© 2005 by center for energy economics, bureau of economic geology, the university of texas at...

TRANSCRIPT

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

1

Energy Finance Considerations

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

2

Principle Market Concepts

• Investors differ according to risk preferences• Returns to investors from different investment

opportunities will vary with risk– Higher return = higher expected/potential

return (losses may be greater)• Cost of investment opportunities will vary with

demand for those opportunities– Increased demand = higher cost (higher risk

premium)

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

3

Investor Objectives and Opportunities

Financial investor

Objectives: taxable

nontaxable income growth stability

Global Capital Markets

Securities: stocks, bonds, royalties, partnerships

Industries: energy, financial, consumer, technology, cyclical, real estate

Currencies

Investment Opportunities

Risk

Return

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

4

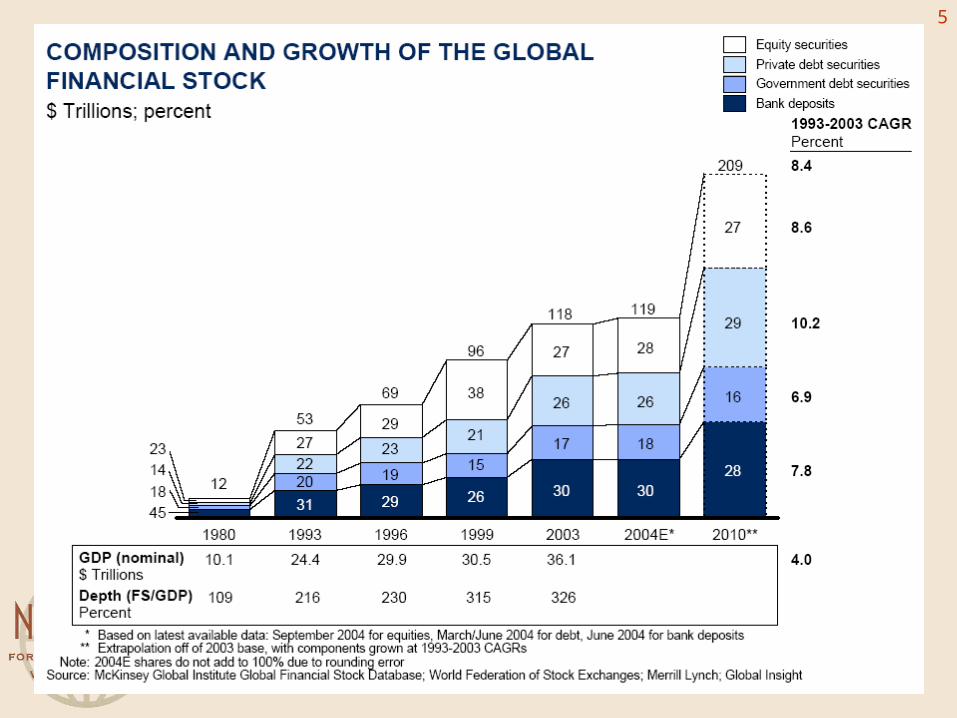

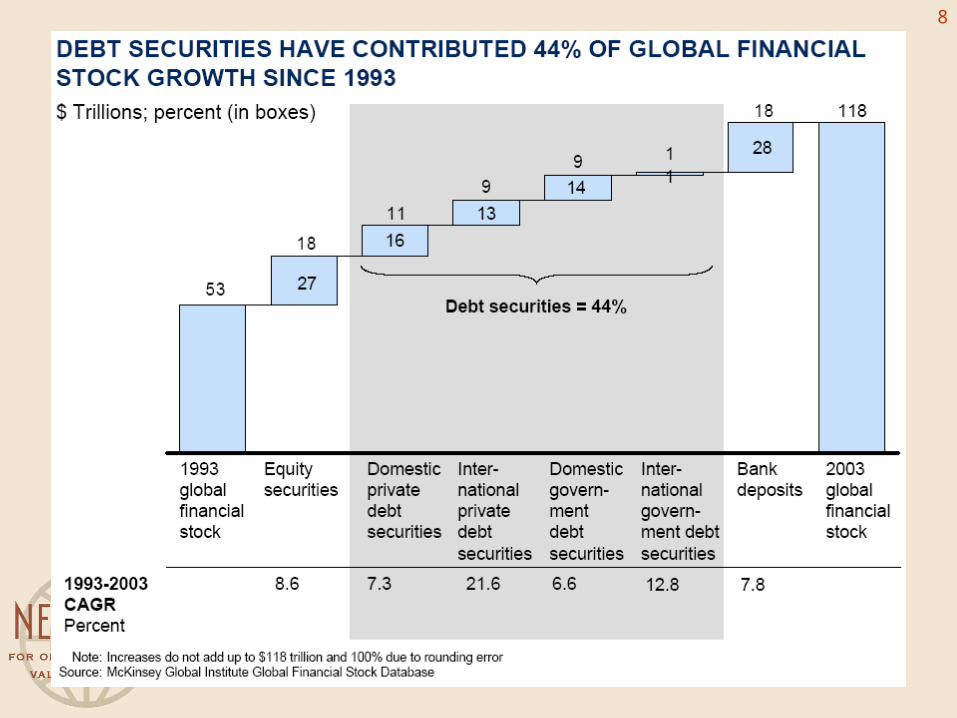

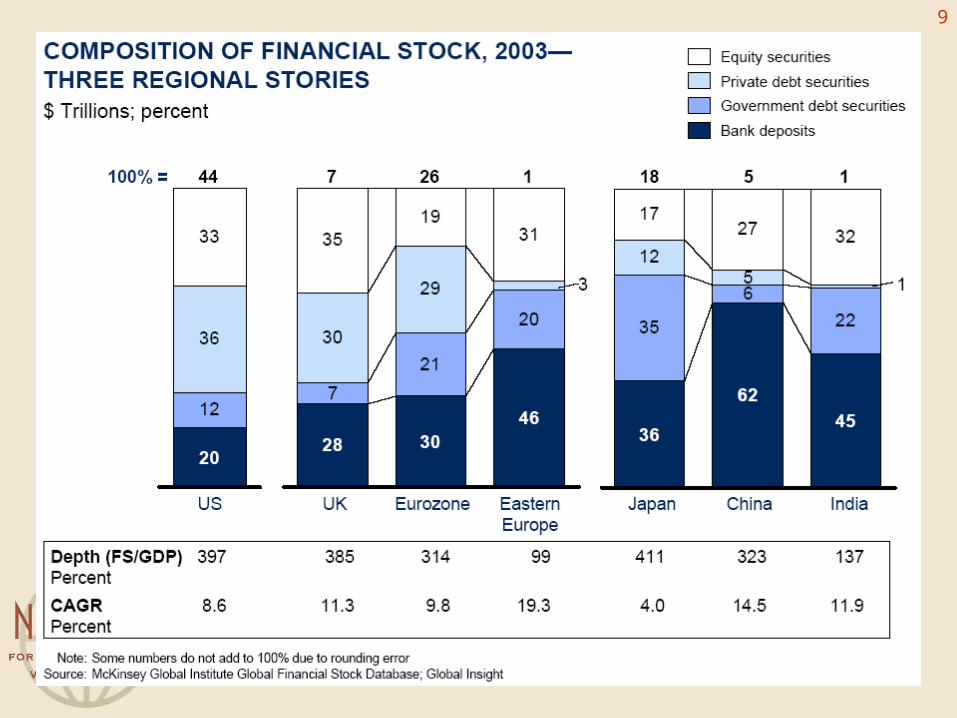

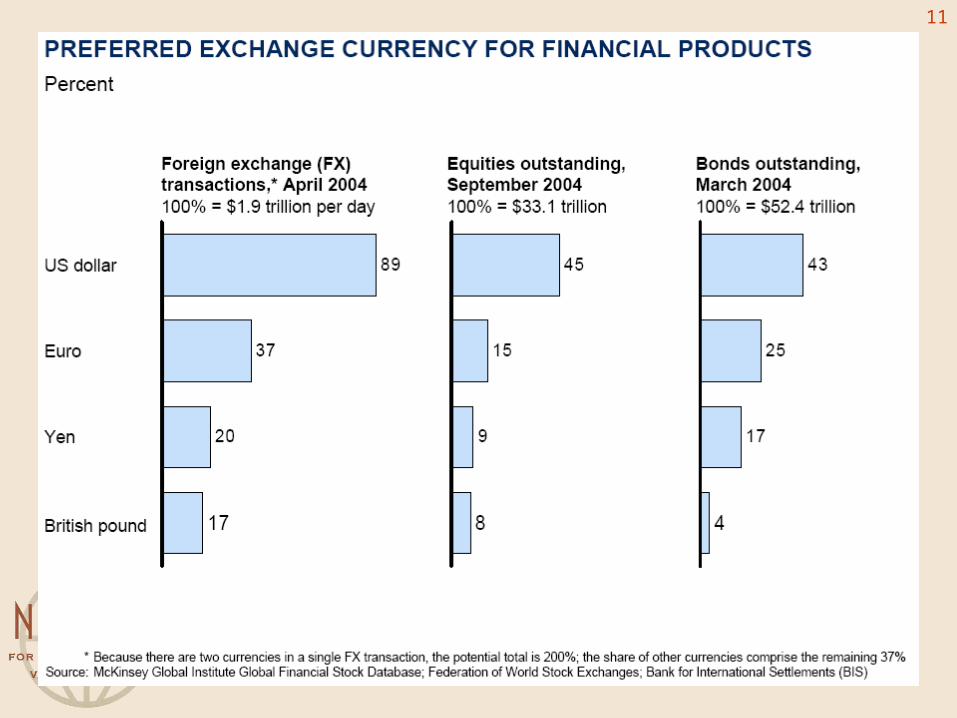

State of Global Capital Markets• Unprecedented breadth and strength.

• $118 trillions of assets to $200 trillion by 2010 if trends persist.

