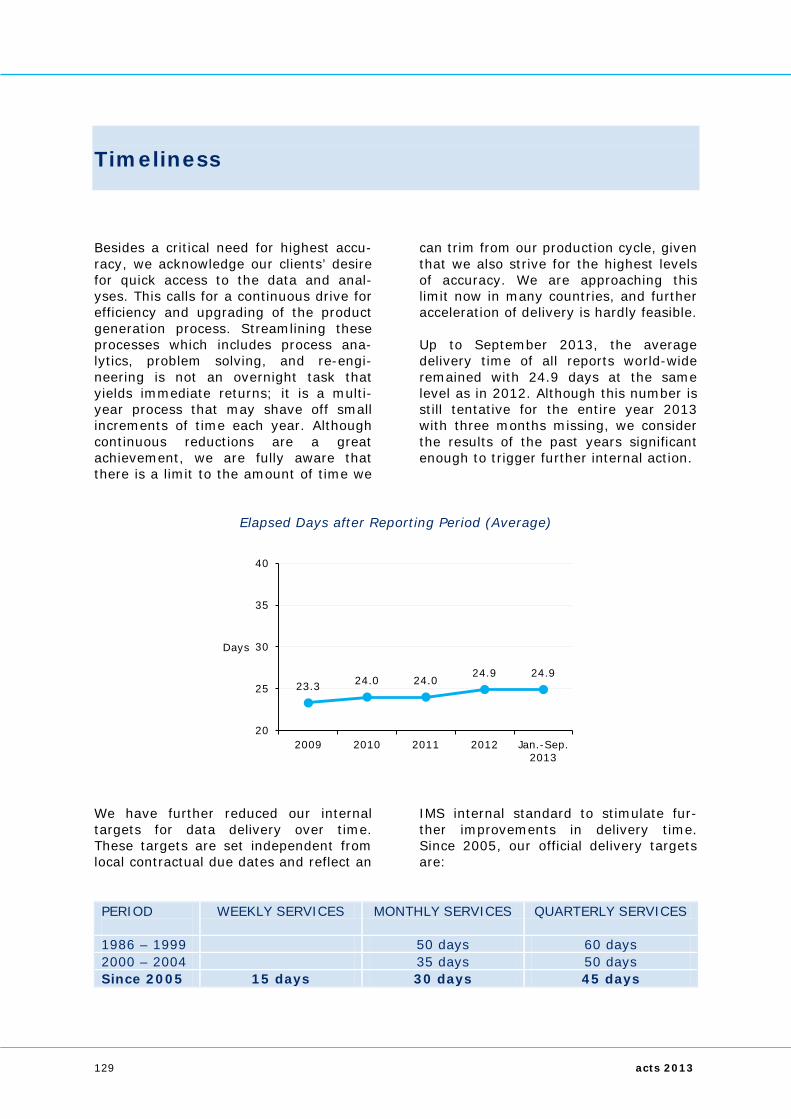

Timeliness 129

Contact 133

2 acts 2013

Abstract Dear Client: With this edition of ACTS – the IMS Health Annual Report on Quality As-sessment – we are continuing a 27-year tradition of documenting the quality of our products for our customers. Quality, which can be expressed quite simply as “sound information at the right time”, can be measured in terms of Accuracy and Timeliness of Delivery. These as-pects of quality are paramount to users of IMS Health data and analytics, and through our publication of ACTS, we demonstrate our commitment to both. In performing our analysis, we hold our last year’s performance against strict thresholds and then report on both achievements and challenges. Accuracy metrics are derived from validation pro-cesses that reflect how close our data estimates were to the industry’s actual numbers. To make the comparison, we collect data down to the pack level on over 70,000 individual product forms – from more than 2,300 pharmaceutical company affiliates – in over 60 countries. Getting returns back from all 2,300 cus-tomers takes time – normally a full year. For this reason, we can only update you now on validity metrics for 2012; the validation process for 2013 has just be-gun. With the 2012 data, we’ve generally seen a minor decline against prior year – typically of one percentage point – in the overall precision index, which is calcu-lated as an aggregate of the precision in the retail, hospital, and pharmacy-based services. The overall precision level is evidence of continued stability for 2012. It is perfectly in line with that of previous years when we saw only slight fluctua-tions on a high precision level of 93% to

94%. This degree of stability is also visi-ble in all underlying offering types: retail and pharmacy at 94% and hospital re-ports at 90%. OTC offerings in the Con-sumer Health area even had their se-cond-best year in a five-year history, at 93%. Clearly, some markets saw economic pressure in 2012, mostly in the Euro zone and shortly after the turning point of the European financial crisis. Valida-tion results indicate that Accuracy in the US has declined by nearly two percent-age points, mainly due to the fact that a series of blockbuster products faced pa-tent expiration, which caused pre-expiry pipeline effects. Meanwhile, the precision level dropped in the two leading emerg-ing markets, China and India, also driven by rapid changes in the logistics and in-frastructure of pharmaceutical distribu-tion. In contrast, 11 countries – more than half from Latin America – have shown improvement over the preceding year. On the delivery side, we are proud to re-port that a challenging trend has come to a stop: in the first three quarters of 2013, delivery on average was made 24.9 days after the end of the reporting period – exactly as it had been in the prior year. Meanwhile, on-target perfor-mance even improved to 82%. This is not yet at the level set in 2011 and ear-lier, but could be interpreted as a turning point. As in previous years, ACTS will give you an honest appraisal of the quality of IMS Health's core offerings, reporting on a mix of favorable and less favorable trends and conditions. Please be assured

3 acts 2013

that the entire IMS Health Statistical Services team, the IMS Health Global Operations community and our local of-fices will strive for further improvement where necessary and retain the excellent results already achieved. The ACTS program is unparalleled across our industry and is very demanding in terms of time and effort. We would like to thank all our clients for helping to make this report possible through your

outstanding collaboration. Your com-ments and questions are very welcome; we invite you to keep the discussion alive and help us make ACTS a superior and relevant reference. Yours sincerely, Stefan Ziegele Vice President IMS Statistical Services

4 acts 2013

Accuracy The IMS Validation Studies, with their global reach and standardized measures, provide pharmaceutical companies with an impartial and forthright reference with which to judge the quality of IMS

data. By thus reporting on the precision of IMS’ decision-support tools, validation studies facilitate pharmaceutical compa-nies’ international decision making.

The Validation Process IMS conducts its Validation Studies in close co-operation with our service sub-scribers. Once we complete our year-end pharmacy audit, we supply our subscrib-ers with software that presents our esti-mated yearly sales volume for each product pack. Subscribers then enter their actual sales volume based on what they supplied to retail pharmacies. We then calculate an “R-Value” repre-senting the ratio of estimated sales as projected by IMS to actual sales as re-ported by our industry partners. For each product examined, we calculate an individual “R-Value.” We also calculate an average R-Value across all validated product forms. R-Values indicate the scale of overesti-mation or underestimation in IMS re-sults. An R-Value of 1.0 is the ideal and would mean that our projection matched reality exactly. Due to the nature of sta-tistical sampling, R-Values typically de-viate from 1.0, and it is only practical to strive for individual R-Values that are clustered tightly around this theoretical ideal. We express audit precision (or the de-gree of clustering) as the percentage of all individual R-Values that fall within a predefined range of deviation around the

average R-Value. The standard precision range is ±22.5 percentage points, some-times paired with a tighter range of ±17.5 percentage points around the av-erage over/underestimation. The greater the data precision, the more tightly R-Values will be clustered in the centre of this range. A precision value of 90 percent, paired with a zero percent bias, can be inter-preted as follows: On average, IMS audit data reflect a high degree of homogene-ity since 90 percent of the validated product forms lie between –22.5 percent and +22.5 percent of the reported in-dustry numbers. If we were to apply the tighter ±17.5 percent precision range to the same data as an additional measure, an 85 percent value would indicate that: • 85 percent of the validated product

forms were between –17.5 percent and +17.5 percent of the average R-Value and

• 5 percent deviated by more than

±17.5 percent but less than ±22.5 percent. The remaining 10 percent were outside the ±22.5 percentage range.

5 acts 2013

Conceptually, comparing IMS audit esti-mates with manufacturer sales data re-quires that the numbers be fully com-patible. This compatibility hinges on the ability of companies participating in the validation study to segregate their inter-nal sales data, isolating those sales channeled to the pharmacy retailing sector. The degree to which they can do this correlates closely with the technical infrastructure of the country and the complexity of the distribution system. When sales to other market sectors (e.g., tenders, exports) are not segre-gated and instead are included in a com-pany’s sales, the assumption is that IMS data have underestimated reality, and consequently they are viewed as incor-rect. Parallel trade practices add another ele-ment of incompatibility to the data. Typi-cally, manufacturers are unaware of the sales volume that sub-distributors and pharmacies export to other countries (parallel exports) or import from other countries (parallel imports). In parallel export situations, the industry numbers are usually inflated by sales that never entered the domestic pharmacy market. Conversely, in parallel import situations in which the imported items are not iso-

lated, for example through official paral-lel traders, IMS numbers are usually in-flated. Due to growing issues with data incom-patibility, validation studies are gradually losing some of their potency as an ob-jective measure of accuracy. Thus we are in the process of evaluating meas-ures of data relevance for those regions highly affected by parallel business (e.g., European rim). Nevertheless, we believe that once we exclude products typically traded in parallel from the validation process, the exercise still provides a good overall picture of the accuracy and trends achieved in the individual mar-kets. Validation Study results are considered to be representative of the survey uni-verse if more than 20 percent of the market is reflected in what our data partners send us. If the total market coverage reported by our data partners falls between 10 and 20 percent, valida-tion results may still give a good indica-tion of change from one year to the next, but otherwise must be used with care. Studies with participation rates less than 10 percent are included in the ACTS report but marked as not representative.

The 2012 Validation Results The validation process usually starts 2-3 months after the close of the year being validated. Typically, it can take up to ten months after we receive final feedback and can complete the analysis of any given country. This year, the last com-pleted materials for 2012 were returned to us in February 2014.

The 2012 participation level decreased slightly to a total of 39 companies on av-erage participating in a country’s valida-tion process, compared to 40 companies in 2011. In total, 2,321 company affili-ates world-wide participated in the 2012 validation surveys and supplied 70,927 product forms for analysis.

Global Validation Results Until a couple of years ago, we only vali-dated IMS retail audits while hospital, OTC and PharmaTrend offerings were quality-assessed more on a sporadic ba-sis. Along with an upgrading of the ACTS

validation process, we also incorporated these other standard deliverables in ACTS and have provided you lately with individual validation results. One request from our readers’ community was to

6 acts 2013

summarize all individual validation re-sults to one single metric – the Global Precision Index. This is an aggregate of all validations performed with uninter-rupted 5-years data and serves as a high level indicator on IMS data accuracy. For 2012, this global index utilizes the

outcome from 88 validation studies and demonstrates a high degree of stability across the 5-years time period. Lately, a slight reduction by 1.2 percentage points has been visible but keeps the index at a robust value of 93.1% - still in line with previous years’ results.

