~ issues in the delivery of ~ commonwealthsocial support...

TRANSCRIPT

CommonwealthSocial SupportProgramstoFarmFamilies

~ Issues in the del ivery of ~

AuthorsJayne Garnaut

Judith Robinson

Milly Lubulwa

ABARE RESEARCH REPORT 97.7

© Commonwealth of Australia 1997

This work is copyright. The Copyright Act 1968 permits fair dealing forstudy, research, news reporting, criticism or review. Selected passages,tables or diagrams may be reproduced for such purposes providedacknowledgment of the source is included. Major extracts or the entiredocument may not be reproduced by any process without the writtenpermission of the Executive Director, ABARE.

ISSN 1037-8286ISBN 0 642 26612 3

Garnaut, J., Robinson, J. and Lubulwa, M. 1997, Issues in the Delivery ofCommonwealth Social Support Programs to Farm Families, ABAREResearch Report 97.7, Canberra.

Australian Bureau of Agricultural and Resource EconomicsGPO Box 1563 Canberra 2601

Telephone +61 2 6272 2000 Facsimile +61 2 6272 2001Internet www.abare.gov.au

ABARE is a professionally independent government economic researchagency.

ABARE projects 1256, 1326

Foreword

Low commodity prices in the early 1990s, combined with widespreaddrought in 1993-94, continued the long term downward trend in the net valueof farm production and income in Australia of the past four decades. Thisaccentuated the need of farm families for fair and equitable access to socialsupport programs provided by the Commonwealth government.

Anecdotal evidence has suggested that farm families have a poor level ofunderstanding of Commonwealth social support programs, indicating a needfor research into farmers’ knowledge and use of these programs. TheCommonwealth government commissioned ABARE to conduct a two stagestudy into the social and financial circumstances of farm families and theirinvolvement (or lack of involvement) with government social supportprograms. A special survey provided information on the demography andfinancial situation of farm families, along with what they know aboutexisting Commonwealth social support and related programs and how theyuse such programs. Statistical analysis was used to predict the likely outcomefor certain groups of farm families if they had applied for governmentsupport. In this report, living standards are examined through qualitative andquantitative analysis.

The second stage involved designing in-depth interviews to draw out issuesin the design and delivery of Commonwealth social support programs tofarm families. These interviews with twelve farm families chosen from thesurvey sample provided insights into issues highlighted by the telephonesurvey. They allowed farm families’ knowledge of, use of, and access toCommonwealth support programs to be examined in a manner not possiblein a large scale survey.

The analysis presented will enable more rigorous examination of issues offarm family welfare and government policy options.

STEPHEN C. BEARE

Acting Executive Director

October 1997

iii

Acknowledgments

The project was undertaken for the Rural Division of the Department ofPrimary Industries and Energy, which acted as secretariat for a SteeringCommittee which included Fiona Smart (Department of Social Security);Eileen Newmarch, Joe Caldwell and Rickman Lilienthal (Department ofEmployment, Education, Training and Youth Affairs); Onko Kingma andBernard Scott (Rural Division of the Department of Primary Industries andEnergy); Matthew Taylor and Tim Andrie (Department of Finance);Michelle Withers (Attorney-General’s Department); and Bill Curran, VinceO’Donnell and Jayne Garnaut (ABARE).

Nationally, over 3500 farm householders cooperated with ABARE’s teamof interviewers to provide the telephone survey information contained in thisreport. The twelve farm families interviewed at their farms were generouswith their time and information. The case studies would not have beenpossible without their cooperation and assistance. Information for preparingthe in-depth interviews was sought from counsellors in rural areas who workwith farmers facing financial difficulties: Clive Sefton (Rural Counsellor,Castlereagh Advisory Centre, Gilgandra), Kathy Sims (Rural Counsellor,Macquarie Rural Advisory Service, Dubbo) and Noel Parkes (Director,Lifeline, Darling Downs and South West Queensland) advised on the currentneeds of farmers from their perspective as counsellors.

The telephone survey questionnaire was developed with advice frommembers of the Steering Committee. A large number of ABARE officersalso made important contributions to the project, including Steve Beare, KenColbert, Catherine Cook-Wass, Caroline Corder, Bill Curran, CarolynDoyle, Jane Gooday, Phil Kokic, Ray Lindsay, Theresa Muller, VinceO’Donnell, Bhamathy Parameswaran, Paul Phillips, Craig Pollard, JudithRobinson and Vern Rudwick.

The authors are also grateful to Ian Williams (Australian Valuation Office)for providing aggregate data on the valuations of farm properties.

iv ABARE research report 97.7

Contents

Summary 1

1 Introduction 10

2 Government programs during the survey period 14Programs 14Assets and income assessment 18

3 Economic conditions in the survey period 21

4 Demographic and locational profile 24Number of farms and household size 24Age and gender distribution 27Employment and education status 28Rural, remote and metropolitan locations 30

5 Assets and income profiles and assets valuation 32Household assets and income 32Modified household assets and income 34Assets valuation 34

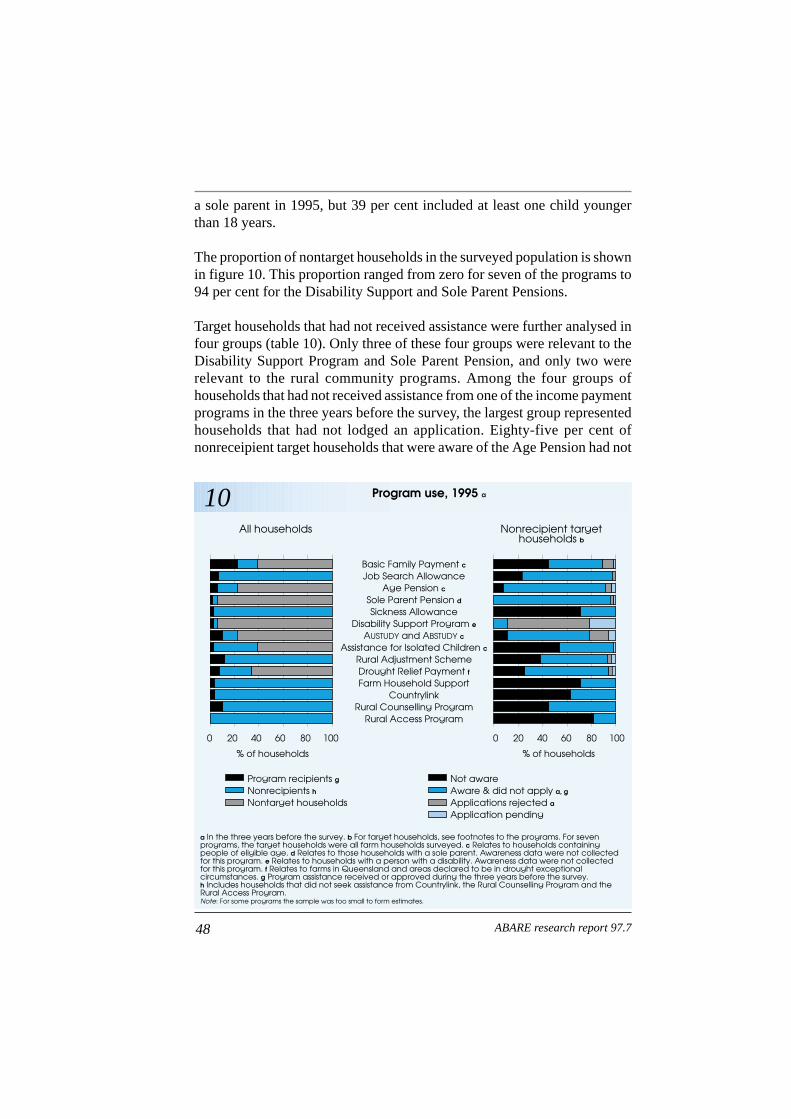

6 Awareness and use of programs 38Target households 38Awareness of programs 39Awareness of hardship tests 39Awareness and location 41Sources of information about programs 45Use of programs 46

7 Reasons for nonapplication 51

8 Reasons for rejection of application 53

vSocial support programs

9 Potential eligibility 55Predictive analysis 57Location of selected household groups 59Potential eligibility – another approach 60

10 Quality of service 62Ratings 62In-depth interviews 63

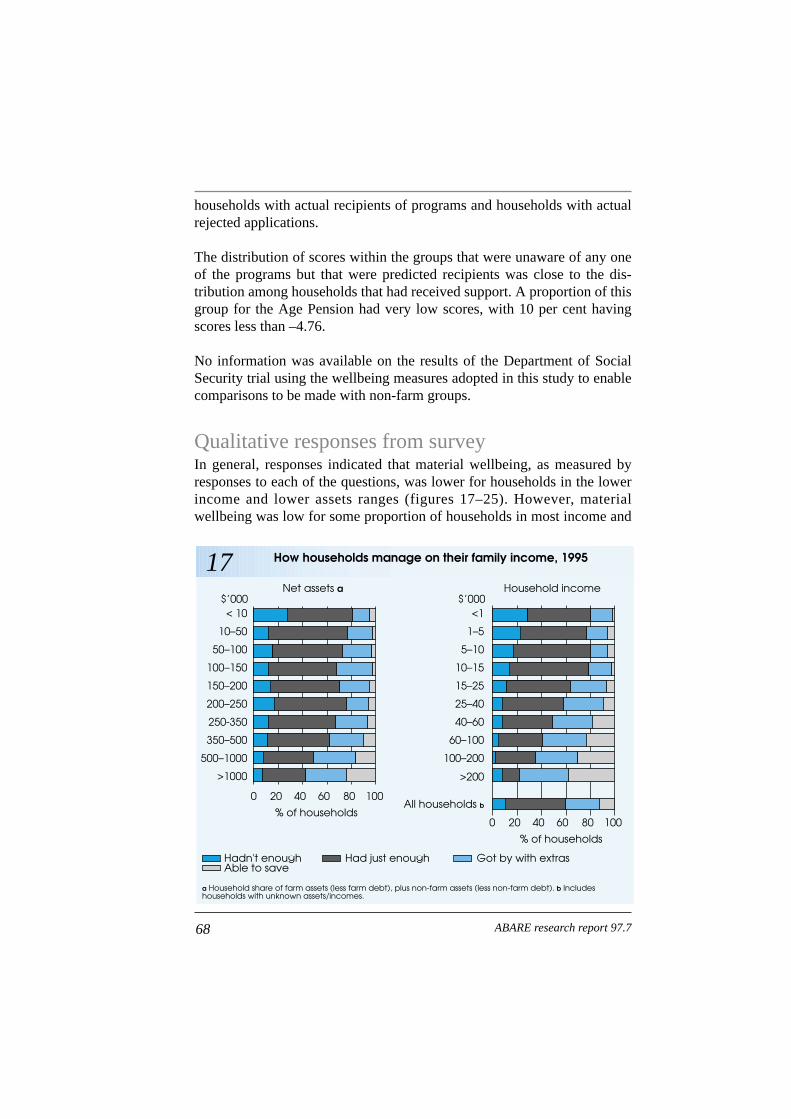

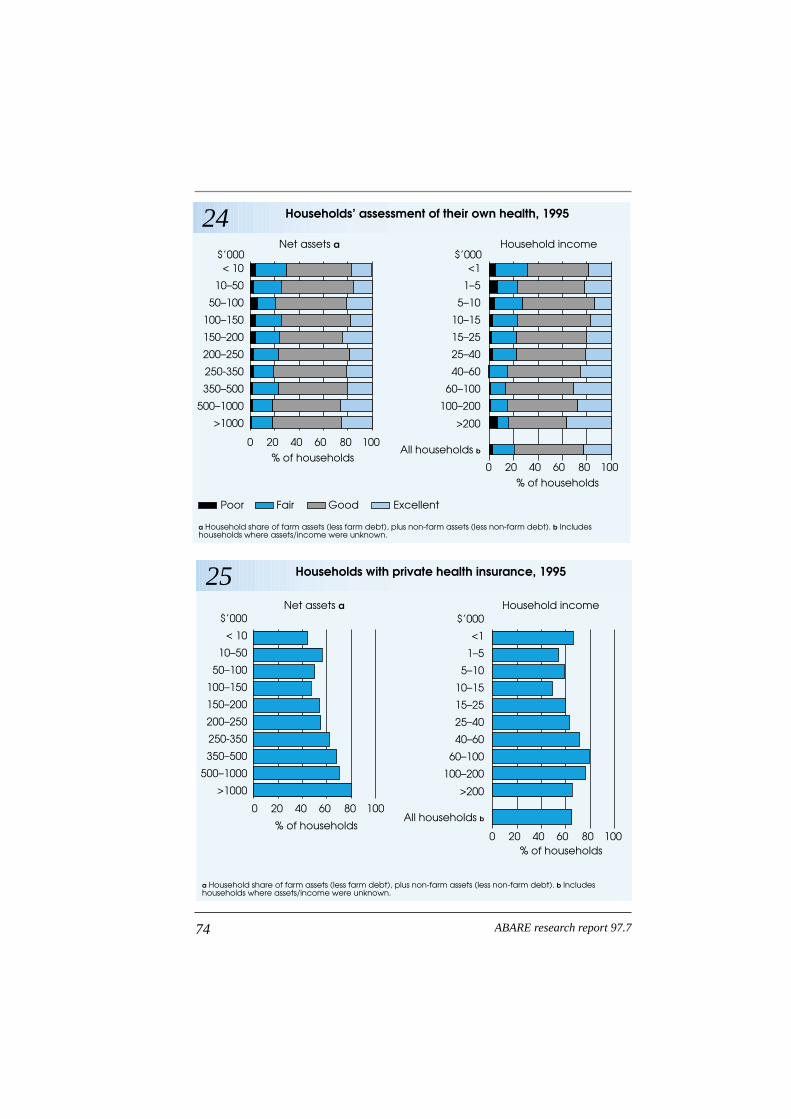

11 Material wellbeing and health 64Wellbeing scale 64Wellbeing, assets and income 65Wellbeing of selected household groups 66Qualitative responses from survey 68Health 73In-depth interviews 75