• Much of the growth comes from a rapid expansion of corporate and government debt: benefits & risks

• Cross-border capital flows and foreign holdings of financial assets continue to grow rapidly

Source: $118 Trillion and Counting: Taking Stock of the World’s Capital Markets, McKinsey Global Institute, February 2005.

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

5

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

6

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

7

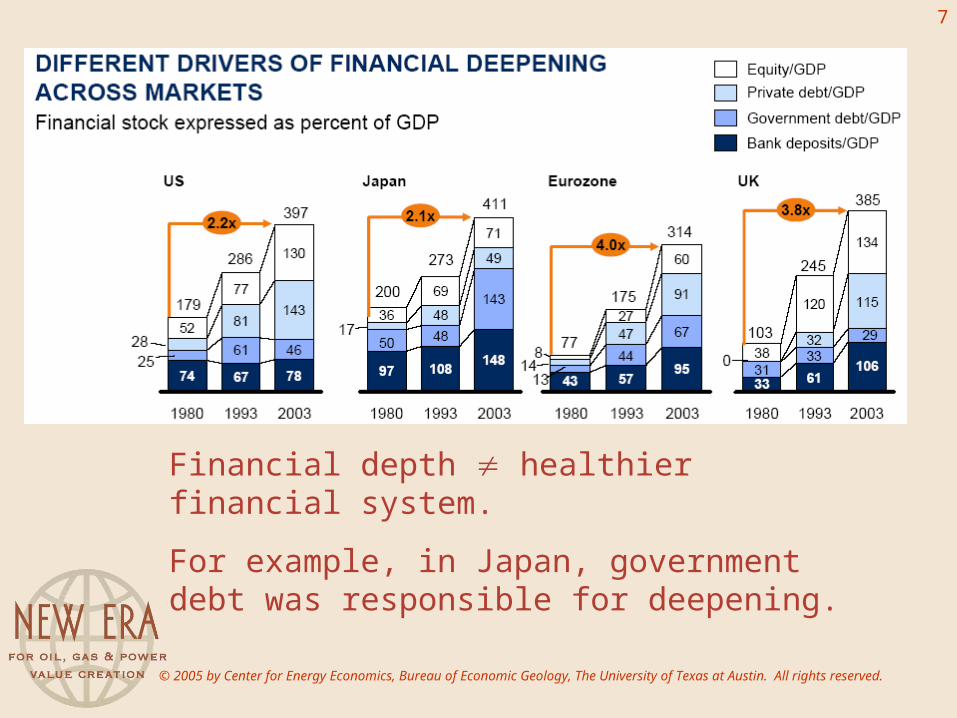

Financial depth healthier financial system.

For example, in Japan, government debt was responsible for deepening.

