© 2007 the mcgraw-hill companies, inc. mcgraw-hill/irwin chapter 21 statement of cash flows...

TRANSCRIPT

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Chapter 21Statement of Cash

Flows Revisited

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-2

Investing ActivitiesOperating Activities Financing ActivitiesSale of operational assets

Sale of investments

Collections of loans

Cash received from revenues

Issuance of stock

Issuance of bonds and notes

CASH INFLOWS

Business

CASH OUTFLOWS

Purchase of operational assets

Purchase of investmentsLoans to others

Cash paid for expenses

Payment of dividends

Repurchase of stock

Repayment of debt

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-3

Cash and Cash Equivalents

Resources immediately available to

pay obligations.

Resources immediately available to

pay obligations.

Short-term, highly liquid investments.

So near maturity that there is insignificant risk of market value fluctuation from interest rate changes.

Maturity of 3 months or less

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-4

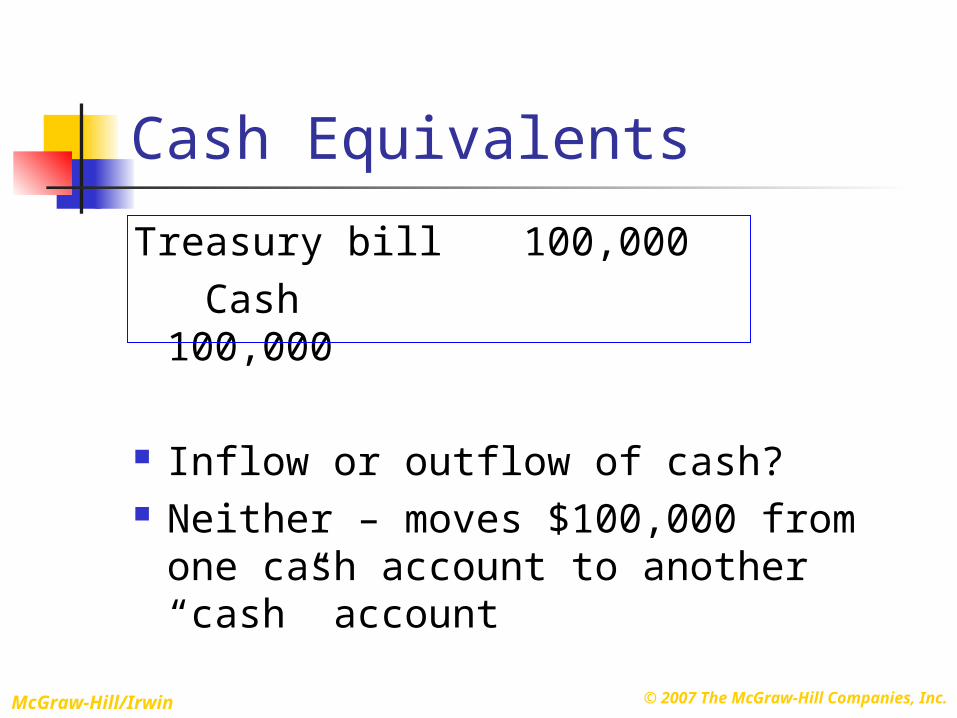

Cash Equivalents

Treasury bill 100,000 Cash 100,000

Inflow or outflow of cash? Neither – moves $100,000 from

one cash account to another “cash” account

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-5

Primary Classifications in the Statement of Cash Flows

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-6 Cash flows from operating activities:

Cash inflows: From customers $98 From investment revenue 3Cash outflows: To suppliers of goods (50) To employees (11) For interest (3) For insurance (4) For income taxes (11)Net cash flows from operating activities $22 Cash flows from investing activities: Purchase of land ($30) Purchase of short-term investment (12) Sale of land 18 Sale of equipment 5Net cash flows from investing activities (19)Cash flows from financing activities: Sale of common shares $26 Retirement of bonds payable (15) Payment of cash dividends (5)Net cash flows from financing activities 6 Net increase in cash $9Cash balance, January 1 20Cash balance, December 31 $29

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-7

Cash Flows From Operating Activities Cash flows from operating

activities are both inflows and outflows of cash that result from activities reported on the income statement.

