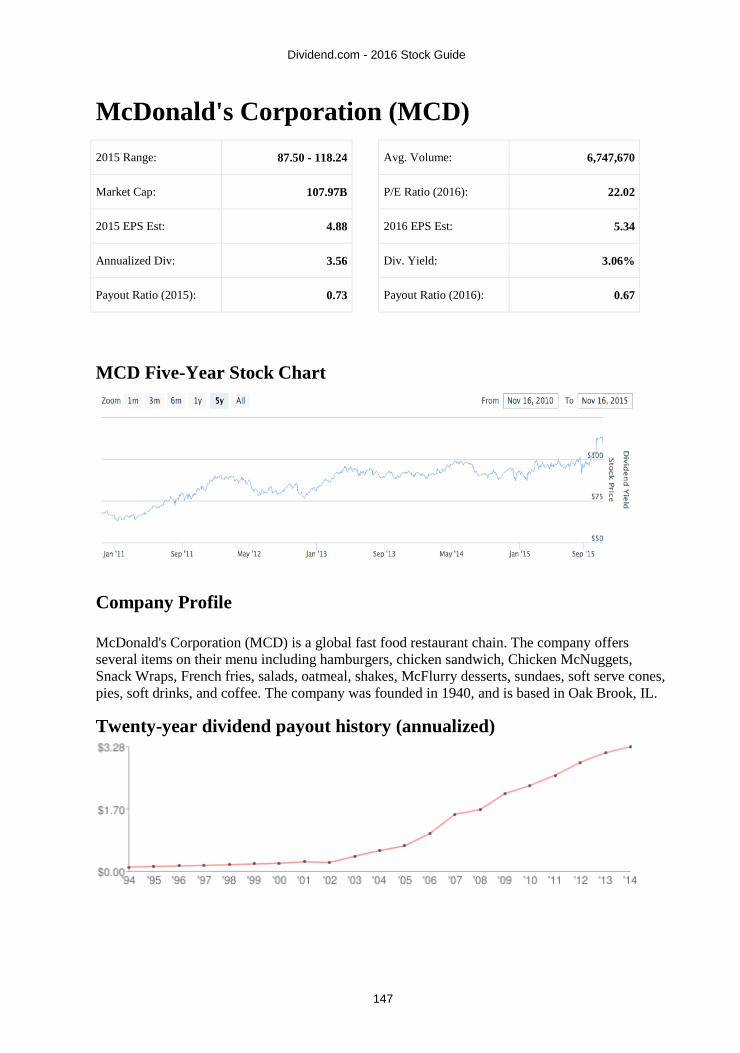

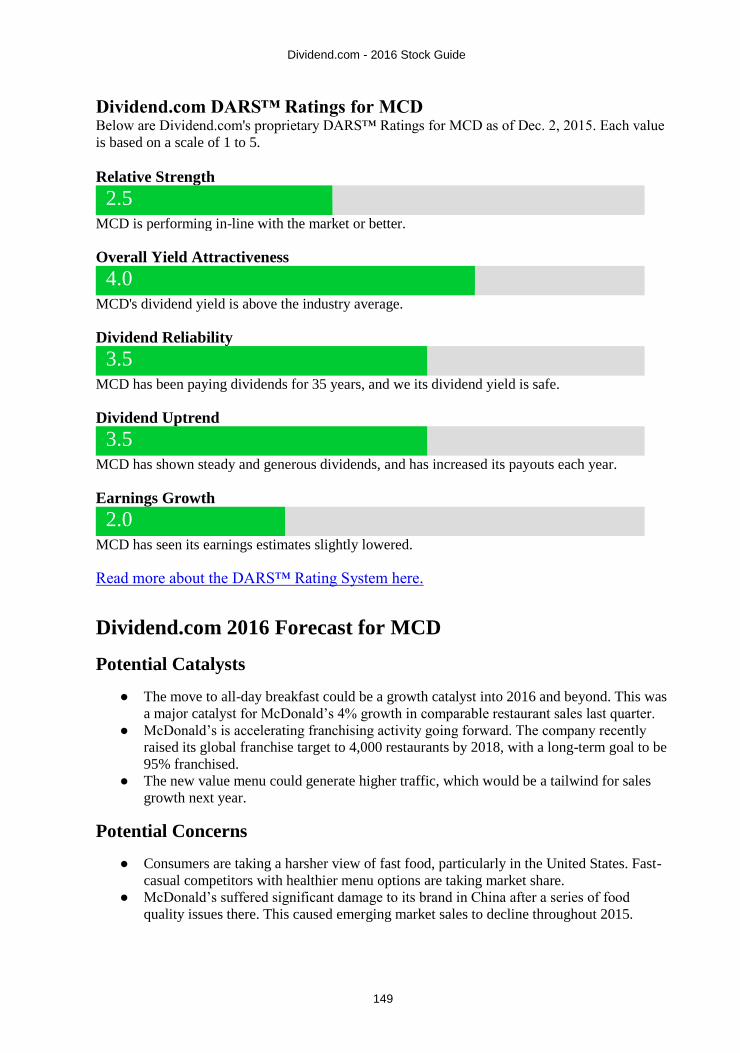

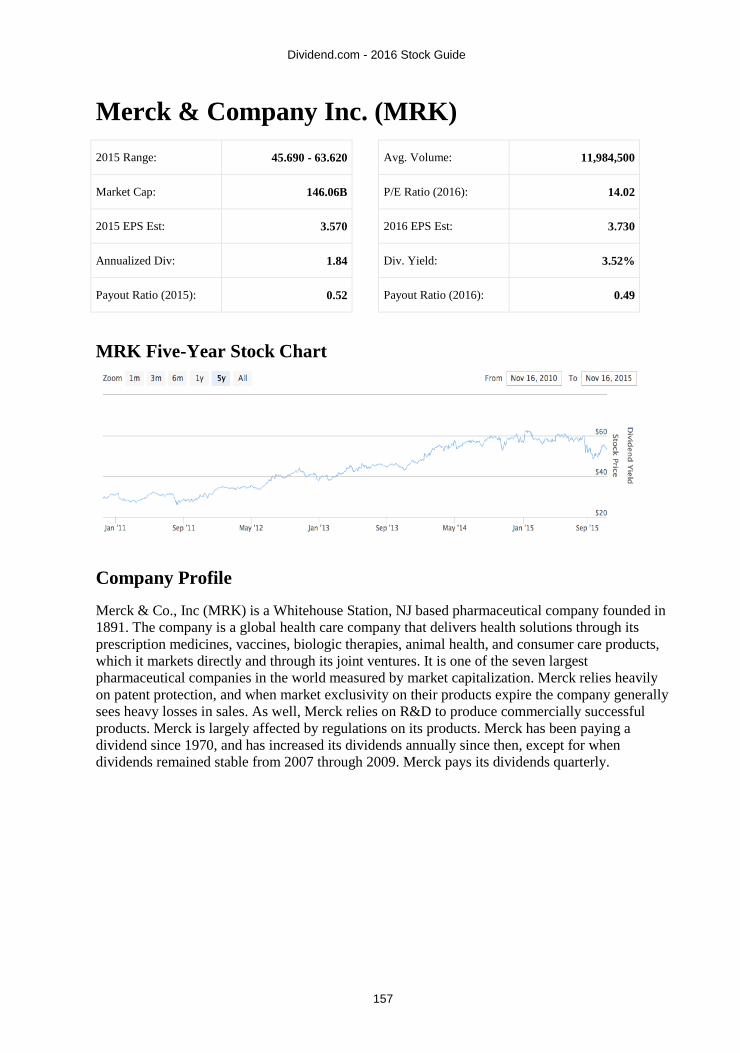

dividend.com - 2016 stock guide - amazon s3 - 2016 stock guide 6 even more dividends and buybacks we...

TRANSCRIPT

1

Dividend.com - 2016 Stock Guide

2

Table of Contents

Introduction 3-4

2015 Review 5-7

2016 Preview 8 -12

Stock-by-Stock Previews 13-226

Dividend.com - 2016 Stock Guide

3

INTRODUCTION

This eBook serves as an investing guide and economic forecast for dividend-minded

investors. In the following pages, we’ll examine the important issues facing both investors

and specific dividend-paying stocks in the coming year.

Despite a dramatic and frightening 11% drop in August, the stock market (as measured

by the S&P 500 Index) ended 2015 just about where it was when the year began.

After a choppy start in January—and a shift to a slightly higher trading plateau in the

spring and early summer—the markets plunged in response to sharp stock declines in

China, and then recovered in the year’s final quarter. Following an 11.4% gain in 2014

and an almost 30% gain in 2013, the market’s go-nowhere 2015 performance was

disappointing. Treasuries as measured by 10-year bonds also were essentially flat. But

considering mounting fears of a global recession and worries over the effects of higher

interest rates, many investors were thankful for a year in which financial markets had no

particular color rather than one that left their portfolios bright red.

Driving markets during the year were two key issues: the health of China (the world’s

second largest economy) and the future of interest rates.

Few Western analysts trust the accuracy of China’s official economic statistics—so what

they see with their own eyes has them concerned. Having built a huge manufacturing

engine largely on credit, which also fueled massive investments in real estate, China now

is burdened by debt. To service the debt, the country must keep up its furious export

pace, even if that means cutting prices—and that pricing pressure, in a world glutted with

goods, keeps driving commodity prices lower.

The price of Dr. Copper (so named because price movements of the widely used metal

have reliably forecast global economic shifts) were off almost 30% in 2015, after a fifth

year of declines in 2014. Other commodities came down too.

Oil prices were the biggest movers, down 40% to the delight of drivers and to the dismay

of energy producers, especially the highly leveraged ones. The broad Bloomberg

Commodity Index was off more than 20% for the year. While the pace of decline

probably won’t continue in 2016, there are few signs of an imminent turnaround.

On the interest-rate front, repeated signals throughout the year from the Federal Reserve

that a modest hike was likely as long as employment and other signs of economic health

continued to improve seemed to serve as a kind of inoculation against shock—there was

little immediate reaction once the Fed eventually pulled the trigger in mid-December. By

that time, analysts had already moved on to concerns about the timing and size of

subsequent rate hikes.