Global Precision Index

Retail Validation Results For the 2012 validation studies, 61 countries provided analyzable results. No validation study was necessary in Den-mark, Finland, the Netherlands, Norway and Sweden because we collect full cen-sus data in these countries. There, preci-sion results are assumed to be 100 per-

cent. This makes a total of 66 sets of validation results, of which 56 had unin-terrupted five-year results. The overall degree of precision in IMS pharmaceuti-cal reports is best described by an ag-gregated precision index for these 56 countries:

Retail Precision Index

93.6 93.9 93.4 94.3 93.1

0.0

20.0

40.0

60.0

80.0

100.0

2008 2009 2010 2011 2012

%

94.5 94.8 94.3 95.0 94.0

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

7 acts 2013

Overall, the Retail Precision Index over the 5-year period documents solid out-come in maintaining existing levels of data quality well above the 90% margin.

However, in 2012, the index showed de-cline of one percentage point over 2011 and with 94.0% reached the lowest pre-cision level of the last five years.

Regional Retail Results The 66 countries are distributed over the greater IMS regions as follows:

Regional Distribution of Participation

Regional Retail Precision Index 2011/2012

2

13

14

3 8

11

14

1

North America

Latin America

North Europe & Africa

Central Europe

East Europe

South Europe & Mid East

AsiaPacific

Japan

0 20 40 60 80 100

Japan

AsiaPacific

South Europe & Mid East

East Europe

Central Europe

North Europe & Africa

Latin America

North America

World

%

Improvement

Deterioration

8 acts 2013

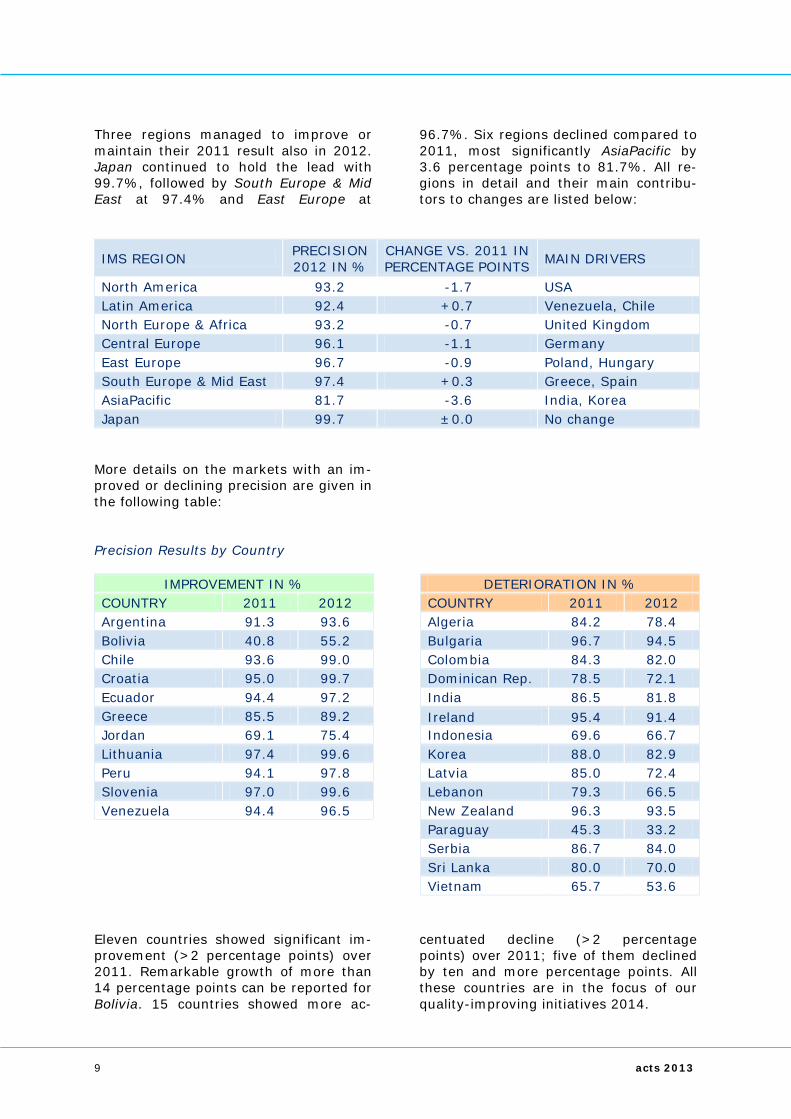

Three regions managed to improve or maintain their 2011 result also in 2012. Japan continued to hold the lead with 99.7%, followed by South Europe & Mid East at 97.4% and East Europe at

96.7%. Six regions declined compared to 2011, most significantly AsiaPacific by 3.6 percentage points to 81.7%. All re-gions in detail and their main contribu-tors to changes are listed below:

IMS REGION PRECISION 2012 IN %

CHANGE VS. 2011 IN PERCENTAGE POINTS MAIN DRIVERS

North America 93.2 -1.7 USA Latin America 92.4 +0.7 Venezuela, Chile North Europe & Africa 93.2 -0.7 United Kingdom Central Europe 96.1 -1.1 Germany East Europe 96.7 -0.9 Poland, Hungary South Europe & Mid East 97.4 +0.3 Greece, Spain AsiaPacific 81.7 -3.6 India, Korea Japan 99.7 ±0.0 No change

More details on the markets with an im-proved or declining precision are given in the following table: Precision Results by Country

IMPROVEMENT IN % DETERIORATION IN % COUNTRY 2011 2012 COUNTRY 2011 2012 Argentina 91.3 93.6 Algeria 84.2 78.4 Bolivia 40.8 55.2 Bulgaria 96.7 94.5 Chile 93.6 99.0 Colombia 84.3 82.0 Croatia 95.0 99.7 Dominican Rep. 78.5 72.1 Ecuador 94.4 97.2 India 86.5 81.8 Greece 85.5 89.2 Ireland 95.4 91.4 Jordan 69.1 75.4 Indonesia 69.6 66.7 Lithuania 97.4 99.6 Korea 88.0 82.9 Peru 94.1 97.8 Latvia 85.0 72.4 Slovenia 97.0 99.6 Lebanon 79.3 66.5 Venezuela 94.4 96.5 New Zealand 96.3 93.5

Paraguay 45.3 33.2

Serbia 86.7 84.0

Sri Lanka 80.0 70.0

Vietnam 65.7 53.6

Eleven countries showed significant im-provement (>2 percentage points) over 2011. Remarkable growth of more than 14 percentage points can be reported for Bolivia. 15 countries showed more ac-

centuated decline (>2 percentage points) over 2011; five of them declined by ten and more percentage points. All these countries are in the focus of our quality-improving initiatives 2014.

9 acts 2013

Country-specific Results The validation studies mentioned on the following country pages refer to the IMS

retail reports, with the following excep-tions:

COUNTRY MARKET COVERED Croatia, Czech Republic, Hungary, India, Poland, Serbia, Slovak Republic, Slovenia, United States

Hospital market included

Hong Kong, Indonesia, Vietnam Total market Malaysia, Singapore Total private market

Further parts of this accuracy section, which follow the retail validation pages, highlight other validation initiatives of high interest to our data subscribers: • OTC Validation Studies • PharmaTrend Validation Studies • Hospital Validation Studies • Specialty Markets Validation Results • Validating IMS Forecasting Services

In addition, we are providing updates on the latest measures we’ve taken to sus-tain today’s quality levels: • Universe Updates • Data Capture • Sample Fulfillment

10 acts 2013

Algeria Retail Validation Study 2012

Participation Number of companies 13 The 2012 LMNPA validation study was at-

tended by 13 companies, two more than in 2011. The participants supplied 235 product forms for evaluation, of which 10 (4%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 27% in terms of units.

Validated market share 27% Number of R-Values 235 Number of extreme values 10

Over/Underestimation

The overall bias turned from 1.3% underestimation in 2011 to 1.2% overestimation in 2012. Low and high sales vol-ume products were overesti-mated by 3.9% and 1.5%, re-spectively, whereas the me-dium sales volume group showed a small underestima-tion of 0.6%.

Precision

The overall precision index de-clined from 84.2% in 2011 to 78.4% in 2012. The medium sales volume group surpassed this score at 83.5%. Low and high sales volume products had precision values of 76.0% and 76.1%, respectively. Looking only at forms validated in both years, 2011 and 2012, the pre-cision index declined from 85.3% in 2011 to 83.1% in 2012.

Actions Enhance projection methodology

0.6

-4.4 -1.3

1.2

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

85.6 83.1 84.2 78.4

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

11 acts 2013

Argentina Retail Validation Study 2012

Participation Number of companies 64 The 2012 PMA validation study was attended

by 64 companies, the same number as in 2011. The participants supplied 2,929 prod-uct forms for evaluation, of which 60 (2%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 59% in terms of units.

Validated market share 59% Number of R-Values 2,929 Number of extreme values 60

Over/Underestimation

The overall underestimation in-creased from 3.7% in 2011 to 4.5% in 2012. Low sales vol-ume products were underesti-mated by 2.9%, medium by 3.1%, and the high sales vol-ume group showed a 5.6% un-derestimation.

Precision

The overall precision index im-proved from 91.3% in 2011 to 93.6% in 2012. The high sales volume group surpassed this score at 95.1%. Low and me-dium sales volume products had precision values of 91.0% and 92.5%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 91.7% in 2011 to 95.2% in 2012.

Actions No action required from the statistical point of view

-1.9 -6.7 -5.6 -3.7 -4.5

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

96.0 93.4 92.8 91.3 93.6

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

12 acts 2013

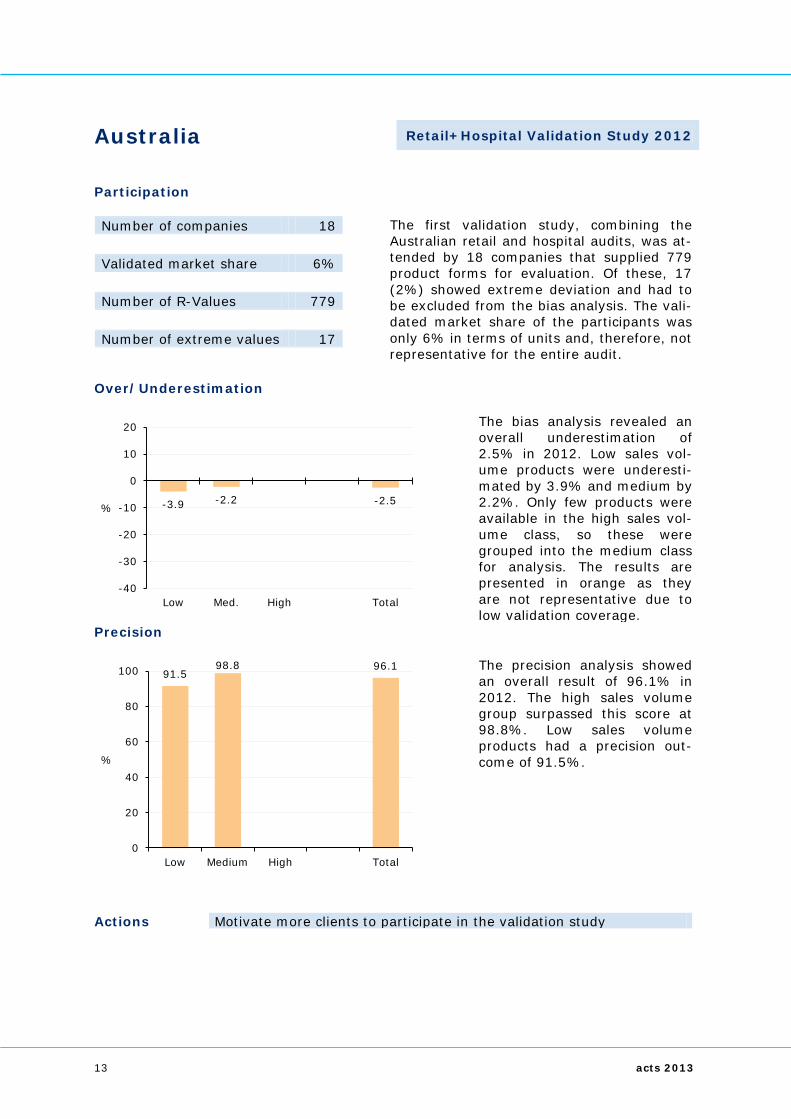

Australia Retail+Hospital Validation Study 2012

Participation Number of companies 18 The first validation study, combining the

Australian retail and hospital audits, was at-tended by 18 companies that supplied 779 product forms for evaluation. Of these, 17 (2%) showed extreme deviation and had to be excluded from the bias analysis. The vali-dated market share of the participants was only 6% in terms of units and, therefore, not representative for the entire audit.