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-8

Income Statement Cash Flows from Operating Activities Revenues: Cash inflows: Sales and service revenue Cash received from customers Investment revenue Cash revenue received Noncash revenues and gains

(e.g., gain on sale of assets) [Not reported]

Less: Expenses: Less: Cash outflows: Cost of goods sold Cash paid to suppliers Salaries expense Cash paid to employees Noncash expenses and losses (depreciation, amortization, bad debts, loss on sale of assets) [Not reported] Interest expense Cash paid to creditors Other operating expenses Cash paid for expenses Income tax expense Cash paid to the government

Net income Net cash flows from operating

activities

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-9 CASH FLOWS FROM OPERATING

ACTIVITIES

Direct Method

Cash flows from operating activities are the elements of net income, but reported on a cash basis. Cash flows from operating activities:Cash inflows: From customers $98 From investment revenue 3Cash outflows: To suppliers of goods(50) To employees(11) For interest (3) For insurance (4) For income taxes (11)Net cash flows from operating activities $22

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-10 CASH FLOWS FROM OPERATING

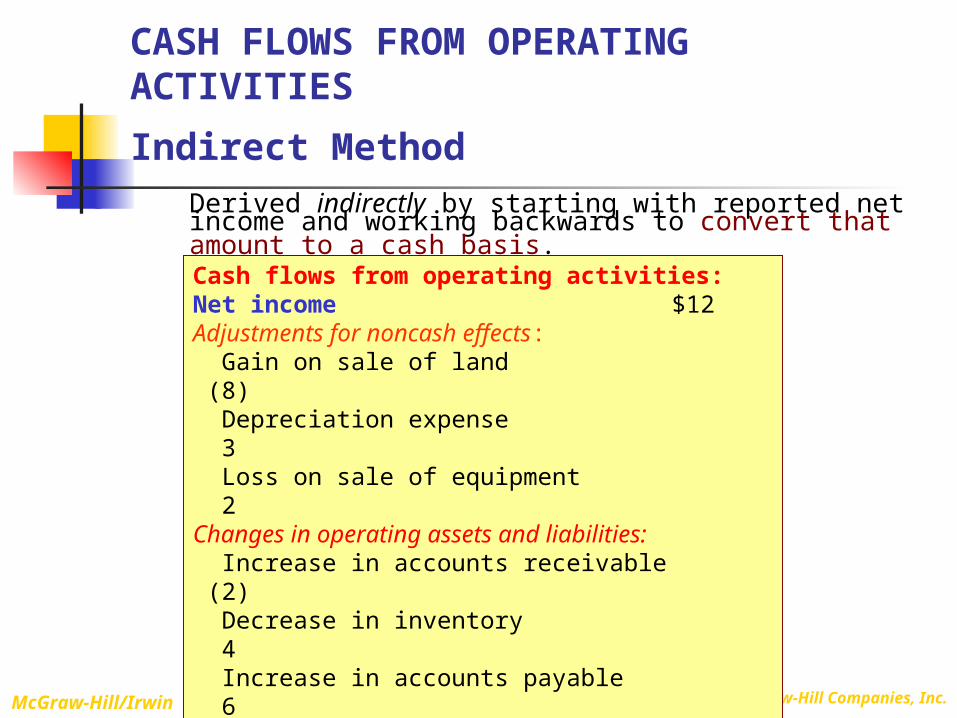

ACTIVITIES

Indirect Method Derived indirectly by starting with reported net income and working backwards to convert that amount to a cash basis. Cash flows from operating activities:Net income $12Adjustments for noncash effects: Gain on sale of land (8) Depreciation expense 3 Loss on sale of equipment 2Changes in operating assets and liabilities: Increase in accounts receivable (2) Decrease in inventory 4 Increase in accounts payable 6 Increase in salaries payable 2 Discount on bonds payable 2 Decrease in prepaid insurance 3 Decrease in income tax payable (2)Net cash flows from operating activities $22