12 Young people and education 76

13 Major findings and discussion 81Awareness of programs 81Take-up and rejection rates 82Nonapplicants who were potentially eligible 83Householders likely to need support 85Assets testing 86Financial management 88Knowledge or understanding of programs 88Service delivery 90Location 91Education participation and achievement 92Utility of the prediction model and the wellbeing scale 92

14 Conclusion 94

AppendixesA Terms of reference 96B Survey method 98C Eligibility for program assistance 115

vi ABARE research report 97.7

References 119

Boxes1 Modified household assets and income for these programs 342 Characteristics of target households 383 Broad questions arising from telephone survey 554 Propositions for case studies analysis 555 Selected household groups for in-depth interviews 56

Figures1 Index of real prices received by far, Australia 223 Age and gender distribution of people in farm households,

1995 274 Households, by household assets net of debt, 1995 325 Households, by household income, 1993-94 336 Households, by modified household assets and income

ranges, 1994-95 357 Comparative total farm valuations, New South Wales,

1994-95 368 Comparative farm house and curtilage valuations,

New South Wales, 1994-95 369 Sources of information about programs, 1995 4610 Program use, 1995 4811 Reasons for nonapplication, 1995 5112 Reasons for rejection, 1995 5313 Rural and remote locations of households in selected

groups, 1995 5914 Quality of service, 1995 6215 Distribution of wellbeing scores of household, by modified

household assets and income ranges, 1995 6516 Distribution of wellbeing scores of households in selected

groups, 1995 6717 How households manage on their family income, 1995 6818 Households’ concern about making ends meet, 1995 6919 Households’ perceptions of level of prosperity, 1995 70

viiSocial support programs

20 Householders who owned or part owned a dwelling off-farm, 1995 71

21 Households’ ability to obtain $5000 within a week for something important, 1995 71

22 Source of funds for households that could obtain $5000, 1995 72

23 Households cutting back on expenditure, 1995 7324 Households’ assessment of their own health, 1995 7425 Households with private health insurance, 1995 7426 Highest level of education achieved, 1995 7627 Reasons for discontinuing education, 1995 7728 AUSTUDY recipients among full time students, 1995 7729 Households with a child at boarding school during the

previous two years 7830 Households that were behind with boarding school fees

during the previous two years 7931 Distance between household and school, 1995 79B1–4 Telephone survey questionnaire 99B5 Regression tree analysis for Age Pension payments 110

MapsA Statistical local areas according to rural and remote

location 30B Awareness of Basic Family Payment, by statistical

division, 1995 42C Awareness of Job Search Allowance, by statistical

ivision, 1995 42D Awareness of Age Pension, by statistical division, 1995 43E Awareness of AUSTUDY/ABSTUDY, by statistical division,

1995 43F Awareness of Rural Adjustment Scheme, by statistical

division, 1995 44G Awareness of Drought Relief Payment, by statistical

division, 1995 44

viii ABARE research report 97.7

Tables1 Maximum assets and income allowed for typical

households 192 Number of farms and household size 243 Age and gender distribution, by state and Northern Territory,

1995 254 Employment and full time student status of adults, 1995 285 Employment and full time student status of young people,

1995 296 Rural and remote location of households, 1995 317 Comparison of farm and Australian household income

distribution 338 Awareness of programs, 1995 409 Awareness of hardship tests for the Age Pension in

selected household groups, 1995 4110 Target households that did not receive assistance in the

three years before the survey 4911 Selected groups as a percentage of target households 5812 Potential eligibility of nonapplicant households for the

Assistance for Isolated Children Scheme, 1995 80B1 Sample size, by program 105B2 Sample size, by assets and income range 106

ixSocial support programs

Glossary of financial terms

Assessable assets (as used by Commonwealth programs at the time ofthe survey)Assets used to determine eligibility under the particular program provisions.The household unit whose assets are assessed varies between programs asdo the asset components. The assessable value of a home and surroundingdomestic land on a farm often differs from the market value. Some programsassess farm assets as a percentage of their value.

Assessable income (as used by Commonwealth programs)Income used to determine eligibility under the particular programprovisions. The household unit whose income is assessed varies betweenprograms. Adjustments or allowances can be made, for example, accordingto the age, number, partner status and student status of household members.

Farm capital valuationValue of the farm (on a walk-in, walk-out basis) — including the value ofland, buildings, livestock, plant and machinery, grain and wool on hand, andso on — at the time of collection (March–May 1995). The value of privatelyleased land is not included.

Farm debtTotal farm debt (not including non-farm debt) at the time of collection(March–May 1995).

Farm liquid assetsValue of liquid assets owned by the farm business — including interestbearing deposits, shares, bank deposits, debentures, bonds, income equal-isation deposits, and so on — at the time of collection (March–May 1995).

Household net assetsTotal combined on-farm and off-farm assets net of debt of all familymembers, including minors, in the household at the time of data collection(March–May 1995).

x ABARE research report 97.7

Household incomeTotal combined on-farm and off-farm income of all household members(including minors), excluding government sources for the 1994-95 financialyear.

Household non-farm debtHousehold’s total non-farm debt at the time of collection (March–May1995).

Household non-farm liquid assetsPresent value of liquid assets (which are not part of the farm business) ownedby members of the household, including interest bearing deposits, shares,bank deposits, debentures, bonds, and so on).

Household non-farm, non-liquid assetsValue of any assets owned by the household (not the farm business) that arenot readily convertible to cash, including real estate, business, and so on.

Household off-farm incomeOff-farm income for this household in 1993-94, excluding governmentassistance but including any income from rents, dividends, wages, share ofother business profits or losses, and so on).

Modified household assetsHousehold assets minus $150 000 (this amount being the assumed value ofthe domestic home on all farms). AUSTUDY includes only 50 per cent of farmassets in its measure.

Modified household income for AUSTUDY

Household income minus allowances under AUSTUDY provisions for thenumber and age of dependent children.

Net farm incomeIncome received from the farm (after business costs but before tax) by themembers of this household in 1993-94, including any wages and salariespaid to household members by the farm business.

xiSocial support programs

Summary

This study of farm families was commissioned by the Commonwealthgovernment to examine issues of delivery of Commonwealth social supportprograms to people in rural areas, and to provide a database for ongoingpolicy development. The study was undertaken in two stages in 1995: first,a telephone survey and analysis of almost 3500 farm households relating tofourteen Commonwealth programs; and, second, a case studies analysisexamining some broad questions arising from the initial survey analysis.

The case studies involved in-depth interviews with twelve households aswell as further statistical analysis of the survey data using a predictive modeland wellbeing analysis.

The prediction model and the wellbeing scale used appear to be useful toolsfor identifying issues in the delivery and development of Commonwealthsocial support programs which need further investigation. The predictionmodel was highly accurate in predicting actual recipients of programsupport, with a probability of 89–96 per cent. The predictions of recipientsamong nonapplicant households were also consistent with the measuresmade using the wellbeing scale.

Overall, the study showed that Commonwealth social support programswere widely used by farm families. It also showed that there were somedeficiencies in the delivery of these programs.

Demographic and locational profileIn 1995, an estimated 451 000 people were living in the main households ofAustralian broadacre and dairy farms with an estimated value of agriculturaloperations greater than $5000. Around 10.5 per cent of the surveyedpopulation was over retirement age compared with 13 per cent in theAustralian population. However, there were proportionately more peopleover retirement age living in subcommercial farm households (15.1 per cent)than in commercial farm households (9.5 per cent). A further demographicfeature was that 38 per cent fewer women than men fell in the group aged18–21 years (including full time students living away from home).

1Social support programs

Eighty-one per cent of surveyed households were in zones designated asrural, while 13 per cent were located in remote zones and the remainder wereclose to metropolitan cities.

Financial profileNo national data exist on assets levels, but anecdotal evidence suggests thataverage farm household assets were above the national average. Manysurveyed households had substantial assets, with 14 per cent reporting morethan $1 million in assets (including the domestic home and net of debt) atthe time of the survey in 1995. However, 42 per cent reported total householdassets of less than $350 000.

The proportion of farm households with nominal household incomes (net ofbusiness costs and before tax) above $40 000 in 1993-94 was similar to thatof the total Australian population in 1991. Twenty per cent of farm house-holds surveyed had household incomes below $10 000; most of these wouldhave been eligible on income grounds alone for support from the fourteenprograms considered.

After excluding an average value for the domestic home, around 14 per centof surveyed households had household assets below $350 000 and householdincomes below $15 000. Generally, households with the highest assets inthis group would have been ineligible under most program assets tests buteligible under income tests. Most households with full time students wouldhave been eligible for AUSTUDY on assets and income grounds.

Income and assets values during the survey period were likely to be lowerthan usual for a large number of farm households given a combination oflow commodity prices in the early 1990s and widespread drought during1993-94. However, there has been a long term downward decline in the netvalue of farm production, with fluctuations commonly occurring either sideof the trend line. The downturn during the survey period was not unusual inthis context, and similar or even lower levels of income can be expected inthe future.

Material wellbeingMaterial wellbeing was examined by a wellbeing score developed from anumber of measures which were being assessed by the Department of SocialSecurity at the time of the study. Differences in material wellbeing scores

2 ABARE research report 97.7

between households of different assets and income combinations reflectedthe broad differences in wellbeing that might be expected — for example,wellbeing scores tended to be lower for households with lower assets andincomes and higher for those with higher assets and incomes.

Further, for all programs, the wellbeing scores of households whoseapplication had been rejected were higher than those of households who hadreceived assistance. It is noteworthy that the distribution of wellbeing scoresfor households that were predicted recipients but unaware of a program wassimilar to the distribution of scores for households that had received supportfrom the program. The median score of predicted recipients that were awareof the Age Pension and AUSTUDY, was between the median scores of actualrecipients and rejected applicants. However, for the Basic Family Payment,the median score of predicted recipients was higher than those for actualrecipients and rejected applications.

High asset values were sometimes associated with low wellbeing scores:around 8 per cent of households with assets worth more than $1 million hadwellbeing scores in the lowest quintile (20 per cent).

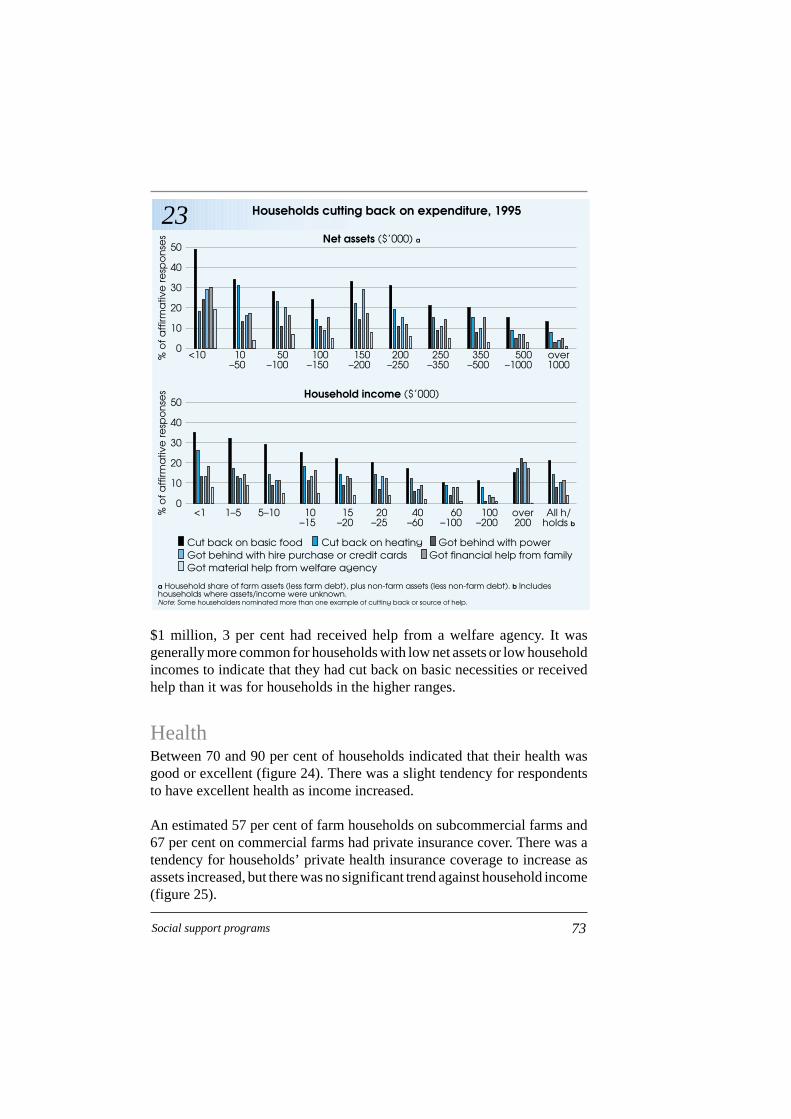

Analysis of the survey responses to questions on wellbeing showed that asignificant number of farm households (including those with high assets)were experiencing difficulty. For example, 21 per cent of all households hadcut back on basic food during the previous two years and slightly more thana quarter were concerned about making ends meet ‘all the time’ or ‘often’.The proportion of households with low assets or low incomes experiencingdifficulty was generally higher than for those with high assets or incomes.For example, approximately 28 per cent of households with assets between$50 000 and $100 000 had cut back on basic food in the two years beforethe survey, compared with approximately 13 per cent of households withassets greater than $1 million. Households that were concerned aboutmaking ends meet ‘all the time’ were much more likely to have low incomesthan were households that were not so concerned. Three per cent ofhouseholds with assets between $500 000 and $1 million received help fromwelfare agencies.

The in-depth interviews further indicated living standards and howhouseholds assessed their material wellbeing. Cutting back on basichousehold expenditure was common among households with low incomesand relatively low assets. Measures included reducing cash expenditures byliving off garden produce, severely restricting use of the family vehicle,

3Social support programs

forgoing farm improvements and sometimes reducing expenditure on fodderfor cattle. Some households with higher assets were able to maintain theirstandard of living by increasing their overdraft. The interviewed householdsrarely took holidays, and most on low incomes and low assets said they were‘struggling’ or ‘just getting by’.

