© copyright d hillman 20001 investments in stocks and bonds

Post on 20-Dec-2015

216 views

TRANSCRIPT

© Copyright D Hillman 2000 1

Investments in Investments in Stocks and BondsStocks and Bonds

© Copyright D Hillman 2000 2

Overview of FASB No. 115Overview of FASB No. 115

Requires most investment Requires most investment securities to be valued at marketsecurities to be valued at market

Securities classified into three Securities classified into three categoriescategories

Held-to-maturityHeld-to-maturity– Only debt securities that will be held Only debt securities that will be held

to maturity dateto maturity date

© Copyright D Hillman 2000 3

Overview of FASB No. 115Overview of FASB No. 115

Trading securitiesTrading securities– Debt and equity securities that are Debt and equity securities that are

purchased and sold for short-term purchased and sold for short-term profitsprofits

Available-for-saleAvailable-for-sale– All debt and equity securities not All debt and equity securities not

classified as held-to-maturity or tradingclassified as held-to-maturity or trading

© Copyright D Hillman 2000 4

Short-term InvestmentsShort-term Investments

Readily saleable securitiesReadily saleable securities Management intends to sell within Management intends to sell within

one yearone year All three of FASB 115 categories All three of FASB 115 categories

applyapply

© Copyright D Hillman 2000 5

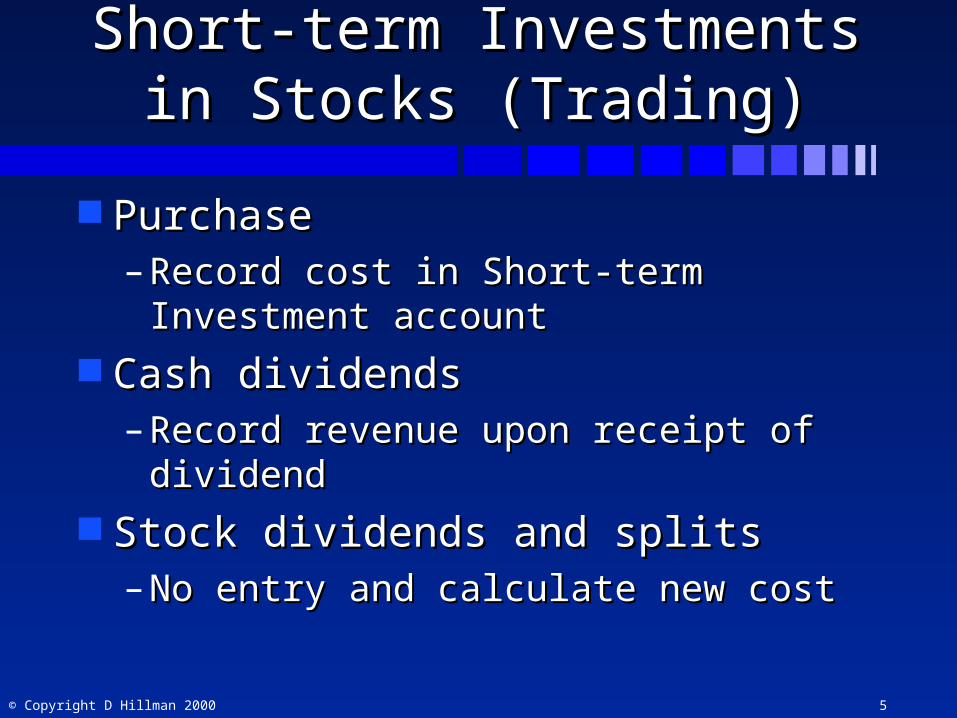

Short-term Investments in Stocks Short-term Investments in Stocks (Trading)(Trading)

PurchasePurchase– Record cost in Short-term Investment Record cost in Short-term Investment

accountaccount Cash dividendsCash dividends

– Record revenue upon receipt of dividendRecord revenue upon receipt of dividend Stock dividends and splitsStock dividends and splits

– No entry and calculate new costNo entry and calculate new cost

© Copyright D Hillman 2000 6

Short-term Investments in Stocks Short-term Investments in Stocks (Trading)(Trading)