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-11

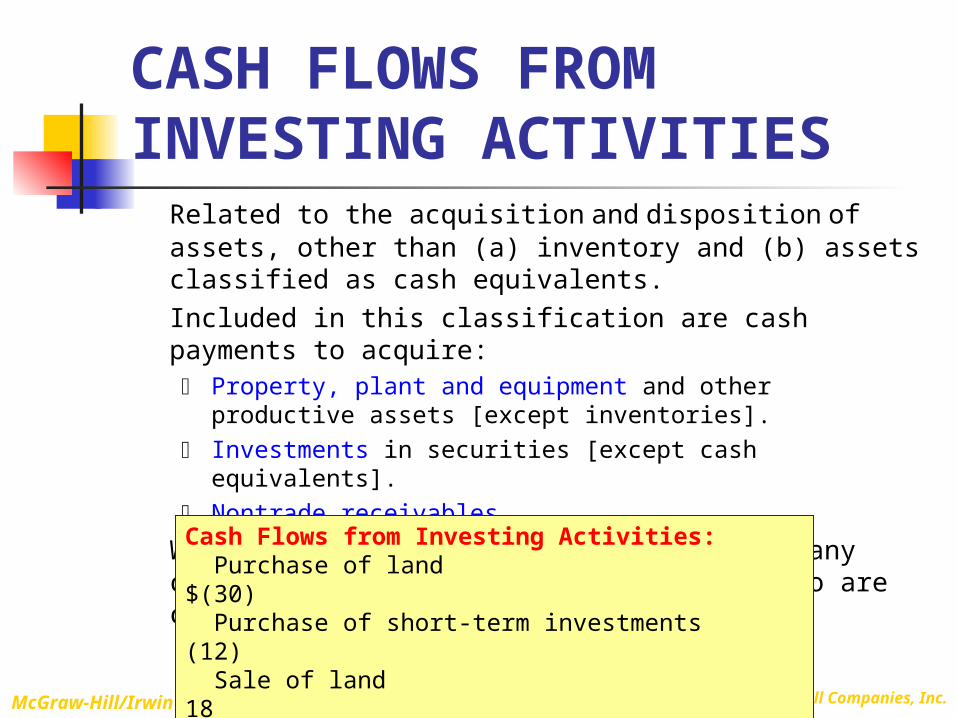

CASH FLOWS FROM INVESTING ACTIVITIES

Related to the acquisition and disposition of assets, other than (a) inventory and (b) assets classified as cash equivalents. Included in this classification are cash payments to acquire: Property, plant and equipment and other productive assets

[except inventories]. Investments in securities [except cash equivalents]. Nontrade receivables.

When these assets later are liquidated, any cash receipts from their disposition also are classified as investing activities.

Cash Flows from Investing Activities: Purchase of land$(30) Purchase of short-term investments (12) Sale of land 18 Sale of equipment 5 Net cash flows from investing activities (19)