Many of those interviewed in-depth who had low living standards did notbelieve they could maintain a viable operation if they subdivided their farm.Others, despite recognising the financial advantage of selling the farm andbuying a home elsewhere to retire, remained as a result of other issues.

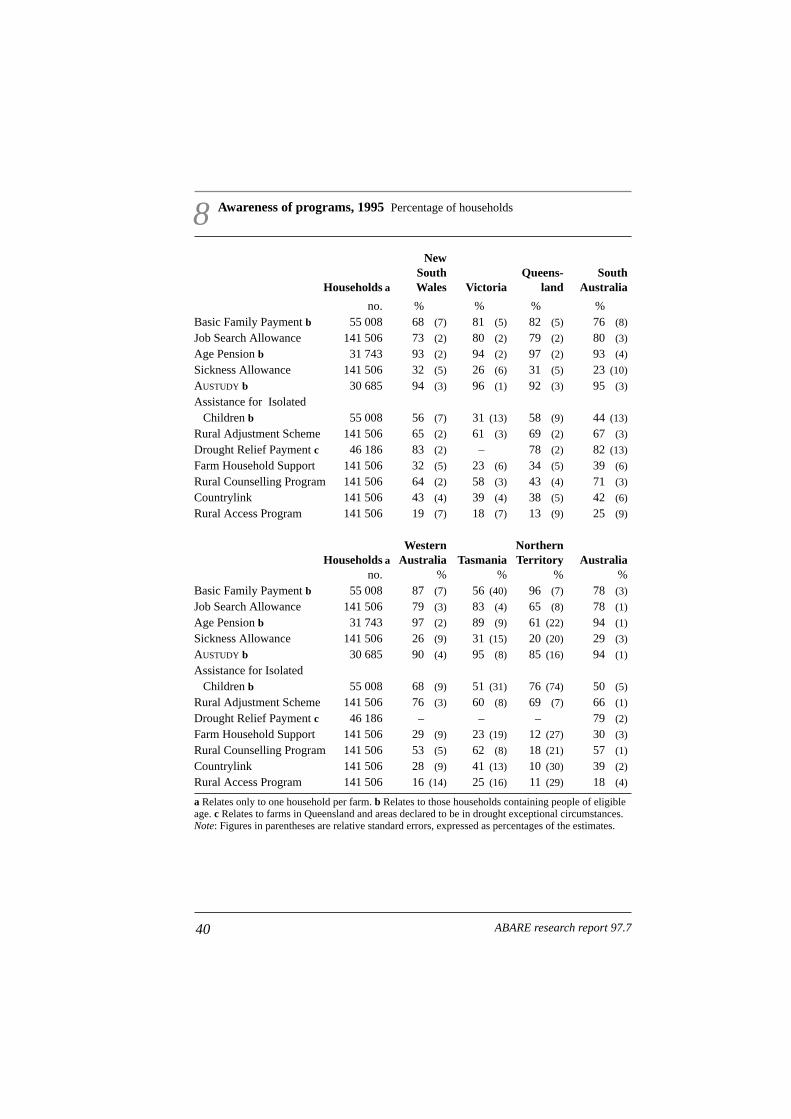

Awareness of programsAwareness of social support programs at the national level was generallyhigh for programs administered by the Department of Social Security andthe Department of Employment, Education, Training and Youth Affairs. Itwas lower for programs such as the Sickness Allowance and those ad-ministered by the Department of Primary Industries and Energy.

Ninety-four per cent of households with a young person aged 16–21 yearswere aware of AUSTUDY. A similar proportion of households with a personof retirement age were aware of the Age Pension. However, while 78 percent of households with children were aware of the Basic Family Payment,only 57 per cent were aware of the Additional Family Payment. Sixty-sixper cent of households were aware of the Rural Adjustment Scheme, 39 percent were aware of the Countrylink information service, and 18 per cent wereaware of the Rural Access Program. In Queensland and areas of New SouthWales, South Australia and Tasmania in drought exceptional circumstances,79 per cent of households were aware of the Drought Relief Payment.

There were some important differences in awareness at the state and regionallevel. For example, awareness of the Basic Family Payment and Job Searchamong farm households with at least one child younger than 18 years rangedfrom 45 per cent to 100 per cent at the statistical division level. Awarenessof the Rural Adjustment Scheme (RAS) among households variedconsiderably at the statistical division level in all states from the nationalaverage of 66 per cent. These differences might have resulted from stateshaving different needs, or from communication strategies of some state RASauthorities being less effective than others, both at the state and statisticaldivision level.

4 ABARE research report 97.7

Hardship tests

Hardship tests were designed to meet the needs of those in severe financialdifficulties but unable to meet the assets or income tests. However, most ofthe farm population were unaware of these tests. Three-quarters of targethouseholds for the Age Pension and one-fifth of the target population forJob Search were unaware that hardship tests applied to these programs.

Knowledge or understanding of programsProgram awareness was high for many programs, but knowledge of theseprograms was often scant, nonexistent or incorrect for many of thosehouseholders interviewed in-depth. Some farm families felt they were beingdenied an entitlement when this was unlikely.

Beneficiaries and rejectionsFifty-seven per cent of households with at least one child younger than 18years received the Basic Family Payment at some time during the three yearsbefore the survey, and 45 per cent of households with a person aged 16–21years received AUSTUDY in that time. Twenty-four per cent of householdswith a female aged over 60 years or a male over 65 years received the AgePension during the three years prior to the survey. Twenty-two per cent ofhouseholds in areas of drought exceptional circumstances at the time of thesurvey had received the Drought Relief Payment since its introduction in1994.

A substantial proportion (18 per cent) of households with a person aged16–21 years had had their application for AUSTUDY rejected during the threeyears before the survey. According to respondents, the main reason forrejections from most programs was that their assets were too high — thereason for 95 per cent of rejections for the Age Pension and more than 60per cent of rejections for AUSTUDY.

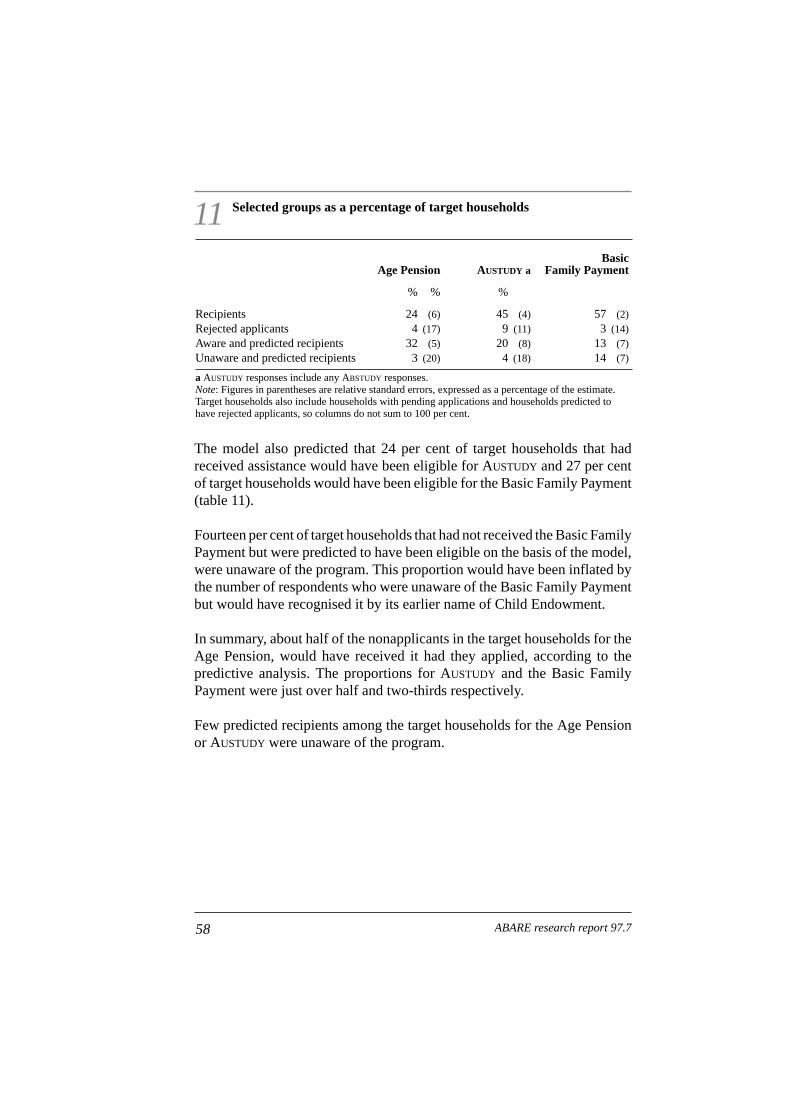

Nonapplication by potentially eligible householdersThe prediction model suggested that a substantial number of farmhouseholds might have received support had they applied. For householdswith a member of eligible age, an additional 35 per cent might have qualifiedfor the Age Pension, 24 per cent might have qualified for AUSTUDY, and 27per cent might have qualified for the Basic Family Payment. These results

5Social support programs

suggest that many of the respondents who indicated that they knew orassumed that they were ineligible for assistance from a program weremistaken.

Why potentially eligible households do not apply for assistanceEvidence from the in-depth interviews and the statistical analysis suggestseveral reasons for nonapplication by householders who are likely to beeligible might not apply for Commonwealth support. Lack of relevantinformation, including information about the differences in assets andincome provisions between programs and hardship tests, is important.

First, some householders, despite having low assets and/or income did notfeel that they needed assistance. This might have been the case for some ofthe predicted recipients who had higher wellbeing scores than those of actualrecipients.

Second, others overvalued their assets — an issue partly related to theinherent difficulties of valuing farm properties for government socialsupport programs — as discussed below.

A third factor was lack of knowledge of the provisions of the programs. Asmall percentage of households knew almost nothing about programs thatwere likely to be relevant to them. Others were not aware that assets andincome tests differ among the programs: some householders interviewed in-depth indicated that they assume that the same assets test is applied to allCommonwealth programs, whereas these tests vary considerably betweenprograms; and some households with people aged 16–21 years were unawarethat farm assets were discounted by 50 per cent for AUSTUDY, while otherswere unaware that farm assets could be ignored in applications for AUSTUDY

in drought exceptional circumstances areas.

Finally, there also appeared to be an access problem with the Age Pensionin some rural areas: the ratio of predicted to actual recipients was higher inthese areas than elsewhere, but 47 per cent of households with a member ofeligible age reside in these areas.

Farm valuationThe in-depth interviews revealed the difficulties of some householders inproviding reliable valuations of farm assets. The difficulties were com-pounded when there were few, if any, sales in an area to indicate market

6 ABARE research report 97.7

values. Some householders relied on shire rates values, and some familiesprovided a valuation that took into account the capital they would need ifthey were to sell the farm.

It seems that some farm families in severe financial difficulty were notapplying for Commonwealth assistance because there were inherentdifficulties in providing a reliable valuation. Comparative analysis of 1099farm property valuations by Department of Social Security clients and theAustralian Valuation Office in New South Wales in 1994-95 showed that asignificant number of farmers attributed a value to their properties (partic-ularly the home and surrounding land) which would have been substantiallydifferent from an official valuation done for a Commonwealth social supportprogram.

Also, compared with other social security clients, a higher proportion offarmers received less than the maximum allowable payment where benefitswere reduced because of high assets.

Views on the assets testHouseholds interviewed in-depth expressed a range of concerns about assetstesting. Some commented that rural residents were disadvantaged by theexemption of the principal residence, which they saw as having a higheraverage value in cities. Others thought that households with high assets butlow incomes associated with severe downturns should be given moreconsideration. Discussion of the options for selling part of the farm to gainfinancial independence in old age led to issues associated with continuingfarm viability, succession and council subdivision regulations.

Views on service providedGenerally, 80–92 per cent of farm households with some contact with aservice rated the quality of that service as average or better on a five pointrating scale, and 8–20 per cent rated the quality as poor or very poor. Similarratings were given in a separate study by 5 per cent of individuals contactingSocial Security regional offices about Social Security programs.

Other service issuesMany of those interviewed felt that the complexity of farm financialaccounts and social security applications required the engagement of a

7Social support programs

financial professional or accountant. This was a burden on people strugglingto make ends meet.

It is not possible to gauge the extent of a number of problems which emergedfrom the in-depth interviews. Long delays in telephone enquiries wereaccepted by some but irritated others. Negative experiences with one agencywere sometimes generalised to all agencies. A long delay in response to acase of extreme hardship caused severe personal distress in one household.

Needy householders unaware of programsWellbeing scores suggest that eligible nonapplicant farm families who wereunaware of relevant programs were at least as much in need of Common-wealth support as those who were aware. Most in need were elderly people.The circumstances of farm families with little or virtually no knowledge oftarget programs, although a small group, make them a high priority forattention.