As the year drew to a close, uncertainty abounded on many fronts: Will the European

Central Bank’s increased monetary easing—a move at odds with Fed tightening—spur

Eurozone growth, attract more investment to the U.S. and drive the dollar even higher, or

Dividend.com - 2016 Stock Guide

4

both? Will the U.S. economy continue to recover or slump in the face of worldwide

deflationary trends? How will the 2016 elections shape markets and the economy?

As we have done in the past, we will look into the economic crystal ball for 2016 from

the perspective of what may go right and what may go wrong. We will then provide our

own view of these potential factors, aware that a multitude of factors could influence

outcomes. We hope this analysis—followed by similar upside and downside previews for

several dozen of the biggest-name dividend stocks in the world—helps you invest

successfully in 2016.

And please keep in mind that the scenarios that follow are possibilities, not predictions.

Dividend.com - 2016 Stock Guide

5

A Look Back At 2015

Before looking ahead, let’s review some of the scenarios laid out in last year’s dividend

guide—a process that will add perspective to our 2016 outlook. First, a retrospective on some

of our optimistic scenarios, then we’ll look at some of the things we thought might go wrong.

Things We Hoped Would Go Right

Continued Unwinding Of Commodities Even after more than three years of declining commodity prices, our year-end 2014 outlook

for the coming year said that commodities would like fall further (possibly much further) as a

great unwinding continued into 2015—the call was right on target.

At the top of the commodity pyramid stands gold, which peaked at $1,921.50 an ounce in

September 2011 and has been riding a downward roller coaster since. It ended 2014 at

$1,188.20 an ounce and was trading at about $1,080 by the time 2015 came to close, a

decline of almost 9%. The drop in the price of oil, which hit $147.27 per barrel in July 2008,

has been even steeper as a result of the astonishing success of new U.S. production. From

roughly $75 per barrel at the end of 2014, the next 12 months saw oil prices fall to $40.

Rounding out the most prominent commodities, copper also continued to sink, down to a few

pennies above $2 a pound, down from its peak near $4.70 in February 2011, and its year-end

2014 price of near $3.

Since commodities traditionally have moved inversely to equities, we were expecting that

lower commodity prices would have a tonic effect on stocks. On that score, we were half

right.

A Booming M&A Market Just as 2014 saw considerable merger and acquisition activity in tobacco, energy,

broadcasting, telecom, tech, biotech, spirits and more, we anticipated that 2015 would be

another big year for M&A—especially in technology and energy, as interest rates remained

low and activist investors demanded greater returns. We were more than right; the year

turned out to be a record for mergers and acquisitions, with deal volume approaching $1.7

trillion. Some of the largest and most notable deals included the merger of Charter

Communications Inc. (CHTR) and Time Warner Cable Inc. (TWC); The Kraft Heinz Co.

(KHC), which combined two giant food companies; the merger of insurance goliaths ACE

Limited (ACE) and The Chubb Corp. (CB); and Dell’s offer for EMC Corp. (EMC).

More IPOs

After a very strong market for initial public offerings in 2014, we felt that market conditions

in 2015 would be ripe for many more companies to make the move. Conditions were good,

and about 230 companies went public during the year—but that was below the blizzard of

364 IPOs in 2014, a recent record, and lower than the 256 of 2013. The less-than-exciting

trajectory of the stock market in 2015, and the sharp correction in August, probably

contributed to the subdued number of newcomers.

Dividend.com - 2016 Stock Guide

6

Even More Dividends And Buybacks We risk self-injury in patting ourselves on the back for this call—U.S. corporations spent a

record $1 trillion on dividends and buybacks in 2015. Prodded into returning more to

shareholders by activist investors such as Carl Icahn, Bill Ackman and Nelson Peltz,

corporate managers are also serving their own ends by buying back company shares to push

up the price of remaining shares and their own share-price dependent compensation—this is

where ordinary shareholders benefit along with the top guys.

Global QE Hits A Crescendo Last year, we said that quantitative easing by the world’s central banks would continue

because: a) central bankers believe more liquidity is the miracle pill for every sick economy;

b) they’re so committed to QE that they have no choice but to convince themselves that the

process works and that it is good for everyone; and c) to believe otherwise, or to question the

long-term ramifications of their practices, is all but forbidden at this point. While the Fed

took its foot off the gas in 2015, their European counterparts stomped down even harder,

driving interest rates further into negative territory. The big money wheels kept on rolling.

Things We Thought Could Go Wrong

The Housing Market Plunges We thought that stagnant household income and weak wage growth would keep the housing

market cool in 2015. In fact, the housing market slogged along in the same way that the

economy slowly and modestly improved. Sales of existing homes continued to improve each

month, while new home sales were up very modestly for the year. The outlook, however, is

optimistic rather than gloomy: In October, a builder sentiment index from the National

Association of Home Builders rose to a 10-year high.

Valuations Finally Come Under Scrutiny Is the market overvalued? We worried about that all through 2013 and 2014, when the price-

to-revenue ratio of the S&P 500 climbed to a record 1.81 toward the end of the year.

Guess what? As 2015 drew to a close, the ratio was still in the 1.8 area, so market

participants clearly were not especially concerned. Since valuations are based on emotions,

which can turn on a dime, what investors are willing to pay for stock may change in 2016—

and then again, it may not.

A New Cold War Freezes The Markets Looking ahead to 2015 last year, the belligerency and aggressiveness of Russian president

Vladimir Putin seemed like a wildcard. Anything from war to energy disruptions to organized

computer hacking seemed possible with the Russian strong man at the helm. There was no

discernable market fallout from the Russian sabre rattling last year, not that conditions have

devolved into a 21st century cold war, but the West is still keeping a wary eye on the Eastern

front.

Another Recession Rocks The Markets

Dividend.com - 2016 Stock Guide

7

Whew! Our lumbering recovery may not be the economic revival of our dreams, but it sure

beats the Almost Depression of 2008-2009, or even a garden variety recession. Thank

goodness that 2015 was a year of slow growth, not negative growth, and that our economic

nightmares remained a dream. But one additional year without a recession only means that

the next inevitable downturn is one year closer. Caution and preparation are warranted more

than ever.

Dividend.com - 2016 Stock Guide

8

Looking Ahead To 2016

Things We Hope Will Go Right

The Economy Continues On Its Low-Growth Path

There’s no law that says recessions are inevitable—but history has shown that they recur

periodically for a variety of reasons, typically every several years. The last one, of course,

was the December 2007 to June 2009 doozy that has come to be known as the Great

Recession when the economy shrank by 4.3%. The National Bureau of Economic Research

(the official record keeper and identifier of recessions) says the two previous recessions

occurred between March and November 2001, when GDP declined by 0.3%, and from July

1990 to March 1991, when it declined by 1.4%. So as we proceed into the seventh year of

recovery, the likelihood of a recession increases.

In the past, inventory accumulation and tighter monetary policy were often seen as the major

causes of slowdowns. Today, information technology has radically reduced the potential for

inventory problems. Concerns over the recessionary consequences of tighter money was the

chief reason the Federal Reserve deliberated for so long in its decision to raise interest rates.

Those concerns remain, but there are several factors suggesting that our current economic

expansion will continue.

First, the absolute level of interest rates, even if the Fed acts a few times, is still

extraordinarily low by historical standards. While it’s true that the size of marginal increases

is significant, the absolute rate of interest is hugely important too, as in a case where the Fed

would raise rates 25% to 1.25% from 1%—a huge percentage hike, but one that kept rates at

a very low level. Even if rates move somewhat higher, our current low-interest rate

environment is likely to continue due to international economic forces, and low rates are a

traditional driver of economic expansion.

Second, consumers appear to be on a better footing. Employment figures continue to

improve, and while much of the gains from the current recovery have gone to the wealthy,

people across the income spectrum seem more disposed to spend.

While countervailing economic forces—including a slowdown in China and weakened global

demand—could tip the scales toward recession, we believe there is a good chance the

domestic economy will continue to lumber along.

The Stock Market Muddles Along If the economy continues to expand slowly, we believe the stock market could follow the

same route. To be sure, as we saw in 2015, volatility can be part of an essentially flat

performance picture; therefore, even if stock prices aren’t much higher a year from now,

there could well be times we reach for the Dramamine.

Those who say the market has little room to rise point to its overvaluation. According to one

important measure—the Cyclically Adjusted Price Earnings Ratio, or P/E10, which measures

current prices against the 10-year average of inflation-adjusted earnings—the market is

priced above its historic average at roughly 26 times adjusted earnings versus the long-term

Dividend.com - 2016 Stock Guide

9

P/E10 average of 16.6. But, current levels are far below the P/E10 peaks of 44.2 before the

dotcom crash in 2000 and the 32.6 level before the 1929 debacle. If corporate earnings

continue to rise the ratio would decline at current price levels, which would continue to make

the market a bit more expensive than average—but not excessively so, supporting the case

for okay, if not spectacular, market performance.

Bi-Partisan Agreement On Lowering Corporate Tax Rates Just as the Citigroup-Travelers merger in 1998 forced Congress into repealing the Glass-

Steagall Act, the 2015 Pfizer-Allergan merger cum tax inversion may be the trigger that sets

off a change in the corporate tax rate. Outrage over the $160 billion merger (in which

Allergan technically takes over Pfizer so that the surviving entity—which presto, change-o

becomes Pfizer again—is domiciled in Ireland) could well prompt an adjustment in the U.S.

corporate income tax rate, which can be as high as 39%. That’s the highest level in the

developed world and a reason that many U.S. companies are looking to leave the U.S.

Avoiding such high taxation is the reason that American companies have parked more than

$2 trillion overseas, which could be used for domestic investment if the tax climate changed.

If a lower corporate tax rate can be spun as a jobs creation measure—rather than as a

giveaway to large corporations (which merely pass along the tax to customers in the form of

higher prices anyway)—it’s possible that sufficient bipartisan support could exist for a

change in the tax law that would address an issue that troubles both sides of the aisle.

Small M&A Deals Continue While huge mergers and acquisitions dominate the headlines, lots of small- and medium-size

deals are going on under the media radar. These acquisitions are quietly transforming the

large American corporations that constitute the dividend-paying universe for a reason cynical

yet simple: Big companies are great at many things these days (including paying dividends),

but aside from the pharmaceutical and software/internet giants, they aren’t especially

innovative. Largely because of their bureaucracy, politics, short-term outlook and avoidance

of risk, big companies aren’t likely to come up with disruptive new products that will

dramatically increase revenue or create processes that encourage revenue growth.