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

8

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

9

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

10

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

11

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

12

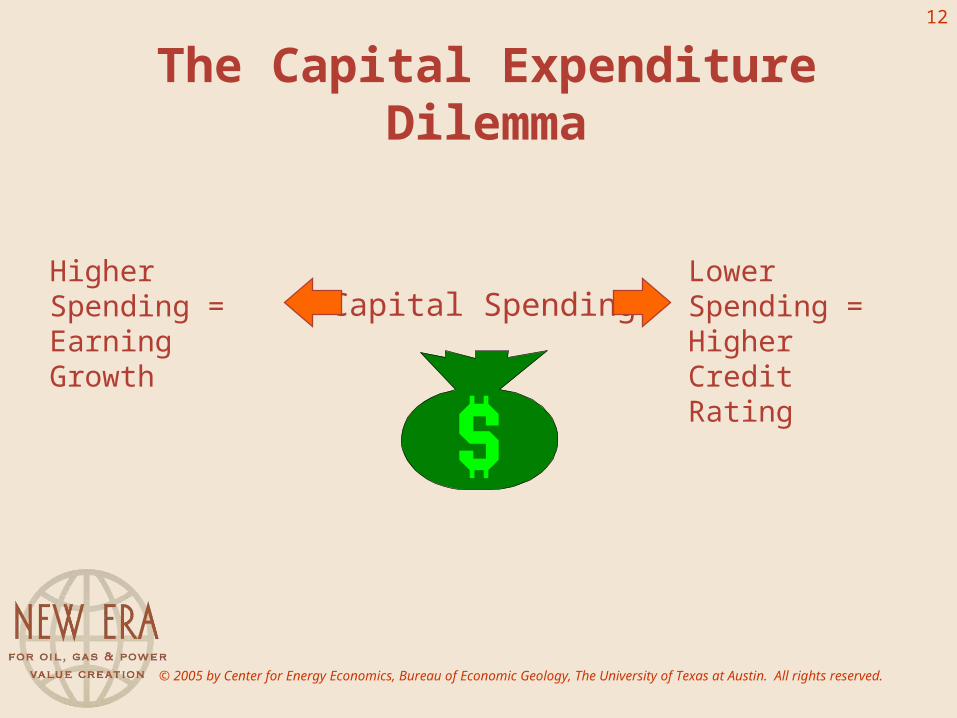

The Capital Expenditure Dilemma

Capital SpendingHigher Spending = Earning Growth

Lower Spending = Higher Credit Rating

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

13Capital Availability for Energy Projects

• Trends in western markets:– Commitments nearing all-time highs– Banks seeking to expand energy portfolios– Mergers/acquisitions fueling energy lending– Technology helps manage risk– Commodity hedging maximizes credit availability– Willingness to accept more risk for higher return– Bank consolidation is not reducing capital pool

• Criteria: high quality management, strategy, high quality reserves, healthy cash flows

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

14

Principle Sources of Project Funds

• NOC (non-privatized)– Cash flow (subject to

national budget)– International bond

markets– Development banks– Joint ventures,

partnerships (new strategies)

• Non-NOCs– Cash flow– Equity markets– Bonds– Commercial Banks– Development Banks– Joint ventures,

partnerships– “Boutique” (specialty

financing)

Importantly, how energy companies are financed is a different question from how projects are to be financed