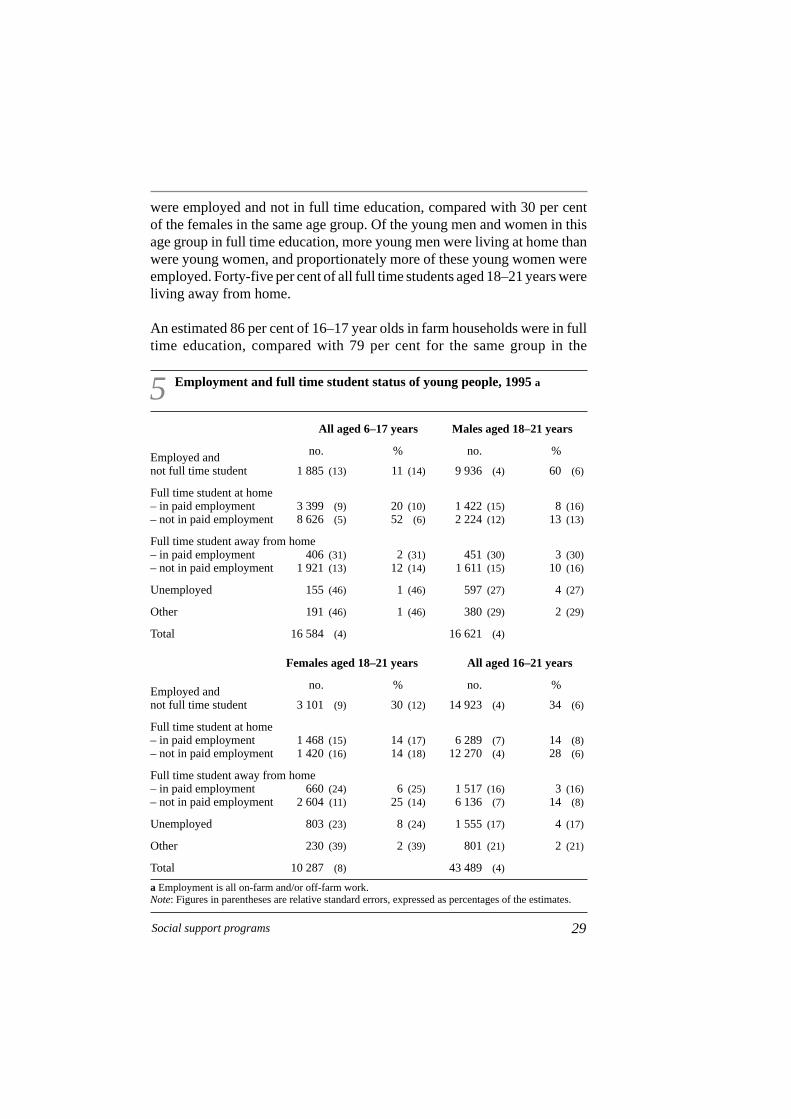

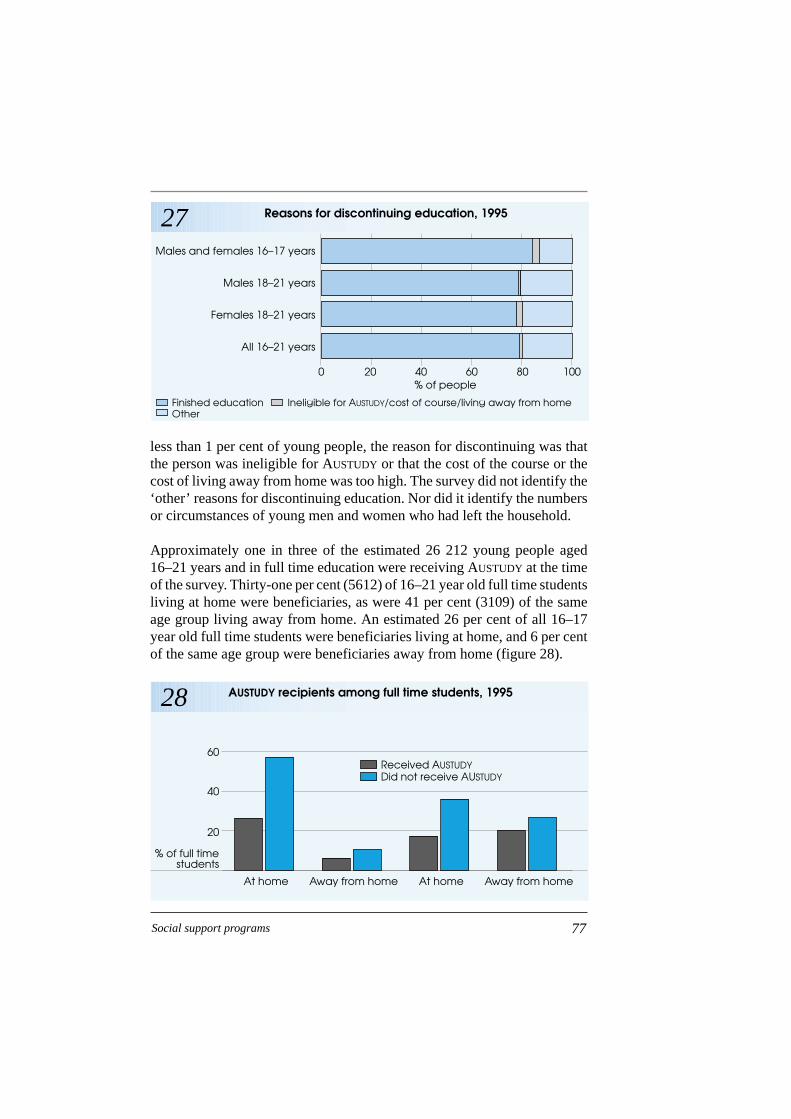

Young people and educationSixteen per cent of people aged 16–17 years and 45 per cent of people aged18–21 years who were in full time study were living away from home at thetime of the survey. A higher proportion of those living away from home wereAUSTUDY beneficiaries. Approximately one in three of the estimated 26 000young people aged 16–21 years in full time education were receivingAUSTUDY.

A higher proportion of those aged 16–17 years in farm households were infull time education compared with the same age group in Australia.Compared with young men, a much larger proportion of young women aged18–21 in farm households were in full time education. However, there wasrelatively little difference between the total number of young women (6152)and young men (5708) aged 18–21 years in farm households in full timeeducation.

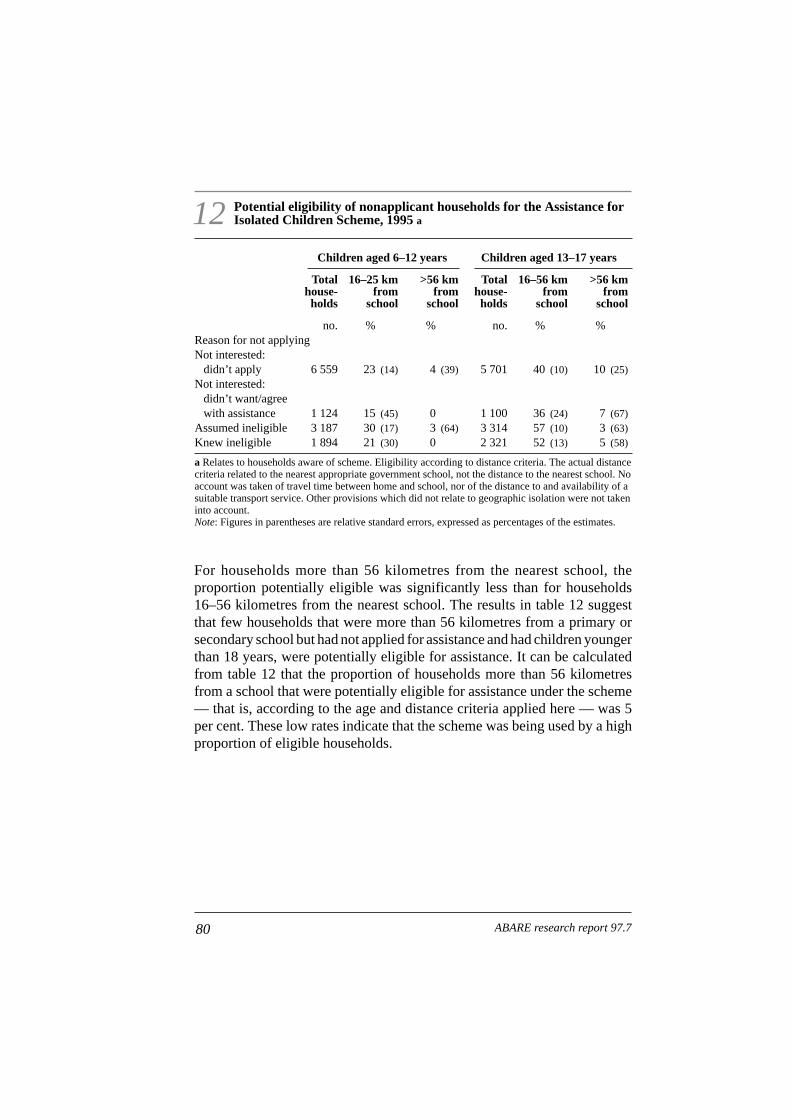

Approximately 19 per cent of farm households were more than 20 kilometresfrom a primary school and almost half were more than 20 kilometres froma secondary school. Of households that did not apply for assistance from theAssistance for Isolated Children Scheme but had children of eligible age andmet the 56 kilometres distance provision, only 5 per cent were potentiallyeligible for assistance.

8 ABARE research report 97.7

An estimated 14 per cent of households with children of school age hadchildren at boarding school at some time during the two years before thesurvey. Slightly more than one in ten of those households with children atboarding school had been behind with boarding school fees in the two yearsbefore the survey.

ConclusionThis study indicated that many farm households relied on the Common-wealth social support system at the time of survey. However, the researchundertaken for this study indicated that a large number of farm families withincome levels and material wellbeing scores similar to those of actualrecipients were not receiving Commonwealth support. Furthermore, manyof these families were likely to be eligible for Commonwealth assistance,but were not applying for it. It would appear that some did not apply becausethey misunderstood the assets limit for a program, and some did notunderstand that some assets might have been discounted or that the value oftheir home should have been assessed as the value of an equivalent homeand block in the nearest regional centre. Many provided valuations thatwould have differed from official valuations done for the Commonwealthprogram. In this context, methods used to determine property valuationsneeded further examination.

9Social support programs

Introduction

The adequacy and equity of Commonwealth social support for farm familieshas come under increased scrutiny both publicly and within government inrecent years. There is some criticism that social support services do not takeproper account of the characteristics of rural Australia, including the relativeremoteness and the high assets but low incomes of some farm families.

Community consultations undertaken by the National Council for theInternational Year of the Family (1994, pp. 154–61) heard concerns thatassets testing for income support was unfair to farm families. The Depart-ment of Social Security viewed the assets test from its inception as affectingfarm families more than any other group (DSS 1993, p. 15).

Another issue emerging from the International Year of the Family study wasthe need for many young people to pursue their education away from homeand thus deal with a major expense. Similar themes emerged from theparliamentary report of the Senate Rural and Regional Affairs and TransportReferences Committee on assets testing (1995b) and the annual conferenceof the Country Women’s Association in New South Wales (The Land, 1 June1995, p. 59). However, there has been little quantitative informationavailable for more rigorously examining such criticisms.

In December 1994, federal Cabinet considered the needs of farm families indifficulty in drought affected areas during its deliberations on the long termresponse to drought. As a result, ABARE was commissioned to undertakea two stage study through the Commonwealth Department of PrimaryIndustries and Energy to assist government policy makers to developpolicies and programs for farm families and others in rural communities.The first stage was a survey of farm families, and the second was an analysisof case studies to follow the initial survey.

The survey was to ascertain farm families’ knowledge of, access to, and useof existing social welfare and related programs. In meeting these aims, thesurvey was to consider problems in access to programs and services; theresponsiveness of Commonwealth social agencies to the needs of ruralclients; geographic differences in the understanding and take-up of pro-grams; assets and income levels; and living standards.

10

1

ABARE research report 97.7

The terms of reference for the two stages of the study are listed inappendix A.

Responding to the terms of reference, ABARE consulted with the Depart-ment of Social Security, the Department of Employment, Education,Training and Youth Affairs, the Department of Finance, the Attorney-General’s Department and the Department of Primary Industries and Energyto design a questionnaire to collect information from Australian farmers.ABARE selected a sample of farms from all agricultural industries andconducted a telephone survey in March, April and May 1995. The surveyresults were weighted to produce population estimates. The telephonequestionnaire and other details of the survey method are provided inappendix B.

The telephone survey collected information on:

• age, gender and employment of all household members;

• awareness and use of various Commonwealth government programs;

• on-farm and off-farm income, assets and debts;

• standard of living and access to services; and

• participation in education.

Income is the measure most commonly used to indicate relative poverty andliving standards, and is used to assess eligibility for a wide range ofCommonwealth support programs. Assets tests have been introduced forassessment of most programs too. Wealth can modify the effects of incomeon wellbeing — that is, home owners usually enjoy a higher level of well-being than non-homeowners with the same income. Wealth and income canalso be interchangeable. However, income levels (with or without assetslevels or other various adjustments such as for the number of children) donot indicate standard of living necessarily. Qualitative measures have beendeveloped and applied instead of, or in addition to, income to assessstandards of living and need for support (Travers and Richardson 1993). Inthis study, the measures of wellbeing used were similar to those developedfor the Department of Social Security.

Results of the telephone survey raised questions about the decision makingdynamics of farm families when it came to Commonwealth social supportprograms, the nature of farmers’ understanding of the programs, their level

11Social support programs

of material wellbeing, and the means by which the Commonwealthgovernment may be more effective in responding to the needs of farmers inthe design and delivery of their social support programs (Leach 1967; Yin1994).

Questions such as these called for a method of research which couldinvestigate a range of behaviours, experiences and opinions which thetelephone survey was unable to examine. In-depth face to face interviewswith twelve selected farm households allowed examination of the context inwhich farmers provided answers to the telephone survey questions, andhighlighted the complexity of their relationships with Commonwealthsupport programs.

An analysis of the telephone survey data indicated, according to assets andincome criteria, that a substantial proportion of farmers may have beeneligible for support under a number of Commonwealth programs. However,a significant proportion did not apply because they indicated that they knewor assumed that they were not eligible. This suggested a need to furtherexamine farmers’ understanding of the criteria for programs, and their meansof arriving at an estimate of their assets. The survey indicated a fairly highlevel of basic awareness of most of the major Commonwealth social supportprograms, but some farm households were not aware of particular programsat all, and only around a quarter of households were aware of hardship tests.These results suggested a need to further examine farmers’ knowledge ofsocial support programs.

Results and analysis from the telephone survey are presented in this report.An outline of major Commonwealth support programs is given in chapter2, and the economic conditions in the survey period are discussed in chapter3. Demographic, locational profiles and assets and income profiles of farmscovered by the survey are contained in chapters 4 and 5. Results arepresented in chapters 6–9, covering awareness and use of programs (chapter6); reasons for nonapplication (chapter 7); reasons for rejection (chapter 8);potential for wider program use (chapter 9). Details are also provided on thequality of program service (chapter 10); householders’ material wellbeingand health (chapter 11); and their education (chapter 12). The findings fromthe study are discussed in chapter 13. The basis on which the householdswere selected for in-depth interview is described in chapter 9.