Validated market share 6% Number of R-Values 779 Number of extreme values 17

Over/Underestimation

The bias analysis revealed an overall underestimation of 2.5% in 2012. Low sales vol-ume products were underesti-mated by 3.9% and medium by 2.2%. Only few products were available in the high sales vol-ume class, so these were grouped into the medium class for analysis. The results are presented in orange as they are not representative due to low validation coverage.

Precision

The precision analysis showed an overall result of 96.1% in 2012. The high sales volume group surpassed this score at 98.8%. Low sales volume products had a precision out-come of 91.5%.

Actions Motivate more clients to participate in the validation study

-3.9 -2.2 -2.5

-40

-30

-20

-10

0

10

20

Low Med. High Total

%

91.5 98.8 96.1

0

20

40

60

80

100

Low Medium High Total

%

13 acts 2013

Austria Retail Validation Study 2012

Participation Number of companies 16 The 2012 DPMOE validation study was at-

tended by 16 companies, the same number as in 2011. The participants supplied 654 product forms for evaluation, of which 5 (<1%) showed extreme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 25% in terms of units.

Validated market share 25% Number of R-Values 654 Number of extreme values 5

Over/Underestimation

The overall underestimation in-creased slightly, from 1.3% in 2011 to 1.9% in 2012. Low sales volume products were underestimated by 2.4%, me-dium by 2.3%, and the high sales volume group showed a 1.7% underestimation.

Precision

The overall precision index im-proved slightly from 97.8% in 2011 to 97.9% in 2012. The medium and high sales volume groups surpassed this score at 98.1% and 99.1%, respec-tively. Low sales volume prod-ucts had a precision value of 93.2%. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 98.8% in 2011 to 98.3% in 2012.

Actions No action required from the statistical point of view

-1.7 -0.1 -1.5 -1.3 -1.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

97.8 94.9 95.6 97.8 97.9

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

14 acts 2013

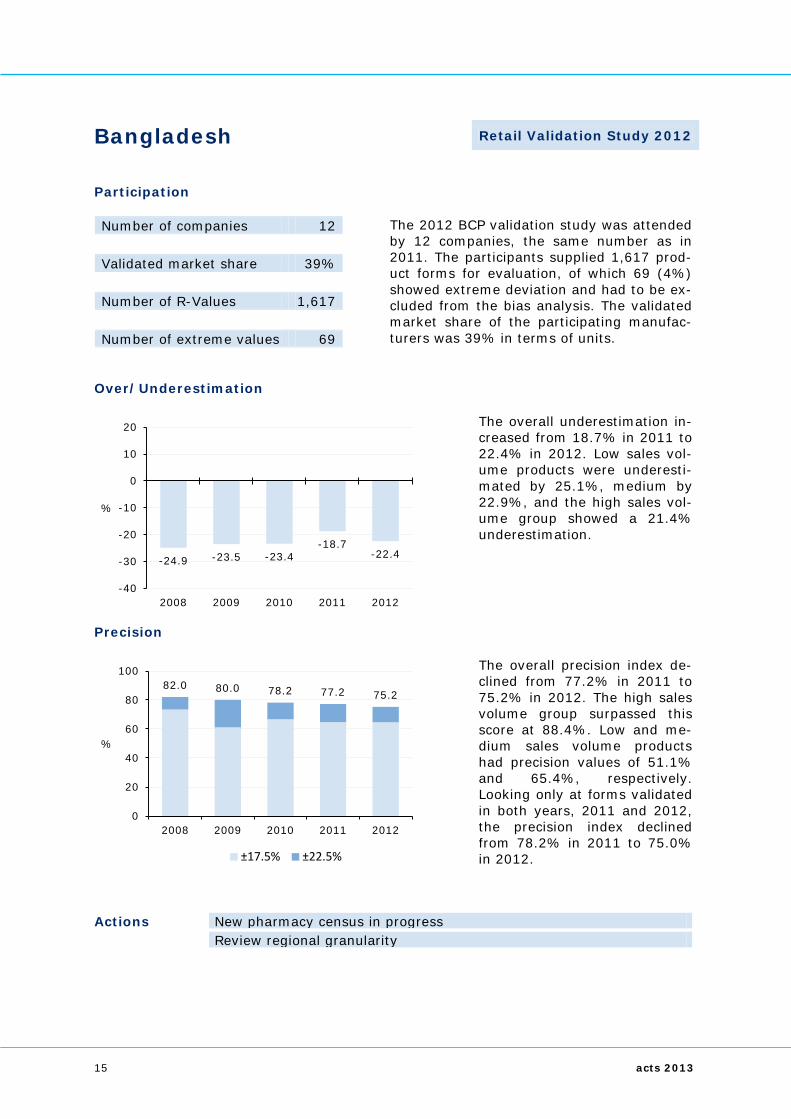

Bangladesh Retail Validation Study 2012

Participation Number of companies 12 The 2012 BCP validation study was attended

by 12 companies, the same number as in 2011. The participants supplied 1,617 prod-uct forms for evaluation, of which 69 (4%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 39% in terms of units.

Validated market share 39% Number of R-Values 1,617 Number of extreme values 69

Over/Underestimation

The overall underestimation in-creased from 18.7% in 2011 to 22.4% in 2012. Low sales vol-ume products were underesti-mated by 25.1%, medium by 22.9%, and the high sales vol-ume group showed a 21.4% underestimation.

Precision

The overall precision index de-clined from 77.2% in 2011 to 75.2% in 2012. The high sales volume group surpassed this score at 88.4%. Low and me-dium sales volume products had precision values of 51.1% and 65.4%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined from 78.2% in 2011 to 75.0% in 2012.

Actions New pharmacy census in progress Review regional granularity

-24.9 -23.5 -23.4 -18.7

-22.4

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

82.0 80.0 78.2 77.2 75.2

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

15 acts 2013

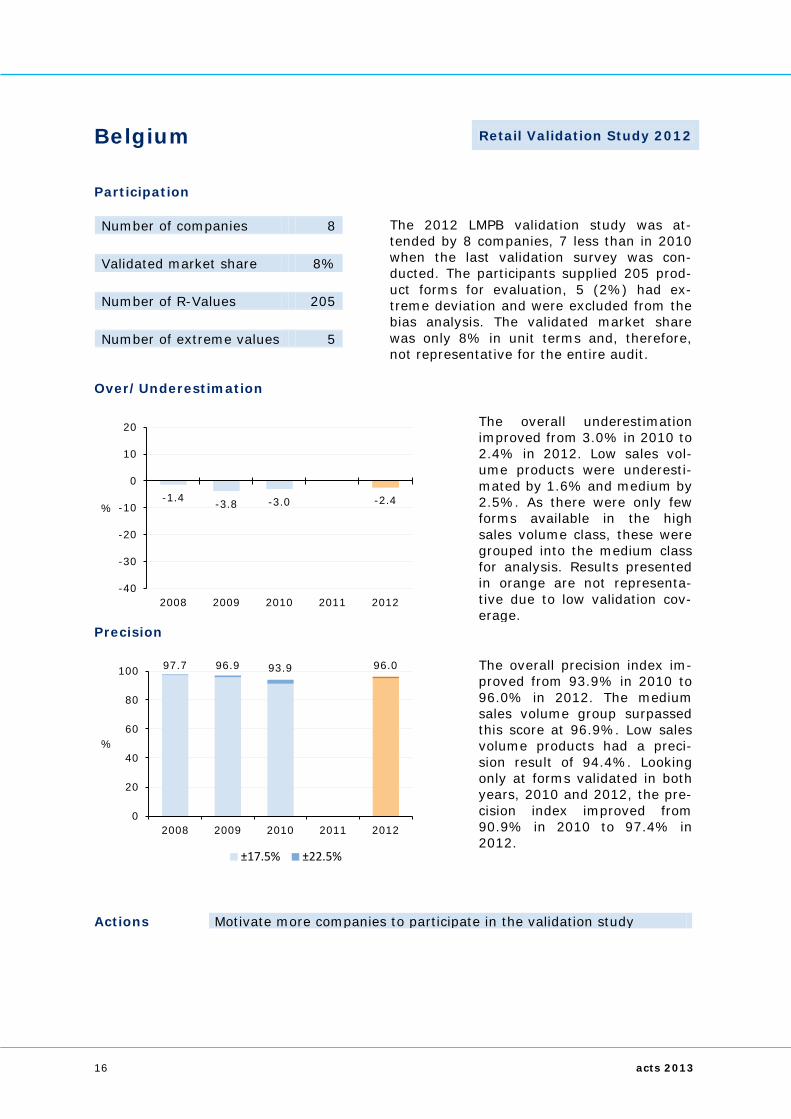

Belgium Retail Validation Study 2012

Participation Number of companies 8 The 2012 LMPB validation study was at-

tended by 8 companies, 7 less than in 2010 when the last validation survey was con-ducted. The participants supplied 205 prod-uct forms for evaluation, 5 (2%) had ex-treme deviation and were excluded from the bias analysis. The validated market share was only 8% in unit terms and, therefore, not representative for the entire audit.

Validated market share 8% Number of R-Values 205 Number of extreme values 5

Over/Underestimation

The overall underestimation improved from 3.0% in 2010 to 2.4% in 2012. Low sales vol-ume products were underesti-mated by 1.6% and medium by 2.5%. As there were only few forms available in the high sales volume class, these were grouped into the medium class for analysis. Results presented in orange are not representa-tive due to low validation cov-erage.

Precision

The overall precision index im-proved from 93.9% in 2010 to 96.0% in 2012. The medium sales volume group surpassed this score at 96.9%. Low sales volume products had a preci-sion result of 94.4%. Looking only at forms validated in both years, 2010 and 2012, the pre-cision index improved from 90.9% in 2010 to 97.4% in 2012.