Fortunately, they have the money to buy what they know they can’t create. And buying

smaller companies that have developed new products and processes is a lot easier than

creating those innovations from scratch.

While the record $3.7 trillion value of global M&A in 2015 was due largely to the size of the

year’s several mammoth transactions, it also included numerous smaller deals. These are

likely to continue in 2016 if the economy continues to grow modestly and interest rates stay

low, even if rising a bit. The acquisitions can continue to fuel the growth that large

companies require to continue paying dividends.

Dividends Continue Even if dividends and buybacks in 2016 do not reach the record $1 trillion spent in 2015, the

corporate community’s strong emphasis on rewarding shareholders is unlikely to abate as

activist investors continue to prod management to share some of the estimated $1.8 trillion in

cash on corporate balance sheets. Corporate management’s use of buybacks to put a glow on

Dividend.com - 2016 Stock Guide

10

modest or non-existent earnings-per-share growth—and boost their own compensation—isn’t

likely to stop either.

The big question mark will be earnings. In 2015, earnings and sales growth were essentially

flat. If the economy continues to expand, stock prices, and dividends, should rise modestly as

well. Barring a recession, all signs point to a continuation of the strong dividend-paying

trend.

Slightly Higher Rates Actually Help Economy While the Fed moves to raise interest rates traditionally seen as an economic depressant—

“removing the punch bowl just as the party gets going,” in the words of the late Federal

Reserve Chairman William McChesney Martin—this time around higher rates actually may

have a salutary effect on the economy and the stock market.

For one, after carefully taking the temperature of the economy for so long before raising

rates, the Fed’s move is a very strong vote of confidence in the underlying strength of the

recovery. That alone should add to optimism.

Second, greater economic confidence and concerns that rates are going up would prompt

many would-be home buyers to act rather than wait. Greater real estate activity would serve

as another economic driver.

Third, and equally important, higher rates would reward savers and take pressure off retirees

living off their savings. Confident of higher income (even if modest), savers would likely

increase their spending, which would add another economic spur.

Things We Worry May Go Wrong

Housing Markets Stumble If rates rise even slightly, the level of income needed to support mortgage payments will rise,

which could make a home purchase impossible for those with stagnant incomes. Higher rates

could also make mortgage lenders even more skittish and demanding than they are now,

which would add to the inability of many would-be buyers to purchase a home.

Another factor that could shift the demand-supply balance for housing includes the

possibility that institutional owners of single-family homes—including the hedge funds and

others that bought hundreds of thousands of homes at depressed prices over the last five

years—could decide to cash out and take their profits.

Finally, since the greatest housing demand generally arises from young couples seeking their

own space to raise a family, the $1 trillion level of student debt—largely among Millennials

in their prime home-buying years—could act as an overwhelming retardant to home

purchases.

Aside from demand in certain red-hot markets such as San Francisco and New York City,

these factors could cause a lull or a slowdown in housing.

Dividend.com - 2016 Stock Guide

11

The High-Yield Market Tanks

The long-term low interest rate environment has driven many investors to the high-yield

bond market. Corporations and securities firms responded to demand by issuing more high-

yield debt—now totaling $2.2 trillion, up by almost $1 trillion over the last five years.

Energy and metals and mining companies account for more than a quarter of that debt, and

those companies are in trouble due to the falling price of oil and other commodities. As the

decline continues, it’s possible that the high-yield default rate (now about 3% and low by

historic standards) may rise. Should that happen, confidence in the market could decline and

sell-off pressures could increase.

According to analysis by UBS, more than a third of the outstanding U.S. high-yield and

leveraged loan universe is “at risk” because issuers may not be able to refinance when the

debt matures because of higher rates and poor cash flow generation. A downturn in the high-

yield market could ricochet through the economy, frightening investors and spreading doubt

about the strength of the recovery.

Terrorism Strikes At Economic Nerve Centers By its very nature, terrorism of the kind that struck Paris and San Bernardino, California at

the end of 2015 is irrational and almost impossible to predict. While the loss of life in these

horrible attacks has been tragic, the direct economic impact of terrorism has been slim aside

from its chilling effect on tourism. That may change.

While we are taking security steps to protect our national economic resources, we remain

vulnerable to terror attacks on vital points of our financial, energy and communications

infrastructure. In his recent book, “Lights Out,” former ABC News anchor Ted Koppel says

that a major cyberattack on the nation’s power grid is not only possible but likely, and that

such an attack would be devastating. He also believes that the evidence points to our

unpreparedness for such an attack.

Should terrorists strike a strategically important nerve center in 2016, the effect on the

national economy and our economic confidence could be enormous.

Global Trade Slumps In the wake of China’s economic problems, world trade tumbled in 2015. Conditions are

right for the slump to continue and possibly worsen in 2016.

Demand for dry bulk shipping (which shrunk 2% to 3% in 2015) is likely to shrink by the

same amount in 2016, say maritime experts, and losses and bankruptcies are already hitting

the global shipping industry. On the higher end of the value chain, air cargo shipments

declined by about 2% in 2015 as well, and the 2016 outlook among specialists in that area

indicate that it too is likely to suffer from a decline in global trade.

If the current declines and persistent weakness in China reinforce the trend, the global trading

decline could become a prominent issue in 2016 and lead to a variety of negative

consequences.

Major Infrastructure Failure

Dividend.com - 2016 Stock Guide

12

The deterioration of the nation’s roads, rails, airports, dams and energy distribution systems

is not news. It’s been discussed ad nauseam; yet, little has been done to address the issue,

which costs the nation untold billions in lost productivity and wasted fuel.

Roadway collapses—such as the I-35 disaster in Minneapolis and rail failures such as the

Amtrak derailment in Philadelphia—have resulted in deaths and short-term dislocations. But

the visible economic impact of these disasters has been negligible. A major infrastructure

failure at a key hub in our national transportation or electrical system, however, could have a

devastating impact. Damage to the Amtrak tunnel between New York and New Jersey, for

example, could cripple the economy of the Northeast corridor. On-going system failures at

airports in Chicago, Atlanta or Dallas could paralyze national air transport.

Luckily, the nation has been spared the worst consequences of its infrastructure neglect. It

may not be so lucky in 2016.

Dividend.com - 2016 Stock Guide

13

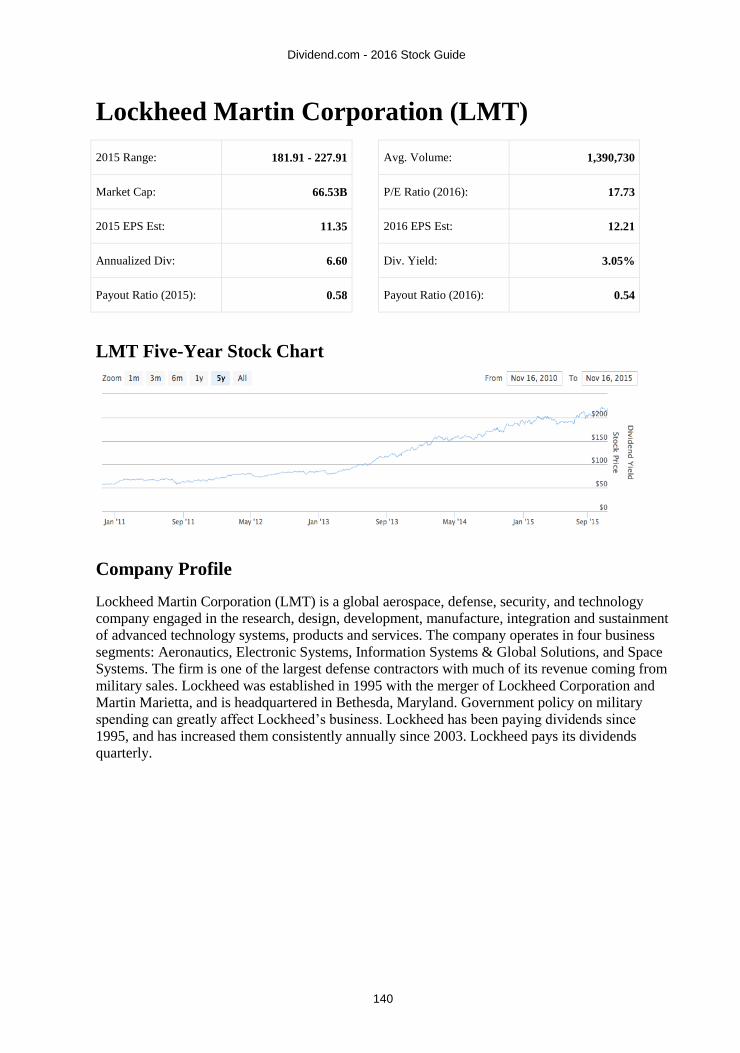

AbbVie, Inc. (ABBV)