Full details of the methods used for the telephone survey and the in-depthinterviews are provided in appendix B.

12 ABARE research report 97.7

Findings and conclusions only from the in-depth household interviews areincluded in this report. Summaries of the interviews have been presented tothe Steering Committee separately.

The results presented are likely to assist policy makers, analysts and programadministrators to improve the targeting of social support (and other) servicesto farm families. They are also likely to help others who wish to considerthis information and demographic and locational detail in work on ruralindustries, adjustment and rural development, for example. The analysismay also assist in improving service delivery to others in rural communities,particularly to those in more remote areas. This study provides informationon commercial and subcommercial farms and all agricultural industries.Much of this information has not been available previously.

13Social support programs

Government programs during thesurvey period

The Department of Social Security, the Department of Employment,Education, Training and Youth Affairs and the Department of PrimaryIndustries and Energy manage a wide range of Commonwealth socialsupport programs. The social security and education programs consideredin this study were developed to meet community needs for short term andlong term income support, for financial assistance with the cost of rearingchildren and for student financial assistance. Other programs providesupport for rural people or farm families (some on a community basis)specifically.

Stemming from their different rationales, different eligibility provisions(including assets and income tests) have been developed for each program.Several programs also have provisions which can be applied in particularsituations of hardship.

The programs examined in this study are described below as they existed atthe time of the survey. Further details about eligibility for these programsare contained in appendix C. (Note that some details have been changedsince the survey was undertaken in 1995 — for example, the Basic FamilyPayment and Additional Family Payment were combined as FamilyPayment in January 1996, and Farm Household Support was closed to newapplications from 5 May 1997.)

Programs

Family paymentsFunds were provided under the Family Payments Program to eligible parentsof children aged up to 16 years, or, in the case of full time dependentsecondary students who are ineligible for AUSTUDY, until the end of the yearin which the student turned 18.

The Basic Family Payment was provided to most families with dependentchildren in recognition of the costs of rearing a child. The Additional FamilyPayment was an extra payment for low income families with dependentchildren.

14

2

ABARE research report 97.7

Job Search Allowance

Job Search Allowance — which was absorbed into the New Start programin July 1996 — was available for eligible unemployed people who wereactively seeking and willing to undertake suitable paid work, aged 18–65years if male or 18–60 years if female, and registered with the Common-wealth Employment Service (CES). People older than 18 years had to havebeen willing to undertake suitable vocational training or other activity ap-proved by the CES. The allowance provided short term income support.

Farmers might have qualified even if they had a limited role in running thefarm, but they had to meet normal provisions such as being willing to workoff-farm and taking reasonable steps to find work. In severe financialhardship, farm assets might have been ignored if the property could nothave been sold because there was no buyer or there was a legal impedimentto selling and the property could not have been used as security forborrowing.

Age PensionThe Age Pension was available for eligible women aged over 60 years andmen aged over 65 years who were not in the workforce. In some situations,retired farmers in severe financial hardship could receive the Age Pensioneven if the value of their farm and other assets exceeded the normal eligibilitylimits. In these cases, a test of ‘reasonableness’ was applied — that is, apension might have been granted if the applicant could not reasonably havebeen expected to realise the farm asset by selling the farm or could notreasonably have been expected to use the farm as security for borrowing.

Sole Parent PensionThe Sole Parent Pension provided income support for eligible people whowere not part of a couple and were caring for a child. The child had to beyounger than 16 years or qualify for a child disability allowance.

Sickness AllowanceThe Sickness Allowance provided short term income support to eligiblewomen aged 16–60 years and men aged 16–65 years whose illness meantthat they were temporarily unable to support themselves by participating inthe labour market.

15Social support programs

Disability Support PensionThe Disability Support Pension was available for eligible people aged 16years or more who had an impairment level of at least 20 per cent that meantthey were unable to work or undertake work related training for at least thefollowing two years. People who were permanently blind were also entitledto this pension.

AUSTUDY

AUSTUDY provided financial support to needy students to complete theirsecondary education and go on to further study. Generally, assistance wasavailable to eligible full time students aged 16 years or over. Students wereeligible for the ‘independent’ rate of AUSTUDY from the age of 22 years, andthis rate was exempt from tests on parental assets and income. The schemeprovided a living allowance and, for some students, assistance with the costof travel between the parental home and the relevant educational institution.

Only 50 per cent of farm assets were included in the total assets assessed.Families receiving Drought Relief Payments were exempt from theAUSTUDY farm assets testing and parental income testing. On-farm assetswere exempt from testing for applicants in areas of drought exceptionalcircumstances.

Students aged over 16 years in isolated geographic areas who met theeligibility requirements for both AUSTUDY and the Assistance for IsolatedChildren Scheme were entitled to receive payment from the program whichprovided the higher benefit.

In this report, analysis mostly relates to AUSTUDY, although telephone surveyquestions about program awareness and the use and quality of services werecollected for AUSTUDY and ABSTUDY (see below) jointly. Few households inthe survey population would have included Aboriginal or Torres Straitpeople, and most responses would have related to AUSTUDY, so referencesto ABSTUDY have been generally omitted (although it is important to notethat no assets test applies to ABSTUDY).

ABSTUDY

ABSTUDY payment was made to Aboriginal and Torres Strait Islanderstudents to support approved secondary or tertiary education courses and

16 ABARE research report 97.7

primary courses for students aged 14 years and over. A number of allowancesapplied. Some ABSTUDY allowances were paid regardless of family income,while others were subject to income testing. Full time, part time andcorrespondence students might have been be eligible. During interview,ABSTUDY information was obtained with information on AUSTUDY.

Assistance for Isolated Children SchemeThe Assistance for Isolated Children Scheme was directed mainly towardstudents aged under 19 years who did not have reasonable access to anappropriate government school because they were geographically isolated.The eligibility criteria for this scheme was based on the distance and traveltime between home and school, and on the availability of transport servicesto the nearest appropriate government school.

Rural Adjustment SchemeThe Rural Adjustment Scheme (RAS) provided financial support to eligiblefarm businesses to facilitate rural adjustment. The scheme was aimed atsupporting farmers to improve the productivity, sustainability and profit-ability of their farm businesses. In addition, the scheme assisted thosefarmers whose farm businesses were not viable and who wished to leavefarming. The scheme also supported those farmers who were considered tobe profitable in the long term but who were experiencing exceptionalcircumstances such as severe drought.

Drought Relief PaymentThe Drought Relief Payment was designed to assist farmers in areas ofexceptional circumstances to meet their living expenses. To qualify for theDrought Relief Payment, a farmer had to be aged at least 18 years and havea drought ‘exceptional circumstances’ certificate from a RAS authority.Payments for this program were equivalent to Job Search Allowance and,where applicable, Partner Allowance and Family Payments. Job SearchAllowance assets and income tests applied but farm assets were excludedfrom assets testing.

Farm Household SupportThe Farm Household Support Scheme helped eligible farmers who couldnot get further commercial finance to meet day to day living expenses. It

17Social support programs

provided a loan available for up to two years. Under certain circumstances,such as if the farm was sold within two years, part of the payment might havebeen converted to a grant and extended repayment periods applied. Norepayments were required until the family ceased using the scheme andrepayments could be made by instalments over a period of up to ten years. TheJob Search assets and income tests applied, but the tests excluded farm assets.

Rural Counselling ProgramThe Rural Counselling Program was aimed at helping rural communities setup services which provided financial advice and counselling for farmbusinesses experiencing hardship. Under this program, rural communitiesreceived government grants toward the cost of setting up and running theseservices. Farm families in financial difficulty could receive free financialcounselling on a confidential basis.

CountrylinkCountrylink provided information on Commonwealth programs throughseveral services including a toll-free telephone service, a printed directory,an electronic database and community information stands. The programaimed to help people living in rural and remote areas to learn aboutCommonwealth services and assistance.

Rural Access ProgramThrough grants to community groups, the Rural Access Program helpedrural and remote communities to increase access to services. This programassisted country people in developing projects that improved the health,education, training, information and social services of their communities.The program supported community oriented projects, including those forwomen, Aborigines and Torres Strait Islanders, people from non-Englishspeaking backgrounds, and people with disabilities. Nonprofit communitygroups, educational institutions and industry groups were eligible to applyfor funds from this program.

Assets and income assessmentReceipt of Commonwealth social support payment depended on theapplicant meeting eligibility criteria, including assets and income tests. Theapplicant’s assessable assets and income had to be below certain values;

18 ABARE research report 97.7

these values varied between programs and were related to characteristicssuch as age, family composition and other policy considerations. Allprograms excluded the value of the domestic home and curtilage fromassessment. The value of the family home and curtilage on a farm wasdetermined as their market value in the closest regional centre.

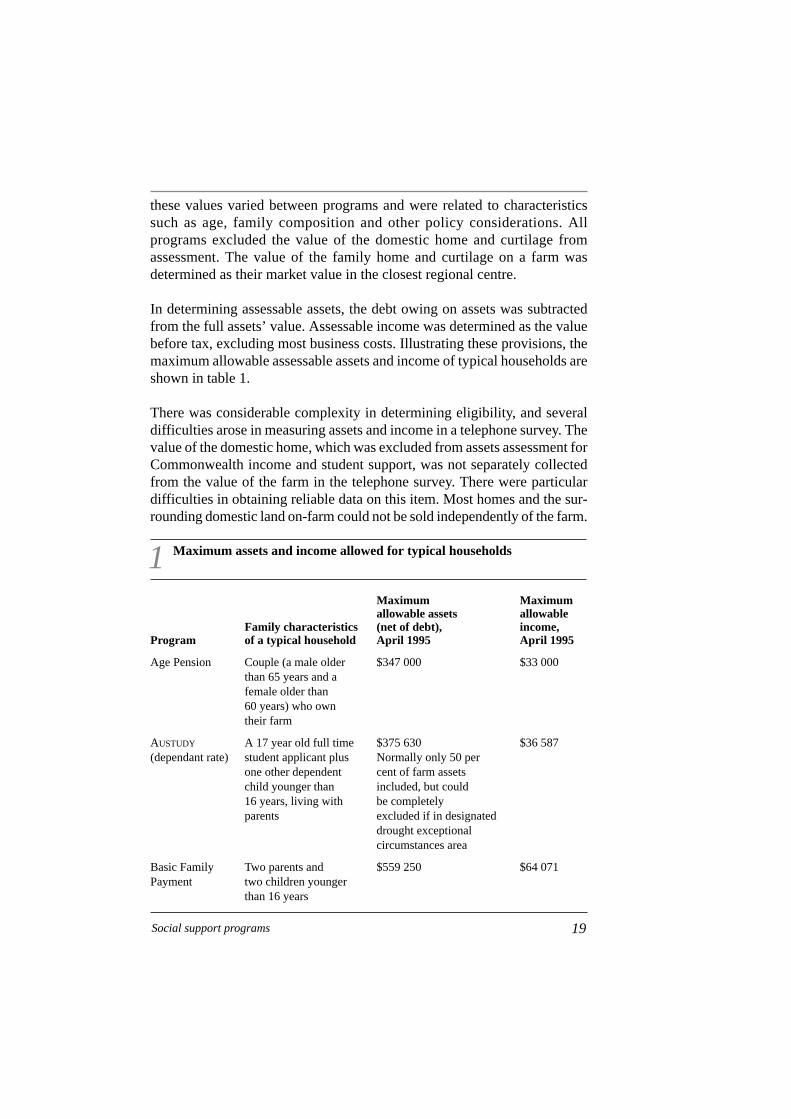

In determining assessable assets, the debt owing on assets was subtractedfrom the full assets’ value. Assessable income was determined as the valuebefore tax, excluding most business costs. Illustrating these provisions, themaximum allowable assessable assets and income of typical households areshown in table 1.

There was considerable complexity in determining eligibility, and severaldifficulties arose in measuring assets and income in a telephone survey. Thevalue of the domestic home, which was excluded from assets assessment forCommonwealth income and student support, was not separately collectedfrom the value of the farm in the telephone survey. There were particulardifficulties in obtaining reliable data on this item. Most homes and the sur-rounding domestic land on-farm could not be sold independently of the farm.

19Social support programs

1 Maximum assets and income allowed for typical households

Maximum Maximumallowable assets allowable

Family characteristics (net of debt), income,Program of a typical household April 1995 April 1995

Age Pension Couple (a male older $347 000 $33 000than 65 years and afemale older than60 years) who owntheir farm

AUSTUDY A 17 year old full time $375 630 $36 587(dependant rate) student applicant plus Normally only 50 per

one other dependent cent of farm assetschild younger than included, but could16 years, living with be completelyparents excluded if in designated

drought exceptional circumstances area

Basic Family Two parents and $559 250 $64 071Payment two children younger

than 16 years

The Department of Social Security and the Department of Employment,Education, Training and Youth Affairs, acting on the advice of the AustralianValuation Office, have determined a method for valuing farmers’ domestichomes which was considered to provide an equitable valuation with that ofhomes of town people: the value of the farm home was taken as the valueof an equivalent home on an averaged sized block in the nearest regionalcentre. Providing a value for their home in these terms during a telephoneinterview would have been very difficult for many farmers.

To derive assessable assets for some programs, certain financial items wereexcluded. For example, in the case of hardship tests for the Basic FamilyPayment, farm assets were not included if the parents’ income was less thana specified minimum. At the time of the survey this was $14 144 for a twoparent family with one child of eligible age.

There were variations within and between programs in relation to the upperassessable assets and income limits for eligibility. These depended on familycomposition and the number and age of dependent children (see appendix C),for example. The assets and income unit assessed for many of the programsconsidered in this report was the parent/s plus dependent children, but thiswas not the case for all programs — for example, if the applicant for JobSearch Allowance was a 20 year old daughter living with her parents, onlythe daughter’s assets and income were assessed.

To further illustrate these types of complexities in program provisions,consider AUSTUDY and the Age Pension. Excluding the Assistance forIsolated Children Scheme, for which an assets and income test applied onlyto the Additional Boarding Allowance component, AUSTUDY had the leastrestrictive eligibility conditions — for example, no farm assets test appliedfor AUSTUDY applicants coming from a farm with a drought exceptionalcircumstances certificate. For standard AUSTUDY, only 50 per cent of farmassets net of debt were assessed. At the time of the survey, the maximumassets value and the maximum income value for eligibility were $375 630and $31 687 respectively for a family with one dependent applicant childyounger than 17 years at home.