SaleSale– Increase Cash for proceedsIncrease Cash for proceeds

– Decrease Investment account by costDecrease Investment account by cost

– Record Realized Gain(Loss) on Record Realized Gain(Loss) on Investment for differenceInvestment for difference

© Copyright D Hillman 2000 7

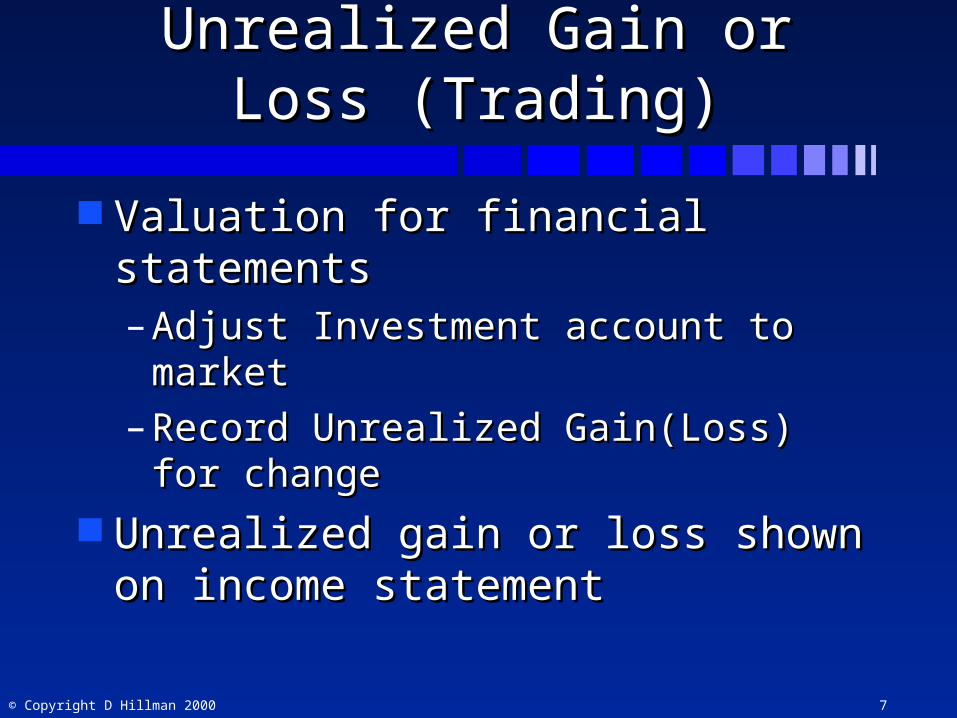

Unrealized Gain or Loss Unrealized Gain or Loss (Trading)(Trading)

Valuation for financial statementsValuation for financial statements– Adjust Investment account to marketAdjust Investment account to market

– Record Unrealized Gain(Loss) for Record Unrealized Gain(Loss) for changechange

Unrealized gain or loss shown on Unrealized gain or loss shown on income statementincome statement