2015 Range: 45.45 - 71.60

Avg. Volume: 10,252,700

Market Cap: 91.69B

P/E Ratio (2016): 11.22

2015 EPS Est: 4.28

2016 EPS Est: 5.00

Annualized Div: 2.28

Div. Yield: 4.11%

Payout Ratio (2015): 0.53

Payout Ratio (2016): 0.46

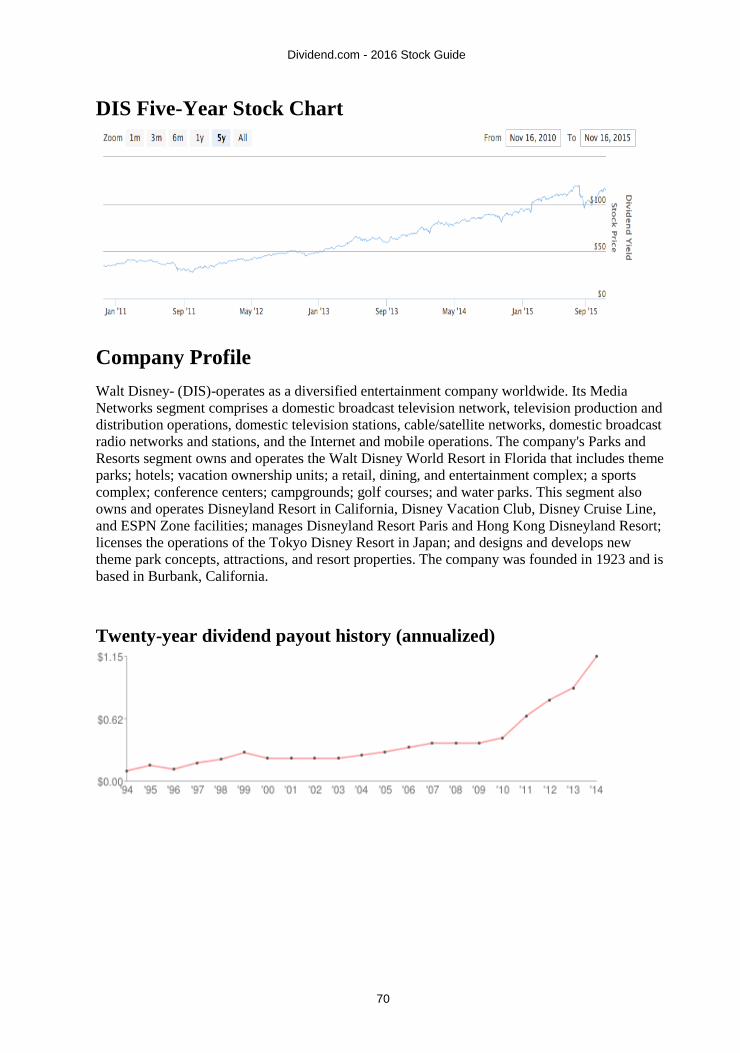

ABBV Five-Year Stock Chart

Company Profile

Abbvie, Inc. (ABBV) is a maker of pharmaceutical products. Its product line includes treatments

for health conditions such as rheumatoid arthritis, psoriasis, Crohn's disease, HIV, low

testosterone, thyroid disease, Parkinson's disease, and many others. The company is

headquartered in North Chicago, Illinois and was spun off from Abbott Laboratories (ABT) in

January 2013.

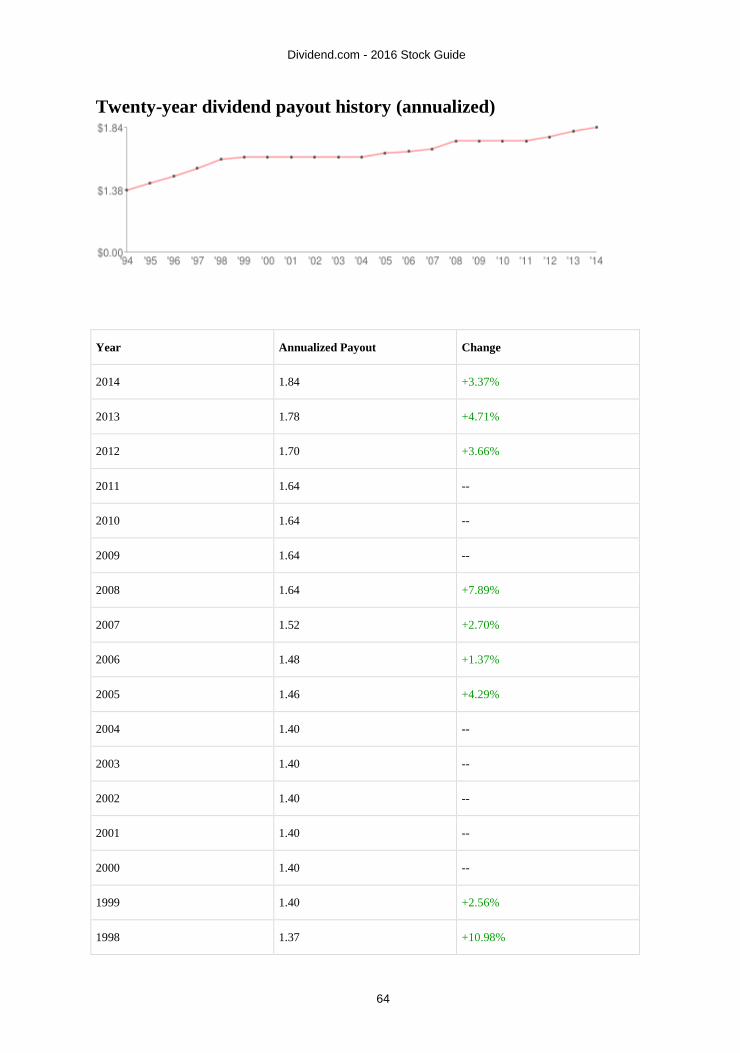

Twenty-year dividend payout history (annualized)

Dividend.com - 2016 Stock Guide

14

Year Annualized Payout Change

2014 1.66 +3.75%

2013 1.60 --

Dividend.com DARS™ Ratings for ABBV

Below are Dividend.com's proprietary DARS™ Ratings for ABBV as of Dec. 2, 2015. Each

value is based on a scale of 1 to 5.

Relative Strength

3.0

ABBV is performing in-line with the market or better.

Overall Yield Attractiveness

3.5

ABBV's dividend yield is above the industry average.

Dividend Reliability

4.5

ABBV has been paying dividends for 2011 years, and we feel its dividend yield is extremely

safe.

Dividend Uptrend

3.5

ABBV has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

ABBV's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com - 2016 Stock Guide

15

Dividend.com 2016 Forecast for ABBV

Potential Catalysts

● As a major healthcare company, Abbvie is poised to benefit from the aging population.

The “baby boomer” generation is the largest in the United States. An aging population

will increase demand for health care products and services.

● Abbvie is growing revenue and earnings at a high rate. Through the first nine months of

the year, revenue and adjusted earnings grew 13% and 38%, respectively.

● Abbvie is a rare stock that offers both a high current dividend yield,(of 3.4%) and a high

dividend growth. Abbvie has increased its dividend by 27% since its first payout in

January 2013.

Potential Concerns

● The main concern for Abbvie is that it generates a majority of total revenue from one

drug, Humira, which constituted 61% of the company’s overall sales in 2015 thus far.

● Another concern is the increased regulatory scrutiny of biotechnology companies. In

October, Abbvie stock fell 14% in a single day after the FDA warned the company that

its hepatitis C treatments – Viekira Pak and Technivie – can cause serious liver injury in

patients with underlying advanced liver disease.

● Abbvie stock is aggressively valued based on its reported earnings. The stock trades for

18 times 2015 GAAP earnings per share, which is a premium valuation.

Bottom Line

Abbvie’s portfolio is highly focused on Humira, but it is aggressively expanding its future drug

pipeline. Last quarter, Abbvie generated $773 million in sales from two of its new drugs:

Imbruvica and Viekira. Abbvie’s future pipeline depends on the success of its new drugs and

continued strong sales of Humira.

Additional Resources for ABBV

● Dividend.com Profile Page for ABBV

● Full Dividend Payout History for ABBV

Dividend.com - 2016 Stock Guide

16

Alliance Resource Partners L.P. (ARLP)

2015 Range: 12.87 - 43.65 Avg. Volume: 304,534

Market Cap: 982.25M P/E Ratio (2016): 5.02

2015 EPS Est: 3.07 2016 EPS Est: 2.64

Annualized Div: 3.30 Div. Yield: 20.49%

Payout Ratio (2015): 1.07 Payout Ratio (2016): 1.25

ARLP Five-Year Stock Chart

Company Profile

Alliance Resource Partners LP (ARLP) engages in the production and marketing of coal

primarily to utilities and industrial users in the United States. As of December 31, 2007, the

company had approximately 712.8 million tons of coal reserves in Illinois, Indiana, Kentucky,

Maryland, Pennsylvania, and West Virginia. Alliance Resource Management GP, LLC is the

general partner of Alliance Resource Partners, L.P. The company was founded in 1971 and is

headquartered in Tulsa, Oklahoma. As a limited partnership, capital gains are accounted for

differently, so please consult with a tax advisor.

Twenty-year dividend payout history (annualized)

Dividend.com - 2016 Stock Guide

17

Year Annualized Payout Change

2014 3.68 -19.33%

2013 4.57 +9.67%

2012 4.16 +14.73%

2011 3.63 +13.20%

2010 3.21 -27.08%

2009 4.40 +73.72%

2008 2.53 +15.00%

2007 2.20 +14.58%

2006 1.92 +21.87%

2005 1.58 +26.65%

2004 1.24 +18.48%

2003 1.05 +5.00%

2002 1.00 --

2001 1.00 --

2000 1.00 +769.57%

1999 0.12 -93.07%

Dividend.com DARS™ Ratings for ARLP

Below are Dividend.com's proprietary DARS™ Ratings for ARLP as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.5

ARLP is outperforming much of the market.

Overall Yield Attractiveness

4.0

ARLP's dividend yield is above the industry average.

Dividend.com - 2016 Stock Guide

18

Dividend Reliability

4.0

ARLP has been paying dividends for 2011 years, and we its dividend yield is safe.

Dividend Uptrend

3.5

ARLP has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

2.5

ARLP's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for ARLP

Potential Catalysts

● Alliance Resource has a unique operational advantage—its mines are situated close to its

end users, which reduces transportation costs.

● The company has priced and committed more than 90% of its 2015 deliveries.

● Strong balance sheet with a manageable 1.27 times total debt to trailing 12 months

EBITDA ratio. This provides Alliance Resource with ample flexibility to sustain its

distribution.

Potential Concerns

● Increased regulatory scrutiny of using coal as an energy source presents significant

regulatory risk.

● Low natural gas prices have incentivized utilities to switch from coal to natural gas for

electricity generation.

Bottom Line

Alliance Resource is a coal company, which is facing significant structural risk from increased

regulatory risk as well as low natural gas prices. However, Alliance Resource generates more

than enough distributable cash flow to sustain its dividend payout. The stock currently yields

14%, which makes this a very attractive income opportunity for investors who are willing to

accept the risk of investing in coal.