The maximum allowable income for the Age Pension for a married applicantwas $33 000 during the survey period. Farm assets could be excluded fromassessment for the Age Pension under hardship circumstances.

20 ABARE research report 97.7

Economic conditions in the surveyperiod

The need for family income support is affected by general economicconditions. Historically, farm businesses have experienced a high degree ofvariability in incomes and adjustment pressures to maintain or improve theirproductivity. The degree of variability in farm incomes is influenced byfluctuations in seasonal conditions and commodity prices mainly (Wrightet al. 1994; Martin 1995).

Some long term perspective on the decline in commodity prices can beobtained from figure 1. However, the effect of these low prices on-farmincomes was exacerbated by the significant decline in farm production in1994-95 (particularly grain production) as a result of the effects of drought.The downward trend in figure 1 indicates the long term pressures on Aus-tralian farm businesses to improve their productivity.

During 1994-95, Australia was faced with the most serious drought since atleast 1982-83. A significant number of family farms within all states andterritories felt the impact of the drought. In some areas, particularly inQueensland, farmers experienced their fourth successive year of low rainfall.As a result of the drought conditions, most farms in drought areas receivedlower than the usual farm income, consequently reducing the cash flow formost of these farms (Martin 1995, pp. 58–64).

21

3

Social support programs

1 Index of real prices received by farmers a

a Movements in prices received by Australian farmers for the products they sell, deflated by the consumer price index. The index measures changes in unit prices and so is not an indicator of changes in farmers' gross income which incorporates both price and quantity changes. Source: ABARE (1995).

index

1.0

1.5

2.0

2.5

1959-60

1954-55

1964-65

1969-70

1974-75

1979-80

1984-85

1989-90

1994-95

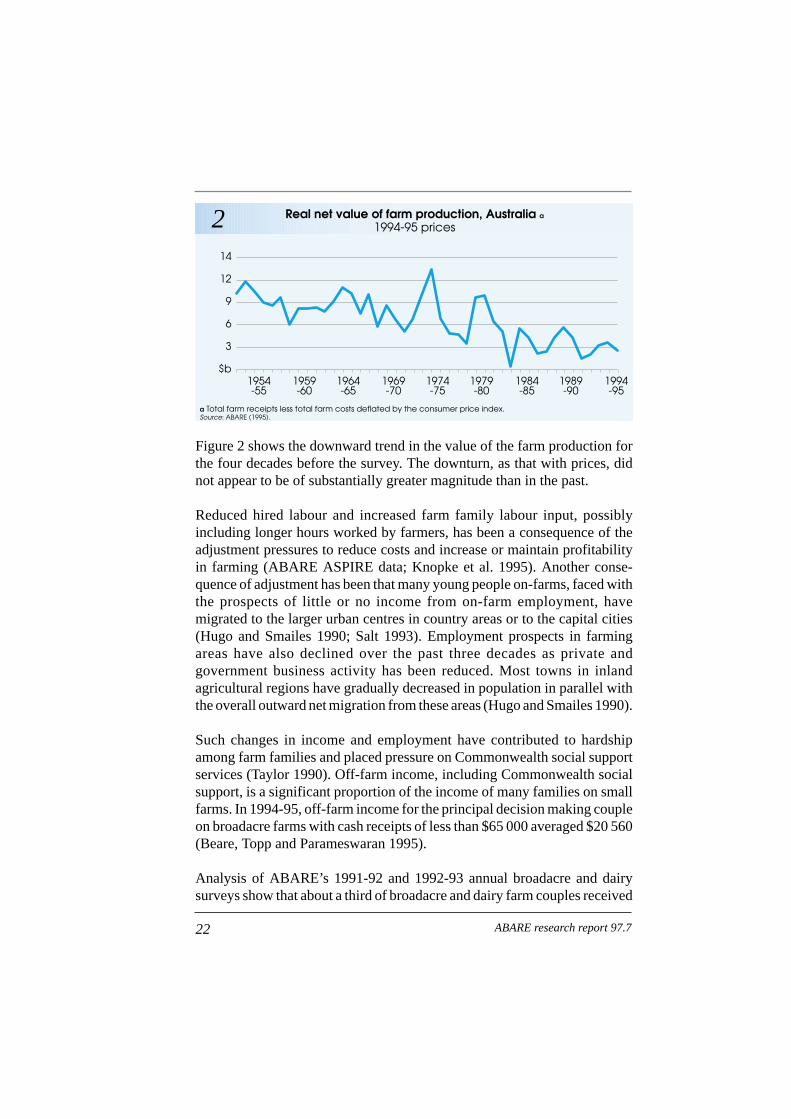

Figure 2 shows the downward trend in the value of the farm production forthe four decades before the survey. The downturn, as that with prices, didnot appear to be of substantially greater magnitude than in the past.

Reduced hired labour and increased farm family labour input, possiblyincluding longer hours worked by farmers, has been a consequence of theadjustment pressures to reduce costs and increase or maintain profitabilityin farming (ABARE ASPIRE data; Knopke et al. 1995). Another conse-quence of adjustment has been that many young people on-farms, faced withthe prospects of little or no income from on-farm employment, havemigrated to the larger urban centres in country areas or to the capital cities(Hugo and Smailes 1990; Salt 1993). Employment prospects in farmingareas have also declined over the past three decades as private andgovernment business activity has been reduced. Most towns in inlandagricultural regions have gradually decreased in population in parallel withthe overall outward net migration from these areas (Hugo and Smailes 1990).

Such changes in income and employment have contributed to hardshipamong farm families and placed pressure on Commonwealth social supportservices (Taylor 1990). Off-farm income, including Commonwealth socialsupport, is a significant proportion of the income of many families on smallfarms. In 1994-95, off-farm income for the principal decision making coupleon broadacre farms with cash receipts of less than $65 000 averaged $20 560(Beare, Topp and Parameswaran 1995).

Analysis of ABARE’s 1991-92 and 1992-93 annual broadacre and dairysurveys show that about a third of broadacre and dairy farm couples received

22 ABARE research report 97.7

2 Real net value of farm production, Australia a

1994-95 prices

a Total farm receipts less total farm costs deflated by the consumer price index. Source: ABARE (1995).

$b

3

6

9

14

12

1959-60

1954-55

1964-65

1969-70

1974-75

1979-80

1984-85

1989-90

1994-95

some income under at least one Commonwealth social support program fromthe Department of Social Security or the Department of Employment,Education, Training and Youth Affairs.

23Social support programs

Demographic and locational profile

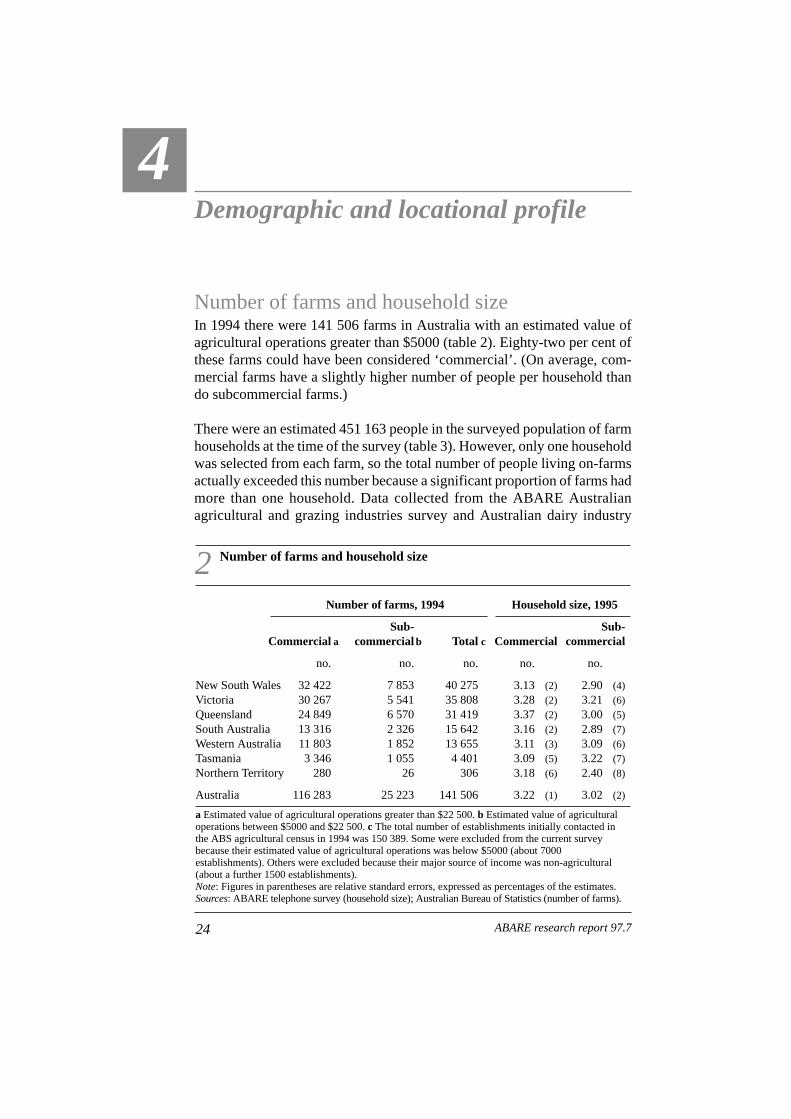

Number of farms and household sizeIn 1994 there were 141 506 farms in Australia with an estimated value ofagricultural operations greater than $5000 (table 2). Eighty-two per cent ofthese farms could have been considered ‘commercial’. (On average, com-mercial farms have a slightly higher number of people per household thando subcommercial farms.)

There were an estimated 451 163 people in the surveyed population of farmhouseholds at the time of the survey (table 3). However, only one householdwas selected from each farm, so the total number of people living on-farmsactually exceeded this number because a significant proportion of farms hadmore than one household. Data collected from the ABARE Australianagricultural and grazing industries survey and Australian dairy industry

24

4

ABARE research report 97.7

2 Number of farms and household size

Number of farms, 1994 Household size, 1995

Sub- Sub-Commercial a commercial b Total c Commercial commercial

no. no. no. no. no.

New South Wales 32 422 7 853 40 275 3.13 (2) 2.90 (4)Victoria 30 267 5 541 35 808 3.28 (2) 3.21 (6)Queensland 24 849 6 570 31 419 3.37 (2) 3.00 (5)South Australia 13 316 2 326 15 642 3.16 (2) 2.89 (7)Western Australia 11 803 1 852 13 655 3.11 (3) 3.09 (6)Tasmania 3 346 1 055 4 401 3.09 (5) 3.22 (7)Northern Territory 280 26 306 3.18 (6) 2.40 (8)

Australia 116 283 25 223 141 506 3.22 (1) 3.02 (2)

a Estimated value of agricultural operations greater than $22 500. b Estimated value of agriculturaloperations between $5000 and $22 500. c The total number of establishments initially contacted inthe ABS agricultural census in 1994 was 150 389. Some were excluded from the current surveybecause their estimated value of agricultural operations was below $5000 (about 7000establishments). Others were excluded because their major source of income was non-agricultural(about a further 1500 establishments).Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates.Sources: ABARE telephone survey (household size); Australian Bureau of Statistics (number of farms).