© Copyright D Hillman 2000 8

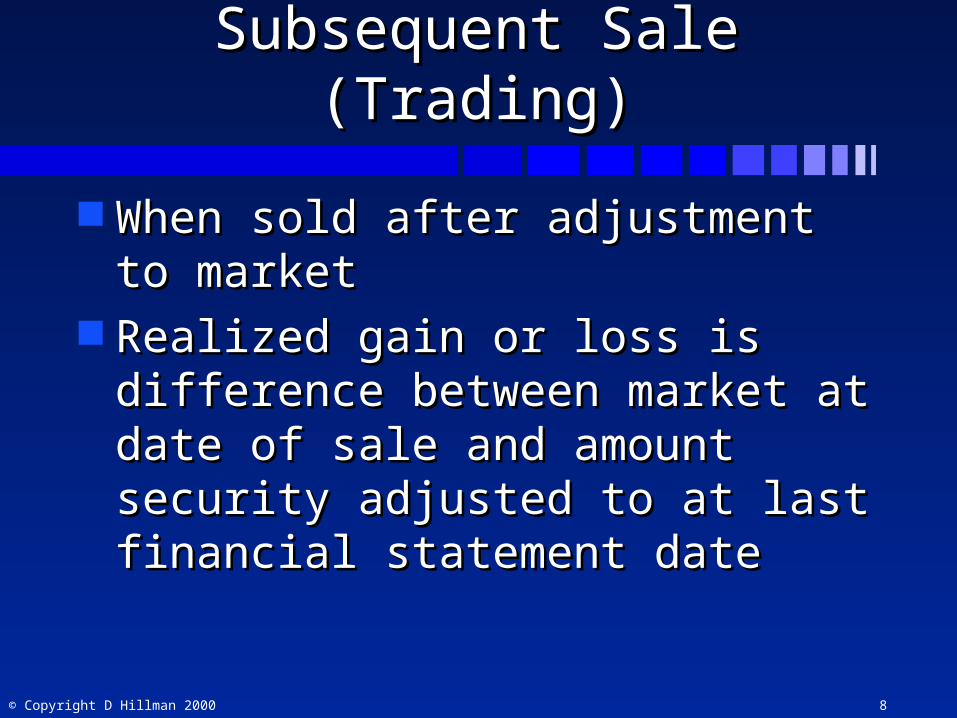

Subsequent Sale (Trading)Subsequent Sale (Trading)

When sold after adjustment to When sold after adjustment to marketmarket

Realized gain or loss is difference Realized gain or loss is difference between market at date of sale and between market at date of sale and amount security adjusted to at last amount security adjusted to at last financial statement datefinancial statement date

© Copyright D Hillman 2000 9

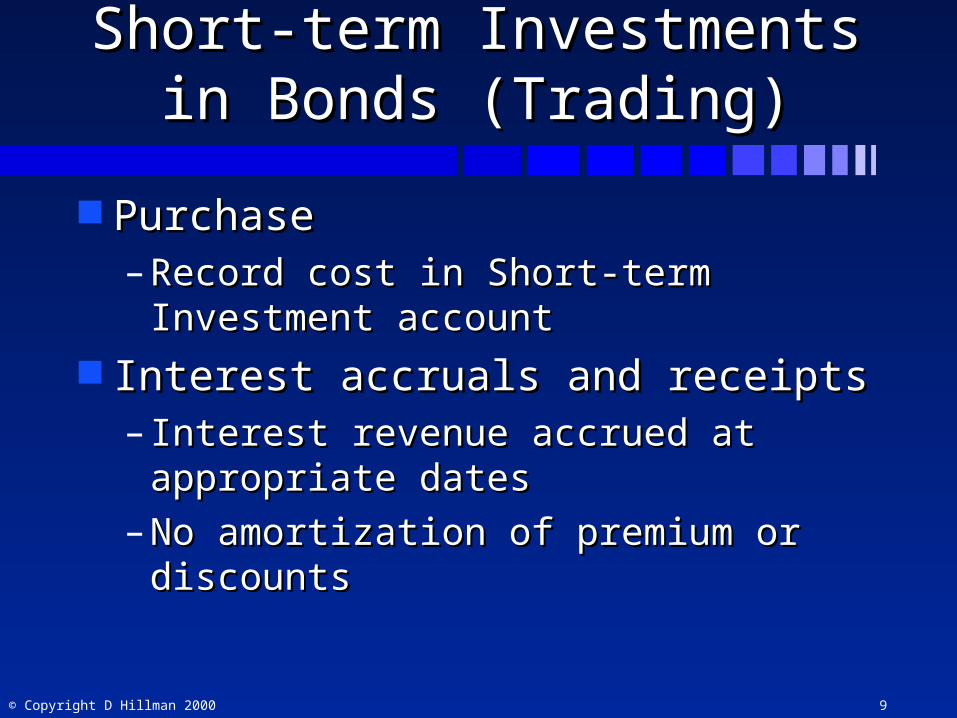

Short-term Investments in Bonds Short-term Investments in Bonds (Trading)(Trading)

PurchasePurchase– Record cost in Short-term Investment Record cost in Short-term Investment

accountaccount Interest accruals and receiptsInterest accruals and receipts

– Interest revenue accrued at appropriate Interest revenue accrued at appropriate datesdates

– No amortization of premium or discountsNo amortization of premium or discounts

© Copyright D Hillman 2000 10

Short-term Investments in Bonds Short-term Investments in Bonds (Trading)(Trading)