Additional Resources for ARLP

● Dividend.com Profile Page for ARLP

● Full Dividend Payout History for ARLP

Dividend.com - 2016 Stock Guide

19

AvalonBay Communities Inc. (AVB)

2015 Range: 158.72 - 186.89 Avg. Volume: 774,577

Market Cap: 24.05B P/E Ratio (2016): 21.35

2015 EPS Est: 8.00 2016 EPS Est: 8.23

Annualized Div: 5.00 Div. Yield: 2.87%

Payout Ratio (2015): 0.63 Payout Ratio (2016): 0.61

AVB Five-Year Stock Chart

Company Profile

AvalonBay Communities (AVB) is an apartment-based real estate investment trust (REIT). AVB

owns or holds an ownership interest in multifamily communities in 10 states and the District of

Columbia. The company, formerly known as Bay Apartment Communities, Inc., was founded in

1978 and is headquartered in Arlington, Virginia. AVB is largely affected by general economic

conditions and the housing market in the U.S. As a REIT, it is mandated to pay out the majority

of its earnings, and as a result has a high dividend yield and payout ratio. AVB has been paying

dividends since 1998, and has increased them consecutively annually since 2013. AVB pays

dividends quarterly.

Dividend.com - 2016 Stock Guide

20

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 4.64 +8.41%

2013 4.28 +10.31%

2012 3.88 +8.62%

2011 3.57 --

2010 3.57 -20.00%

2009 4.47 -16.99%

2008 5.38 +58.21%

2007 3.40 +8.97%

2006 3.12 +9.86%

2005 2.84 +1.43%

2004 2.80 --

2003 2.80 --

2002 2.80 +9.38%

2001 2.56 +14.29%

2000 2.24 +8.74%

1999 2.06 +34.64%

1998 1.53 -58.45%

Dividend.com - 2016 Stock Guide

21

Dividend.com DARS™ Ratings for AVB

Below are Dividend.com's proprietary DARS™ Ratings for AVB as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.5

AVB is outperforming much of the market.

Overall Yield Attractiveness

2.5

AVB's dividend yield is just average.

Dividend Reliability

4.5

AVB has been paying dividends for 13 years, and we feel its dividend yield is extremely

safe.

Dividend Uptrend

3.5

AVB has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

AVB's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for AVB

Potential Catalysts

● Avalon Bay operates residential apartments, which are seeing increased demand—

particularly among younger generations, who are reluctant or otherwise unable to buy

homes. High demand for apartments results in favorable pricing power.

● Strong tenant profile. Avalon Bay operates a diversified portfolio of 282 apartment

communities across 11 states and the District of Columbia. These apartment buildings are

in high barrier to entry communities characterized by a low supply of zoned land.

● Compelling dividend growth. As its funds from operation grow, Avalon Bay has

increased its dividend by 7% per year over the past five years.

Dividend.com - 2016 Stock Guide

22

Potential Concerns

● As a REIT, Avalon Bay is sensitive to changes in interest rates. The U.S. Federal Reserve

may increase interest rates as soon as December. This would put pressure on REITs,

which utilize debt heavily within their capital structures, and would suffer higher interest

costs if rates rise.

● Avalon Bay carries a significantly leveraged balance sheet. Debt-to-EBITDA is 4.9 times

higher than many other stocks in its peer group.

● Low dividend yield. Avalon Bay’s share price is close to its 52-week high. This has

caused its dividend yield to fall to 2.8% currently. That is a fairly low dividend yield—

especially for a REIT, which commonly yield 4%-5%, or higher.

Bottom Line

As the company does not want to issue debt to further stress its balance sheet, Avalon Bay is

issuing equity, which is dilutive to existing shareholders. FFO per share fell 5% last quarter

largely because of more shares outstanding.

Additional Resources for AVB

● Dividend.com Profile Page for AVB

● Full Dividend Payout History for AVB

American Express Company (AXP)

2015 Range: 67.80 - 94.89 Avg. Volume: 5,533,700

Market Cap: 68.65B P/E Ratio (2016): 12.82

2015 EPS Est: 5.28 2016 EPS Est: 5.44

Annualized Div: 1.16 Div. Yield: 1.69%

Payout Ratio (2015): 0.22 Payout Ratio (2016): 0.21

Dividend.com - 2016 Stock Guide

23

AXP Five-Year Stock Chart

Company Profile

American Express (AXP)--or AmEx for short--is a multinational financial services company that

is primarily known for its payment services. The company operates in four segments: U.S. Card

Services, International Card Services, Global Commercial Services (GCS) and Global Network &

Merchant Services. The company employs over 62,500 people worldwide. AmEx is largely

affected by financial and credit markets, and well as general macroeconomic conditions. As well,

AmEx is affected by regulations about lending and interest rates. AmEx was founded in 1950,

and is headquartered in New York, NY. AmEx has been paying dividends since 1993, and has

increased them consecutively annually since 2012. AmEx pays its dividends quarterly.

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 0.98 +13.95%

2013 0.86 +10.26%

2012 0.78 +8.33%

2011 0.72 --

Dividend.com - 2016 Stock Guide

24

2010 0.72 -20.00%

2009 0.90 +25.00%

2008 0.72 +20.00%

2007 0.60 +11.11%

2006 0.54 +12.50%

2005 0.48 +50.00%

2004 0.32 -15.79%

2003 0.38 -5.00%

2002 0.40 +25.00%

2001 0.32 +1.59%

2000 0.32 +4.88%

1999 0.30 +33.48%

1998 0.23 -25.00%

1997 0.30 -20.00%

1996 0.38 +66.67%

1995 0.23 -85.94%

1994 1.60 -65.52%

Dividend.com DARS™ Ratings for AXP

Below are Dividend.com's proprietary DARS™ Ratings for AXP as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.5

AXP is outperforming much of the market.

Overall Yield Attractiveness

2.5

AXP's dividend yield is just average.

Dividend.com - 2016 Stock Guide

25

Dividend Reliability

4.5

AXP has been paying dividends for 2011 years, and we feel its dividend yield is extremely

safe.

Dividend Uptrend

3.5

AXP has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

AXP's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for AXP

Potential Catalysts

● American Express will benefit from continued recovery in the global economy.

Consumer spending remains resilient, which is a long-term positive catalyst for the

company. Long-term growth initiatives are expected to materialize as early as 2016,

when earnings per share are projected to return to growth then increase 12%-15% in

2017.

● Attractive valuation. American Express stock trades for 12 times earnings per share,

which is close to a five-year low valuation.

Potential Concerns

● American Express’ earnings per share declined 11% last quarter as its return on equity

contracted by two percentage points. The company is spending aggressively on growth

initiatives including renewals and changes made earlier this year to certain co-brand

relationships.

● Low dividend yield. American Express yields just 1.5%, which is significantly below the

market average yield. This does not provide much of a margin of safety.

Bottom Line

American Express stock is cheap and the company recently formed a partnership with Sam’s

Club, the eighth largest retailer in the United States. It is also expanding its customer rewards

program to drive further increases in membership, which will be positive for earnings growth as

well.

Dividend.com - 2016 Stock Guide

26

Additional Resources for AXP

● Dividend.com Profile Page for AXP

● Full Dividend Payout History for AXP

Boeing Company (BA)

2015 Range: 115.14 - 158.83 Avg. Volume: 3,604,130

Market Cap: 97.76B P/E Ratio (2016): 15.46

2015 EPS Est: 8.25 2016 EPS Est: 9.44

Annualized Div: 4.36 Div. Yield: 3.05%

Payout Ratio (2015): 0.53 Payout Ratio (2016): 0.46

BA Five-Year Stock Chart

Company Profile

Boeing (BA) is the world's leading aerospace company and the largest manufacturer of

commercial jetliners and military aircraft combined. The company is located in over 90 countries,

and is the largest exporter in the U.S. It has three divisions: commercial airplanes, Integrated

Defense Systems (IDS), and Boeing Capital Corporation. BA was founded in 1916, and is based

in Chicago, IL. Boeing is affected by increasing costs of developing aircraft, as well as increasing

litigation costs. Boeing faced a probe in January 2013 over its new 787 dreamliner as batteries in

two aircraft overheated. Boeing has been paying dividends since 1937, and has been increasing it

steadily since 1970. Boeing is a dividend aristocrat and pays its dividend quarterly.

Dividend.com - 2016 Stock Guide

27

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 2.92 +50.52%

2013 1.94 +10.23%

2012 1.76 +4.76%

2011 1.68 --

2010 1.68 -33.33%

2009 2.52 +57.50%

2008 1.60 +14.29%

2007 1.40 +16.67%

2006 1.20 +20.00%

2005 1.00 +29.87%

2004 0.77 +13.24%

2003 0.68 --

2002 0.68 --

2001 0.68 +21.43%

2000 0.56 --

1999 0.56 --

1998 0.56 --

Dividend.com - 2016 Stock Guide

28

1997 0.56 +2.75%

1996 0.55 +9.00%

1995 0.50 --

1994 0.50 -48.98%

Dividend.com DARS™ Ratings for BA

Below are Dividend.com's proprietary DARS™ Ratings for BA as of Dec. 2, 2015. Each value is

based on a scale of 1 to 5.

Relative Strength

3.5

BA is outperforming much of the market.

Overall Yield Attractiveness

3.0

BA's dividend yield is just average.

Dividend Reliability

4.0

BA has been paying dividends for 74 years, and we its dividend yield is safe.

Dividend Uptrend

4.0

BA has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

2.5

BA's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com - 2016 Stock Guide

29

Dividend.com 2016 Forecast for BA

Potential Catalysts

● Refocused business strategy. Boeing is scaling back on exposure to global defense

budgets—a wise strategy in an environment of declining national defense spending.

● Boeing generates two-thirds of its revenue from the commercial markets. This is a strong

tailwind, as the commercial airline order backlog for planes is at a record high. Deliveries

of commercial aircraft rose 3% last year, representing the fourth consecutive record year.

● Huge backlog of growth opportunities. Boeing ended last quarter with a $485 billion

backlog for nearly 5,700 commercial airplane orders.

Potential Concerns

● Boeing currently has more than $24 billion in long-term liabilities on its balance sheet as

a result of accrued retiree health care and accrued pension plan liabilities.

● Geopolitical concerns. Boeing caters heavily to the commercial markets. Growth in

commercial aircraft is reliant on higher demand in the emerging markets, particularly in

Asia and the Middle East. Increased geopolitical risk could curtail Boeing’s growth.