25Social support programs

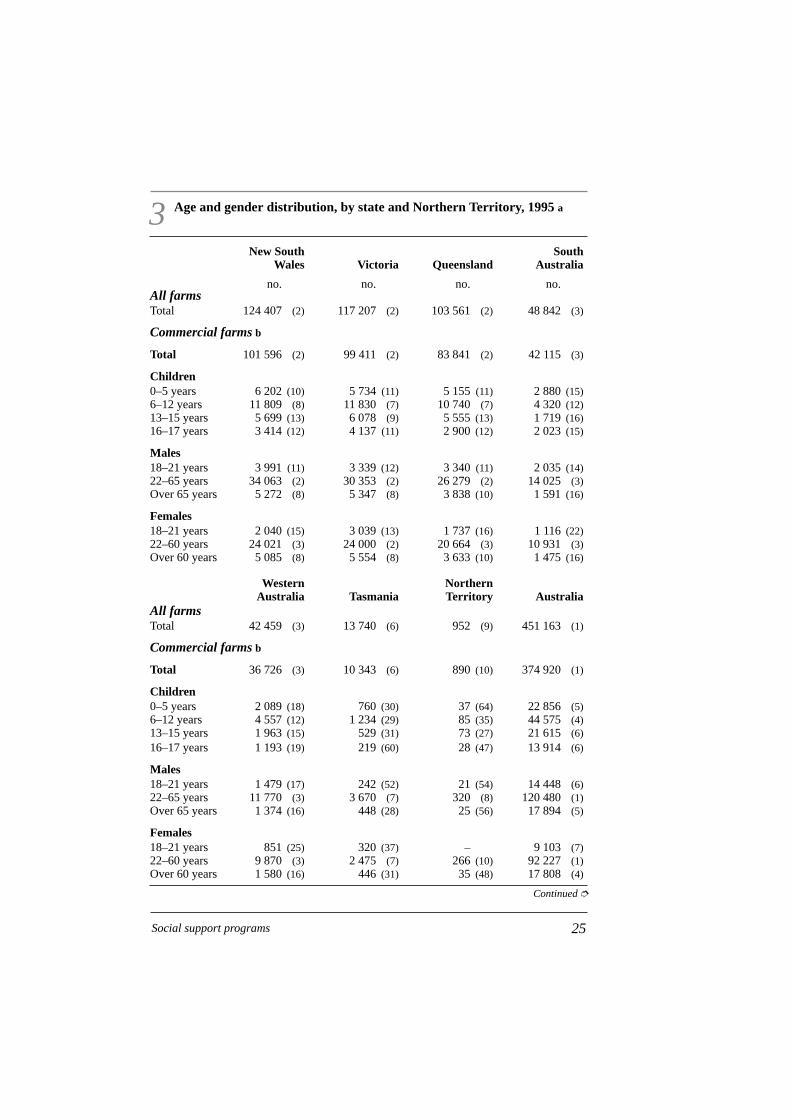

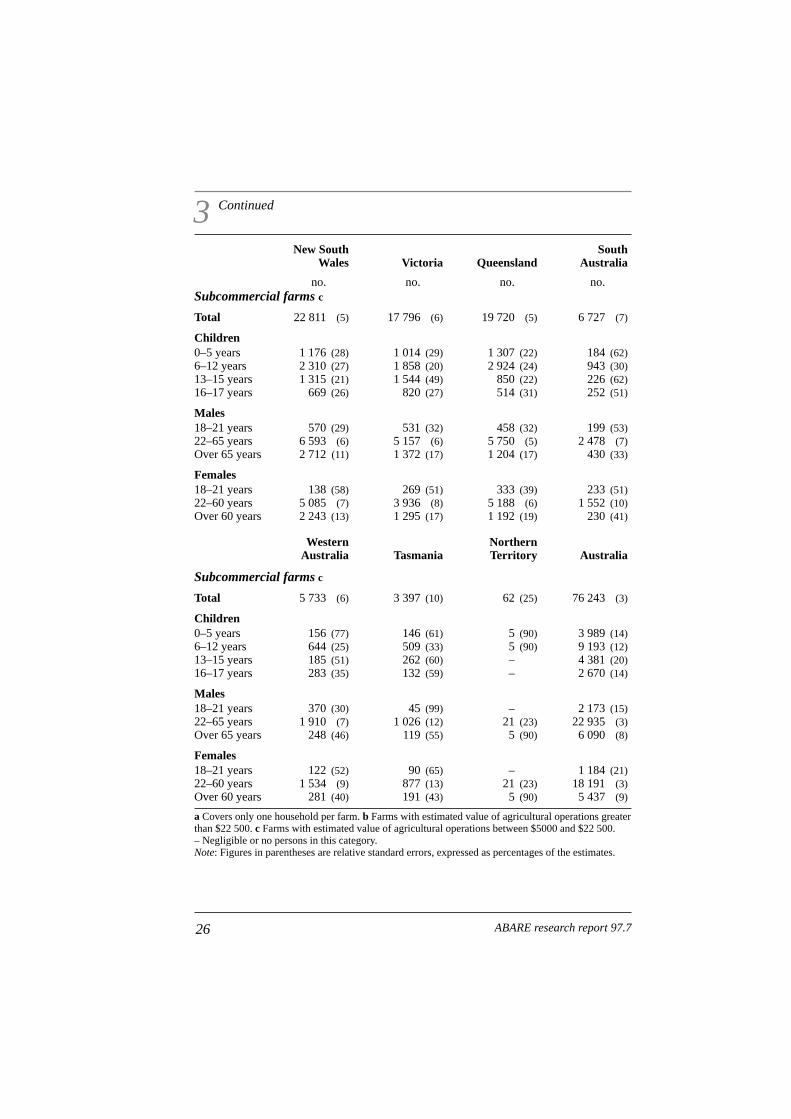

3 Age and gender distribution, by state and Northern Territory, 1995 a

New South SouthWales Victoria Queensland Australia

no. no. no. no.All farmsTotal 124 407 (2) 117 207 (2) 103 561 (2) 48 842 (3)

Commercial farms b

Total 101 596 (2) 99 411 (2) 83 841 (2) 42 115 (3)

Children0–5 years 6 202 (10) 5 734 (11) 5 155 (11) 2 880 (15)6–12 years 11 809 (8) 11 830 (7) 10 740 (7) 4 320 (12)13–15 years 5 699 (13) 6 078 (9) 5 555 (13) 1 719 (16)16–17 years 3 414 (12) 4 137 (11) 2 900 (12) 2 023 (15)

Males18–21 years 3 991 (11) 3 339 (12) 3 340 (11) 2 035 (14)22–65 years 34 063 (2) 30 353 (2) 26 279 (2) 14 025 (3)Over 65 years 5 272 (8) 5 347 (8) 3 838 (10) 1 591 (16)

Females18–21 years 2 040 (15) 3 039 (13) 1 737 (16) 1 116 (22)22–60 years 24 021 (3) 24 000 (2) 20 664 (3) 10 931 (3)Over 60 years 5 085 (8) 5 554 (8) 3 633 (10) 1 475 (16)

Western NorthernAustralia Tasmania Territory Australia

All farmsTotal 42 459 (3) 13 740 (6) 952 (9) 451 163 (1)

Commercial farms b

Total 36 726 (3) 10 343 (6) 890 (10) 374 920 (1)

Children0–5 years 2 089 (18) 760 (30) 37 (64) 22 856 (5)6–12 years 4 557 (12) 1 234 (29) 85 (35) 44 575 (4)13–15 years 1 963 (15) 529 (31) 73 (27) 21 615 (6)16–17 years 1 193 (19) 219 (60) 28 (47) 13 914 (6)

Males18–21 years 1 479 (17) 242 (52) 21 (54) 14 448 (6)22–65 years 11 770 (3) 3 670 (7) 320 (8) 120 480 (1)Over 65 years 1 374 (16) 448 (28) 25 (56) 17 894 (5)

Females18–21 years 851 (25) 320 (37) – 9 103 (7)22–60 years 9 870 (3) 2 475 (7) 266 (10) 92 227 (1)Over 60 years 1 580 (16) 446 (31) 35 (48) 17 808 (4)

Continued ➮

3 Continued

New South SouthWales Victoria Queensland Australia

no. no. no. no.Subcommercial farms c

Total 22 811 (5) 17 796 (6) 19 720 (5) 6 727 (7)

Children0–5 years 1 176 (28) 1 014 (29) 1 307 (22) 184 (62)6–12 years 2 310 (27) 1 858 (20) 2 924 (24) 943 (30)13–15 years 1 315 (21) 1 544 (49) 850 (22) 226 (62)16–17 years 669 (26) 820 (27) 514 (31) 252 (51)

Males18–21 years 570 (29) 531 (32) 458 (32) 199 (53)22–65 years 6 593 (6) 5 157 (6) 5 750 (5) 2 478 (7)Over 65 years 2 712 (11) 1 372 (17) 1 204 (17) 430 (33)

Females18–21 years 138 (58) 269 (51) 333 (39) 233 (51)22–60 years 5 085 (7) 3 936 (8) 5 188 (6) 1 552 (10)Over 60 years 2 243 (13) 1 295 (17) 1 192 (19) 230 (41)

Western NorthernAustralia Tasmania Territory Australia

Subcommercial farms c

Total 5 733 (6) 3 397 (10) 62 (25) 76 243 (3)

Children0–5 years 156 (77) 146 (61) 5 (90) 3 989 (14)6–12 years 644 (25) 509 (33) 5 (90) 9 193 (12)13–15 years 185 (51) 262 (60) – 4 381 (20)16–17 years 283 (35) 132 (59) – 2 670 (14)

Males18–21 years 370 (30) 45 (99) – 2 173 (15)22–65 years 1 910 (7) 1 026 (12) 21 (23) 22 935 (3)Over 65 years 248 (46) 119 (55) 5 (90) 6 090 (8)

Females18–21 years 122 (52) 90 (65) – 1 184 (21)22–60 years 1 534 (9) 877 (13) 21 (23) 18 191 (3)Over 60 years 281 (40) 191 (43) 5 (90) 5 437 (9)

a Covers only one household per farm. b Farms with estimated value of agricultural operations greaterthan $22 500. c Farms with estimated value of agricultural operations between $5000 and $22 500.– Negligible or no persons in this category.Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates.

26 ABARE research report 97.7

survey in 1990-91 indicated an average of 1.35 households per farm onbroadacre and dairy farms with an estimated value of agricultural operationsgreater than $22 500 (Stayner 1995). The principal decision makinghouseholds were larger on average than other farm households, having anaverage of 3.22 persons compared with 2.37 persons in other households.Based on these numbers and on the households in this survey being those ofthe principal decision making households, there were an estimated 573 028people in farm households in 1994-95.

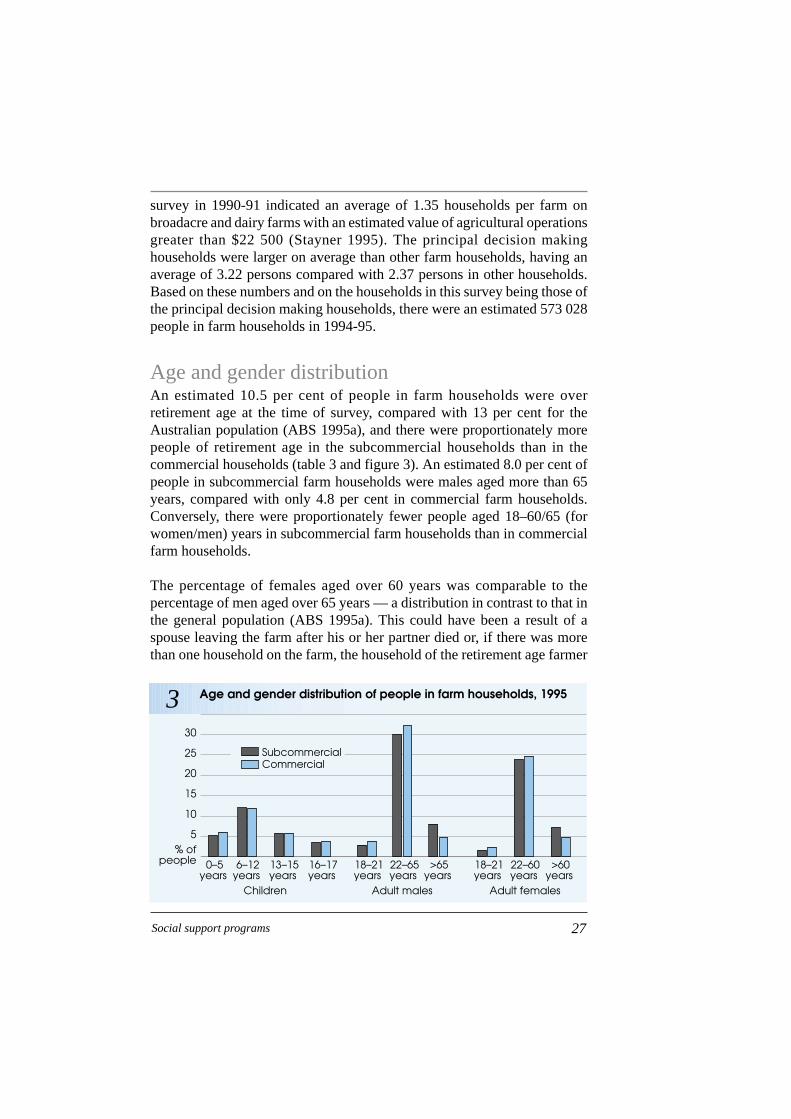

Age and gender distributionAn estimated 10.5 per cent of people in farm households were overretirement age at the time of survey, compared with 13 per cent for theAustralian population (ABS 1995a), and there were proportionately morepeople of retirement age in the subcommercial households than in thecommercial households (table 3 and figure 3). An estimated 8.0 per cent ofpeople in subcommercial farm households were males aged more than 65years, compared with only 4.8 per cent in commercial farm households.Conversely, there were proportionately fewer people aged 18–60/65 (forwomen/men) years in subcommercial farm households than in commercialfarm households.

The percentage of females aged over 60 years was comparable to thepercentage of men aged over 65 years — a distribution in contrast to that inthe general population (ABS 1995a). This could have been a result of aspouse leaving the farm after his or her partner died or, if there was morethan one household on the farm, the household of the retirement age farmer

27Social support programs

3 Age and gender distribution of people in farm households, 1995

% ofpeople

5

20

15

10

25

30

SubcommercialCommercial

>60years

22–60years

18–21years

>65years

22–65years

18–21years

16–17years

13–15years

6–12years

0–5years

Children Adult males Adult females

becoming less important to the farm business, in which case another farmhousehold might have become the principal decision making householdsurveyed.

There were an estimated 10 287 young women and 16 621 young men aged18–21 years living on-farms or away in full time education in 1995 (table 3and figure 3). The large gender difference among this age group in the farmpopulation suggests a substantially larger net migration of young womenfrom farms than of men. This is because the small differences in birth rates,infant mortality rates and child mortality rates between males and femalesin the Australian population tend to balance each other out by mid-adolescence (ABS 1994b).

Employment and education statusAt the time of the interview, an estimated 97 per cent of males aged 22–65years and 79 per cent of females aged 22–60 years were in paid employmenton-farm and/or off-farm (table 4). A further 19 per cent of females and 1 percent of males were employed in home duties. An estimated 1 per cent ofadults aged 22–60 (for women) or 22–65 (for men) years in households wereunemployed. Eleven per cent of 16–17 year olds who were not full timestudents were employed (table 5). Thirty-four per cent of young people aged16–21 years who were not full time students were employed while 4 per centwere unemployed.

The employment status of young men and young women aged 18–21 yearsand living on-farm differed substantially (table 5): 60 per cent of the males

28 ABARE research report 97.7

4 Employment and full time student status of adults, 1995

Males a Females b Total

no. % no. % no. %

Employed c 138 547 (3) 97 (4) 86 968 (1) 79 (2) 225 516 (4) 89 (6)Full time student 1 346 (17) 1 (17) 1250 (17) 1 (17) 2 596 (12) 1 (13)Home duties 1 659 (16) 1 (16) 20 809 (4) 19 (4) 22 468 (4) 9 (6)Unemployed 1 021 (21) 1 (21) 531 (27) 1 (27) 1 553 (17) 1 (17)Other 841 (23) 1 (23) 860 (22) 1 (22) 1 701 (16) 1 (16)

Total 143 414 (3) 100 110 419 (1) 100 253 833 (4) 100

a Aged 22–65 years. b Aged 22–60 years. c Excludes those who were also in full time education orwho were only engaged in home duties.Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates.