Actions Motivate more companies to participate in the validation study

-1.4 -3.8 -3.0 -2.4

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

97.7 96.9 93.9 96.0

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

16 acts 2013

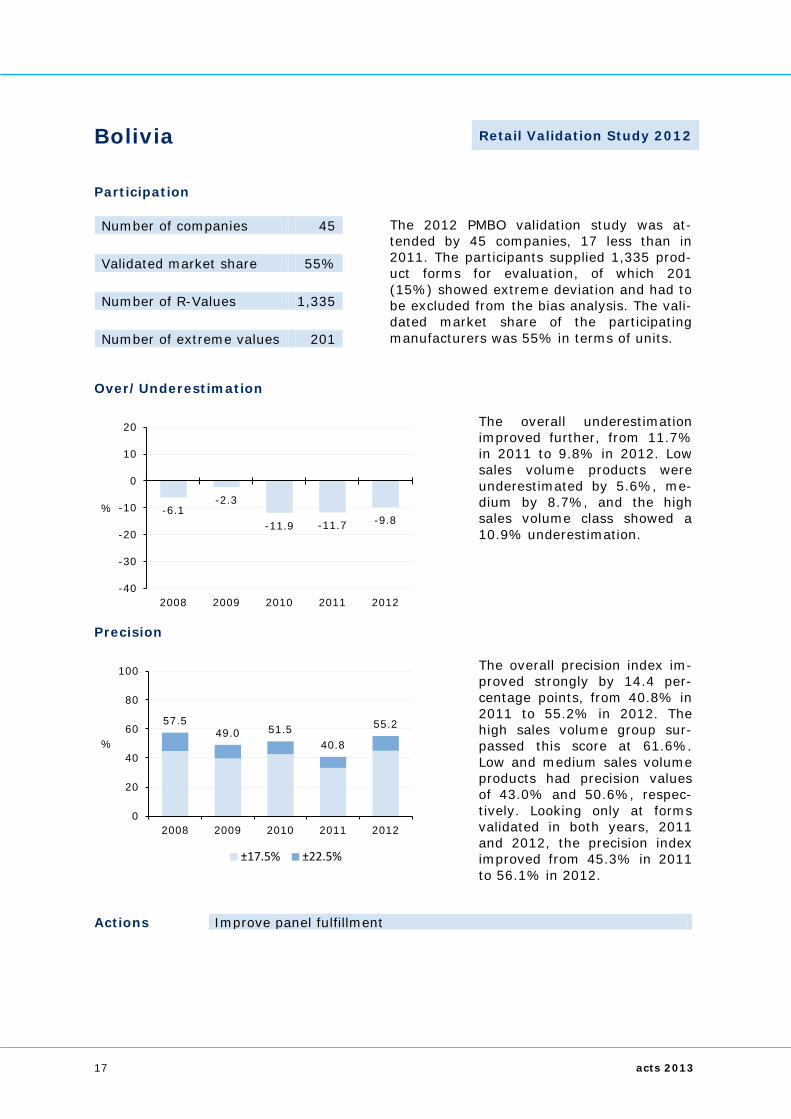

Bolivia Retail Validation Study 2012

Participation Number of companies 45 The 2012 PMBO validation study was at-

tended by 45 companies, 17 less than in 2011. The participants supplied 1,335 prod-uct forms for evaluation, of which 201 (15%) showed extreme deviation and had to be excluded from the bias analysis. The vali-dated market share of the participating manufacturers was 55% in terms of units.

Validated market share 55% Number of R-Values 1,335 Number of extreme values 201

Over/Underestimation

The overall underestimation improved further, from 11.7% in 2011 to 9.8% in 2012. Low sales volume products were underestimated by 5.6%, me-dium by 8.7%, and the high sales volume class showed a 10.9% underestimation.

Precision

The overall precision index im-proved strongly by 14.4 per-centage points, from 40.8% in 2011 to 55.2% in 2012. The high sales volume group sur-passed this score at 61.6%. Low and medium sales volume products had precision values of 43.0% and 50.6%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 45.3% in 2011 to 56.1% in 2012.

Actions Improve panel fulfillment

-6.1 -2.3

-11.9 -11.7 -9.8

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

57.5 49.0 51.5

40.8

55.2

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

17 acts 2013

Brazil Retail Validation Study 2012

Participation Number of companies 28 The 2012 PMB validation study was attended

by 28 multinational companies, the same number as in 2011. The participants sup-plied 1,250 product forms for evaluation, of which 9 (<1%) showed extreme deviation and had to be excluded from the bias analy-sis. The validated market share of the participating manufacturers was 18% in terms of units.

Validated market share 18% Number of R-Values 1,250 Number of extreme values 9

Over/Underestimation

The overall underestimation in-creased by four percentage points, from 3.8% in 2011 to 7.8% in 2012. Low sales vol-ume products were underesti-mated by 9.9%, medium by 8.3%, and the high sales vol-ume group showed a 6.9% un-derestimation.

Precision

The overall precision index de-clined slightly, from 93.9% in 2011 to 93.7% in 2012. The high sales volume group sur-passed this score at 95.8%. Low and medium sales volume products had precision values of 89.8% and 92.0%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 95.8% in 2011 to 98.4% in 2012.

Actions Conduct distribution channel survey in 2014

-3.2 -5.4 -6.5 -3.8

-7.8

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

91.2 92.6 94.9 93.9 93.7

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

18 acts 2013

Bulgaria Retail Validation Study 2012

Participation Number of companies 59 The 2012 BGPI validation study was at-

tended by 59 companies, ten more than in 2011. The participants supplied 851 product forms for evaluation, of which 16 (2%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 58% in terms of units.

Validated market share 58% Number of R-Values 851 Number of extreme values 16

Over/Underestimation

The overall bias turned from 1.0% underestimation in 2011 to a small overestimation of 0.5% in 2012. Low sales vol-ume products were underesti-mated by 1.5%, medium by 0.8%, and the high sales vol-ume group showed a 1.5% overestimation.

Precision

The overall precision index de-clined from 96.7% in 2011 to 94.5% in 2012. The high sales volume group surpassed this score at 97.5%. Low and me-dium sales volume products had precision values of 87.8% and 92.9%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined from 97.7% in 2011 to 94.4% in 2012.

Actions No immediate action required from the statistical point of view

-0.2

2.2

-3.3 -1.0

0.5

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

93.6 94.8 97.7 96.7 94.5

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

19 acts 2013

Canada Retail Validation Study 2012

Participation Number of companies 88 Data from 88 companies, one more than in

2011, was available for the 2012 CDH Drug-stores validation study. In total, 3,259 prod-uct forms were processed, of which 7 (<1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share equaled 95% in terms of units, representing the highest participation rate across all countries.

Validated market share 95% Number of R-Values 3,259 Number of extreme values 7

Over/Underestimation

The overall overestimation in-creased slightly, from 0.6% in 2011 to 1.2% in 2012. Low and high sales volume products were both overestimated by 1.0% and medium sales vol-ume products showed a 1.6% overestimation.

Precision

The overall precision index showed stability at 98.9% in 2012. The high sales volume group surpassed this score at 99.5%. Low and medium sales volume products had precision values of 97.3% and 98.7%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 99.1% in 2011 to 98.9% in 2012.

Actions No action required from the statistical point of view

1.1 0.6 0.7 0.6 1.2

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

98.2 99.0 98.8 99.1 98.9

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

20 acts 2013

Central America Retail Validation Study 2012

Participation Number of companies 31 The 2012 PMCA validation study was at-

tended by 31 companies, two more than in 2011. The participants supplied 1,833 prod-uct forms for evaluation, of which 68 (4%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 33% in terms of units.

Validated market share 33% Number of R-Values 1,833 Number of extreme values 68

Over/Underestimation

The overall underestimation in-creased slightly, from 1.5% in 2011 to 2.9% in 2012. Low sales volume products were underestimated by 3.7%, me-dium by 2.6%, and the high sales volume classes showed a 3.0% underestimation.

Precision

The overall precision index im-proved slightly, from 87.4% in 2011 to 87.9% in 2012. The high sales volume group sur-passed this score at 91.3%. Low and medium sales volume products had precision results of 77.1% and 87.6%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 89.1% in 2011 to 91.8% in 2012.

Actions Review projection level

-8.4 -3.6 -3.0 -1.5 -2.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

84.8 86.9 88.9 87.4 87.9

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

21 acts 2013

Chile Retail Validation Study 2012

Participation Number of companies 15 The 2012 PMCH validation study was at-

tended by 15 companies, two more than in 2011. The participants supplied 842 product forms for evaluation, of which only one (<1%) showed extreme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 20% in terms of units.

Validated market share 20% Number of R-Values 842 Number of extreme values 1

Over/Underestimation

The 2012 overall bias analysis revealed the same result of 0.1% overestimation as in 2011. Low sales volume prod-ucts were overestimated by 1.7%, whereas medium and high sales volume products were underestimated by 0.4% and 0.3%, respectively.

Precision

The overall precision index im-proved by 5.4 percentage points, from 93.6% in 2011 to 99.0% in 2012. The high sales volume group surpassed this score at a perfect 100%. Low and medium sales volume products had precision values of 96.7% and 98.5%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 96.5% in 2011 to 99.4% in 2012.

Actions Conduct distribution channel survey in 2014

-3.1 -2.9 -4.8

0.1 0.1

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

90.9 94.9 93.4 93.6 99.0

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

22 acts 2013

Colombia Retail Validation Study 2012

Participation Number of companies 18 The 2012 PMC validation study was attended

by 18 companies, ten more than in 2011. The participants supplied 1,078 product forms for evaluation, of which 82 (8%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 23% in terms of units.

Validated market share 23% Number of R-Values 1,078 Number of extreme values 82

Over/Underestimation

The overall underestimation improved from 9.8% in 2011 to 7.8% in 2012. Low sales vol-ume products were underesti-mated by 2.7%, medium by 4.8%, and the high sales vol-ume group showed a 10.4% underestimation.

Precision

The overall precision index de-clined from 84.3% in 2011 to 82.0% in 2012. The medium and high sales volume groups surpassed this score at 83.4% and 85.7%, respectively. Low sales volume products had a precision value of 66.9%. Looking only at forms validated in both years, 2011 and 2012, the precision index improved slightly from 87.8% in 2011 to 88.0% in 2012.

Actions Conduct distribution channel survey Update universe and sample

-3.1

1.5

-3.5 -9.8 -7.8

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

86.4 89.0 77.1

84.3 82.0

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

23 acts 2013

Croatia Retail+Hospital Validation Study 2012

Participation Number of companies 10 The 2012 validation study, combining the

Croatian retail and hospital audits, was at-tended by 10 companies, two more than in 2011. The participants supplied 541 product forms for evaluation, of which 2 (<1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participants equaled 41% in terms of units.

Validated market share 41% Number of R-Values 541 Number of extreme values 2

Over/Underestimation

The overall overestimation in-creased from 0.6% in 2011 to 2.4% in 2012. Low sales vol-ume products were overesti-mated by 0.7%, medium by 1.6%, and the high sales vol-ume group revealed a 3.4% overestimation.

Precision

The overall precision index im-proved from 95.0% in 2011 to 99.7% in 2012. The medium and high sales volume classes surpassed this score both at a perfect 100%. Low sales vol-ume products had a precision value of 98.3%. Looking only at forms validated in both years, 2011 and 2012, the pre-cision index improved from 99.6% in 2011 to 100% in 2012.

Actions No action required from the statistical point of view

0.6 2.4

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

95.0 99.7

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

24 acts 2013

Czech Republic Retail+Hospital Validation Study 2012

Participation Number of companies 29 The 2012 validation study, combining the

Czech retail and hospital audits, was at-tended by 29 companies, four more than in 2011. The participants supplied 1,147 prod-uct forms for evaluation, of which four showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participants was 48% in terms of units.

Validated market share 48% Number of R-Values 1,147 Number of extreme values 4

Over/Underestimation

The overall underestimation in-creased slightly, from 0.7% in 2011 to 0.9% in 2012. Low sales volume products were underestimated by 1.4%, me-dium by 0.7%, and high sales volume products were under-estimated by 1.0%.