Bottom Line

Boeing is a high-quality dividend stock with a 3% yield and a track record of high dividend

growth. Over the past five years, Boeing has increased its dividend by 16% compounded annually

– thanks to its strong earnings growth and large backlog – which will help fuel future earnings

and dividend growth.

Additional Resources for BA

● Dividend.com Profile Page for BA

● Full Dividend Payout History for BA

BlackRock Inc. (BLK)

2015 Range: 275.00 - 382.84 Avg. Volume: 771,494

Market Cap: 53.88B P/E Ratio (2016): 15.45

2015 EPS Est: 19.70 2016 EPS Est: 21.00

Annualized Div: 8.72 Div. Yield: 2.73%

Payout Ratio (2015): 0.44 Payout Ratio (2016): 0.42

Dividend.com - 2016 Stock Guide

30

BLK Five-Year Stock Chart

Company Profile

BlackRock, Inc. (BLK) is an independent investment management firm. The company provides

risk management, investment management, and advisory services to corporate, public, and Taft-

Hartley pension plans, insurance companies, mutual funds, endowments, foundations, nuclear

decommissioning trusts, banks, charities, corporations, official institutions, and individuals

worldwide. BlackRock was founded in 1988 and is based in New York, New York.

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 7.72 +14.88%

2013 6.72 +12.00%

2012 6.00 +9.09%

2011 5.50 +10.00%

2010 5.00 +60.26%

2009 3.12 --

Dividend.com - 2016 Stock Guide

31

2008 3.12 +16.42%

2007 2.68 +59.52%

2006 1.68 +40.00%

2005 1.20 +20.00%

2004 1.00 +149.98%

2003 0.40 -86.30%

Dividend.com DARS™ Ratings for BLK

Below are Dividend.com's proprietary DARS™ Ratings for BLK as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.0

BLK is performing in-line with the market or better.

Overall Yield Attractiveness

3.0

BLK's dividend yield is just average.

Dividend Reliability

4.5

BLK has been paying dividends for 8 years, and we feel its dividend yield is extremely safe.

Dividend Uptrend

3.5

BLK has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

BLK's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com - 2016 Stock Guide

32

Dividend.com 2016 Forecast for BLK

Potential Catalysts

● The rally in equity markets since the financial crisis has been a big positive for

BlackRock. This has fueled strong stock price gains and earnings growth. BlackRock

grew operating profit by 4% over the first three quarters of the year, thanks largely to $50

billion of net inflows in the third quarter.

● BlackRock is valued modestly given its earnings growth. The stock trades for 17 times

trailing earnings, a discount to the S&P 500 Index, which trades for 19 times EPS.

● Strong dividend yield and dividend growth. BlackRock yields 3% and has raised its

dividend by 16% compounded annually in the past five years.

Potential Concerns

● Equity markets have declined this year. Going forward, continued concerns regarding

global equity markets could deter investors from adding funds to ETF holdings, which

would lower BlackRock’s assets under management and earnings.

● Price deflation. Sponsors of ETFs are engaging in a price war, as each sponsor wants to

be the lowest-fee provider. Further compression of ETF expenses and fees would

negatively impact earnings growth.

Bottom Line

The financial industry is seeing a structural shift. Exchange-traded funds are becoming

increasingly popular with investors, due to their all-day tradability and lower fees than traditional

mutual funds. BlackRock has a leadership position in this growth category with its iShares lineup

of ETFs. This is what has fueled BlackRock’s compelling earnings and dividend growth, which

makes it a very good dividend pick.

Additional Resources for BLK

● Dividend.com Profile Page for BLK

● Full Dividend Payout History for BLK

Dividend.com - 2016 Stock Guide

33

Bristol-Myers Squibb Company (BMY)

2015 Range: 51.820 - 70.540 Avg. Volume: 6,730,380

Market Cap: 116.60B P/E Ratio (2016): 30.52

2015 EPS Est: 1.900 2016 EPS Est: 2.290

Annualized Div: 1.52 Div. Yield: 2.21%

Payout Ratio (2015): 0.8 Payout Ratio (2016): 0.66

BMY Five-Year Stock Chart

Company Profile

Bristol Myers Squibb Co. (BMY) is a global biopharmaceutical company. The company partakes

in the discovery, development, licensing, manufacturing, marketing, distribution and sale of

biopharmaceutical products. Its products are sold globally to wholesalers, retail pharmacies,

hospitals, government entities and to the medical profession. BMY was founded in 1933, and is

based in New York. BMY relies heavily on patents to maintain market exclusivity, as well as

research and development, and the continued development and commercialization of new

products. BMY started paying a dividend in 1970, and has been consecutively raising its dividend

since 2010, when it last made a cut to the dividend. BMY pays its dividend quarterly.

Twenty-year dividend payout history (annualized)

Dividend.com - 2016 Stock Guide

34

Year Annualized Payout Change

2014 1.45 -17.61%

2013 1.76 +29.41%

2012 1.36 +3.03%

2011 1.32 +37.50%

2010 0.96 -23.20%

2009 1.25 -19.35%

2008 1.55 +38.39%

2007 1.12 --

2006 1.12 --

2005 1.12 +33.33%

2004 0.84 -25.00%

2003 1.12 -20.00%

2002 1.40 -63.92%

2001 3.88 +295.92%

2000 0.98 +13.82%

1999 0.86 +47.18%

1998 0.59 -23.53%

1997 0.77 -18.62%

1996 0.94 +69.37%

1995 0.56 -39.34%

1994 0.92 -88.15%

Dividend.com - 2016 Stock Guide

35

Dividend.com DARS™ Ratings for BMY

Below are Dividend.com's proprietary DARS™ Ratings for BMY as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.0

BMY is performing in-line with the market or better.

Overall Yield Attractiveness

3.0

BMY's dividend yield is just average.

Dividend Reliability

4.5

BMY has been paying dividends for 111 years, and we feel its dividend yield is extremely

safe.

Dividend Uptrend

3.5

BMY has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

BMY's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for BMY

Potential Catalysts

● Bristol-Myers Squibb is a premier growth stock. Shares are up more than 150% in the

past five years, which is a much stronger performance than the S&P 500 in the same

period.

● There is high optimism over Bristol-Myers Squibb’s drug pipeline, including recently

launched Opdivo and continuing positive trends for Eliquis.

Potential Concerns

● Extremely high valuation. Bristol-Myers Squibb stock trades for 60 times earnings. This

is a massive premium to the broader market.

● Risk of Bristol-Myers Squibb’s drug pipeline under-performing expectations. This carries

significant risk if new drugs do not deliver growth as expected. Revenue was up just 4%

last quarter, which may not deserve such a high P/E.

● The stock has rallied in the past few years, which has significantly lowered its dividend

yield to 2.5% and is below many other stocks in the pharmaceutical peer group.

Dividend.com - 2016 Stock Guide

36

Bottom Line

Bristol-Myers Squibb stock has rewarded investors with huge stock price appreciation in the past

several years. But the stock is not attractive to dividend investors going forward. The stock trades

for a rich valuation and a low dividend yield, and thus does not offer a margin of safety.

Additional Resources for BMY

● Dividend.com Profile Page for BMY

● Full Dividend Payout History for BMY

Bank of Nova Scotia (BNS)

2015 Range: 39.55 - 57.83 Avg. Volume: 797,802

Market Cap: 49.15B P/E Ratio (2016): 6.46

2015 EPS Est: 5.95 2016 EPS Est: 6.32

Annualized Div: 2.80 Div. Yield: 5.40%

Payout Ratio (2015): 0.47 Payout Ratio (2016): 0.44

BNS Five-Year Stock Chart

Company Profile

Bank of Nova Scotia (BNS) (commonly known as Scotiabank) is a financial services company

that focuses on retail, commercial, corporate and investment banking. The bank has three

business lines, Canadian Banking, International Banking, and Scotia Capital and Global Wealth

Management. The company was founded in 1832, and is based in Toronto, Canada. Bank of

Nova Scotia is largely affected by the general Canadian economy. As well, Bank of Nova Scotia

is affected by capital markets in Canada. Bank of Nova Scotia has been paying dividends since

1833, and has increased dividends in 42 of the last 45 years. The most recent cut to its dividend

was in 2013. Bank of Nova Scotia pays its dividends quarterly.

Dividend.com - 2016 Stock Guide

37

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 2.56 +40.66%

2013 1.82 -18.75%

2012 2.24 +7.33%

2011 2.09 -13.19%

2010 2.40 +12.76%

2009 2.13 +50.04%

2008 1.42 -16.71%

2007 1.71 +24.98%

2006 1.37 +8.42%

2005 1.26 -7.43%

2004 1.36 +61.90%

2003 0.84 +127.03%

2002 0.37 -74.48%

Dividend.com - 2016 Stock Guide

38

Dividend.com DARS™ Ratings for BNS

Below are Dividend.com's proprietary DARS™ Ratings for BNS as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.5

BNS is outperforming much of the market.

Overall Yield Attractiveness

3.5

BNS's dividend yield is above the industry average.

Dividend Reliability

4.0

BNS has been paying dividends for 2011 years, and we its dividend yield is safe.

Dividend Uptrend

3.5

BNS has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

BNS's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for BNS

Potential Catalysts

● Banks are some of the biggest beneficiaries of rising interest rates, because higher rates

cause net interest margin to expand. This will be a meaningful driver of growth once rates

rise.

● Bank of Nova Scotia is a very cheap stock with a high yield. The stock trades for 11

times earnings and yields 4.7%.

● A very well-run business. The company generated 14% return on equity last quarter

along with 5% revenue growth.

Potential Concerns

● Increasing expenses. Bank of Nova Scotia is making several smaller acquisitions to drive

revenue growth, but this comes at a cost. Expenses rose 6% last quarter and outpaced

revenue growth.

● Core banking margin fell slightly last quarter. Until interest rates rise, it will be difficult

for a regional bank like Nova Scotia to grow margins.

Dividend.com - 2016 Stock Guide

39

Bottom Line

Bank of Nova Scotia stock screens very well for value and income investors. The stock offers

significant income potential, as well as the potential for future dividend growth. When interest

rates rise, this will boost the company’s profits. Income investors should view this stock

favorably within the financial sector.