29Social support programs

5 Employment and full time student status of young people, 1995 a

All aged 6–17 years Males aged 18–21 years

no. % no. %Employed and not full time student 1 885 (13) 11 (14) 9 936 (4) 60 (6)

Full time student at home– in paid employment 3 399 (9) 20 (10) 1 422 (15) 8 (16)– not in paid employment 8 626 (5) 52 (6) 2 224 (12) 13 (13)

Full time student away from home– in paid employment 406 (31) 2 (31) 451 (30) 3 (30)– not in paid employment 1 921 (13) 12 (14) 1 611 (15) 10 (16)

Unemployed 155 (46) 1 (46) 597 (27) 4 (27)

Other 191 (46) 1 (46) 380 (29) 2 (29)

Total 16 584 (4) 16 621 (4)

Females aged 18–21 years All aged 16–21 years

no. % no. %Employed and not full time student 3 101 (9) 30 (12) 14 923 (4) 34 (6)

Full time student at home– in paid employment 1 468 (15) 14 (17) 6 289 (7) 14 (8)– not in paid employment 1 420 (16) 14 (18) 12 270 (4) 28 (6)

Full time student away from home– in paid employment 660 (24) 6 (25) 1 517 (16) 3 (16)– not in paid employment 2 604 (11) 25 (14) 6 136 (7) 14 (8)

Unemployed 803 (23) 8 (24) 1 555 (17) 4 (17)

Other 230 (39) 2 (39) 801 (21) 2 (21)

Total 10 287 (8) 43 489 (4)

a Employment is all on-farm and/or off-farm work.Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates.

were employed and not in full time education, compared with 30 per centof the females in the same age group. Of the young men and women in thisage group in full time education, more young men were living at home thanwere young women, and proportionately more of these young women wereemployed. Forty-five per cent of all full time students aged 18–21 years wereliving away from home.

An estimated 86 per cent of 16–17 year olds in farm households were in fulltime education, compared with 79 per cent for the same group in the

Australian population (ABS 1995b). Seventy-two per cent of 16–17 yearolds were in full time education and living at home, while 14 per cent werefull time students residing away from home (table 5).

Rural, remote and metropolitan locationsUnder the Rural, Remote and Metropolitan Areas Classification (DPIE andDHSH 1994) remoteness is measured by an index which is a function ofpopulation density and distance to the nearest urban centre in each of fourpopulation size groups. It is assumed that availability of and access to otherpeople and goods and services decreases as remoteness increases. Theclassification of statistical local areas is shown in map A.

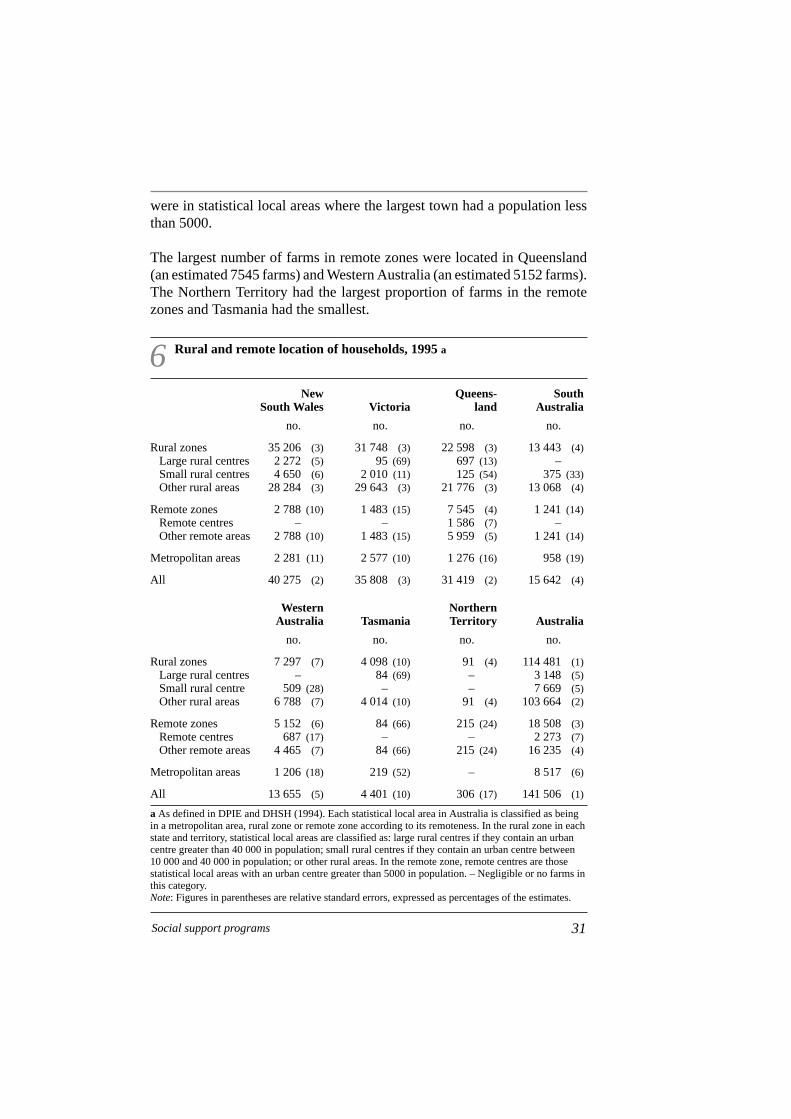

An estimated 81 per cent of farms were in rural zones and 13 per cent werein remote zones, with the remaining 6 per cent in close proximity tometropolitan cities (table 6). Most farms were located a considerabledistance from towns of any substantial size. In rural zones, 91 per cent offarm households were in statistical local areas where the largest town had apopulation less than 10 000. In remote zones, 88 per cent of farm households

30 ABARE research report 97.7

Metropolitan areasLarge rural centresSmall rural centresOther rural areasRemote centresOther remote areas

A Statistical local areas according to rural andremote location a

a 1990-91 census edition. Source: Based on DPIE and DHSH (1994).

6 Rural and remote location of households, 1995 a

New Queens- SouthSouth Wales Victoria land Australia

no. no. no. no.

Rural zones 35 206 (3) 31 748 (3) 22 598 (3) 13 443 (4)Large rural centres 2 272 (5) 95 (69) 697 (13) –Small rural centres 4 650 (6) 2 010 (11) 125 (54) 375 (33)Other rural areas 28 284 (3) 29 643 (3) 21 776 (3) 13 068 (4)

Remote zones 2 788 (10) 1 483 (15) 7 545 (4) 1 241 (14)Remote centres – – 1 586 (7) –Other remote areas 2 788 (10) 1 483 (15) 5 959 (5) 1 241 (14)

Metropolitan areas 2 281 (11) 2 577 (10) 1 276 (16) 958 (19)

All 40 275 (2) 35 808 (3) 31 419 (2) 15 642 (4)

Western NorthernAustralia Tasmania Territory Australia

no. no. no. no.

Rural zones 7 297 (7) 4 098 (10) 91 (4) 114 481 (1)Large rural centres – 84 (69) – 3 148 (5)Small rural centre 509 (28) – – 7 669 (5)Other rural areas 6 788 (7) 4 014 (10) 91 (4) 103 664 (2)

Remote zones 5 152 (6) 84 (66) 215 (24) 18 508 (3)Remote centres 687 (17) – – 2 273 (7)Other remote areas 4 465 (7) 84 (66) 215 (24) 16 235 (4)

Metropolitan areas 1 206 (18) 219 (52) – 8 517 (6)

All 13 655 (5) 4 401 (10) 306 (17) 141 506 (1)

a As defined in DPIE and DHSH (1994). Each statistical local area in Australia is classified as beingin a metropolitan area, rural zone or remote zone according to its remoteness. In the rural zone in eachstate and territory, statistical local areas are classified as: large rural centres if they contain an urbancentre greater than 40 000 in population; small rural centres if they contain an urban centre between10 000 and 40 000 in population; or other rural areas. In the remote zone, remote centres are thosestatistical local areas with an urban centre greater than 5000 in population. – Negligible or no farms inthis category.Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates.

31Social support programs

were in statistical local areas where the largest town had a population lessthan 5000.

The largest number of farms in remote zones were located in Queensland(an estimated 7545 farms) and Western Australia (an estimated 5152 farms).The Northern Territory had the largest proportion of farms in the remotezones and Tasmania had the smallest.

Assets and income profiles and assetsvaluation

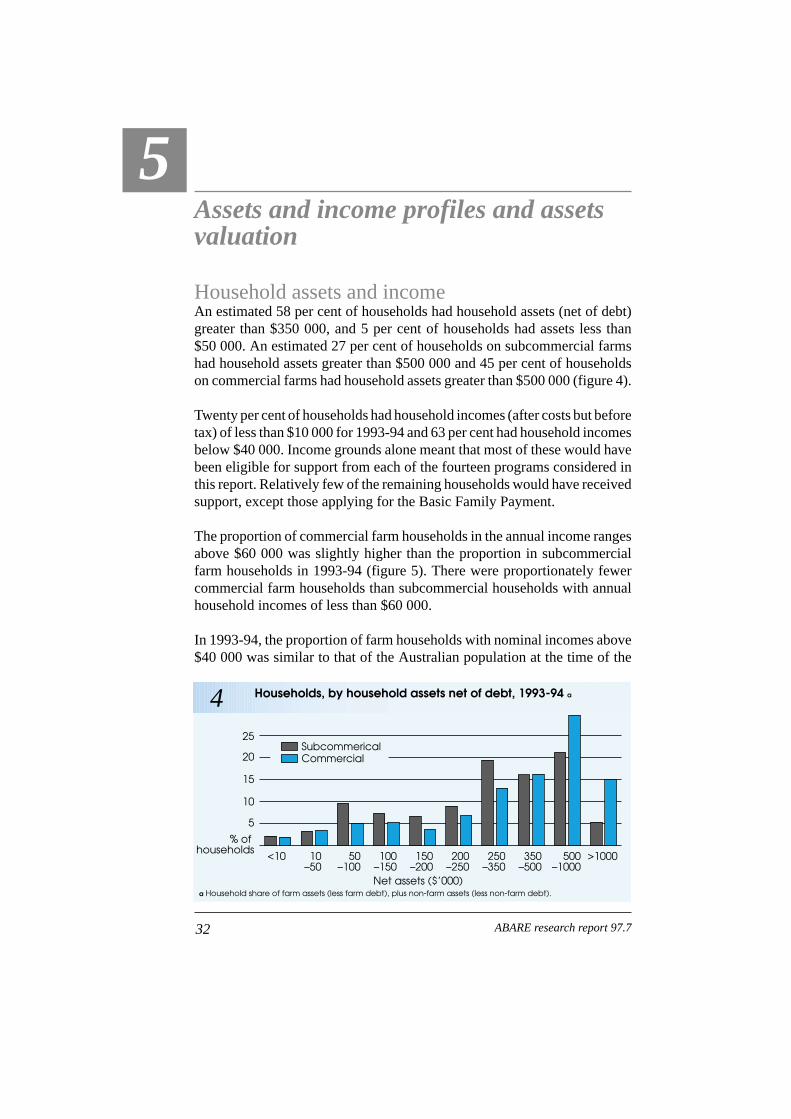

Household assets and incomeAn estimated 58 per cent of households had household assets (net of debt)greater than $350 000, and 5 per cent of households had assets less than$50 000. An estimated 27 per cent of households on subcommercial farmshad household assets greater than $500 000 and 45 per cent of householdson commercial farms had household assets greater than $500 000 (figure 4).

Twenty per cent of households had household incomes (after costs but beforetax) of less than $10 000 for 1993-94 and 63 per cent had household incomesbelow $40 000. Income grounds alone meant that most of these would havebeen eligible for support from each of the fourteen programs considered inthis report. Relatively few of the remaining households would have receivedsupport, except those applying for the Basic Family Payment.

The proportion of commercial farm households in the annual income rangesabove $60 000 was slightly higher than the proportion in subcommercialfarm households in 1993-94 (figure 5). There were proportionately fewercommercial farm households than subcommercial households with annualhousehold incomes of less than $60 000.

In 1993-94, the proportion of farm households with nominal incomes above$40 000 was similar to that of the Australian population at the time of the

32

5

ABARE research report 97.7

a Household share of farm assets (less farm debt), plus non-farm assets (less non-farm debt).

4 Households, by household assets net of debt, 1993-94 a

Net assets ($’000)

<10 10–50

50–100

100–150

150–200

200–250

250–350

350–500

500–1000

>1000

% of households

5

15

10

20

25SubcommericalCommercial

1991 census (table 7). However, there were differences between the pro-portions of the two populations in the lower ranges: 14 per cent of farm house-holds had nominal incomes of less than $5000 and 49 per cent had nominalincomes between $5000 and $40 000, compared with 2 per cent and 63 percent respectively of the whole Australian population.

The response rate on financial items was high given the sensitivity andcomplexity of the questions, and given that the information was collectedby telephone. Only 13 per cent of respondents were unable to providesufficient information to enable calculation of their household assets, and15 per cent were unable to provide sufficient information to enablecalculation of their household income. These respondents were excludedfrom the statistical analysis.

33Social support programs

a Income after costs but before tax.

5 Households, by household income, 1993-94 a

Income ($’000)

>200100–200

60–100

40–60

25–40

15–25

10–15

5–101–5<1% of

households

5

15

10

20SubcommericalCommercial

7 Comparison of farm and Australian household income distribution

Household Percentage of farm Percentage of Australianincome range a households, 1993-94 households, 1991

< $5000 14 (12) 2$5000–40 000 49 (3) 63$40 000–60 000 19 (9) 21$60 000 –100 000 12 (14) 11>$100 000 6 (29) 4

a Nominal income in 1993-94 after costs but before tax for farm households. Nominal income in1991 after superannuation, health insurance and similar deductions but before tax for Australianhouseholds. Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates.Source: ABS (1995c) for Australian data.

Modified household assets andincome for three programs

Modified household assets Household assets minus $150 000 ($150 000 isthe average value of the domestic home of NewSouth Wales farm applicants whose propertieswere referred to the Australian ValuationOffice in 1994-95)

For AUSTUDY Includes only 50 per cent of farm assets

Modified household income Household income minus an allowance based(applies to AUSTUDY only) on the number and age of dependent children

broadly in accordance with Austudy provisions

1