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

15

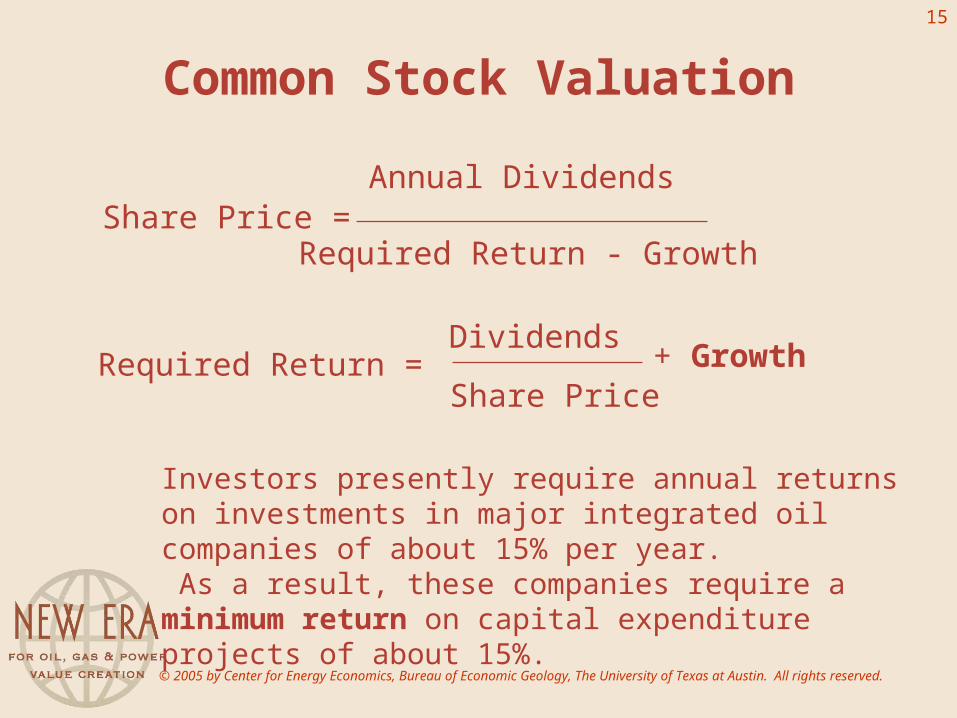

Common Stock Valuation

Share Price = Annual Dividends

Required Return - Growth

Required Return =Dividends

Share Price+ Growth

Investors presently require annual returns on investments in major integrated oil companies of about 15% per year. As a result, these companies require a minimum return on capital expenditure projects of about 15%.

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

16

U.S.: Equity Finance Mechanisms

• Sell assets to boost value of stock– Link to realignment around core businesses for

new investment

• Equity issues for joint ventures• IPOs based on technology plays

– Enhanced seismic and drilling; combine with j.v.s

• Privatizations for NOCs

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

17

U.S.: Commercial Bank Products, 1920-1989

• Amortize senior loans based on proved reserves (1920s-1970s)

• ABC production payment loans (1960s-1970s)

• Revolving lines of credit secured by proved producing reserves (1970s to present)

• Lease lines of credit (early 1980s)• Acquisition (warehouse) lines of credit (early

1980s)

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

18

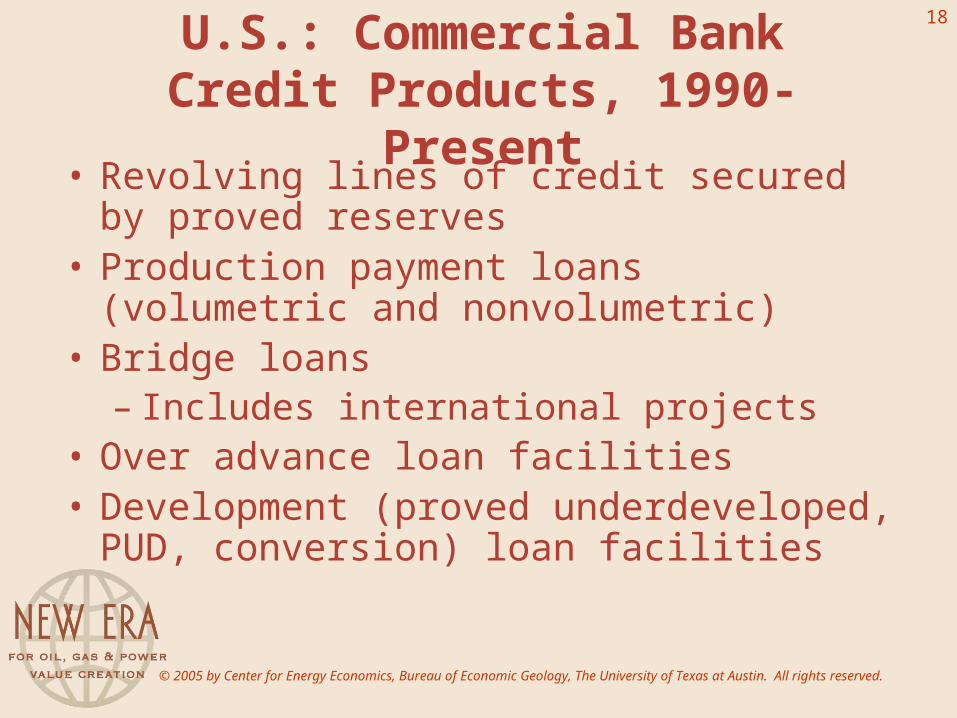

U.S.: Commercial Bank Credit Products, 1990-Present

• Revolving lines of credit secured by proved reserves

• Production payment loans (volumetric and nonvolumetric)

