© 2015 ihs presentation ihs.com ihs crude oil markets: outlook to 2020 oil market services aaron...

TRANSCRIPT

© 2015 IHS

Presentation

ihs.com

IHS

Crude oil markets: outlook to 2020

Oil Market Services

Aaron Brady, Senior Director, [email protected]

James Fallon, Senior Director, [email protected]

21 April 2015

ENERGY

© 2015 IHS 2

Base case outlook: Two oil price phases to 2020

Two price phases to 2020

© 2015 IHS: 50104-3Source: IHS

PHASE ONE: 2015–2016 PHASE TWO: 2017–2020

Supply surplus—Oil prices under pressure

Weaker supply gains—Demand growth pushes prices up

© 2015 IHS 3

Crude oil price outlookAnnual average price in nominal US$ per barrel

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20$20

$40

$60

$80

$100

$120

$140

Brent and WTI price outlook to 2020

Source: IHS © 2015 IHS

Cru

de

oil

pri

ce p

er

ba

rre

l

Brent

WTI

© 2015 IHS

Geopolitical factors kept ~3 MMb/d oil off the market which held off price declines – until mid 2015

4

• Through mid-2015, oil off the market countered-balanced the rise in supply from North America.

• Libyan factions reached agreements which returned 500,000 b/d to the market quickly, causing the first downdraft in oil prices.

• Baghdad and Erbil reached agreement in early December 2015 which will allow 400,000 b/d to flow from KRG in 2015.

• Markets “suddenly” realized the structural market imbalance.

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4-1,600

-1,400

-1,200

-1,000

-800

-600

-400

-200

0

Iraq Nigeria Libya Iran Non-OPEC Saudi Arabia Kuwait

Th

ou

san

d b

arre

ls p

er d

ay

Global crude production outages

Source: IHS, EIA

Libya

IraqNigeria

Iran

Non-OPEC

© 2015 IHS

© 2015 IHS

1st Tipping Point: return of Libyan production brought fundamentals back into focus

5

Jan-

13

Feb-1

3

Mar

-13

Apr-1

3

May

-13

Jun-

13

Jul-1

3

Aug-1

3

Sep-1

3

Oct

-13

Nov-1

3

Dec-1

3

Jan-

14

Feb-1

4

Mar

-14

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-1

4

Sep-1

4

Oct

-14

Nov-1

4

Dec-1

4-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

$/b mmb/dFirst Tip-

ping point mid 2015

Global oil supply growth and the Brent forward curve (3rd month – 1st month)

Source: IHS Energy Crude Oil Markets © 2015 IHS

Brent forward curve(3rd to 1st month)

US + Libya cumulative production change

Contango (upward sloping forward curve) indicates loose market

Backwardation (downward sloping forward curve) indicates tight market

© 2015 IHS 6

2nd Tipping Point: Saudi Arabia stepped back from being the market balancer to guard market share

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

28.0

28.5

29.0

29.5

30.0

30.5

31.0

31.5

32.0

32.5

33.0

$0

$20

$40

$60

$80

$100

$120

$140

$/b

bl

OPEC dynamics: OPEC crude production vs call on OPEC

Source: IHS Energy Crude Oil Markets service

MM

b/d

Brent $/bbl

OPEC output

Call on OPEC

© 2015 IHS

OPEC’s roll-over of production reflects a willingness to incur short-term pain to let market find the weak producers.

© 2015 IHS 7

US crude production faces increasing headwinds, leading to month-to-month production declines in 2H15

7,500,000.0

8,000,000.0

8,500,000.0

9,000,000.0

9,500,000.0

10,000,000.0

Former Base Case: 30% Capex Cut in 2015, 14% Capex Cut in 2016

New Base Case: 40% Capex cut in 2015, Flat Capex in 2016 ( With Stripper Well Adjustment)

Mil

lio

n b

arre

ls p

er d

ay

US Crude Production Forecast (With Stripper Well Adjustment)

Source: IHS © 2015 IHS

2015 2015 2016

© 2015 IHS 8

There is a wide range of production economics among and within onshore US plays

Jan-13

Feb-13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Nov-13

Dec-13

Jan-14

Feb-14

Mar-14

Apr-14

May-14

0.0

500,000.0

1,000,000.0

1,500,000.0

2,000,000.0

2,500,000.0

3,000,000.0

3,500,000.0

120+

110-120

100-110

90-100

80-90

70-80

60-70

50-60

40-50

30-40

Under 30

2013 On-shore Main-tenance Mtn

MM

b/d

US onshore crude brought online in 2013 by WTI $/bbl breakeven categories

Breakeven $/bbl WTI

Source: IHS Energy © 2015 IHS

$50-$60/bbl

Volume needed to replace 2013 onshore base decline

$30-$40/bbl

$40-$50/bbl

$60-$70/bbl

In 2013, the US needed 1.45 MMb/d of new production to cover base decline, all of which could have come from wells breaking even at $60-$70/bbl

© 2015 IHS 9

World economic and oil demand growth

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20200.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