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-12

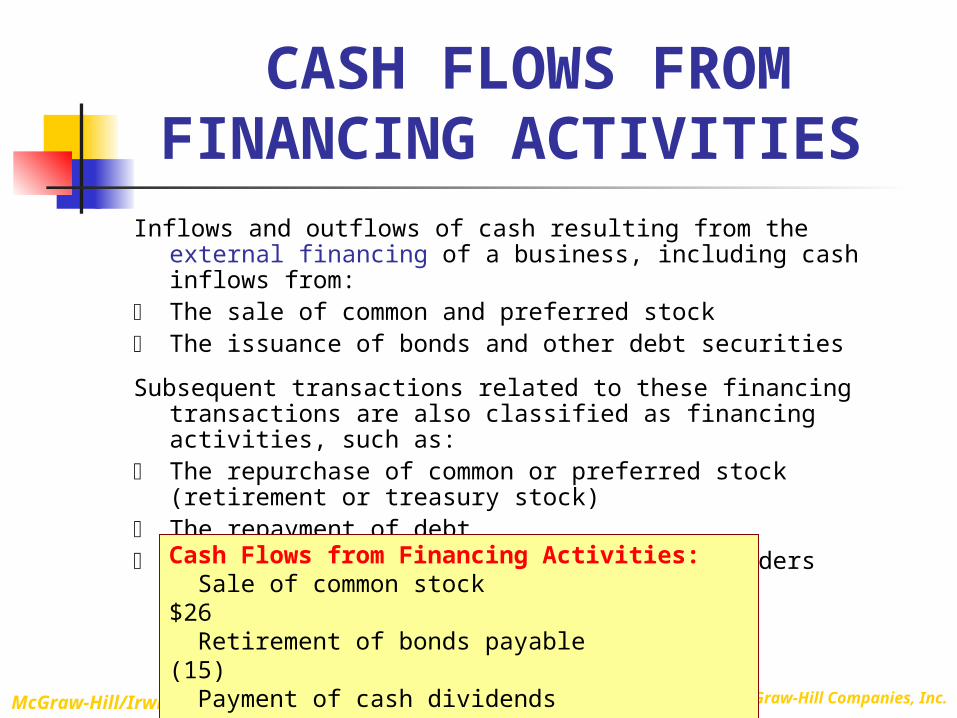

CASH FLOWS FROM FINANCING ACTIVITIES

Inflows and outflows of cash resulting from the external financing of a business, including cash inflows from:

The sale of common and preferred stock The issuance of bonds and other debt securities

Subsequent transactions related to these financing transactions are also classified as financing activities, such as:

The repurchase of common or preferred stock (retirement or treasury stock)

The repayment of debt The payment of cash dividends to shareholders

Cash Flows from Financing Activities: Sale of common stock $26 Retirement of bonds payable (15) Payment of cash dividends (5)Net cash flows from financing activities 6

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-13

SignificantNoncash Activities

Common noncash activities include:

Retiring bonds by issuing stock.

Retiring bonds by issuing stock.

Retiring debt by transferring

noncash assets.

Retiring debt by transferring

noncash assets.

Acquiring an asset by issuing a note

payable.

Acquiring an asset by issuing a note

payable.

Acquiring an asset by capital

lease.

Acquiring an asset by capital

lease.

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-14

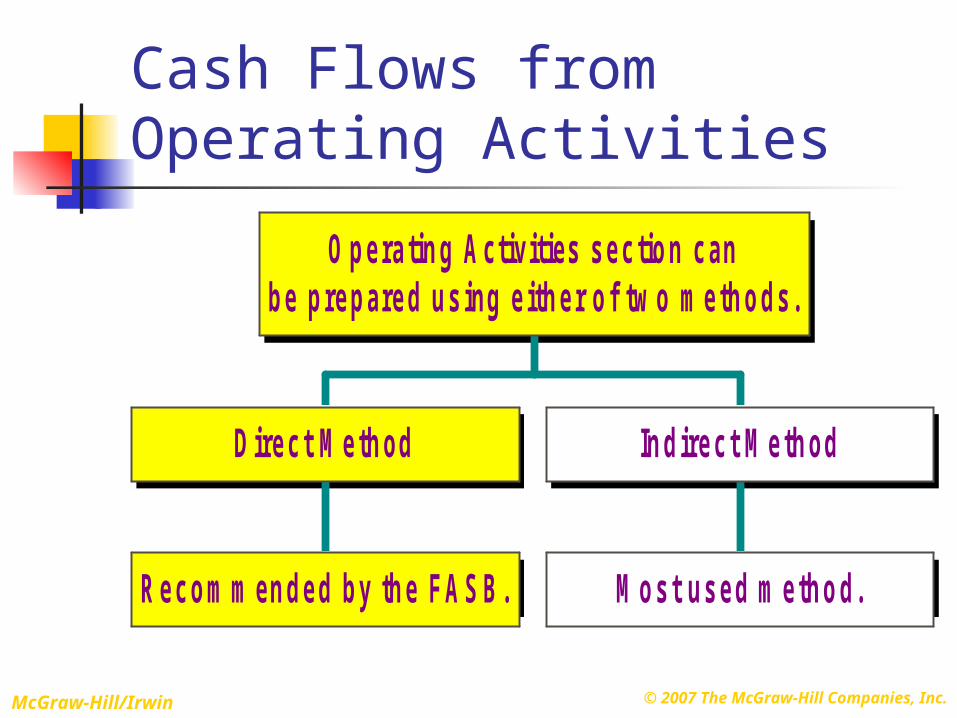

Cash Flows from Operating Activities

Recom m ended by the FASB.