Additional Resources for BNS

● Dividend.com Profile Page for BNS

● Full Dividend Payout History for BNS

Dividend.com - 2016 Stock Guide

40

ConAgra Foods Inc. (CAG)

2015 Range: 33.45 - 45.49 Avg. Volume: 3,427,370

Market Cap: 17.11B P/E Ratio (2016): 16.54

2015 EPS Est: 2.23 2016 EPS Est: 2.39

Annualized Div: 1.00 Div. Yield: 2.55%

Payout Ratio (2015): 0.45 Payout Ratio (2016): 0.42

CAG Five-Year Stock Chart

Company Profile

ConAgra Foods, Inc. (CAG) is a packaged foods company. CAG offers several products

including consumer foods, including meals, entrees, condiments, sides, snacks, and desserts

across frozen, refrigerated, and shelf-stable temperature classes to customers through grocery

retailers, restaurants, and foodservice establishments. Its primary brands include Chef Boyardee,

Healthy Choice, Marie Callender's, Orville Redenbacher's, Slim Jim, Hebrew National, Kid

Cuisine, Reddi-Wip, VanCamp, Libby's, LaChoy, The Max, Manwich, Egg Beaters, Blue

Bonnet, Parkay, and many more. ConAgra Foods was founded in 1919 and is headquartered in

Omaha, Nebraska.

Twenty-year dividend payout history (annualized)

Dividend.com - 2016 Stock Guide

41

Year Annualized Payout Change

2014 1.00 --

2013 1.00 +3.09%

2012 0.97 +4.30%

2011 0.93 +12.05%

2010 0.83 +7.79%

2009 0.77 +1.32%

2008 0.76 +4.11%

2007 0.73 -10.21%

2006 0.81 -25.55%

2005 1.09 +3.70%

2004 1.05 +4.88%

2003 1.00 +5.35%

2002 0.95 +7.32%

2001 0.89 +6.09%

2000 0.84 +13.41%

1999 0.74 +13.19%

1998 0.65 +15.19%

1997 0.57 -7.52%

1996 0.61 +42.00%

1995 0.43 +15.24%

1994 0.37 -85.39%

Dividend.com - 2016 Stock Guide

42

Dividend.com DARS™ Ratings for CAG

Below are Dividend.com's proprietary DARS™ Ratings for CAG as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.0

CAG is performing in-line with the market or better.

Overall Yield Attractiveness

3.5

CAG's dividend yield is above the industry average.

Dividend Reliability

4.0

CAG has been paying dividends for 35 years, and we its dividend yield is safe.

Dividend Uptrend

3.5

CAG has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

2.5

CAG's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for CAG

Potential Catalysts

● Debt reduction. ConAgra has eliminated $2.1 billion of debt since its acquisition of

Ralcorp Holdings. This has strengthened the company’s balance sheet.

● Sale of private brands business. ConAgra will sell Ralcorp for $2.7 billion. This cash can

be allocated toward improving ConAgra’s existing brands to restore future earnings

growth.

Potential Concerns

● Shifting consumer preferences. Health-conscious consumers are buying less pre-

packaged, shelf-stable and frozen foods, which make up a large component of ConAgra’s

product portfolio.

● Weak earnings performance. ConAgra reported a $252 million net loss in fiscal 2015,

due to poor sales of its flagship Healthy Choice, Orville Redenbacher’s and Chef

Boyardee brands.

● Over-valuation. ConAgra stock trades for 17 times forward earnings estimates, which is

an above-market multiple. The company lost money last fiscal year, meaning its earnings

growth expectations may be too aggressive.

Dividend.com - 2016 Stock Guide

43

Bottom Line

ConAgra is in the middle of a lengthy turnaround. The company will sell its private label business

for nearly half the purchase price. This was a very poor decision that cost the company billions of

dollars in losses. Because of this, ConAgra has not raised its dividend since 2012. As a result,

ConAgra cannot be recommended as a dividend growth stock.

Additional Resources for CAG

● Dividend.com Profile Page for CAG

● Full Dividend Payout History for CAG

Caterpillar Inc. (CAT)

2015 Range: 62.99 - 94.66 Avg. Volume: 6,838,460

Market Cap: 38.12B P/E Ratio (2016): 17.94

2015 EPS Est: 4.60 2016 EPS Est: 3.65

Annualized Div: 3.08 Div. Yield: 4.66%

Payout Ratio (2015): 0.67 Payout Ratio (2016): 0.84

CAT Five-Year Stock Chart

Dividend.com - 2016 Stock Guide

44

Company Profile

Caterpillar Inc. (CAT) is a manufacturer of construction and mining equipment, diesel and natural

gas engines, industrial gas turbines and diesel-electric locomotives. CAT is the largest

manufacturer of construction and mining equipment in the world. It has over $70 billion in assets,

which has made it the number one company in its industry. Caterpillar was founded in 1925, and

is based in Peoria, IL. Volatility in global financial markets has a large impact on the markets in

which Caterpillar operates. As well, many of Caterpillar’s global operations are exposed to

political and economic risks. Caterpillar has been paying a dividend since 1996. Most years,

Caterpillar increases its dividend, but there have been years where the company has cut its

dividend. Caterpillar pays its dividend quarterly. Caterpillar is the world's largest manufacturer of

construction and mining equipment, diesel and natural gas engines and industrial gas turbines.

With more than US$70 billion in assets, Caterpillar was ranked number one in its industry and

number 44 overall in the 2009 Fortune 500.

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 2.60 +51.16%

2013 1.72 -30.65%

2012 2.48 +37.78%

2011 1.80 +4.65%

2010 1.72 +2.38%

2009 1.68 +7.69%

2008 1.56 +18.18%

2007 1.32 +20.00%

2006 1.10 +20.88%

2005 0.91 +16.67%

Dividend.com - 2016 Stock Guide

45

2004 0.78 +9.86%

2003 0.71 +1.43%

2002 0.70 +1.45%

2001 0.69 +3.76%

2000 0.67 +6.40%

1999 0.63 +13.64%

1998 0.55 +22.22%

1997 0.45 +20.00%

1996 0.38 +25.00%

1995 0.30 +166.67%

1994 0.11 -88.75%

Dividend.com DARS™ Ratings for CAT Below are Dividend.com's proprietary DARS™ Ratings for CAT as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

2.0

CAT is slightly underperforming relative to its peers.

Overall Yield Attractiveness

4.0

CAT's dividend yield is above the industry average.

Dividend Reliability

4.0

CAT has been paying dividends for 15 years, and we its dividend yield is safe.

Dividend Uptrend

4.0

CAT has shown steady and generous dividends, and has increased its payouts each year.

Dividend.com - 2016 Stock Guide

46

Earnings Growth

2.0

CAT has seen its earnings estimates slightly lowered.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for CAT

Potential Catalysts

● Attractive valuation. Caterpillar stock trades for 14 times earnings, a significant discount

to the broader market multiple.

● Compelling 4.3% dividend yield and dividend growth. The company generates enough

cash flow to continue paying its high dividend, and increased its dividend by 10%.

● Continued recoveries in the U.S. housing and construction markets are a positive for

Caterpillar.

Potential Concerns

● The slowdown in precious metals prices like gold and copper over the past year has

caused significant damage to the mining industry, which Caterpillar’s machinery caters

to.

● 2016 earnings estimated to be down 31% from peak 2012 levels. Most of this,

approximately 2/3, is due to declines in natural resource industry.

● Caterpillar is also heavily exposed to the strong U.S. dollar. Of the 31% decline in 2016

earnings versus 2012 levels, 10% of the decline is due to negative foreign exchange

effects.

Bottom Line

As the precious metals and natural resources industries contract, Caterpillar is experiencing

falling sales and earnings. Revenue fell 18% last quarter. In response, the company is

aggressively cutting costs, which is keeping profitability intact. This at least supports current

dividend, which is very high.

Additional Resources for CAT

● Dividend.com Profile Page for CAT

● Full Dividend Payout History for CAT

Dividend.com - 2016 Stock Guide

47

Colgate-Palmolive Company (CL)

2015 Range: 50.84 - 71.56 Avg. Volume: 3,573,440

Market Cap: 59.81B P/E Ratio (2016): 22.45

2015 EPS Est: 2.79 2016 EPS Est: 2.97

Annualized Div: 1.52 Div. Yield: 2.31%

Payout Ratio (2015): 0.54 Payout Ratio (2016): 0.51

CL Five-Year Stock Chart

Company Profile

Colgate Palmolive (CL) is a consumer products company that specializes in household,

healthcare, and personal products. The company operates in two segments: Oral, Personal and

Home Care and Pet Nutrition. CL offers hundreds of products, and operates in over 200 countries

throughout the world. The company was founded in 1806, and is based in New York, NY.

Colgate is affected by its ability to research and develop new products, as well as raw material

costs. Colgate has been increasing dividends since 1964. The company is known as a dividend

aristocrat, as it has been increasing its dividend consecutively annually for more than 25 years.

Colgate pays its dividend quarterly.

Twenty-year dividend payout history (annualized)

Dividend.com - 2016 Stock Guide

48

Year Annualized Payout Change

2014 1.42 -28.28%

2013 1.98 -18.85%

2012 2.44 +7.49%

2011 2.27 +11.82%

2010 2.03 +18.02%

2009 1.72 +10.26%

2008 1.56 +11.43%

2007 1.40 +12.00%

2006 1.25 +12.61%

2005 1.11 +15.63%

2004 0.96 +6.67%

2003 0.90 +25.00%

2002 0.72 +6.51%

2001 0.68 +6.96%

2000 0.63 +6.94%

1999 0.59 +7.45%

1998 0.55 +3.77%

1997 0.53 +12.77%

1996 0.47 +6.82%

1995 0.44 +14.29%

1994

0.39 -85.19%

Dividend.com - 2016 Stock Guide

49

Dividend.com DARS™ Ratings for CL

Below are Dividend.com's proprietary DARS™ Ratings for CL as of Dec. 2, 2015. Each value is

based on a scale of 1 to 5.

Relative Strength

3.0

CL is performing in-line with the market or better.

Overall Yield Attractiveness

3.0

CL's dividend yield is just average.

Dividend Reliability

4.5

CL has been paying dividends for 25 years, and we feel its dividend yield is extremely safe.