World economic and oil demand growth

Source: IHS, IEA © 2015 IHS

Pe

rce

nt c

ha

ng

e fr

om

pre

vio

us

yea

rWorld economic growth

World oil demand growth

© 2015 IHS

Liquids demand growth approaches 1.3-1.4 MMb/d, mostly due to improving economic conditions

10

2014 2015 2016 2017 2018 2019 2020-200

0

200

400

600

800

1,000

0

300

600

900

1,200

1,500

1,800

Africa Asia_Pacific CIS Europe Latin America Middle East

North America World

Change from preceding year (regions left-scale, world right-scale)

© 2015 IHS

Th

ou

san

d b

bl/d

Source: IHS

World demand (right-scale)

© 2015 IHS 11

OPEC crude oil production

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20200

5

10

15

20

25

30

35

OPEC crude oil production to 2020

Source: IHS © 2015 IHS

Mill

ion

ba

rre

ls p

er

da

y

Saudi Arabia

Iraq

Iran

Kuwait

Nigeria

UAELibya

Other OPEC members

© 2015 IHS 12

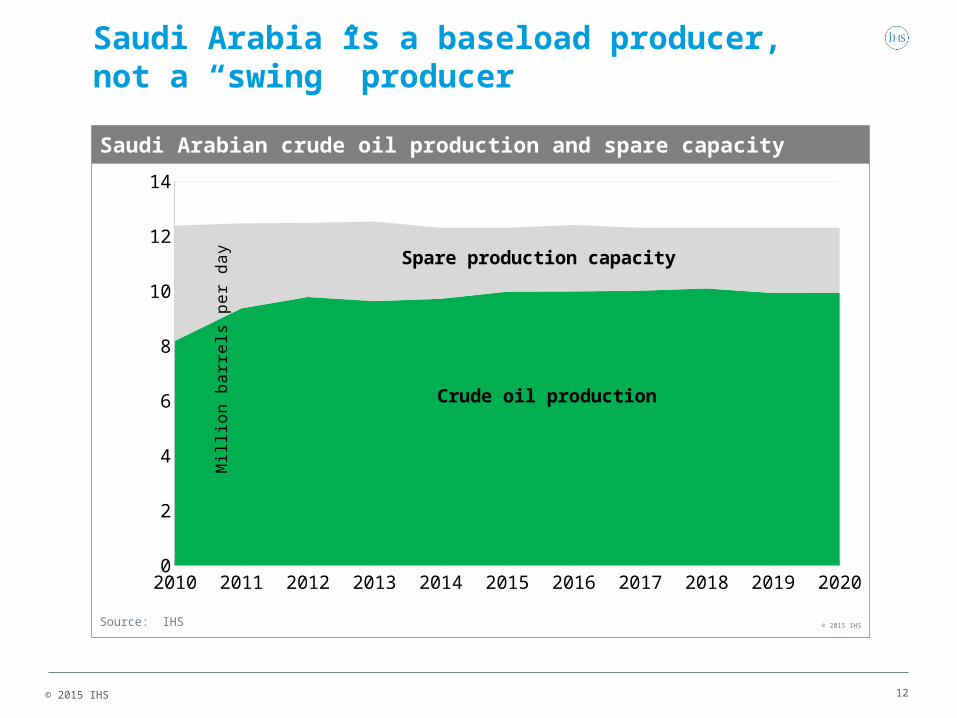

Saudi Arabia is a baseload producer, not a “swing” producer

Tight oil

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20200

2

4

6

8

10

12

14

Saudi Arabian crude oil production and spare capacity

Source: IHS © 2015 IHS

Mill

ion

ba

rre

ls p

er

da

y

Spare production capacity

Crude oil production

© 2015 IHS 13

United States crude oil production outlookAnnual average production volume

Tight oil

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20205

6

7

8

9

10

11

12

USA crude oil production to 2020

Source: IHS, EIA. Note: Data include segregated condensate. © 2015 IHS

Mill

ion

ba

rre

ls p

er

da

yMonth-to-month growth halts, temporarily

© 2015 IHS 14

Full cycle Brent $60/barrel breakeven would put a number of key producers at risk of cancelling projects

Venez

uela

Gabon

Iraq

Norway UK

Denm

ark

Niger

ia

Canad

a-SAGD

Azerb

aija

n

Sudan &

South

Sudan

Chad

Vietn

am

Indones

ia

China

Ghana

Egypt

Brunei

Yemen

Qatar

Oman

UAE

Saudi A

rabia

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

2015 Brent breakeven price analysis: Ranked according country, highest to lowest and showing high and low price range

Source: IHS Energy Cost Services © 2015 IHS

Bre

nt

$/b

bl

2015 Average Brent breakeven price full cycle 10% discount rate by country: Ranked highest to lowest breakeven with high and low price range

High range

Average breakeven

$60/bbl breakeven

Low range

© 2015 IHS 15

Non-OPEC crude oil production outlook, excluding USA

Tight oil

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20200

5

10

15

20

25

30

35

40

Non-OPEC crude oil production, excluding United States

Source: IHS, IEA, EIA © 2015 IHS

Mill

ion

bar

rels

per

day

Canada

Latin America (incl. Mexico)