Precision

The overall precision index de-clined marginally by 0.1 per-centage point, from 99.0% in 2011 to 98.9% in 2012. The high sales volume group sur-passed this score at a perfect 100%. Low and medium sales volume products had precision values of 94.1% and 99.5%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 99.4% in 2011 to 99.1% in 2012.

Actions No action required from the statistical point of view

-1.2 -0.4

0.5

-0.7 -0.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

99.1 98.7 98.7 99.0 98.9

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

25 acts 2013

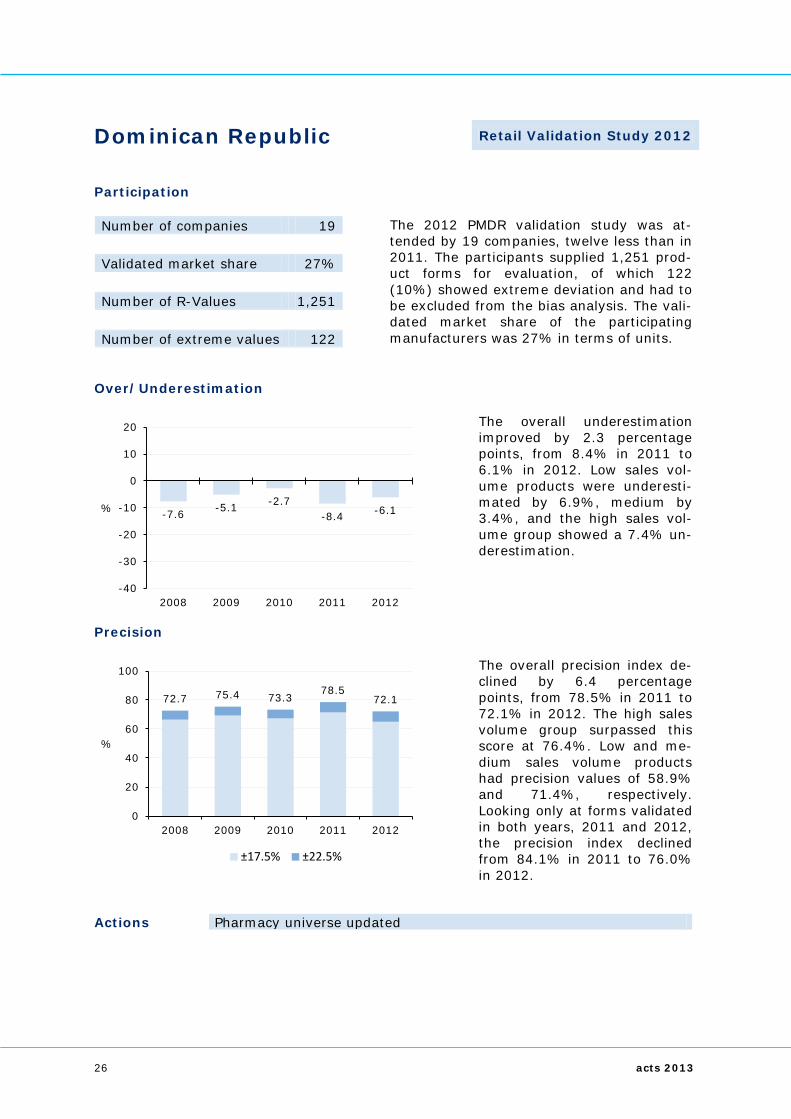

Dominican Republic Retail Validation Study 2012

Participation Number of companies 19 The 2012 PMDR validation study was at-

tended by 19 companies, twelve less than in 2011. The participants supplied 1,251 prod-uct forms for evaluation, of which 122 (10%) showed extreme deviation and had to be excluded from the bias analysis. The vali-dated market share of the participating manufacturers was 27% in terms of units.

Validated market share 27% Number of R-Values 1,251 Number of extreme values 122

Over/Underestimation

The overall underestimation improved by 2.3 percentage points, from 8.4% in 2011 to 6.1% in 2012. Low sales vol-ume products were underesti-mated by 6.9%, medium by 3.4%, and the high sales vol-ume group showed a 7.4% un-derestimation.

Precision

The overall precision index de-clined by 6.4 percentage points, from 78.5% in 2011 to 72.1% in 2012. The high sales volume group surpassed this score at 76.4%. Low and me-dium sales volume products had precision values of 58.9% and 71.4%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined from 84.1% in 2011 to 76.0% in 2012.

Actions Pharmacy universe updated

-7.6 -5.1 -2.7 -8.4 -6.1

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

72.7 75.4 73.3 78.5

72.1

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

26 acts 2013

Ecuador Retail Validation Study 2012

Participation Number of companies 89 The 2012 PME validation study was attended

by 89 companies, one more than in 2011. The participants supplied 2,449 product forms for evaluation, of which 8 (<1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 72% in terms of units.

Validated market share 72% Number of R-Values 2,449 Number of extreme values 8

Over/Underestimation

The overall underestimation improved marginally from 4.8% in 2011 to 4.7% in 2012. Low sales volume products were underestimated by 2.7%, medium by 3.7%, and the high sales volume group showed a 5.8% underestimation.

Precision

The overall precision index im-proved from 94.4% in 2011 to 97.2% in 2012. The medium sales volume group surpassed this score at 98.2%. Low and high sales volume groups both had precision values of 96.7%. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 95.1% in 2011 to 97.9% in 2012.

Actions Include more distributors to improve panel coverage

-2.5 -4.1 -3.0 -4.8 -4.7

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

93.2 93.8 91.9 94.4 97.2

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

27 acts 2013

Egypt Retail Validation Study 2012

Participation Number of companies 46 The 2012 PIE validation study was attended

by 46 companies, 16 more than in 2011. The participants supplied 604 product forms for evaluation, none of which showed any extreme deviation. The validated market share of the participating manufacturers equaled 24% in terms of units.

Validated market share 24% Number of R-Values 604 Number of extreme values 0

Over/Underestimation

The overall underestimation improved by 2.1 percentage points, from 4.0% in 2011 to 1.9% in 2012. Low sales vol-ume products were underesti-mated by 1.8%, medium by 2.2%, and the high sales vol-ume class showed a 1.7% un-derestimation.

Precision

The overall precision index showed again a perfect result of 100% in 2012. This excellent result is also distributed over all sales volume groups. Look-ing only at forms validated in both years, 2011 and 2012, the precision index remained at 100%.

Actions No action required from the statistical point of view

-1.8 -2.6 -2.8 -4.0 -1.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

98.6 100.0 99.9 100.0 100.0

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

28 acts 2013

Estonia Retail Validation Study 2012

Participation Number of companies 17 The 2012 ESTPI validation study was at-

tended by 17 companies, eleven more than in 2011. The participants supplied 220 prod-uct forms for evaluation, of which 3 (1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers equaled 15% in terms of units.

Validated market share 15% Number of R-Values 220 Number of extreme values 3

Over/Underestimation

The overall bias improved from a 2.0% underestimation in 2011 to a small 0.9% overes-timation in 2012. Low sales volume products were under-estimated by 1.4%, medium by 1.3%, and the high sales vol-ume group showed a 2.3% overestimation.

Precision

The overall precision index im-proved slightly, from 88.1% in 2011 to 88.4% in 2012. The medium and high sales volume groups surpassed this score at 92.0% and 89.1%, respec-tively. Low sales volume prod-ucts had a precision value of 79.1%. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 92.5% in 2011 to 94.4% in 2012.

Actions Review projection level for OTC data

-8.6

-15.8 -15.3

-2.0

0.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

84.6 85.2 80.7 88.1 88.4

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

29 acts 2013

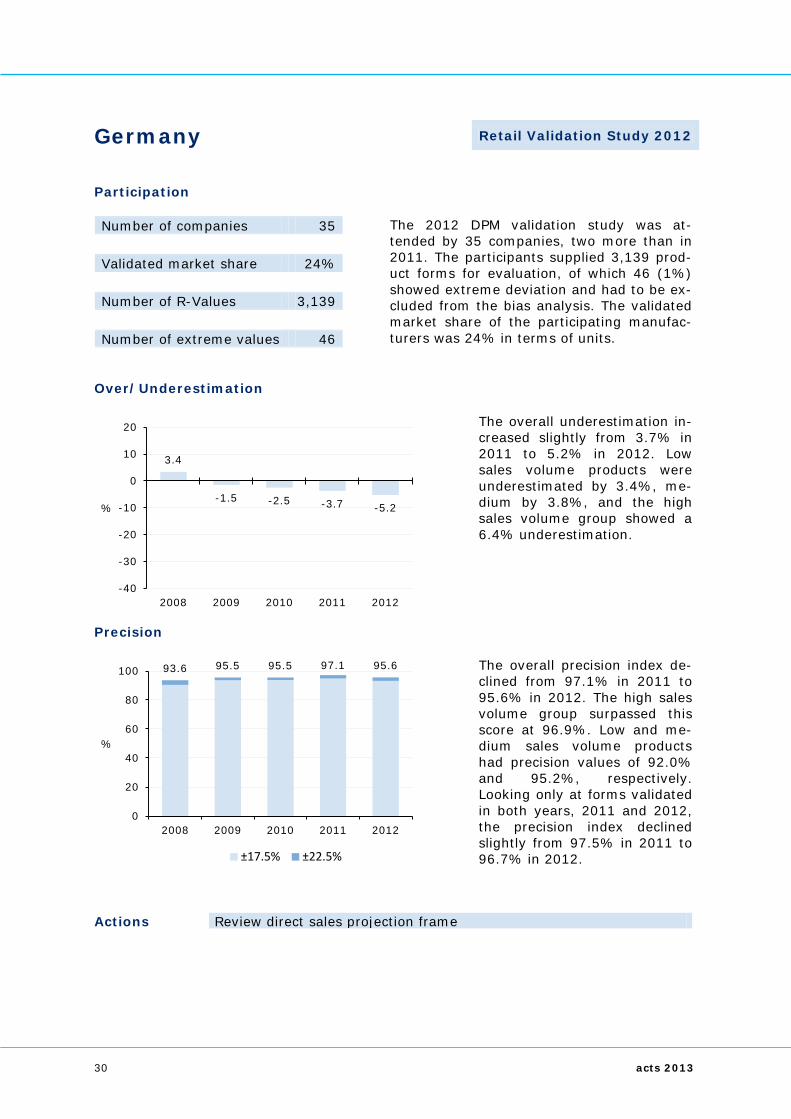

Germany Retail Validation Study 2012

Participation Number of companies 35 The 2012 DPM validation study was at-

tended by 35 companies, two more than in 2011. The participants supplied 3,139 prod-uct forms for evaluation, of which 46 (1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 24% in terms of units.

Validated market share 24% Number of R-Values 3,139 Number of extreme values 46

Over/Underestimation

The overall underestimation in-creased slightly from 3.7% in 2011 to 5.2% in 2012. Low sales volume products were underestimated by 3.4%, me-dium by 3.8%, and the high sales volume group showed a 6.4% underestimation.

Precision

The overall precision index de-clined from 97.1% in 2011 to 95.6% in 2012. The high sales volume group surpassed this score at 96.9%. Low and me-dium sales volume products had precision values of 92.0% and 95.2%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 97.5% in 2011 to 96.7% in 2012.