SaleSale– Increase Cash for proceedsIncrease Cash for proceeds

– Accrue interest revenue to date of Accrue interest revenue to date of salesale

– Decrease Investment account by costDecrease Investment account by cost

– Record Realized Gain(Loss) on Record Realized Gain(Loss) on Investment for differenceInvestment for difference

© Copyright D Hillman 2000 11

Unrealized Gain or Loss Unrealized Gain or Loss (Trading)(Trading)

Valuation for financial statementsValuation for financial statements– Adjust Investment account to marketAdjust Investment account to market

– Record Unrealized Gain(Loss) for Record Unrealized Gain(Loss) for changechange

Unrealized gain or loss shown on Unrealized gain or loss shown on income statementincome statement

© Copyright D Hillman 2000 12

Subsequent Sale (Trading)Subsequent Sale (Trading)

When sold after adjustment to When sold after adjustment to marketmarket

Realized gain or loss is difference Realized gain or loss is difference between market at date of sale and between market at date of sale and amount security adjusted to at last amount security adjusted to at last financial statement datefinancial statement date

© Copyright D Hillman 2000 13

Investments in Investments in Available-For-Sale SecuritiesAvailable-For-Sale Securities

Acquired as short-term or long-term Acquired as short-term or long-term investmentinvestment

When available-for-sale bonds held When available-for-sale bonds held as long-term, premium or discount as long-term, premium or discount should be amortized as adjustment should be amortized as adjustment to interest revenueto interest revenue

© Copyright D Hillman 2000 14

Investments in Investments in Available-For-Sale SecuritiesAvailable-For-Sale Securities

Accounting similar to trading except:Accounting similar to trading except: Unrealized gains or losses reported as a Unrealized gains or losses reported as a

separate component of stockholders’ separate component of stockholders’ equityequity

When sold, realized gain or loss is When sold, realized gain or loss is difference between proceeds and difference between proceeds and original costoriginal cost– Unrealized gain or loss closedUnrealized gain or loss closed

© Copyright D Hillman 2000 15

Long-term Investments in StocksLong-term Investments in Stocks

Own less than Own less than 20% of voting 20% of voting stockstock

Own 20-50% of Own 20-50% of voting stockvoting stock

Own more than Own more than 50% of voting 50% of voting stockstock

Market value Market value methodmethod

Equity methodEquity method

Prepare Prepare consolidated consolidated statementsstatements

© Copyright D Hillman 2000 16

Equity Method of AccountingEquity Method of Accounting

Investment initially recorded at costInvestment initially recorded at cost Receipt of dividendsReceipt of dividends

– Reduces investment accountReduces investment account

– No revenueNo revenue

© Copyright D Hillman 2000 17

Equity Method of AccountingEquity Method of Accounting

Investee reported incomeInvestee reported income– Increase Investment by investor’s shareIncrease Investment by investor’s share

– Report share of investee income as Report share of investee income as incomeincome

Investee reported lossInvestee reported loss– Decrease Investment by shareDecrease Investment by share

– Report share as lossReport share as loss

© Copyright D Hillman 2000 18

Investment in Bonds Investment in Bonds Held-to-MaturityHeld-to-Maturity

FASB 115FASB 115 states must not be any states must not be any foreseeable intent to sell bonds foreseeable intent to sell bonds before maturity datebefore maturity date

Accounting is mirror image of Accounting is mirror image of accounting for long-term debtaccounting for long-term debt

Reported in financial statements at Reported in financial statements at amortized costamortized cost

© Copyright D Hillman 2000 19

Analyzing InformationAnalyzing Information

What is overall percent of total What is overall percent of total assets invested in current and assets invested in current and noncurrent securities?noncurrent securities?

What is mix of trading, available-What is mix of trading, available-for-sale, and held-to-maturity for-sale, and held-to-maturity investments?investments?

© Copyright D Hillman 2000 20

Analyzing InformationAnalyzing Information

Has company been successful in Has company been successful in generating additional income from generating additional income from investments?investments?

How does current market value and How does current market value and cost compare?cost compare?

Is there good range of maturity Is there good range of maturity dates?dates?

© Copyright D Hillman 2000 21

Analyzing InformationAnalyzing Information

If equity securities accounted for If equity securities accounted for using equity methodusing equity method– does significant influence exist?does significant influence exist?

– how much of share of income has how much of share of income has been received as dividends?been received as dividends?