Direct M ethod

M ost used m ethod.

Indirect M ethod

Operating Activities section canbe prepared using either of tw o methods.

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-15

Now, let’s look at the Indirect Method for presenting the Cash Flows from

Operating Activities section.

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-16

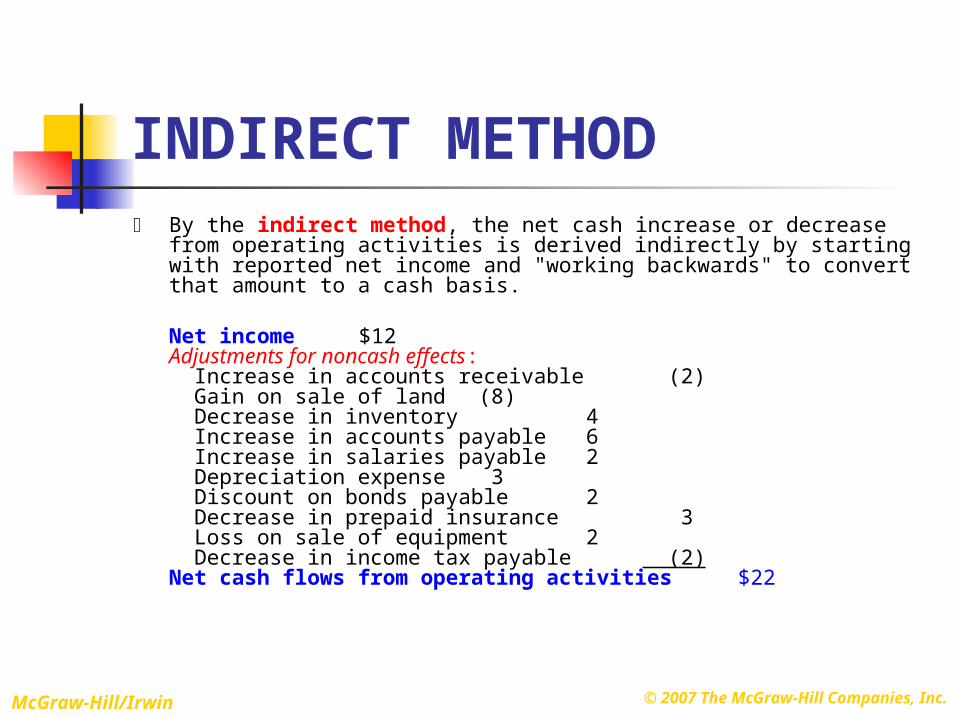

INDIRECT METHOD By the indirect method, the net cash increase or decrease from

operating activities is derived indirectly by starting with reported net income and "working backwards" to convert that amount to a cash basis.

Net income $12Adjustments for noncash effects: Increase in accounts receivable (2) Gain on sale of land (8) Decrease in inventory 4 Increase in accounts payable 6 Increase in salaries payable 2 Depreciation expense 3 Discount on bonds payable 2 Decrease in prepaid insurance 3 Loss on sale of equipment 2 Decrease in income tax payable (2)Net cash flows from operating activities$22

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-17

Net Income Adjustments for Noncash Components

Amounts that were increases

in net income

Gains Subtract from net income

Amounts that were

reductions of net

income

Depreciation, depletion, and amortizationLosses

Add backto net

income

© 2007 The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Slide22-18 Net Income Adjustments for

Changes in Assets and Liabilities

Increase Decrease

Asset - +

Liability + -