Actions Review direct sales projection frame

3.4

-1.5 -2.5 -3.7 -5.2

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

93.6 95.5 95.5 97.1 95.6

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

30 acts 2013

Greece Retail Validation Study 2012

Participation Number of companies 85 The 2012 GPI validation study was attended

by 85 companies, 17 more than in 2011. The participants supplied 1,074 product forms for evaluation, of which 27 (3%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 69% in terms of units.

Validated market share 69% Number of R-Values 1,074 Number of extreme values 27

Over/Underestimation

The overall bias analysis re-vealed a 2.6% underestimation in 2012. Low sales volume products were underestimated by 3.1%, medium by 2.7%, and the high sales volume group revealed a 2.5% under-estimation.

Precision

The overall precision index im-proved further, from 85.5% in 2011 to 89.2% in 2012. The high sales volume group sur-passed this score at 94.6%. Low and medium sales volume products had precision values of 71.9% and 89.0%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 90.1% in 2011 to 89.0% in 2012.

Actions New universe study conducted Enhance sampling method based on universe study outcome

0.0 2.0

-1.4

0.0

-2.6

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

85.2 83.3 82.8 85.5 89.2

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

31 acts 2013

Hong Kong Retail Validation Study 2012

Participation Number of companies 26 Data from 26 companies, ten less than in

2009 when the previous validation study was conducted, was available for the 2012 HKPA validation study. In total, 964 product forms were processed, of which 132 (14%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share equaled 31% in terms of units.

Validated market share 31% Number of R-Values 964 Number of extreme values 132

Over/Underestimation

The overall underestimation showed stability at 11.8% in 2012. Low sales volume prod-ucts were underestimated by 19.8%, medium by 18.0%, and the high sales volume group had a 2.6% underestimation.

Precision

The overall precision index de-clined from 75.2% in 2009 to 73.0% in 2012. The high sales volume group surpassed this score at 80.0%. Low and me-dium sales volume products had precision values of 60.3% and 67.7%, respectively. Looking only at forms validated in both years, 2009 and 2012, the precision index declined marginally from 83.8% in 2009 to 83.7% in 2012.

Actions Review projection level and panel composition

-11.3 -11.9 -11.8

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

74.9 75.2 73.0

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

32 acts 2013

Hungary Retail+Hospital Validation Study 2011

Participation Number of companies 82 The 2012 validation study, combining the

Hungarian retail and hospital audits, was at-tended by 82 companies, eight less than in 2011. The participants supplied 1,703 prod-uct forms for evaluation, of which 19 (1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating companies equaled 76% in terms of units.

Validated market share 76% Number of R-Values 1,703 Number of extreme values 19

Over/Underestimation

The overall underestimation improved from 4.1% in 2011 to 1.7% in 2012. Low sales vol-ume products were underesti-mated by 1.5%, medium by 1.9%, and the high sales vol-ume group showed a 1.7% un-derestimation.

Precision

The overall precision index de-clined slightly, from 98.6% in 2011 to 96.9% in 2012. The high sales volume group sur-passed this score at 97.9%. Low and medium sales volume products had precision values of 94.6% and 96.4%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 98.7% in 2011 to 97.7% in 2012.

Actions No action required from the statistical point of view

-1.0 -1.2 -1.8 -4.1 -1.7

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

99.4 99.4 98.9 98.6 96.9

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

33 acts 2013

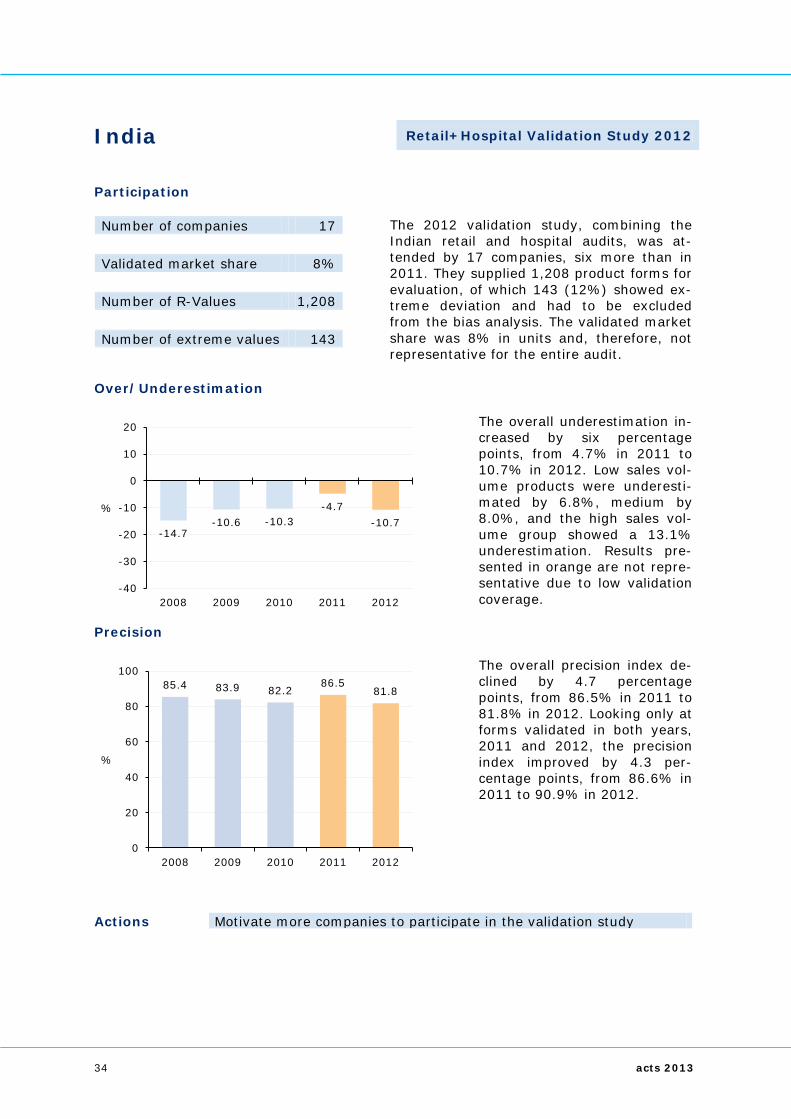

India Retail+Hospital Validation Study 2012

Participation Number of companies 17 The 2012 validation study, combining the

Indian retail and hospital audits, was at-tended by 17 companies, six more than in 2011. They supplied 1,208 product forms for evaluation, of which 143 (12%) showed ex-treme deviation and had to be excluded from the bias analysis. The validated market share was 8% in units and, therefore, not representative for the entire audit.

Validated market share 8% Number of R-Values 1,208 Number of extreme values 143

Over/Underestimation

The overall underestimation in-creased by six percentage points, from 4.7% in 2011 to 10.7% in 2012. Low sales vol-ume products were underesti-mated by 6.8%, medium by 8.0%, and the high sales vol-ume group showed a 13.1% underestimation. Results pre-sented in orange are not repre-sentative due to low validation coverage.

Precision

The overall precision index de-clined by 4.7 percentage points, from 86.5% in 2011 to 81.8% in 2012. Looking only at forms validated in both years, 2011 and 2012, the precision index improved by 4.3 per-centage points, from 86.6% in 2011 to 90.9% in 2012.

Actions Motivate more companies to participate in the validation study

-14.7 -10.6 -10.3

-4.7 -10.7

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

85.4 83.9 82.2 86.5

81.8

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

34 acts 2013

Indonesia Total Market Validation Study 2012

Participation Number of companies 62 Data from 62 companies, sixteen less than

in 2011, was available for the 2012 ITMA validation study. In total, 4,981 product forms were processed, of which 843 (17%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share equaled 43% in terms of units.

Validated market share 43% Number of R-Values 4,981 Number of extreme values 843

Over/Underestimation

The overall bias increased slightly to a 1.2% underesti-mation. Low sales volume products were underestimated by 6.6%, medium by 4.0%, and the high sales volume group showed a slight 0.1% underestimation.

Precision

The overall precision index de-clined to 66.7% in 2012. The low sales volume class sur-passed this score at 71.6%. Medium and high sales volume products had precision results of 64.3% and 66.7%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 73.6% in 2011 to 80.7% in 2012.

Actions Enhance projection methodology Improve data collection and coding quality

-2.2 -1.3 -2.7

0.0

-1.2

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

67.5 70.1 69.5 69.6 66.7

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

35 acts 2013

Ireland Retail Validation Study 2012

Participation Number of companies 12 The 2012 IPI validation study was attended

by 12 companies, eleven less than in 2011. The participants supplied 188 product forms for evaluation, of which 6 (3%) showed ex-treme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was only 6% in terms of units and, therefore, not representative for the entire audit.

Validated market share 6% Number of R-Values 188 Number of extreme values 6

Over/Underestimation

The overall bias turned from 1.2% underestimation in 2011 to 1.0% overestimation in 2012. Low sales volume prod-ucts were overestimated by 0.1% and medium by 1.2%. Only few forms were available in the high sales volume class, so these were grouped into the medium class for analysis. Re-sults presented in orange are not representative due to low validated market coverage.

Precision

The overall precision index de-clined from 95.4% in 2011 to 91.4% in 2012. The medium sales volume group surpassed this score at 95.8%. Low sales volume products had a preci-sion result of 83.8%. Looking only at forms validated in both years, 2011 and 2012, the pre-cision index remained at a perfect 100%.

Actions Motivate more companies to participate in the validation study

-1.5 -0.6 -1.2

1.0

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

97.3 98.2 95.4 91.4

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

36 acts 2013

Italy Retail Validation Study 2012

Participation Number of companies 29 The 2012 IMF validation study was attended

by 29 companies, one more than in 2011. The participants supplied 1,081 product forms for evaluation, of which ten (<1%) showed extreme deviation and had to be ex-cluded from the bias calculation. The vali-dated market share of the participating manufacturers was 32% in terms of units.

Validated market share 32% Number of R-Values 1,081 Number of extreme values 10

Over/Underestimation

The overall underestimation in-creased slightly by 0.3 per-centage points, from 2.2% in 2011 to 2.5% in 2012. Low sales volume products were underestimated by 2.4%, me-dium by 3.7%, and the high sales volume class revealed a 1.9% underestimation.

Precision

The overall precision index de-clined from 98.7% in 2011 to 96.8% in 2012. The high sales volume group surpassed this score at 98.0%. Low and me-dium sales volume products had precision results of 94.4% and 96.1%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 99.1% in 2011 to 98.3% in 2012.

Actions No action required from the statistical point of view

-2.7 -2.3 -1.9 -2.2 -2.5

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

97.3 96.7 97.3 98.7 96.8

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

37 acts 2013

Japan Retail+Hospital Validation Study 2012

Participation Number of companies 53 The 2012 JPM validation study was attended

by 53 companies, two more than in 2011. The participants supplied 3,056 product forms for evaluation, of which six (<1%) showed extreme deviation and were ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 71% in terms of units.

Validated market share 71% Number of R-Values 3,056 Number of extreme values 6

Over/Underestimation

The overall bias improved to +0.1% in 2012. Low sales vol-ume products were overesti-mated by 0.5%, medium by 1.2%, and the high sales vol-ume group showed a 0.1% overestimation.

Precision

The overall precision index showed again a very good re-sult in 2012, ending at 99.7%. The high sales volume group surpassed this score at a per-fect 100%. Low and medium sales volume products had pre-cision indices of 99.0% and 99.6%, respectively. Measure-ment at the tighter ±17.5% interval revealed a precision result of 99.5%.