• Bridge loans– Includes international projects

• Over advance loan facilities• Development (proved underdeveloped,

PUD, conversion) loan facilities

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

19

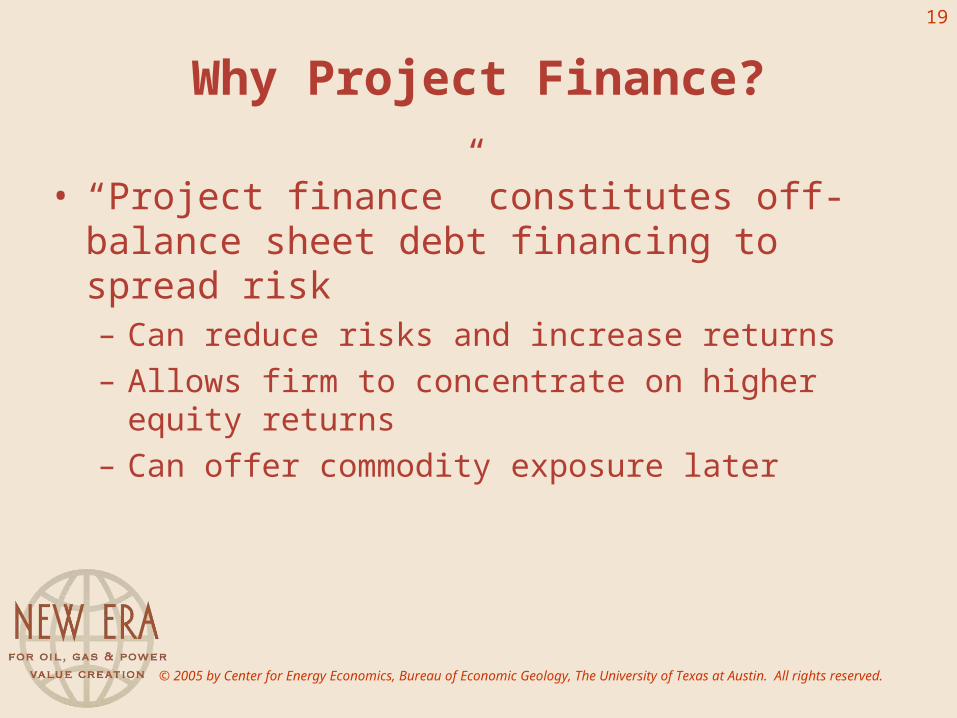

Why Project Finance?

• “Project finance” constitutes off-balance sheet debt financing to spread risk– Can reduce risks and increase returns– Allows firm to concentrate on higher equity

returns– Can offer commodity exposure later

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

20

Advantages of Project Finance

• Control (freedom to decide on reinvestment, salaries, etc.)

• Non-recourse (no obligation to make payments if revenues are insufficient to cover principal + interest)

• Leverage maximization (80-100% debt, less own funds at risk)

• Off-balance sheet treatment• Maximize tax benefits

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

21

Advantages of Project Finance

• Capturing economic rent (e.g., via long-term agreements)

• Achieving economies of scale• Sharing risk• Lower cost of funds (if better credit for