Asia Pacific

Europe

AfricaMiddle East

CISCommonwealth of

Independent States

© 2015 IHS 16

Trends in upstream oil field development costsIndex illustrates change in cost of developing a global portfolio of upstream assets

Tight oil

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20140

160

180

200

220

240

260

Indicative upstream capital cost trends

Note: History is the IHS Upstream Capital Cost Index. Projection is indicative trend for future costs. Source: IHS © 2015 IHS

Ind

ica

tive

ca

pita

l co

st in

de

x (2

00

0 =

10

0)

In 2020 costs are still 7% below 2014 level

© 2015 IHS 17

Annual change in world oil demand and supply

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 20200.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

$0

$20

$40

$60

$80

$100

$120

Do

llars

pe

r b

arr

el

Change from previous year in world oil supply and demand

Notes: Annual changes are changes from the previous year. Liquids demand includes LPG and biofuels. Liquids supply includes natural gas liquids and biofuels.Source: IHS, IEA, EIA © 2015 IHS

Mill

ion

ba

rre

ls p

er

da

y

Brent price (right scale)

Demand Supply

© 2015 IHS 18

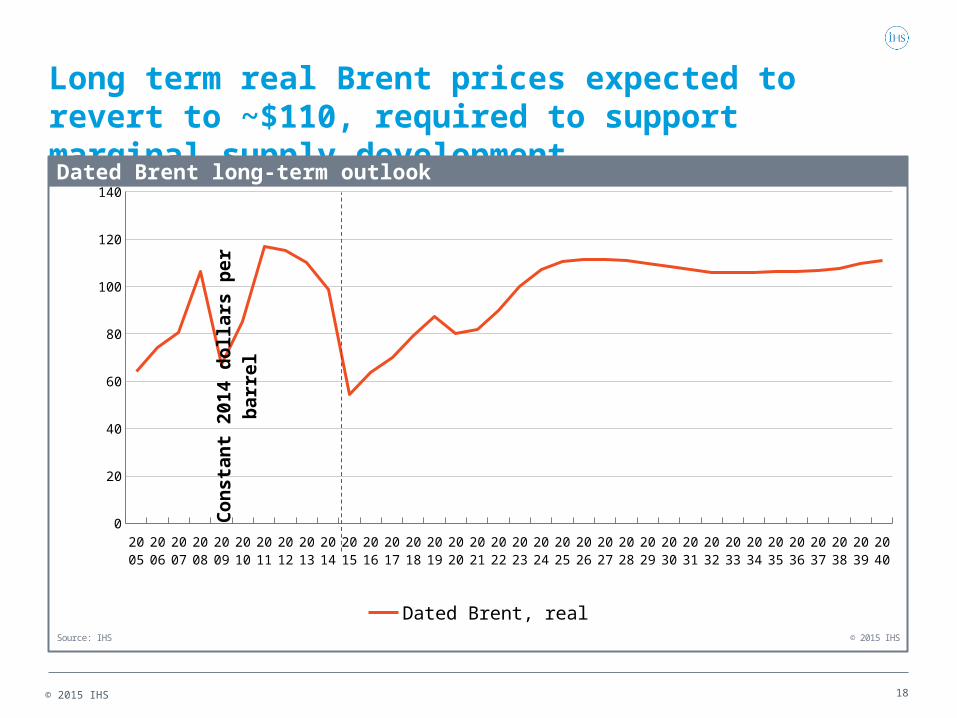

Long term real Brent prices expected to revert to ~$110, required to support marginal supply development

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

0

20

40

60

80

100

120

140

Dated Brent, real

Dated Brent long-term outlook

© 2015 IHS

Co

ns

tan

t 2

01

4 d

olla

rs p

er

ba

rre

l

Source: IHS

© 2015 IHS

Wedge of ~50 million bbl/d new oil production by 2040 needed to offset declines and meet demand growth

19

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2005 2010 2015 2020 2025 2030 2035 2040

Segregated Condensate FIP FUD FUA YTF Tight Oil

World Crude and Condensate Production Outlook

Source: IHS © 2015 IHS

Th

ou

san

d b

arre

ls p

er d

ay

© 2015 IHS 20

Long term Brent-WTI spread reflects export parity economics (US crude trade liberalization)

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

-20

0

20

40

60

80

100

120

140

Brent - WTI Dated Brent, Spot FOB WTI, Spot Cushing

Brent vs WTI Crude Prices

© 2015 IHS

Rea

l 201

4 D

olla

rs p

er B

arre

l

Source: IHS

© 2015 IHS 21

The case for a wider WTI-Brent spread: refining constraints for light tight oil processing

Tier 1 – Displace light sweet crude imports

($2 – 4/Barrel)

($1 – 2/Barrel)

($0.5 – 1.0/Barrel)

($8 – 18+/Barrel)

© 2015 IHS 22

North America crude price relationships

IHS Customer Care:• Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected] • Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected] • Asia and the Pacific Rim: +604 291 3600; [email protected]

© 2015 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS. Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more information, please contact IHS at [email protected], +1 800 IHS CARE (from North American locations), or +44 (0) 1344 328 300 (from outside North America). All products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.