Actions No action required from the statistical point of view

0.2 0.0 0.1 0.3 0.1

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

99.7 99.7 99.8 99.7 99.7

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

38 acts 2013

Jordan Retail Validation Study 2012

Participation Number of companies 10 The 2012 JPI validation study was attended

by 10 companies, five less than in 2011. The participants supplied 349 product forms for evaluation, of which 7 (2%) showed ex-treme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 17% in terms of units.

Validated market share 17% Number of R-Values 349 Number of extreme values 7

Over/Underestimation

The overall underestimation improved further, from 16.6% in 2011 to 10.1% in 2012. Low sales volume products were underestimated by 4%, me-dium by 6.8%, and the high sales volume group showed a 13.7% underestimation.

Precision

The overall precision index im-proved by 6.3 percentage points, from 69.1% in 2011 to 75.4% in 2012. The medium sales volume group surpassed this score at 77.3%. Low and high sales volume products had precision values of 83.2% and 72.0%, respectively. Looking only at forms validated in both years, 2011 and 2012, the pre-cision index declined slightly from 76.9% in 2011 to 76.3% in 2012.

Actions Motivate more companies to participate in the validation study

-32.1 -29.5

-21.7 -16.6

-10.1

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

69.4 62.7 62.9

69.1 75.4

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

39 acts 2013

Korea Retail Validation Study 2012

Participation Number of companies 16 The 2012 KPA validation study was attended

by 16 companies, three less than in 2011. The participants supplied 696 product forms for evaluation, of which 31 (4%) showed extreme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 12% in terms of units.

Validated market share 12% Number of R-Values 696 Number of extreme values 31

Over/Underestimation

The overall underestimation in-creased from 11.0% in 2011 to 15.9% in 2012. Low sales vol-ume products were underesti-mated by 18.9%, medium by 14.3%, and high sales volume products showed a 16.7% un-derestimation.

Precision

The overall precision index de-clined from 88.0% in 2011 to 82.9% in 2012. The high sales volume group surpassed this score at 91.3%. Low and me-dium sales volume products had precision values of 64.4% and 78.1%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined from 88.8% in 2011 to 79.1% in 2012.

Actions Review projection level and panel composition Improve data collection and coding quality

-17.1 -17.7 -15.5 -11.0

-15.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

82.2 83.7 85.1 88.0 82.9

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

40 acts 2013

Kuwait Retail Validation Study 2012

Participation Number of companies 26 The 2012 KWPI validation study was at-

tended by 26 companies, three more than in 2011. The participants supplied 520 product forms for evaluation, none of which showed any extreme deviation. The validated market share of the participating manufacturers was 46% in terms of units.

Validated market share 46% Number of R-Values 520 Number of extreme values 0

Over/Underestimation

The overall underestimation of 0.5% in 2011 remained at the same level in 2012. Low sales volume products were under-estimated by 1.1%, medium by 0.7%, and the high sales vol-ume class revealed a 0.3% un-derestimation.

Precision

The overall precision index im-proved from 98.7% in 2011 to 99.6% in 2012. The high sales volume group reached a per-fect 100%. Low and medium sales volume products had pre-cision scores of 98.9% and 99.4%, respectively. Looking only at forms validated in both years, 2011 and 2012, the pre-cision index declined slightly from 99.8% in 2011 to 99.5% in 2012.

Actions No action required from the statistical point of view

-0.9 -1.0

0.5

-0.5 -0.5

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

99.2 95.9 99.8 98.7 99.6

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

41 acts 2013

Latvia Retail Validation Study 2012

Participation Number of companies 13 The 2012 LVPI validation study was at-

tended by 13 companies, four less than in 2011. The participants supplied 303 product forms for evaluation, of which 24 (8%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers equaled 15% in terms of units.

Validated market share 15% Number of R-Values 303 Number of extreme values 24

Over/Underestimation

The overall bias increased from a 6.6% underestimation in 2011 to a 10.3% overestima-tion in 2012. Low sales volume products were overestimated by 8.7%, medium by 9.2%, and the high sales volume group showed an 11.2% over-estimation.

Precision

The overall precision index de-clined further, from 85.0% in 2011 to 72.4% in 2012. The high sales volume group sur-passed this score at 77.4%. Low and medium sales volume products had precision values of 59.1% and 70.8%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index dropped from 91.2% in 2011 to 61.7% in 2012.

Actions Pharmacy panel increased Adjust projection level

3.2 3.0 1.4

-6.6

10.3

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

96.1 94.7 96.3 85.0

72.4

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

42 acts 2013

Lebanon Retail Validation Study 2012

Participation Number of companies 8 The 2012 LPI validation study was attended

by 8 companies, 16 less than in 2011. The participants supplied 131 product forms for evaluation, of which 19 (15%) showed ex-treme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was only 6% in terms of units and, therefore, not representative for the entire audit.

Validated market share 6% Number of R-Values 131 Number of extreme values 19

Over/Underestimation

The overall underestimation improved from 13.1% in 2011 to 0.2% in 2012. Low sales vo-lume products were underesti-mated by 3.9% and medium were overestimated by 0.3%. As there were only few forms available in the high sales vol-ume class, these were grouped into the medium class for anal-ysis. Results presented in or-ange are not representative due to low validation coverage.

Precision

The overall precision index de-teriorated further, from 79.3% in 2011 to 66.5% in 2012. The medium sales volume group surpassed this score at 67.9%. Low sales volume products had a precision value of 64.1%. Looking only at forms validated in both years, 2011 and 2012, the precision index dropped from 77.8% in 2011 to 66.7% in 2012.

Actions Motivate more companies to participate in the validation study

-15.7 -13.1

-0.2

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

93.1

79.3

66.5

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

43 acts 2013

Lithuania Retail Validation Study 2012

Participation Number of companies 12 The 2012 LTPI validation study was attended

by 12 companies, nine less than in 2011. The participants supplied 203 product forms for evaluation, none of which showed any extreme deviation. The validated market share of the participating manufacturers was 13% in terms of units.

Validated market share 13% Number of R-Values 203 Number of extreme values 0

Over/Underestimation

The overall overestimation in-creased slightly, from 1.3% in 2011 to 1.7% in 2012. Low sales volume products were underestimated by 1.7%, me-dium had no bias at all, and the high sales volume group showed a 2.9% overestimation.

Precision

The overall precision index im-proved from 97.4% in 2011 to 99.6% in 2012. The medium and high sales volume groups both surpassed this score at a perfect 100%. Low sales vol-ume products had a precision value of 97.5%. Looking only at forms validated in 2011 and 2012, the precision index was 100% in both years.

Actions Slightly adjust projection level

0.5 2.2 1.8 1.3 1.7

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

98.3 98.6 98.8 97.4 99.6

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

44 acts 2013

Malaysia Retail Validation Study 2012

Participation Number of companies 64 Data from 64 companies, one more than in

2011, was available for the 2012 MPA vali-dation study. In total, 2,795 product forms were processed, of which 245 (9%) showed extreme deviation and had to be excluded from the bias analysis. The validated market share equaled 32% in terms of units.

Validated market share 32% Number of R-Values 2,795 Number of extreme values 245

Over/Underestimation

The overall underestimation improved by 1.5 percentage points, from 12.4% in 2011 to 10.9% in 2012. Low sales vol-ume products were underesti-mated by 12.2%, medium by 12.9%, and the high sales vol-ume group showed a 9.3% un-derestimation.

Precision

The overall precision index showed stability at 81.1% in 2012. The high sales volume group surpassed this score at 85.3%. Low and medium sales volume products had precision values of 72.7% and 78.4%, respectively. Looking only at forms validated in both years, 2011 and 2012, the precision index declined slightly from 83.8% in 2011 to 82.2% in 2012.

Actions Review projection level and panel composition

-15.9 -15.0 -16.4 -12.4 -10.9

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

80.2 80.6 80.1 81.2 81.1

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

45 acts 2013

Mexico Retail Validation Study 2012

Participation Number of companies 25 The 2012 PMM validation study was at-

tended by 25 companies, twelve less than in 2011. The participants supplied 1,619 prod-uct forms for evaluation, of which 38 (2%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 35% in terms of units.

Validated market share 35% Number of R-Values 1,619 Number of extreme values 38

Over/Underestimation

The overall overestimation im-proved slightly from 1.6% in 2011 to 1.4% in 2012. Low sales volume products were underestimated by 0.1%, whereas the medium and high sales volume classes were overestimated by 0.6% and 2.0%, respectively.

Precision

The overall precision index im-proved slightly, from 90.4% in 2011 to 90.7% in 2012. The high sales volume group sur-passed this score at 93.9%. Low and medium sales volume products had precision results of 82.9% and 89.4%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved slightly from 90.8% in 2011 to 91.3% in 2012.

Actions Update universe and sample Conduct distribution channel survey

0.0

-0.8 -0.8

1.6 1.4

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

89.9 92.1 89.5 90.4 90.7

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

46 acts 2013

Morocco Retail Validation Study 2012

Participation Number of companies 95 The 2012 LMPM validation study was at-

tended by 95 companies, 60 less than in 2011. The participants supplied 958 direct and indirect product forms for evaluation, of which only one (<1%) showed extreme de-viation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 59% in terms of units.

Validated market share 59% Number of R-Values 958 Number of extreme values 1

Over/Underestimation

The overall underestimation improved from 2.2% in 2011 to 0.8% in 2012. Low and me-dium sales volume products were both underestimated by 0.7% and the high sales vol-ume class showed a 0.9% un-derestimation.

Precision

The overall precision index im-proved from 99.2% in 2011 to 99.6% in 2012. The high sales volume group surpassed this score at a perfect 100%. Low and medium sales volume products had precision results of 99.4% and 99.1%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved from 98.9% in 2011 to 99.9% in 2012.

Actions No action required from the statistical point of view

-5.8 -1.4 -0.8 -2.2 -0.8

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

92.2 95.2 96.9 99.2 99.6

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

47 acts 2013

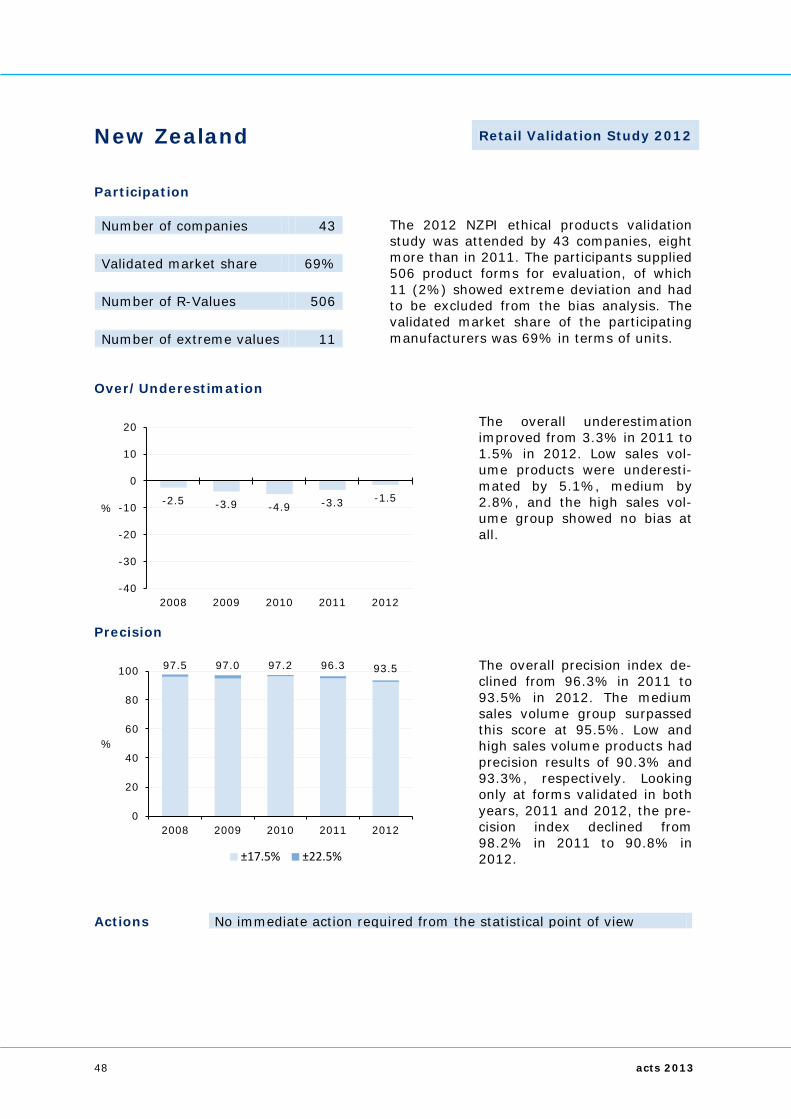

New Zealand Retail Validation Study 2012

Participation Number of companies 43 The 2012 NZPI ethical products validation

study was attended by 43 companies, eight more than in 2011. The participants supplied 506 product forms for evaluation, of which 11 (2%) showed extreme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 69% in terms of units.