one of the parties on either side)• Reduced cost of resolving financial

distress• Reduced legal and regulatory costs

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

22

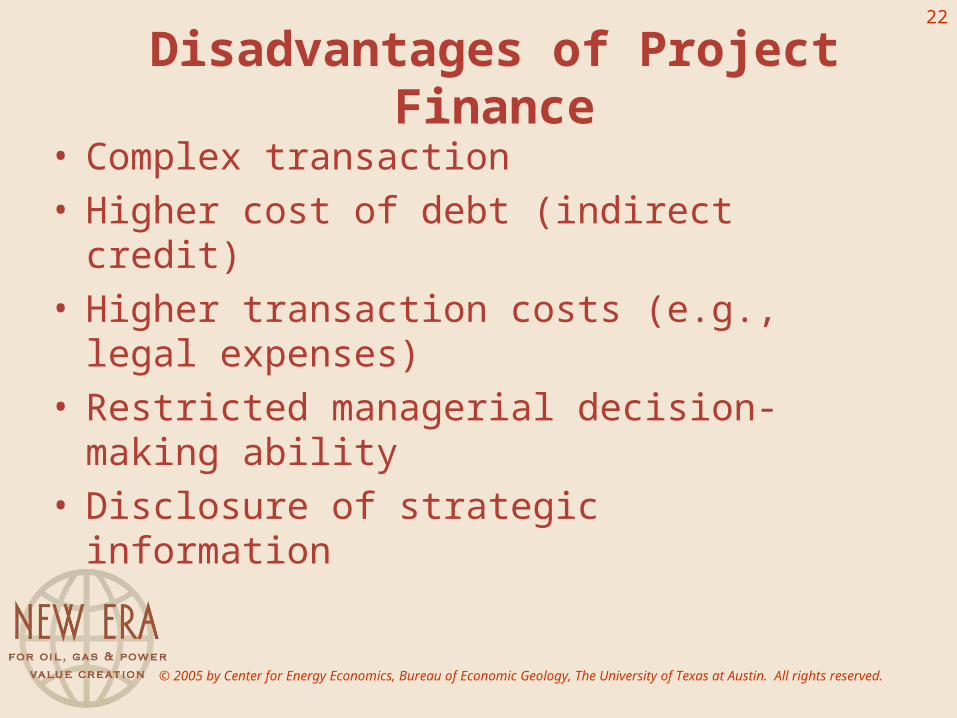

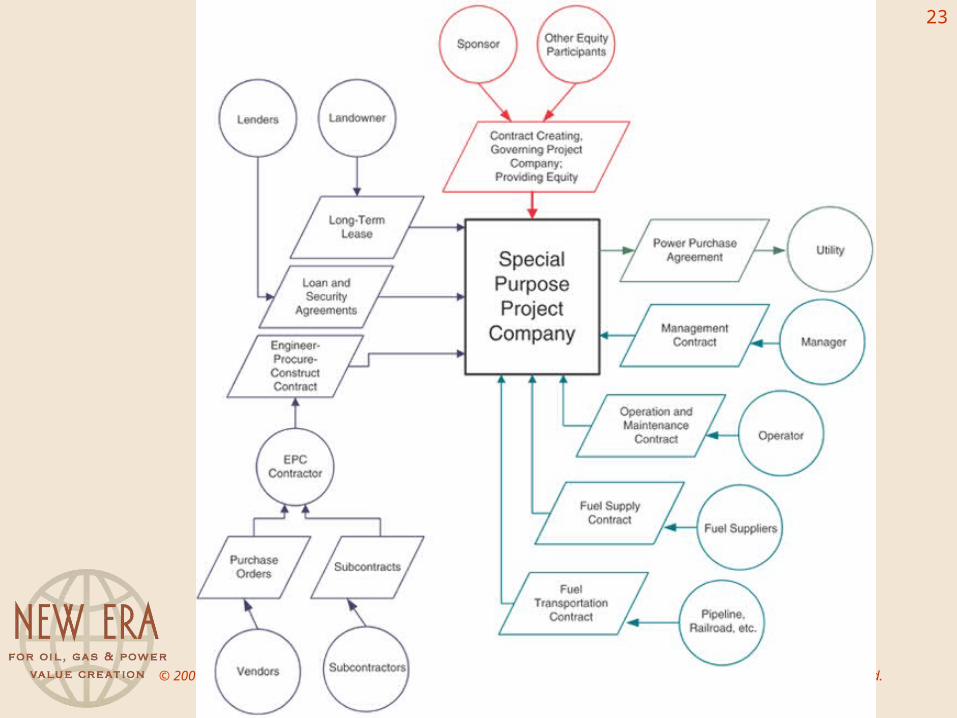

Disadvantages of Project Finance

• Complex transaction• Higher cost of debt (indirect credit)• Higher transaction costs (e.g., legal

expenses)• Restricted managerial decision-making

ability• Disclosure of strategic information

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

23

© 2005 by Center for Energy Economics, Bureau of Economic Geology, The University of Texas at Austin. All rights reserved.

24

Sources of Project Finance

• Development financial institutions – IFC & MIGA at the World Bank– EBRD– EIB– ADB

• Export credit agencies– EXIMBANK in the U.S.– JBIC

• Private sources of capital