Dividend Uptrend

3.5

CL has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

CL's earnings estimates are flat.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for CL

Potential Catalysts

● Excellent brand strength. Colgate-Palmolive has a number of successful brands, including

its Colgate toothpaste, Palmolive soap and its pet care business.

● Colgate is a top dividend growth stock. It is a Dividend Aristocrat, having paid

uninterrupted dividends each year since 1895.

● Colgate-Palmolive generates significant free cash flow, which is returned to shareholders

through both dividends and buybacks. The dividend yields 2.4% and the company

recently announced a new $5 billion share buyback program.

Potential Concerns

● Slowing economic growth in the emerging markets. Colgate-Palmolive generates 80% of

its total revenue from outside North America; weak economic growth in the

underdeveloped nations could be a significant future headwind.

● The rising U.S. dollar. Colgate-Palmolive is heavily exposed to foreign exchange

fluctuations. Revenue growth was negatively impacted by 13 percentage points last

quarter just because of currency.

Dividend.com - 2016 Stock Guide

50

● Over-valuation. Colgate-Palmolive stock trades for 25 times earnings, approximately

31% above the S&P 500 Index valuation. Slowing growth could result in compression of

Colgate-Palmolive’s valuation multiple.

Bottom Line

Colgate-Palmolive is experiencing near-term challenges from currency impacts, but it remains a

strong business with top brands. According to the company, Colgate-Palmolive stock delivered a

1,137% total return in the 20-year period from Dec. 31, 1994 through June 30, 2015. This handily

beat the 563% total return for the S&P 500 index in the same period.

Additional Resources for CL

● Dividend.com Profile Page for CL

● Full Dividend Payout History for CL

ConocoPhillips (COP)

2015 Range: 41.10 - 71.37 Avg. Volume: 8,561,520

Market Cap: 62.72B P/E Ratio (2016): 137.3

2015 EPS Est: -0.80 2016 EPS Est: 0.37

Annualized Div: 2.96 Div. Yield: 5.98%

Payout Ratio (2015): -3.7 Payout Ratio (2016): 8

COP Five-Year Stock Chart

Dividend.com - 2016 Stock Guide

51

Company Profile

ConocoPhillips (COP) is an international integrated energy company. COP focuses on crude oil,

natural gas, natural gas liquids, liquefied natural gas and bitumen. The company's segments

include exploration and production (E&P), midstream, refining and marketing (R&M), and

emerging businesses. The company was founded in 2002 as a result of a merger between Conoco

Inc. and Phillips Petroleum Co., and is based in Houston, Texas. ConocoPhillips is affected by

two major risks, commodity price risk and interest rate risk. ConocoPhillips’s net income is

generally highly correlated with the price of crude oil. ConocoPhillips has been paying dividends

since its inception in 2002, and has consistently increased them annually since then.

ConocoPhillips pays its dividend quarterly.

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 2.84 +5.19%

2013 2.70 +2.27%

2012 2.64 --

2011 2.64 +22.79%

2010 2.15 +12.57%

2009 1.91 +1.60%

2008 1.88 +14.63%

2007 1.64 +13.89%

2006 1.44 +22.03%

2005 1.18 +31.84%

2004 0.90 +9.82%

Dividend.com - 2016 Stock Guide

52

2003 0.82 +10.14%

2002 0.74 +5.71%

2001 0.70 +2.94%

2000 0.68 --

1999 0.68 --

1998 0.68 +1.49%

1997 0.67 +7.20%

1996 0.63 +4.60%

1995 0.60 +6.70%

1994 0.56 -60.56%

Dividend.com DARS™ Ratings for COP

Below are Dividend.com's proprietary DARS™ Ratings for COP as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

2.0

COP is slightly underperforming relative to its peers.

Overall Yield Attractiveness

4.0

COP's dividend yield is above the industry average.

Dividend Reliability

4.5

COP has been paying dividends for 77 years, and we feel its dividend yield is extremely safe.

Dividend Uptrend

3.5

COP has shown steady and generous dividends, and has increased its payouts each year.

Earnings Growth

3.0

COP's earnings estimates are flat.

Dividend.com - 2016 Stock Guide

53

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for COP

Potential Catalysts

● Potential for a recovery in oil prices. ConocoPhillips’ stock would likely outperform if

commodity prices increase in 2016.

● High dividend yield. The stock yields 5.5%, and the company increased its dividend by

1% this year.

● Strong free cash flow generation. Thanks to asset sales and significant cost cuts,

ConocoPhillips expects to cover its dividend with free cash flow by 2017.

Potential Concerns

● Falling oil prices. ConocoPhillips’ revenue is down 56% through the first three quarters

of 2015, year-over-year.

● Inconsistent profitability. ConocoPhillips lost $978 million in the first three quarters of

the year, reversing a $6.8 billion profit in the comparable 2014 period.

● Lack of integrated structure. ConocoPhillips spun off its downstream refining unit, which

gave valuable support when oil prices decline. As an independent exploration and

production company, ConocoPhillips is entirely reliant on commodity prices.

Bottom Line

ConocoPhillips showed its resilient business model by increasing its dividend in 2015, while

many of its peers had to cut dividends to stay afloat. ConocoPhillips received $600 million in

disposition proceeds year-to-date. These actions collectively allowed the company to raise its

dividend; however, if oil prices continue to decline, the dividend may be in jeopardy.

Additional Resources for COP

● Dividend.com Profile Page for COP

● Full Dividend Payout History for COP

Cisco Systems Inc. (CSCO)

2015 Range: 23.030 - 30.310 Avg. Volume: 27,077,800

Market Cap: 136.15B P/E Ratio (2016): 11.18

2015 EPS Est: 2.270 2016 EPS Est: 2.400

Annualized Div: 0.84 Div. Yield: 3.17%

Payout Ratio (2015): 0.37 Payout Ratio (2016): 0.35

Dividend.com - 2016 Stock Guide

54

CSCO Five-Year Stock Chart

Company Profile

Cisco Systems (CSCO) is a technology company that designs, manufactures, and sells networking

equipment. The company focuses on three main segments which include Enterprise and Service

Provider, Small Business and the Home. The stock was added to the Dow Jones in 2009, and is

also included in the S&P 500 Index, the Russell 1000 Index, NASDAQ 100 Index and the Russell

1000 Growth Stock Index. CSCO was founded in 1984, and is based in San Jose, CA.

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 0.74 +45.10%

2013 0.51 +2.00%

2012 0.50 +177.78%

2011 0.18 -93.66%

Dividend.com - 2016 Stock Guide

55

Dividend.com DARS™ Ratings for CSCO

Below are Dividend.com's proprietary DARS™ Ratings for CSCO as of Dec. 2, 2015. Each value

is based on a scale of 1 to 5.

Relative Strength

3.5

CSCO is outperforming much of the market.

Overall Yield Attractiveness

3.5

CSCO's dividend yield is above the industry average.

Dividend Reliability

3.5

CSCO has been paying dividends for 2011 years, and we its dividend yield is safe.

Dividend Uptrend

3.0

CSCO has shown consistency in its payouts, but any increases have been small.

Earnings Growth

3.5

CSCO's earnings estimates have been raised nicely.

Read more about the DARS™ Rating System here.

Dividend.com 2016 Forecast for CSCO

Potential Catalysts

● Excellent balance sheet. Cisco holds $59 billion in cash and short-term investments, and

$21 billion in long-term debt.

● Attractive valuation. Cisco stock trades for 14 times earnings, a significant discount from

the market multiple.

● High dividend yield and dividend growth. Cisco stock yields 3.2% and raised its dividend

by 10% earlier this year.

Potential Concerns

● Exposure to emerging markets like China, where economic growth is slowing, could

weigh on Cisco’s growth.

● The strengthening U.S. dollar is a headwind for large multi-national companies such as

Cisco.

Dividend.com - 2016 Stock Guide

56

Bottom Line

Cisco is a quality company. Revenue grew 3% last quarter. It is highly profitable – with a great

deal of cash on the balance sheet – and an excellent dividend. The company has seen growth

slow-down in the near term due to the rising U.S. dollar and economic challenges in the emerging

markets, but these are likely to be short-term challenges. The long-term investment case remains

positive.

Additional Resources for CSCO

● Dividend.com Profile Page for CSCO

● Full Dividend Payout History for CSCO

Chevron Corporation (CVX)

2015 Range: 69.580 - 114.450 Avg. Volume: 10,389,400

Market Cap: 172.85B P/E Ratio (2016): 22.96

2015 EPS Est: 3.320 2016 EPS Est: 4.000

Annualized Div: 4.28 Div. Yield: 4.79%

Payout Ratio (2015): 1.29 Payout Ratio (2016): 1.07

CVX Five-Year Stock Chart

Dividend.com - 2016 Stock Guide

57

Company Profile

Chevron Corporation (CVX) is a Fortune 500 multinational energy corporation based out of San

Ramon, California. Founded in 1984, it is involved in every aspect of energy production and

services, including petroleum operations, chemicals operations, mining operations, power

generation and energy services. The company has a focus in developing and producing crude oil

and natural gas. CVX is constantly named among the largest corporations in the world in terms of

revenue. Chevron is one of the world's six supermajor oil companies. Chevron's profitability is

mainly affected by the price of crude oil. The company's operations, especially upstream, can also

be affected by changing economic, regulatory, and political environments around the world.

Chevron has been increasing its dividend consistently since 1993, when the company first started

paying dividends.

Twenty-year dividend payout history (annualized)

Year Annualized Payout Change

2014 4.21 +7.95%

2013 3.90 +11.11%

2012 3.51 +13.59%

2011 3.09 +8.80%

2010 2.84 +6.77%

2009 2.66 +5.14%

2008 2.53 +11.95%

2007 2.26 +12.44%

2006 2.01 +14.86%

2005 1.75 +14.38%

2004 1.53 +6.99%

Dividend.com - 2016 Stock Guide

58

2003 1.43 +2.14%

2002 1.40 +5.66%

2001 1.33 +1.92%

2000 1.30 +4.84%

1999 1.24 +1.64%

1998 1.22 +7.02%

1997 1.14 +9.62%

1996 1.04 +8.11%

1995 0.96 +4.06%

1994 0.92 +24.93%

Dividend.com DARS™ Ratings for CVX