Validated market share 69% Number of R-Values 506 Number of extreme values 11

Over/Underestimation

The overall underestimation improved from 3.3% in 2011 to 1.5% in 2012. Low sales vol-ume products were underesti-mated by 5.1%, medium by 2.8%, and the high sales vol-ume group showed no bias at all.

Precision

The overall precision index de-clined from 96.3% in 2011 to 93.5% in 2012. The medium sales volume group surpassed this score at 95.5%. Low and high sales volume products had precision results of 90.3% and 93.3%, respectively. Looking only at forms validated in both years, 2011 and 2012, the pre-cision index declined from 98.2% in 2011 to 90.8% in 2012.

Actions No immediate action required from the statistical point of view

-2.5 -3.9 -4.9 -3.3 -1.5

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

97.5 97.0 97.2 96.3 93.5

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

48 acts 2013

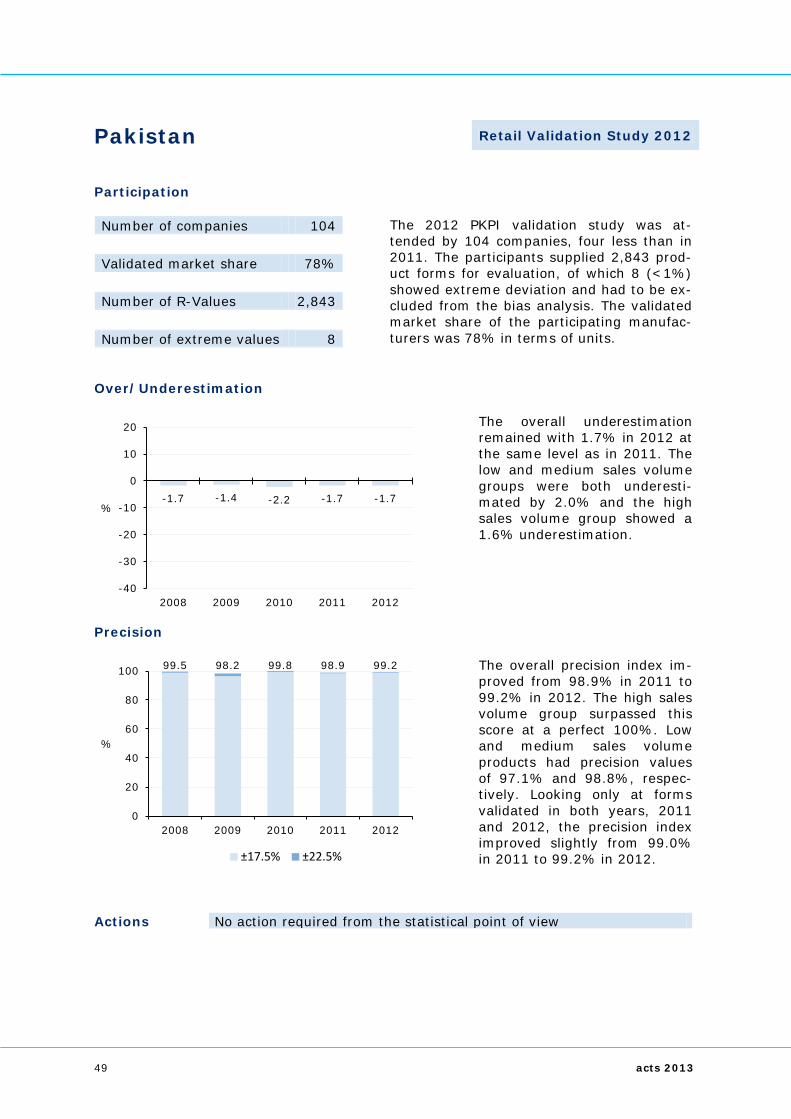

Pakistan Retail Validation Study 2012

Participation Number of companies 104 The 2012 PKPI validation study was at-

tended by 104 companies, four less than in 2011. The participants supplied 2,843 prod-uct forms for evaluation, of which 8 (<1%) showed extreme deviation and had to be ex-cluded from the bias analysis. The validated market share of the participating manufac-turers was 78% in terms of units.

Validated market share 78% Number of R-Values 2,843 Number of extreme values 8

Over/Underestimation

The overall underestimation remained with 1.7% in 2012 at the same level as in 2011. The low and medium sales volume groups were both underesti-mated by 2.0% and the high sales volume group showed a 1.6% underestimation.

Precision

The overall precision index im-proved from 98.9% in 2011 to 99.2% in 2012. The high sales volume group surpassed this score at a perfect 100%. Low and medium sales volume products had precision values of 97.1% and 98.8%, respec-tively. Looking only at forms validated in both years, 2011 and 2012, the precision index improved slightly from 99.0% in 2011 to 99.2% in 2012.

Actions No action required from the statistical point of view

-1.7 -1.4 -2.2 -1.7 -1.7

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

99.5 98.2 99.8 98.9 99.2

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

49 acts 2013

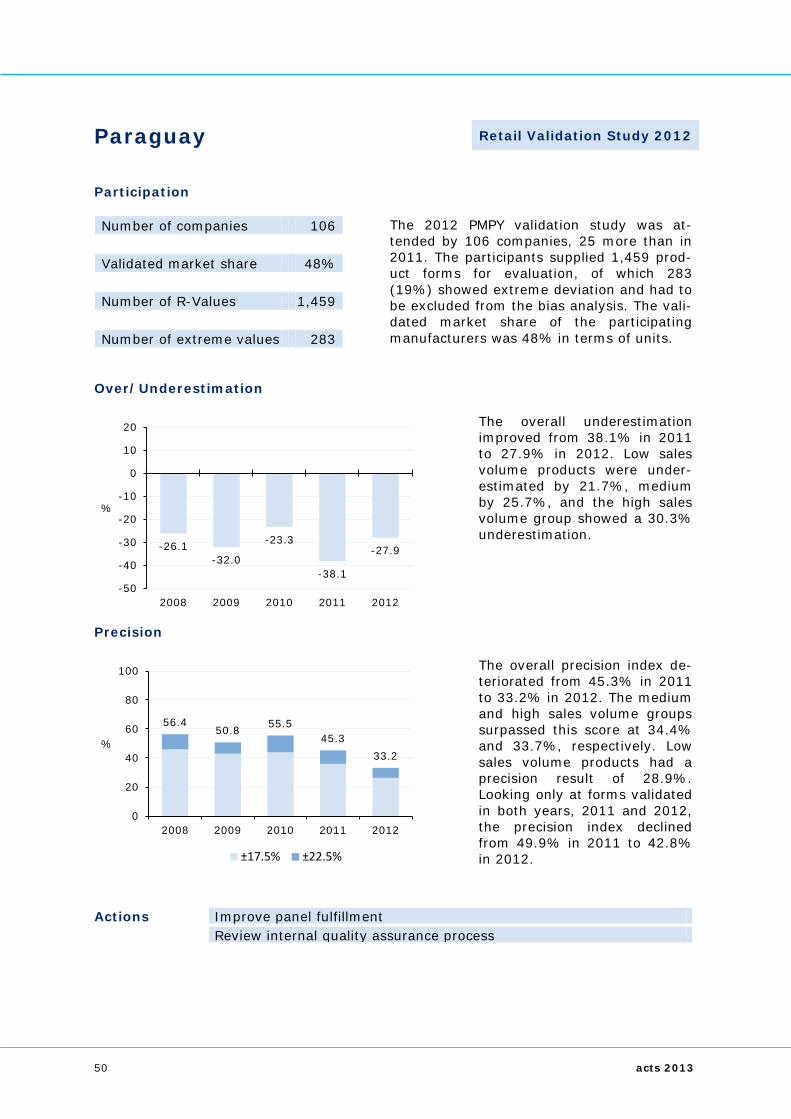

Paraguay Retail Validation Study 2012

Participation Number of companies 106 The 2012 PMPY validation study was at-

tended by 106 companies, 25 more than in 2011. The participants supplied 1,459 prod-uct forms for evaluation, of which 283 (19%) showed extreme deviation and had to be excluded from the bias analysis. The vali-dated market share of the participating manufacturers was 48% in terms of units.

Validated market share 48% Number of R-Values 1,459 Number of extreme values 283

Over/Underestimation

The overall underestimation improved from 38.1% in 2011 to 27.9% in 2012. Low sales volume products were under-estimated by 21.7%, medium by 25.7%, and the high sales volume group showed a 30.3% underestimation.

Precision

The overall precision index de-teriorated from 45.3% in 2011 to 33.2% in 2012. The medium and high sales volume groups surpassed this score at 34.4% and 33.7%, respectively. Low sales volume products had a precision result of 28.9%. Looking only at forms validated in both years, 2011 and 2012, the precision index declined from 49.9% in 2011 to 42.8% in 2012.

Actions Improve panel fulfillment Review internal quality assurance process

-26.1 -32.0

-23.3

-38.1

-27.9

-50

-40

-30

-20

-10

0

10

20

2008 2009 2010 2011 2012

%

56.4 50.8 55.5

45.3 33.2

0

20

40

60

80

100

2008 2009 2010 2011 2012

%

±17.5% ±22.5%

50 acts 2013

Peru Retail Validation Study 2012

Participation Number of companies 14 The 2012 PMP validation study was attended

by 14 companies, 14 less than in 2011. The participants supplied 710 product forms for evaluation, of which 5 (<1%) showed ex-treme deviation and had to be excluded from the bias analysis. The validated market share of the participating manufacturers was 23% in terms of units.

Validated market share 23% Number of R-Values 710 Number of extreme values 5

Over/Underestimation

The overall underestimation in-creased from 9.2% in 2011 to 10.9% in 2012. Low sales vol-ume products were underesti-mated by 10.2%, medium by 9.4%, and the high sales vol-ume group showed an 11.9% underestimation.

Precision